Webinar Slides: Mid-Year Audit and Tax Brief for Public Companies

55

1 #CBIZMHMwebinar CBIZ & MHM Executive Education Series™ Mid-Year Audit and Tax Brief Presented by: Rich Howard, Brad Hale, Scott Wragg & Dave Lewin June 29, 2015

-

Upload

mayer-hoffman-mccann-pc -

Category

Economy & Finance

-

view

66 -

download

5

Transcript of Webinar Slides: Mid-Year Audit and Tax Brief for Public Companies

1 #CBIZMHMwebinar

CBIZ & MHM Executive Education Series™ Mid-Year Audit and Tax Brief

Presented by: Rich Howard, Brad Hale, Scott Wragg

& Dave Lewin June 29, 2015

2 #CBIZMHMwebinar

To view this webinar in full screen mode, click on view options in the upper right hand corner.

Click the Support tab for technical assistance.

If you have a question during the presentation, please use the Q&A feature at the bottom of your screen.

Before We Get Started…

3 #CBIZMHMwebinar

This webinar is eligible for CPE credit. To receive credit, you will need to answer periodic participation markers throughout the webinar.

External participants will receive their CPE certificate via email immediately following the webinar.

CPE Credit

4 #CBIZMHMwebinar

The information in this Executive Education Series course is a brief summary and may not include all

the details relevant to your situation.

Please contact your service provider to further discuss the impact on your business.

Disclaimer

5 #CBIZMHMwebinar

Today’s Presenters

Rich Howard, CPA Shareholder, MHM 949.450.4402 | [email protected] Rich serves as Vice President of the Board of Directors of MHM and is a member of both our Executive Committee and Professional Standards Group. He is also the Regional Attest Practice Leader for the West Region. Rich leads our SEC practice nationwide and is a member of the Board of Directors for Kreston International, the firm's international accounting network.

Brad Hale, CPA Shareholder, MHM 727.572.1400 | [email protected] Brad has extensive experience providing audit and consulting services to public companies. He assists clients with new standard implementation, review of complex contracts and technical account matters, initial public offerings and SEC reporting. As a member of MHM's Professional Standards Group, Brad provides technical expertise to engagement teams and clients regarding revenue recognition and public company reporting.

6 #CBIZMHMwebinar

Today’s Presenters

Scott Wragg, CPA Shareholder, MHM 401.626.3234 | [email protected] Scott is a Managing Director at CBIZ Tofias and a Shareholder with MHM. He is the Tax Practice Leader for New England. Scott has over 25 years of experience in planning, supervising, and coordinating comprehensive tax services for privately-held businesses and publicly traded multinational companies. He works with many of the largest companies in New England with a primary focus in the technology, manufacturing, professional services, retail and real estate industries, and has extensive experience with federal, state, and international tax minimization strategies.

David Lewin, CPA Managing Director 617.761.0508 | [email protected] Dave is the Leader of the Accounting Advisory Practice for CBIZ Tofias. Some of the services provided by Dave include revenue recognition consulting, financial statement preparation, interpretation and implementation of new accounting standards, technical memo preparation and internal control effectiveness and efficiency. Dave has 20 years of experience in financial leadership roles and public accounting.

7 #CBIZMHMwebinar

Today’s Agenda

1

2

U.S. Regulatory Update

Other SEC and PCAOB Hot Topics

Disclosure Effectiveness 3

4 SEC Comment Letters

5 Income Taxes

8 #CBIZMHMwebinar

U.S. REGULATORY UPDATE

9 #CBIZMHMwebinar

U.S. Regulators

10 #CBIZMHMwebinar

SEC Activities

Whistleblower program IFRS Convergence Proposed Rules Pay for performance Tick size pilot

Regulation A+ Use of administrative

courts (in-house judges)

11 #CBIZMHMwebinar

Mary Jo White – Northwestern University Referred to as “Game Changer” Volume of tips greater and higher quality Whistleblowers increase efficiency 17 whistleblowers have received rewards

Payouts total nearly $50 million Awards > $1 million – 3 times Largest award - >$30 million to one individual

