Attention Disorders After Right Brain Damage: Living in Halved Worlds

Wealth ManagementASIAFINANCIAL TIMES SPECIAL REPORT | Friday December 5 2008

InsideDidier von Daeniken, headof Barclays’ private bankingoperations inAsia, ontheimportance offinding theright teamPage 2

www.ft.com/asiawealth2008

Simplicity and safetyare back in fashion

As 2008 draws to an end,private bankers andwealth managers inAsia seem battered, a

little humble and cautious,although not always disheart-ened at the outlook.

“The next two months will bepainful,” says Burkhard Varn-holt, chief investment officer ofthe Swiss private bank, Sarasin.“[But] if you focus on quality,you will have a great time in theupswing.”

The past few months have beenespecially dismal. Stock marketshave plummeted. “Losing 10 percent on a client’s portfolio is thenew break-even,” says onewealth manager.

Investors who lost money onstructured products, such asaccumulators and Lehman mini-bonds, protested on Hong Kongstreets, alleging banks had mis-led them about the risks.

In private, many wealth man-agers will tell you of impendinglaw suits launched by angry cli-ents – but somehow it is alwaysrivals who are being sued, andnot their own institution. Every-one seems to be reviewing proce-dures and they say clients aretaking fresh interest in readingthe small print.

As oil and commodity pricessurged during the first part ofthe year, private banks said cli-

ents were worried about infla-tion. Six months later, deflationis the big fear.

Private bankers look a littleembarrassed these days whenyou ask them about their hotnew investment products: theydo not seem to have any. Oftenadvice focuses on bonds and gold– especially physical gold, andnot structured products based ongold.

“I don’t think there will be a‘new new thing’ for 12 months,”says Ivan Leung, chief invest-ment strategist for JP MorganPrivate Bank in Asia.

Risk is out and capital protec-tion is in. Bonds look interesting.There is renewed emphasis ondiversification. Simplicity is backin fashion. So is safety. LehmanBrothers may not have had a pri-vate banking arm, but its col-lapse in September disturbed pri-

vate bankers and their clientsalike.

Even Citigroup, one of thegiants of the financial world,needed $300bn of governmenthelp and guarantees to survive. Ifthat were not enough, the USauthorities indicted the globalhead of wealth management atthe Swiss bank UBS as part oftheir investigation into the off-shore banking activities of richAmericans.

“Markets will continue to bevolatile and that’s something wecan’t control,” says Paul Sci-betta, chief executive officer ofJP Morgan Private Bank in Asia,based in Hong Kong. “We need tofocus on the things we can con-trol. Clients want to know thatwe will be there for them.

“Clients don’t remember youas much when times are good aswhen times are bad. Every pri-

vate bank has a chance to differ-entiate itself. When you are in across-country race, you make thebiggest difference when you arerunning uphill.”

The problems of the big univer-sal banks may help the smaller,more focused private banks thathave no investment bankingarms or exposure to subprime.

“I don’t consider them [bou-tique private banks] to be athreat because the business mod-els are very different, although Inever underestimate them,” saysMarcel Kreis, head of privatebanking in Asia-Pacific for CreditSuisse, one of the world’s finan-cial giants. “Their key focus is onasset management,” Mr Kreissays. “Ours, in Asia, is leverag-ing the investment bank relation-ship.” And, he could add, sup-porting the investment bankers.

Credit Suisse’s investmentbank lost SFr3.2bn in the thirdquarter, as it wrote downSFr2.4bn to cover problems withleveraged finance and structuredproducts. The private bank divi-sion showed global profits ofSFr789m before tax.

The private bank within alarger organisation still has itsappeal. A big retail branch net-work and a well-known brandname are a great starting point.

The Bank of China, for exam-ple, which has more than 10,000branches, has been working withRoyal Bank of Scotland toexpand private banking services.

Standard Chartered, which hasbeen in Asia for nearly 160 years,is relative latecomer to having adedicated private bank,

Everyone has madelosses, but longtermprospects are stillpromising, writesAndrew Wood

Inside this issueIndia and China Joe Leahyreports on the new kids on thewealthy block when it comesto private banking Page 2

Family finances Andrew Woodon the difficulty finding peoplewith the right range offinance and diplomacy skillsto manage family affairsPage 3

Back to school AssifShameen reports on theSingapore institute thatspecialises in trainingprivate bankers Page 3

Alternatives Collectables suchas wine and art (below) havebeen promoted as the savvyinvestor’s alternative to stockpicking and market timing,writes Peter Shadbolt Page 3

