Wärtsilä - Q4 & Full Year Results 2015

36

Result presentation 2015, 27 January 2016 Jaakko Eskola, President & CEO Wärtsilä Corporation

-

Upload

waertsilae-corporation -

Category

Investor Relations

-

view

370 -

download

1

Transcript of Wärtsilä - Q4 & Full Year Results 2015

Result presentation 2015, 27 January 2016

Jaakko Eskola, President & CEO

Wärtsilä Corporation

Highlights 2015

27 January 2016 ©Wärtsilä2

• Order intake EUR 4,932 million, -3%

• Net sales EUR 5,029 million, +5%

• Book-to-bill 0.98 (1.06)

• EBIT EUR 612 million, 12.2% of net sales

(EUR 569 million or 11.9%)

• EBITA EUR 643 million, 12.8% of net sales

(EUR 594 million or 12.4%)

• Cash flow from operating activities EUR 255 million (452)

• Order book at the end of the period EUR 4,882 million, +8%

• Earnings per share EUR 2.25 (1.76)

• Dividend proposal EUR 1.20 per share

EBIT is shown excluding non-recurring items.

EBITA is shown excluding non-recurring items and purchase price allocation amortisation.

0

200

400

600

800

1 000

1 200

1 400

1 600

1 800

Q4/2014 Q4/2015

Year to date order intake supported by Services

Fourth quarter development

3

0

500

1 000

1 500

2 000

2 500

3 000

3 500

4 000

4 500

5 000

5 500

2011 2012 2013 2014 2015

MEUR

MEUR

Q1-Q3 Q4

-8%

-27%

1,5221,403

1%

2%

Energy

Solutions

Marine

Solutions

Services

27 January 2016 ©Wärtsilä

1,549

0

500

1 000

1 500

2 000

2 500

3 000

3 500

4 000

4 500

5 000

5 500

2011 2012 2013 2014 2015

0

200

400

600

800

1 000

1 200

1 400

1 600

1 800

Q4/2014 Q4/2015

Net sales developed in line with expectations

4

MEUR

MEUR

3%

10%

8%

-14%

1,590

27 January 2016 ©Wärtsilä

5%

Q1-Q3 Q4

Energy

Solutions

Marine

Solutions

Services

Fourth quarter development

5

Net sales by business 2015

Marine Solutions

34% (36)

Energy Solutions

22% (24)

Services

43% (41)

27 January 2016 ©Wärtsilä

1.07 1.05 1.05 1.06 0.98

0,0

0,2

0,4

0,6

0,8

1,0

1,2

0

500

1 000

1 500

2 000

2 500

3 000

3 500

4 000

4 500

5 000

5 500

2011 2012 2013 2014 2015

27 January 2016 ©Wärtsilä6

Book-to-bill ratio

MEUR

Order intake Net sales Book-to-bill

0

500

1 000

1 500

2 000

2 500

3 000

3 500

31.12.2014 31.12.2015

Delivery next year Delivery after next year

27 January 2016 ©Wärtsilä7

Order book distribution

MEUR

11.1% 10.9%11.2%

11.9%12.2%

0%

2%

4%

6%

8%

10%

12%

14%

0

100

200

300

400

500

600

700

2011 2012 2013 2014 2015

27 January 2016 ©Wärtsilä8

Operating result and profitability

MEUR

EBIT is shown before non-recurring items. Figures for 2011-2013 include both discontinued and continuing operations.

EBIT EBIT%

Energy Solutions

0

2 000

4 000

6 000

8 000

10 000

12 000

14 000

16 000

18 000

Q1

/20

12

Q2

/20

12

Q3

/20

12

Q4

/20

12

Q1

/20

13

Q2

/20

13

Q3

/20

13

Q4

/20

13

Q1

/20

14

Q2

/20

14

Q3

/20

14

Q4

/20

14

Q1

/20

15

Q2

/20

15

Q3

/20

15

Q4

/20

15

MW

27 January 2016 ©Wärtsilä10

Energy Solutions’ quotation activity on a high level

Liquid fuel

Gas

Multi-fuel

0

200

400

600

800

1 000

1 200

1 400

1 600

1 800

2011 2012 2013 2014 2015

Energy Solutions’ order intake

27 January 2016 ©Wärtsilä11

MEUR

IPP’s

(Independent

Power Producers)