Tips span various securities law violations Corporate disclosures and financial

statements Securities offering fraud Market manipulation

Whistleblower Program

12 #CBIZMHMwebinar

Issues/Concerns Companies may be imposing requirements

Employees to sign confidentiality agreements Impose requirements to receive severance Foregoing whistleblower rewards Representing that they haven’t reported any prior misconduct

SEC taking action to create safe environment Investigate/charge retaliation by companies (even inadvertent) Discourage actions that limit the willingness to report fraud Wall Street Journal article stated: SEC recently contacted a number of companies Requested copies of non-disclosure, employment and other agreements

Whistleblower Program

13 #CBIZMHMwebinar

Example: Enforcement action against KBR, Inc. Related to a confidentiality agreement Used by KBR in internal investigations SEC said wording violated the whistleblower rule

(Rule 21F-17) KBR settled the matter and paid $130,000 fine KBR amended the agreement wording SEC acknowledged no actual instance where an

employee was prevented from communicating

Whistleblower Program

14 #CBIZMHMwebinar

SEC is near completing a recommendation James Schnurr, SEC Chief Accountant – May 7, 2015 No details provided but one possibility offered

Voluntary production of IFRS information In a supplemental format

Themes heard from SEC staff discussions Virtually no support for SEC to mandate IFRS Little support for an option allowing IFRS for

domestic companies Continued support for a single, global set

of standards FASB/IASB efforts

Schnurr believes collaboration is the only realistic path

IFRS Convergence

15 #CBIZMHMwebinar

Pay for Performance

Proposed disclosure rule SEC voted 3-2 on April 29, 2015 Objectives

Provide transparency to shareholders How executive compensation aligns with financial

performance Specific disclosures required

New pay vs. performance comp table Must be disclosed in proxy Comp “actually paid” to CEO and Officers Total shareholder return of company Total return of company peer group Table may cover up to 5 years Clear description of relationship between comp

actually paid and Company performance

16 #CBIZMHMwebinar

Pay for Performance

Proposed disclosure rule (cont) Required by Dodd Frank Act Section 953(a) Exemptions

Emerging Growth Companies (EGCs) Foreign Private Issuers (FPIs) Registered investment companies

Smaller Reporting Companies Scaled disclosure requirements

Filed in XBRL Must be filed using XBRL tagging First-time proxy disclosures would be tagged

17 #CBIZMHMwebinar

Pilot to Assess Tick Size

SEC approved pilot program – May 6, 2015 Proposed by securities exchanges & FINRA Assess whether wider tick sizes enhance market quality of

stocks for the benefit of investors and issuers Pilot will begin May 6, 2016 Pilot period – 2 years Include stocks of companies

$3 billion or less in market capitalization

Average daily trading volume of 1 million shares or less

Volume Weighted Average Price of at least $2.00/trading day

18 #CBIZMHMwebinar

SEC approved pilot program – (cont.) Pilot program will consist of:

1,400 securities and 3 test groups (400 securities each) Control group

Be quoted in increments of $0.01/share Trade at currently permitted increments

First test group Be quoted in increments of $0.05/share Trade at any price increment currently permitted

Second test group Be quoted in increments of $0.05/share Trade at $0.05 increments subject to certain exceptions

Third test group Same terms as Second test group Subject to “trade at” requirement to prevent price matching Additional exceptions will also apply

Pilot To Assess Tick Size

19 #CBIZMHMwebinar

SEC adopted amendment to Regulation A Enhances exempt securities offering rules Increases amount companies can raise through exempt

public offerings Impacts Tier 1 and 2 offerings Permits non-reporting U.S. and Canadian issuers

Tier 1 offerings up to $20 million Tier 2 offerings up to $50 million In 12 months, without registration Beginning June 19, 2015

Regulation A+

20 #CBIZMHMwebinar

Regulation A+ offering statement Must be qualified with SEC prior to securities sales Permits “testing the waters” solicitations without any filing Simplified qualification and disclosure requirements