Going for gold: advice from private bankers has started to focus on gold – especially physical gold AFPContinued on Page 2

DECEMBER 5 2008 Section:Reports Time: 2/12/2008 - 16:01 User: graysteph Page Name: AWM1, Part,Page,Edition: AWM, 1, 1

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

2 ★ FINANCIAL TIMES FRIDAY DECEMBER 5 2008

Asia Wealth Management

Contributors

Andrew WoodAsia Markets & InvestmentCorrespondent

Joe LeahyMumbai Correspondent

Assif ShameenFT Contributor

Peter ShadboltFT Contributor

Rohit Jaggi &Stephanie GrayCommissioning Editors

Steven BirdDesigner

Andy MearsPicture Editor

For advertising details,contact:Angela MackayPhone +852 2905 5552Fax +852 2537 1211Email:[email protected] oryour usual representative

Simplicity back in fashion

but is catching up fast. Lastyear it opened 11 offices infive weeks.

“Not having a privatebanking arm is like sayingyou don’t have a mortgagebusiness,” says Peter Flavel,Standard Chartered’s headof private banking. “Westarted in mid-2006 withthree people and now we areup to 1,500 people globally.”

Last year was alwaysgoing to be difficult to fol-low. In China the surge inthe stock market mademany people feel they werewealthy. The Shanghai com-posite index gained 133 percent in nine months. ManyAsian entrepreneurs tookthe opportunity to float theircompanies. Initial publicofferings raised $147bn inAsia-Pacific in 2007 – a bigsource of fresh customers forprivate banks. Asia’s eco-nomic momentum seemedunstoppable. That percep-tion was part of the problem.

“Forecasts of rocketingwealth have exacerbated theproblems facing some pri-vate banks in the region,”says Enid Yip, Bank Sara-sin’s chief executive forAsia. “We’ve seen an irra-tional exuberance becauseAsia is such a temptation. Itwas an easy story to sell,and an easy story to buy, sowe have seen people pileinto the market, while estab-lished players haveexpanded. But many will nothave factored a downturninto their costs because theynever had a credible long-term strategy.”

The boom did go bustspectacularly. IPOs haveraised little more than aquarter of last year’s record

amounts, according toThomson Reuters. Sincepeaking in October 2007,mainland Chinese shareshave lost nearly three-quar-ters of their value. Makingmoney in those conditions isdifficult. Even hedge funds,supposed to make returns ifmarkets go up or down, havehad an awful time.

Andrea Benenati, chiefexecutive officer for northAsia at Julius Baer, a Swissboutique private bank, saysit set itself a test to see if itcould have advised clientsbetter. The result was a“perfect foresight” portfoliothat a manager with God-like forecasting skills wouldhave recommended. Backtesting showed that the port-folio would have weatheredall the storms of recentyears: the bursting of thetech bubble, the after-effectsof the September 11 attackson the US, the outbreak ofSevere Acute RespiratorySyndrome (Sars) in Asia. Itwould have returned about10 per cent a year. But itwould have lost money dur-ing October.

“Even with this knowledgeand hindsight, you couldn’tstructure something thatwouldn’t have been downthis year,” Mr Benenati says.“The problem now is: do youwant to lose money or doyou want to miss an oppor-tunity. People would rathermiss an opportunity.”

Markets are beginning toheal, says Ivan Leung at J PMorgan. “It’s less compli-cated than two months agowhen the worst-case sce-nario was ‘the great reces-sion’. That’s been averted.It’s going to feel a lot likethe 1980s in the US.”Another private banker is

sceptical that some clientshave learned anything.“They want something thatwill preserve their capitalright now,” he says. “Soonthey will want better returnsand they will forget again.”

A rich and sophisticatedclient wanted to talk aboutwhy his portfolio had per-formed so badly. “He com-plained for an hour, so wesuggested he diversify andtake a very conservativeapproach. We laid out aninvestment strategy for him,very conservative, and hesaid: ‘So how much can I lev-erage this by?’”

Additional reporting byRobin Kwong in Taiwan

Continued from Page 1

Virgin territory in the world of the ultrawealthyIn 2007, as the Indian

stock market enteredthe fifth year of a bullrun that had multiplied

the value of the BombayStock Exchange’s bench-mark Sensitive Index four-fold, a strange competitionbegan to emerge.

The country’s biggest bil-lionaires seemed to beengaged in a competition to

outdo each other on theForbes rich list, which ranksthe country’s wealthy.

