W. BentzA&MIS 5251 Agenda - Session 20 Continue our discussion of transfer pricing Talk about review...

49

W. Bentz A&MIS 525 1 Agenda - Session 20 Agenda - Session 20 • Continue our discussion of transfer pricing • Talk about review session • Talk about final

-

Upload

maude-watson -

Category

Documents

-

view

216 -

download

0

Transcript of W. BentzA&MIS 5251 Agenda - Session 20 Continue our discussion of transfer pricing Talk about review...

W. Bentz A&MIS 525 1

Agenda - Session 20Agenda - Session 20

• Continue our discussion of transfer pricing

• Talk about review session

• Talk about final

W. Bentz A&MIS 525 2

DivisionsDivisions

• Divisions are investment centers whose managers have the broad decision-making authority associated with decentralized management systems

• Divisions may have a variety of legal forms (corporations, unincorporated, etc.)

W. Bentz A&MIS 525 3

DivisionsDivisions

• Divisions vary greatly in size

• Financial controls dominate since the decision-making is decentralized

W. Bentz A&MIS 525 4

Transfer PricingTransfer Pricing

• A transfer price is the price at which a product or service is transferred from one entity to another entity within the same firm. Typically when products are moved from one cost center to another within a manufacturing system, the transfer price is the cumulative cost of the product to date.

W. Bentz A&MIS 525 5

Pricing Goods and ServicesPricing Goods and Services

Large, decentralized organizations simulate market economies by allowing internal (transfer) prices to guide intra-firm economic activity. Ideally, managers would be free to price transfers of goods and services at a mutually agreed upon price, as in a market economy. Divisions would buy from the best sources and sell to maximize their own profitability.

W. Bentz A&MIS 525 6

Decentralization PurposesDecentralization Purposes

• To decentralize authority and responsibility to those managers closest to the business.

• To train future executives

• To provide managerial incentives to operating executives

• To isolate economic efficiency by responsible entity

W. Bentz A&MIS 525 7

Decentralization PurposesDecentralization Purposes

• Distribute overall profitability among contributing entities

• Distribute overall profitability among taxing entities, usually countries

W. Bentz A&MIS 525 8

Transfer Pricing MethodsTransfer Pricing Methods

• Transfer pricing methods that include a profit element include:– Marginal cost (economic theory)– Administered prices– Cost-plus prices– Negotiated prices– Market prices

W. Bentz A&MIS 525 9

Transfer Price = Internal PriceTransfer Price = Internal Price

Primary or inter-mediate producer

Intermediate Producer or Distributor

External Customer

Transfer price

Final price

Corporate Entity

W. Bentz A&MIS 525 10

Note!!Note!!

• The selling division’s “price” is the buying division’s “cost” for divisional performance measurement purposes.

• Production decisions are differential analysis decisions in a multi-entity context. Resources may be constrained.

W. Bentz A&MIS 525 11

Three PerspectivesThree Perspectives

In making production decisions in a decentralized management system, one must consider three different perspectives:

• The total firm

• The selling division

• The purchasing division

W. Bentz A&MIS 525 12

The Texas Two-StepThe Texas Two-Step

• First, the financial analyst must decide if transfers should take place to enhance the profitability of the overall firm. The objective in this context is to maximize periodic income from operations.

W. Bentz A&MIS 525 13

The Other StepThe Other Step

• Second, if transfers are to the benefit of the overall firm, then the pricing system should encourage such transfers. Conversely, if transfers are not in the best interests of the overall firm, then the pricing system should discourage transfers. The pricing system should provide an incentive to “do the right thing.”

W. Bentz A&MIS 525 14

Artic DelightsArtic Delights

• Artic delights sells ice cream to franchisees for $1.75 per gallon. An external supplier is willing to supply comparable ice cream for $1.50 per gallon.

W. Bentz A&MIS 525 15

Artic DelightsArtic Delights

Total Per Unit

Sales $17,500 $ 1.75

Variable cost 10,000 1.00

Contribution margin $ 7,500 $ .75

Machine & rental cost 6,000 .60

Income from operations $ 1,500 $ .15

W. Bentz A&MIS 525 16

Sandwich StandsSandwich Stands

We do not know the ultimate sales price to final customers, but price increases are not at issue.