Utilities

Industrials

Review period developmentTotal EUR 1,009 million (1,293)

Review period order intake

by fuel in MW

Gas

46%Oil

54%

Q1-Q3 Q4

27 January 2016 ©Wärtsilä12

Energy Solutions’ orders globally

Americas 638 (686)

Asia 299 (394)

Africa and Middle East 457 (639)

IPP’s

Utilities

Industrials

Europe 1,042* (769)

418220

254137

65

980

Order intake 2015: 2,436 MW (2,489)

584

165103

31

*Turkish owners contributed to the high level of activity in Europe.

Enabling the transition to a sustainable power system

The flexibility and efficiency of

Wärtsilä’s Smart Power

Generation power plants is

gaining interest in the USA

with several orders received

for peaking and renewable

support power plants

during 2015.

Market for gas and liquid fuel power plants, <500 MW

1-9/2014 1-9/2015

Market data includes all Wärtsilä power plants and other manufacturers’ gas and liquid fueled gas turbine based power plants with prime movers above 5 MW,

as well as estimated output of steam turbines for combined cycles. The data is gathered from the McCoy Power Report.

Other combustion engines not included. In engine technology Wärtsilä has a leading position.

<500 MW market volume: 17.0 GW (16.5), +3%

Total market volume: 43.9 GW (37.7), +16%

GE

55.1%

MHI

14.6%

Siemens

12.7%

Wärtsilä

10.5%

Ansaldo

3.6%

Alstom

1.8%Other GT’s

1.8%

GE

38.8%

Siemens

25.2%

MHI

19.8%

Wärtsilä

9.9%

Ansaldo

5.5%

Other GT’s

0.8%

27 January 2016 ©Wärtsilä14

Marine Solutions

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

4,0

4,5

5,0

0

50

100

150

200

250

01

.09

03

.09

05

.09

07

.09

09

.09

11

.09

01

.10

03

.10

05

.10

07

.10

09

.10

11

.10

01

.11

03

.11

05

.11

07

.11

09

.11

11

.11

01

.12

03

.12

05

.12

07

.12

09

.12

11

.11

01

.13

03

.13

05

.13

07

.13

09

.13

11

.13

01

.14

03

.14

05

.14

07

.14

09

.14

11

.14

01

.15

03

.15

05

.15

07

.15

09

.15

11

.15

Mill

ion C

GT

*

Num

ber

of

vessels

Merchant Offshore Cruise and Ferry Special vessels 3 months moving average in CGT

27 January 2016 ©Wärtsilä16

Vessel contracting activity remains low

Source: Clarkson Research Services, figures exclude late contracting

* CGT= gross tonnage compensated with workload

*

12.1

5

0

300

600

900

1 200

1 500

1 800

2011 2012 2013 2014 2015

Marine Solutions’ order intake

27 January 2016 ©Wärtsilä17

Review period development

Total EUR 1,599 million (1,746)