The fortunes of tycoonssuch as Mukesh Ambani, thehead of Reliance Industries,India’s biggest private sectorcompany, and Anil Ambani,his younger brother andrival, mushroomed to doubletheir previous levels.

Others made it on to the

list through initial publicofferings that many analystscriticised as being over-valued – the $2.5bn listing,for instance, of DLF, India’slargest real estate company,that helped send KP Singh, aproperty tycoon, rocketingup the list.

The bubble has sinceimploded with the credit cri-sis. The wealth of Mukesh

Ambani has more thanhalved to about $20.8bnwhile his younger brother’sfortune has fallen by nearlytwo-thirds to $12.5bn.

But that was before thewealth management indus-try got the point – India isthe new kid on the blockwhen it comes to privatebanking, matching China forthe speedy growth of its

wealthy and ultra-wealthy.Capgemini and Merrill

Lynch concluded in a study,Asia Pacific Wealth Report:“Although the number ofemerging high net worthindividuals and Ultra-HNWIsin China and India is stillrelatively small, we expectthese and other emergingmarkets to continue to growat double-digit rates and,within 10 years, to surpassthe mature markets.”

The growing importance ofthe subcontinent for wealthmanagers is underlined bythe findings of the report.

The Indian market in 2007was the fastest growing interms of the wealth and pop-ulation-size of rich individu-als in Asia.

The study found that thenumber of wealthy people inIndia increased 23 per centto 167,000 individuals lastyear. The highest growthtook place at the top of theultra-wealthy category in theranks of those with morethan $100m in investableassets.

The growth in China wassimilar, with the wealthygrowing in number by 19.9per cent, with total loot ofabout $100bn.

The number of ultra-richin China eclipsed that ofJapan for the first time,growing at a rate of 22.2 percent. In addition, thenumber of extremelywealthy – those with morethan $100m – increased by

22.9 per cent in 2007. “In2008, we expect the wealthheld by Ultra-HNWIs toeclipse the $1,000bn mark,”the study found.

That may prove optimisticin the current economic cli-mate, with India and Chinawrestling with rapidly slow-ing economies.

Both are reporting a decel-eration in manufacturingand both of their stock mar-kets have been badly hit,with India’s alone downmore than 60 per cent. Small

businessmen may beaffected by the slowdowns,but many believe the middleand ultra-wealthy of the twocountries are relatively insu-lated from the worst effectsof the economic crisis.

Their close relationshipswith their bankers meanthat they are usually able togain access to funds in timesof need.

If they are able to weatherthe present difficulties,China and India’s marketsfor private banking for theultra-rich could yet becomethe most important in the

region, as predicted by thestudy.

Conquering these marketswill be no pushover.

Private bankers say thatChina’s wealthy, forinstance, are still relativelyunfamiliar with the servicesoffered by the industry.

Tight regulations in Chinaalso limit the sophisticationand range of products thatbanks can offer to their cli-ents. While most believe themarket’s importance willgrow with greater liberalisa-tion, it remains an opportu-nity with great potentialrather one that has beenrealised.

India shares some ofChina’s challenges – heavyregulation, particularly capi-tal controls. The market isjust introducing some of thestructured options commonin developing markets, suchas interest rate and currencyfutures. Even short selling isa new phenomenon. Yet thismarket, too, is promisingamid a growing equity cul-ture that most expect to sur-vive the current turmoil.

Indians traditionallyinvested most of their highlevels of savings in gold andproperty. But they areexpected to become moreaggressive in deploying itinto other investments. Adoubling of the amount ofmoney Indians can investoverseas in any given year –to $200,000 – will also helpthe industry.

INDIA AND CHINA

Joe Leahy onopportunitiesamong an everlarger number ofreally rich people

Trick is to find the right team

Recruiting Didier von Daenikento head Barclays privatebanking operations inAsia-Pacific last year was widelyseen as a coup in the wealthmanagement industry.

The British bank lured Mrvon Daeniken from CreditSuisse, where he had beenco-head of Asia-Pacific privatebanking and head of privatebanking in south-east Asia andAustralasia, based in Singapore.

He had been at Credit Suissefor 17 years in Zurich, Geneva,Dubai and Istanbul. Before that,Mr von Daeniken, who is Swiss,had worked for the Red Cross inIraq prior to the first Gulf war.

Barclays, whose origins dateback 300 years, has had awell-established private bankserving its UK home market formany years. However, it has not

been much of internationaloperator until recently and inAsia has lagged behind wealthmanagers such as UBS,Citigroup, HSBC and CreditSuisse

In 2006, it relaunched theBarclays Wealth brand, withglobal ambitions. Last year itsaid it would invest $725m inwealth managers andinfrastructure by the end of thisyear, with about a fifthearmarked for Asia.