1. Sandwich stands should buy from Artic Delights so long as the purchase price paid by the stand exceeds the variable cost of producing ice cream.

W. Bentz A&MIS 525 17

Artic DelightsArtic Delights

2. Artic delights should produce so long as the purchase price is above variable cost of $1 per gallon.

3. If the stands could buy ice cream for $1.50 per gallon, then Artic Delights will have to drop its price.

W. Bentz A&MIS 525 18

Artic DelightsArtic Delights

4. How does the transfer price affect the profitability of (a) Artic Delights excluding the stands, (b) each Sandwich stand, and (c) Artic Delights and its sandwich stands combined.

• (a) The higher the transfer price, the higher the profits of Artic Delights, excluding the stands. The lower the price, the lower the income from operations.

W. Bentz A&MIS 525 19

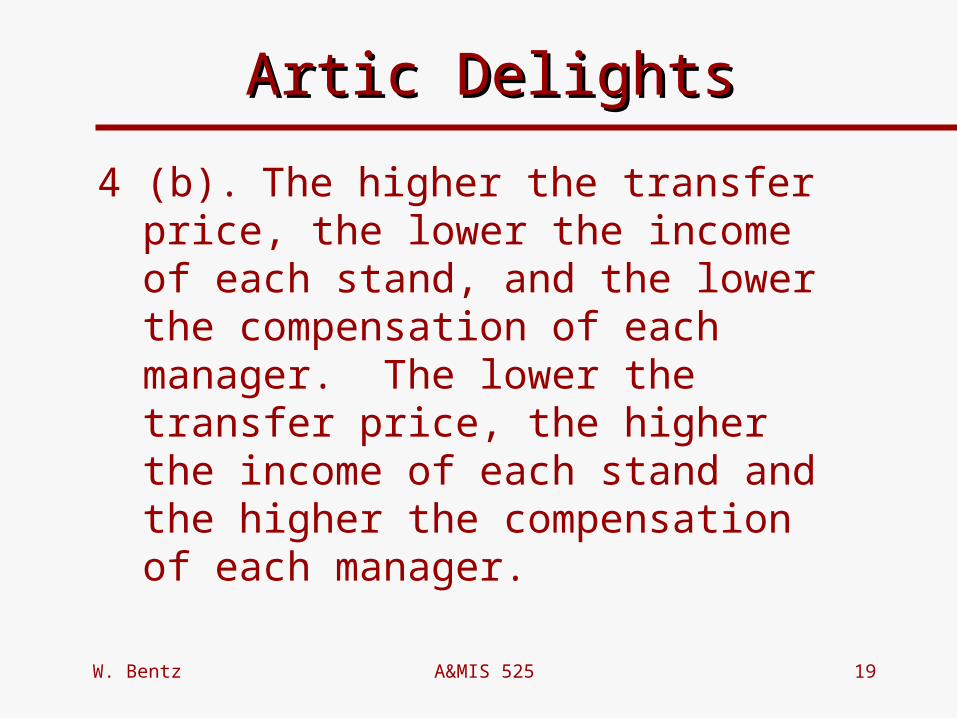

Artic DelightsArtic Delights

4 (b). The higher the transfer price, the lower the income of each stand, and the lower the compensation of each manager. The lower the transfer price, the higher the income of each stand and the higher the compensation of each manager.