(examples include): First time A+ issuer may submit drafts on a confidential basis Final must be filed 21 days before qualification Financial statements - 2 years required In US GAAP (IFRS ok for Canadian issuers) No audits for Tier 1 offering Audits required for Tier 2 offering PCAOB auditor not required for Tier 2

Regulation A+

21 #CBIZMHMwebinar

OTHER SEC AND PCAOB HOT TOPICS

22 #CBIZMHMwebinar

SEC and PCAOB Hot Topics and Activity

SEC Focus Looking for Potential

Fraud Use of Big Data Auditor Independence Enforcement Actions

PCAOB Activity Current Agenda Items Reorganization of Audit

Standards Impact of AS 18 on

Executive Compensation

23 #CBIZMHMwebinar

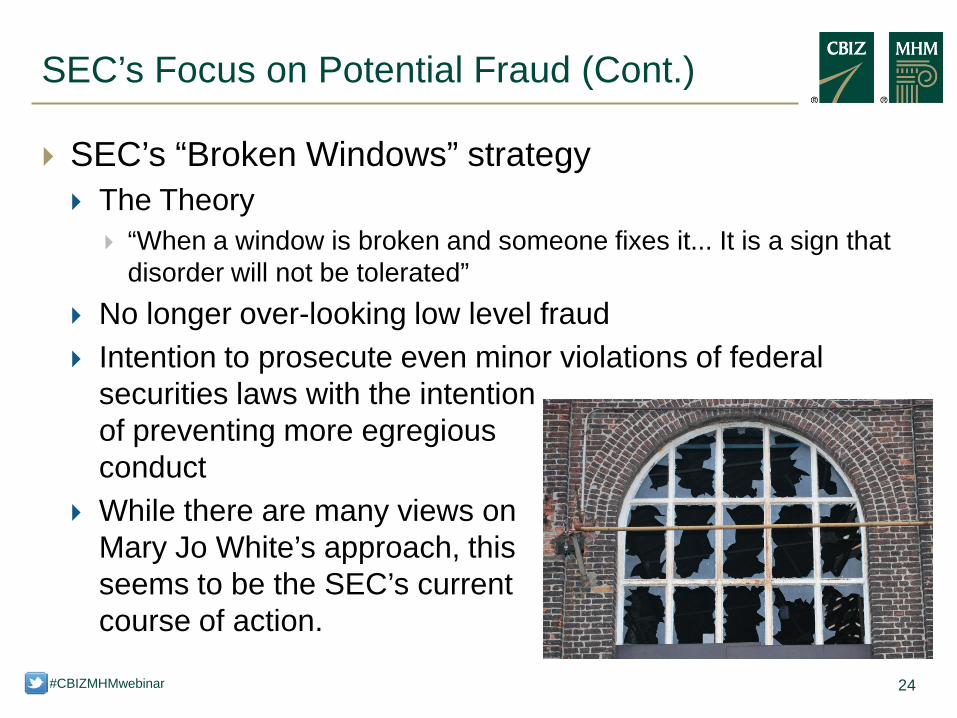

The SEC is going on the offensive and are setting their own agenda: Chairwoman Mary Jo White’s “Broken Windows” Strategy for

securities enforcement No longer waiting for self-reporting on the heals of a restatement Proactively looking for potential fraud More sophisticated in their approach to gathering and analyzing

data Gathering “Big Data” through required XBRL tagging Analyzing the Data with their Accounting Quality Model tool

Enforcement actions are increasing in number, covering a broader scope of items and the ramifications are more severe in nature.

SEC’s Focus on Potential Fraud

24 #CBIZMHMwebinar

SEC’s “Broken Windows” strategy The Theory

“When a window is broken and someone fixes it... It is a sign that disorder will not be tolerated”

No longer over-looking low level fraud Intention to prosecute even minor violations of federal

securities laws with the intention of preventing more egregious conduct

While there are many views on Mary Jo White’s approach, this seems to be the SEC’s current course of action.

SEC’s Focus on Potential Fraud (Cont.)

25 #CBIZMHMwebinar

SEC’s Use of Big Data

Big Data The SEC is using all of its data sources to: • Identify potential fraud • Carry out investigations • Prosecute cases • Create policy

XBRL – SEC’s Treasure Chest of Data! • Public companies are required to use XBRL for: • 10-K and 10-Q • 20-F and 40-F filings • Audited financial information included in 8-K filings • Within these filings, there are thousands of “Tags” in XBRL

26 #CBIZMHMwebinar

SEC’s Use of Big Data

Focus on XBRL Quality

As of October 31, 2014 the SEC rules protecting filers from liability related to XBRL misstatements and mistakes have expired.

SEC has shifted focus to the quality of the XBRL submissions.

• Pressure on SEC by Congress for high quality

High quality XBRL submissions have two traits:

• Prepared in a manner that is consistent with other filers • Convey the same information as the traditional HTML financial statements

Use of third party service providers for XBRL filings is high.

“A sloppy XBRL filing by a company whose financials are in good order may be flagged for examination.”

• Lou Rohman – Merrill Corp’s President of XBRL Services

27 #CBIZMHMwebinar

SEC’s Use of Big Data

Accounting Quality Management (AQM)

Powerful tool that culls XBRL tagged data

• Also utilized data in MD&A, press releases and other investor communications

Aids in identifying earnings management by identifying unusual trends when compared to:

• Past filings • Industry data and trends • Competitor data

AQM generates a risk score.

• SEC uses for priority examinations • Scores provided to directly to enforcement division

The higher the risk rating the more likely to be picked for examination…

28 #CBIZMHMwebinar

SEC’s Use of Big Data

How AQM works

Analyzing discretionary accruals

• Start with total accruals = GAAP net income minus cash flows • Non-discretionary accruals are then culled out to get to discretionary

accruals,

Discretionary accruals are subjective, require judgment and subject to significant management estimate. Examples are as follows:4 • Allowance for bad debts • Allowances for doubtful loans or lease losses • Inventory reserves • Fair value accounting • Reserves and accruals

29 #CBIZMHMwebinar

SEC’s Focus on Auditor Independence

SEC continues to focus on Auditor Independence “Independence is an issue that we are very focused on, and will continue to stay focused on,” Michael

Maloney, chief accountant at the SEC’s Division of Enforcement – WSJ, May 12th 2015 Outside of enforcement, the SEC gets about 400 auditor-independence questions a year, or about

one a day, says the agency’s chief accountant, James Schnurr. WSJ, May 12th 2015

Under Rule 2-01 of Regulation S-X, there are four questions the SEC considers when assessing auditor independence: Does the engagement create a mutual or conflicting interest? Does it put the auditor in a position of auditing his or her own work? Does it result in the auditor acting as a member of management or an employee of its

audit client? Does it put the auditor in a position of being the client’s advocate?

SEC Areas of Focus on Auditor Responsibilities: Auditor assistance in the preparation of financial statements they were auditing

Even items as little as report processing Audit partner rotation Prohibited services

$8.2M dollar settlement with a big 4 firm in 2014 Lobbying on behalf of audit client

$4M settlement with a big 4 firm in 2014

30 #CBIZMHMwebinar

The current trend does not appear to be changing…

Enforcement Actions

Numbers for FY Ended 9/2014 Largest amount of enforcement actions brought in a single year

755

Largest total value of monetary sanctions $4 Billion+ Largest number of cases taken to trial 30 SEC’s largest whistleblower case paid to a single individual (Sept. 2014)

$30 Million

31 #CBIZMHMwebinar

Enforcement Actions

Administrative Proceedings vs. Federal Court • Far fewer discovery and other rights • Significantly faster trial • SEC has a significantly higher success

rate • Appeals are first heard by the SEC

SEC has come under heavy fire for last two years • Both inside and outside the

Commission • For its increased use of its own

administrative proceedings rather than federal courts as preferred forum for enforcement actions

• Some believe it is unconstitutional

Certain judges expressing doubt as to the use of Administrative

proceedings

32 #CBIZMHMwebinar

Enforcement Actions (Cont.)

