Weekly Credit Update - Danske · PDF fileInvestor AB EUR 2016 SpareBank 1 SR ... BUY TVO 19s...

27

26 May 2015 Weekly Credit Update Important disclosures and certifications are contained from page 22 of this report Analyst Niklas Ripa +45 45 12 80 47 niri@danskebank.com Investment Research www.danskebank.com/CI

Transcript of Weekly Credit Update - Danske · PDF fileInvestor AB EUR 2016 SpareBank 1 SR ... BUY TVO 19s...

26 May 2015

Weekly Credit Update

Important disclosures and certifications are contained from page 22 of this report

Analyst Niklas Ripa +45 45 12 80 47 [email protected]

Investment Research www.danskebank.com/CI

2

- Market news

- Company news

- Trade ideas

Contents

- Chart pack

- List of official and shadow ratings and recommendations

- Best and worst performers

3

Sources: Bloomberg, Danske Bank Markets

What’s on our mind - General credit market news

• European credit indices ended the week a tad wider on the back of worrying signs from Greece that a default on the IMF-payment in June could be approaching. The iTraxx Main and Crossover-index ended the week with spreads of 61bp and 279bp, respectively.

• The volatility in long dated interest rates continued, with 10 year bund yields opening the week at around 56bp, widening to 66bp to close around 60bp. However, the peak rates were lower than past weeks.

• Our macro house view is that the euro area recovery is taking a breather as the boost from oil fades. US recovery looks imminent as also witnessed by last week’s US core CPI increase. Tentative signs of bottoming in China. Moderate gains in stocks in coming months. Bond yields heading moderately higher as Fed hike draws closer. EUR/USD to go lower.

• Despite volatile underlying rates, the Nordic secondary IG credit markets remained constructive, with decent trading flows over the past week. The story is different for the Nordic HY market, where the secondary markets are very illiquid and technical despite an active primary market.

• The event risk to spreads (and the EUR credit market) is a possible uncontrolled Greek default and/or exit from the euro and to a lesser extent other possible credit events, such as a rating downgrade of France and/or other European countries.

• Despite the rate volatility, there were a handful of deals printed, including EUR150m by Technopolis, NOK700m by Color Group, EUR750m by Swedbank, SEK1bn by DnB bank and EUR250m by Ålandsbanken. We expect further IG and HY issuance short term.

4

Best and worst performers - Investment grade

Source: Bloomberg, Danske Bank Markets (both charts)

1 week in local currencies 1 month in local currencies

3.8

3.1

2.0

1.9

1.5

1.4

1.3

0.7

0.6

0.6

-3.8

-3.8

-3.9

-4.2

-4.8

-4.9

-4.9

-5.0

-5.6

-5.8

-8-6-4-20246

Sampo Oyj EUR 2016

SpareBank 1 SR-Bank ASA EUR 2016

Vattenfall AB EUR 2016

Skandinaviska Enskilda Banken AB EUR …

Nordea Bank AB EUR 2016

Danske Bank A/S EUR 2016

Swedbank AB EUR 2016

Telenor ASA EUR 2017

DONG Energy A/S EUR 2019

Telefonaktiebolaget LM Ericsson EUR …

Telenor ASA EUR 2025

TeliaSonera AB EUR 2027

DNB Bank ASA EUR 2022

Danske Bank A/S SEK 2017

Skandinaviska Enskilda Banken AB EUR …

Nordea Bank AB EUR 2016

SBAB Bank AB EUR 2016

Carlsberg Breweries A/S EUR 2022

Fingrid OYJ EUR 2024

Vattenfall AB EUR 2024

Change in local currencies (bp)

24.3

24.3

17.5

15.1

13.8

13.6

12.1

9.8

9.7

7.8

-25.1

-25.4

-26.1

-27.4

-30.2

-30.4

-32.3

-33.2

-33.3

-34.6

-40-30-20-100102030

Vattenfall AB EUR 2016

Sampo Oyj EUR 2016

Investor AB EUR 2016

SpareBank 1 SR-Bank ASA EUR 2016

Skandinaviska Enskilda Banken AB EUR …

Swedbank AB EUR 2016

Danske Bank A/S EUR 2016

Neste Oil OYJ EUR 2016

Fortum OYJ EUR 2016

Svenska Cellulosa AB SCA EUR 2016

Telenor ASA EUR 2024

Fingrid OYJ EUR 2024

Telenor ASA EUR 2025

Statoil ASA EUR 2025

Nordea Bank AB EUR 2025

TeliaSonera AB EUR 2025

TeliaSonera AB EUR 2031

TeliaSonera AB EUR 2027

TeliaSonera AB EUR 2027

TeliaSonera AB EUR 2025

Change in local currencies (bp)

5

Best and worst performers - High yield

Source: Bloomberg, Danske Bank Markets (both charts)

1 week in local currencies 1 month in local currencies

3

2

-1

-2

-2

-3

-3

-3

-3

-4

-34

-34

-36

-38

-39

-40

-41

-45

-47

-198

-250-200-150-100-50050

Nokia OYJ USD 2039

Stena AB EUR 2020

Stena International SA USD 2024

Stora Enso OYJ EUR 2019

Akelius Residential Property AB SEK …

Nokia OYJ EUR 2019

YIT OYJ EUR 2016

SSAB AB EUR 2019

Outokumpu OYJ EUR 2016

Metsa Board OYJ EUR 2019

North Atlantic Drilling Ltd USD 2019

Seadrill Ltd NOK 2018

Seadrill Ltd SEK 2019

Olympic Ship AS NOK 2017

Finnair OYJ EUR 2049

SAS AB SEK 2019

SAS AB SEK 2017

Olympic Ship AS NOK 2019

Teekay Offshore Partners LP NOK 2019

Golden Close Maritime Corp Ltd USD …

Change in local currencies (bp)

