Webinar Slides: How DOL Enforcement and Recent Litigation is Impacting Your Employee Benefit Plan

93

CBIZ & MHM Executive Education Series™ Recent DOL Enforcement Actions Presented by: Melanie Hancock, Mary Snyder and Jenny Matasic June 10, 2015

-

Upload

mayer-hoffman-mccann-pc -

Category

Economy & Finance

-

view

106 -

download

0

Transcript of Webinar Slides: How DOL Enforcement and Recent Litigation is Impacting Your Employee Benefit Plan

CBIZ & MHM Executive Education Series™ Recent DOL Enforcement Actions

Presented by: Melanie Hancock, Mary Snyder and Jenny Matasic

June 10, 2015

2 #CBIZMHMwebinar Co-presented by:

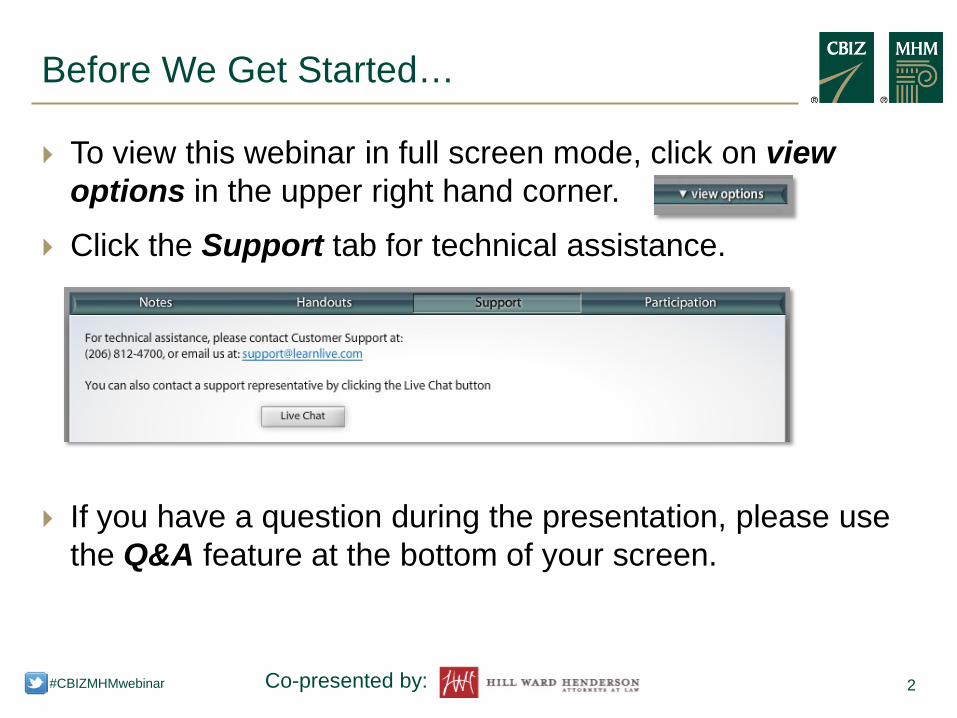

To view this webinar in full screen mode, click on view options in the upper right hand corner.

Click the Support tab for technical assistance.

If you have a question during the presentation, please use the Q&A feature at the bottom of your screen.

Before We Get Started…

3 #CBIZMHMwebinar Co-presented by:

This webinar is eligible for CPE credit. To receive credit, you will need to answer periodic participation markers throughout the webinar.

External participants will receive their CPE certificate via email immediately following the webinar.

CPE Credit

4 #CBIZMHMwebinar Co-presented by:

The information in this Executive Education Series course is a brief summary and may not include all

the details relevant to your situation.

Please contact your service provider to further discuss the impact on your business.

Disclaimer

5 #CBIZMHMwebinar Co-presented by:

Today’s Presenters

Jenny Matasic Senior Manager, CBIZ 727.572.1400 | [email protected] Jenny is a senior manager in our Tampa Bay office where she leads the employee benefit plan (EBP) audit practice. Prior to joining the company in 2004, she worked for a regional public accounting firm in the Washington, D.C. area for four years. She also serves in the company’s peer review and quality control activities.

Melanie J. Hancock Shareholder, Hill Ward Henderson 813.222.3138 | [email protected] Melanie is a Shareholder in Hill Ward Henderson’s Executive Compensation & Employee Benefits Group. She practices in the area of ERISA, employee benefits and executive compensation. Melanie counsels a diverse clientele of for-profit and nonprofit entities of all sizes regarding their qualified and nonqualified employee benefit plans, including 401(k) and profit sharing plans, defined benefit plans, ESOPs and other stock based benefits, and health, welfare and other fringe benefit plans.

6 #CBIZMHMwebinar Co-presented by:

Today’s Presenters

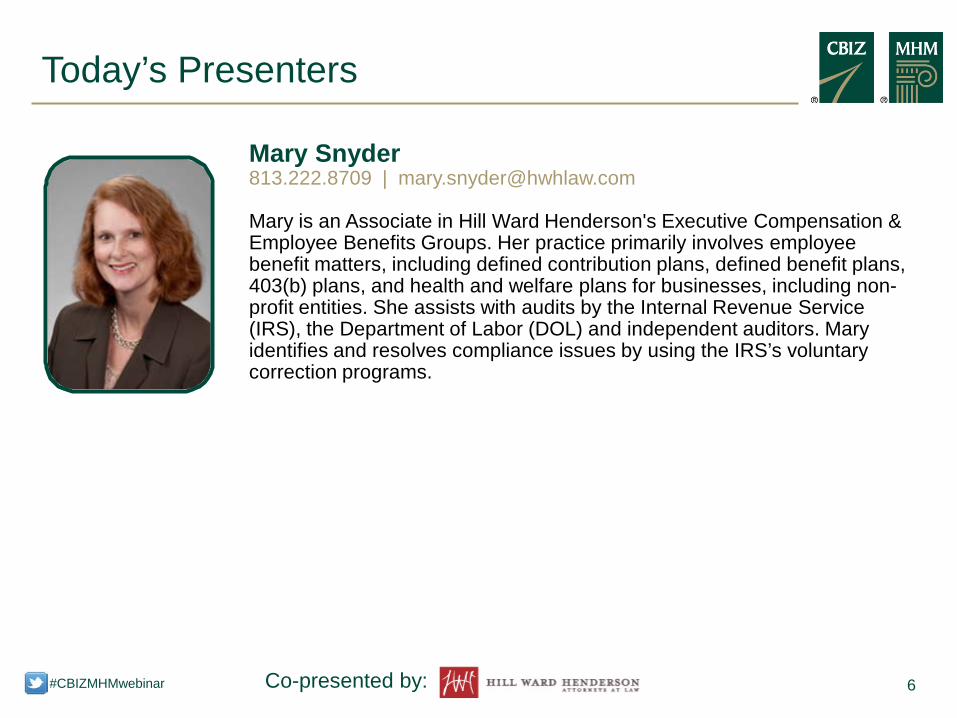

Mary Snyder 813.222.8709 | [email protected] Mary is an Associate in Hill Ward Henderson's Executive Compensation & Employee Benefits Groups. Her practice primarily involves employee benefit matters, including defined contribution plans, defined benefit plans, 403(b) plans, and health and welfare plans for businesses, including non-profit entities. She assists with audits by the Internal Revenue Service (IRS), the Department of Labor (DOL) and independent auditors. Mary identifies and resolves compliance issues by using the IRS’s voluntary correction programs.

7 #CBIZMHMwebinar Co-presented by:

Today’s Agenda

1

2

ERISA and fiduciary duties

DOL enforcement and recent litigation involving plan sponsors

Audit quality study conducted by the DOL 3

4 Questions

ERISA AND FIDUCIARY DUTIES

9 #CBIZMHMwebinar Co-presented by:

The Employee Retirement Income Security Act (ERISA) is a federal law that governs both qualified retirement plans (pension, profit sharing, and 401(k) plans) and health and welfare benefit plans (e.g., group life, health, dental, and disability insurance plans and other fringe benefit plans).

ERISA is enforced primarily by the Department of Labor (DOL).

ERISA: What is it?

10 #CBIZMHMwebinar Co-presented by:

ERISA is designed to protect the benefits and rights of participants and their beneficiaries.

To do that, ERISA imposes duties upon plan “fiduciaries” High standard of behavior Fiduciaries who breach their duties can be personally liable

for damages to the plan and for Internal Revenue Code and ERISA penalties

ERISA: What does it require?

11 #CBIZMHMwebinar Co-presented by:

A person (or entity) is a fiduciary with respect to a plan if he or she Is a named fiduciary under the plan (e.g., plan administrator,

administrative and investment committees, trustee); Exercises any discretionary authority or discretionary control

with respect to the management of the plan; Has any discretionary authority or discretionary responsibility

in the administration of such plan; Exercises any authority or control respecting management or

disposition of a plan’s assets; OR Renders investment advice for a fee or other compensation,

direct or indirect, with respect to any money or other property of such plan, or has any authority or responsibility to do so.

Who is a Fiduciary?

12 #CBIZMHMwebinar Co-presented by:

The determination of who is an ERISA fiduciary is generally based on the function that the individual or entity is performing.

Except for named fiduciaries whose roles automatically convey a fiduciary function, a person’s title is not determinative.

Representations in a contract are also not necessarily controlling.

Discretion is not required to be a fiduciary if you have control of plan assets.

Who is a Fiduciary?

13 #CBIZMHMwebinar Co-presented by:

Certain roles are fiduciary in nature: Trustees Directed trustees (to a more limited extent) Plan sponsors Plan administrators To the extent they have fiduciary responsibility for the plan:

Investment advisors Investment managers Corporate officers Plan sponsor’s board of directors Plan committees

Who is a Fiduciary?

14 #CBIZMHMwebinar Co-presented by:

Who controls the plan’s money? Who are the plan’s investment managers and trustees? Who appoints the financial managers and trustees? Who makes decisions regarding the interpretation of the

plan? Who has the discretionary authority to determine plan

eligibility, or to approve or deny a claim?

Who is a Fiduciary?

