Webinar Series: Manufacturing Opportunities in Clean ... · 2/27/2013 · Improve planning and...

64

www.theCEMC.com Webinar Series: Manufacturing Opportunities in Clean Energy Markets Solar Industry Domestic Supply Chain Opportunities (PV)

Transcript of Webinar Series: Manufacturing Opportunities in Clean ... · 2/27/2013 · Improve planning and...

www.theCEMC.com

Webinar Series: Manufacturing

Opportunities in Clean Energy

MarketsSolar Industry Domestic Supply

Chain Opportunities (PV)

www.theCEMC.com

Agenda

• Introduction– Jacques Koppel, CEMC Director

• Solar Energy Industry in the U.S.– Alexander Winn, The Solar Foundation

• U.S. Department of Energy and Solar– Doug Hall, US DOE SunShot Initiative’s

Photovoltaic Manufacturing Initiative

• Solar Manufacturing Resources– Jim Haider, CEMC

– Dale Reckman, CEMC

• Questions and Answers – Submit using Chat

• Goal is to help MEP Centers provide their clients supply

chain opportunities in the clean energy manufacturing

economy to support growth & diversification strategies

• Services have expanded beyond wind sector to include

off-shore wind, solar, advanced transportation, natural

gas and geothermal markets.

• We offer market expertise that helps both the MEP

center/clients identify services/next steps needed to

approach the clean energy market with a higher

assurance of success. Our services include:

– Workshops/Webinars

– Technical assessments/assistance

www.theCEMC.com

For info contact [email protected] or call 612 466.4506

www.theCEMC.com

Webinar ScheduleJanuary 23rd

Offshore Wind Manufacturing Opportunities

February 27th

Solar Industry Domestic Supply Chain Opportunities (PV)

March 27th

U.S. Department of Energy Clean Energy Manufacturing Initiatives

April 24th

Manufacturing Opportunities in Mass Transit

May 22nd

Exploring Growth Opportunities in the Natural Gas Industry

June 26th

Financing Growth in Clean Energy Manufacturing

July 24th

Batteries for Electrical Energy Storage in Transportation

August 28th

Geothermal Market and Manufacturing Opportunities

September 25th

Utility-Scale Wind Manufacturing – State of the Market

*View archived webinars at

www.thecemc.com under “Latest News”

www.theCEMC.com

Alexander Winn

The Solar Foundation

Solar Industry Domestic Supply Chain Opportunities –

Market Overview

About The Solar Foundation

Founded in 1977 and based in Washington, DC, The Solar Foundation is an independent nonprofit working to demonstrate the global benefits of solar energy through research and education.

National Solar Jobs Census & SunShot Solar Outreach Partnership Resources: http://www.thesolarfoundation.org

8

� Increase installed capacity of solar in U.S. communities

� Streamline and standardize permitting and interconnection processes

� Improve planning and zoning codes/regulations for solar technologies

� Increase access to solar financing options

� Provide complimentary technical assistance

About the SunShot Solar Outreach Partnership

9

Fact: Solar works across the US

Source: National Renewable Energy Laboratory 10

Fact: The solar industry is growing

Source: Solar Energy Industries Association/ GTM Research. Solar Market Insight: 2011 Year-in-Review, 2012 Q1, 2012 Q2, & 2012 Q3

11

0

500

1000

1500

2000

2500

3000

3500

4000

2006 2007 2008 2009 2010 2011 2012

Inst

all

ed

Ca

pa

city

(M

W)

New U.S. Solar Electric Installations

Annual Q1 Q2 Projected

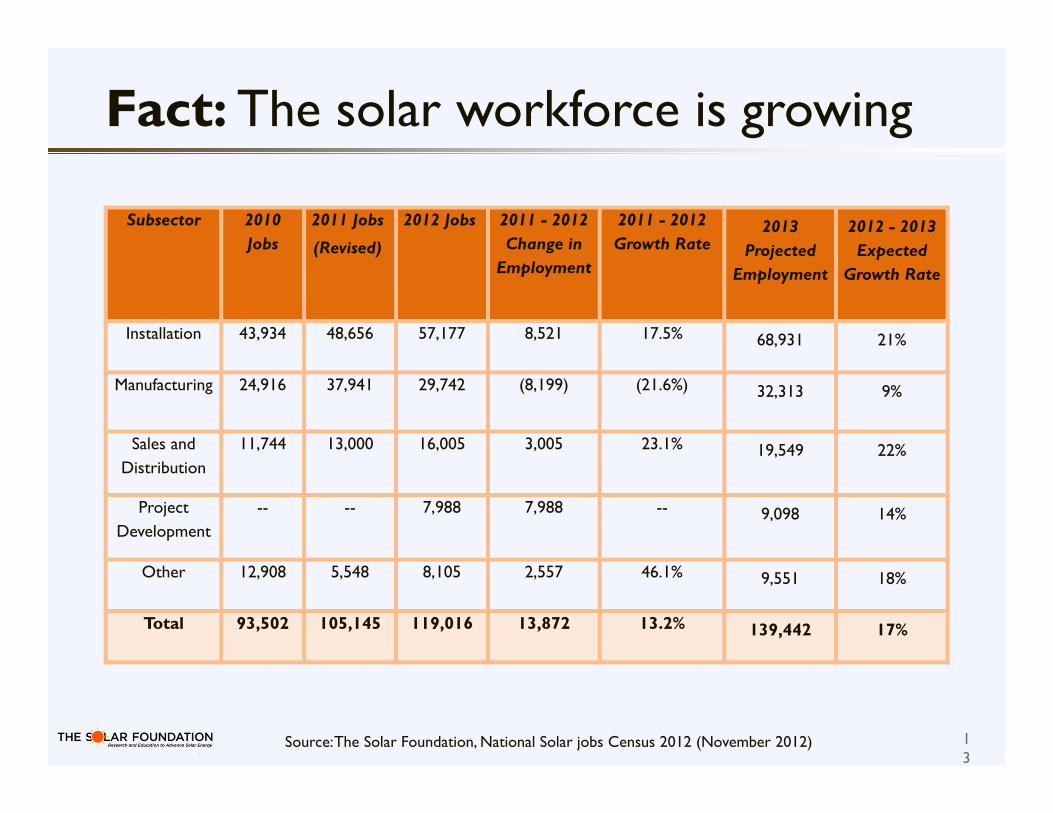

Fact: The solar workforce is growing

Source: The Solar Foundation, National Solar jobs Census 2012 (November 2012) 12

Fact: The solar workforce is growing

Source: The Solar Foundation, National Solar jobs Census 2012 (November 2012) 13

Subsector 2010

Jobs

2011 Jobs

(Revised)