W. Bentz A&MIS 525 20

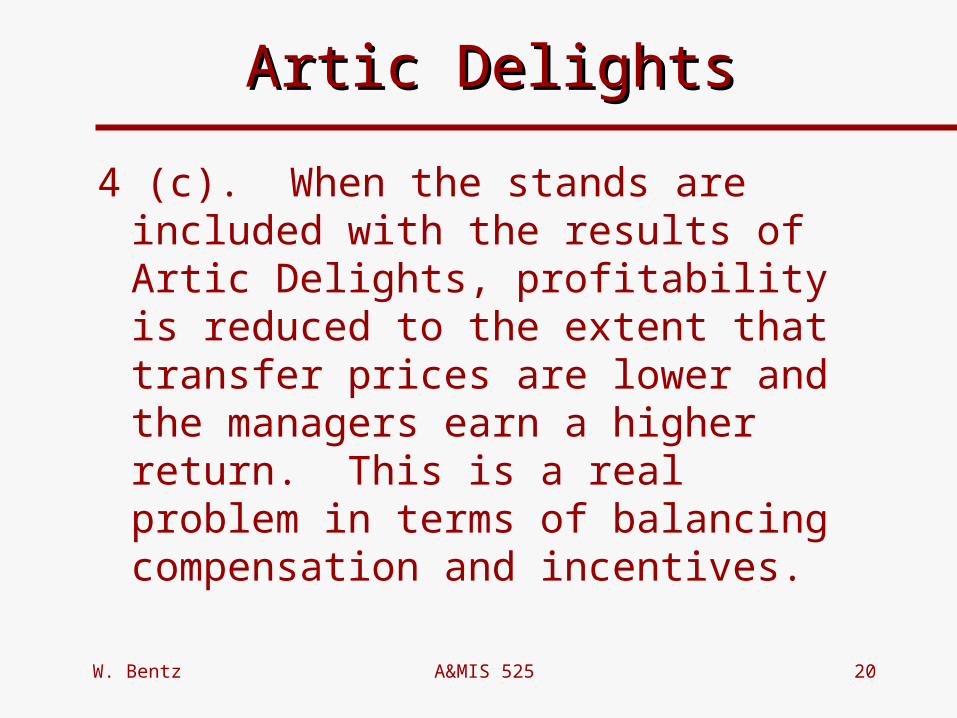

Artic DelightsArtic Delights

4 (c). When the stands are included with the results of Artic Delights, profitability is reduced to the extent that transfer prices are lower and the managers earn a higher return. This is a real problem in terms of balancing compensation and incentives.

W. Bentz A&MIS 525 21

EFG CompanyEFG Company

• Division S (Supplying) makes:

Subassemblies

Price $260

Variable cost 200

Contribution margin $ 60 (1)

Widgets

Price $150

Variable cost 125

Contribution margin $ 25 (4)

W. Bentz A&MIS 525 22

EFG CompanyEFG Company

Division P (Purchasing) makes:

Product B

Price $400

Variable cost* 160

Contribution margin $240 (2-$40)

Gadgets

Price $180

Variable cost 150

Contribution margin $ 30 (3)

W. Bentz A&MIS 525 23

EFG CompanyEFG Company

Case A:

Maximum external sales:

Division S - 1,600 subassemblies

(capacity = 2,000 units)

Division P - 500 Gadgets

(capacity = 1,000 units)

W. Bentz A&MIS 525 24

EFG CompanyEFG Company

Division S

[Capacity: 2,000 units]

Division P

[Capacity: 1,000 units]