15 #CBIZMHMwebinar Co-presented by:

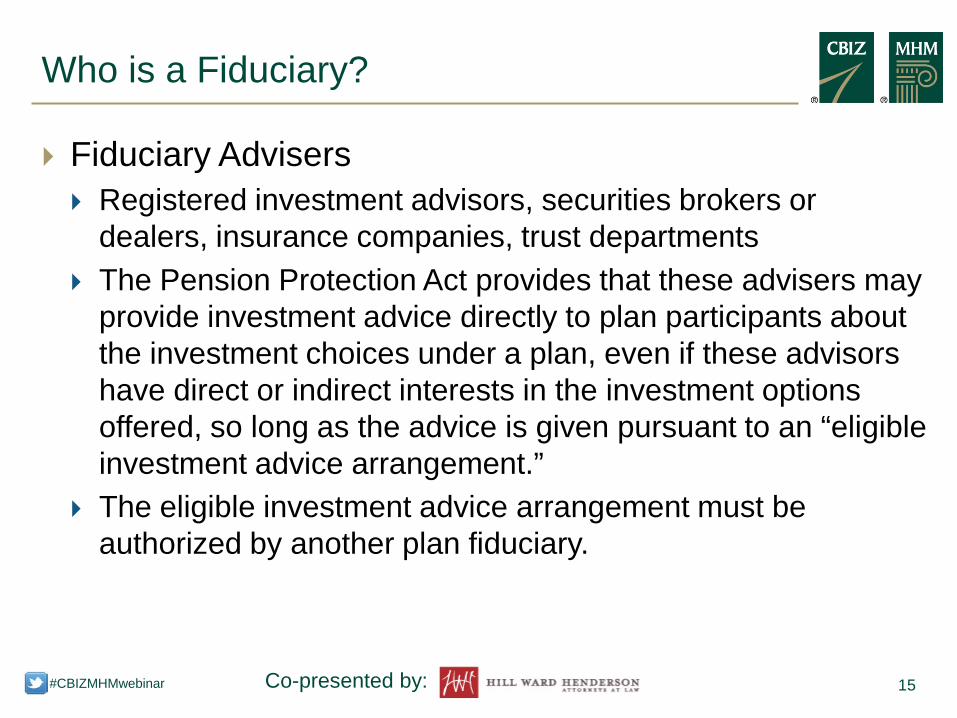

Fiduciary Advisers Registered investment advisors, securities brokers or

dealers, insurance companies, trust departments The Pension Protection Act provides that these advisers may

provide investment advice directly to plan participants about the investment choices under a plan, even if these advisors have direct or indirect interests in the investment options offered, so long as the advice is given pursuant to an “eligible investment advice arrangement.”

The eligible investment advice arrangement must be authorized by another plan fiduciary.

Who is a Fiduciary?

16 #CBIZMHMwebinar Co-presented by:

Guidelines for determining who is a fiduciary when providing investment advice to a retirement plan or a plan’s participants or beneficiaries

The DOL has proposed regulations and related exemptions that would expand the types of advice and recommendations given to a retirement plan or a plan's participants that may lead to ERISA fiduciary status.

DOL Proposed Fiduciary Regulations

17 #CBIZMHMwebinar Co-presented by:

Four types of advice regarding securities or other property could trigger fiduciary status when the advice is provided for a fee:

1) recommendations to invest, buy, sell, or hold, including recommendations to take a distribution of benefits and recommendations regarding investment of distributions or rollovers;

2) investment management recommendations; 3) verbal or written appraisals or fairness opinions provided in

connection with a specific transaction; and 4) recommendations of persons to provide investment advice

or manage plan assets for a fee.

DOL Proposed Fiduciary Regulations

18 #CBIZMHMwebinar Co-presented by:

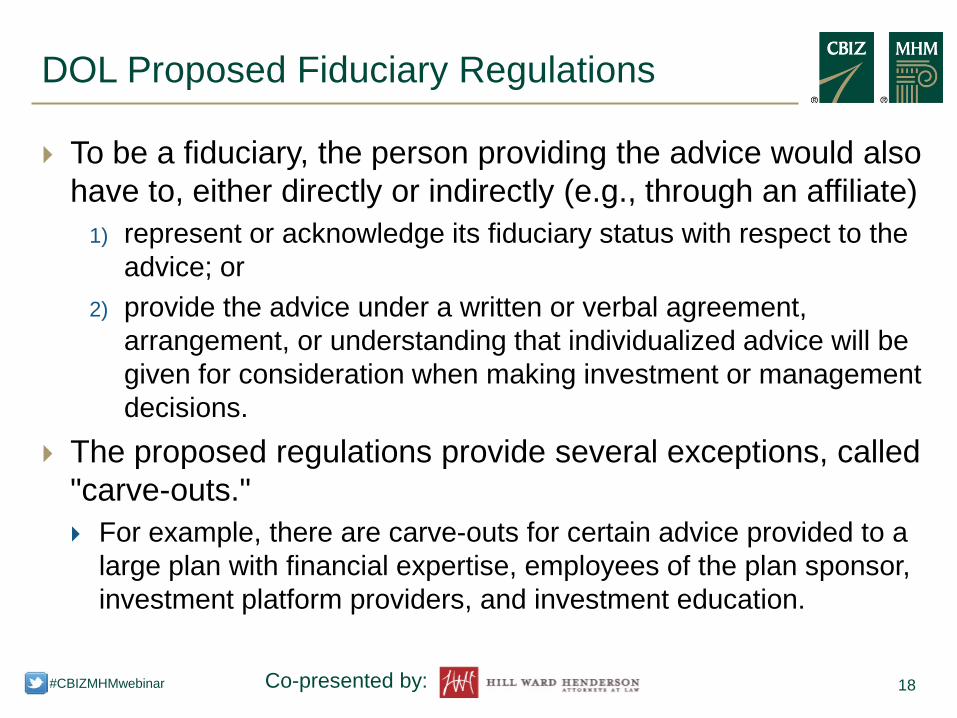

To be a fiduciary, the person providing the advice would also have to, either directly or indirectly (e.g., through an affiliate)

1) represent or acknowledge its fiduciary status with respect to the advice; or

2) provide the advice under a written or verbal agreement, arrangement, or understanding that individualized advice will be given for consideration when making investment or management decisions.

The proposed regulations provide several exceptions, called "carve-outs." For example, there are carve-outs for certain advice provided to a

large plan with financial expertise, employees of the plan sponsor, investment platform providers, and investment education.

DOL Proposed Fiduciary Regulations

19 #CBIZMHMwebinar Co-presented by:

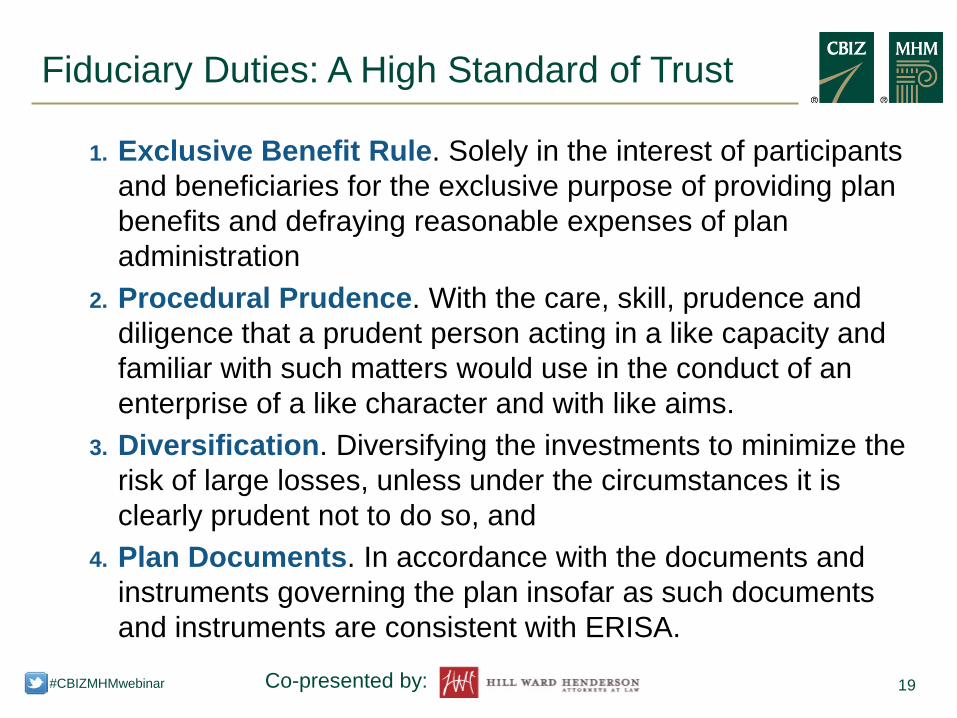

1. Exclusive Benefit Rule. Solely in the interest of participants and beneficiaries for the exclusive purpose of providing plan benefits and defraying reasonable expenses of plan administration

2. Procedural Prudence. With the care, skill, prudence and diligence that a prudent person acting in a like capacity and familiar with such matters would use in the conduct of an enterprise of a like character and with like aims.

3. Diversification. Diversifying the investments to minimize the risk of large losses, unless under the circumstances it is clearly prudent not to do so, and

4. Plan Documents. In accordance with the documents and instruments governing the plan insofar as such documents and instruments are consistent with ERISA.

Fiduciary Duties: A High Standard of Trust

20 #CBIZMHMwebinar Co-presented by:

A fiduciary must discharge all plan duties solely in the interests of plan participants for the exclusive purpose of providing benefits under the plan and defraying reasonable expenses of administering the plan.