2012 Jobs 2011 - 2012

Change in

Employment

2011 - 2012

Growth Rate2013

Projected

Employment

2012 - 2013

Expected

Growth Rate

Installation 43,934 48,656 57,177 8,521 17.5% 68,931 21%

Manufacturing 24,916 37,941 29,742 (8,199) (21.6%) 32,313 9%

Sales and

Distribution

11,744 13,000 16,005 3,005 23.1% 19,549 22%

Project

Development

-- -- 7,988 7,988 -- 9,098 14%

Other 12,908 5,548 8,105 2,557 46.1% 9,551 18%

Total 93,502 105,145 119,016 13,872 13.2% 139,442 17%

Fact: The cost of solar is falling

Source: Solar Energy Industries Association/ GTM Research. Solar Market Insight: 2011 Year-in-Review, 2012 Q1, 2012 Q2, & 2012 Q3

$0.00

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

$7.00

$8.00

Q1 2010 Q2 2010 Q3 2010 Q4 2010 Q1 2011 Q2 2011 Q3 2011 Q4 2011 Q1 2012 Q2 2012 Q3 2012

Inst

all

ed

Pri

ce (

$/W

DC)

Residential Commerical Utility

↓ 44%

14

AVERAGE

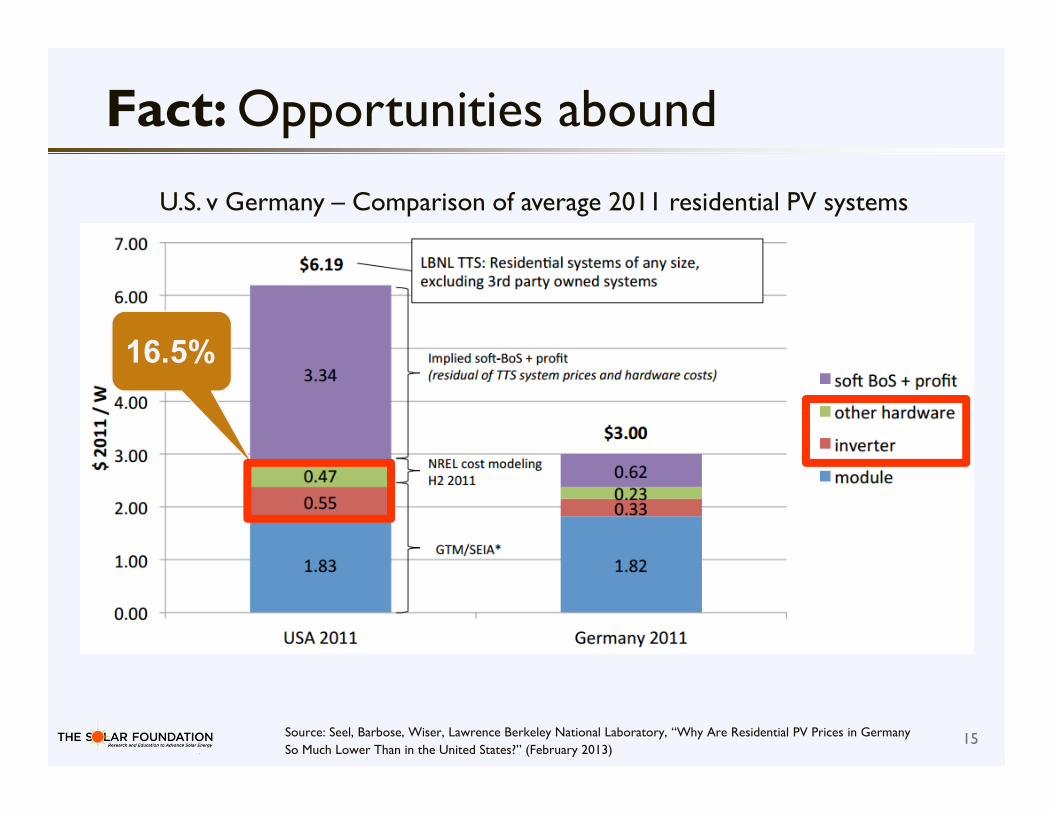

Fact: Opportunities abound

Source: Seel, Barbose, Wiser, Lawrence Berkeley National Laboratory, “Why Are Residential PV Prices in Germany

So Much Lower Than in the United States?” (February 2013)

↓ 25%

15

16.5%

U.S. v Germany – Comparison of average 2011 residential PV systems

Fact: Opportunities abound

Source: Seel, Barbose, Wiser, Lawrence Berkeley National Laboratory, “Why Are Residential PV Prices in Germany

So Much Lower Than in the United States?” (February 2013)

↓ 25%

16

16.5%

� Think about the whole system:

– Power electronics:

• Inverters

• Wiring

– Metal Racking (Other materials?)

– PV-grade glass

– Glass coatings

– Feedstcok

– Transportation

www.theCEMC.com

Doug Hall

US Department of Energy

SunShot Initiative’s Photovoltaic

Manufacturing Initiative

US DOE’s SunShot InitiativeCEMC Webinar

Doug HallPhotovoltaic Manufacturing Initiative Portfolio Manager

February 27, 2013

19

“We’re telling America’s scientists and engineers that if they assemble teams of the best minds in their fields, and focus on the hardest problems in clean energy, we’ll fund the Apollo projects of our time.”

- President Obama

2011 State of the Union

“Apollo project of our times”

