The Entrepreneurs Guide to Wealth Generation, Wealth Growth , and Wealth Preservation

WEBSITES FOR WEALTH

MANAGEMENT 2016 THE DIGITAL DIVIDE BETWEEN

WEALTH MANAGERS DEEPENS

Benchmarking – Analysis – Recommendations

www.MyPrivateBanking.com

September 2016

Emma Haffenden Roxana Palade

Senior Analyst Analyst

Report Extract

Original Report with 229 pages plus comprehensive data appendix

WEBSITES FOR WEALTH MANAGEMENT 2016 │ 2

CONTENT

1.0 EXECUTIVE SUMMARY 7

2.0 RANKING 12

2.1 OVERALL RANKING 12

2.2 DESKTOP WEBSITE RANKING 13

2.3 MOBILE WEBSITE RANKING 14

3.0 METHODOLOGY 15

3.1 SELECTION OF WEBSITES 15

3.2 USE CASES AND GUIDELINES 16

3.3 EVALUATION PROCEDURE 17

3.4 DETERMINING THE CRITERIA 18

4.0 STRATEGY – THE INTERCONNECTED WORLD AND

CONSEQUENCES FOR WEALTH MANAGER’S WEBSITE

STRATEGIES 24

4.1 MOBILE WEBSITE STRATEGY 33

4.2 DESKTOP WEBSITE STRATEGY 35

4.3 INTEGRATING SOCIAL MEDIA AND INTERACTIVITY IN THE OVERALL STRATEGY 37

4.4 THE PROGRESS OF WEALTH MANAGERS TO DATE 38

5.0 SUMMARY OF FINDINGS 40

5.1. DESKTOP 44

5.2 MOBILE 48

5.3 CONCLUSION 51

Mobile URL(s) analyzed

WEBSITES FOR WEALTH MANAGEMENT 2016 │ 3

6.0 PROFILES 52

6.1 ABN AMRO 52

6.2 ANZ 57

6.3 BARCLAYS 62

6.4 BNP PARIBAS 66

6.5 BNY MELLON 70

6.6 CHARLES SCHWAB 74

6.7 CIBC 78

6.8 CITI PRIVATE BANK 82

6.9 COMMERZBANK 86

6.10 COUTTS 91

6.11 CREDIT SUISSE 96

6.12 DANSKE BANK 101

6.13 DBS 105

6.14 DEUTSCHE BANK 110

6.15 EFG BANK 114

6.16 GOLDMAN SACHS 118

6.17 HSBC 123

6.18 BANK OF SINGAPORE 127

6.19 ING 131

6.20 INVESTEC 135

6.21 J.P. MORGAN 140

6.22 JULIUS BAER 145

6.23 KBL 149

6.24 LLOYDS 154

6.25 MERRILL LYNCH 159

6.26 MORGAN STANLEY 164

WEBSITES FOR WEALTH MANAGEMENT 2016 │ 4

6.27 PICTET 168

6.28 RBC 173

6.29 SOCIETE GENERALE 178

6.30 TD BANK 183

6.31 UBS 187

6.32 UNICREDIT 192

6.33 VONTOBEL 196

6.34 WELLS FARGO 210

6.35 WESTPAC 205

7.0 TOP 15 BEST PRACTICES 210

7.1 INTRODUCING THE ORGANIZATION AND ITS SERVICES 210

Segment specific design to attract wealthy individuals - XXX and XXX 210

Digital introduction to the business - XXX and XXX 212

Fee transparency - XXX 213

Discretionary portfolio philosophy – XXX 214

7.2 WEALTH MANAGEMENT EXPERTISE AND ENGAGING CONTENT 215

Pragmatic and relevant online advice – XXX 215

Thought leadership content and navigation - XXX and XXX 216

Encouraging interaction and propositions based around client needs – XXX 218

Educational programs and tools – XXX 219

Well-presented and accessible wealth expertise - XXX 220

7.3 FORWARD THINKING DIGITAL STRATEGY AND TOOLS 222

Digital strategy aligned to the business - XXX 222

Online services clearly part of the offer - XXX 223

Proactive approach to help clients to manage their online security - XXX 224

Innovative accessibility feature – XXX 225

Interactive tools to attract new or prospective clients – XXX 226

Integration with Social Media - XXX 227

WEBSITES FOR WEALTH MANAGEMENT 2016 │ 5

AUTHORS 228

DISCLAIMER 229

ORDER THE REPORT HERE

WEBSITES FOR WEALTH MANAGEMENT 2016 │ 6

TABLE OF CHARTS

Overall Performance Matrix, 2015 vs. 2016 rankings 8

Rich-push notifications on desktop and mobile (example via Accengage) 25

Polly Portfolio’s investments chatbot 26

The website of Essence, a private concierge office 27

Google Knowledge Graph, example output 28

Desktop and Mobile overall and top performers (average % of total available points) 40

Performance trends by category and channel, 2014-16 41

Results and winners for key user journeys 43

Desktop Navigation, Structure and Design, 2015-16 44

Desktop Content, 2015-16 45

Desktop Interactivity and Social Media, 2015-16 47

Mobile Navigation and Structure, 2015-16 48

Mobile Content, 2015-16 49

Mobile Interactivity and Social Media, 2015-16 51

Performance by category, 2015-16 51

Best Practices: XXX has embraced a segment specific approach to website design 210

Best Practices: XXX’ luxury reputation extends to their digital interface design 211

Best Practices: XXX share their client commitment principles 212

Best Practices: XXX publish extensive pricing details 213

Best Practices: XXX offer insight into their investment approach 214

Best Practices: XXX financial advice column 215

Best Practices: Engaging with our digital future via XXX’s blog 216

Best Practices: XXX offers a multimedia resource focused on client life goals 217

Best Practices: XXX is a role model for client centric websites 218

Best Practices: XXX’s multichannel approach to educating the next generation 219

Best Practices: XXX contact page and links 220

Best Practices: XXX contact page and links 221

Best Practices: XXX mobile app and website design links to the advisory approach 222

Best Practices: XXX demo of secure website features 223

Best Practices: XXX security infographic 224

Best Practices: XXX online sign language tool 225

Best Practices: Interactive eligibility test from XXX 226

Best Practices: XXX social media hub page 227

WEBSITES FOR WEALTH MANAGEMENT 2016 │ 7

EXTRACT OF THE EXECUTIVE SUMMARY

EXTRACT OF THE

EXECUTIVE SUMMARY

>> There is a growing digital divide between

those wealth managers who offer engaging

and client-friendly websites that are

continually updated and improved, and

those who are lacking in a number of key

areas. The quality of the websites of the

latter group is, at best, stagnating, and

mobile websites in particular remain a

weakness. These are the key findings of our

report for which we analyzed and ranked,

for the seventh year, the desktop and

mobile websites of 35 leading wealth

managers worldwide. Based on 36 criteria

for the desktop websites and 21 criteria for

the mobile websites, the report

benchmarks, among others, user-

friendliness and the quality of the content,

contact options and interactivity offered by

the wealth management desktop and

mobile websites of each institution. <<

The research shows that wealth managers are

stumbling where other retail industries and FinTech

players are striving to deliver great user experiences

and apply the latest technologies to their websites.

Around one third of the wealth managers we

analyzed appear to be lagging behind their peers to

such an extent that only a relaunch of their websites

would enable them to catch up. The leading wealth

managers, however, are beginning to form a

breakaway group, having developed the skills to

continuously improve their websites each year. The

report details which wealth managers are lagging

behind, improving, evolving or starting to slip in a

performance matrix that compares the results of

our 2016 benchmark with those of previous years.

Fewer than half of the benchmarked wealth

managers had consistently improved their website

performance from year to year. The average mobile

score for mobile websites remains with 50% of the

possible points low; however, on a more positive

note the number of wealth managers with no

mobile offerings at all has declined from twelve to

seven. The report identifies how the 35 wealth

managers scored for each of the 57 analyzed and

benchmarked criteria for their desktop and mobile

websites.

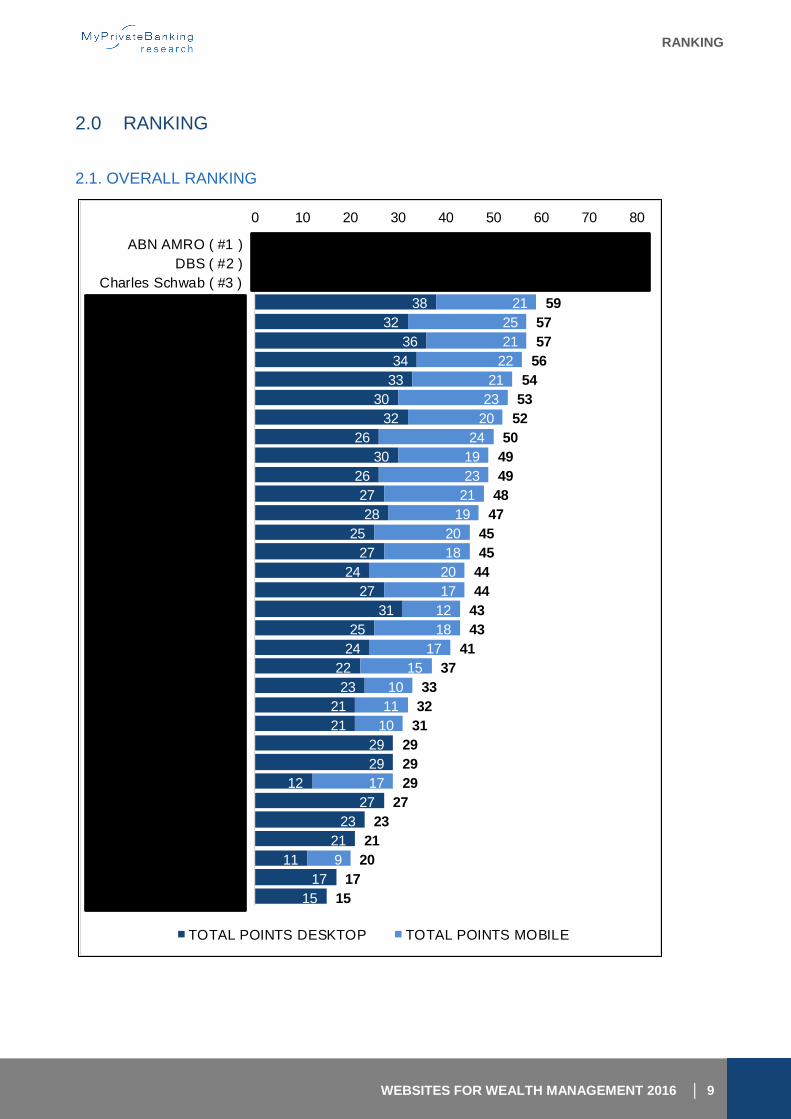

ABN AMRO, DBS AND SCHWAB TOP THE

OVERALL RANKING

The top performers continue to enhance and evolve

their websites in an effort to keep pace with new

technologies and the steadily rising bar of client

expectations. ABN AMRO is the overall winner of

MyPrivateBanking’s 2016 ranking with a total of 66

points (out of a maximum of 80), achieving this top

spot for the third consecutive year. DBS holds onto

second place with 63 points, closely followed by

Charles Schwab with 62 points and Investec with 59

points. Barclays and Vontobel are ranked joint fifth

with 57 points each.

The report includes full rankings of the 35 wealth

managers for both desktop and mobile websites.

The results for each wealth manager are analyzed in

individual profiles, including specific

recommendations for improving their websites. A

comprehensive data appendix further details the

evaluation for each criteria.

WEBSITES FOR WEALTH MANAGEMENT 2016 │ 8

EXTRACT OF THE EXECUTIVE SUMMARY

DESKTOP WEBSITES LACK TRANSPARENCY;

MOBILE WEBSITES MISS OUT ON

INTERACTIVITY

Overall in this year’s survey, desktop websites are

generally not keeping pace with user needs, and

have suffered a loss of transparency regarding key

performance measures. With respect to mobile

websites, it is a positive sign that most wealth

managers now seem to understand that a mobile

app is not a substitute for a mobile website, because

mobile websites and mobile apps have distinctive

use cases. Nevertheless, a lot of work has to be

done, particularly when it comes to interactivity.

The research data offer an in-depth assessment on

the degree to which each wealth manager’s

desktop and mobile websites are keeping up with

the needs of a demanding group of clients.

The benchmarking results demonstrate how crucial

it is for wealth managers to continuously monitor

not only each of their websites, but also those of

their competitors to ensure a competitive set of

capabilities and stay abreast of changes in

technology. Using MyPrivateBanking Research’s

proprietary evaluation framework as a

management tool, wealth managers can anticipate

new trends and focus areas to help them evolve

their websites. By keeping an objective view of their

websites, firms can avoid creating any unintended

gaps as they develop future versions. Leaders stand

out for their ability to continually evolve their

websites, but all firms need to do more to balance

out their offering so that each website performs

well independently. The report looks at how wealth

managers should enhance and evolve their desktop

and mobile websites to stand out in the market in

order to successfully engage existing clients and win

new ones.

WEBSITES FOR WEALTH MANAGEMENT 2016 │ 9

RANKING

2.0 RANKING

2.1. OVERALL RANKING

44

39

36

38

32

36

34

33

30

32

26

30

26

27

28

25

27

24

27

31

25

24

22

23

21

21

29

29

12

27

23

21

11

17

15

22

24

26

21

25

21

22

21

23

20

24

19

23

21

19

20

18

20

17

12

18

17

15

10

11

10

17

9

66

63

62

59

57

57

56

54

53

52

50

49

49

48

47

45

45

44

44

43

43

41

37

33

32

31

29

29

29

27

23

21

20

17

15

0 10 20 30 40 50 60 70 80

ABN AMRO ( #1 )

DBS ( #2 )

Charles Schwab ( #3 )

Investec ( #4 )

Barclays ( #5 )

Vontobel ( #5 )

UBS ( #7 )

BNPP ( #8 )

Coutts ( #9 )

Credit Suisse ( #10 )

Lloyds ( #11 )

Julius Bär ( #12 )

Merrill Lynch ( #12 )

J.P. Morgan ( #14 )

RBC ( #15 )

HSBC ( #16 )

Morgan Stanley ( #16 )

Pictet ( #18 )

SGPB ( #18 )

ING ( #20 )

Unicredit ( #20 )

Wells Fargo ( #22 )

Citi Private Bank ( #23 )

KBL ( #24 )

ANZ ( #25 )

Commerzbank ( #26 )

BNY Mellon ( #27 )

EFG Bank ( #27 )

Goldman Sachs ( #27 )

Danske Bank ( #30 )

CIBC ( #31 )

TD Bank ( #32 )

Westpac ( #33 )

Deutsche Bank ( #34 )

BOS ( #35 )

TOTAL POINTS DESKTOP TOTAL POINTS MOBILE

WEBSITES FOR WEALTH MANAGEMENT 2016 │ 10

METHODOLOGY

3.0 METHODOLOGY

3.1 SELECTION OF WEBSITES

This report analyzes the private banking desktop

and mobile websites of 35 leading global private

banks/wealth managers. For integrated banking

groups with multiple websites, those websites that

offered information specifically for wealthy private

clients were chosen. Secure sites, i.e. websites that

can be used only by private banks’ existing clients

and which require a login were not evaluated. The

wealth managers included were chosen by their size

in terms of assets under management to ensure

that they have a strong global influence. Of these

wealth managers, approximately eight do not have

a particularly strong global presence, but they are

among the leading providers in their national or

regional markets. In order to represent all

important regions we have included these

institutions as well.

Only content on the private banking presence itself,

or content that was directly linked from the private

banking presence, was included in the analysis.

Consideration of content that was only available on

the bank’s group or retail banking websites was

excluded, since private banking clients cannot be

expected to refer to various websites when looking

for information. On the contrary, they should be

provided with one platform that provides them with

all the information they are looking for. As the

information needs of retail and wealth

management clients differ, it is also important for a

bank to not just transfer content from the general

website, but to adapt it appropriately (e.g. provide

corporate information dedicated to the wealth

management division).

(… more in full report)

4.0 STRATEGY – THE

INTERCONNECTED WORLD

AND CONSEQUENCES FOR

WEALTH MANAGER’S

WEBSITE STRATEGIES

In this chapter we explore some important digital

trends impacting website development and shaping

our future online experiences, considering the big

picture, as well as what this means for wealth

managers.

WHERE IS THE WEB HEADING AND WHAT

DOES IT MEAN FOR WEALTH MANAGERS?

(… more in full report pages 24-39)

5.0 SUMMARY OF FINDINGS

As we now turn to consider the findings of our

analysis of 35 wealth managers’ websites, it is

important to refer to our methodology (see Chapter

3) where we explain the streamlining of this year’s

evaluation grid. This is to ensure that our evaluation

framework is updated to keep up with modern

usability and technology standards. In effect, we

apply the ‘standing on the shoulders of giants’

principle as is well-known in IT development and

expect to see a continual improvement from wealth

managers’ website efforts. This is especially as the

maturity of browser based functionality, design

tools and open source web technology such as APIs

has advanced significantly in the last couple of years

to deliver increasingly rich, sophisticated web

experiences.

(… more in full report pages 40-51)

6.0 PROFILES

(… more in full report pages 52-209)

7.0 TOP 15 BEST PRACTICES

(… more in full report pages 210-227)

AUTHORS

Steffen Binder, Managing Director and co-founder of MyPrivateBanking Research.

Steffen is Head of Research and oversees the research agenda and analyst teams.

He is responsible for creating and developing powerful concepts and relevant

content to help our clients navigate a rapidly changing digital environment. As

a regular speaker at finance and technology industry events around the globe,

Steffen is frequently quoted by leading business media such as the Wall Street

Journal, Handelsblatt and the Financial Times. Prior to this, Steffen was Managing

Director of Forrester Germany, Switzerland and Austria. He came to Forrester

through its acquisition of Forit GmbH, a leading European technology research

company, of which he was also a co-founder. Prior to that, Steffen was a partner at Monitor Company (Strategy

Consulting). He holds Master’s Degrees in Organizational Behavior from Rutgers University (USA) and in Public

Administration from the University of Konstanz (Germany).

Emma Haffenden, Senior Analyst, has over 10 years of experience in wealth

management and technology, mostly delivering analysis, business and technology

strategy consulting and research services to C level Executives of the leading global

financial institutions. In her previous roles, she led the Wealth & Private Banking

practice at Expand Research, a subsidiary of BCG, and was a Senior Consultant and

member of the Wealth Leadership team at Capco in London. Emma has a degree in

IT and Criminology, and a Master’s in Database Systems from the University of

Westminster.

Roxana Palade, Analyst, specializes in research in the fields of mobile apps for

wealth management and online presences of wealth managers. Her specific

interests are in the areas of Web 2.0 technologies, vendor management and data

mining. Roxana has held a number of research positions in business and

academia in Germany, India and Romania. She has a Master’s Degree in British

and American Studies from the University of Konstanz (Germany) and a Master’s

Degree in Literature from the Alexandru Ioan Cuza University, lasi (Romania).

DISCLAIMER

IMPORTANT NOTICE AND DISCLAIMERS:

NO INVESTMENT ADVICE

This report is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction where

such an offer or solicitation would be illegal. This report is distributed for informational purposes only and

should not be construed as investment advice or a recommendation to sell or buy any security or other

investment, or undertake any investment strategy. It does not constitute a general or personal

recommendation or take into account the particular investment objectives, financial situations, or needs of

individual investors. The price and value of securities referred to in this report will fluctuate. Past performance

is not a guide to future performance, future returns are not guaranteed, and a loss of all of the original capital

invested in a security discussed in this report may occur. Certain transactions, including those involving futures,

options, and other derivatives, give rise to substantial risk and are not suitable for all investors.

DISCLAIMERS

There are no warranties, expressed or implied, as to the accuracy, completeness, or results obtained from any

information set forth in this report. MyPrivateBanking GmbH will not be liable to you or anyone else for any

loss or injury resulting directly or indirectly from the use of the information contained in this report, caused in

whole or in part by its negligence in compiling, interpreting, reporting or delivering the content in this report.

COPYRIGHT

MyPrivateBanking GmbH’s Products are the property of MyPrivateBanking GmbH, Switzerland, and are

protected by Swiss and international copyright law and other intellectual property laws. Customers are

prohibited to copy, forward or store MyPrivateBanking Products outside of the legal entity that has made the

purchase.

MyPrivateBanking GmbH

Hafenstrasse 50B

CH-8280 Kreuzlingen, Switzerland

Tel. +41 71 566 10 05

For our latest reports please check: http://www.myprivatebanking.com/Category/reports