Duty of loyalty Returning contributions to the employer may violate rule Plan-paid expenses must be reasonable

DOL’s participant-level fee disclosure regulations Participant communications must not be misleading and no

harmful silence Duty to disclose contemplated plan changes under “serious

consideration”

Fiduciary Duties: Exclusive Benefit Rule

21 #CBIZMHMwebinar Co-presented by:

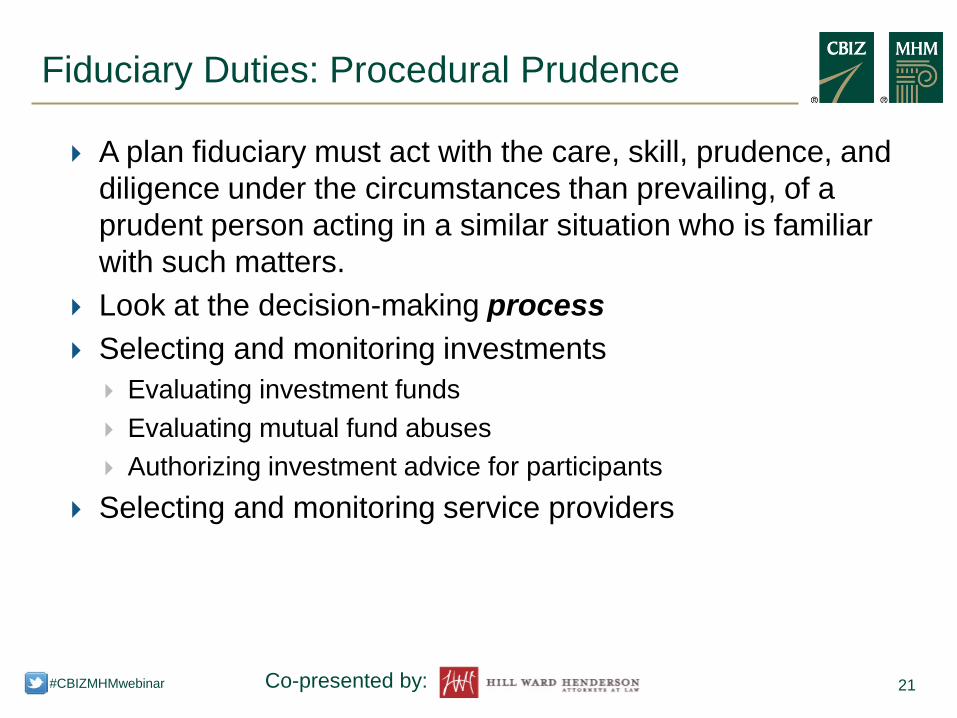

A plan fiduciary must act with the care, skill, prudence, and diligence under the circumstances than prevailing, of a prudent person acting in a similar situation who is familiar with such matters.

Look at the decision-making process Selecting and monitoring investments

Evaluating investment funds Evaluating mutual fund abuses Authorizing investment advice for participants

Selecting and monitoring service providers

Fiduciary Duties: Procedural Prudence

22 #CBIZMHMwebinar Co-presented by:

A plan fiduciary must diversify plan investments to minimize the risk of large losses unless it is clearly prudent not to do so. Evaluated at the time of purchase, rather than in hindsight

ESOPs may be an exception to the diversification rule. How to determine investments

Will participants get to choose? If so, what number and kinds of investments? If not, how will investment decisions be made and what principles will

guide those decisions? What about default investments?

Selecting plan investments is generally a fiduciary function.

Fiduciary Duties: Diversify Investments

23 #CBIZMHMwebinar Co-presented by:

Selecting the plan’s investment funds Gather and analyze information on several fund providers Gather and analyze information about fund asset classes, styles

and fees Consider the frequency of investment changes by participants

Monitor investment performance – facts and circumstances Use of investment advisors if the decision makers do not have

expertise Periodic review of funds, service providers, trustees, investment

managers, etc. Ongoing reassessment of the selected funds based upon industry

benchmarks Use of an investment policy

Fiduciary Duties: Diversify Investments

24 #CBIZMHMwebinar Co-presented by:

ERISA Sec 404(c) provides some protection from the risk associated with the participant’s investment choices.

Plan must satisfy specific plan design and disclosure requirements Plan fiduciaries retain responsibility for selecting and monitoring the

plan’s investment choices and for communicating with participants.

Fiduciary Duties: Diversify Investments

25 #CBIZMHMwebinar Co-presented by:

A plan fiduciary must discharge its duties in accordance with the terms of the plan documents to the extent that they are consistent with law.

A plan fiduciary must carry out its duties in the law Reporting obligations Disclosure obligations

Fiduciary Duties: Follow the Plan’s Terms

26 #CBIZMHMwebinar Co-presented by:

Establish a trust for plan assets Except insurance contracts or policies

Late deposits of participant contributions and loan repayments are a violation of the trust requirement

Fiduciary Duties: Trust

27 #CBIZMHMwebinar Co-presented by:

Provide a fidelity bond that covers all persons who handle plan funds Purpose is to protect plans against loss due to fraud or dishonesty

by plan officials Amount is fixed at the beginning of the year

At least 10% of the highest amount of funds the plan official handled in the preceding plan year.

Minimum is $1,000 Maximum is $500,000 for plans not holding employer securities or

$1million for plans with employer securities

Fiduciary Duties: Fidelity Bond

28 #CBIZMHMwebinar Co-presented by:

Adhere to a code of conduct that prohibits self-dealing, conflicts of interest, and other “prohibited transactions”

Both ERISA and the Code prohibit certain listed transactions, unless a statutory or administrative exemption applies to permit the transaction.

The “prohibited transaction” rules prohibit fiduciaries from entering into transactions with parties that have a significant relationship with the plan. ERISA uses the term “parties in interest” Code uses the term “disqualified persons” Similar, but not identical

Fiduciary Duties: No Self-Dealing

29 #CBIZMHMwebinar Co-presented by:

Plan fiduciaries Persons providing services to the plan Employer sponsoring the Plan An employee organization whose members are covered by

the Plan Employees, officers, directors, or 10% or more owners of the

employer sponsoring the plan (Code definition of “disqualified person” does not include employees)

Relatives or 10% or more owners of any other party in interest

Prohibited Transactions: Party in Interest

30 #CBIZMHMwebinar Co-presented by:

Transactions between a plan and party in interest Sale, exchange or leasing of any property between plan & PII Lending of money or other extensions of credit between plan & PII Furnishing of good, services, or facilities between plan & PII Transfer to, or use by or for the benefit of, a PII of any assets of the

plan; or Acquisition on behalf of a plan of any employer security or real

property in violation of ERISA Sec. 407(a)

Prohibited Transactions

31 #CBIZMHMwebinar Co-presented by:

Fiduciary Self-Dealing No self-dealing. Dealing with assets of the plan in the fiduciary’s

own interest or account No conflicts of interest. Acting in any plan transaction involving the

plan on behalf of a party whose interests are adverse to those of the plan or the interests of its participants or beneficiaries

No kickbacks. Receiving any consideration for the fiduciary’s account from any party dealing with such plan in connection with a transaction involving the assets of the plan

Prohibited Transactions

32 #CBIZMHMwebinar Co-presented by:

Plan Transactions and DOL Opinions Trustee Retaining Short-Term Earnings or “Float” If the trustee exercises discretion to keep the float, it could be a

prohibited transaction May be openly negotiated and fully disclosed as part of its fees

12-b1 fees are allowed under certain circumstances Excise taxes on prohibited transactions

In addition to the potential breach of fiduciary duty claim, the IRS may assess an excise tax penalty against a party in interest (a disqualified person under the Code)

DOL is required to advise the IRS of any prohibited transactions of which it becomes aware

Prohibited Transactions

33 #CBIZMHMwebinar Co-presented by:

Statutory Exemptions Necessary services for the establishment or operation of the plan If the contract is reasonable and no more than reasonable compensation

is paid Fiduciary-level service provider fee disclosures

Party in interest in a fiduciary capacity must be careful not to use its authority, control or responsibility to cause a plan to pay the fiduciary

Participant Loans – technically is a loan from the plan to a party in interest Provided that the

Investment Advice in Self-Directed Plans Administrative Exemptions

Class exemption that provides certain guidelines to follow

Prohibited Transactions Exemptions

34 #CBIZMHMwebinar Co-presented by:

Personal Liability For any losses to the plan resulting from the breach Restoring to the plan any profits that the fiduciary made through

using any plan asset Multiple fiduciaries have joint and several liability

Excise Tax for prohibited transaction from IRS Civil Penalty from DOL equal to 20% of the amount

recovered by the DOL, reduced by the amount of any excise tax paid

ERISA specifically grants the right to sue a fiduciary (and nonfiduciary parties in interest) that cause a plan to enter into a prohibited transaction with a party in interest.

Potential criminal liability for embezzlement, conversion, etc.

Consequences of Breach of Fiduciary Duty

35 #CBIZMHMwebinar Co-presented by:

A civil action may be brought by participants, beneficiaries, plan fiduciaries or the DOL against a fiduciary for breach of its fiduciary duties. ERISA does not provide a remedy for individual injuries distinct from

plan injuries, it does authorize recovery for fiduciary breaches that impair the value of plan assets in a participant’s individual account. Thus, individuals can bring breach claims so long as the relief sought is

for the plan, even if it is not for the entire plan. For individual relief for fiduciary breaches, participants, beneficiaries

and fiduciaries can seek either to enjoin an act or practice that violates ERISA or the terms of the plan, or to obtain other appropriate equitable relief.

Claims for Breach of Fiduciary Duty

36 #CBIZMHMwebinar Co-presented by:

A plan fiduciary is liable for a breach of fiduciary duty of another plan fiduciary if the first fiduciary. Knowingly participates in or undertakes to conceal an act or

omission of the other fiduciary, aware that such act or omission is a breach

Through neglect of duties, enables the other fiduciary to commit a breach, OR

Has knowledge of a breach of fiduciary duty by the other fiduciary and does not make reasonable efforts under the circumstances to remedy the breach

Co-Fiduciary Liability

37 #CBIZMHMwebinar Co-presented by:

Understand your fiduciary obligations Document all steps taken Follow plan terms, as long as they are consistent with ERISA Employer, not the plan, can indemnify plan fiduciaries

Limiting Fiduciary Liability

38 #CBIZMHMwebinar Co-presented by:

Delegation of some fiduciary duty to others The delegating fiduciary remains responsible for the prudent

selection and retention of the delegates. Must review performance of delegates Periodically review performance Review procedures for selection and retention Review participant comments and complaints about the services

DOL (and SEC) published tips on its website to help plan fiduciaries evaluate potential conflicts of interest of pension consultants and tips for selecting and monitoring other service providers.