SunShotMoon Shot

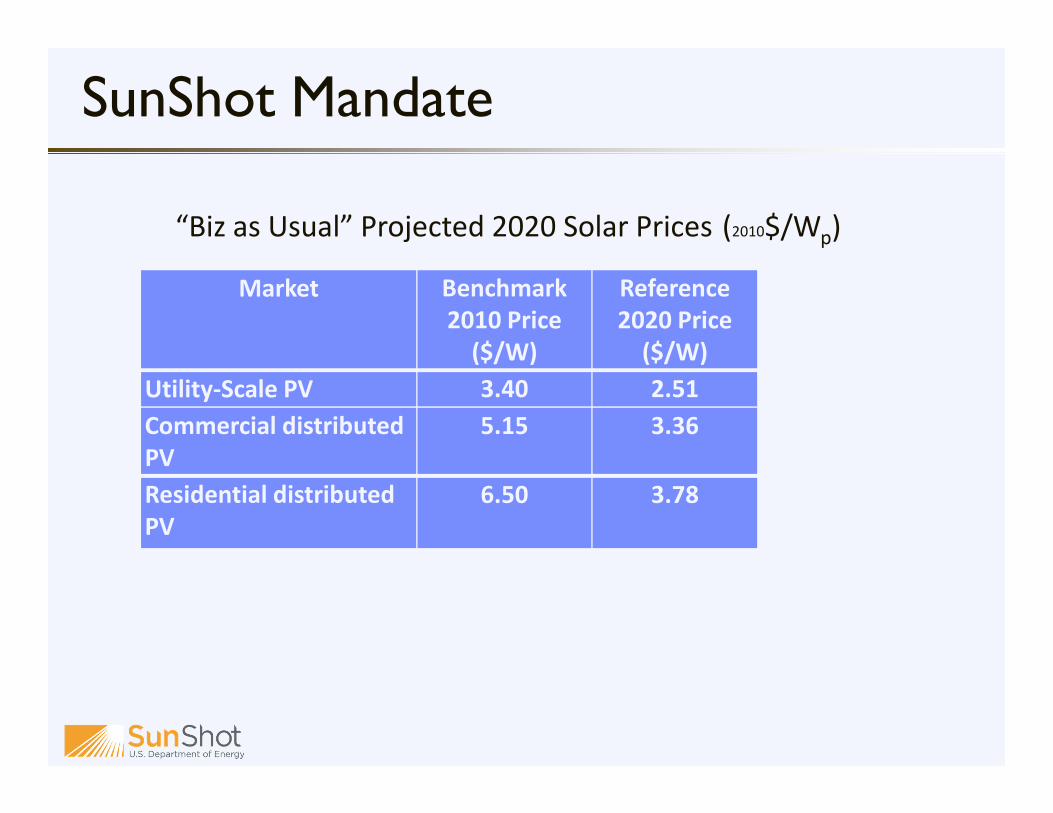

Market Benchmark

2010 Price

($/W)

Reference

2020 Price

($/W)

Utility-Scale PV 3.40 2.51

Commercial distributed

PV

5.15 3.36

Residential distributed

PV

6.50 3.78

“Biz as Usual” Projected 2020 Solar Prices (2010$/Wp)

SunShot Mandate

2030 Utility Scale PV Base Case

OR

ID

NV

MT ND

SD

NE

WY

UT

NM AR

MS

AZSC

OK

KS

ME

WA

CA CO

TX

MO

IL

IA

MN

WI

MI

OH

KY

TN

AL GA

VA

NY

PA

LA

NC

IN

Installed PV (GW)

< 0.1

0.1 - 1

1 - 5

5 - 10

10 - 20

20 - 30

> 30

OR

ID

NV

MT ND

SD

NE

WY

UT

NM AR

MS

AZ OK

KS

ME

WA

CA CO

TX

MO

IL

IA

MN

WI

MI

OH

KY

TN

AL GA

VA

NY

PA

LA

NC

IN

Installed Capacity: 30 GW

1.5% of electrical demand

modeled with Regional Energy Deployment System (ReEDS)

capacity-expansion model

SunShot Mandate

Market Benchmark

2010 Price

($/W)

Reference

2020 Price

($/W)

SunShot

2020 Price

($/W)

Utility-Scale PV 3.40 2.51 1.00

Commercial distributed

PV

5.15 3.36 1.25

Residential distributed

PV

6.50 3.78 1.50

SunShot Target 2020 Solar Prices (2010$/Wp)

WV

MD

NJ

CT

RI

MA

FLFL

VTVT NHNH

2030 Utility Scale PV with SunShot

OR

ID

NV

MT ND

SD

NE

WY

UT

NM AR

MS

AZSC

OK

KS

ME

DE

WA

CA CO

TX

MO

IL

IA

MN

WI

MI

OH

KY

TN

AL GA

VA

NY

PA

LA

NC

IN

Installed PV (GW)

< 0.1

0.1 - 1

1 - 5

5 - 10

10 - 20

20 - 30

> 30

OR

ID

NV

MT ND

SD

NE

WY

UT

NM AR

MS

AZSC

OK

KS

ME

WV

WA

CA CO

TX

MO

IL

IA

MN

WI

MI

OH

KY

TN

AL GA

VA

NY

PA

LA

MD

NC

IN

CT

RI

NJ

MA

DE

Installed Capacity: 302 GW

14% of electrical demand

Utility System with $1/W Price Goal

Estimates do not include the cost of land.

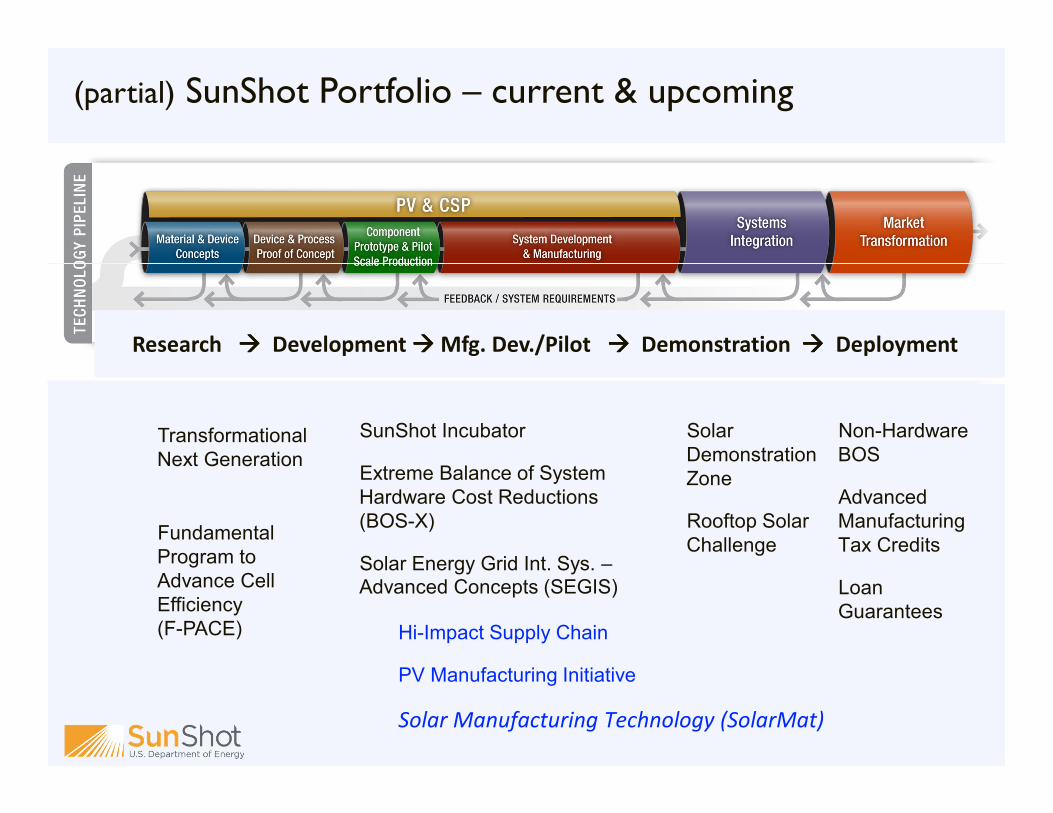

(partial) SunShot Portfolio – current & upcoming

Transformational

Next Generation

Fundamental

Program to

Advance Cell

Efficiency

(F-PACE)

SunShot Incubator

Extreme Balance of System

Hardware Cost Reductions

(BOS-X)

Solar Energy Grid Int. Sys. –Advanced Concepts (SEGIS)

