Wealth, money, knowledge: how much do people know?...

45

Wealth, money, knowledge: how much do people know? Where are the gaps? What’s working? What’s next? Presentation to Financial Literacy 09 Retirement Commission, New Zealand Annamaria Lusardi Dartmouth College and NBER June 26, 2009

Transcript of Wealth, money, knowledge: how much do people know?...

Wealth, money, knowledge: how much do people know? Where are the gaps? What’s working? What’s next?

Presentation to Financial Literacy 09Retirement Commission, New Zealand

Annamaria LusardiDartmouth College and NBER

June 26, 2009

Significance

Individuals are increasingly in charge of making saving and investment decisions

Changes in the pension landscape

Financial markets are more complex

Financial mistakes can have devastating consequences

This presentation summarizes a multi-year project on financial literacy and saving

The “great risk shift”

How well equipped are people to make saving and investment decisions?

Scheme of the presentation

How much do people know?Evidence from different surveys

Who knows the least?

Does financial literacy matter?

What to do in the presence of financial illiteracy?

Collecting data on literacy

Financial LiteracyDo people know basic economics/finance?PlanningDo people calculate how much they need to save for retirement? How well do they plan?

Olivia Mitchell (Wharton School) and I devised a module on Financial Literacy & Planning for the 2004 Health and Retirement Study (HRS)

Measuring Financial Literacy (I)

“Suppose you had $100 in a savings account and the interest rate was 2% per year. After 5 years, how much do you think you would have in the account if you left the money to grow?”

i) more than $102; ii) exactly $102; iii) less than $102; iv) don’t know (DK); v) refuse to answer.

To test numeracy and understanding of interest rates, we asked:

Measuring Financial Literacy (II)

“Imagine that the interest rate on your savings account was 1% per year and inflation was 2% per year. After 1 year, would you be able to buy:”

i) more than today with the money in this account; ii) exactly the same as;iii) less than todayiv) DK; v) refuse.

To test understanding of inflation, we asked:

Measuring Financial Literacy (III)

“Do you think the following statement is true or false? Buying a single company stock usually provides a safer return than a stock mutual fund.”

i) true;ii) false; iii) DK; iv) Refuse.

Finally, to test understanding of risk diversification, we asked:

How much do older people know?

NB: Only ONE THIRD (34%) correctly answer all 3 questions; only around HALF (56%) correctly answer Inflation & Compound Interest.

We analyzed the knowledge of people aged 50+:

Scheme of presentation

How much do people know?Evidence from different surveys

Who knows the least?

Does financial literacy matter?

What to do in the presence of financial illiteracy?

Financial Literacy and Age

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

90.00%

≤ 60 75.88% 80.79% 59.95%61-70 67.22% 79.72% 54.01%> 70 57.63% 64.89% 42.61%

Compound Interest Inflation Stock Risk

Correct responses: By Gender

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

90.00%

Male 74.70% 82.20% 59.30%

Female 61.90% 70.50% 47.50%

Compound Interest Inflation Stock risk

Financial Literacy in other surveys

These questions have now been added to many other surveys in the US• NLSY (23-27 years old)• Rand American Life Panel (all

age groups)

These questions have been added to many surveys abroad• The Netherlands• Italy and Germany• Russia• New Zealand

Distribution of Responses to Financial Literacy Questions (%)

NB: Only LESS THAN HALF (45%) correctly answer all 3 questions.

0.0737.515.8646.57Risk diversif.

0.1815.4130.5353.88Inflation

0.125.8714.7679.24Interest rateRefuseDKIncorrectCorrect

Responses

How much do young people know?

We analyzed the knowledge of people between the ages of 23 and 27:

Correct responses: By Gender

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

90.00%

Male 81.79% 59.98% 53.29%Female 76.61% 47.57% 39.62%

interest rate Inflation Stock risk

Debt LiteracyTogether with Peter Tufano(HBS), I designed questions about debt literacy

Relevant given sharp increase in debt

We engaged a market research firm (TNS) to provide timely data

TNS is leader firm in opinion pollingRepresentative sample of the US population

TNS Survey: Compound interest

Suppose you owe $1,000 on your credit card and the interest rate you are charged is 20% per year compounded annually. If you didn’t pay anything off, at this interest rate, how many years would it take for the amount you owe to double?

