Wealth tax CA Bhanwar Borana [email protected] +91-8291454999.

39

-

Upload

lionel-lawrence -

Category

Documents

-

view

226 -

download

1

Transcript of Wealth tax CA Bhanwar Borana [email protected] +91-8291454999.

Introduction

Its Direct tax

Governed by Wealth Tax Act, 1957

Charge of wealth-tax (Section 3)

Wealth tax shall be charged for every assessment year in respect of the net wealth on the corresponding valuation date of every individual, Hindu undivided family and company at the rate of one percent of the amount by which net wealth exceeds 30 lakhs.

For assessment year 2015-16, the valuation date is 31.3.2015.

Persons covered u/s 3

Individual

Hindu Undivided Family (HUF)

Company

Exclusion of persons (Section 45)

Section 25 Companies Any co-operative society Any Social club Any Political party Specified Mutual fund Reserve Bank of India (RBI)

Scope of taxation (Section 6)

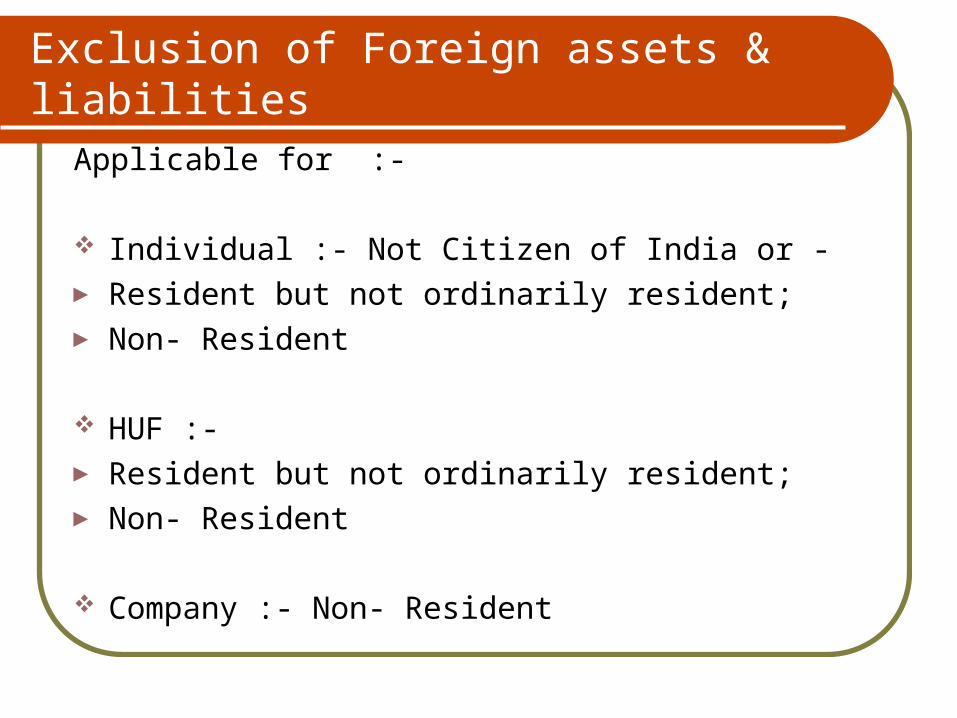

Exclusion of Foreign assets & liabilities

Applicable for :-

Individual :- Not Citizen of India or - Resident but not ordinarily resident; Non- Resident