Solar

Demonstration

Zone

Rooftop Solar

Challenge

Non-Hardware

BOS

Advanced

Manufacturing

Tax Credits

Loan

Guarantees

Research ���� Development ���� Mfg. Dev./Pilot ���� Demonstration ���� Deployment

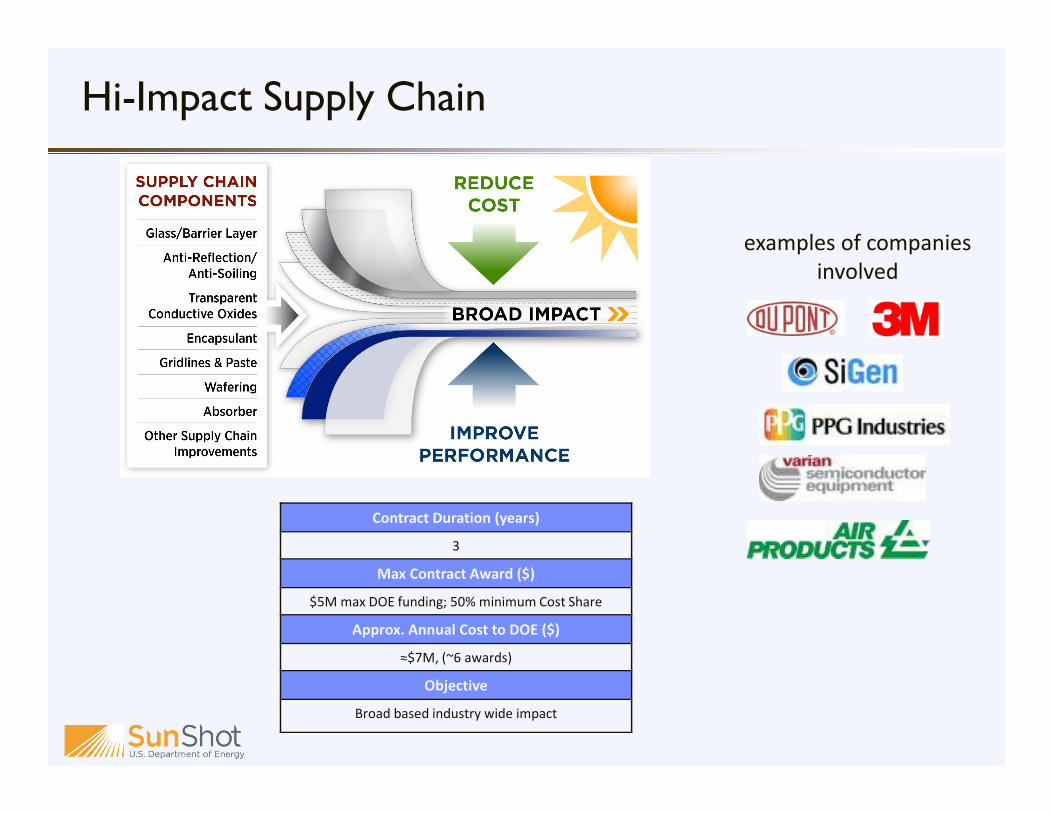

Hi-Impact Supply Chain

PV Manufacturing Initiative

Solar Manufacturing Technology (SolarMat)

Hi-Impact Supply Chain

Contract Duration (years)

3

Max Contract Award ($)

$5M max DOE funding; 50% minimum Cost Share

Approx. Annual Cost to DOE ($)

≈$7M, (~6 awards)

Objective

Broad based industry wide impact

Sample Awardees

examples of companies

involved

PV Manufacturing Initiative Projects

US PV Manufacturing Consortium (PVMC)

Industry Consortium (modeled after SEMATECH)

Thin-Film Manufacturing Development Facility

Component, BOS, and System Reliability Testing

Volume Manufacturing Best Practices

Solar Rochester

c-Si Manufacturing Development Facility

Bay Area PV Consortium (BAPVC)

Industry-directed University research

� Development and demonstration of innovative, but commercially and technically viable, manufacturing technology that can achieve a significant market or manufacturing impact in 1 to 4 years.

� Must drive down the cost of manufacturing and/or implementing efficiency-increasing technology in manufacturing

� Addresses both PV and Concentrated Solar Power areas of solar technology

– CSP Topic Area must be for a hardware demonstration of manufacturing technologies and methodologies that reduce the solar field costs

– PV Topic Area must achieve significant demonstrated cost reductions in module, supply chain (tools and BOM), or BOS

Solar Manufacturing Technology (SolarMat)Funding Opportunity released 2/22/2013

Contract Duration (years)

2-4

Contract Award ($)

$5M max DOE funds, 50% minimum Cost Share

Approx. Annual Cost to DOE ($)

≈5 M

Objective

Move next generation manufacturing technology into

US factories

� SunShot homepage– http://eere1.energy.gov/solar/sunshot/index.html

� Financial Opportunities page– http://eere1.energy.gov/solar/sunshot/financial.html

� Current Opportunities page– http://eere1.energy.gov/solar/sunshot/fcurrent_opportunities.html

� also

� US DOE SBIR� http://science.energy.gov/sbir/funding-opportunities/

Information about SunShot and SunShot Funding Opportunities

31

www.theCEMC.com

Jim Haider and Dale Reckman

CEMC Energy Specialists

www.theCEMC.com

Solar Manufacturing Resources

Tools developed for the Solar

Industry by the Clean Energy

Manufacturing Center

www.theCEMC.com

The Goal of Our Work

To educate manufacturers, suppliers, MEP’s and other on clean

energy manufacturing opportunities and the available tools to help in the successful

diversification into these often times challenging market sectors.

www.theCEMC.com

The NIST MEP Program in Short

• Program started in 1988, with at least one center in all

50 states by 1996

• 59 centers with over 370 field locations

• System wide, Non-Federal staff is over 1,450

• Contracting with over 2,190 third party service providers

• Partnership Model –Federal/State/Industry

• Emphasis on performance – program and center –

measured based upon impact of center services on

client firms

www.theCEMC.com

What NIST MEP Does• Focus on meeting manufacturer’s short term needs, but in context

of overall company strategy

• NIST MEP Center areas of common strength:– Engineering Services for products and processes

– Growth Services

– Lean Manufacturing

– Quality Systems

– Environmental Services

– Workforce Development

• Reach nearly 33,000 manufacturing firms and complete over 10,000 projects per year*