19

18

17

10

1

-2

-5

-5

-6

-7

-59

-63

-68

-72

-75

-81

-83

-102

-163

-327

-400-300-200-1000100

Meda AB SEK 2018

Meda AB SEK 2016

Meda AB SEK 2019

YIT OYJ EUR 2016

Outokumpu OYJ EUR 2016

DLG Finance AS DKK 2018

Stena AB EUR 2020

Stora Enso OYJ EUR 2018

Stolt-Nielsen Ltd NOK 2019

Nokia OYJ EUR 2019

Odfjell SE NOK 2017

SAS AB SEK 2017

Solstad Offshore ASA NOK 2016

North Atlantic Drilling Ltd NOK 2018

Seadrill Ltd SEK 2019

Seadrill Ltd NOK 2018

Seadrill Ltd USD 2020

Seadrill Ltd USD 2017

North Atlantic Drilling Ltd USD 2019

Golden Close Maritime Corp Ltd USD …

Change in local currencies (bp)

6

BUY TVO 19s vs SELL Fortum 19s (published 11 May 2015) – Spread compression ahead

Jakob Magnussen +45 45 12 85 03 [email protected]

* Source: Bloomberg, Danske Bank Markets

• TVO (BBB/NO) is currently trading wider than the ‘BB+’ curve.

• Fortum (A-/NW) is in line or slightly tight to the ‘BBB+’ curve.

• The longer-term spread trajectory of TVO should be positive, following more clarity on OL3 and arbitration.

• Fortum’s trajectory is likely to be negative due to high shareholder focus, Russian exposure, divestment of stable assets and re-leveraging.

• Both companies are currently afected by weak Finnish power prices.

• We have an Overweight recommendation on TVO and an Underweight recommendation on Fortum.

• The spread between the two companies’ 2019s is currently 69bp.

• This trade also makes sense in longer maturities.

FUMVFH 4.5 16

FUMVFH 6 19TVO 6 16

FUMVFH 4 21

TVO 4.625 19

FUMVFH 2.25 22 (A2/A-)

'BB+' EU utilities

'BBB-' EU utilities

'BBB' EU utilities

'BBB+' EU utilities

TVO 2.5 21

TVO 2.25 25 (NR/BBB/BBB)

0

20

40

60

80

100

120

140

160

180

0 5 10 15

Z-spd (bp)

Years to maturity

7

Source: Danske Bank Markets

Recent trade ideas

See the end of this presentation for a list of our coverage including shadow ratings and recommendations

Recent ideas

Type Trade Idea

Sector spread Switch from Fortum 19s to TVO 19s Sell the Fortum 19s trading tight compared to fair value and buy TVO 19s trading wide even if they are downgraded

Opened 11/05/2015

Start spread 69 Sector spread Switch from Metso 2019 to Sandvik

2026

We suggest selling the METSO 2019s, which have had a good run since the spin-off of the group’s Pulp, Paper and Power business in 2014. Metso and Sandvik have similar business exposure (mining and energy), but Sandvik is c.3x larger (in terms of revenues) and diversified into sectors to which Metso has no exposure.

Opened 27/04/2015

Start spread 56 Outright Buy Neste Oil 2022 The Neste Oil 2022s trade wider than the 'BB+' curve, making

them seem cheap relative to our shadow rating of 'BBB-' Closed 21/04/2015

Start spread 161

Outright Buy Akelius Residential 2019 in SEK The Akelius Residential SEK 2019 FRN 3M Stibor+240bp trades wide relative to other similar unrated SEK bonds.

Opened 13/04/2015

Start spread 225 Outright Buy Vestas 2022 The Vestas EUR 2.75% 2022 trades cheap to a EUR corporate

BBB. curve. Opened 19/03/2015

Start spread 245

Currency trade Close of trade SSAB Recent performance in the SSAB EUR bond has closed the earlier 19bp gap between the EUR and the SEK 2019 bonds.

Opened 10/03/2015

Start spread -2 Outright Buy Tallink 2018 FRN Tallink 2018 in NOK trades cheap to a global median ‘BB-’

credit curve (converted into NOK). Opened 27/02/2015

Start spread 470 Outright CITCON '3.75 We believe that CITCON'3.75s trade at an attractive level relative

the 'BBB' curve. Opened 10/02/2015

Start spread 112 Outright EGASDK '20 EGASDK '20s, which we see as 'B' indicatively trade far too cheaply

relative to the industrial 'B' curve Opened 02/02/2015

Start spread 608

8

Source: Danske Bank Markets

Company news from the past week

Name News Implication

Meda

At its CMD last Tuesday, Meda said that it wants to increase the share of bond financing and has begun preparations for a EUR bond issue (but with no specific timing mentioned). If this is the case, it seems likely it will also look to get official credit ratings - which we believe will be assigned in the BB-/B+ range (our rating on Meda is BB-). There was also a lot of talk on M&A at the CMD but with an indication that leverage will continue to fluctuate in the 5.5-3.5 range as deals are consumated - and with likely timing for another larger deal around 2016 (i.e once Rottapharm has been integrated and leverage reduced below 4x). All in all, in line with our expectations for our BB- view on the company.

Credit Neutral

Heimstaden

Heimstaden (Corp: BB, Senior Unsecured: BB-) announced that it will issue preference shares amounting to SEK750m and an additional SEK250m if there is demand for it. The initial yield will be 6.25%. From a bond holder perspective this is good for two reasons. First, there is more junior capital which should increase the senior recovery rate in a default scenario and second, the willingness for Heimstaden to cancel dividends on the preference shares should be higher than for a public traded company (since it typically means that the main shareholders cannot receive dividends either). On the negative side, this is fairly expensive capital compared to bonds, which should burden the cash flow.