HUF :- Resident but not ordinarily resident; Non- Resident

Company :- Non- Resident

What is to be excluded

i. The value of the assets and debts located outside India; and

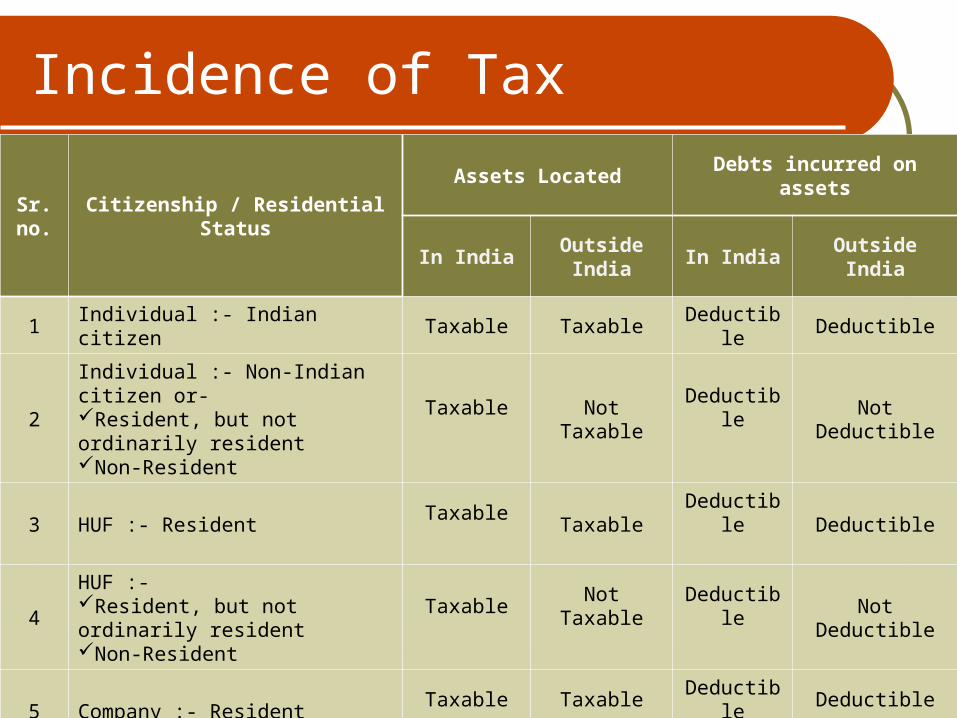

Incidence of Tax

Sr. no.

Citizenship / Residential Status

Assets Located Debts incurred on assets

In IndiaOutside

IndiaIn India Outside India

1 Individual :- Indian citizen Taxable Taxable Deductible Deductible

2

Individual :- Non-Indian citizen &Resident, but not ordinarily residentNon-Resident

TaxableNot Taxable

DeductibleNot Deductible

3 HUF :- ResidentTaxable

TaxableDeductible

Deductible

4

HUF :- Resident, but not ordinarily residentNon-Resident

Taxable Not Taxable DeductibleNot Deductible

5 Company :- ResidentTaxable Taxable Deductible Deductible

6 Company :- Non-ResidentTaxable Not Taxable Deductible

Not Deductible

Sr. no.

Citizenship / Residential Status

Assets Located Debts incurred on assets

In IndiaOutside

IndiaIn India Outside India

1 Individual :- Indian citizen Taxable Taxable Deductible Deductible

2

Individual :- Non-Indian citizen or-Resident, but not ordinarily residentNon-Resident

TaxableNot Taxable

DeductibleNot Deductible

3 HUF :- ResidentTaxable

TaxableDeductible

Deductible

4

HUF :- Resident, but not ordinarily residentNon-Resident

Taxable Not Taxable DeductibleNot Deductible

5 Company :- ResidentTaxable Taxable Deductible Deductible

6 Company :- Non-ResidentTaxable Not Taxable Deductible

Not Deductible

Valuation date [Section 2(q)]

Valuation date in relation to any year for which an assessment is to be made under this Act, means the last day of the previous year as defined in section 3 of the Income-tax Act,1961 i.e., 31st March if an assessment were to be made under that Act for that year.

Where an assessment is made in pursuance of section 19A, then for computation of net wealth of a deceased person, the valuation date would be the adopted in respect of the net wealth of the deceased if he were alive;.