* Based on FY2009 NIST MEP Center reported performance data

www.theCEMC.com

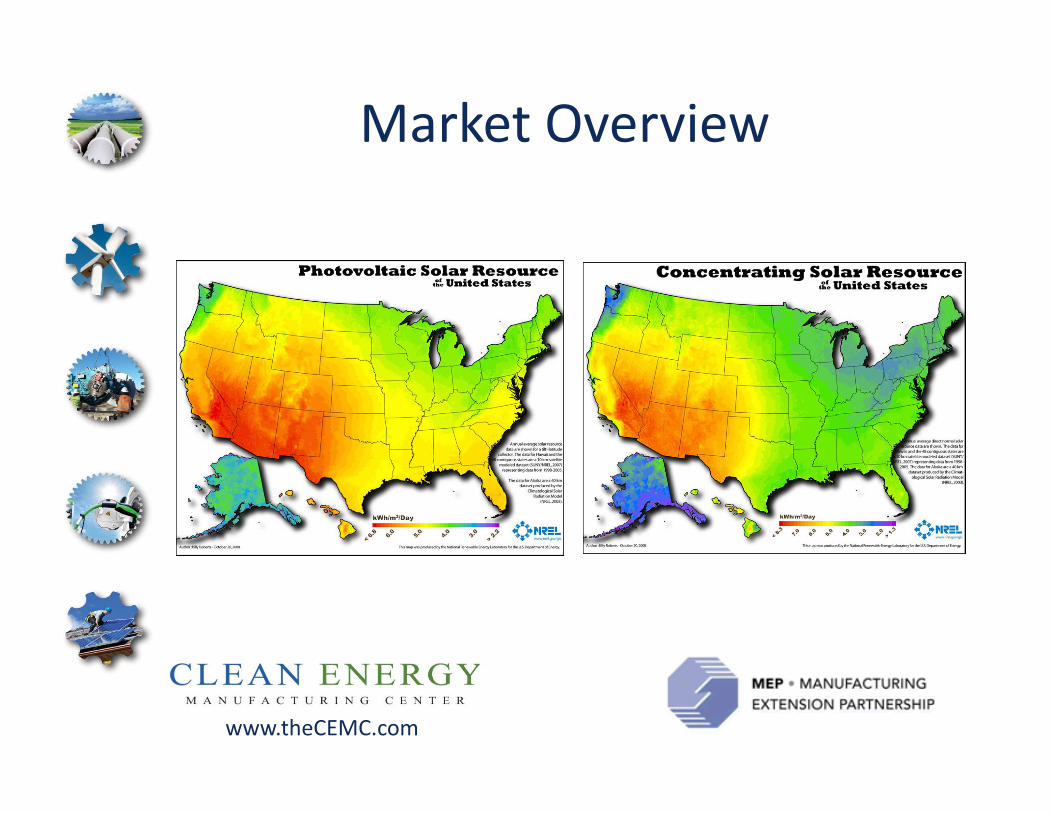

Market Overview

www.theCEMC.com

Market Overview

0100020003000400050006000700080009000

10000

US PV installations (annual installations in MWdc)

US PV installations

(annual installations in

MWdc)

www.theCEMC.com

Market Overview

0

2

4

6

8

10

12

14

16

US PV global market share

US PV global market

share in %

www.theCEMC.com

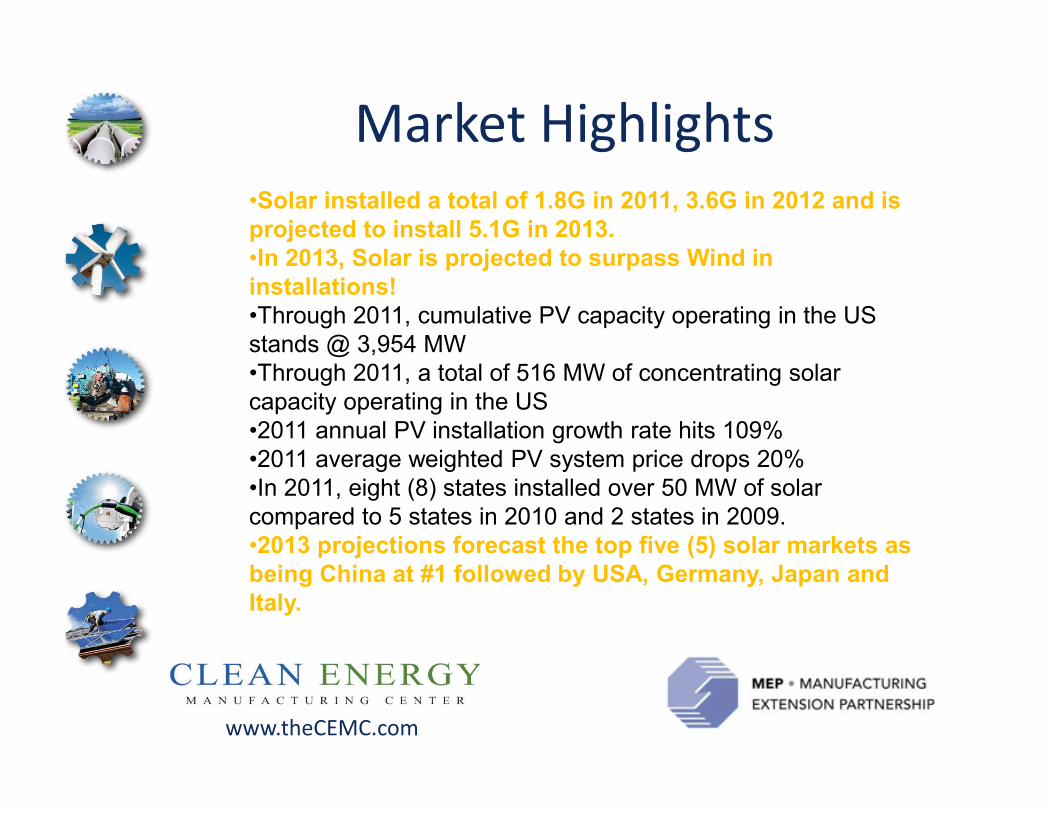

Market Highlights•Solar installed a total of 1.8G in 2011, 3.6G in 2012 and is

projected to install 5.1G in 2013.

•In 2013, Solar is projected to surpass Wind in

installations!

•Through 2011, cumulative PV capacity operating in the US

stands @ 3,954 MW

•Through 2011, a total of 516 MW of concentrating solar

capacity operating in the US

•2011 annual PV installation growth rate hits 109%

•2011 average weighted PV system price drops 20%

•In 2011, eight (8) states installed over 50 MW of solar

compared to 5 states in 2010 and 2 states in 2009.