Credit positive

Tallink

Tallink Q1 15 - Credit update. Following another moderately credit-positive quarterly result, we continue to view the credit profile of Tallink’s bond as commensurate with a ‘BB-’ shadow rating. The FRN Tallink 2018 in NOK is currently priced around 70-90bp above a Nordic ‘BB-’ credit curve (EUR) and close to a ‘B+’ credit (one notch less than DBM’s shadow rating). This seems attractive to us from a carry perspective despite the bond’s recent price performance. This bond may be of relevance to investors able to hold exposure to NOK. We highlight the limited liquidity in the bond issue.

Credit positive

ISS

ISS A/S (S&P:BBB-/PO; Baa3/S) reported a Q1 15 overall as expected and kept guidance for 2015 unchanged. Adjusted EBITDA rose 7% y/y driven by a 3% rise in organic growth and an unchanged operating margin before special items y/y. Please note that the Q1 15 report was for ISS A/S, whereas ISS Global A/S (the bond issuing entity) does not publish quarterly reports). ISS A/S Reported Net debt to pro-forma LTM EBITDA of 2.9x vs. 3.2x in Q1 14 and 2.6x end-2014. The rise compared to end-2014 is mainly due to normal seasonally variation in working capital and should not be a sign of concern, in our view. ISS A/S targets net debt of EBITDA below 2.5x - and ISS has stated that it wants to get "comfortably below 2.5x" - we interpret this as 2.2-2.3x. Hence, we expect ISS to focus on deleveraging during 2015 - although bolt-on acquisition, especially within Catering in the US, could also be an option during 2015. Reduced leverage could fuel rating upgrade to BBB from the current BBB-/PO from S&P. We maintain our Overweight recommendation on ISS.

Credit positive

9

Source: Danske Bank Markets

Company news from the past week

DFDS

DFDS (DBM Shadow rating BBB-). Last week the UK Court of Appeal ruled in favour of SCOP’s (employees of MyFerryLink owned by Eurotunnel and a fierce DFDS competitor) appeal against the decision by the UK Competition Appeal Tribunal on 9 January 2015 to uphold the decision of the UK Competition and Markets Authority (CMA) banning Eurotunnel/SCOP from operating ferries out of Dover as of 9 July 2015. CMA later announced an appeal against this ruling. The ruling from the Court of Appeals is surprising news and moderately credit negative – since DFDS’s Channel-business (France/UK ferry route) was expected to recover significantly when the ferry competition from Eurotunnel was to be finally removed in July 2015. Last week’s ruling suddenly creates uncertainty as to whether Eurotunnel may suddenly decide to continue to operate the MyFerryLink ferries on the Channel-route (with the tough competition for DFDS not ceasing, implying that at best a break-even scenario may unfold). Alternatively, Eurotunnel may continue with its current sales process of the three ferries operated by MyFerryLink. Time will tell where this (possibly lengthy) situation is heading, and what kind of implications it has for DFDS - both short and longer term. However, we see this as clearly more negative from an equity perspective than from a credit perspective. We do not think this ruling will have any significant consequences for our rating assessment on DFDS or for DFDS’s credit spreads, since the worst-case outcome is an ‘as-is’ situation, which is more or less neutral from a credit perspective since the route is generating positive cash flows.

Credit neutral

DFDS

DFDS Q1 15- credit update: Credit positive, but leverage to trend upwards. Following a credit-positive quarterly result, we continue to view DFDS’s credit profile as commensurate with a ‘BBB-’ shadow rating. The FRN DFDS bonds are currently priced with a discount of 50-150bp to an indicative ‘BBB-’ credit curve (converted into NOK and DKK, respectively). Significant higher discount margins in the FRN bonds seems fair to us, given our expectation of increasing leverage going forward and the inherent significant M&A event risk linked to the DFDS name.

Credit positive

Volvo

Volvo (MW): Deliveries from Volvo's truck operations in April 2015 amounted to 17,715 vehicles. This was an increase of 8% y/y. In April 2015, truck deliveries rose by 24% in Europe and by 18% in North America. Deliveries in South America were down by 42%, while deliveries rose by 9% in Asia. By region, North and South America was above expectations, while all other markets were somewhat below. By brand Mack and Volvo were stronger while Renault and UD trucks were weaker, implying a good mix (better margins on Mack and Volvo brands). Overall, the news is neutral from a credit perspective given the inherent volatility in monthly deliveries.