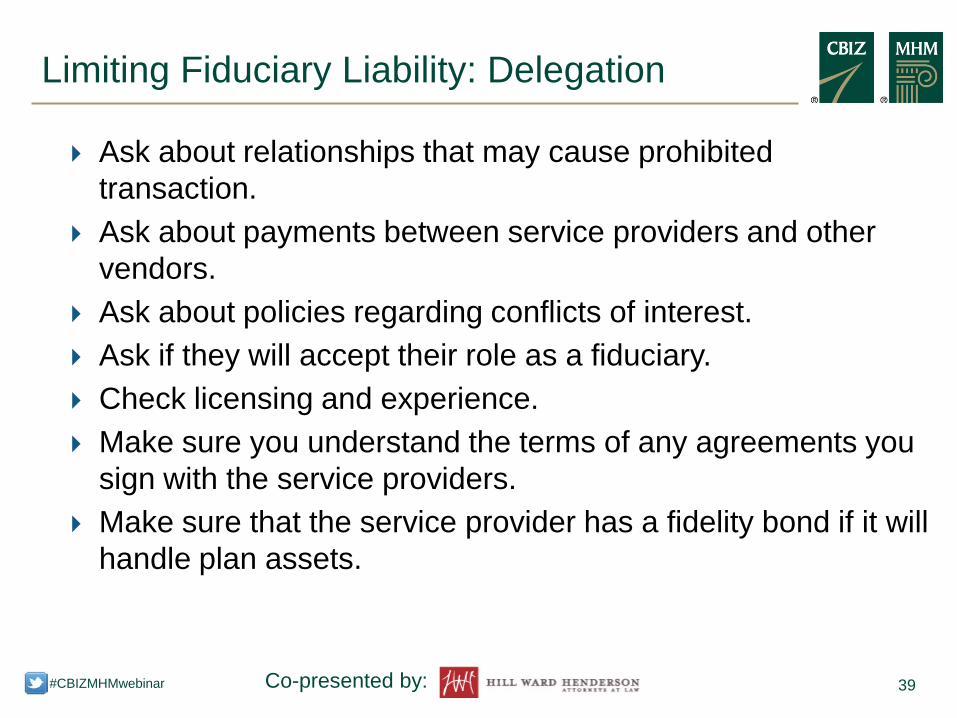

Limiting Fiduciary Liability: Delegation

39 #CBIZMHMwebinar Co-presented by:

Ask about relationships that may cause prohibited transaction.

Ask about payments between service providers and other vendors.

Ask about policies regarding conflicts of interest. Ask if they will accept their role as a fiduciary. Check licensing and experience. Make sure you understand the terms of any agreements you

sign with the service providers. Make sure that the service provider has a fidelity bond if it will

handle plan assets.

Limiting Fiduciary Liability: Delegation

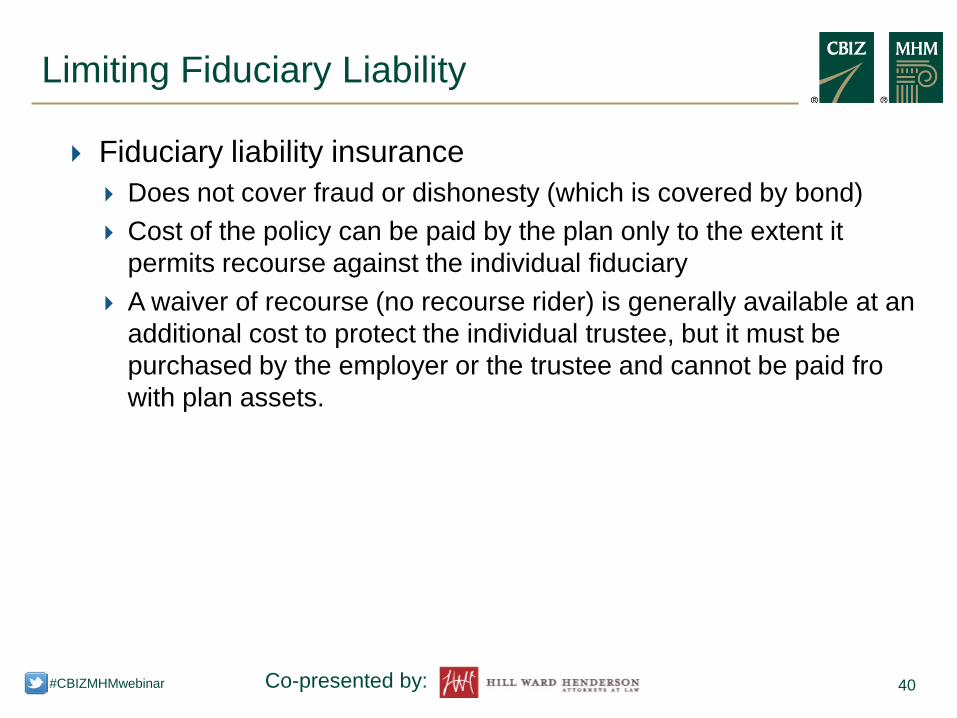

40 #CBIZMHMwebinar Co-presented by:

Fiduciary liability insurance Does not cover fraud or dishonesty (which is covered by bond) Cost of the policy can be paid by the plan only to the extent it

permits recourse against the individual fiduciary A waiver of recourse (no recourse rider) is generally available at an

additional cost to protect the individual trustee, but it must be purchased by the employer or the trustee and cannot be paid fro with plan assets.

Limiting Fiduciary Liability

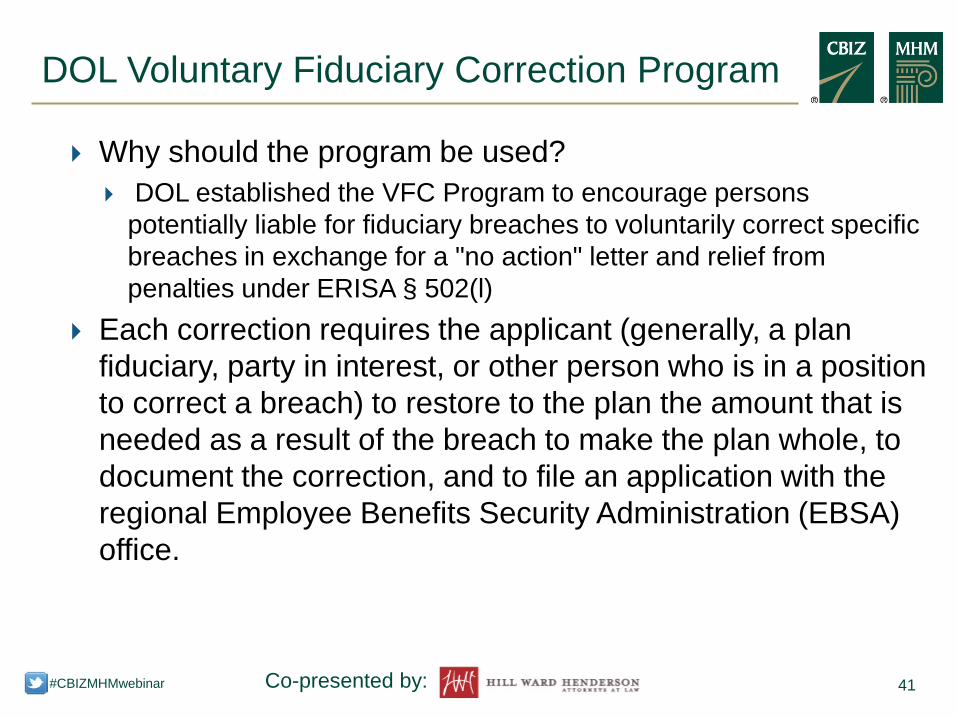

41 #CBIZMHMwebinar Co-presented by:

Why should the program be used? DOL established the VFC Program to encourage persons

potentially liable for fiduciary breaches to voluntarily correct specific breaches in exchange for a "no action" letter and relief from penalties under ERISA § 502(l)

Each correction requires the applicant (generally, a plan fiduciary, party in interest, or other person who is in a position to correct a breach) to restore to the plan the amount that is needed as a result of the breach to make the plan whole, to document the correction, and to file an application with the regional Employee Benefits Security Administration (EBSA) office.

DOL Voluntary Fiduciary Correction Program

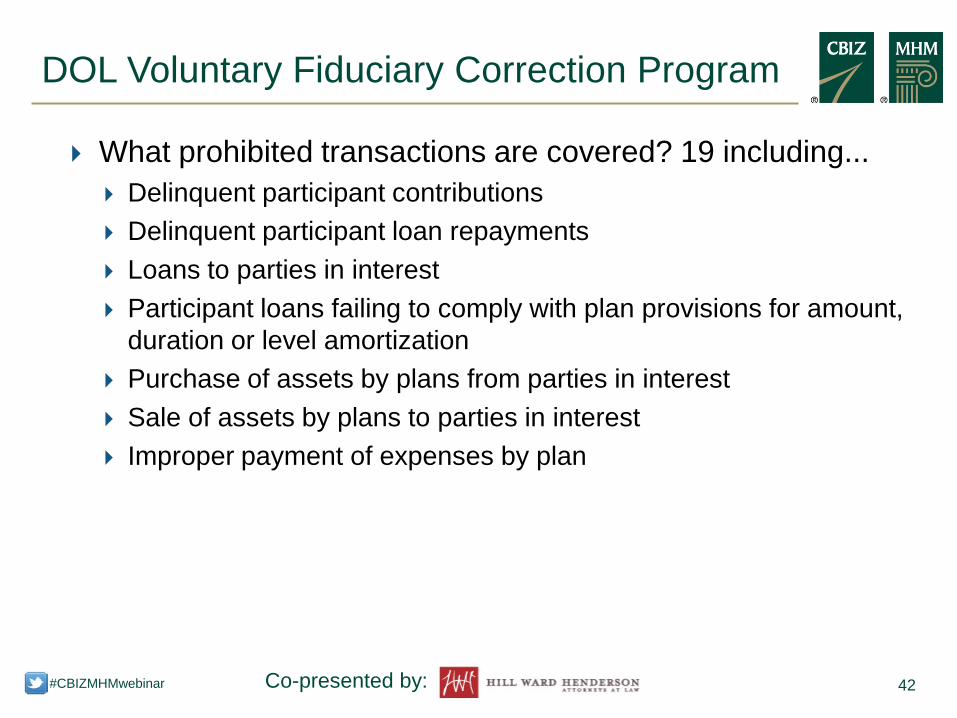

42 #CBIZMHMwebinar Co-presented by:

What prohibited transactions are covered? 19 including... Delinquent participant contributions Delinquent participant loan repayments Loans to parties in interest Participant loans failing to comply with plan provisions for amount,

duration or level amortization Purchase of assets by plans from parties in interest Sale of assets by plans to parties in interest Improper payment of expenses by plan

DOL Voluntary Fiduciary Correction Program

43 #CBIZMHMwebinar Co-presented by:

The DOL issued a prohibited transaction exemption (PTE) that offers relief from excise taxes under Code §4975 for some, but not all, of the transactions that are eligible for the VFC Program.