•2013 projections forecast the top five (5) solar markets as

being China at #1 followed by USA, Germany, Japan and

Italy.

www.theCEMC.com

Unique Attributes of

Wind Industry

• Technology has matured in Wind industry

with the 1.25 – 3 MW tower mounted

turbines

• Several large European OEM’s drive the

market

• Warrantee requirements along with high

maintenance costs drive strict quality

requirements for industry

www.theCEMC.com

Solar Industry is Different

• Technology still developing

• Market is still evolving

• Suppliers and Solar companies enter and

exit the market continuously

• Cost / megawatt is still high relative to

wind

www.theCEMC.com

Market Overview

• Three (3) distinct Market Sectors

Residential – less than 10kW

Commercial – 10kW to 1MW

Utility – greater than 1MW

www.theCEMC.com

Key Industry Players(a partial list)

• Acciona

• Iberdrola

• ABB

• GE

• Ingeteam

• 3M

• Bosch

• Jinko Solar

• MAGE solar

• Mitsubishi

• SolarWorld

• tenKsolar

• Westinghouse

• AREVA solar

• Panasonic

• Samsung

• Siemens

• LG

• First Solar

www.theCEMC.com

Top 15 Solar PV Module Mfrs, 2011

www.theCEMC.com

Taxonomy

• Solar warranty structures are tiered in

nature. An example might be:• Guaranteed to produce 95% rated output for 5

years +

• A Guarantee to produce 90% rated output for 12

years +

• A Guarantee to produce 80% rated output for 25

years.

The industry demands quality if to dispel the

historic stereotype of being a bit gimmicky!

www.theCEMC.com

Solar Cost Breakdown

Poly Silicon

Production

Ingot / Wafer

Production

Cell /Panel

Manufacturing

System

Manufacturing

and Assembly Installation

Market Character Very Global Regional Local

Cost ~$0.80 per watt peak ~$4.20 per watt peak

• The manufacturing of panels may become more regional as freight

becomes larger portion of cost

• Cost pressure on the Poly / Ingot / Cell manufacturers has driven

costs to industry competitive point

• System assembly and installation costs still keep solar market from

being cost competitive

• This represents opportunity in the system assembly and

installation categories

www.theCEMC.com

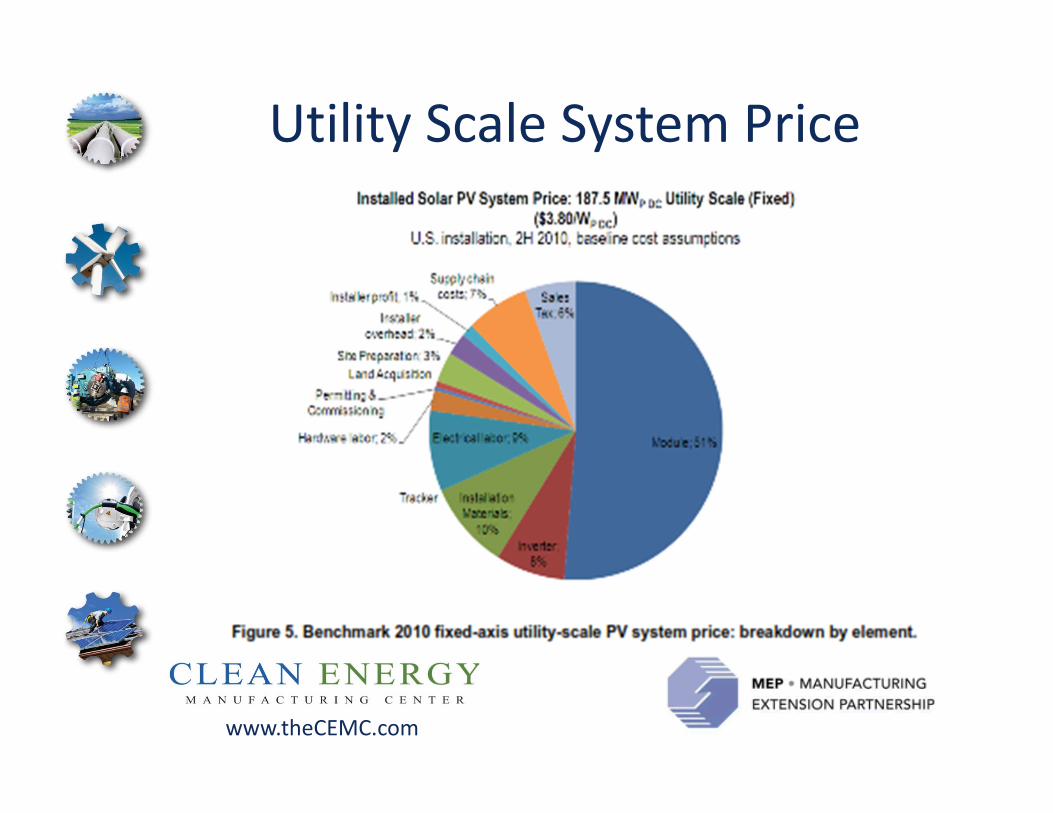

Utility Scale System Price

www.theCEMC.com

Competitive Solar Prices

Something has to change

1. Cost of all other energy

options must rise to the level

of solar

2. Solar costs must come down

to the level of the market

3. Other…

www.theCEMC.com

Falling Cost of Solar, 2010-2012

www.theCEMC.com

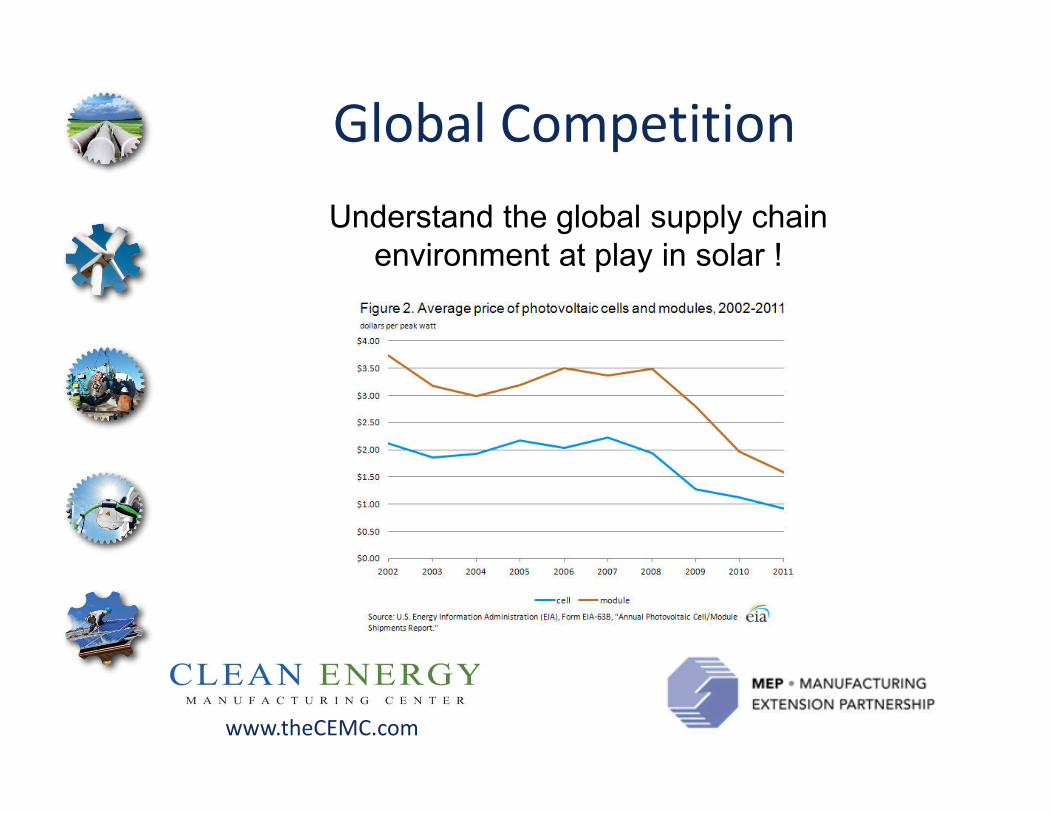

Global Competition

Understand the global supply chain

environment at play in solar !

www.theCEMC.com

World Class

• Solar warranty structures are tiered in

nature. An example might be:• Guaranteed to produce 95% rated output for 5

years +

• A Guarantee to produce 90% rated output for 12

years +

• A Guarantee to produce 80% rated output for 25

years.