Credit neutral

10

Source: Danske Bank Markets

Company news from the past week

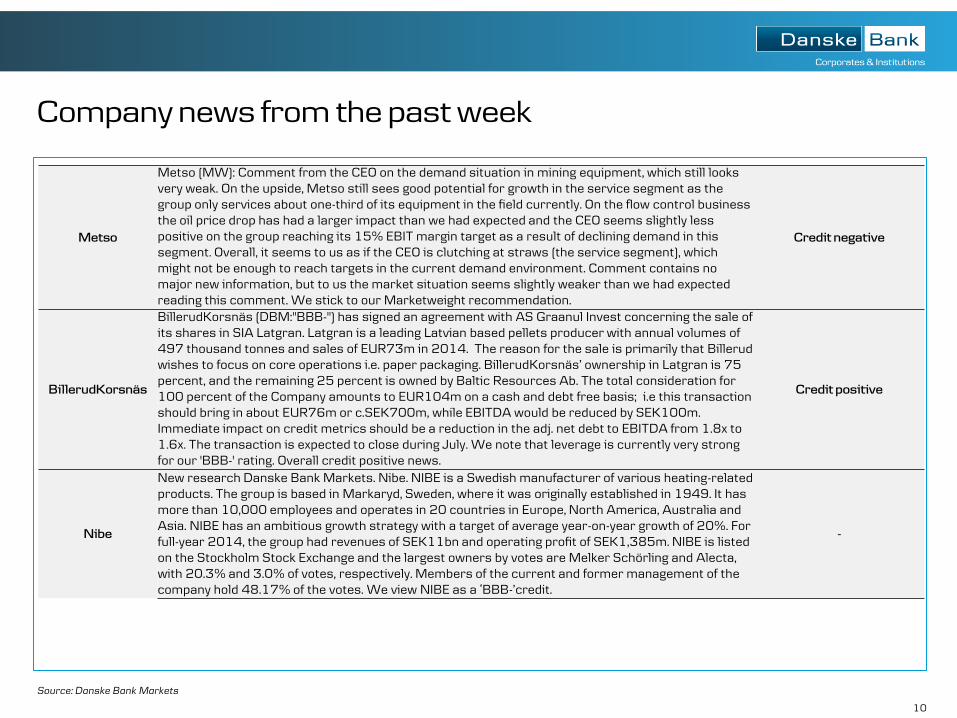

Metso

Metso (MW): Comment from the CEO on the demand situation in mining equipment, which still looks very weak. On the upside, Metso still sees good potential for growth in the service segment as the group only services about one-third of its equipment in the field currently. On the flow control business the oil price drop has had a larger impact than we had expected and the CEO seems slightly less positive on the group reaching its 15% EBIT margin target as a result of declining demand in this segment. Overall, it seems to us as if the CEO is clutching at straws (the service segment), which might not be enough to reach targets in the current demand environment. Comment contains no major new information, but to us the market situation seems slightly weaker than we had expected reading this comment. We stick to our Marketweight recommendation.

Credit negative

BillerudKorsnäs

BillerudKorsnäs (DBM:"BBB-") has signed an agreement with AS Graanul Invest concerning the sale of its shares in SIA Latgran. Latgran is a leading Latvian based pellets producer with annual volumes of 497 thousand tonnes and sales of EUR73m in 2014. The reason for the sale is primarily that Billerud wishes to focus on core operations i.e. paper packaging. BillerudKorsnäs’ ownership in Latgran is 75 percent, and the remaining 25 percent is owned by Baltic Resources Ab. The total consideration for 100 percent of the Company amounts to EUR104m on a cash and debt free basis; i.e this transaction should bring in about EUR76m or c.SEK700m, while EBITDA would be reduced by SEK100m. Immediate impact on credit metrics should be a reduction in the adj. net debt to EBITDA from 1.8x to 1.6x. The transaction is expected to close during July. We note that leverage is currently very strong for our 'BBB-' rating. Overall credit positive news.

Credit positive

Nibe

New research Danske Bank Markets. Nibe. NIBE is a Swedish manufacturer of various heating-related products. The group is based in Markaryd, Sweden, where it was originally established in 1949. It has more than 10,000 employees and operates in 20 countries in Europe, North America, Australia and Asia. NIBE has an ambitious growth strategy with a target of average year-on-year growth of 20%. For full-year 2014, the group had revenues of SEK11bn and operating profit of SEK1,385m. NIBE is listed on the Stockholm Stock Exchange and the largest owners by votes are Melker Schörling and Alecta, with 20.3% and 3.0% of votes, respectively. Members of the current and former management of the company hold 48.17% of the votes. We view NIBE as a ‘BBB-’credit.

-

11

Source: Danske Bank Markets

Company news from the past week

Danfoss

Dansfoss (MW) Q1 15 – Credit update. Q1 15: Weighed down by Russia Danfoss released a Q1 15 earnings announcement that showed modest sales growth. Most of the 13% revenue growth came from currency tailwinds and the added revenue from the Vacon acquisition late last year. Clean EBITDA rose by only 1% despite the added earnings from Vacon. This is primarily because of Vacon integration costs. Group credit metrics improved slightly on the back of a positive FCF and we now see adjusted net debt to EBITDA at 2.0x versus 2.1x in Q4 14. We expect Danfoss’s ‘BBB’ rating from S&P to remain intact after this. Overall, we consider these credit neutral results and we see the DNFSDC 1.375% 2022s trading at fair to slightly tight levels.

Credit neutral

Color Group

Issuer profile – Color Group. Color Group AS (the issuer) is the parent company of Norway’s largest short-sea shipping company Color Line, established in 1990. Based in Oslo, Color Group AS is privately owned by Olav Nils Sunde and his family through the company O. N. Sunde AS. The fleet numbers six vessels operating on four ferry services between seven ports in Norway, Germany, Denmark and Sweden. Color Group enjoys a strong market position, holding around a 55% share of all sea-based passenger traffic into Norway and 23% of all goods hauled to Norway by road. In 2014, the group reported net sales of NOK4,594m and EBITDA of NOK533m. In future years, the company aims to strengthen its profitability significantly. We assign a corporate issuer credit rating of ‘BB-’. Due to a significant amount of ship mortgages ranking ahead of the bonds, we assign a ‘B+’ issue rating to the outstanding bonds of Color Group AS. Our rating assumes improving credit metrics over the coming years as per our baseline forecasts.

-

Destia

Destia (DBM:"BB-" issuer rating and "B+" senior unsecured): While budget cuts have generally been high on the agenda of new Finnish government plans, it plans to invest c.EUR1.6bn in improving Finnish transportation infra in three years. Should this EUR500m+ boost materialise, it would be a sizeable addition as the current value of Finnish transportation infra spending is EUR3.2bn (Euroconstruct, Nov 2014). Thus, instead of a slight decline in the segment it could now grow by 15-20% y/y. This could substantially benefit Destia, which has significant exposure to both Road and Rail infrastructure construction and maintenance in Finland. The company has more than 50% of the market share of Road Maintenance in Finland and holds a market share of more than 30% within infrastructure construction projects larger than EUR20m. Destia's adj. net debt to adj. EBITDA currently stands at around 2.2x (end Q1 15).