Offshore

8%

Traditional merchant

18%

Special vessels

10%

Others

6%

Gas carriers

38%

Cruise & Ferry

15%

Navy

4%

MEUR

Q1-Q3 Q4

0

100

200

300

400

500

600

700

Q1/2

010

Q2/2

010

Q3/2

010

Q4/2

010

Q1/2

011

Q2/2

011

Q3/2

011

Q4/2

011

Q1/2

012

Q2/2

012

Q3/2

012

Q4/2

012

Q1/2

013

Q2/2

013

Q3/2

013

Q4/2

013

Q1/2

014

Q2/2

014

Q3/2

014

Q4/2

014

Q1/2

015

Q2/2

015

Q3/2

015

Q4/2

015

27 January 2016 ©Wärtsilä18

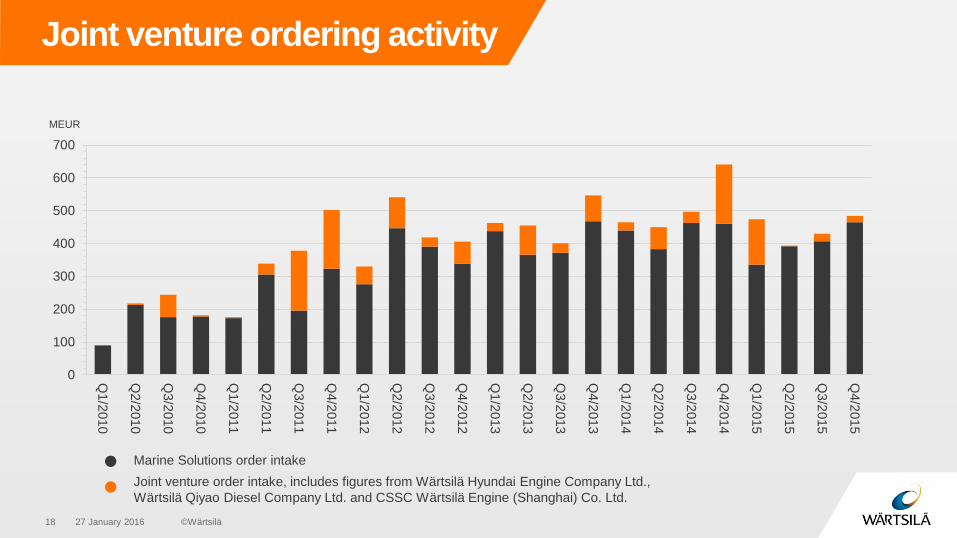

Joint venture ordering activity

Marine Solutions order intake

Joint venture order intake, includes figures from Wärtsilä Hyundai Engine Company Ltd.,

Wärtsilä Qiyao Diesel Company Ltd. and CSSC Wärtsilä Engine (Shanghai) Co. Ltd.

MEUR

27 January 2016 ©Wärtsilä19

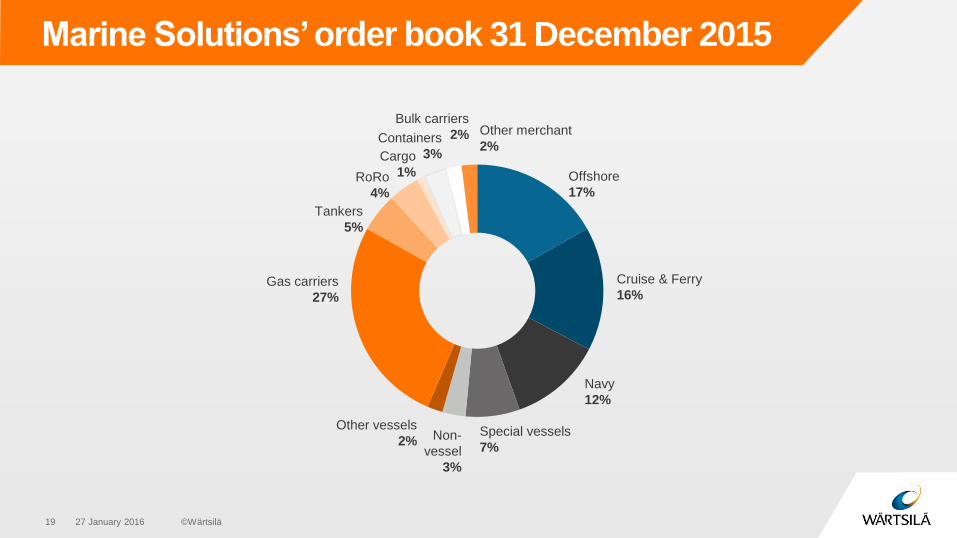

Marine Solutions’ order book 31 December 2015

Offshore

17%

Special vessels

7%

Navy

12%

Cruise & Ferry

16%Gas carriers

27%

Non-

vessel

3%

Tankers

5%

RoRo

4%

Other merchant

2%Containers

3%

Bulk carriers

2%

Cargo

1%

Other vessels

2%

Marine markets shifting towards gas Increased environmental awareness

and the regulatory environment is

driving interest in gas as a marine

fuel in the broader marine

markets. Wärtsilä’s proven gas

engine technology and

gas handling systems

enable us to support our

customers with integrated

solutions.

Strong position in marine engine market

Medium-speed main engines Auxiliary engines

27 January 2016 ©Wärtsilä21

Wärtsilä’s market shares are calculated on a 12 months rolling basis, numbers in brackets are from the end of the previous quarter.

The calculation is based on Wärtsilä’s own data portal.

Wärtsilä

59% (63)

Others

18% (16)

MAN D&T

16% (8)

Caterpillar

7% (13)

Total market volume last 12 months:

3,246 MW (4,519)

Wärtsilä

12% (9)

Total market volume last 12 months:

4,668 MW (3,986)

Others

88% (91)

Services

Services net sales all time high

27 January 2016 ©Wärtsilä23

0

200

400

600

800

1 000

1 200

1 400

1 600

1 800

2 000

2 200

2 400

2011 2012 2013 2014 2015

-3%

0

100

200

300

400

500

600

700

Q4/2014 Q4/2015

5% 5% 13%

MEUR

MEUR

564

10%

619

Fourth quarter development

Q1-Q3 Q4

27 January 2016 ©Wärtsilä24

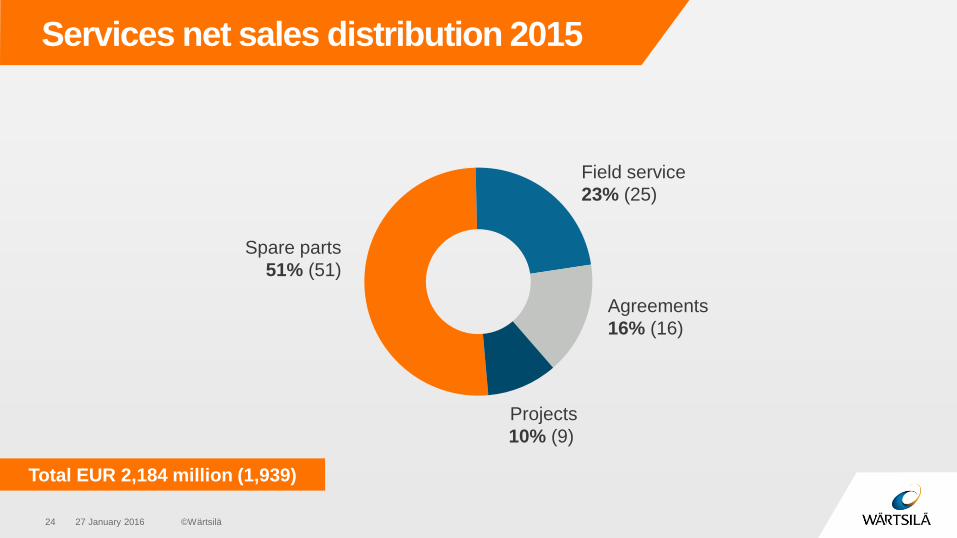

Services net sales distribution 2015

Spare parts

51% (51)

Field service

23% (25)

Projects

10% (9)

Agreements

16% (16)

Total EUR 2,184 million (1,939)