The industry demands quality if to dispel the

historic stereotype of being a bit gimmicky!

www.theCEMC.com

Opportunities

• Raw Materials

– Materials such as structural’s are often

procured near the final installation site due to

the associated logistics costing.

• Installation Materials

– Fabrications associated with final installations

are often procured near the final installation

site.

www.theCEMC.com

Raw Material Opportunities

• Raw Materials

– Steel, aluminum and stainless steels in there un-processed forms including angle, channel, wide flange beam, bar stock & plate.

– Fasteners & fastening systems.

– Materials of an aggregate nature including rock, stone, gravel, cement.

www.theCEMC.com

Installation Opportunities

• Installation Materials

– Fabrications including those completed on and off-site. ( typically AWS D01.1, D01.2 & D01.4 )

– Contract machining

– Processed Raw Material including punched / drilled structurals, formed / bent plate, threaded bar stock.

www.theCEMC.com

Opportunities

• Technology associated items such as

those associated with the rapidly

developing inverter or panel /

module markets where partially

completed product is imported and

final assembly is performed on US

soil.

www.theCEMC.com

Opportunities & Challenges

• American Manufacturers can enter Solar market with new and innovative solutions to lower total installed cost of Solar Systems

• However, American Manufacturers need to be able to find customers

• Installers, OEM’s and upper tier suppliers need to be able to find new technologies and new vendors

www.theCEMC.com

Moving Forward• A basic taxonomy was developed to help

manufacturers identify opportunities

• An assessment tool was developed to objectively critique a manufacture's strengths and weaknesses in the Solar Market and continues refinement to this day

• A Solar Manufacturing Capabilities matrix was developed to characterize a supplier’s position within the industry

• This matrix allows a manufacturer to easily identify areas of improvement and areas of strength

• The matrix also allows companies to characterize “good fit” vendors and customers

www.theCEMC.com

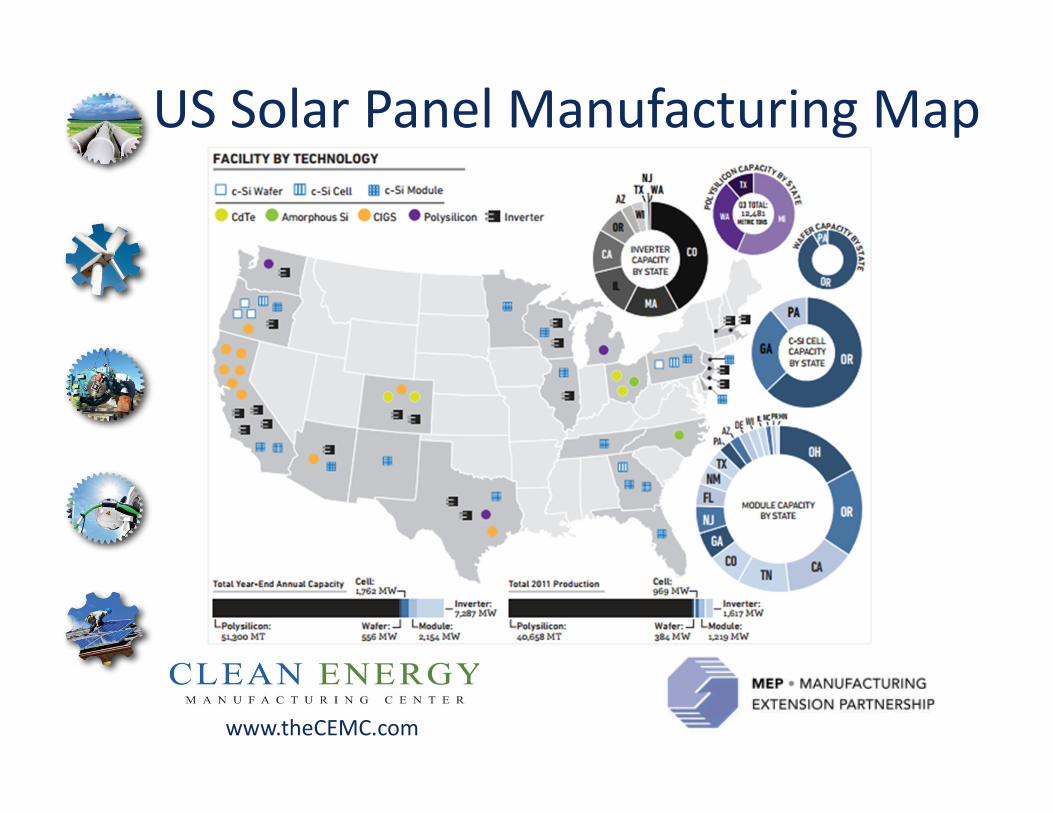

US Solar Panel Manufacturing Map

www.theCEMC.com

Solar Supply Chain Tool• Took industry best practices

– U.S. Department of Defense

– MEP System

– Wind Supply Chain.