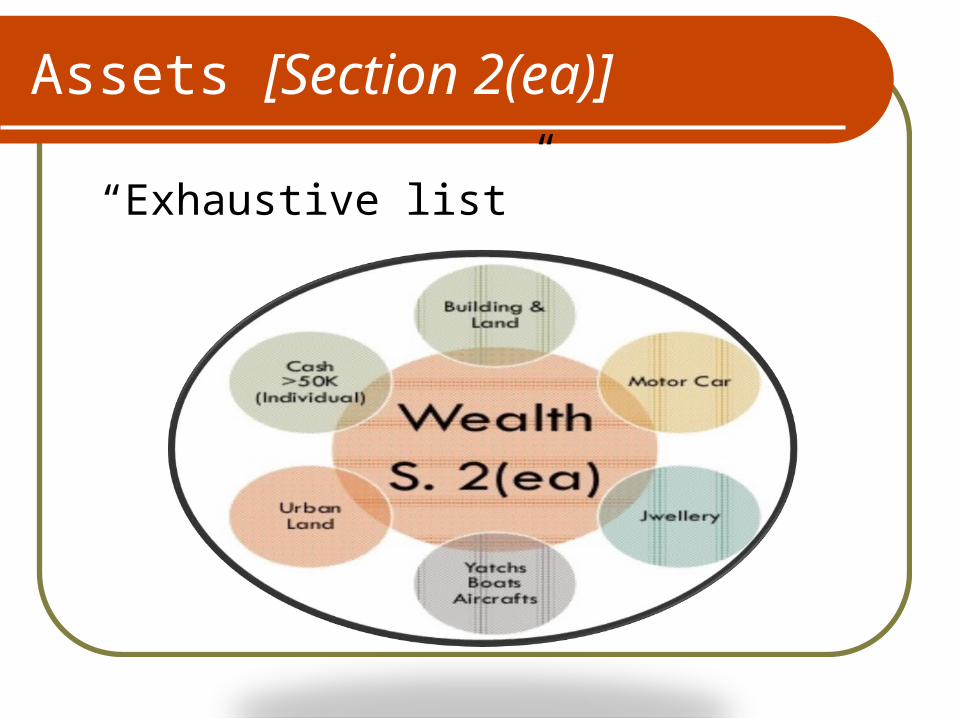

Assets [Section 2(ea)]

“Exhaustive list”

(i) House property

Any building or land appurtenant thereto (House), → Whether used for residential or

→ Commercial purposes or

→ For the purpose of maintaining a guest house or

→ Otherwise including a farm house situated within 25 “km.” from local limits of any municipality

What about ‘Under-constructed property’ ??

CIT vs. Smt. Neena Jain

Exclusion from House property

• A house meant exclusively for residential purposes and which is allotted by a company to an employee or an officer or a director who is in whole-time employment, having a gross annual salary of less than Rs. 10 lakhs;

•Any house for residential or commercial purposes which forms part of stock-in-trade;

•Any house which the assessee may occupy for the purposes of any business or profession carried on by him;

•Any residential property that has been let-out for a minimum period of three hundred days in the previous year;

•Any property in the nature of commercial establishments or complexes

(ii) Motor cars

Other than those used by assessee (Either a or b)- a)In the business of running them on hire :- Eg. Meru cabsb)Held as stock in trade :- Eg. SaiMotors

No where in this Act the term ‘Motor cars’ is defined

(iii) Jewellery, bullion, etc.

Jewellery, bullion and furniture, utensils or any other article made wholly or partly of gold, silver, platinum or any other precious metal or any alloy containing one or more of such precious metals:- Other than those used by the assessee as stock in trade

“Jewellery" includes- (As per the Explanation to the clause)(i) Ornaments made of gold, silver, platinum or any other precious metal or any alloy containing one or more of such precious metals, whether or not containing any precious or semi-precious stones, and whether or not worked or sewn into any wearing apparel;(ii) Precious or semi-precious stones, whether or not set in any furniture, utensils or other article or worked or sewn into any wearing apparel;

Jewellery does not include the Gold Deposit Bonds issued under Gold Deposit Scheme,1999 notified by central government

(iv) Yachts, Boats and Aircrafts

Yachts, boats and aircrafts (other than those used by the assessee for commercial purposes);

What about use of company’s aircraft by director for travelling purpose ??