At the end of June, theprivate bank was managing£133bn of client assetsworldwide. Globally, Barclays’asset management arm andretail and investment bankshave 25m customers – a big poolin which Barclays Wealth canfish for rich clients.

Mr von Daeniken started hisnew job on June 1 last year,when the credit crisis wassomething that only affected USbanks and Asia-Pacific stockmarkets still had nearly sixmonths of rally ahead of them.A boom in initial publicofferings, especially in China,seemed to create freshmillionaires every day.

Much has changed. Asianstock markets are trading atabout half their levels a yearago. Some big banks havedisintegrated and others havetaken government handouts andguarantees to survive.

Barclays benefited from thecollapse of Lehman Brothers,snapping up its North Americaninvestment banking and capital

markets businesses for $1.75bn.But it did need to raise £7bn

of fresh capital and manyinvestors were angry that itignored the UK government’sbail-out in favour of a moreexpensive deal that offeredMiddle East investorspreferential terms.

However, Mr von Daenikensays he would have still takenthe job, even had he known

what the next 18 months wouldbe like.

The recent recapitalisationmay have been controversialbut, he says, it has left Barclaysas one of the best capitalisedbanks in the industry. “Withhindsight, the fact that we arenot the biggest player today isan advantage. You can movefaster. That’s a good position tobe in.”

India and China are the twomain targets. “We have a strongpresence in India,” Mr Daenikensays. “That will be our focus.”Barclays has a big retailnetwork in the country and,because of the historic ties withBritain, there is high awarenessof the Barclays brand.

The “sheer numbers” ofpotential customers in Chinamake the country an obviousplace to expand, although thereare none of the traditionalfoundations it has in India tobuild on.

Japan is also on the radar.“We would be very interested inpartnering with someone. It’schallenging in Japan. TheJapanese private bank market isunlike others in Asia.”

Analysts say Barclays’expansion will depend on thebank’s ability to attract andretain talent. In recent monthsMr von Daeniken has beefed uphis senior team. He hiredPheabe Chau to head theSingapore team of investmentspecials. She previously workedfor RBS Coutts’ private bankjoint-venture with Bank ofChina in Beijing and Shanghai.

Also from RBS is Nitin Birla,who has been given a brief ofattracting rich south Asiansliving in north Asia to becomeBarclays Wealth clients.Manpreet Singh Gill joined fromICICI Bank in India to be Asiastrategist.

With investment banks layingoff staff, finding good peoplemay become easier. “But thatdoesn’t change the fact thatfinding the right talent iscrucial,” Mr von Daeniken says.Many private bankers areproducts of the boom in thesector in Asia in the past six orseven years.

“Obviously, we have very fewbankers who have seen a whole[economic] cycle. They are inhigh demand.”

INTERVIEWDIDIER VON DAENIKEN

Andrew Wood talksto the head of Barclaysprivate wealth in Asia

Didier von Daeniken: no regrets about the timing of his new job

‘Obviously, we havevery few bankerswho have seen awhole cycle. Theyare in high demand’

The Indian marketin 2007 was thefastestgrowing interms of the wealthand population sizeof the rich in Asia

DECEMBER 5 2008 Section:Reports Time: 2/12/2008 - 16:02 User: graysteph Page Name: AWM2, Part,Page,Edition: AWM, 2, 1

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

FINANCIAL TIMES FRIDAY DECEMBER 5 2008 ★ 3

Asia Wealth Management

Training groundfor a new breed

The main facilities of Singa-pore’s Wealth ManagementInstitute are tucked away ina corner of a city-centreoffice block that houses theheadquarters of the island-republic’s sovereign wealthfund, Temasek Holdings.

In just seven years, theTemasek-run institute hasbecome the main trainingground for a new breed ofAsia’s wealth managers.

“Our main objective is tohelp meet the training needsof the private banking indus-try in Singapore and the restof the region,” says Lim JuinIn, chief operating officer.

The institute trains about150 aspiring private bankersevery year through an arrayof courses, including a certif-icate in private banking, anadvanced wealth manage-ment programme for experi-enced relationship manag-ers.

In addition, it runs an MScin wealth management inconjunction with the SwissFinance Institute and theSingapore Management Uni-versity, or SMU.

About half the studentsare employed in privatebanking, while the rest areswitching careers. “What dif-ferentiates us isn’t just ourpractical curriculum but our

emphasis on the soft skills,because, ultimately, privatebanking is a relationshipbusiness,” says Mr Lim.