For more information: www.dol.gov/ebsa/newsroom/fs2006vfcp.html

DOL Voluntary Fiduciary Correction Program

DOL ENFORCEMENT AND RECENT LITIGATION INVOLVING

PLAN SPONSORS

45 #CBIZMHMwebinar Co-presented by:

Disclaimer DOL Enforcement Actions Results of DOL Investigations in 2015 Recent Large Settlements with the DOL Recent Court Cases Regarding Fiduciary Duty

Other Consequences of Prohibited Transactions or Fiduciary Breaches

Fiduciary Best Practices

Introduction

46 #CBIZMHMwebinar Co-presented by:

How does the DOL decide who to investigate? Random selection and initiatives Form 5500 Participant complaints Court cases News media Potential referrals from PBGC or IRS

DOL Investigations in 2015

47 #CBIZMHMwebinar Co-presented by:

35 investigations by DOL for retirement plans in 2015: 15 involved failure of plan administrator to timely deposit

elective deferrals and loan repayments 12 involved improper administration of abandoned plans 5 involved excessive fees 3 involved breaches of fiduciary duty

2 involved prohibited transactions

DOL Enforcement Actions in 2015

48 #CBIZMHMwebinar Co-presented by:

Recent large settlements as a result of DOL investigations

In 2015 - $4 million settlement with City National Bank

In 2014 - $5.25 million settlement with GreatBanc Trust

Co.

In 2013 - $80 million settlement with Sherwin-Williams Co.

DOL Enforcement Actions in 2015

49 #CBIZMHMwebinar Co-presented by:

Lessons to learn Top concern - late deposit of elective deferrals and

loan repayments Periodically review both service provider fees and

investment charges Identify plan fiduciaries and parties-in-interest

DOL Enforcement Actions in 2015

50 #CBIZMHMwebinar Co-presented by:

Lessons to learn (con’t) Mergers, acquisitions, or dissolutions Proper valuation of employer stock Small plans are not under the radar

DOL Enforcement Actions in 2015

51 #CBIZMHMwebinar Co-presented by:

Continuing Duty to Monitor Investments Tibble et. al. v. Edison International et. al. (Supreme Court, May 18, 2015) Participants allege that the plan and its executives breached their fiduciary duties by choosing certain retail-priced investments over less-expensive institutionally priced versions of the same investments. Three of the original investments were added to the Plan in 1999, another three were added in 2002. However, suit was not filed until 2007. The lower court found a breach of the duty of prudence with respect to the 2002 funds, but Edison argued that the 6-year statute of limitation for claiming a breach had expired and that circumstances had not changed sufficiently in the 6 years to warrant a review of the funds. The lower court agreed. On appeal the Supreme Court found that fiduciaries have a continuing duty to monitor investments and remove imprudent ones. Remanded case for consideration of whether duty to monitor was raised by participants, and if so, breached within 6 year period.

Recent Court Cases Regarding Fiduciary Duty

52 #CBIZMHMwebinar Co-presented by:

Lessons to learn from court cases Develop a Investment Policy Statement Consider an investment committee Document all actions taken

Recent Court Cases Regarding Fiduciary Duty

53 #CBIZMHMwebinar Co-presented by:

Stock Drop Cases and Reverse Stock Drop Cases Many lower cases dismissed for failure to state a claim

Fifth Third Bancorp et. al v. Dudenhoeffer et al. (Supreme Court, June 25, 2014) Participants allege that the plan and its officers breached their fiduciary duties of loyalty and prudence by maintaining company stock in the plan even though the stock was overpriced and risky based on both public information and insider information. Participants alleged that the fiduciaries should have sold stock, stopped buying stock, and disclosed the negative insider information to allow the market price to adjust. Lower court found that ESOP fiduciaries have a special presumption of prudence (“Moench”) that can only be overcome by a showing that the company is on the brink of collapse. The Supreme Court found no special presumption of prudence, although there is no duty to diversify investments. However, Court found that fiduciary duties under ERISA do not require a fiduciary to violate other federal laws, such as securities laws.

Recent Court Cases Regarding Fiduciary Duty

54 #CBIZMHMwebinar Co-presented by:

Stock Drop Cases and Reverse Stock Drop Cases (con’t)

Tatum v. RJR Pension Investment Committee et al. (4th Cir., Aug. 4, 2014) Participants allege that the retirement plan lost $50 million when Nabisco stock was elimination as an investment option. The Circuit court found that fiduciaries must (1) employ appropriate methods to investigate the merits of a particular investment; (2) engage in reasoned decision-making processes consistent with that of a prudent man acting in a like capacity; and (3) monitor the prudence of an investment decision to ensure that it remains in the best interest of plan participants. Defendants bore the burden of proof as to whether, despite their breach, their ultimate investment decision was objectively prudent. Appealed to U.S. Supreme Court.

Recent Court Cases Regarding Fiduciary Duty

55 #CBIZMHMwebinar Co-presented by:

Lessons to learn from court cases Cannot avoid fiduciary liability through plan language

Tread carefully

Non-publicly traded stock - independent appraisal Prudent procedures

Recent Court Cases Regarding Fiduciary Duty

56 #CBIZMHMwebinar Co-presented by:

Duty of Prudence – Excessive Fees Tussey et. al v. ABB, Inc. (8th Cir. March 19, 2014) The participants allege that ABB, the investment committee, the benefits committee, and a director breached their fiduciary duty of prudence by paying excessive revenue sharing fees and mapping investments from one fund to another absent an investment election. The Circuit court agreed that a fiduciary's decisions must be given deference if the plan gives the fiduciary discretionary authority. However, the Circuit Court upheld the lower court's ordered that ABB pay $13.4 million for the fiduciaries failure to (1) calculate the amount the plan was paying Fidelity for recordkeeping through revenue sharing, (2) determine whether Fidelity’s pricing was competitive, (3) adequately leverage the Plan’s size to reduce fees, and (4) “make a good faith effort to prevent the subsidization of administration costs of ABB corporate services” with plan assets, even after ABB’s own outside consultant notified ABB that the plan was overpaying for recordkeeping and might be subsidizing ABB’s other corporate services. However, the Circuit court vacated the order for ABB to pay $21.8 million for its decision to remove the Wellington Fund and add the Fidelity Freedom Funds to the plan’s investment options, and to map investments in the former to the latter absent another investment election. US Supreme Court denied cert.

Recent Court Cases Regarding Fiduciary Duty

57 #CBIZMHMwebinar Co-presented by:

Duty of Prudence – Excessive Fees Abbott et al v. Lockheed Martin Corp et al. (February 2015, U.S. District Court, Southern District of Illinois). The participants allege that the fiduciaries to the Lockheed Martin 401(k) plans cause the plans to pay excessive administrative fees and that the fiduciaries had imprudently managed the money market fund and company stock fund. Further, they allege that Lockheed allowed an unreasonably high level of participants’ retirement assets to be held in low-yielding money market funds of State Street Bank & Trust, with whom Lockheed had multiple business relationships. Finally, the participants allege that they were charged excessive recordkeeping fees. After years of litigation, Lockheed has not admitted breaches, but has agreed to pay $62 million into the plan and implement extensive affirmative relief.

Recent Court Cases Regarding Fiduciary Duty

58 #CBIZMHMwebinar Co-presented by:

Lessons to learn from court cases

Discretionary fiduciary authority in plan document Review service agreements and fees

Cannot pay for other benefits

DOL regulations regarding fee disclosures

Diversify

Recent Court Cases Regarding Fiduciary Duty

59 #CBIZMHMwebinar Co-presented by:

Misc. cases of note Grabek et al v. Northrop Grumman. (fall 2014) DOL granted permission to intervene in an excessive investment and administrative fees case brought by participants in a 401(k) plan that invested in mutual funds and company stock.

Thomas v. CIGNA Group Ins. (E.D.N.Y. 2015) The court found that the posting a SPD with respect to life insurance benefits on the company’s intranet did not satisfy the electronic disclosure rules under ERISA. A SPD is considered properly distributed only if the communication satisfies DOL Regulations. The court held that posting on an Intranet without additional action does not satisfy the distribution requirements.

Recent Court Cases Regarding Fiduciary Duty

60 #CBIZMHMwebinar Co-presented by:

Lessons to learn from court cases

Separate DOL investigation DOL electronic notice requirements

Recent Court Cases Regarding Fiduciary Duty

61 #CBIZMHMwebinar Co-presented by:

Fiduciary is personally liable to the plan Prohibited transactions Civil penalties - 5% of amount involved No corrective action, 100% of the amount involved Offset by IRS excise taxes

Fiduciary breaches Mandatory penalty - 20% of amount recovered

Other Consequences of a Prohibited Transaction or a Fiduciary Breach

62 #CBIZMHMwebinar Co-presented by:

Prohibited transactions Investment selection and monitoring Excessive fees Overvaluation of employer stock sold to ESOPs

Summary of the Major Themes of DOL Investigations

63 #CBIZMHMwebinar Co-presented by:

Plan Documents

Fiduciary Training

Fidelity Bonds

Investment Policy Statement

Valuation of Employer Securities

Best Fiduciary Practices

64 #CBIZMHMwebinar Co-presented by:

Internal Audits Review Service Provides Agreements

Understand and Negotiate Fees

Required Participant Disclosures

Best Fiduciary Practices

AUDIT QUALITY STUDY

66 #CBIZMHMwebinar Co-presented by:

Department of Labor’s Audit Quality Study Background Summary of Findings Conclusion Population Detail of Findings Recommendations

Impact on Plan Sponsors

Overview

67 #CBIZMHMwebinar Co-presented by:

The Employee Benefits Security Administration (EBSA) which is part of the DOL conducted a review to assess the level and quality of audit work performed by independent qualified public accountants (IPQAs).