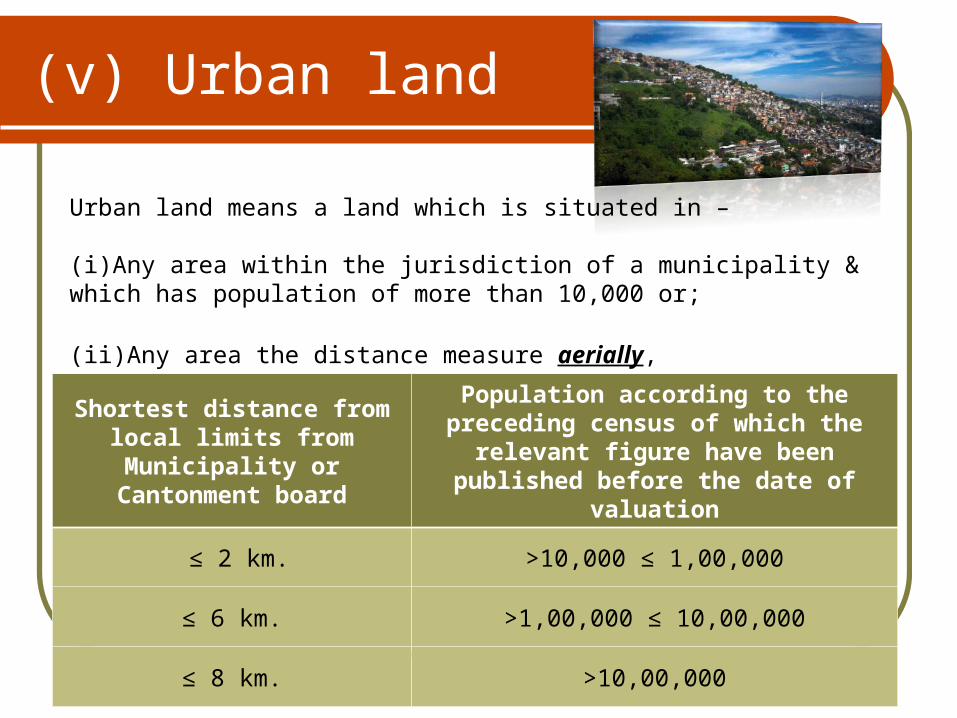

(v) Urban land

Urban land means a land which is situated in –

(i)Any area within the jurisdiction of a municipality & which has population of more than 10,000 or;