May 6, 2015 Wall Street Journal article - “SEC Wins With In-House Judges” • Article criticized the SEC’s use of

administrative courts. • It reported that since 2010, SEC

has won its cases: • 90% of cases brought before its

own administrative judges • 69% of cases when using federal

court • SEC responded to this article two

days later with its four-step “approach” to selecting forum

Andrew Ceresney, Head of Enforcement, argues • They are fair and unbiased • Federal securities laws should be

interpreted by experts at SEC

33 #CBIZMHMwebinar

Office of the Chief Auditor issued the PCAOB’s most recent Standard Setting Agenda on March 31, 2015 Going Concern

Pending creation of a consultation paper to seek public comment on potential approaches to take to improve assessments of going concern

Response to ASU No. 2014-15 (Presentation of FS – Going Concern) Supervision of Other Auditors and Multi-location Audit Engagements

More important with increasing number of Global Audits Staff is drafting a proposal for improving standards that govern planning,

supervision and performance of audits involving other auditors and multi-location audit engagements.

Use of specialists Continues to be an area of greater significance as the number and type of

specialists companies are engaging are growing. Typically used for complex or high risk areas that are often subject to estimate

Staff Consultation Paper 2015-1 - Open for comments due July 31,2015 Item discussed at the June 2015 SAG meeting. (Led by Greg Scates, Deputy

Chief Auditor and Greg Fletcher and Joy Thurgood, Associate Chief Auditors).

PCAOB Agenda Items

34 #CBIZMHMwebinar

Auditing Accounting Estimates, Including Fair Value Measurements and Related Disclosures Staff is considering a proposal to the Board for a standard on auditing

accounting estimates Item discussed at the June 2015 SAG meeting. (Led by Barbara Vanich,

Assoc Chief Auditor) Improving Transparency Through Disclosure of Engagement Partner and

Certain Other Participants in Audits Comment period ended March 17, 2015 Staff is drafting for the Board’s consideration a supplemental request for

comment related to the liability and an alternative location for the disclosure.

PCAOB Agenda Items

35 #CBIZMHMwebinar

Auditor’s Reporting Model Amendments to the auditor report and auditor's responsibilities Proposed new elements to the auditor’s report: Communication of critical audit matters Independence and tenure Evaluation of other information outside the financial statements

for material misstatement of facts inconsistency with information in the financial statements require communication in the auditor’s report

Re-proposal for public comment expected in Q3

PCAOB Agenda Items

36 #CBIZMHMwebinar

Quality Control Standards, Including Assignment and Documentation of Firm Supervisory Responsibilities’ Focus on improving the audit quality control process Recommendation resulting from recent PCAOB inspections Anticipated staff consultation paper to be issued in 4th quarter of

2015 Confirmation – anticipated reproposal of a proposed

auditing standard Subsequent events has been removed from the agenda

PCAOB Agenda Items

37 #CBIZMHMwebinar

On March 31, 2015, the Board adopted amendments to reorganize the PCAOB’s existing interim and currently approved auditing standards using a topical structure with a single integrated numbering system. Updated section numbers and cross references and titles Removed of standards no longer necessary Updated PCAOB rules to reflect updated standards

To-date the Board has issued 18 new auditing standards which have Superseded 12 interim standards and Amended the majority of the remaining interim standards

Will be effective 12/31/2016 pending SEC approval

Reorganization of PCAOB Audit Standards

38 #CBIZMHMwebinar

Where: PCAOB Release No. 2015-002 dated March 31, 2015 provides

details and an outline of the reorganized audit standards. Why:

Goals of the Reorganization Intended to improve the usability of the Board's standards and help users

navigate the standards more easily Replace the two part interim model – ASB / AICPA Easier to modify over time

What: None of the technical amendments made to its rules and

standards impose new requirements on auditors or change the substance of the requirements for performing and reporting on audits under PCAOB standards.

Reorganization of PCAOB Audit Standards

39 #CBIZMHMwebinar

Under the reorganization the individual standards will be grouped into the following topical categories as follows: General auditing standards Audit procedures Auditor reporting Matters relating to filings under federal securities laws Other matters associated with audits

Board also recommending that the SEC approve the amendments for application to audits of EGCs pursuant to the Jumpstart Our Business Startups (JOBS) Act.

