Wednesday, September 09, 2015 The Value of eCommerce in the Healthcare Supply Chain.

41

Wednesday, March 16, 2022 The Value of eCommerce in the Healthcare Supply Chain

-

Upload

alan-potter -

Category

Documents

-

view

221 -

download

1

Transcript of Wednesday, September 09, 2015 The Value of eCommerce in the Healthcare Supply Chain.

Wednesday, April 19, 2023

The Value of eCommerce in the Healthcare Supply Chain

2

TRYING TO PREDICT WHERE THE INTERNET AND E-BUSINESS WILL TAKE US … IS LIKE ASKING THE WRIGHT BROTHERS WHAT THEY THOUGHT

ABOUT THE FREQUENT FLIER PROGRAMS!

3

Content of Discussion

•Market Overview

•eBusiness Expectations

•Australian Landscape

•Strategic Issues

•Supply Chain Reform

•GHX Overview

4

Asia-Pacific Market

• The Asia-Pacific market for Medical Equipment and Med/Surg Consumables is estimated at US$24 billion – 21% of the global market

Pharmaceuticals

80% (US $94 bn)

Med Eqpt &Med/Surg Consumables

20% (US$24 bn)

Asia Pacific Human Healthcare Products MarketUS$118 billion*

* Substantial disagreement exists on the market definitionSource : Medistat; Dash Report; PwC Analysis

• Medical Equipment and Med/Surg Consumables account for approximately 20% of the US$118 billion Asia-Pacific Human Healthcare Products Market

Global Medical Device MarketUS$113 billion*

Japan

US $16 bn (14%)

Other Asia-Pacific

US $8 bn (7%)

5

Australian Market

Global Healthcare Exchange Confidential Information

Med/Sur

g

Capital

MDD Market = US$1.1BMDD Market = US$1.1B

Retail

Hospital

Pharma Market = US$3.0BPharma Market = US$3.0B

$0.85B$0.85B

$0.25B$0.25B $0.75B$0.75B

$2.25B$2.25B

6

GHX Equity members alone hold sizable market share

Medical Equipment & Med/Surg Consumables Markets

Total US$24 bn

Source : Medistat; PwC Analysis

11 GHX equity members

c. US$8.4 bn

Other suppliers

(>10,000)

c. US$15.6 bn

65%

35%

GHX equity members have approximately 55% share of the Medical Equipment & Med/Surg Consumables market in Australia/New Zealand

GHX equity members have approximately 55% share of the Medical Equipment & Med/Surg Consumables market in Australia/New Zealand

Market Size US$ mm

Japan 16,100 Australia / New Zealand 1,770 China 1,600 Korea 880 Taiwan 770 Thailand 350 Hong Kong 270 Malaysia 240 Singapore 145 Philippines 130 Indonesia 90 Vietnam 60 India / Pakistan 1,540 Other 55

Total APAC

US$24bn

55%

45%

AUSUS$1.1bn

11 GHX equity members

c. US$0.60 bn

Other suppliers

c. US$0.50 bn

7

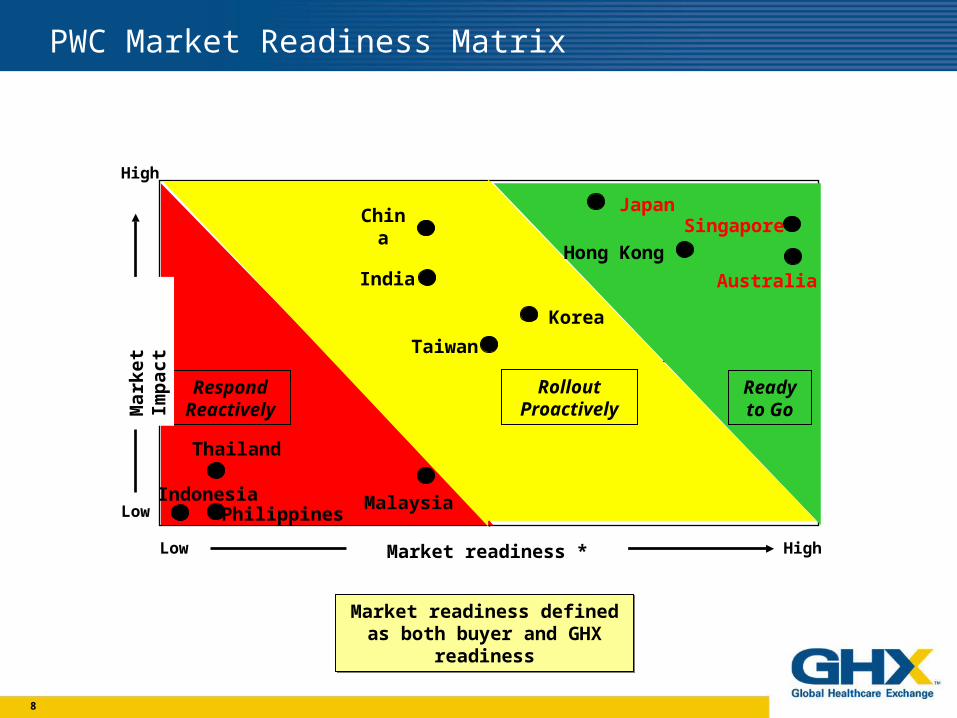

Market readiness criteria focus on issues impacting potential speed of launch and rollout