(ii)Any area the distance measure aerially,

Shortest distance from local limits from Municipality or

Cantonment board

Population according to the preceding census of which the relevant figure have

been published before the date of valuation

≤ 2 km. >10,000 ≤ 1,00,000

≤ 6 km. >1,00,000 ≤ 10,00,000

≤ 8 km. >10,00,000

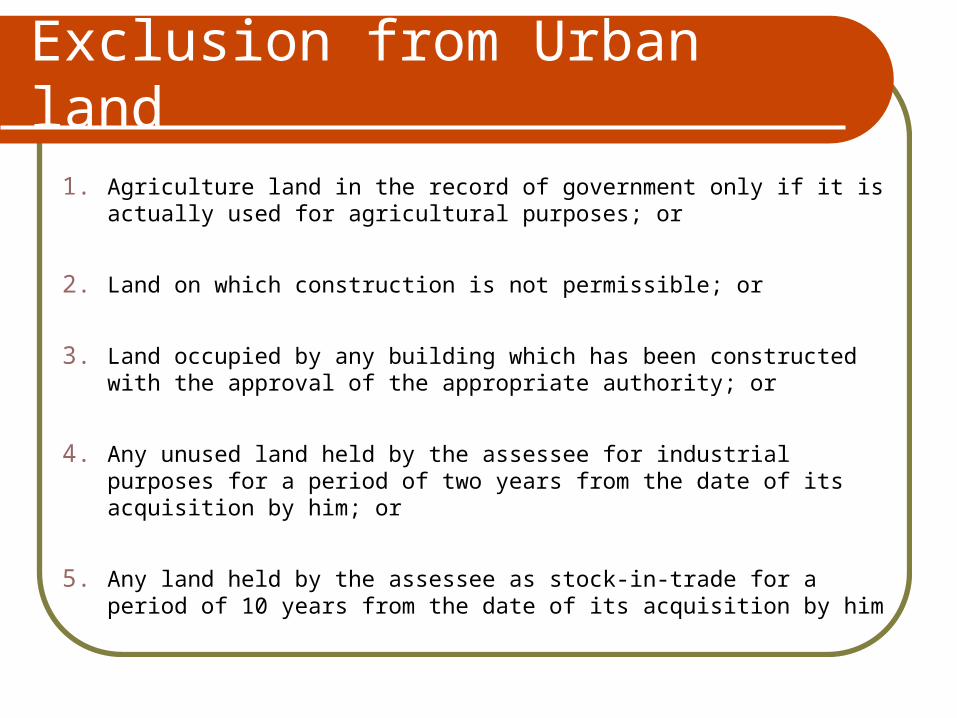

Exclusion from Urban land

1. Agriculture land in the record of government only if it is actually used for agricultural purposes; or

2. Land on which construction is not permissible; or

3. Land occupied by any building which has been constructed with the approval of the appropriate authority; or

4. Any unused land held by the assessee for industrial purposes for a period of two years from the date of its acquisition by him; or

5. Any land held by the assessee as stock-in-trade for a period of 10 years from the date of its acquisition by him

Cash in hand

For Individuals & HUF :- In excess of Rs. 50,000

For Company :- Any amount not recorded in books of accounts

Deemed Assets [Section 4]

• Transfer to spouse/son's wife [u\s 4(1)(a)(i) or 4(1)(a)(iv)] :

Assets transferred by the assessee in the following circumstances for inadequate consideration to the persons mentioned below shall be deemed as assets belonging to him for computation of net wealth - Assets transferred to spouse not in connection with an agreement to live apart; or Assets transferred to a person or association of persons for immediate or deferred benefit of the transferor or transferor's spouse; or Assets transferred to the son's wife; or Assets transferred to a person or an AOP for immediate or deferred benefit of the son's wife.

Deemed Assets… (Continued)• Clubbing of minor's wealth- Assets held by minor child. [u\s 4(1)(a)

(ii)] :

Ø If the marriage subsist: In the hands of the parent whose net wealth is greater before including the minor’s asset,

Ø If the marriage does not subsist: In the hands of the parent who maintains the minor child in the relevant previous year.

Exception:

a. Assets held by a minor child who is suffering from any disability as specified U/s 80U of the Income Tax Act, 1961; or

b. Assets held by a minor married daughter; or

c. Assets acquired by a minor child out of the Income from manual work done by him or income from activity involving application of his skill, knowledge or experience; or

Child means legitimate child and includes adopted children.

Deemed Assets… (Continued)

• Interest in the assets of firm or AOP [u\s 4(1)(b)] :

Where the assessee is a partner in a firm or a member of an AOP, the value of interest the assets of the firm or the AOP is included in the net wealth of the assessee. Where a minor is admitted to the benefits of partnership in a firm, the value of the interest of such minor in the firm shall be included in the net wealth of the parent of the minor in the manner stated above.

Deemed Assets… (Continued)

• Transfer or conversion by member of HUF [u\s 4(1A)] :

Where an individual converts his self-acquired property into property belonging to family or transfers the property to the family for inadequate consideration, it shall deemed to be the asset of the individual. If partition takes place, the converted property as received by the spouse shall be deemed to be the assets of the individual.

Deemed Assets… (Continued)

• Assets transferred under a revocable transfer [u\s 4(5)] : The value of any assets transferred under an irrevocable transfer shall be liable to

be included in computing the net wealth of the transferor as and when the power to revoke arises to him. This implies that the value of any asset transferred under a revocable transfer shall be liable to be included in computing the net wealth.

Revocable transfer means the following transfers in accordance with explanations :- Transfers revocable within a period of 6 years. Transfers revocable during the lifetime of the transferee. Transfers where the transferor continues to derive the benefit from the asset,

directly or indirectly. Transfer of an asset where the transfer deed provides for the retransfer of either

the income or the asset to the assessee. Transfer of an asset where the transfer deed gives the transferor assessee a right

to reassume power over the asset or the income.