Product B

Gadgets

Widgets

Subassemblies

Ext

erna

l Cus

tom

ers

Subassemblies

W. Bentz A&MIS 525 25

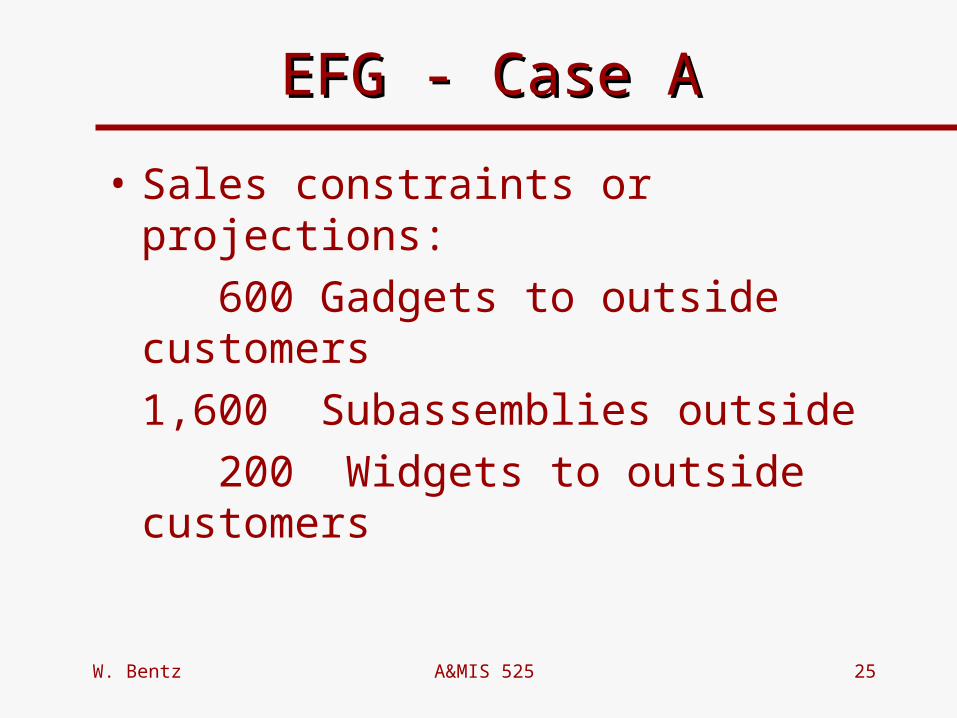

EFG - Case AEFG - Case A

• Sales constraints or projections:

600 Gadgets to outside customers

1,600 Subassemblies outside

200 Widgets to outside customers

W. Bentz A&MIS 525 26

EFG - Case AEFG - Case A

Division S Production Plan:

1,600 subassemblies for external sale

400 subassemblies for Div. P

Division P Production Plan:

400 units of Product B

500 Gadgets

100 units of idle capacity

W. Bentz A&MIS 525 27

EFG - Case BEFG - Case B

Case B:

Maximum external sales:

Division S - 1,600 subassemblies

- 200 widgets

(capacity = 2,000 units)

Division P - 600 Gadgets

(capacity = 1,000 units)

W. Bentz A&MIS 525 28

EFG - Case BEFG - Case B

Division S Production Plan: 1,600 subassemblies for external sale 400 subassemblies to Div. P

Division P Production Plan: 400 units of Product B 600 Gadgets

W. Bentz A&MIS 525 29

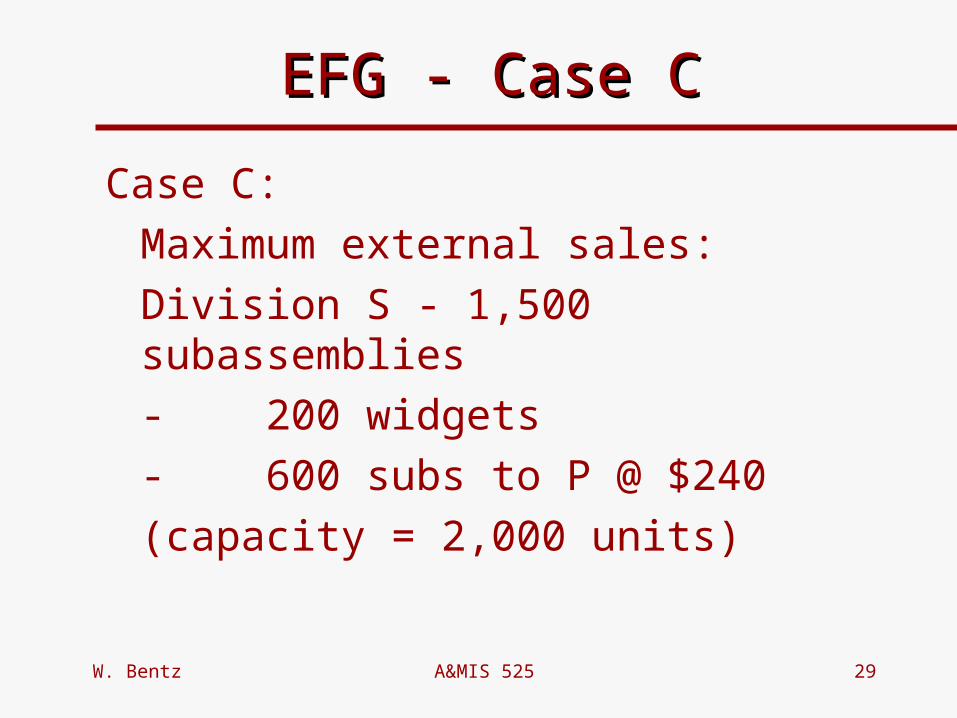

EFG - Case CEFG - Case C

Case C:

Maximum external sales:

Division S - 1,500 subassemblies

- 200 widgets

- 600 subs to P @ $240

(capacity = 2,000 units)

W. Bentz A&MIS 525 30

EFG - Case C (Div. S)EFG - Case C (Div. S)

Division S Production Plan:1,500 subassemblies for external

sale 500 subassemblies for Div. P

0 Widgets

W. Bentz A&MIS 525 31

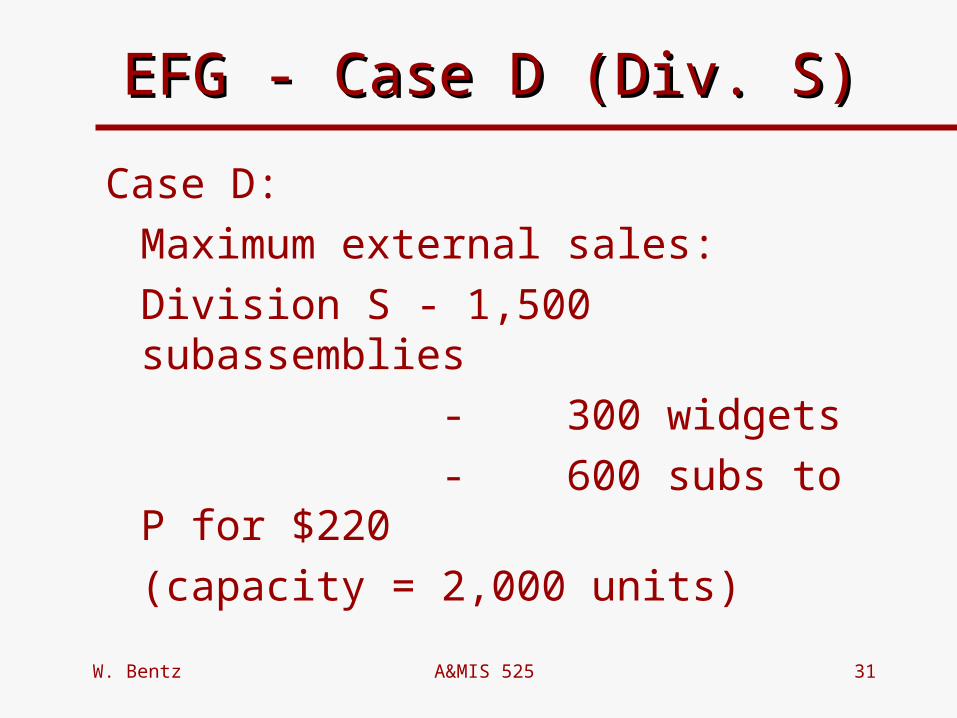

EFG - Case D (Div. S)EFG - Case D (Div. S)

Case D:

Maximum external sales:

Division S - 1,500 subassemblies

- 300 widgets

- 600 subs to P for $220

(capacity = 2,000 units)

W. Bentz A&MIS 525 32

EFG Case D (Div. S)EFG Case D (Div. S)

Division S Production:1,500 subassemblies for external

sale 200 subassemblies for Div. P

300 Widgets for external sale

Subassemblies to outside get $60

Widgets get $25

Subassemblies get $20 (at TP of $220)

W. Bentz A&MIS 525 33

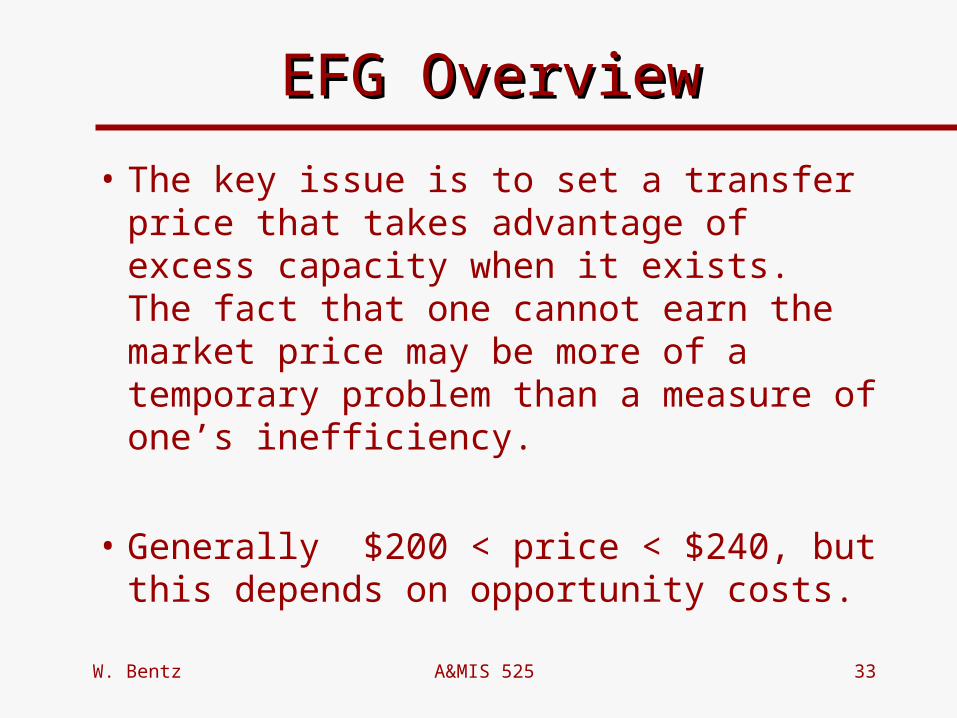

EFG OverviewEFG Overview

• The key issue is to set a transfer price that takes advantage of excess capacity when it exists. The fact that one cannot earn the market price may be more of a temporary problem than a measure of one’s inefficiency.

• Generally $200 < price < $240, but this depends on opportunity costs.

W. Bentz A&MIS 525 34

EFG2 Anyone?EFG2 Anyone?

• Do you want another problem?

W. Bentz A&MIS 525 35

EFG2 CompanyEFG2 Company

• Division S (Supplying) makes:

Subassemblies

Price $270

Variable cost 210

Contribution margin $ 60 (1)

Widgets

Price $150

Variable cost 125

Contribution margin $ 25 (4)

W. Bentz A&MIS 525 36

EFG2 CompanyEFG2 Company

Division P (Purchasing) makes:

Product B

Price $400

Variable cost* 160

Contribution margin $240 (2-$30)

Gadgets

Price $180

Variable cost 150

Contribution margin $ 30 (2)

W. Bentz A&MIS 525 37

EFG2 CompanyEFG2 Company

Case A:

Maximum external sales:

Division S - 1,500 subassemblies

(capacity = 2,000 units)

Division P - 400 Gadgets

(capacity = 1,000 units)

W. Bentz A&MIS 525 38

EFG2 CompanyEFG2 Company

Division S

[Capacity: 2,000 units]

Division P

[Capacity: 1,000 units]

Product B

Gadgets

Widgets

Subassemblies

Ext

erna

l Cus

tom

ers

Subassemblies

W. Bentz A&MIS 525 39

EFG2 - Case AEFG2 - Case A

Division S Production Plan:

1,500 subassemblies for external sale

500 subassemblies for Div. P

Division P Production Plan:

500 units of Product B

400 Gadgets

100 units of idle capacity

W. Bentz A&MIS 525 40

EFG2 - Case BEFG2 - Case B

Case B:

Maximum external sales:

Division S - 1,600 subassemblies

- 500 widgets

(capacity = 2,000 units)

Division P - 600 Gadgets

(capacity = 1,000 units)

W. Bentz A&MIS 525 41

EFG2 - Case BEFG2 - Case B

Division S Production Plan: 1,600 subassemblies for external sale 400 subassemblies to Div. P