Determine if audit quality had improved since last study

Assess effectiveness of the DOL

Background

68 #CBIZMHMwebinar Co-presented by:

61% of audits fully complied with auditing standards or had only minor deficiencies.

Remaining 39% of audits contained major deficiencies which would lead to a rejection of the Form 5500 filing.

CPA firms performing few audits had a 76% deficiency rate.

CPA firms performing the most audits had a 12% deficiency rate.

17% of audit reports failed to comply with one or more of ERISA’s reporting and disclosure requirements.

Summary of Findings

69 #CBIZMHMwebinar Co-presented by:

Quality of EBP audits has not improved from previous studies (most recent in 2004).

The smaller the number of EBP audits performed, the greater the number of deficiencies.

Areas of deficiency were unique to EBP audits. The peer review process established and administered by

the AICPA and state society boards doesn’t appear to be an effective tool for ensuring quality EBP audits.

Employee Benefit Plan Audit Quality Center (EBPAQC) members tend to have fewer audits containing numerous deficiencies.

Conclusion

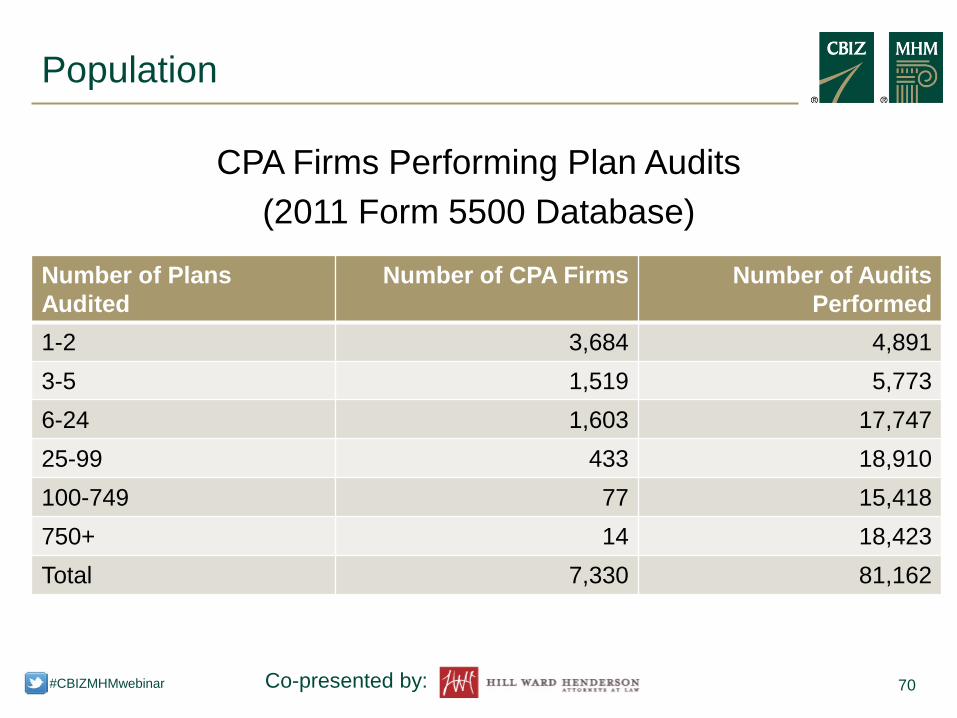

70 #CBIZMHMwebinar Co-presented by:

Column Heading Column Heading Column Heading Item 1 Item 2 Item 3 Item 4 Item 5 Item 6

Population

CPA Firms Performing Plan Audits (2011 Form 5500 Database)

Number of Plans Audited

Number of CPA Firms Number of Audits Performed

1-2 3,684 4,891 3-5 1,519 5,773 6-24 1,603 17,747 25-99 433 18,910 100-749 77 15,418 750+ 14 18,423 Total 7,330 81,162

71 #CBIZMHMwebinar Co-presented by:

Designed a statistical sample to ensure large and small CPA firms were included

6 strata were created based on number of audits performed by CPA firms

Selected 400 audits from the 2011 Form 5500 filings performed by 232 CPA firms

Sample included: Limited scope (81%) and full scope (19%) Defined contribution (89%), defined benefit (6%) and welfare (5%)

plans Single (95%), multi (3%) and multiple (2%) employers

Population

72 #CBIZMHMwebinar Co-presented by:

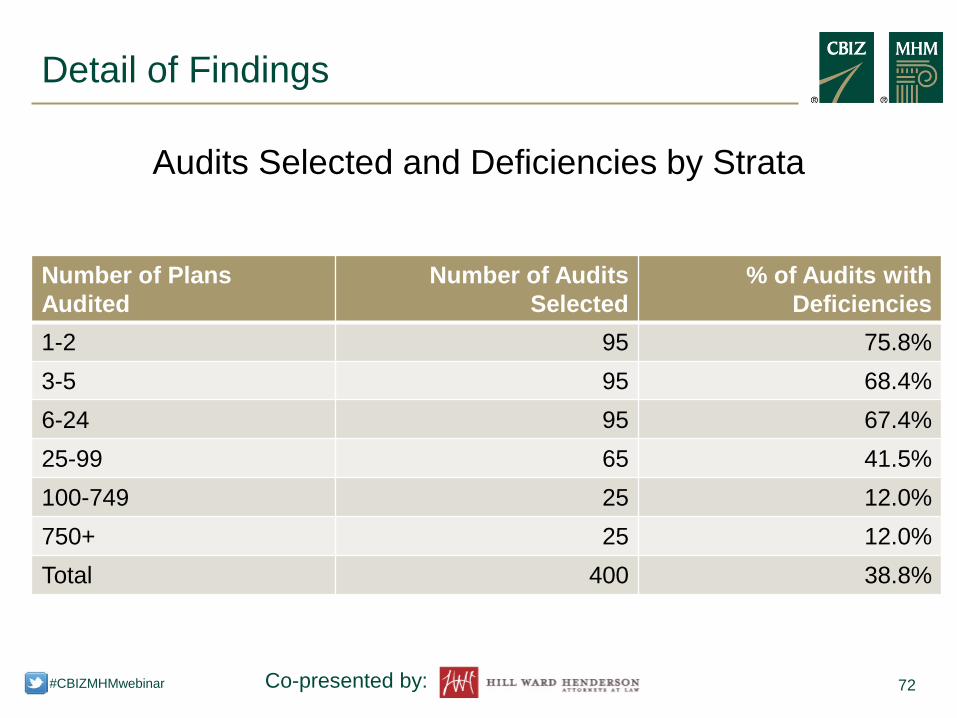

Column Heading Column Heading Column Heading Item 1 Item 2 Item 3 Item 4 Item 5 Item 6

Detail of Findings

Audits Selected and Deficiencies by Strata

Number of Plans Audited

Number of Audits Selected

% of Audits with Deficiencies

1-2 95 75.8% 3-5 95 68.4% 6-24 95 67.4% 25-99 65 41.5% 100-749 25 12.0% 750+ 25 12.0% Total 400 38.8%

73 #CBIZMHMwebinar Co-presented by:

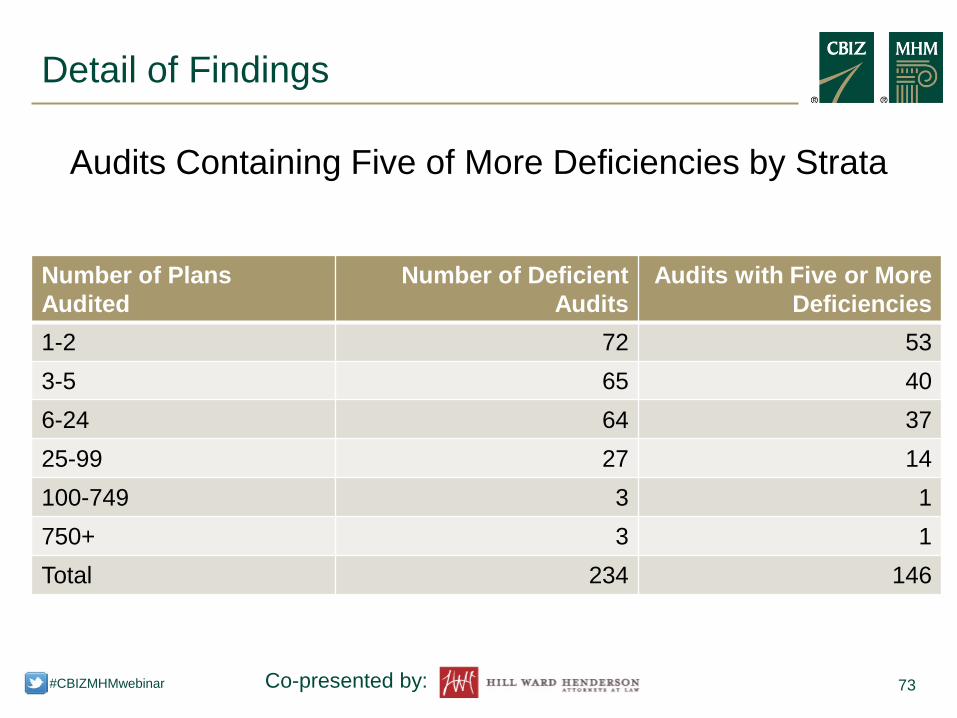

Column Heading Column Heading Column Heading Item 1 Item 2 Item 3 Item 4 Item 5 Item 6

Detail of Findings

Audits Containing Five of More Deficiencies by Strata

Number of Plans Audited

Number of Deficient Audits

Audits with Five or More Deficiencies

1-2 72 53 3-5 65 40 6-24 64 37 25-99 27 14 100-749 3 1 750+ 3 1 Total 234 146

74 #CBIZMHMwebinar Co-presented by:

The increase in non-compliant audits correlates to the increase in limited-scope audits.