Deemed Assets… (Continued)

• Gift by book entries [u\s 4(5A)] :

Gifts of money by book entries made in the books maintained by the assessee to any other person with whom he has business relationship or any other relationship it shall be deemed to be his asset unless the Assessing Officer is satisfied that money has actually been delivered to the other person at the time the entries were made.

Deemed Assets… (Continued)

• Impartible Estate [u\s 4(6)] :

Holder of an impartible estate shall be deemed to be the individual owner of all the properties comprised in the estate.

Deemed Assets… (Continued)

• Building allotted by Housing Society [u\s 4(7)] :

Where the assessee is a member of a cooperative housing society or a company or any association of persons to whom a building or part thereof is allotted or leased to him under a house building scheme, the assessee is deemed to be the owner of such building or part thereof. In determining the value of such building any outstanding installments payable by the assessee to the society towards the cost of such building or part thereof shall be deductible as debts owed by the assessee.

Exemption of Certain Assets [Section 5]

Section Description of Assets

5(1)(i)

Property held under trust for public purpose of charitable/religious nature in India (excluding assets of business other than business carried on by an institution/fund, etc., referred to in section10 (23B), and (23C) and business referred to in section 11 (4A) (a)/(b) of the Income tax Act, 1961;

5(1)(ii) Interest in coparcenary property of HUF;

5(1)(iii) Any 1 building (being official residence) in the occupation of a Ex-Ruler;

5(1)(iv) Jewellery in possession of Ruler, recognized as his heirloom;

5(1)(v)

Money/assets brought by person of Indian origin/citizen of India (returning from abroad for permanent residence) into India and assets acquired out of such money within 1 year preceding date of return and at any time later. Such exemption is available for 7 successive assessment years from the date of his arrival in India.

5(1)(vi)In case of an Individual or a HUF :-(a) A house or a part of house; or(b) A plot of land not exceeding 500 sq.meters in area.

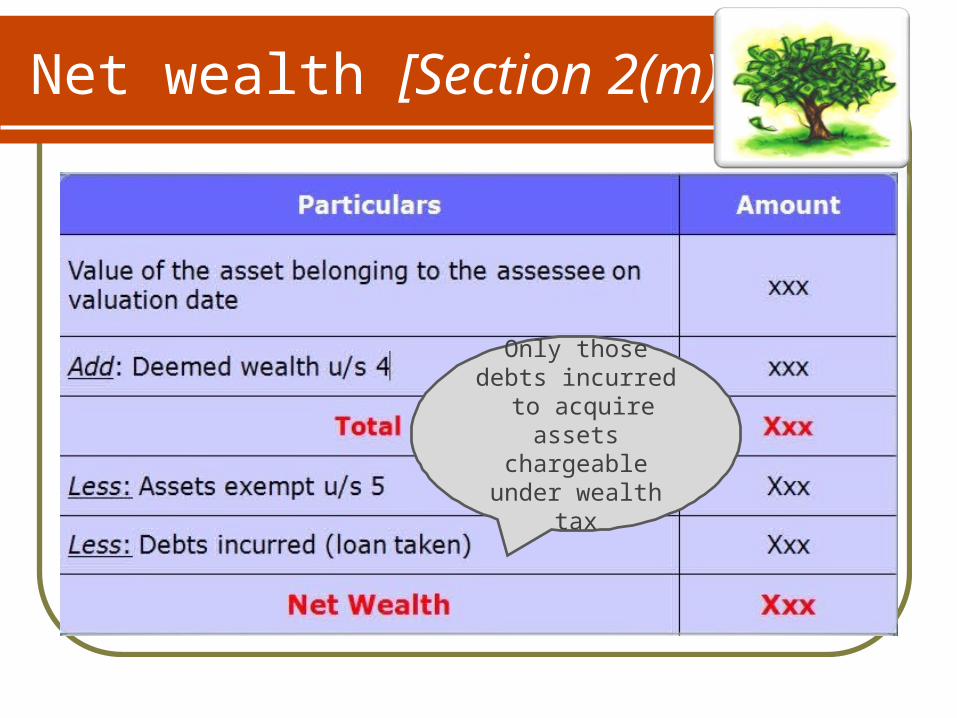

Net wealth [Section 2(m)]