Market size E-readinessEnglish /

single byte

Customerconcentra-

tion

Supply chainoperations

hub

Customer ITconcentra-

tion

Supply chainefficiency

Govt supportfor e-

business

Japan

Australia

China

India

Korea

Taiwan

Thailand

Hong Kong

Malaysia

Singapore

Philippines

Indonesia

% Internet usage

% public sector &

presence of private chains

Exports & production of medical equipment

% using major ERP

systems

Direct distribution & delivery

times

Infrastructure support & investment incentives

Ease of use of US

platform

8

GHX Proposed Strategy & Timing in Asia Pacific is Based on Market Readiness

Low High

High

Low

Ready to Go

Respond Reactively

Market readiness *

Mar

ket

Imp

act

Rollout Proactively

IndonesiaPhilippines

Singapore

Malaysia

Hong Kong

Thailand

Taiwan

Korea

India

China

Australia

Japan

Market readiness defined as both buyer and GHX readinessMarket readiness defined as

both buyer and GHX readiness

PWC Market Readiness Matrix

9

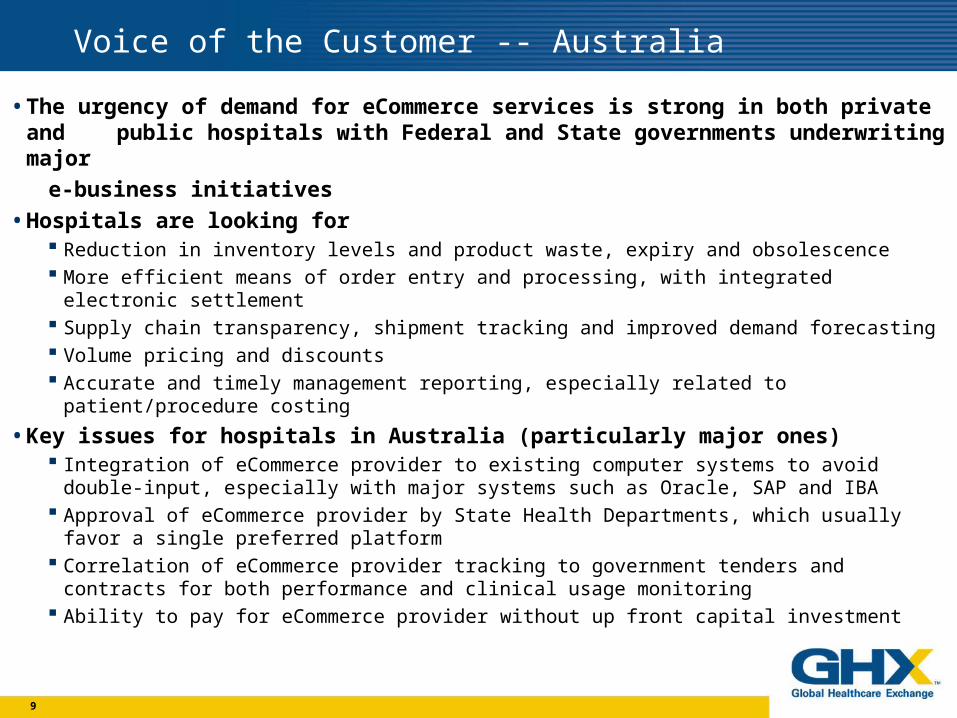

Voice of the Customer -- Australia

• The urgency of demand for eCommerce services is strong in both private and public hospitals with Federal and State governments underwriting major

e-business initiatives

• Hospitals are looking for Reduction in inventory levels and product waste, expiry and obsolescence More efficient means of order entry and processing, with integrated electronic settlement Supply chain transparency, shipment tracking and improved demand forecasting Volume pricing and discounts Accurate and timely management reporting, especially related to patient/procedure costing

• Key issues for hospitals in Australia (particularly major ones) Integration of eCommerce provider to existing computer systems to avoid double-input,

especially with major systems such as Oracle, SAP and IBA Approval of eCommerce provider by State Health Departments, which usually favor a single

preferred platform Correlation of eCommerce provider tracking to government tenders and contracts for both

performance and clinical usage monitoring Ability to pay for eCommerce provider without up front capital investment

10

(A) Some of the supplier cost may be shifted to the hospital if full freight is charged. This is most common in Australia with smaller specialised companies and non-stock products.

(B) Assume: AUD$1.54 billion/year medical-surgical product sales AUD$1.74 billion/year total delivered cost for these same sales

(C) Not including facility costs

Supplier supply chain costs (C)

Hospital supply chain costs(C)

Product manufacturing and sales costs(includes related indirects, taxes and profit margin)

13-14%

12-13%

73-75%

Product sale price (A)

Summary of supply chain (process) costs as a percentage of total delivered cost (B)

© DASH Project Team

11

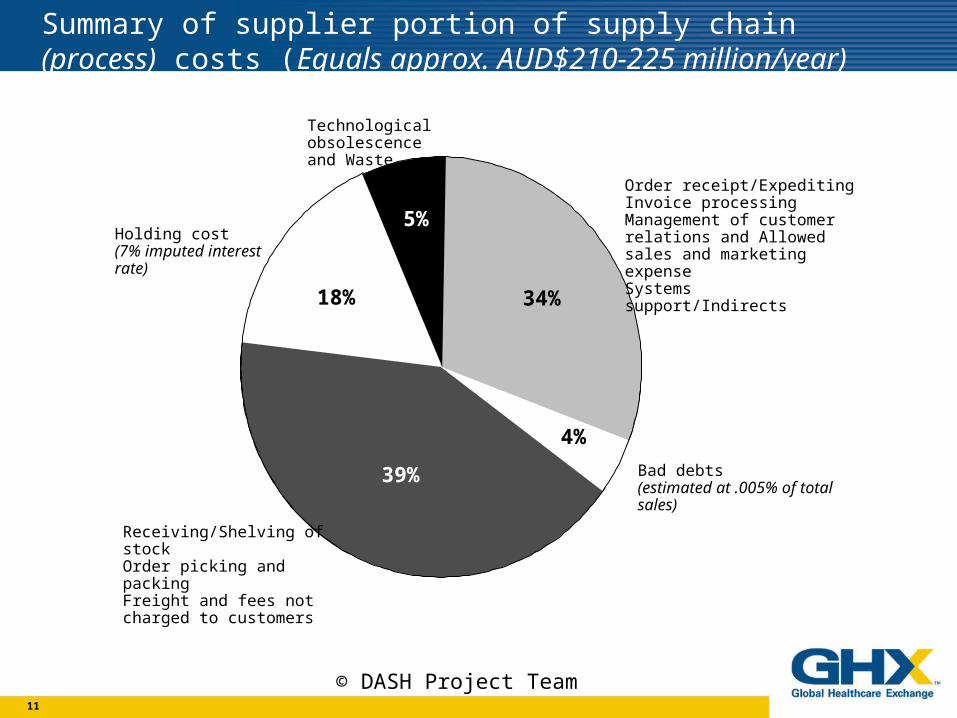

Bad debts (estimated at .005% of total sales)

Order receipt/ExpeditingInvoice processingManagement of customer relations and Allowed sales and marketing expenseSystems support/Indirects

4%

18% 34%

39%

Technological obsolescenceand Waste

Holding cost (7% imputed interest rate)

Receiving/Shelving of stockOrder picking and packingFreight and fees not charged to customers

5%

Summary of supplier portion of supply chain (process) costs (Equals approx. AUD$210-225 million/year)

© DASH Project Team

12

(A) Does not include external contract assistance from separate organisation such as HSA, NSW Peak Purchasing Council, Qld Health, Catholic HealthCare Services, etc.