- 2 years- Under 5 years- 5 to 10 years- More than 10 years- Do not know- Prefer not to answer

Interest compounding Percent2 years 9.6Less than 5 years (correct) 35.95 to 10 years 18.8More than 10 years 13.1Do not know 18.2No answer 4.3

We tested understanding of compound interest:

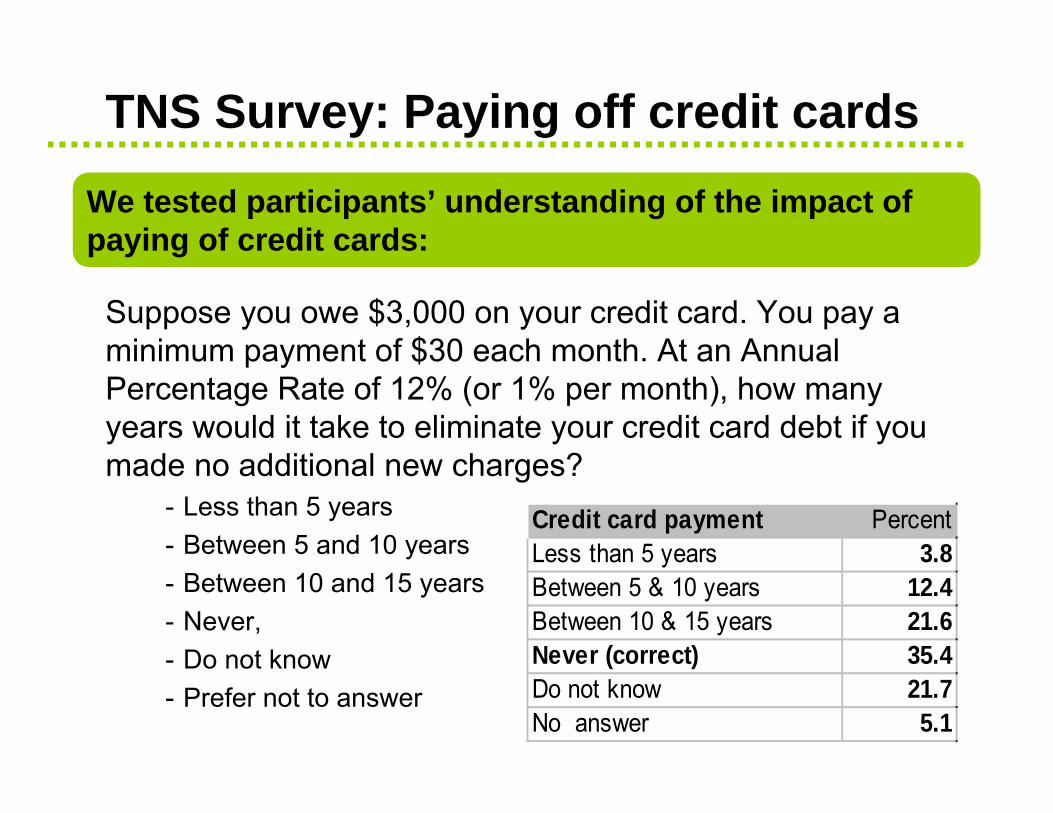

TNS Survey: Paying off credit cards

Suppose you owe $3,000 on your credit card. You pay a minimum payment of $30 each month. At an Annual Percentage Rate of 12% (or 1% per month), how many years would it take to eliminate your credit card debt if you made no additional new charges?

- Less than 5 years- Between 5 and 10 years- Between 10 and 15 years- Never,- Do not know- Prefer not to answer

Credit card payment PercentLess than 5 years 3.8Between 5 & 10 years 12.4Between 10 & 15 years 21.6Never (correct) 35.4Do not know 21.7No answer 5.1

We tested participants’ understanding of the impact of paying of credit cards:

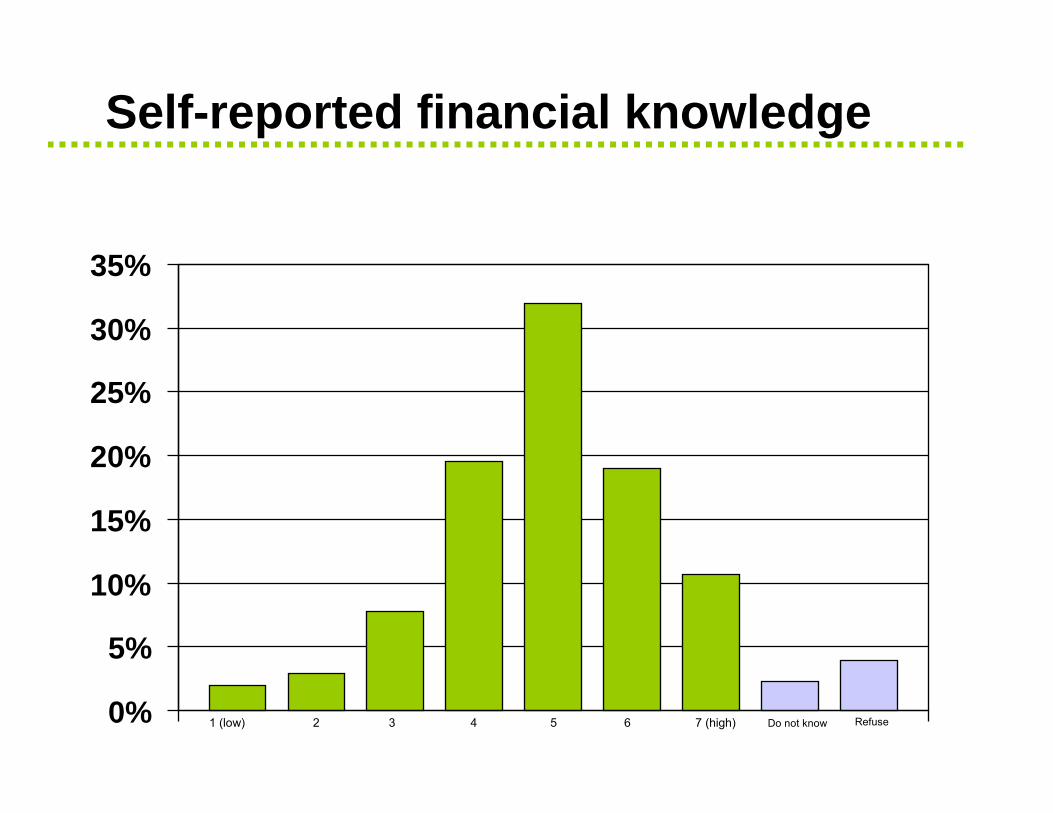

Self-reported financial knowledge

0%

5%

10%

15%

20%

25%

30%

35%

21 (low) 7 (high) Do not know Refuse3 4 5 6

Who know the least?

Question about interest compounding• Only 28.6% answer correctly• 28.3% answer they “do not know”

Question about credit cards• Only 32.3 answer correctly• 30.7% answer they “do not know”

However, the elderly rate themselves highest in term of self-reported literacy• Average score is 5.3!

TNS survey results from among the elderly showed several important findings

Who has lower debt literacy?

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Correct answer Do not knowMale Female

Percent answering credit card question correctly or “do not know” by gender

The debt literacy question showed marked differences between men and women:

Two Takeaway Points

Financial literacy should not be taken for granted

Illiteracy is widespread

Financial literacy varies widely among demographic groups.

Scheme of presentation

How much do people know?Evidence from different surveys

Who knows the least?

Does financial literacy matter?

What to do in the presence of financial illiteracy?

Does Financial Literacy Matter?

Consumers may not need financial knowledge because they can consult “experts” or get help when making financial decisions

Even without being mechanics, we all drive cars

Consumers may make good decisions even without knowledge or advanced knowledge

We can be good at playing pool even without knowing physics

Financial Literacy and Advice

6.97.38.219.7Other

12.47.66.66.3Fin. Information on Internet

0.51.10.30.2Fin. Computer programs

24.127.523.619.4Professional advisers

1.45.03.64.0Advertisement on TV

6.211.36.76.6Brochures from my bank

17.09.77.62.1Financial magazines, books

13.710.66.01.1Information from newspapers

17.919.937.440.7Parents, friends, acquaintances4th (high)3rd2nd1st (low)

Levels of Financial literacy

Where do people turn for financial advice?

Retirement planning and net worth in 1992 ($2004) Age : 51-56 in 1992

Total net worthdistribut.

% ofsample

25th

PercentileMedian 75th

PercentileMean

Planning (1992 HRS): How much have you thought about retirement?