Only those debts incurred to acquire assets chargeable under wealth tax

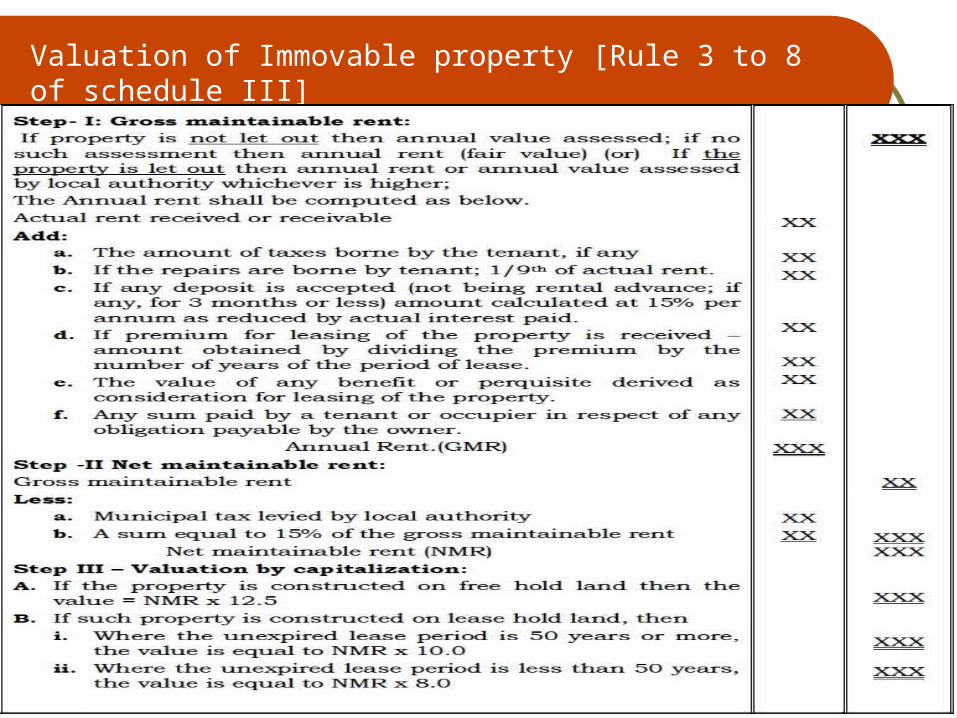

Valuation of Immovable property [Rule 3 to 8 of schedule III]

Interest in firm and Association of Persons (AOP) [Rule 15 & 16]

→ Net wealth of the firm or association of persons on the valuation date shall be first determined as if it were the assessee. Consequently, Rule 16 would apply.

→ The net wealth determined in hands of the firm or association of persons shall be without considering exemptions u/s 5(1).

→ The net wealth equivalent to the capital contribution shall be allocated among the partners in proportion to capital contribution. The residue of the net wealth shall be allocated in accordance with the agreement for distribution of assets in the event of dissolution and in the absence of such agreement, in proportion of their sharing of profits.

→ The assets in respect of which exemptions u/s 5(1) is available shall be deemed to be included in the value of interest of the partner or member in the profit & loss sharing ratio and the provisions of section 5(1) shall apply to him accordingly.

Valuation of Jewellery [Rule 18 & 19]

The value of jewellery shall be estimated to be the price which it would fetch if sold in the open market on the valuation date.

The return of wealth shall be supported by :

i. Where the value of jewellery does not exceed Rs. 5 lakhs on the valuation date, a statement in prescribed form;

ii. Where the value of jewellery exceeds Rs. 5 lakhs, a report of a registered valuer in the prescribed form

Valuation of Other Assets [Rule 20 & 21]

The value of residuary assets for wealth tax purposes shall be estimated to be price which in the opinion of the Assessing Officer it would fetch if sold in the open market on the valuation date.

The Assessing Officer may refer the valuation of any asset to a valuation Officer only if the following two requirements are fulfilled :

i. The valuation is necessary for the purpose of making an assessment.

ii. The market value of the asset is required to be adopted while making such assessment.