Credit positive

12

Source: Danske Bank Markets

Company news from the past week

Citycon

Citycon (BBB/Baa2) is to acquire Sektor Gruppen, Norway's second largest shopping centre owner. The price on a debt free basis is EUR1.5bn. Citycon intends to finance the acquisition through a rights issue of approximately EUR600m, a EUR250m bridge financing facility, with a maturity of one year and from available financing facilities if necessary. In addition, waivers have been obtained for approximately EUR 671m of the existing bank financing facilities of Sektor to remain in place post-closing. The closing of the transaction is expected to take place in July 2015. The acquisition seems to be well anchored with the rating agencies and the company states that "Based on discussions with

rating agencies, Citycon expects its current ratings (‘BBB’ by Standard & Poor’s and ‘Baa2’ by

Moody’s) to be affirmed with stable outlook, subject to currently planned Rights Issue and other

conditions relating to the transaction.” According to the company, the LTV will remain in the 40-45% area after the transaction (which we believe is a requirement from both S&P and Moody's for the current rating). Further, we consider the improved geographical footprint, the larger scale and synergies (systems, advertising, processes etc.) as credit positive. Citycon's largest shareholders, Gazit-Globe Ltd. (42.8%) and CPP Investment (15%) have (subject to some conditions) provided undertakings to subscribe to their pro-rata portion of the right issue which in our view shows a great willingness to support the company (since the last right issue was performed less than a year ago). All in all, we consider the transaction as credit positive due to the increased diversification, larger scale and maintained financial position. Further, we encourage the commitment from the company to maintain its current rating (considering the wording in the press release and the rights issue).

Credit positive

Technopolis

Issuer profile – Technopolis. Technopolis is a Finnish commercial property company, which specialises in providing an operating environment and service concept for high-tech enterprises. In 2014, the company reported net sales of EUR162m, with a total property portfolio market value of EUR1.4bn as of end-March 2015. Technopolis's credit profile benefits from a good geographical diversification in overall attractive regions with sound growth characteristics. As for other listed property companies, the company's leverage is fairly high with a consequent exposure to potential swings in the economic cycle and to interest rate fluctuations. All in all, we view Technopolis as a 'BB+' company with a stable outlook, with the bonds one notch lower at 'BB'.

-

13

.

Source: Danske Bank Markets

Selected new issues

Selected new issues

Date Issuer Coupon CCY Volume Maturity S&P / Mdy / Fitch ASW/DM

22-05-2015 Aker Asa NIBOR3M +350bps NOK 1 000 m May-21 / / 138

21-05-2015 Color Group Asa NIBOR3M +485bps NOK 700 m May-21 / / 138

21-05-2015 Technopolis Plc 3.75% EUR 150 m Oct-20 A / A2 / A 75

21-05-2015 Swedbank Ab 1% EUR 750 m Jun-22 A+ / A1e / A+e 45

21-05-2015 Rabobank Nederland EUR003M +30bps EUR 1 500 m May-20 / Aa2e / AA-e 30

21-05-2015 Dnb Bank Asa 1.97% SEK 1 000 m May-25 / / -

21-05-2015 Esb Finance Limited 2.125% EUR 500 m Jun-27 / Baa1e / A-e 107

19-05-2015 Alandsbanken Ab 0.375% EUR 250 m May-20 AAA / / 9

20-05-2015 Sampo Oyj 1.25% SEK 1 000 m May-20 / Baa2e / 77

14

Chart pack: euro spreads and returns Euro IG ASW, iBoxx indices

Source: Macrobond Financial, Danske Bank Markets [all charts]

Euro HY ASW, Merrill Lynch indices

IG Total Return, iBoxx indices, 2014-01=100

HY Total Return, Merrill Lynch indices, 2014-01=100

15

Chart pack: relative value iTraxx vs iBoxx

Source: Bloomberg, Macrobond Financial, Danske Bank Markets [all charts]

Euro vs US CDS indices - IG (Markit)

EUR CDS Spreads – Nordic Banks

Euro vs US HY bond indices (Merrill Lynch)

16

Chart pack: general market development European swap and government yields

Source: Macrobond, Danske Bank Markets [all charts]

Euro swap curve spread

3M TED-spread, US and euro area

EUR/USD basis swaps

17

Chart pack: fund flows Europe, net sales

Source: Macrobond Financial, Danske Bank Markets [all charts]

Sweden, net sales

US, net sales

Norway, net sales

18

Chart pack: macro GDP y/y growth, calendar adjusted

Source: Macrobond Financial, Danske Bank Markets [all charts]

Euro area y/y change in bank lending

Purchasing Manager Indices

Euro area lending standards

19

Our coverage and shadow ratings 1 of 5

Ratings from S&P/Moody's/Fitch and Danske Bank Markets shadow ratings

Analyst(s)

Company Rating Outlook Sr. Unsec Rating Outlook Rating Outlook Rating OutlookAhlstrom Oyj B+ Stable Mads RosendalAkelius Residential Property Ab BBB- Stable BBB- Louis LandemanAmbu A/S BBB- Stable Jakob MagnussenAp Moeller - Maersk A/S BBB+ Stable Baa1 Stable Brian Børsting MARKETWEIGHTArla Foods Amba BBB+ Stable Mads RosendalAtlas Copco Ab A Stable A2 Stable Mads Rosendal UNDERWEIGHTAvinor As AA- Stable A1 Stable Ola Heldal MARKETWEIGHTBank 1 Oslo Akershus As BBB+ Stable T. Hovard / L. HolmBank Norwegian As BBB Stable T. Hovard / L. HolmBeerenberg Holdco Ii As B Stable Øyvind MossigeBillerudkorsnas Ab BBB- Stable Mads RosendalBw Offshore BB+ Stable Øyvind MossigeCargotec Oyj BBB- Stable Mads RosendalCarlsberg Breweries A/S Baa2 Neg BBB Stable Brian Børsting MARKETWEIGHTCermaq Asa BB Stable Knut-Ivar BakkenCitycon Oyj BBB Stable Baa2 Stable Emil Hjalmarsson OVERWEIGHTColor Group As BB- Stable B+ Niklas RipaCom Hem Holding Ab BB- Stable Ola HeldalCorem Property Group Ab BB- Stable B+ Emil HjalmarssonDanfoss A/S BBB Stable Jakob MagnussenDanske Bank A/S A Neg A3 A StableDfds A/S BBB- Stable Niklas RipaDlg Finance As BB- Stable Mads RosendalDna Ltd BBB- Stable Ola HeldalDnb Bank Asa A+ Stable A1 T. Hovard / L. Holm UNDERWEIGHTDong Energy A/S BBB+ Stable Baa1 Stable BBB+ Stable Jakob Magnussen MARKETWEIGHTDsv A/S BBB Stable Brian BørstingEg Holding B Stable Jakob MagnussenEika Boligkreditt As A- Stable T. Hovard / L. HolmEika Gruppen As BBB Stable T. Hovard / L. HolmEksportfinans Asa BBB- Pos Ba3 Stable T. Hovard / L. HolmElectrolux Ab BBB Stable Wr WD Brian Børsting MARKETWEIGHT