Waste (Expiry, Theft, Loss and Damage)

Freight and fees

Order placement/ExpeditingInvoice payments and creditsManagement of supplier relations (A)Systems support/indirects

4%

9%

20%

40%

21%

6%

Technological obsolescence(Unused non-stock product due to changes in clinical practice, physician preference, or technological development)

Holding cost of stock and non-stock (7% imputed interest rate)

Receiving/Shelving of stockOrder picking and packingDelivery and imprest replenishment

Summary of hospital portion of supply chain (process) costs (Equals approx. AUD$225-245 million/year)

© DASH Project Team

13

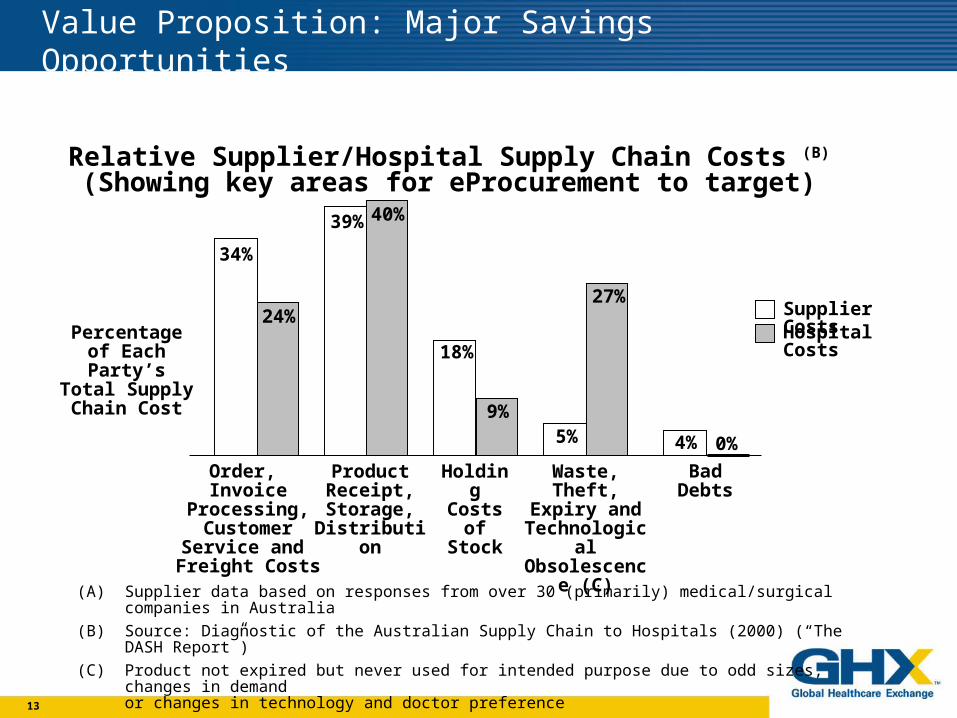

Value Proposition: Major Savings Opportunities

Relative Supplier/Hospital Supply Chain Costs (B)

(Showing key areas for eProcurement to target)

(A) Supplier data based on responses from over 30 (primarily) medical/surgical companies in Australia

(B) Source: Diagnostic of the Australian Supply Chain to Hospitals (2000) (“The DASH Report”)

(C) Product not expired but never used for intended purpose due to odd sizes, changes in demand or changes in technology and doctor preference

34%

24%

39% 40%

18%

9%5%

27%

4% 0%

Percentage of Each Party’s Total

Supply Chain Cost

Order, Invoice Processing, Customer Service

and Freight Costs

Product Receipt,Storage,

Distribution

Holding Costs of

Stock

Waste,Theft,

Expiry andTechnological Obsolescence

(C)

Bad Debts

Supplier CostsHospital Costs

14

Key Findings

• The potential benefits of eCommerce in Healthcare are staggering -$235MM in annual savings

• The savings are derived from: Improved Process efficiency through standardisation & automation Elimination of off-contract buying through better defined, tightly controlled processes Improved standardisation & rationalisation of products Improved productivity associated with efficient, effective product search processes

and improved demand forecasting Reduced product inventories and obsolescence throughout the supply chain

• The initiatives with the highest priority within the trading community include:

Process/Product standardisation Electronic Catalogue eBusiness platform with a National/International Hub

Source: Diagnostic of the Australian Supply Chain to Hospitals (2000) (“The DASH Report”)

15

Key strategic issues

• Australian Health is struggling to define which entity will lead e-commerce (ie, States, Private, Wholesalers, Industry, etc.)