Return of Wealth tax

To be filed in Form BB Electronic format

Within due dates specified u/s 139(1) :- 31st July of A. Y. 30th September of A. Y.

No requirement to file ‘Nil return’ [Section 14(2)]

Revised return or Belated return within 1 year from relevant A.Y. or Completion of assessment whichever is earlier [Section 15]

Return to be signed by

1. Individual :-• By himself;• By his representative with valid power of attorney (if absent from India or

not possible to sign);• By his guardian or any other competent person.

2. HUF :-• By Karta;• Any other adult member (if Karta is absent from India or not possible to

sign).

3. Company :-• Managing director;• Any other authorized person with valid power of attorney.

Assessment

Self Assessment [Section 15B]

Scrutiny Assessment [Section 16] Intimation=Within 2 years from end of A.Y. Notice=Within 12 months from end of the month in

which the return is furnished

Best judgment Assessment [Section 16(5)]

Wealth escaping Assessment [Section 17]

Assessment in Special cases

Executor

After partition of HUF

When assets are held by courts of wards, administrators-general, etc.

Charitable trust in specified circumstances

Assets are held by certain association of persons

Persons residing outside India

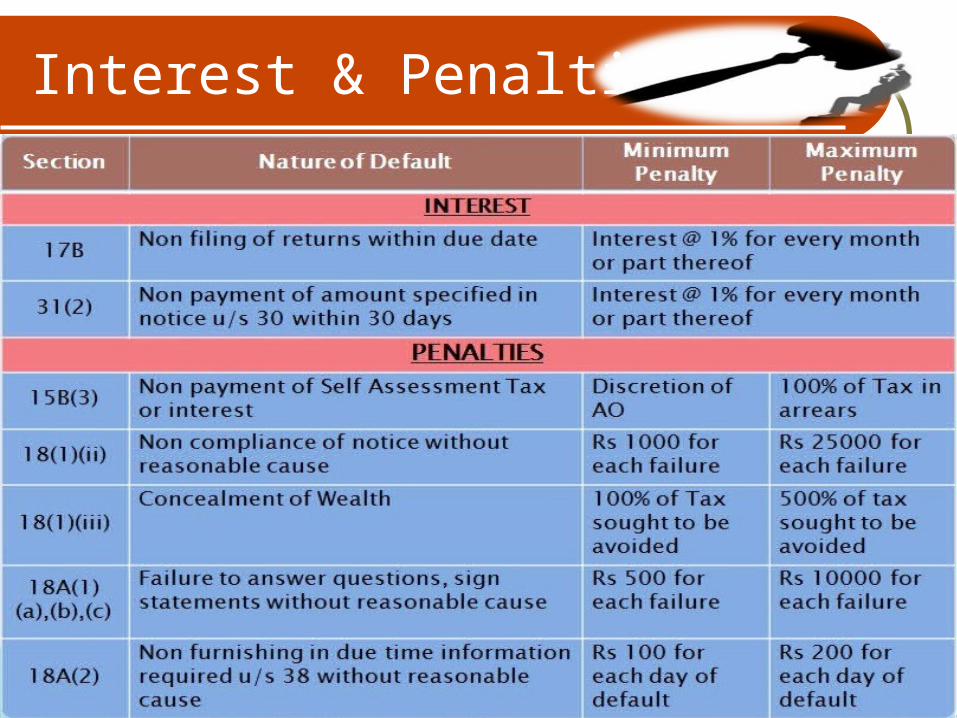

Interest & Penalties

![tworeal4u1@yahoo.com [mailto:tworeal4u1@yahoo.com]clkrep.lacity.org/onlinedocs/2015/15-1368_pc_01-25-16.pdf · From: Cameron Moore [mailto:kobys8@yahoo.com] Sent: Monday, January](https://static.fdocuments.in/doc/165x107/5e34bdff6a95ba262b2e2de7/tworeal4u1yahoocom-mailtotworeal4u1yahoocom-from-cameron-moore-mailtokobys8yahoocom.jpg)