Recomm.Danske Bank S&P Moody's Fitch

20

Our coverage and shadow ratings 2 of 5

Ratings from S&P/Moody's/Fitch and Danske Bank Markets shadow ratings

Analyst(s)

Company Rating Outlook Sr. Unsec Rating Outlook Rating Outlook Rating OutlookElenia Oy Jakob Magnussen OVERWEIGHTElisa Oyj BBB+ Stable Baa2 Stable Ola Heldal OVERWEIGHTEntra Eiendom As A- Stable Ola HeldalFarstad Shipping Asa BB Neg BB- Øyvind MossigeFingrid Oyj A+ Stable A1 Stable A+ Stable Jakob Magnussen MARKETWEIGHTFinnair Oyj BB Stable Brian BørstingFortum Oyj A- A2 A- Neg Jakob Magnussen UNDERWEIGHTFortum Varme Holding Samagt Med Stockholms Stad Ab BBB+ Stable Jakob MagnussenFred Olsen Energy Asa BB Stable BB- Sondre StormyrG4S Plc BBB- Stable Brian Børsting OVERWEIGHTGetinge Ab BB+ Neg Louis LandemanGolden Close Maritime Corp Ltd B- Sondre StormyrHeimstaden Ab BB Stable BB- Louis LandemanHemso Fastighets Ab BBB+ Stable BBB A- Stable Emil HjalmarssonHkscan Oyj BB Stable Brian Børsting MARKETWEIGHTHoist Kredit Ab BB- Stable B+ Gabriel BerginHusqvarna Ab BBB- Pos Emil HjalmarssonIkano Bank Ab BBB Stable T. Hovard / L. HolmInvestor Ab AA- Stable A1 Stable Brian Børsting OVERWEIGHTIss A/S BBB- Pos Brian Børsting OVERWEIGHTJ Lauritzen A/S B Stable B- Bjørn Kristian RøedJernhusen Ab A- Stable Gabriel BerginJyske Bank A/S A- Stable Baa T. Hovard / L. Holm OVERWEIGHTKemira Oyj BBB- Stable Wr Mads RosendalKesko Oyj BBB Stable Mads RosendalKlaveness Ship Holding As BB- Stable B+ Bjørn Kristian RøedLoomis Ab BBB- Stable Brian BørstingLuossavaara-Kiirunavaara Ab BBB+ Stable Louis LandemanMeda Ab BB- Stable Louis LandemanMetsa Board Oyj BB Stable B1 Pos Mads Rosendal MARKETWEIGHTMetso Oyj BBB Stable Baa2 Stable Mads Rosendal MARKETWEIGHTNcc Ab BBB- Stable Emil HjalmarssonNeste Oil Oyj BBB- Stable Jakob Magnussen OVERWEIGHT

Recomm.Danske Bank S&P Moody's Fitch

21

Our coverage and shadow ratings 3 of 5

Ratings from S&P/Moody's/Fitch and Danske Bank Markets shadow ratings

Analyst(s)

Company Rating Outlook Sr. Unsec Rating Outlook Rating Outlook Rating OutlookNibe Industrier Ab BBB- Stable Emil HjalmarssonNokia Oyj BB+ Pos Ba2 Stable BB Pos Ola Heldal MARKETWEIGHTNokian Renkaat Oyj BBB+ Stable Jakob MagnussenNordax Finans Ab BBB- Stable T. Hovard / L. HolmNordea Bank Ab AA- Neg Aa3 AA- Stable T. Hovard / L. Holm UNDERWEIGHTNorth Atlantic Drilling Ltd BB- Neg B+ Sondre StormyrNorwegian Air Shuttle Asa BB- Neg B+ Brian BørstingNorwegian Property Asa BBB- Stable Ola HeldalNykredit Bank A/S A+ Baa A Stable T. Hovard / L. Holm MARKETWEIGHTNynas Group B+ Stable B+ Jakob MagnussenOcean Yield Asa BB BB- Øyvind MossigeOdfjell Se B+ Stable B Bjørn Kristian RøedOlav Thon Eiendomsselskap Asa BBB+ Stable Ola HeldalOrava Residential Reit Plc B+ Stable B+ Mads RosendalOlympic Ship As B+ Stable B Øyvind MossigeOrkla Asa BBB+ Pos Ola HeldalOutokumpu Oyj B Pos Mads RosendalPohjola Bank Oyj AA- Neg Aa3 Stable A+ Stable T. Hovard / L. Holm MARKETWEIGHTPosten Norge As A- Stable Ola HeldalPostnord Ab BBB+ Stable Gabriel BerginProsafe Se BB Stable Sondre StormyrRamirent Oyj BB+ Stable Brian BørstingSandnes Sparebank BBB+ Stable T. Hovard / L. HolmSandvik Ab BBB Neg Mads Rosendal OVERWEIGHTSas Ab B- Stable Wr Stable Brian BørstingSbab Bank Ab A Neg A2 Stable T. Hovard / L. Holm MARKETWEIGHTScania Ab A- Stable Mads Rosendal MARKETWEIGHTSchibsted Asa BBB Stable Ola HeldalSeadrill Ltd BB Neg BB- Sondre StormyrSecuritas Ab BBB Stable Wr Brian Børsting MARKETWEIGHTSkandinaviska Enskilda Banken Ab A+ Neg A1 A+ Pos T. Hovard / L. Holm OVERWEIGHTSkanska Ab BBB+ Stable Emil Hjalmarsson