• A set of objective eyes are

required

• CEMC

• MEP

• others

• Assessment made in several key

areas

• Commercial and Financial

Stability

• Product Design

• Manufacturing Process

• Quality

• Supply Chain

• Global Competiveness

• Areas of improvement and

opportunity identified

• Matchmaking

• MEP Engagement

• Growth

www.theCEMC.com

Solar Manufacturing Capabilities MatrixSMC Level 1 SMC Level 2 SMC Level 3 SMC Level 4 SMC Level 5 SMC Level 6 SMC Level 7 SMC Level 8

Research Technology DevelopmentEngineering and Manufacturing

DevelopmentProduction and Deployment

Initial ResearchProduct in Lab

Environment

Component

Development

System

Development

Process

Development

Process

Maturity

Low Rate

Production

LEAN, Full Rate

ProductionK

ey

Co

nsi

de

rati

on

s

Basic to Advanced

Research

Manufacturing

Feasibility

Determined

Manufacturing

Process Emerging

Manufacturing

Processes

Demonstrated

Manufacturing

Processes in

Development

Process Maturity

Demonstrated

Manufacturing

Process Operating

at Target

Performance

Lean / Six Sigma

Production in

Place

Advanced

Technology

Development

Manufacturing

Processes

Identified

Manufacturing

Cost Drivers

Identified

Cost Drivers

Analyzed

Producability

Improvements

Underway

Manufacturing

Processes Proven

Quality and Cost

Metrics met

Meeting or

Exceeding Cost,

Schedule, &

Performance

Goals

Manufacturing

Concepts

Identified

Key Processes

Identified

Long Lead Items

Identified

Supply Chain

Management in

Place

Supply Chain

Stable

Supply Chain

Mature and

Meeting Lead

Times

Lev

el

Ad

va

nce

me

nt

Cri

teri

a

Characterize Basic

Materials for

Manufacturing

Identify Baseline

Materials and

Issues

Key

Characteristics

Identified

Initial Trade /

Market Studies

Materials Being

ProvenMaterials Proven

Continuous

Process

Improvement is

Ongoing

Monitor and

Manage all Key

Characteristics at

Six Sigma Level

Identify Material

Concerns

Funding and

Budget for Trade

Studies

Mfg/QA approach

identified

Materials

Matured

Supply Chain

Being Assessed

Design For

Manufacturability

and Assembly

Materials In

Control

Funding to Meet

Six Sigma Goals

Identify Funding

Development

Strategy Should

Include Elements

of Mfg/QA

Early Supply

Chain Assessment

Quality

Thresholds

Established

QA Data Collected

Quality

Characteristics

Validated

Quality ValidatedNo Make / Buy

Changes

Funding to Meet

Next Level

Funding to Meet

Next Level

Supply Chain

Strategies Include

Mfg/QA

BOM Identified

BOM Supports

Low Rate

Production

Supply Chain

Supports Full Rate

Production

Key Critical

Suppliers Meet

Six Sigma Goals

Funding to Meet

Next Level

Funding to Meet

Next Level

Funding to Meet

Next Level

Funding to Meet

Next Level

www.theCEMC.com

Moving Forward

• Consider attending one (1) of the many available CEMC

events. More can be learned by visiting

www.thecemc.org or connect with CEMC staff directly.

• Connect with other industry specialists including SEIA,

SEPA, Blue Green Alliance Foundation and GLWN.– www.seia.org

– www.solarelectricpower.org

– www.bgafoundation.org

– www.glwn.org

www.theCEMC.com

Questions and AnswersSubmit using Webinar Chat feature

www.theCEMC.com

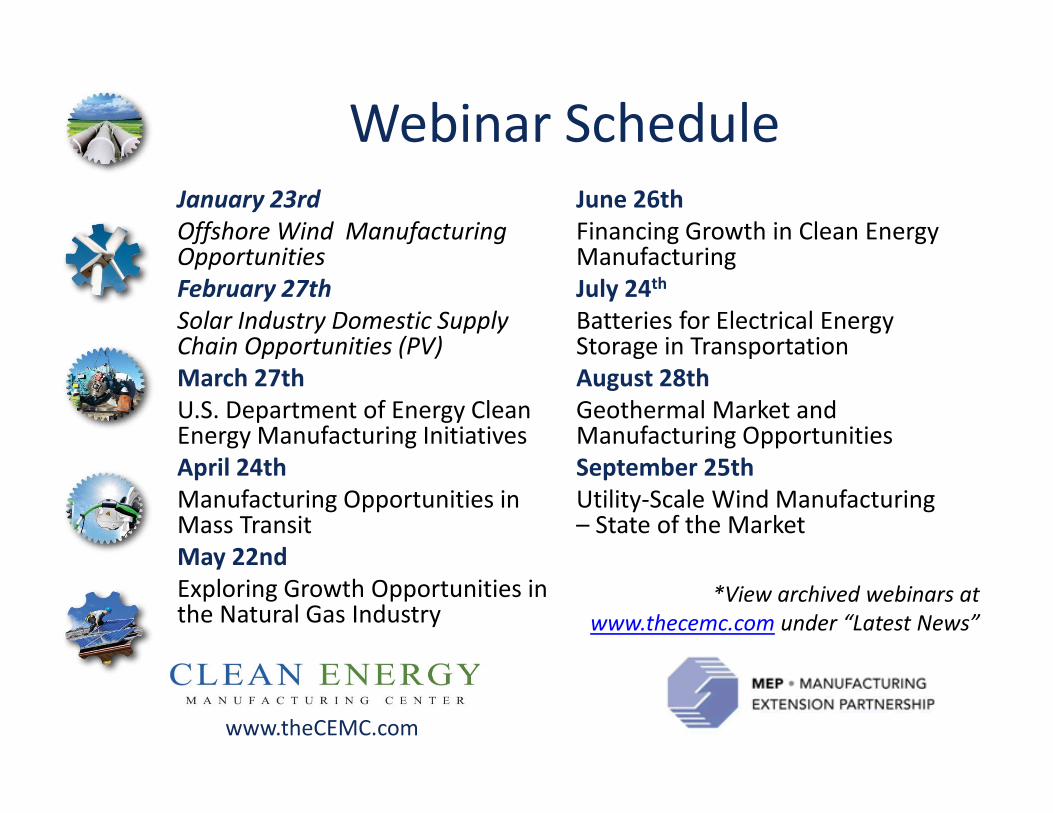

Webinar ScheduleJanuary 23rd

Offshore Wind Manufacturing Opportunities

February 27th

Solar Industry Domestic Supply Chain Opportunities (PV)

March 27th

U.S. Department of Energy Clean Energy Manufacturing Initiatives

April 24th

Manufacturing Opportunities in Mass Transit

May 22nd

Exploring Growth Opportunities in the Natural Gas Industry

June 26th

Financing Growth in Clean Energy Manufacturing

July 24th

Batteries for Electrical Energy Storage in Transportation

August 28th

Geothermal Market and Manufacturing Opportunities

September 25th

Utility-Scale Wind Manufacturing – State of the Market

*View archived webinars at

www.thecemc.com under “Latest News”

www.theCEMC.com

For Further Information

• Contact Linda Nielsen, Program Manager, Clean Energy Manufacturing Center, [email protected] , 612.466.4506

• Or visit our website at www.thecemc.com

Be with us next month as we learn about the US Department of Energy Clean Energy Manufacturing – 4th Wednesday at 1:00 Eastern

![U.S. Photovoltaic Manufacturing Consortium PVMC.pdfFeb 24, 2011 · Microsoft PowerPoint - MJ Presentation PVMC FSEC 2-24-11.ppt [Compatibility Mode] Author: JFenton Created Date:](https://static.fdocuments.in/doc/165x107/5fe4d681b229671e8d506d3d/us-photovoltaic-manufacturing-pvmcpdf-feb-24-2011-microsoft-powerpoint-.jpg)