“It has an excellent mix ofacademic courses and practi-cal training,” says CarmenLow, 25, an MSc student andan intern at Schroeder’sAsset Management.

Ms Low was a civil serv-ant when she decided on acareer switch. “What’s dif-ferent about this course com-pared with other MBA pro-grammes I looked at is thatit allowed me to internwithin the industry, so I getto try out what I want todo,” she says.

The master’s programmewas designed by the indus-try to meet its growingneeds to serve extremelywealthy people, says FrancisKoh, who heads the pro-gramme at SMU.

Its industry focus isanother plus. “An MBA infinance is too generalised.We focus on just the practi-cal aspects of the wealthmanagement value chain.”

For two weeks every year,SMU’s master class studentsgo to Switzerland toimmerse themselves inSwiss-style private bankingin a programme hosted bythe Swiss Finance Institute.

WMI constantly tweaksthe curriculum to keepabreast of industry needs.Among the topics introducedthis year are Islamic bank-ing and family business.

Courses help studentsunderstand not just balancesheets but also an array of

asset classes from deriva-tives and structured prod-ucts to plain-vanilla equitiesand real estate.

“We teach students how tomanage clients’ expectationsas well as client relation-ships. We also look at legalaspects of wealth manage-ment, ethics as well as riskmanagement,” says Mr Koh.

“Graduates can walk fromthe classroom to a seniorposition in private banking.”

Henrik Mikkelson, analumnus, is head of privatebanking at Commerzbank. Anative of Denmark, he had abusiness degree from Copen-hagen but knew little aboutwealth management. Mid-way through the course, hewas promoted to head Com-merzbank’s private bankingoperations in Singapore.

What did he get out of thecourse? Invaluable network-ing and high-level industrycontacts, for one. “There isno way any other degreecourse would have given methe opportunity to meet somany people from the indus-try,” he says.

WMI is gearing up to be atraining centre for wealthmanagers across Asia ratherthan just Singapore. “Wehave trained people frommore than 30 countries,”says Mr Lim. Over the nextthree to five years, he says,WMI would probably doubleits annual student intake.

“Clearly, as the industryrepairs its battered reputa-tion, it will need a freshbatch of qualified profession-als to keep growing.”

BACK TO SCHOOL

Assif Shameen onan institute thatteaches aspiringprivate bankers

A preference for privacy

As ia’s rapid eco-nomic growth overthe past half cen-tury has created

many wealthy dynasties.Some have set up family

offices to look after theirfinancial affairs, althoughthe idea of professionallyrun businesses to serve thefinancial and personal needsof a family group has beenslower to catch on in theregion than in other parts ofthe world.

The forerunners of today’sfamily offices are thought tohave emerged in Italy duringthe Renaissance, as richmerchants tried to look aftertheir wealth. Some Swiss pri-vate banks also resembledfamily offices when theyfirst developed in the 18thand 19th centuries.

However, the modern fam-ily office really came of agein the 19th century in theUS, when the industrial rev-olution the created dynastieswith enormous wealth.

Tycoons such as Rockefel-ler, Carnegie, and DuPontset up offices which firstlooked after their personalfinancial affairs. Some lateroffered their services tofriends, and then, more for-mally, to other affluent fami-lies.

“In Asia, family offices doexist, but they may not be

very high profile,” says Cyn-thia Lee, executive directorof the Asia-Pacific wealthadvisory group for JPMor-gan’s private bank in HongKong.

“The key functions areadministering investmentsfor the family and, in mostcases, they do things likeconsolidating a number ofinvestment accounts.”

At first glance, they maylook like rivals to privatebanks: who needs an exter-nal wealth manager if youhave your own inhouse dedi-cated office serving suchneeds as tax planning, willwriting and even, in some

cases, helping you to buyart?

However, she says thereare still many services thatfamily offices are not bigenough to provide.

“As a private bank, we canprovide global custody orprovide consolidated state-ments. These are areaswhere we can help.”

As with many aspects ofwealth management, HongKong and Singapore areAsia’s two big hubs for sin-gle family offices, or SFOs,she says.

“In 2006, Hong Kong alsomade tax changes to encour-age family offices to set upin the territory,” she says.

Apart from the tax incen-tives – such as only taxingincome made in Hong Kong– the city has many well-established advisers such aslawyers and is a centre ofexpertise in cross-borderwealth management.

Singapore has establisheditself over the past four orfive years as the centre forsouth-east Asian and Indianfamilies to set up offices.