Recomm.Danske Bank S&P Moody's Fitch

22

Our coverage and shadow ratings 4 of 5

Ratings from S&P/Moody's/Fitch and Danske Bank Markets shadow ratings

Analyst(s)

Company Rating Outlook Sr. Unsec Rating Outlook Rating Outlook Rating OutlookSkf Ab BBB Stable Baa1 Neg Mads Rosendal UNDERWEIGHTSognekraft As BBB Stable BBB Jakob MagnussenSolstad Offshore Asa BB- Stable B+ Øyvind MossigeSpar Nord Bank A/S BBB+ Stable T. Hovard / L. HolmSparebank 1 Boligkreditt As A- Stable T. Hovard / L. HolmSparebank 1 Nord Norge A1 Stable A Stable T. Hovard / L. Holm UNDERWEIGHTSparebank 1 Smn A1 Stable A- Stable T. Hovard / L. Holm MARKETWEIGHTSparebank 1 Sr-Bank Asa A1 Stable A- Stable T. Hovard / L. Holm UNDERWEIGHTSponda Oyj BBB- Stable Emil HjalmarssonSsab Ab BB- Stable Mads RosendalSt1 Nordic Oy BB Stable Jakob MagnussenStatkraft Sf A- Stable Aaa Stable Jakob Magnussen OVERWEIGHTStatnett Sf A+ Stable Wr Stable Jakob Magnussen MARKETWEIGHTStatoil Asa AA- Stable Aa2 Stable Jakob Magnussen UNDERWEIGHTSteen & Strom As BBB+ Stable Ola HeldalStena Ab BB Stable B2 Stable Niklas Ripa MARKETWEIGHTStockmann Oyj Abp B+ Stable Mads RosendalStolt-Nielsen Ltd BB+ Stable BB Bjørn Kristian RøedStora Enso Oyj BB Stable Ba2 Stable WD Mads Rosendal MARKETWEIGHTStorebrand Bank Asa BBB+ Stable BBB+ Neg Nr Stable T. Hovard / L. HolmStorebrand Livsforsikring As A- Neg Baa1 Stable T. Hovard / L. HolmSunnfjord Energi As BBB- Stable BBB- Jakob MagnussenSuomen Hypoteekkiyhdistys A- Stable T. Hovard / L. HolmSvensk Fastighetsfinansiering Ab BBB Stable Louis LandemanSvenska Cellulosa Ab Sca A- Stable Baa1 Stable Mads Rosendal MARKETWEIGHTSvenska Handelsbanken Ab AA- Neg Aa3 AA- Stable T. Hovard / L. Holm MARKETWEIGHTSwedavia Ab A- Stable Gabriel BerginSwedbank Ab A+ Neg A1 A+ Pos T. Hovard / L. Holm MARKETWEIGHTSwedish Match Ab BBB Stable Baa2 Stable Brian Børsting MARKETWEIGHTSydbank A/S Baa T. Hovard / L. Holm OVERWEIGHTSaab Ab BBB+ Stable Wr Emil HjalmarssonTallink Grupp As BB Stable BB- Niklas Ripa

Recomm.Danske Bank S&P Moody's Fitch

23

Our coverage and shadow ratings 5 of 5

Source: Standard & Poor's, Moody's, Fitch, Danske Bank Markets

Ratings from S&P/Moody's/Fitch and Danske Bank Markets shadow ratings

Analyst(s)

Company Rating Outlook Sr. Unsec Rating Outlook Rating Outlook Rating OutlookTdc A/S BBB Neg Baa3 Stable BBB Neg Ola Heldal MARKETWEIGHTTechnopolis Oyj BB+ Stable BB Louis LandemanTeekay Offshore Partners Lp BB- Stable B+ Bjørn Kristian RøedTele2 Ab BBB Stable Ola HeldalTelefonaktiebolaget Lm Ericsson BBB+ Stable Baa1 Stable BBB+ Stable Ola Heldal MARKETWEIGHTTelenor Asa A Stable A3 Stable Ola Heldal MARKETWEIGHTTeliasonera Ab A- Stable A3 Neg A- Stable Ola Heldal UNDERWEIGHTTeollisuuden Voima Oyj BBB Neg Wr BBB Stable Jakob Magnussen OVERWEIGHTThon Holding As BBB+ Stable Ola HeldalTine Sa BBB+ Stable Ola HeldalUpm-Kymmene Oyj BB+ Stable Ba1 Stable WD Mads Rosendal MARKET WEIGHTVasakronan Ab A- Stable Emil HjalmarssonVattenfall Ab A- Stable A3 Stable A- Neg Jakob Magnussen MARKETWEIGHTVestas Wind Systems A/S BBB- Niklas Ripa OVERWEIGHTVictoria Park Ab BB- Stable B+ Louis LandemanVolvo Ab BBB Neg Baa2 Neg BBB Stable Mads Rosendal MARKETWEIGHTWilh Wilhelmsen Asa BBB- Stable Bjørn Kristian RøedWihlborgs Fastigheter Ab BB+ Stable BB Louis LandemanYit Oyj B Stable Emil Hjalmarsson

Recomm.Danske Bank S&P Moody's Fitch

24

Fixed Income Credit Research team Thomas Hovard, Chief Analyst Head of Credit Research +45 45 12 85 05 [email protected]

Louis Landeman, Senior Analyst TMT, Industrials +46 8 568 80524 [email protected]

Mads Rosendal, Analyst Industrials, Pulp & Paper +46 8 568 80594 [email protected]

Jakob Magnussen, Senior Analyst Utilities, Energy +45 45 12 85 03 [email protected]