Division P Production Plan: 400 units of Product B 600 Gadgets

W. Bentz A&MIS 525 42

EFG2 - Case CEFG2 - Case C

Case C:

Maximum sales:

Division S - 1,500 subassemblies

- 200 widgets

- 1,000 subs to P @ $240

(capacity = 2,000 units)

W. Bentz A&MIS 525 43

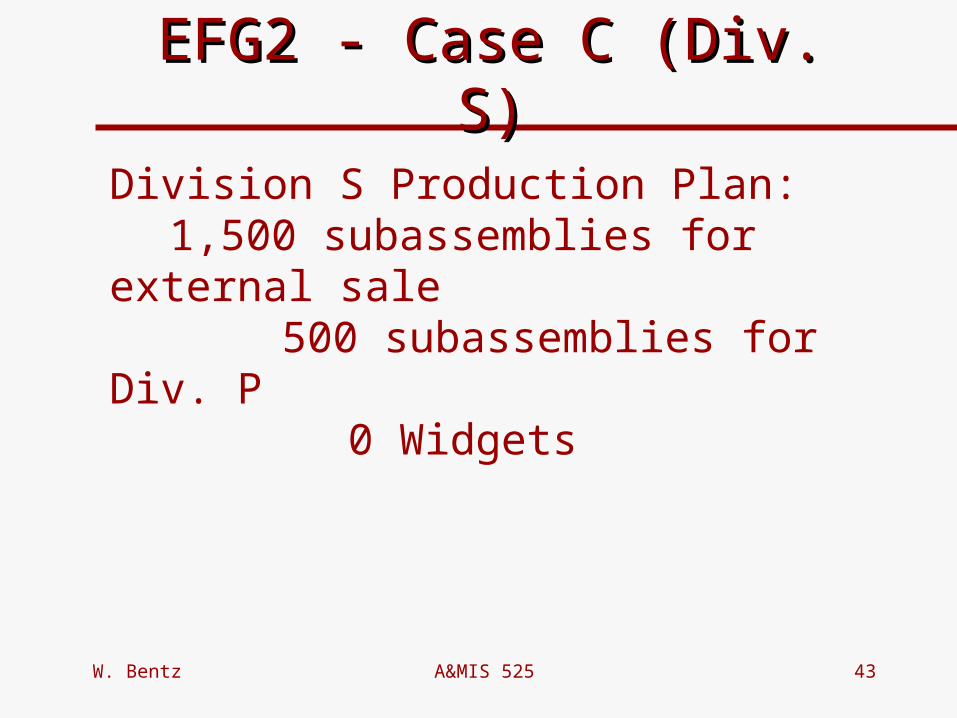

EFG2 - Case C (Div. S)EFG2 - Case C (Div. S)

Division S Production Plan:1,500 subassemblies for external

sale 500 subassemblies for Div. P

0 Widgets

W. Bentz A&MIS 525 44

EFG2 - Case D (Div. S)EFG2 - Case D (Div. S)

Case D:

Maximum external sales:

Division S - 1,500 subassemblies

- 300 widgets

- 1,000 subs to P for $220

(capacity = 2,000 units)

W. Bentz A&MIS 525 45

EFG2 Case D (Div. S)EFG2 Case D (Div. S)

Division S Production:1,500 subassemblies for external

sale 200 subassemblies for Div. P

300 Widgets for external sale

Subassemblies to outside get $60

Widgets get $25

Subassemblies get $20 (at TP of $220)

W. Bentz A&MIS 525 46

EFG2 OverviewEFG2 Overview

• The key issue is to set a transfer price that takes advantage of excess capacity when it exists. The fact that one cannot earn the market price may be more of a temporary problem than a measure of one’s inefficiency.

• Generally $210 < price < $240, but this depends on opportunity costs.

W. Bentz A&MIS 525 47

Quiz Discussion?Quiz Discussion?

W. Bentz A&MIS 525 48

Final Examination DiscussionFinal Examination Discussion

• Content

• Preparation

• Presentation

• Grading

W. Bentz A&MIS 525 49