“We do occasionally havead hoc requests for similarset-ups from mainland Chi-nese,” Ms Lee says. “Theymay have property in Singa-pore, or their kids may go toschool there.”

In the past year, Dubai hasalso emerged as a locationfor some Asian SFOs, espe-cially from India, she says.SFOs can be simple to setup, she says, but significantassets are required to justifythe expense – with at least$300m to $500m globally tomake it worthwhile.

But it can be hard to findpeople with the right rangeof skills, from understandingfinance to diplomacy in plan-ning family conferences anddealing with disagreementsbetween relatives.

“Often they may haveserved the family in anotherprofessional capacity beforejoining the family office, forexample as a lawyer,” shesays.

The family office businessin Asia is relatively under-researched – after all, one ofthe main reasons to set up afamily office rather thanrelying on outside wealthmanagers is to keep the fam-ily’s affairs secret. Few wantto talk to nosy outsiders.

Singapore ManagementUniversity took part in arecent pioneering global sur-vey of SFOs with WhartonBusiness School in the US,IESE Business School ofSpain and Bocconi School ofManagement in Italy. Thatincluded about 40 lengthyinterviews with wealthyindividuals who use SFOsfrom families that spannedmany countries.

All the SFOs managed atleast $100m of assets, andmore than half of themlooked after $1bn or more.“Only a small fraction ofimportant fortunes aredirectly managed by thelargest of the world’s privatebanks,” says Raffi Amit, theWharton professor who ledthe research team.

SFOs have a significant

role to fulfil in this domain,he says, where discretionand preference for privacymean that little is knownabout inner workings andfunctions.

The researchers found sig-nificant differences betweenAsian family wealth andthat in other parts of theworld.

Much of it has been morerecently created, and manyfamilies are still much moreclosely connected to thesource of their fortunes.

“On average, a higher per-centage of affluent familiesin Asia is still involved inbusinesses compared withother regions,” Prof Amitsays.

“It is 40 per cent in Asia,28 per cent in Europe and 24per cent in the Americas.”

FAMILY OFFICES

Dynasties havebeen slow to catchon to dedicatedservices, writesAndrew Wood

Family fortunes: a Qing dynasty reenactment performance. One of the main reasons to set up a family office is to keep affairs secret Getty

Thousands of casesof wine come home

A bunker mentality mightbe bad for the financial mar-kets, but it has been greatnews for Hong Kong’s grow-ing reputation as a globalwine hub.

Crown Wine Cellars,which stores valuable winesfor more than 1,000 clients ina former British army muni-tions depot at Shouson Hill,says the city’s collectionsare coming back home.

“There’s a flight to safetyand what we are seeing is amassive increase in thenumber of collections com-ing back,” says GregoryDe’eb, the general manager.

“The days when peoplebelieved it was important tokeep their collections in Lon-don have been blown out thewindow. What people aresaying is that they wanttheir assets close to them. IfI want money, where can Iliberate these assets?”

In recent years, wine as anasset class has increasinglycemented its position inHong Kong, especiallyamong the pool of mainlandcollectors who want theirwines close and accessible.

The territory’s removal ofa 40 per cent duty on wine inFebruary made conditionsfavourable for wine inves-tors, says Mr De’eb, but noone was prepared for thenumber of bottles comingback. “You have to remem-ber that Hongkongers ownmillions of cases – perhapsbetween 15 and 20 per centof the world’s fine winestocks.”

Before February, collectorsand investors were sending

back 2,400 bottles a month.With the scrapping of duties,the numbers grew to 8,400 amonth. Now with the finan-cial crisis beginning to bite,the number has swollen to20,160 a month, he says.

The advantages of wineare well known. There hasbeen growth of 12 to 15 percent a year in certain coun-tries. As a so-called “wastingasset”, it has tax advantages,and there is always the con-solation of drinking theasset if the price falls.

In May, Acker Merrall &Condit, a wine auction com-pany based in New York,sold HK$64m ($8.2m) worthof wine in its first Asian auc-

tion at the Island Shangri-LaHotel – an event that wasexpected to last six hoursand raise $6m.

Spirited bidding for the 922lots went on until well intothe evening, with the top lot,12 bottles of 1990 Domaine dela Romanée-Conti, fetchingHK$1.89m, the high end ofan estimated range and anauction record for a case ofRomanée-Conti.

Other collectables, such asart, have been promoted asthe savvy investor’s alterna-tive to stock picking andmarket timing. Nick Simu-novic, director of the Gago-

sian Gallery in Hong Kong,says art is still holding itsown in Asia, despite thefinancial crisis. “There is ofcourse some trepidation inthe market and prices arerolling back to 2006 levels,”says Mr Simunovic. “Butseasoned and new collectorscan realise substantial valueat these prices.”

While Sotheby’s AsiaWeek sales in Hong Kong inearly October (and in NewYork in September) ended inunsatisfactory results, thecompany warned that longerterm trends could be harderto predict because the salewas held at a time of “acutestress and uncertainty”.

The global events sur-rounding the end of thecredit bubble created a vola-tile environment, Sotheby’ssaid in a report, adding thatit would be “naive to thinkbuying decisions on Asianart and works of art werenot made in the context ofthis economic uncertainty”.“Clearly, Hong Kong buyershad a reason to be cautious,”the report said.

Nevertheless, Asia Weekin New York had a combinedsale value of $77m acrossnearly a dozen separate salesat Sotheby’s and Christie’s,with nearly 60 per cent ofthe lots at both houses sold.

Even in an uncertain mar-ket, there will always be topprices for hotly contestedlots – an early 18th centuryQing dynasty armchair soldfor $332,500, well above itsestimate of $180,000.

According to Sotheby’s,the Asia Week sales showedthe market pulling in twodirections – high premiumswere paid for quality workswith a connection to theimperial throne and also forworks by contemporary less-established artists which, infuture, could show strongreturns.

ALTERNATIVES

Peter Shadbolt onwhy investors wantto keep theirinvestments close

‘There’s a flight tosafety and amassive increasein collectionscoming back’

Gregory De’eb,Crown Wine Cellars

All SFOs surveyedmanaged at least$100m of assets,and half of themlooked after $1bn

DECEMBER 5 2008 Section:Reports Time: 2/12/2008 - 16:02 User: graysteph Page Name: AWM3, Part,Page,Edition: AWM, 3, 1

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

4 ★ FINANCIAL TIMES FRIDAY DECEMBER 5 2008

Asia Wealth Management

Rich and becoming more important

When a Hong Kongbuyer snapped up a101.27 carat dia-mond the size of a

ping pong ball at a Christie’s auc-tion in the city in May for morethan $6m, many wealth manage-ment professionals in Asiaseemed relieved.

The jewellery sale, whichraised more than $60m, was thebiggest the auction house hadever organised.

The wealthy, it seemed, stillwere rich enough to splash outsome cash despite the ever-

deepening worries about theeffects of the credit crisis and thesteep decline in share prices.

Asians have long had a pen-chant for luxury and conspicuousconsumption.

The World Gold Council saysthat India alone consumed 250tonnes of gold, worth about $5bn,in the third quarter of this year –a rise of nearly a third on thesame period in 2007.

Hong Kong itself, famously,has the highest concentration ofRolls-Royce cars in the world – italso has the highest concentra-tion of households with morethan $1m of investable assets.

Research by Barclays Wealthand the Economist IntelligenceUnit has found 26.4 per cent ofHong Kong families living underone roof fell into this category in2007.

The report predicts that the

proportion will rise to 39.4 percent by 2017.

But by then, Hong Kong’s long-time rival, Singapore, will haveinched ahead to take the numberone spot, with 40.7 per cent of itshouseholds controlling $1m ormore of assets.

Barclays’ latest figures suggestthere are seven countries with1m or more households withinvestable wealth of $1m ormore. Just one of them, Japan, isin Asia.

By 2017 there will be 12 suchcountries or territories, andAustralia, Taiwan and SouthKorea will be on that list. China,which has 22,000 millionairehouseholds, should have 409,00 in2017.

If the forecasts are correct, thatis. As 2008 draws to an end andglobal recession looks imminent,you might be forgiven for taking

some of these projections with apinch of salt.

Sales of luxury goods areweaker – even Asia’s makers offake handbags seem to be havinga hard time.

Asian stock markets have col-

lapsed. Most are down bybetween a half and two-thirds sofar this year. Much of the analy-sis of the distribution of theregion’s rich people is based onfigures for 2007.

Even so, it is worth remember-ing that Japan’s stock marketpeaked at the end of the 1980s,and has since then lost aboutthree-quarters in value.

But for all the talk of lost dec-ades and a moribund financialsystem, the country still has theworld’s second-largest economyand, according to the BostonConsulting Group’s annual globalwealth report, about half ofAsia’s $25,500bn of personalassets under management is con-centrated in Japan.

The economic miracle createdenormous amounts of wealth,and there are still plenty of Japa-nese millionaires.