Knut-Ivar Bakken, Senior Analyst Fish Farming +47 85 40 70 74 [email protected]

Brian Børsting, Senior Analyst Industrials +45 45 12 85 19 [email protected]

Lars Holm, Senior Analyst Financials +45 45 12 80 41 [email protected]

Gabriel Bergin, Analyst Strategy, Industrials +46 8 568 80602 [email protected]

Niklas Ripa, Senior Analyst High Yield, Industrials +45 45 12 80 47 [email protected]

Bjørn Kristian Røed, Senior Analyst Shipping +47 85 40 70 72 [email protected]

Ola Heldal, Senior Analyst TMT +47 85 40 84 33 [email protected]

Sondre Dale Stormyr, Senior Analyst Offshore Rigs +47 85 40 70 70 [email protected]

Henrik René Andresen, Senior Analyst Credit Portfolios +45 45 13 33 27 [email protected]

Øyvind Mossige, Senior Analyst Oil Services +47 85 40 54 91 [email protected]

Emil Hjalmarsson, Analyst Real Estate, Construction +46 8 568 80634 [email protected]

25

Disclosures

This research report has been prepared by Danske Bank Markets, a division of Danske Bank A/S (‘Danske Bank’). The author of this research report is Niklas Ripa, Senior Analyst.

Analyst certification

Each research analyst responsible for the content of this research report certifies that the views expressed in the research report accurately reflect the research analyst’s personal view about the financial instruments and issuers covered by the research report. Each responsible research analyst further certifies that no part of the compensation of the research analyst was, is or will be, directly or indirectly, related to the specific recommendations expressed in the research report.

Regulation

Danske Bank is authorised and subject to regulation by the Danish Financial Supervisory Authority and is subject to the rules and regulation of the relevant regulators in all other jurisdictions where it conducts business. Danske Bank is subject to limited regulation by the Financial Conduct Authority and the Prudential Regulation Authority (UK). Details on the extent of the regulation by the Financial Conduct Authority and the Prudential Regulation Authority are available from Danske Bank on request.

The research reports of Danske Bank are prepared in accordance with the Danish Society of Financial Analysts’ rules of ethics and the recommendations of the Danish Securities Dealers Association.

Conflicts of interest

Danske Bank has established procedures to prevent conflicts of interest and to ensure the provision of high-quality research based on research objectivity and independence. These procedures are documented in Danske Bank’s research policies. Employees within Danske Bank’s Research Departments have been instructed that any request that might impair the objectivity and independence of research shall be referred to Research Management and the Compliance Department. Danske Bank’s Research Departments are organised independently from and do not report to other business areas within Danske Bank.

Research analysts are remunerated in part based on the overall profitability of Danske Bank, which includes investment banking revenues, but do not receive bonuses or other remuneration linked to specific corporate finance or debt capital transactions.

Danske Bank, its affiliates and subsidiaries are engaged in commercial banking, securities underwriting, dealing, trading, brokerage, investment management, investment banking, custody and other financial services activities, may be a lender to the companies mentioned in this publication and have whatever rights are available to a creditor under applicable law and the applicable loan and credit agreements. At any time, Danske Bank, its affiliates and subsidiaries may have credit or other information regarding the companies mentioned in this publication that is not available to or may not be used by the personnel responsible for the preparation of this report, which might affect the analysis and opinions expressed in this research report.

See http://www-2.danskebank.com/Link/researchdisclaimer for further disclosures and information.

26

General disclaimer

This research has been prepared by Danske Bank Markets (a division of Danske Bank A/S). It is provided for informational purposes only. It does not constitute or form part of, and shall under no circumstances be considered as, an offer to sell or a solicitation of an offer to purchase or sell any relevant financial instruments (i.e. financial instruments mentioned herein or other financial instruments of any issuer mentioned herein and/or options, warrants, rights or other interests with respect to any such financial instruments) (‘Relevant Financial Instruments’).

The research report has been prepared independently and solely on the basis of publicly available information that Danske Bank considers to be reliable. While reasonable care has been taken to ensure that its contents are not untrue or misleading, no representation is made as to its accuracy or completeness and Danske Bank, its affiliates and subsidiaries accept no liability whatsoever for any direct or consequential loss, including without limitation any loss of profits, arising from reliance on this research report.

The opinions expressed herein are the opinions of the research analysts responsible for the research report and reflect their judgement as of the date hereof. These opinions are subject to change, and Danske Bank does not undertake to notify any recipient of this research report of any such change nor of any other changes related to the information provided in this research report.

This research report is not intended for retail customers in the United Kingdom or the United States.

This research report is protected by copyright and is intended solely for the designated addressee. It may not be reproduced or distributed, in whole or in part, by any recipient for any purpose without Danske Bank’s prior written consent.

27

Disclaimer related to distribution in the United States

This research report is distributed in the United States by Danske Markets Inc., a U.S. registered broker-dealer and subsidiary of Danske Bank, pursuant to SEC Rule 15a-6 and related interpretations issued by the U.S. Securities and Exchange Commission. The research report is intended for distribution in the United States solely to ‘U.S. institutional investors’ as defined in SEC Rule 15a-6. Danske Markets Inc. accepts responsibility for this research report in connection with distribution in the United States solely to ‘U.S. institutional investors’.

Danske Bank is not subject to U.S. rules with regard to the preparation of research reports and the independence of research analysts. In addition, the research analysts of Danske Bank who have prepared this research report are not registered or qualified as research analysts with the NYSE or FINRA but satisfy the applicable requirements of a non-U.S. jurisdiction.

Any U.S. investor recipient of this research report who wishes to purchase or sell any Relevant Financial Instrument may do so only by contacting Danske Markets Inc. directly and should be aware that investing in non-U.S. financial instruments may entail certain risks. Financial instruments of non-U.S. issuers may not be registered with the U.S. Securities and Exchange Commission and may not be subject to the reporting and auditing standards of the U.S. Securities and Exchange Commission.