Reorganization of PCAOB Audit Standards

40 #CBIZMHMwebinar

Audit procedures to address the risks related to executive compensation Auditor’s risk assessment – to obtain an understanding of

the company’s financial relationships and transactions with its executive officers to identify potential incentives or pressures for the achievement of a particular financial position or operating results

For compensation arrangements with executive officers, auditors will, at a minimum, need to read employment and compensation contracts, proxy statements and other relevant filings with the SEC and other regulatory agencies that relate to the company’s financial relationships and transactions with executive officers to identify risks of material misstatement.

Impact of AS 18 on Executive Compensation

41 #CBIZMHMwebinar

Require auditors to consider making inquiries of the compensation committee chair and any compensation consultants engaged by the company about the structure of the company’s compensation for executive officers and to obtain an understanding of the company’s policies and procedures for authorizing and approving executive officer expense reimbursements.

The amendments do not affect processes that compensation committees use to design executive compensation programs.

Financial relationships and transactions with its executive officers does not include an assessment of the appropriateness or reasonableness of executive compensation arrangements.

Impact of AS 18 on Executive Compensation

42 #CBIZMHMwebinar

The definition of “executive officers” is relatively broad and may include individuals whose compensation is not described in the proxy statement.

The new procedures are required to be performed in conjunction with the auditor’s risk assessment procedures pursuant to Auditing Standard No. 12, Identifying and Assessing Risks of Material Misstatement.

Impact of AS 18 on Executive Compensation

43 #CBIZMHMwebinar

DISCLOSURE EFFECTIVENESS

44 #CBIZMHMwebinar

Initially a requirement of the JOBS Act Review of Regulations S-K, S-X and Form 8-K How to leverage technology and EDGAR Objective is to make financial statements more

meaningful to investors, not just reduce the number of disclosures.

Corp Fin’s Disclosure Effectiveness Project

45 #CBIZMHMwebinar

Regulation S-K Mixture of bright lines and principles-based

requirements Outdated or duplicative requirements including

appropriate scale; Encouraging hyperlinking Number of time periods in MD&A Risk related disclosures Sustainability and social responsibility disclosures Materiality

Corp Fin’s Disclosure Effectiveness Project

46 #CBIZMHMwebinar

Regulation S-X Acquired businesses Subsidiary issuers and guarantors Equity method investees Possible solution with changes to pro forma requirements

Corp Fin’s Disclosure Effectiveness Project

47 #CBIZMHMwebinar

COMMENT LETTERS

48 #CBIZMHMwebinar

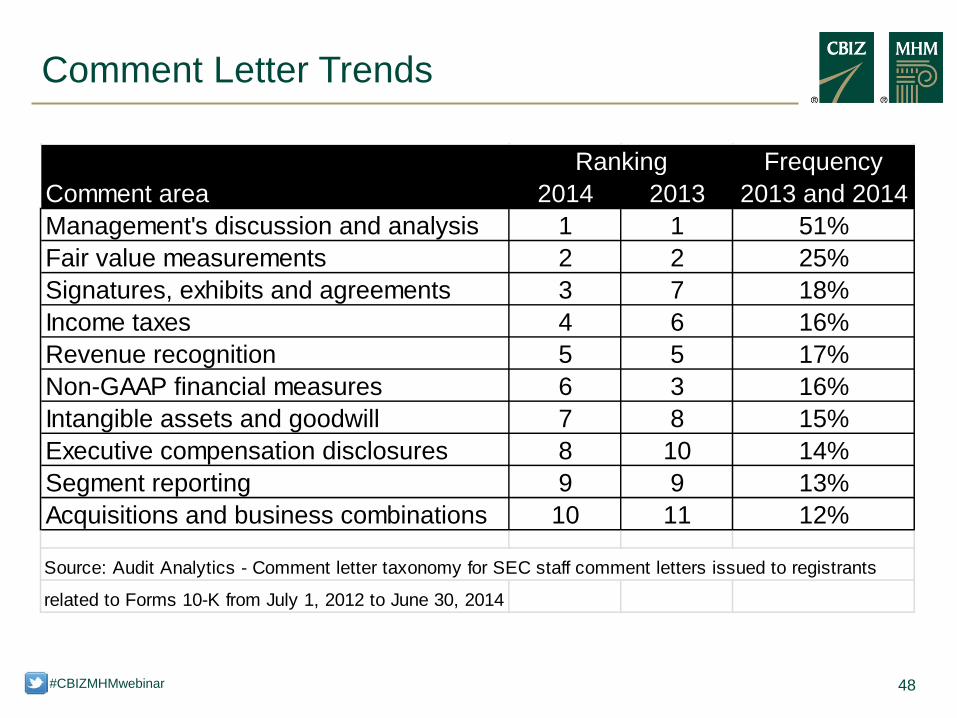

Comment Letter Trends

FrequencyComment area 2014 2013 2013 and 2014Management's discussion and analysis 1 1 51%Fair value measurements 2 2 25%Signatures, exhibits and agreements 3 7 18%Income taxes 4 6 16%Revenue recognition 5 5 17%Non-GAAP financial measures 6 3 16%Intangible assets and goodwill 7 8 15%Executive compensation disclosures 8 10 14%Segment reporting 9 9 13%Acquisitions and business combinations 10 11 12%

Source: Audit Analytics - Comment letter taxonomy for SEC staff comment letters issued to registrants

related to Forms 10-K from July 1, 2012 to June 30, 2014

Ranking

49 #CBIZMHMwebinar

Critical accounting estimates in MD&A Results of operations, known trends and uncertainties in

MD&A Income taxes Fair value Venezuelan currency matters Oil and gas industry considerations IPO registration

Areas of Focus

50 #CBIZMHMwebinar

INCOME TAXES

51 #CBIZMHMwebinar

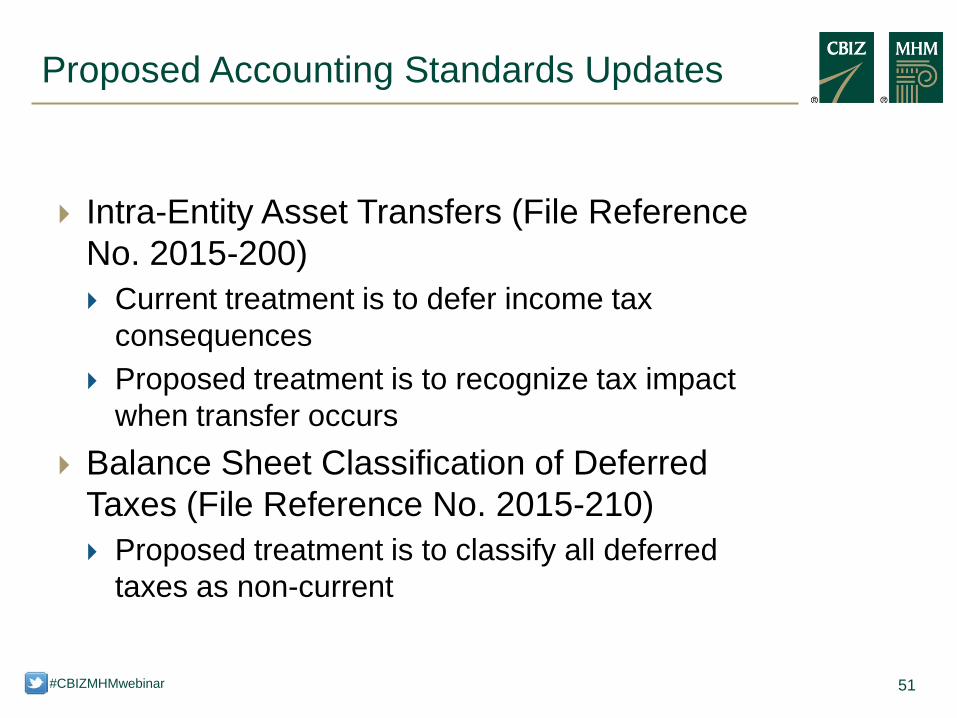

Proposed Accounting Standards Updates

Intra-Entity Asset Transfers (File Reference

No. 2015-200) Current treatment is to defer income tax

consequences Proposed treatment is to recognize tax impact

when transfer occurs Balance Sheet Classification of Deferred

Taxes (File Reference No. 2015-210) Proposed treatment is to classify all deferred

taxes as non-current

52 #CBIZMHMwebinar

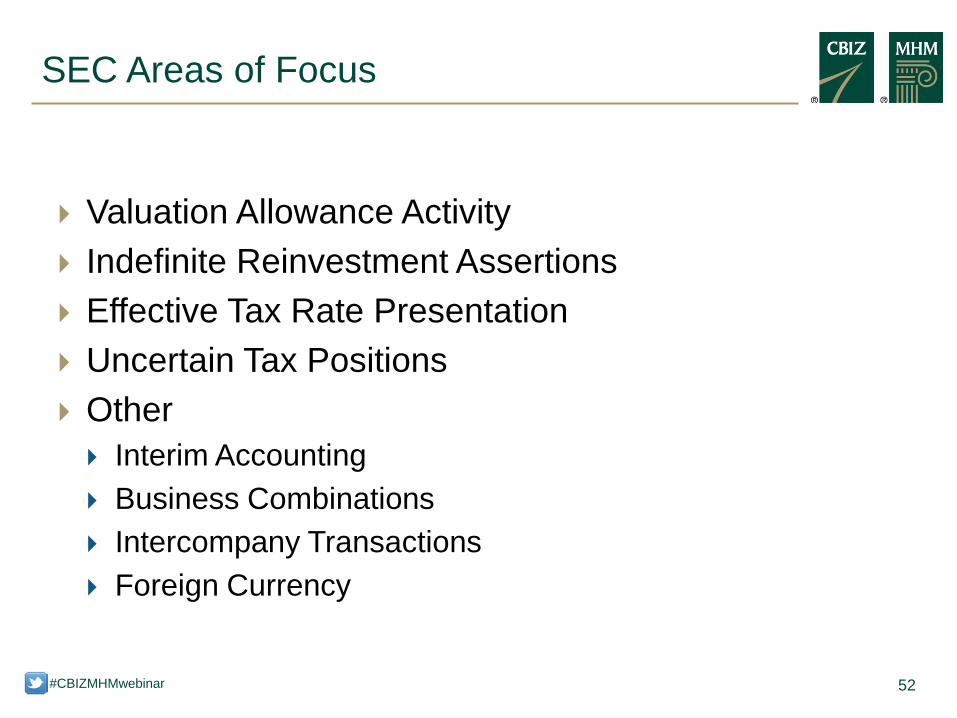

SEC Areas of Focus

Valuation Allowance Activity Indefinite Reinvestment Assertions Effective Tax Rate Presentation Uncertain Tax Positions Other Interim Accounting Business Combinations Intercompany Transactions Foreign Currency

53 #CBIZMHMwebinar

Questions?

54 #CBIZMHMwebinar

Join us for these courses: 6/30 & 7/7: Second Quarter Accounting and Financial Reporting

Update 7/8: How DOL Enforcement and Recent Litigation is Impacting Your

Employee Benefit Plan 7/9 & 7/23: Unclaimed Property - What You Don't Know Can Hurt You 7/30, 8/4 & 8/5: Eye on Washington: Quarterly Business Tax Update,

Q2 2015

Read this related publication: SEC Cracking Down on Internal Whistleblower Policies

If You Enjoyed This Webinar…

55 #CBIZMHMwebinar

Connect with Us

linkedin.com/company/ mayer-hoffman-mccann-p.c.

@mhm_pc

youtube.com/ mayerhoffmanmccann

slideshare.net/mhmpc

linkedin.com/company/ cbiz-mhm-llc

@cbizmhm

youtube.com/user/BizTipsVideos

slideshare.net/CBIZInc

MHM CBIZ