• Australia will probably have different solutions for payment (Medicare/Private Funds), clinical data and procurement

• Australia will probably have different solutions for B2C (downstream) and B2B (upstream) procurement

16

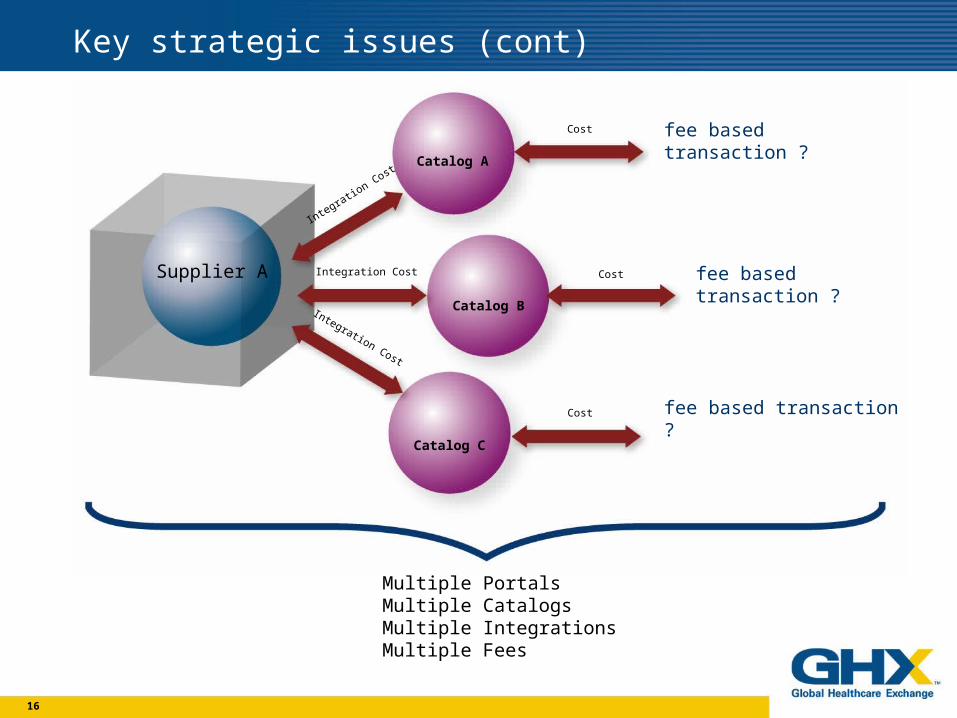

Key strategic issues (cont)

Supplier A

Integration Cost

Integration Cost

Integration Cost

Cost

Cost

Cost

Catalog A

Catalog B

Catalog C

fee based transaction ?

fee based transaction ?

fee based transaction ?

Multiple PortalsMultiple CatalogsMultiple IntegrationsMultiple Fees

17

Key strategic issues (cont)

• B2C has suffered recently because of company negatives – but this is different than concept negatives

• B2C in reality has always been very tough to implement - but very rewarding to those who do.

• Full B2C benefits will require “deep integration” between suppliers/customers in some form

18

Asia Pacific Landscape

• PACIFIC HEALTHCARE EXCHANGE (AUSTRALIA)• Underwent significant capital restructuring

• Change in management

• Layoff about 50% of organization

• Focus on technical consultancy and hardware exchange(core business)

• HEALTHNET ASIA• Operations in Singapore, Thailand and Japan

• Terminate operations in November 2001.

• ASIA RX• Supported by Zuellig Pharma, the largest pharm distributor in

the region

• Targeting small and medium size retail pharmacies with internet based product.

• Possible entry into Australia.

Global Healthcare Exchange Confidential Information

19

The Challenges for Materials Managers

• Purchasing complexities • Wholesaler, no Wholesaler, on contract, off contract, specialty items • Tracking contracts/purchases/rebates • No price validation at the time of order = $$ manual follow-up

• Distribution • Consolidation of hospitals means centralisation of warehousing; distribution to numerous facilities

• Information systems • Disparate standalone or manual systems evolving toward integrated, enterprise-wide IT solutions. • Limited use of data warehouse and historical information • Automated connections to external partners non-existent or under utilised

• Financial responsibility • Responsible for cost/budget management • Total lifecycle costs vs. product costs • Organisationally, link to clinical effectiveness is not well defined

20

What’s Driving Change to the Supply Chain?

• Materials managers are focused on managing costs

• According to the Australian DASH Report, there are significant industry wide savings

•Emerging global drive for common standards in e-healthcare

21

Win - Win B2C Exchange Goals

Customer Goals• Reduce inventory / waste / obsolescence• Improve supply chain efficiency• Standardise on (govt./mgt.) tenders• Conform to (govt./mgt.) reporting needs • Overall – decrease total cost Supplier Goals• Single Industry Catalog• Protect market position• Improve customer support/service• Improve supply chain efficiency• Obtain key market/usage data• Overall – increase market share

22

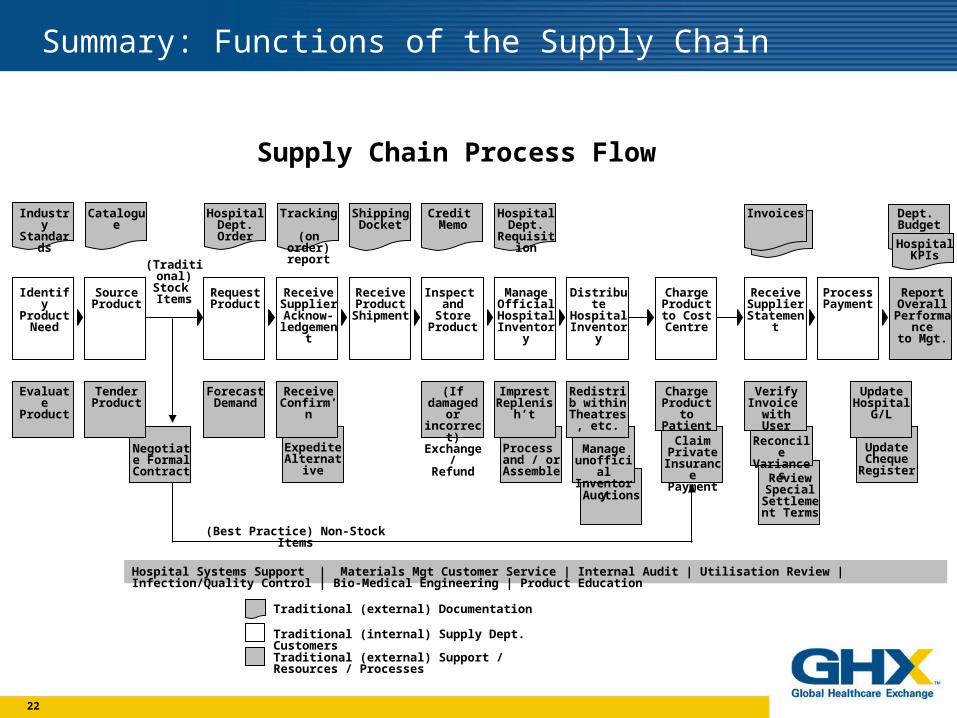

Summary: Functions of the Supply Chain

Industry Standards

Catalogue Hospital Dept. Order

Tracking (on order)

report

Shipping Docket

Credit Memo

Hospital Dept.