However, BCG says thatdespite its size, the wealth man-agement market is still “rela-tively immature and difficult toaccess”.

There are large numbers of

people with between $1m and$5m of assets, and 71,000 house-holds with more than that, but“their investment needs are notas well developed as theirwealth”, BCG says.

The personal wealth managedin China may be smaller – about$3,200bn of assets in 2007 com-pared with Japan’s $12,500bn –but has expanded more quickly.Compounded growth was 25 percent a year from 2002 to 2007. Thefigure for Japan in that time was3 per cent, according to BCG.

However, when you look at thenumbers of millionaires, Indiawas the fastest-growing marketin percentage terms, according tothe latest annual World Wealthreport by the French consultantsCapgemini and the US invest-ment bank Merrill Lynch. (Mer-rill Lynch was one of the victimsof the subprime crisis and has

since been absorbed by Bank ofAmerica.)

Overall the world population ofmillionaires grew 6 per cent in2007 to 10.1m, Capgemini and MLsay. In Asia-Pacific, numbersincreased 8.7 per cent to 2.8m andwealth expanded by 12.5 per centto $9,500bn.

India was the world’s fastest-growing market with a 22.7 percent gain to 123,000 millionaires,followed by China, which saw a20.3 per cent increase to 415,000.

Taking 2007’s growth and theweakening of global conditions in2008, Capgemini projects thewealth of Asia Pacific’s million-aires should grow at an annualrate of 7.9 per cent to $13,900bnby 2012.

“Asia-Pacific will replaceEurope as the second-largestrepository of high net worth indi-viduals’ wealth,” it says.

DISTRIBUTION OF WEALTH

Andrew Wood reportson the changingstatistics of theregion’s millionaires

There are largenumbers of people inJapan with $1m to$5m of assets, and71,000 householdswith more than that

31

20

-14

34

-6

7

n.a.

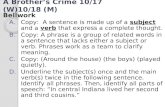

Where the rich live

The territory size shows the earnings of the richest tenth of the population living there, as a proportion of the earnings of the richest tenth living in all territories.

84%of people in Hong Kong disagree with the

statement that designer clothes or luxury

goods are a waste of money

26.4%Percentage of households in Hong

Kong with overall wealth in excess of

US$1m

101.27The weight in carats of the largest

diamond ever sold in Asia, for $6m in

Hong Kong in May

202The number of Rolls-Royce cars sold in

Asia Pacific last year, an increase of 31

per cent compared with the previous year

14The largest-ever single order of

Rolls-Royce Phantoms, for the

Peninsula hotel in Hong Kong

40.7%The proportion of Singapore’s

households expected to have $1m or

more of overall wealth by 2017

0200400600800

India

China

Vietnam

Indonesia

Taiwan

Hong Kong

Japan

Taiwan

Thailand

New Caledonia

New Zealand

Hong Kong

Singapore

Australia

Japan

Net retail gold demand*

The map

2007 (tonnes)

Champagne sold in AsiaMillions of bottles equivalent, 2007

Q3 annual % change

10 8 6 4 2 0

Sources: GFMS/World Gold Council; Barclays Wealth; Capgemini; Merrill Lynch; Economist Intelligence Unit; CIVC; FT Research; Christie’s

* Includes jewellery, coins, and bullion

Russia India South Korea

JapanUS UKGermany China

Australia VietnamIndonesiaTaiwanSingaporeHong Kong

136 123 118

1,5103,028 495826 415

172 1.223717795

power parity and compiled by Danny Dorling at the University of Sheffield in the UK from United Nations Development Programme’s Human Development Report 2004.

1

1

2

2

3

3

4

4

5

5

6

6

7

7

8

8

9

9

10

10

11

11

12

12

13

13

14

14

This map of the world’s wealth is a cartogram. The size of a country is not based on its area, but on how many wealthy individuals there are, and how much they earn.

As a result, the tiny cities of Hong Kong and Singapore, where a quarter of households have investable assets of $1m or more, balloon in size.

Japan, which holds about one-third of Asia’s private wealth, rivals India on the map. Australia, which is a big, but sparsely-populated, country with relatively few rich individuals, shrinks, and much of Africa almost disappears.

This map is based on data for 200 countries on purchasing

Number of individuals worth $1m or more(’000)

www.worldmapper.org

DECEMBER 5 2008 Section:Reports Time: 2/12/2008 - 16:03 User: graysteph Page Name: AWM4, Part,Page,Edition: AWM, 4, 1

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��

��