Hardly at All

32.0 10,098 76,906 200,613 224,310

A Little 14.3 37,699 126,562 290,149 343,145

Somewhat 24.8 72,032 173,753 367,298 340,681

A Lot 28.9 71,393 173,686 356,796 353,523

Retirement planning and net worth in 2004 ($2004) age 51-56

Total net worthdistribut.

% ofsample

25th

PercentileMedian 75th

PercentileMean

Planning (2004 HRS): How much have you thought about retirement?

Hardly at All

27.7 10,300 84,100 289,900 350,770

A Little 16.7 59,700 172,000 390,500 357,215

Somewhat 27.9 56,000 189,000 450,000 367,832

A Lot 27.7 55,000 199,000 467,600 508,269

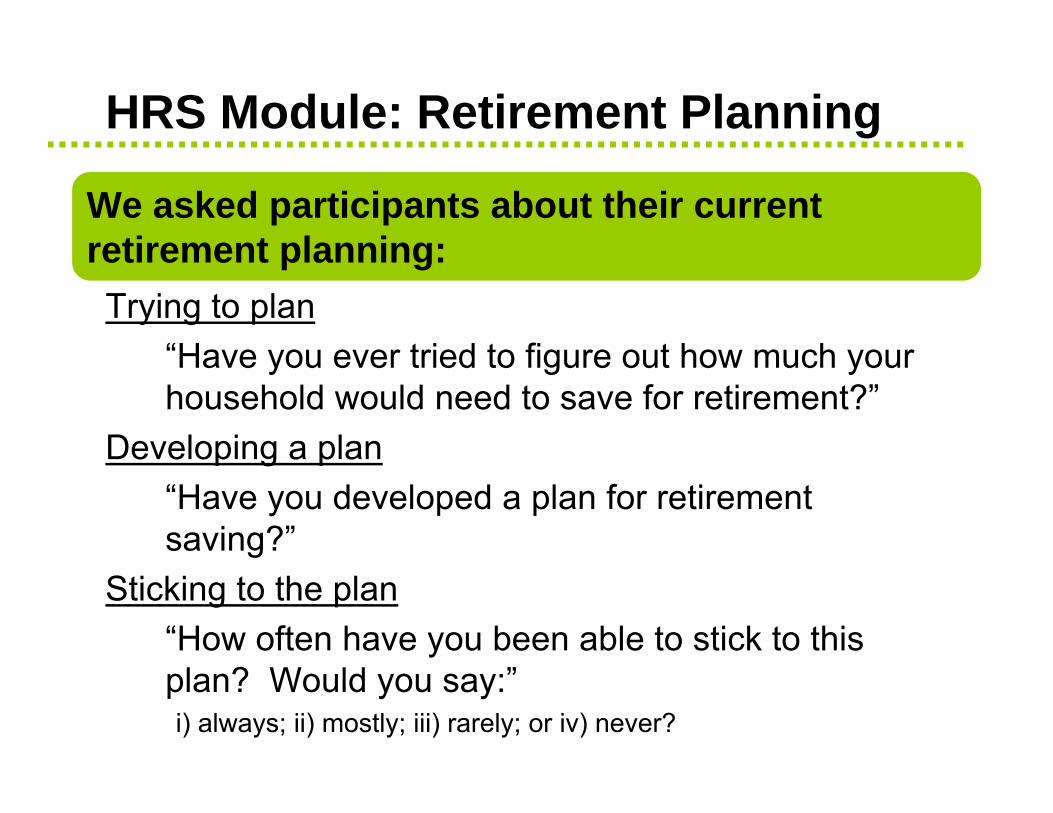

HRS Module: Retirement Planning

Trying to plan“Have you ever tried to figure out how much your household would need to save for retirement?”

Developing a plan“Have you developed a plan for retirement saving?”

Sticking to the plan“How often have you been able to stick to this plan? Would you say:”i) always; ii) mostly; iii) rarely; or iv) never?

We asked participants about their current retirement planning:

HRS Module: Findings

Tried: Have you ever tried to figure out how much your household would need to save for retirement?

Yes (31.1%) No (67.8%)Developed a plan Have you developed a plan for retirement saving?

Yes (58.4%) More or Less (9.0%) No (32.0%)

Stuck to the plan How often have you been able to stick to the plan?