Services distribution per business 2015

Net sales

Total EUR 2,184 million

Installed base

Total 181,000 MW

27 January 2016 ©Wärtsilä25

Marine

Solutions

Energy

Solutions

Energy

Solutions

Marine

Solutions

2-stroke

Marine Solutions

4-stroke

0%

5%

10%

15%

20%

25%

30%

0

2 000

4 000

6 000

8 000

10 000

12 000

14 000

2009 2010 2011 2012 2013 2014 2015

MW

27 January 2016 ©Wärtsilä26

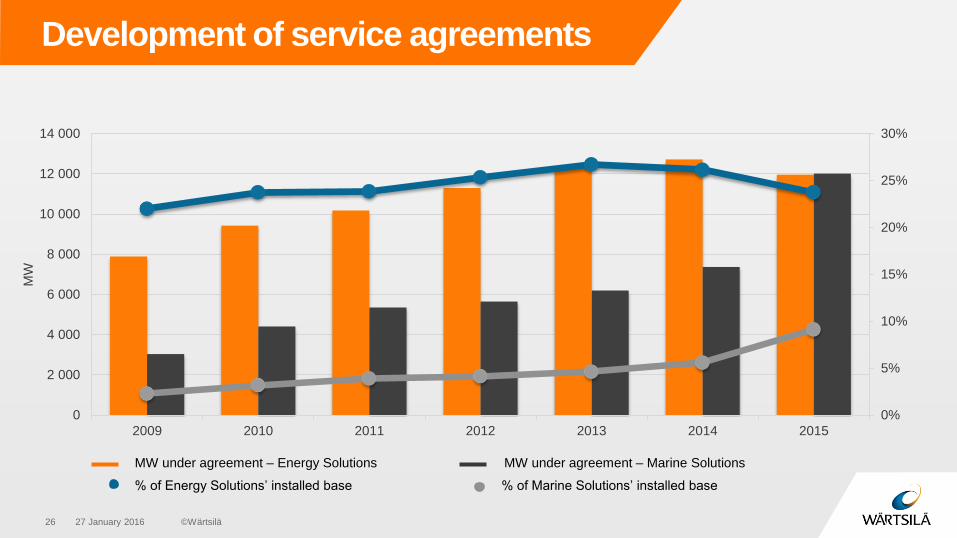

Development of service agreements

MW under agreement – Energy Solutions MW under agreement – Marine Solutions

% of Marine Solutions’ installed base% of Energy Solutions’ installed base

A lifecycle approach

The focus on optimising

maintenance and performance,

and the shift to gas based

technology in the marine

industry is increasing interest

in long-term service

agreements.

Financials

0

100

200

300

400

500

600

700

2011 2012 2013 2014 2015

27 January 2016 ©Wärtsilä29

Cash flow from operating activities

MEUR

Working capital affected by timing of power plant deliveries

27 January 2016 ©Wärtsilä30

235

465

313251

543

5.6%

9.8%

6.8%5.2%

10.8%

0%

5%

10%

15%

20%

25%

0

200

400

600

800

1 000

1 200

1 400

1 600

2011 2012 2013 2014 2015

MEUR

Working capital Total inventories Advances received Working capital / Net sales

Gearing impacted by working capital build up and L-3 MSI acquisition

0,00

0,10

0,20

0,30

0,40

0,50

2011 2012 2013 2014 2015

27 January 2016 ©Wärtsilä31

* Dividend 2015 - Proposal of the Board

27 January 2016 ©Wärtsilä32

EPS and dividend per share

EPS Dividend

0,0

0,5

1,0

1,5

2,0

2,5

2011 2012 2013 2014 2015*

2.25

1.20

Market outlook

Energy Solutions

The market for liquid and gas fuelled

power generation is expected to remain

challenging as economic uncertainty

continues. The megatrend towards

distributed, flexible, gas-fired power

generation continues to gain ground

globally.

27 January 2016 ©Wärtsilä33

Marine Solutions

The outlook for the shipping and

shipbuilding markets remains

challenging. Oversupply is limiting

demand for newbuild vessels and low

oil prices continues to impact

investments in offshore exploration and

development. Gas carrier contracting is

expected to remain at a normalised

level and the outlook for the cruise and

ferry segment remains positive.

Services

The service market outlook is positive

with growth opportunities in selected

regions and segments. Customers in

both the marine and power plant

markets continue to show healthy

interest in long-term service

agreements.

Prospects for 2016

Wärtsilä expects its net sales

for 2016 to grow by 0-5% and

its operational profitability

(EBIT% before non-recurring

items) to be 12.5-13.0%.

Wärtsilä’s strategy

IR Contact:

Natalia Valtasaari

Director, Investor & Media Relations

Tel. +358 (0) 40 187 7809

E-mail: [email protected]

Thank you