The size of a CPA firm’s EBP practice correlates to audit quality.

“Specialized” CPA firms were less likely to have deficiencies. Specialized = 20% or more of revenues are from EBP audits.

A number of CPA firms with deficient audits had received a “clean” peer review report.

In the lowest stratum (1-2 audits performed), 52% of deficient audits had a “clean” peer review report.

Detail of Findings

75 #CBIZMHMwebinar Co-presented by:

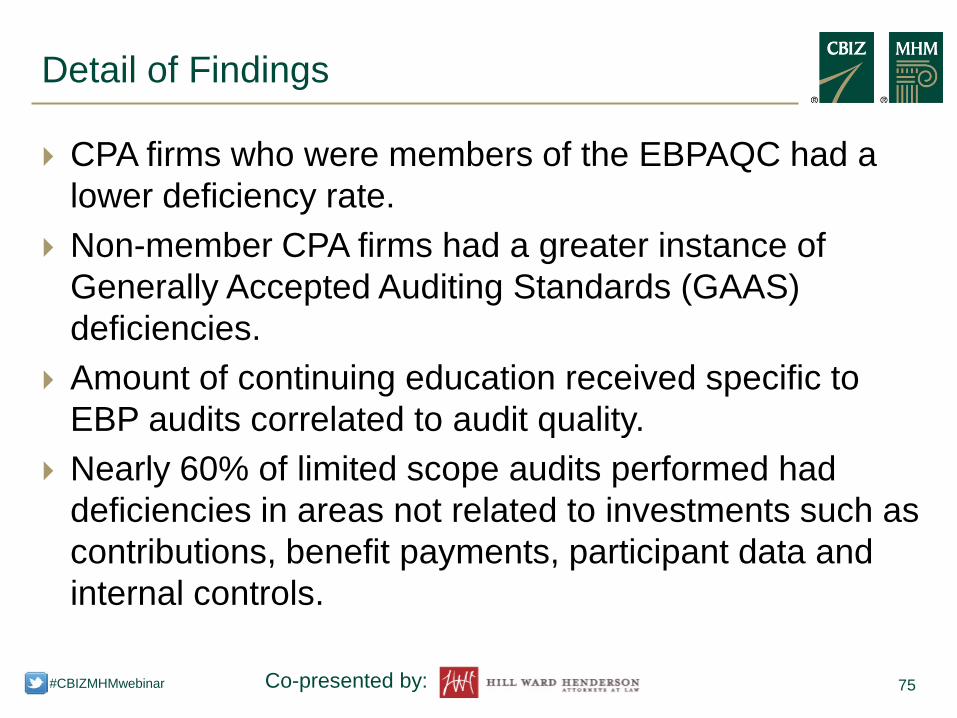

CPA firms who were members of the EBPAQC had a lower deficiency rate.

Non-member CPA firms had a greater instance of Generally Accepted Auditing Standards (GAAS) deficiencies.

Amount of continuing education received specific to EBP audits correlated to audit quality.

Nearly 60% of limited scope audits performed had deficiencies in areas not related to investments such as contributions, benefit payments, participant data and internal controls.

Detail of Findings

76 #CBIZMHMwebinar Co-presented by:

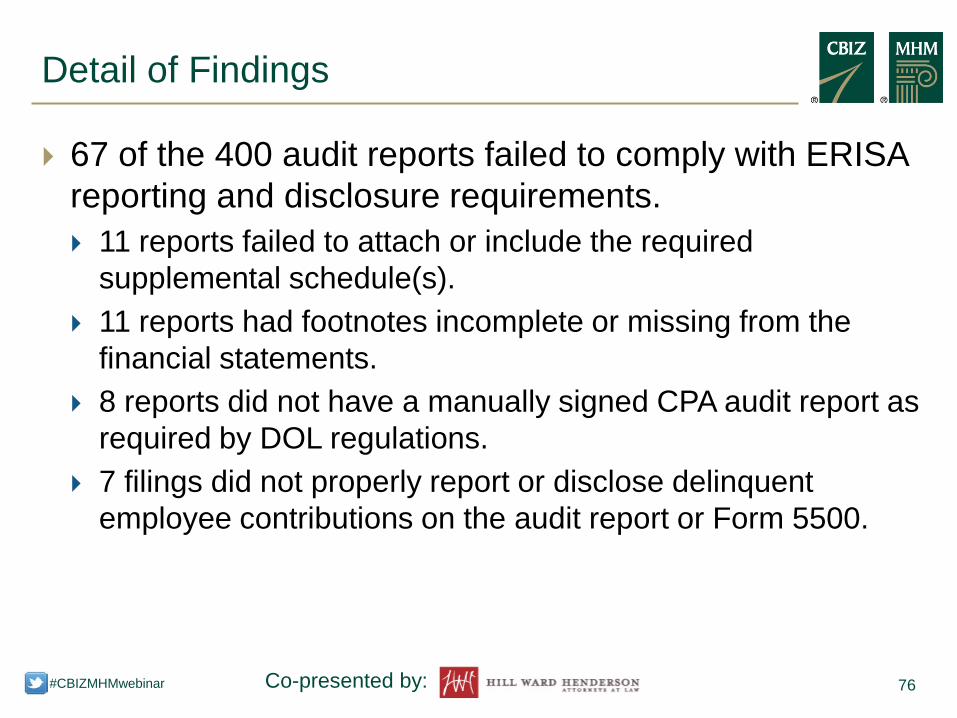

67 of the 400 audit reports failed to comply with ERISA reporting and disclosure requirements. 11 reports failed to attach or include the required

supplemental schedule(s). 11 reports had footnotes incomplete or missing from the

financial statements. 8 reports did not have a manually signed CPA audit report as

required by DOL regulations. 7 filings did not properly report or disclose delinquent

employee contributions on the audit report or Form 5500.

Detail of Findings

77 #CBIZMHMwebinar Co-presented by:

Enforcement Regulatory Outreach

Recommendations

78 #CBIZMHMwebinar Co-presented by:

Focus DOL efforts to target cases towards CPA firms with small EBP audit practices auditing plans with high dollars and CPA firms in the 25-99 plan stratum

Work with NASBA and AICPA to improve investigations and sanctions against CPA firms who perform significantly deficient audits

Amend ERISA to ensure civil penalties focus on the responsible party. The annual reporting penalty of $1,100 per day could potentially be assessed against the CPA firm if a plan’s annual report is rejected due to a deficient audit or if the CPA firm was not qualified to perform an ERISA plan audit.

Recommendations - Enforcement

79 #CBIZMHMwebinar Co-presented by:

Work with the AICPA Peer Review program to: Make the process more responsive in helping improve EBP

audit quality. Ensure CPAs subject to peer review are undergoing peer

review. Identify CPAs who have not received an acceptable peer

review and refer them to state licensing boards.

Recommendations - Enforcement

80 #CBIZMHMwebinar Co-presented by:

Amend the ERISA definition of qualified public accountant to include additional requirements and qualifications

Amend ERISA to repeal the limited scope exemption Amend ERISA to give the Secretary of Labor authority

to establish accounting principles and auditing standards to address reporting issues unique to EBPs

Recommendations - Regulatory

81 #CBIZMHMwebinar Co-presented by:

Work with NASBA to encourage state boards of accountancy to require specific licensing for CPAs who perform EBP audits

Continue and expand outreach activities Work with plan administrator organizations to explain the

importance of hiring competent CPAs Use information from eFast2 to target correspondence to

Plan administrators in the strata of less than 5 plans CPA firms in the 25-99 stratum

Communicate with state licensing boards regarding the results of the study

Expand EBSA’s outreach to state societies of CPAs where a large number of CPA firms perform less than 5 audits

Recommendations - Outreach

82 #CBIZMHMwebinar Co-presented by:

Auditor focus on areas of deficiency Planning and supervision Internal controls Investments Contributions Benefit payments Participant data Party-in-interest transactions

Impact on Plan Sponsors

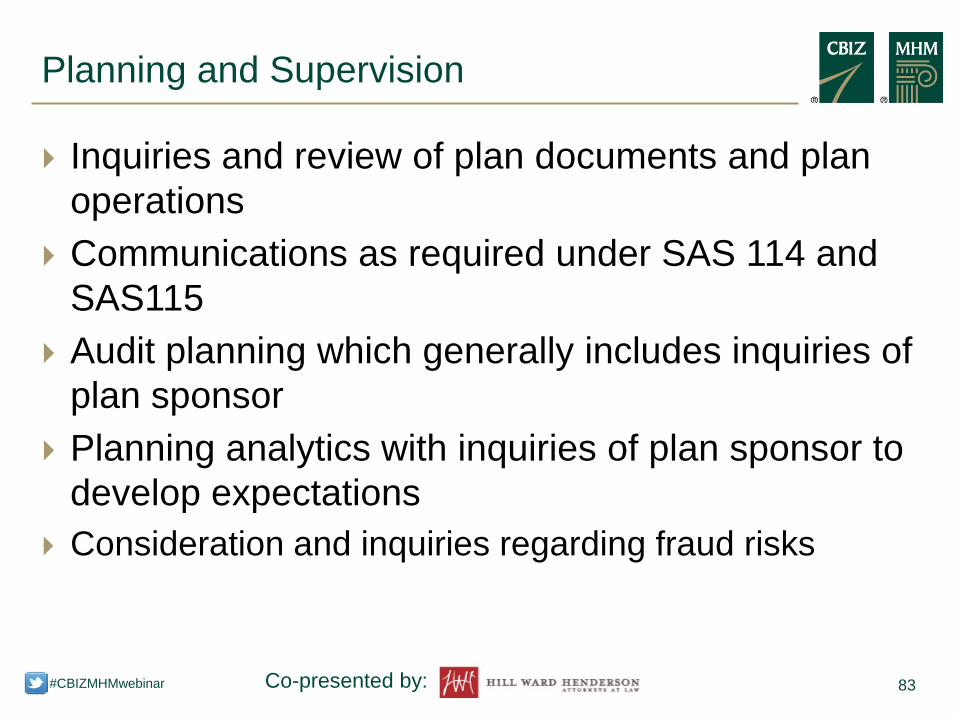

83 #CBIZMHMwebinar Co-presented by:

Inquiries and review of plan documents and plan operations

Communications as required under SAS 114 and SAS115

Audit planning which generally includes inquiries of plan sponsor

Planning analytics with inquiries of plan sponsor to develop expectations

Consideration and inquiries regarding fraud risks

Planning and Supervision

84 #CBIZMHMwebinar Co-presented by:

Request for documentation of internal control environment

Request SOC 1 report for service providers

Internal Controls

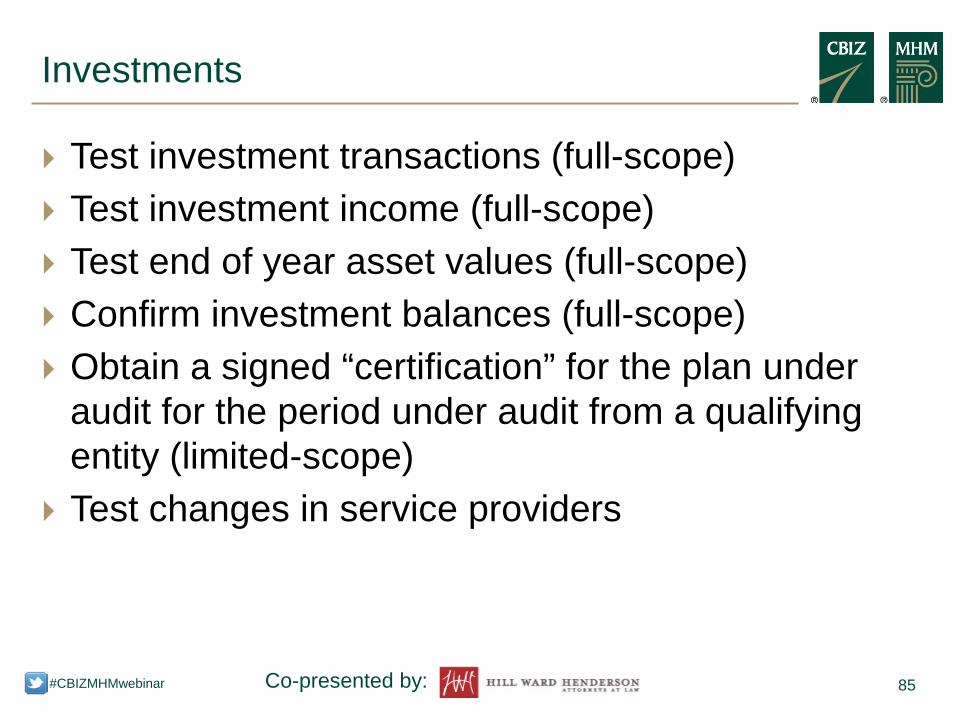

85 #CBIZMHMwebinar Co-presented by:

Test investment transactions (full-scope) Test investment income (full-scope) Test end of year asset values (full-scope) Confirm investment balances (full-scope) Obtain a signed “certification” for the plan under

audit for the period under audit from a qualifying entity (limited-scope)

Test changes in service providers

Investments

86 #CBIZMHMwebinar Co-presented by:

Test timely remittance of employee contributions Test compliance with plan compensation provisions Test use of forfeitures Reconcile contributions to plan sponsor payroll

records, employee records, custodian trustee records and/or Schedule H of Form 5500

Test significant rollovers

Contributions

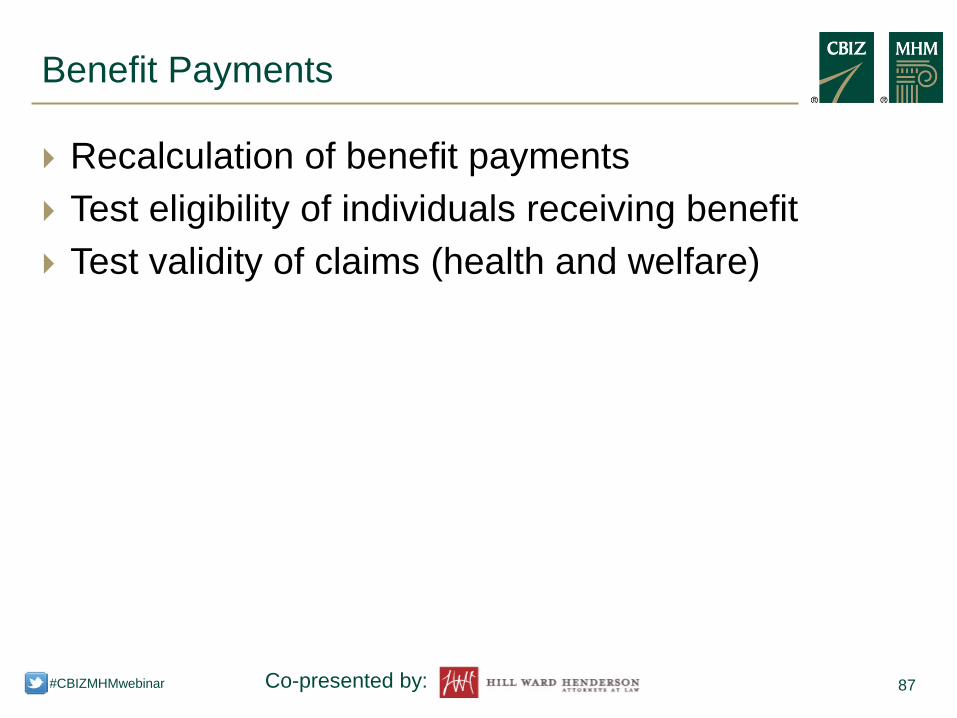

87 #CBIZMHMwebinar Co-presented by:

Recalculation of benefit payments Test eligibility of individuals receiving benefit Test validity of claims (health and welfare)

Benefit Payments

88 #CBIZMHMwebinar Co-presented by:

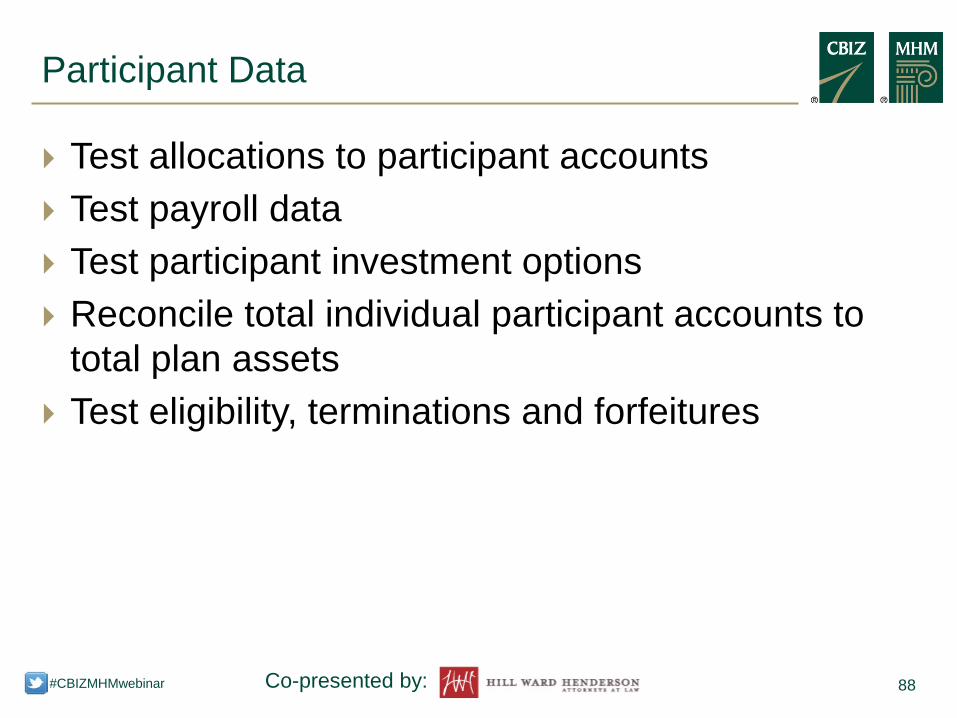

Test allocations to participant accounts Test payroll data Test participant investment options Reconcile total individual participant accounts to

total plan assets Test eligibility, terminations and forfeitures

Participant Data

89 #CBIZMHMwebinar Co-presented by:

Most frequent deficiency was no work performed – expect an inquiry from the plan auditor

Inquiry and testing of prohibited transactions

Party In Interest Transactions

90 #CBIZMHMwebinar Co-presented by:

Questions?

91 #CBIZMHMwebinar Co-presented by:

Save the date for this course: 8/27 and 9/11: Caring for Your Retirement Plan

Read these related publications: Assessing the Quality of Employee Benefit Plan Audits (DOL) Lessons from the GreatBanc Settlement - ESOPs to Face More

Scrutiny Project Aims to Simplify Employee Benefit Plan Reporting

If You Enjoyed This Webinar

92 #CBIZMHMwebinar Co-presented by:

Connect with CBIZ & MHM

linkedin.com/company/ mayer-hoffman-mccann-p.c.

@mhm_pc

youtube.com/ mayerhoffmanmccann

slideshare.net/mhmpc

linkedin.com/company/ cbiz-mhm-llc

@cbizmhm

youtube.com/user/BizTipsVideos

slideshare.net/CBIZInc

MHM CBIZ

93 #CBIZMHMwebinar Co-presented by:

Connect with Hill Ward Henderson

http://www.linkedin.com/company/hill-ward-henderson

@hwhlawfirm

http://www.facebook.com/HillWardHenderson

http://www.hwhlaw.com/blog