Always (37.7%) Mostly (50.0%) Rarely 8% Never 2.6%

Depending on whether participants had tried to plan, results varied:

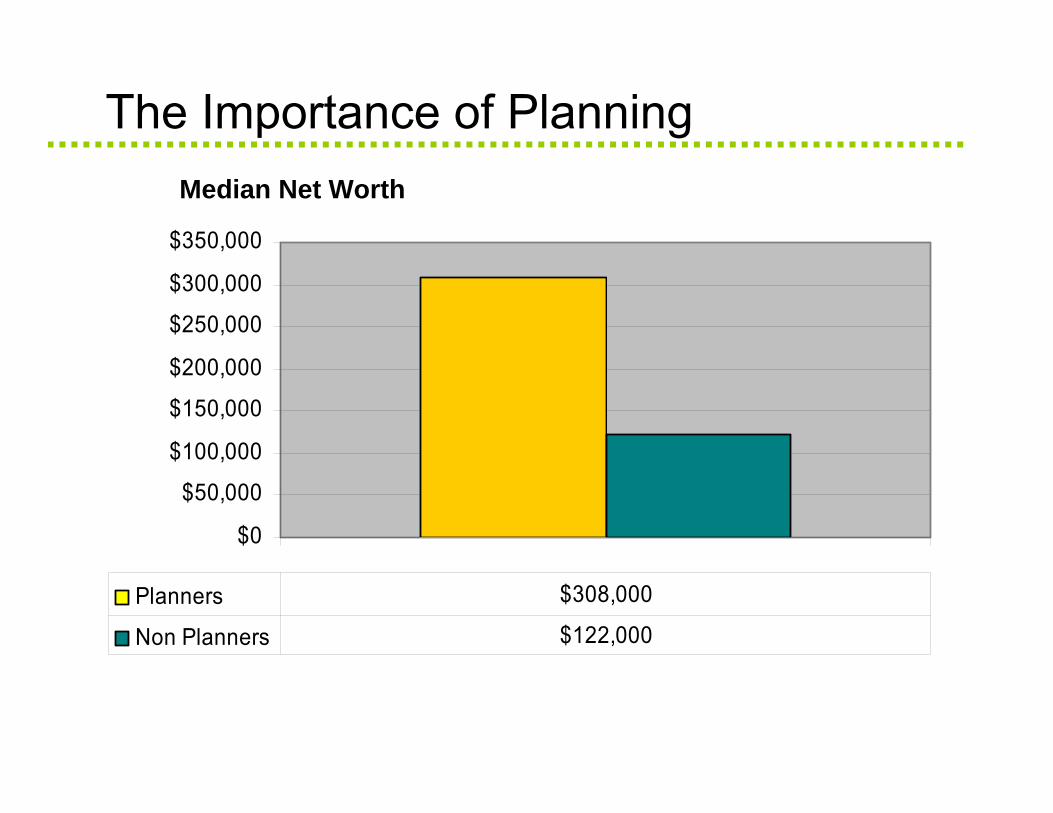

HRS Module: Prevalence of planners

The Importance of PlanningMedian Net Worth

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

$350,000

Planners $308,000

Non Planners $122,000

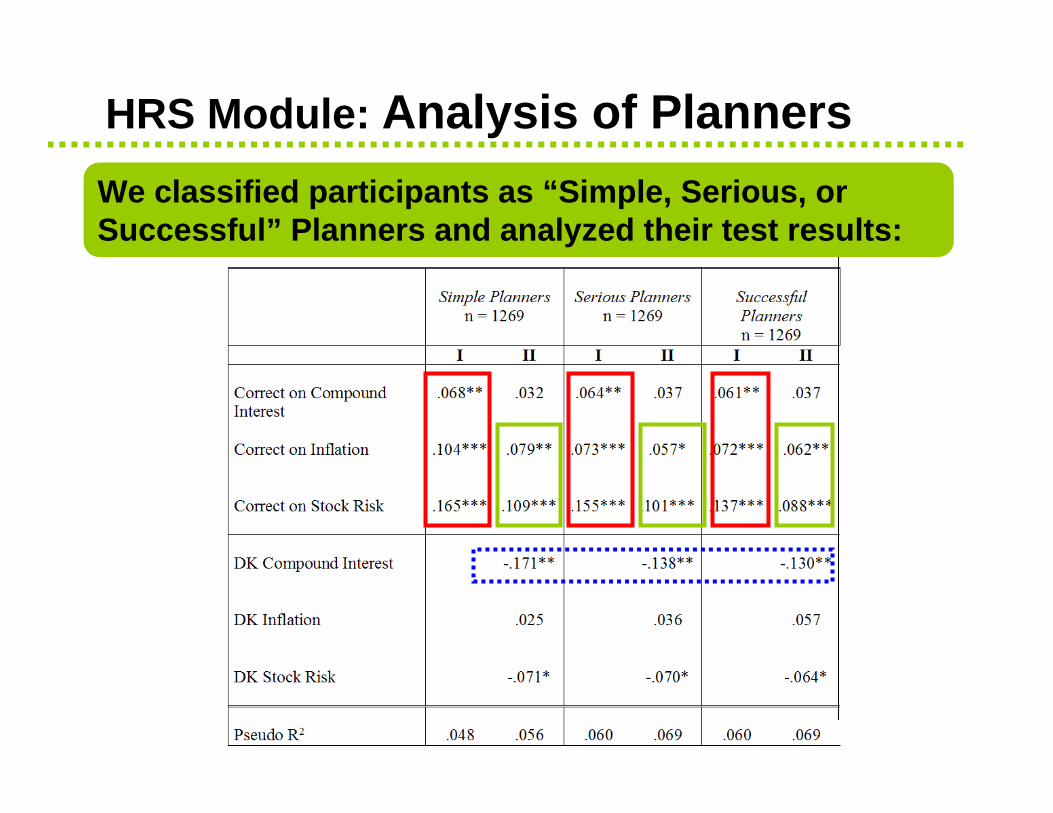

HRS Module: Analysis of PlannersWe classified participants as “Simple, Serious, or Successful” Planners and analyzed their test results:

Information & calculations

The building blocks

Planning

Wealth

The cost of ignorance

• High cost debt

• No stocks

• Lack of saving

Takeaway Points

Financial literacy influences behavior. Those with low literacy:• are more likely to use family and friends as

sources of advice• are less likely to plan for retirement and

consequently accumulate less wealth

In other work using Dutch data I show that those with lower literacy are less likely to invest in stocks• This finding is now confirmed in US data

Table of contents

How much do people know?Evidence from different surveys

Who knows the least?

Does financial literacy matter?

What to do in the presence of financial illiteracy?

What to do given widespread illiteracy?

The Dartmouth Project• Simplify financial

decisions• Provide information and

advice• Target specific groups• Use communication that

does not rely on figures and numeracy

The Dartmouth Project: Planning Aid

Together with a Tuck School of Business Marketing professor, I designed a planning aid intended to help college staff enroll in the college supplementary retirement account (SRA)