Requisition

Invoices Dept. Budget

Identify Product

Need

Source Product

Request Product

Receive Supplier Acknow-

ledgement

Receive Product

Shipment

Inspect and Store Product

Manage Official

Hospital Inventory

Distribute Hospital

Inventory

Charge Product to

Cost Centre

Receive Supplier

Statement

Process Payment

Report Overall

Performanceto Mgt.

Evaluate Product

Tender Product

Forecast Demand

Receive Confirm’n

(If damaged or incorrect)Exchange/

Refund

Imprest Replenish’t

Redistrib within

Theatres, etc.

Charge Product to

Patient

Verify Invoice

with User

Update Hospital

G/L

Hospital KPIs

Negotiate Formal

Contract

Expedite Alternative

Process and / or

Assemble

Manage unofficial Inventory

Auctions

Claim Private

InsurancePayment

Reconcile Variances

Review Special

Settlement Terms

Update Cheque Register

Supply Chain Process Flow

(Traditional)Stock Items

Hospital Systems Support | Materials Mgt Customer Service | Internal Audit | Utilisation Review | Infection/Quality Control | Bio-Medical Engineering | Product Education

Traditional (internal) Supply Dept. Customers

Traditional (external) Documentation

Traditional (external) Support / Resources / Processes

(Best Practice) Non-Stock Items

23

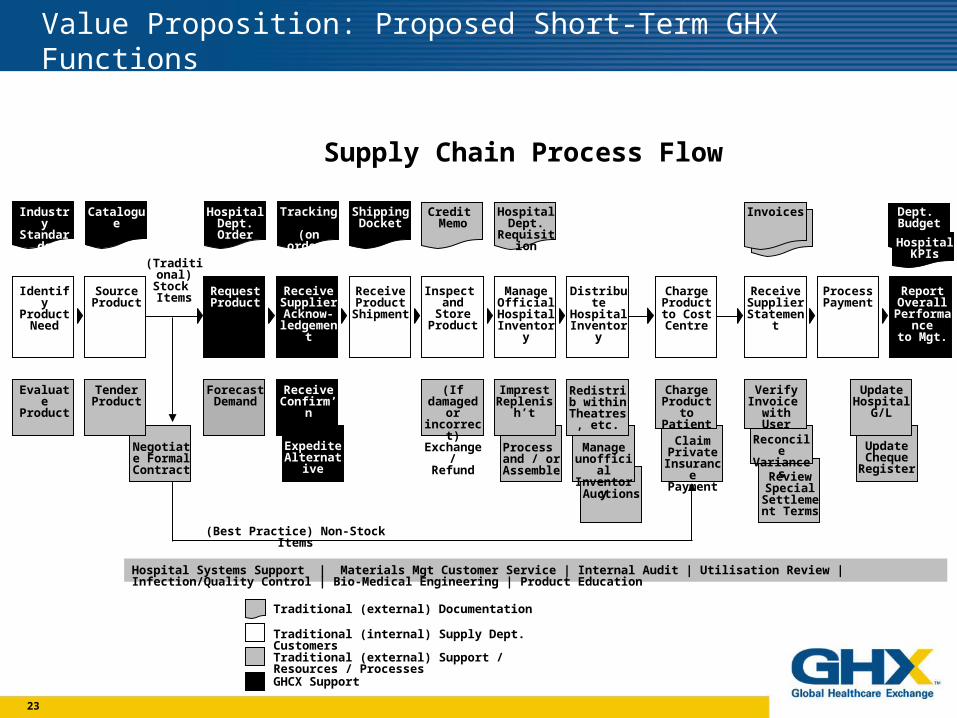

Value Proposition: Proposed Short-Term GHX Functions

Industry Standards

Catalogue Hospital Dept. Order

Credit Memo

Invoices

Identify Product

Need

Source Product

Request Product

Receive Product

Shipment

Manage Official

Hospital Inventory

Distribute Hospital

Inventory

Charge Product to

Cost Centre

Receive Supplier

Statement

Process Payment

Evaluate Product

Tender Product

Forecast Demand

Receive Confirm’n

(If damaged or incorrect)Exchange/

Refund

Imprest Replenish’t

Charge Product to

Patient

Verify Invoice

with User

Update Hospital

G/L

Hospital KPIs

Negotiate Formal

Contract

Expedite Alternative

Manage unofficial Inventory

Auctions

Reconcile Variances

Review Special

Settlement Terms

Update Cheque Register

Supply Chain Process Flow

(Traditional)Stock Items

Hospital Systems Support | Materials Mgt Customer Service | Internal Audit | Utilisation Review | Infection/Quality Control | Bio-Medical Engineering | Product Education

(Best Practice) Non-Stock Items

Tracking (on order)

report

Shipping Docket

Hospital Dept.

Requisition

Dept. Budget

Receive Supplier Acknow-

ledgement

Inspect and Store Product

Report Overall

Performanceto Mgt.

Redistrib within

Theatres, etc.

Process and / or

Assemble

Traditional (internal) Supply Dept. Customers

Traditional (external) Documentation

Traditional (external) Support / Resources / Processes

GHCX Support

Claim Private

InsurancePayment

24

Value Proposition: Proposed Long-Term GHX Functions

Industry Standards

Catalogue Hospital Dept. Order

Credit Memo

Invoices

Identify Product

Need

Source Product

Request Product

Receive Product

Shipment

Manage Official

Hospital Inventory

Distribute Hospital

Inventory

Charge Product to

Cost Centre

Receive Supplier

Statement

Process Payment

Evaluate Product

Forecast Demand

Receive Confirm’n

(If damaged or incorrect)Exchange/

Refund

Imprest Replenish’t

Redistrib within

Theatres, etc.

Verify Invoice

with User

Update Hospital

G/L

Hospital KPIs

Negotiate Formal

Contract

Expedite Alternative

Process and / or

Assemble

Manage unofficial Inventory

Auctions

Reconcile Variances

Review Special

Settlement Terms

Update Cheque Register

Supply Chain Process Flow

(Traditional)Stock Items

Hospital Systems Support | Materials Mgt Customer Service | Internal Audit | Utilisation Review | Infection/Quality Control | Bio-Medical Engineering | Product Education

(Best Practice) Non-Stock Items

Tracking (on order)

report

Shipping Docket

Hospital Dept.

Requisition

Dept. Budget

Receive Supplier Acknow-

ledgement

Inspect and Store Product

Report Overall

Performanceto Mgt.

Tender Product

Charge Product to

Patient

Claim Private

InsurancePayment

Traditional (internal) Supply Dept. Customers

Traditional (external) Documentation

Traditional (external) Support / Resources / Processes

GHCX Support

25

Need to better understand the value proposition in Australia

• To succeed in building an efficient and functional B2C in healthcare:

Suppliers and Buyers must collaborate to drive overall supply chain costs down on both sides.

Understand the 3 key category: MedSurg, Pharm and Non-Medical product groups have unique challenges.

Not just focus on the technology, but on adopting open standards and making the process more transparent and efficient.

The CATALOG is a significant task to normalise but is the cornerstone of any B2C.

Look beyond transactional efficiency -- drive operational efficiencies, eg. Reduce safety stock thus reducing risk of obsolescence and free up working capital

Need to speak the same “language”– need for an independent market value analysis so that we can work from the same page.

26

GHX Founding Members

• Founded by leading healthcare manufacturers in early 2000

• Focused on customer value, not market value

• Independent, open and integrated

• Providers and suppliers collaborating to drive inefficiency out of the healthcare supply chain

27

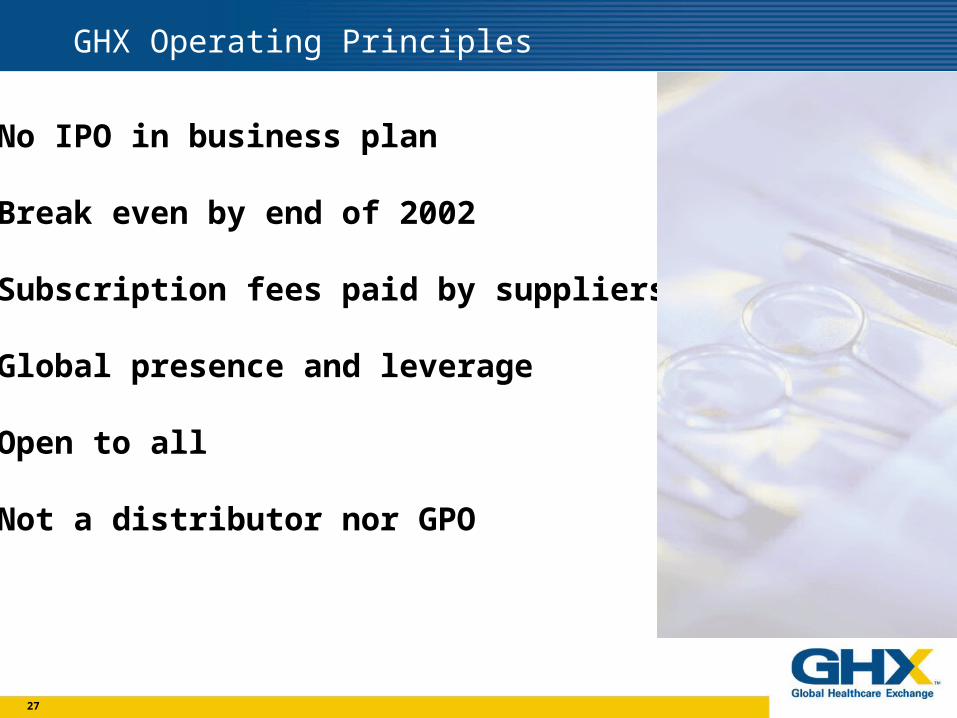

GHX Operating Principles

• No IPO in business plan

• Break even by end of 2002

• Subscription fees paid by suppliers

• Global presence and leverage

• Open to all

• Not a distributor nor GPO

28

Introducing GHX

29

How Can GHX Help Lead Change?

• Shared motivation • All participants share the pain of inefficient processes in healthcare

• Business model • No transaction fees to suppliers or providers

• Stability • Focused on customer value, not market value

• True value proposition for all participants • Adding measurable value across the supply chain

• Breadth of suppliers & products • Independent and open to all manufacturers and distributors

• Deliver technology excellence • 18 months of focused development in healthcare vertical • End-to-end connectivity • Centralised content management

30

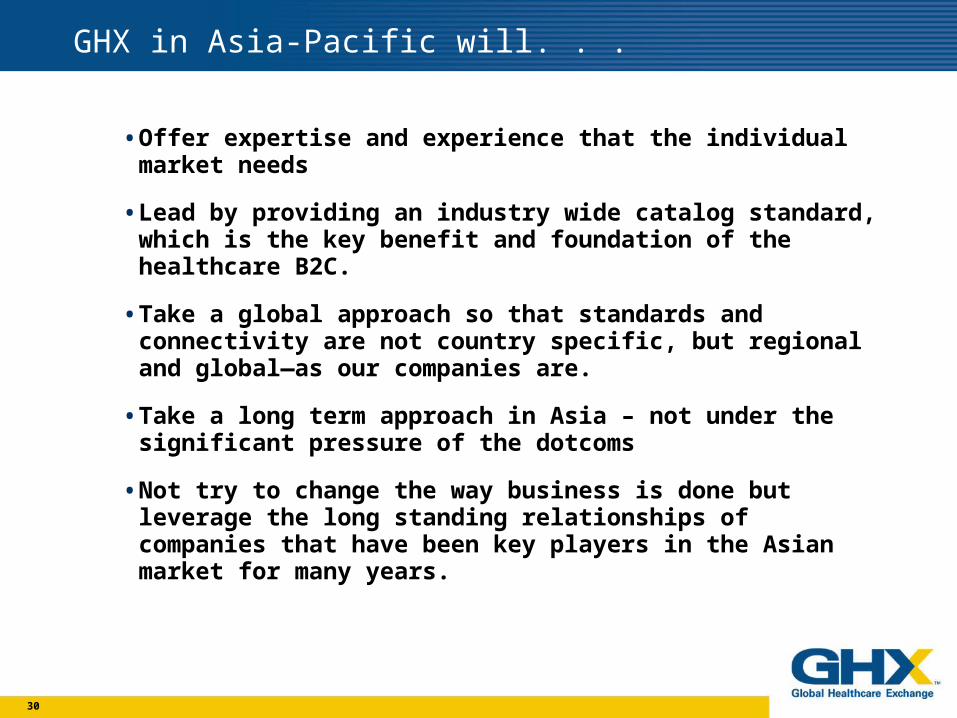

GHX in Asia-Pacific will. . .

• Offer expertise and experience that the individual market needs

• Lead by providing an industry wide catalog standard, which is the key benefit and foundation of the healthcare B2C.

• Take a global approach so that standards and connectivity are not country specific, but regional and global—as our companies are.

• Take a long term approach in Asia – not under the significant pressure of the dotcoms

• Not try to change the way business is done but leverage the long standing relationships of companies that have been key players in the Asian market for many years.

31

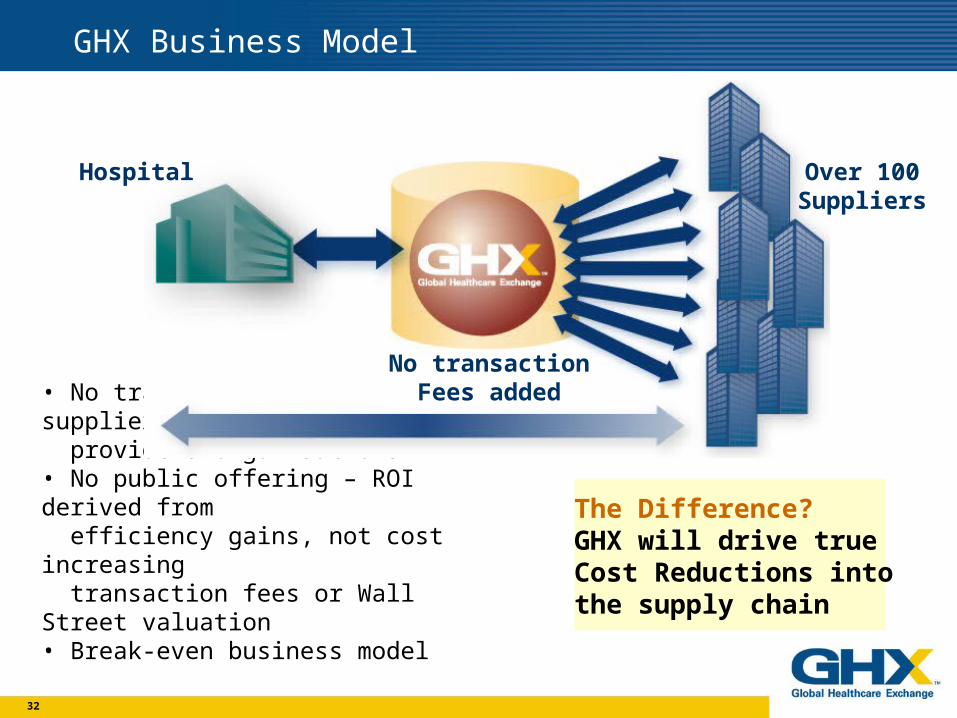

GHX Business Model

• Common connection point • Open and independent exchange • Focus on supply chain cost reduction • Improve accuracy of information (pricing / status / content / rebating) • Deliver value to all members of the healthcare supply chain

IDN

Distributors

Office ProductsSuppliers

Other Suppliers

HospitalsGPO’s

Healthcare ProductsSuppliers

Capital EquipmentSuppliers

Pharmacy Suppliers

32

GHX Business Model

• No transaction fees to suppliers or providers organisations• No public offering – ROI derived from efficiency gains, not cost increasing transaction fees or Wall Street valuation• Break-even business model

Hospital

No transactionFees added

Over 100Suppliers

The Difference?GHX will drive true Cost Reductions intothe supply chain

33

GHX Strengthens Existing Relationships

The Difference?GHX supports the existing supply chain, allowing relationships between hospitals and their trusted business partners to prosper.

GHX brings• Support to relationships between hospitals, suppliers, GPOs and distributors• Opportunities for savings to all members of the supply chain

Hospital

Supplier

Supplier

Supplier

GPO

Distributors

34

Industry Common Pain Points & Shared Motivation

The Difference?GHX is uniquely positioned to connect providers, suppliers and distributors in a real time environment for efficiencies and savings throughout the supply chain.

• All participants share the pain of inefficient processes in healthcare

• Suppliers spend millions on marketing and communication to providers, physicians and patients

• Reaching out to community is a priority for GHX member suppliers

35

GHX Core Focus in Building the Exchange

ALLSOURCE* Catalog Services • Catalog data is reviewed, maintained and updated by the manufacturers - "normalized, verified and connected" • Ability for ERP vendors to integrate into GHX catalog solution

Core Exchange Functionality • Transfer of information is reliable and efficient • Supports workability with existing systems

Connectivity Solutions • High quality, deep integration with suppliers and providers • Reproducible process, without GHX resource dependency

36

2002 Standards Approach

• Provide Industry Standard Catalog (UPN, Normalized format, support both EAN & HIBCC)

• Implement ECRI clinical taxonomy into GHX catalog

• Provide catalog synchronization services

• Industry Registry (HIN)

• Publication of GHXml 2.0 Schema for industry review

Standard Bodies + Critical Mass = Adoption

37

GHX Core Competencies

Foundation for Success

• Connectivity•suppliers and providers

• Catalog•normalized content

• Core•transaction•service

38

GHX Core Competencies

Services • Data services • Decision support • Contracting/rebates • ASP • Advanced/rich content

Strong foundation provides a good base to build on

• Connectivity•suppliers and providers

• Catalog•normalized content

• Core•transaction•service

39

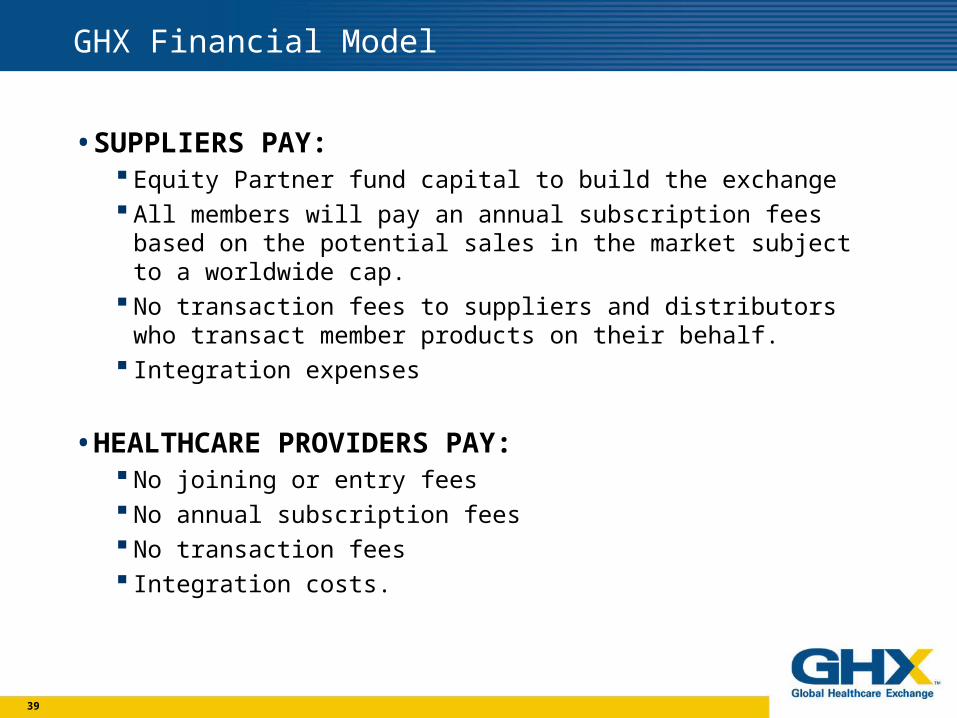

GHX Financial Model

• SUPPLIERS PAY: Equity Partner fund capital to build the exchange All members will pay an annual subscription fees based on the

potential sales in the market subject to a worldwide cap. No transaction fees to suppliers and distributors who transact

member products on their behalf. Integration expenses

• HEALTHCARE PROVIDERS PAY: No joining or entry fees No annual subscription fees No transaction fees Integration costs.

40

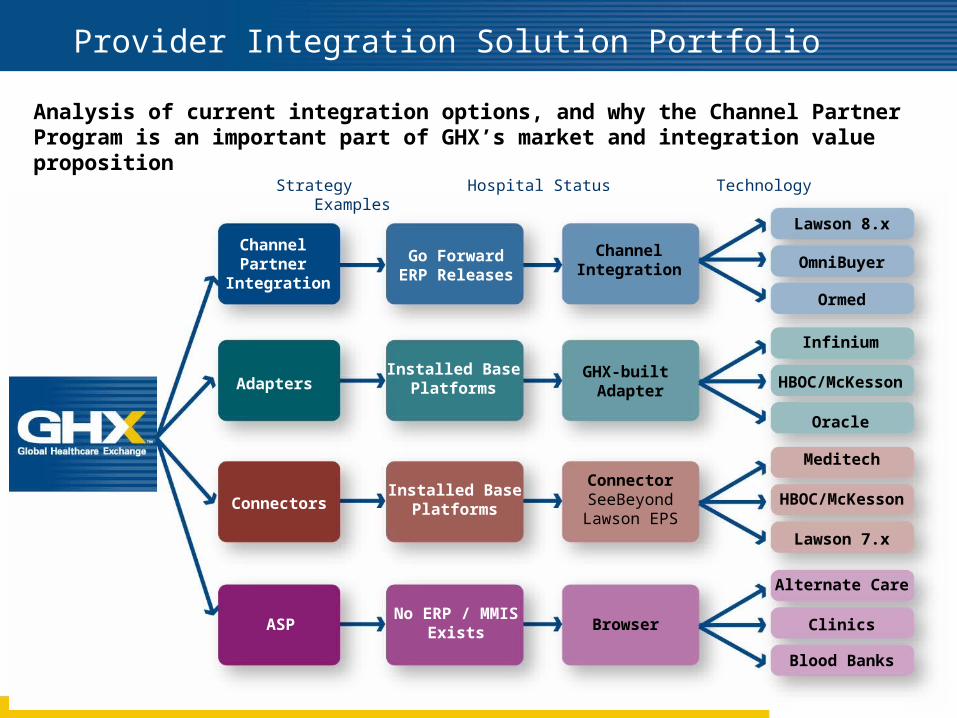

Provider Integration Solution Portfolio

Adapters

ASP

Go ForwardERP Releases

Installed BasePlatforms

No ERP / MMISExists

Channel Partner

Integration

Clinics

HBOC/McKesson

Oracle

Ormed

OmniBuyer

Lawson 8.x

Alternate Care

Blood Banks

Infinium

Strategy Hospital Status Technology Examples

Browser

ConnectorSeeBeyondLawson EPS

ChannelIntegration

Analysis of current integration options, and why the Channel Partner Program is an important part of GHX’s market and integration value proposition

ConnectorsInstalled Base

Platforms

GHX-built Adapter

HBOC/McKesson

Lawson 7.x

Meditech

41

… we recommend that the Board do not further invest in the device referred to as the “talking telegraph” as there is no market save for a

few major corporations who may have such a need …” WESTERN UNION *

* Paraphrase

HINDSIGHT 20:20 THANK YOU

![[Srijan Wednesday Webinars] Truly Scalable eCommerce with Drupal Commerce](https://static.fdocuments.in/doc/165x107/587f71dc1a28ab3f4e8b45df/srijan-wednesday-webinars-truly-scalable-ecommerce-with-drupal-commerce.jpg)