Most people plan on electing a supplemental retirement account, but feel they don’t have the time or information right now. We have outlined 7 simple steps to help you complete the election process. It will take between 15 – 30 minutes, from start to finish. It will take less time for you to start to insure your future than it takes you to unload your dishwasher!

Don’t give up! Contact the Benefits Office (6-3588) if for any reason you could not complete the online application.

It takes no time to prepare for your lifetime!

The Dartmouth Project: Planning Aid

Program Effectiveness

166 44.7% 21.7%7-StepPlanning aid

210 28.9% 7.3% Control Group

Number of Observations

60 days After Hire

30 days After Hire

There was a sharp increase in savings enrollment within 30 days of hiring among participants who received the brochure, and the number who enrolled within 60 nearly doubled:

Other Ideas

Provide incentives to become literate (the UK Child Trust Fund)

Have financial education in school

Provide information from “experts” and make it widely available

Additional programs to increase financial literacy and saving rates:

Recommendations

Simplify decision-makingStep-by-step approach

Use effective communication:Stories, testimonialsAs simple as a traffic light!

The Financial Literacy Initiative

A survey on financial capability for the U.S. Treasury

A new survey on risk literacy

I have a blog dedicated exclusively to financial literacy

I have several financial literacy projects underway, in addition to continued research on the topic:

My new book

My new book has recommendations on how to address the retirement savings crisis

Do you want to read more?

Other papers I have written on this topic are available on my webpage:http://www.dartmouth.edu/~alusardi

Initiatives in progress dedicated to women

For more information: