VMA Market Outlook Workshop Omni Parker …...East Asia $1,163 bn 6,832 projects Southeast Asia $659...

22

VMA Market Outlook Workshop Omni Parker House, Boston, MA CONFIDENTIAL - No portion of this presentation may be reproduced without prior written consent. © 2017 Industrial Info Resources, Inc. 1-713-783-5147 Presented By: Industrial Info Resources, Inc. August 3, 2017

Transcript of VMA Market Outlook Workshop Omni Parker …...East Asia $1,163 bn 6,832 projects Southeast Asia $659...

VMA Market Outlook WorkshopOmni Parker House, Boston, MA

CONFIDENTIAL - No portion of this presentation may be reproduced without prior written consent. © 2017 Industrial Info Resources, Inc. 1-713-783-5147

Presented By:

Industrial Info Resources, Inc.

August 3, 2017

Britt BurtVP of Global Research,Power Industry

26 Years Tenure with IIR

Britt Burt leads teams of global researchers responsible for the traditional Power market and Industrial Energy Producers (IEP) in other industries. He is also responsible for a team of researchers that identify planned and unplanned unit outages for energy traders. Prior to joining IIR, Mr. Burt worked for Brown & Root, Zachry Construction and Bay Offshore Limited.

CONFIDENTIAL - No portion of this presentation may be reproduced without prior written consent. © 2017 Industrial Info Resources, Inc. 1-713-783-5147

VMA Market Outlook WorkshopOmni Parker House, Boston, MA

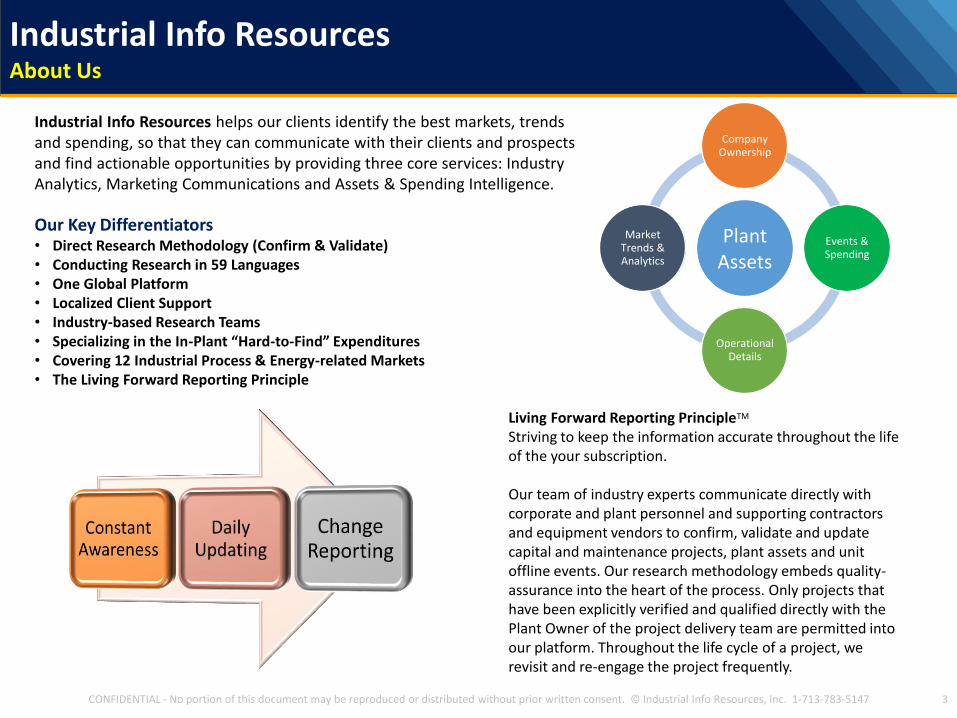

Industrial Info Resources helps our clients identify the best markets, trends and spending, so that they can communicate with their clients and prospects and find actionable opportunities by providing three core services: Industry Analytics, Marketing Communications and Assets & Spending Intelligence.

Our Key Differentiators • Direct Research Methodology (Confirm & Validate)• Conducting Research in 59 Languages • One Global Platform• Localized Client Support• Industry-based Research Teams • Specializing in the In-Plant “Hard-to-Find” Expenditures • Covering 12 Industrial Process & Energy-related Markets• The Living Forward Reporting Principle

3CONFIDENTIAL - No portion of this document may be reproduced or distributed without prior written consent. © Industrial Info Resources, Inc. 1-713-783-5147

PlantAssets

Company Ownership

Events & Spending

Operational Details

Market Trends & Analytics

Living Forward Reporting PrincipleStriving to keep the information accurate throughout the life of the your subscription.

Our team of industry experts communicate directly with corporate and plant personnel and supporting contractors and equipment vendors to confirm, validate and update capital and maintenance projects, plant assets and unit offline events. Our research methodology embeds quality-assurance into the heart of the process. Only projects that have been explicitly verified and qualified directly with the Plant Owner of the project delivery team are permitted into our platform. Throughout the life cycle of a project, we revisit and re-engage the project frequently.

TM

Industrial Info ResourcesAbout Us

Industrial Info ResourcesIndustry Coverage

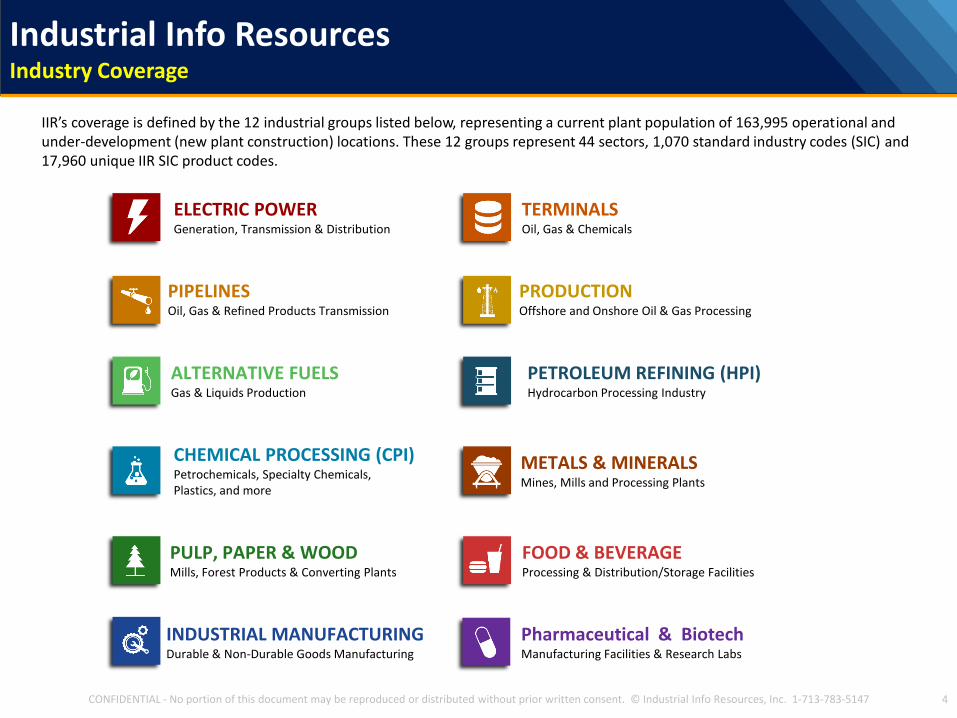

IIR’s coverage is defined by the 12 industrial groups listed below, representing a current plant population of 163,995 operational and under-development (new plant construction) locations. These 12 groups represent 44 sectors, 1,070 standard industry codes (SIC) and 17,960 unique IIR SIC product codes.

4CONFIDENTIAL - No portion of this document may be reproduced or distributed without prior written consent. © Industrial Info Resources, Inc. 1-713-783-5147

ELECTRIC POWERGeneration, Transmission & Distribution

TERMINALSOil, Gas & Chemicals

CHEMICAL PROCESSING (CPI)Petrochemicals, Specialty Chemicals, Plastics, and more

METALS & MINERALSMines, Mills and Processing Plants

PRODUCTION Offshore and Onshore Oil & Gas Processing

PIPELINESOil, Gas & Refined Products Transmission

ALTERNATIVE FUELSGas & Liquids Production

PETROLEUM REFINING (HPI)Hydrocarbon Processing Industry

FOOD & BEVERAGEProcessing & Distribution/Storage Facilities

PULP, PAPER & WOODMills, Forest Products & Converting Plants

INDUSTRIAL MANUFACTURINGDurable & Non-Durable Goods Manufacturing

Pharmaceutical & BiotechManufacturing Facilities & Research Labs

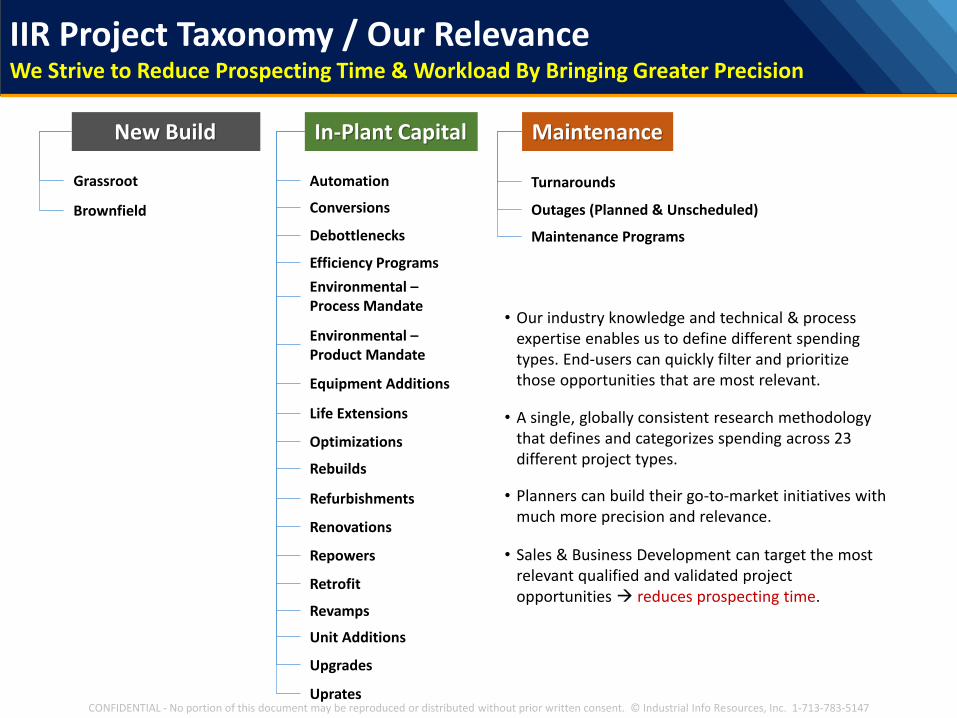

IIR Project Taxonomy / Our RelevanceWe Strive to Reduce Prospecting Time & Workload By Bringing Greater Precision

New Build In-Plant Capital Maintenance

Grassroot

Brownfield

Turnarounds

Outages (Planned & Unscheduled)

Maintenance Programs

• Our industry knowledge and technical & process expertise enables us to define different spending types. End-users can quickly filter and prioritize those opportunities that are most relevant.

• A single, globally consistent research methodology that defines and categorizes spending across 23 different project types.

• Planners can build their go-to-market initiatives with much more precision and relevance.

• Sales & Business Development can target the most relevant qualified and validated project opportunities reduces prospecting time.

Automation

Conversions

Debottlenecks

Efficiency Programs

Environmental –Process Mandate

Environmental –Product Mandate

Equipment Additions

Life Extensions

Optimizations

Rebuilds

Refurbishments

Renovations

Repowers

Retrofit

Revamps

Unit Additions

Uprates

Upgrades

CONFIDENTIAL - No portion of this document may be reproduced or distributed without prior written consent. © Industrial Info Resources, Inc. 1-713-783-5147

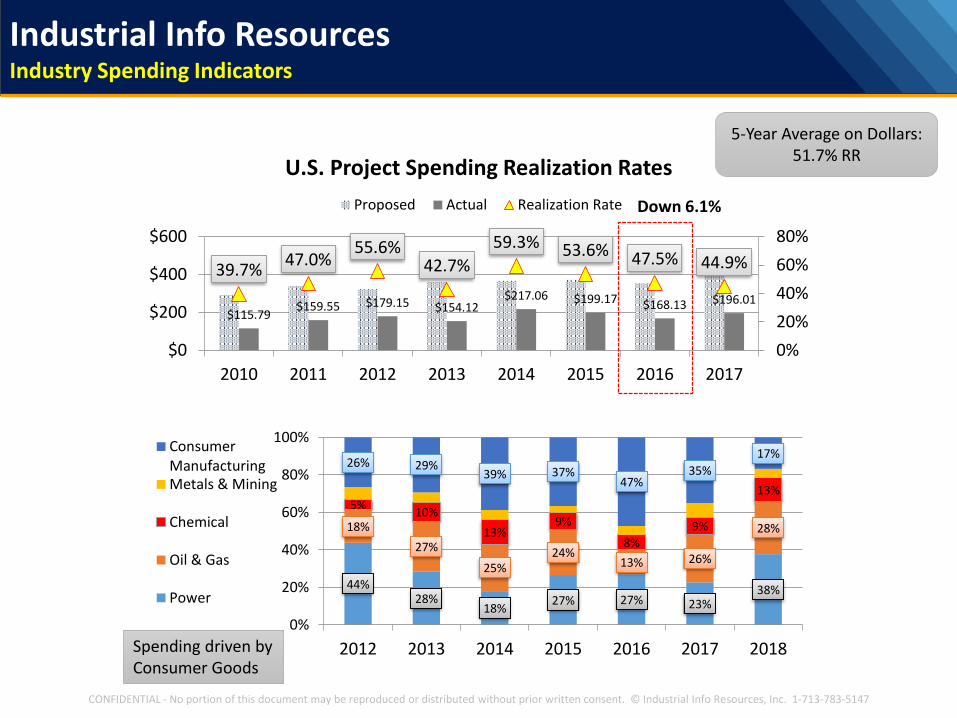

$115.79$159.55 $179.15 $154.12

$217.06 $199.17 $168.13 $196.01

39.7%47.0%

55.6%42.7%

59.3% 53.6% 47.5% 44.9%

0%

20%

40%

60%

80%

$0

$200

$400

$600

2010 2011 2012 2013 2014 2015 2016 2017

U.S. Project Spending Realization Rates

Proposed Actual Realization Rate Down 6.1%

Spending driven byConsumer Goods

5-Year Average on Dollars: 51.7% RR

44%28%

18%27% 27% 23%

38%

18%

27%

25%24%

13% 26%

28%

5%10%

13%9%

8%

9%

13%

26% 29%39% 37%

47%35%

17%

0%

20%

40%

60%

80%

100%

2012 2013 2014 2015 2016 2017 2018

ConsumerManufacturingMetals & Mining

Chemical

Oil & Gas

Power

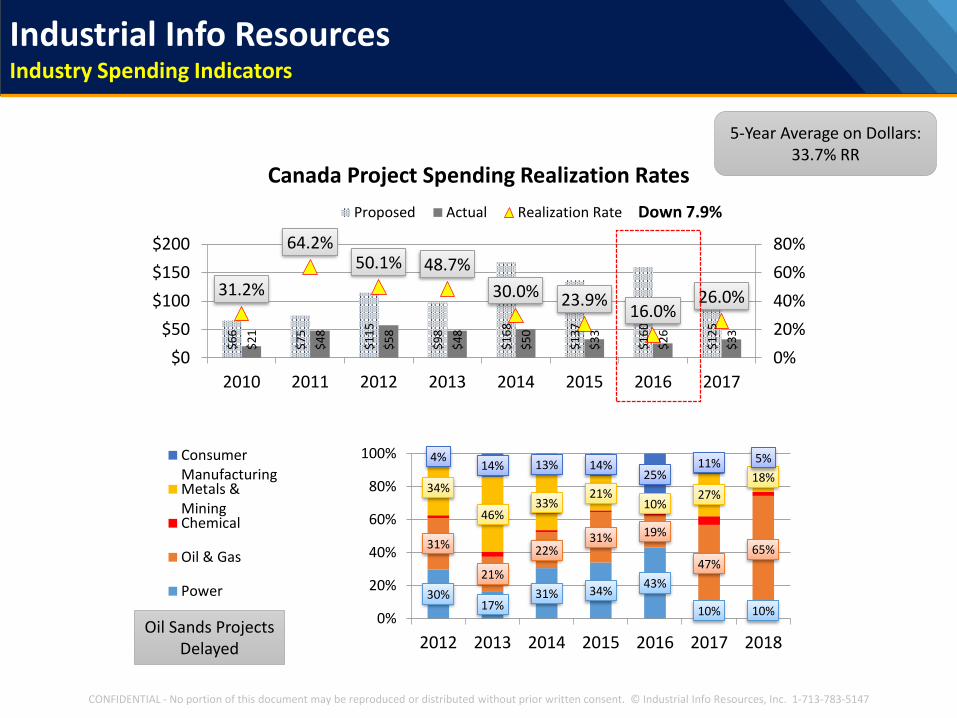

Industrial Info ResourcesIndustry Spending Indicators

CONFIDENTIAL - No portion of this document may be reproduced or distributed without prior written consent. © Industrial Info Resources, Inc. 1-713-783-5147

$6

6

$7

5

$1

15

$9

8

$1

68

$1

37

$1

60

$1

25

$2

1

$4

8

$5

8

$4

8

$5

0

$3

3

$2

6

$3

3

31.2%

64.2%50.1% 48.7%

30.0% 23.9%16.0%

26.0%

0%

20%

40%

60%

80%

$0

$50

$100

$150

$200

2010 2011 2012 2013 2014 2015 2016 2017

Canada Project Spending Realization Rates

Proposed Actual Realization Rate Down 7.9%

Oil Sands ProjectsDelayed

5-Year Average on Dollars: 33.7% RR

30%17%

31% 34%43%

10% 10%

31%

21%

22%31% 19%

47%65%

34%

46%33%

21%10%

27%

18%

4%14% 13% 14%

25%11% 5%

0%

20%

40%

60%

80%

100%

2012 2013 2014 2015 2016 2017 2018

ConsumerManufacturingMetals &MiningChemical

Oil & Gas

Power

Industrial Info ResourcesIndustry Spending Indicators

CONFIDENTIAL - No portion of this document may be reproduced or distributed without prior written consent. © Industrial Info Resources, Inc. 1-713-783-5147

Current Active ProjectsPlanning & Engineering Stage only

& MaintenanceStart/Kick-off Date – ALL DATES

Source: IIR PowerProject Database

Global Power Generation Project 24-Month OutlookActive Capital & Maintenance Projects

4,065 Projects - $1,105 trillion Under Construction

N. America

$712 bn4,188

Middle Am

$17.2 bn278

Europe

$945 bn7,126

Oceania

$46.7 bn615 projects

Africa

$405 bn1,645

South America

$322 bn2,949

Global Planned Projects32,558 Active Projects - $5.43 Trillion TIV

Planning & Engineering Stage Construction Starts - ALL DATES

South Asia

$733 bn4,720 projects

Central Asia

$21.3 bn246 projects

Western Asia

$265 bn1,115 projects

East Asia

$1,163 bn6,832 projects

Southeast Asia

$659 bn2,791 projects

Russia

$74 bn816 projects

$5.8bn

$7.7bn

$8.6bn

$13.7bn

$37bn

$49bn

$68bn

$69bn

$82bn

$86.5bn

$92bn

$101bn

$113bn

$368bn

Southern Europe

Middle America

Central Asia

Russia

Eastern Europe

Latin America

Southeast Asia

Western Europe

Africa

Western Asia

North Europe

South Asia

North America

East Asia

Total Active Power Under Construction Projects

All Years

CONFIDENTIAL - No portion of this document may be reproduced or distributed without prior written consent. © Industrial Info Resources, Inc. 1-713-783-5147

Global Power Generation Project Outlook By Fuel TypeStart Date 2017-2018

0% 20% 40% 60% 80% 100%

Middle America

Russia

Oceania

Central Asia

Western Asia

North America

South America + MX

Africa

Southeast Asia

Europe

South Asia

East Asia

Next 2 Years Project Spending By Fuel TypeStart Dates 2017-2018

Grassroot, Unit Additions, Other In-plant Capital & Maintenance

Coal Natural Gas Fuel Oil

Nuclear Hydro Solar

Wind Other Renewables

$14.3bn

$26.3bn

$39bn

$39.2bn

$183.5bn

$218.8bn

$223.4bn

$235bn

$284bn

$316bn

$489bn

$800bn

Market Region Total2017-18

CONFIDENTIAL - No portion of this document may be reproduced or distributed without prior written consent. © Industrial Info Resources, Inc. 1-713-783-5147

• Natural gas the dominant fuel for electricity generation.

• Multiple drivers, including federal tax credits, are driving growth in renewables.

• Future generation mix will be defined by natural gas prices and electricity.

North American Power Industry OutlookGeneration, Transmission & Distribution

CONFIDENTIAL - No portion of this document may be reproduced or distributed without prior written consent. © Industrial Info Resources, Inc. 1-713-783-5147

• Challenging business climate for nuclear sector.

• Environmental regulations continue to target coal-fired power plants.

• In-plant capital and maintenance for aging fleet.

• Ongoing investment for transmission and distribution.

North American Power Industry OutlookGeneration, Transmission & Distribution

CONFIDENTIAL - No portion of this document may be reproduced or distributed without prior written consent. © Industrial Info Resources, Inc. 1-713-783-5147

0

5,000

10,000

15,000

20,000

25,000

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

Coal, Nuclear, Gas & Oil

Coal Nuclear Natural Gas Fuel Oil

Tota

l Meg

awat

ts

• Over 85 Gigawatts retired since 2012

• 67 Gigawatts 2017-2022

North American (USA & Canada) Power IndustryUnit Closures from 2012-2022

CONFIDENTIAL - No portion of this document may be reproduced or distributed without prior written consent. © Industrial Info Resources, Inc. 1-713-783-5147

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

Unit Closure by Region & Fuel

Coal Nuclear Natural Gas Fuel Oil

2012 2013 2014 2015 2016 2017 *2018 *2019

Landfill 174 121 56 3 54 34 58 46

Biomass 292 658 282 73 73 197 191 192

Coal 3,668 1,530 160 0 0 35 0 0

Fuel Oil 254 165 15 281 39 68 12 76

Geothermal 148 104 15 30 70 0 39 33

Hydro 1,285 1,639 2,190 2,226 872 1,800 1,906 1,399

Natural Gas 11,296 7,795 9,729 6,728 8,757 13,383 18,599 11,728

Nuclear 0 0 0 0 1,150 0 0 0

Solar 693 2,483 2,561 3,550 5,629 3,865 6,809 8,566

Wind 14,164 2,687 5,904 10,455 9,215 7,714 13,343 28,040

0

10,000

20,000

30,000

40,000

50,000

60,000

31,974 17,182 20,912 23,346 25,859 27,096 40,957 50,080

Tota

l Meg

awat

tsNorth American Power Industry (USA & Canada)Unit Startups by Energy Source (2012 – 2019 Total MW)

CONFIDENTIAL - No portion of this document may be reproduced or distributed without prior written consent. © Industrial Info Resources, Inc. 1-713-783-5147

2012 2013 2014 2015 2016 *2017* *2018* 2019

Landfill 89 50 49 52 0 3 33 0

Biomass 403 80 181 42 65 331 154 66

Coal/ Pet Coke 160 0 0 0 35 240 0 0

Fuel Oil 116 38 134 34 45 213 72 42

Geothermal 41 30 30 0 70 63 91 266

Hydro 1,825 1,008 2,472 88 1,692 893 2,372 4,374

Natural Gas 8,717 7,423 13,770 16,985 11,839 12,822 18,503 17,871

Nuclear 4,451 0 0 0 0 0 0 0

Solar 2,041 2,259 3,202 4,102 3,619 5,996 11,781 4,707

Wind 6,336 7,646 5,868 9,132 8,886 9,490 16,908 21,459

0

10,000

20,000

30,000

40,000

50,000

60,000

Tota

l Meg

awat

ts

24,179 18,534 25,706 30,435 26,437 30,051 49,914 48,785

North American Power Industry (USA & Canada)Unit Construction Start by Energy Source (2012 – 2019 Total MW)

CONFIDENTIAL - No portion of this document may be reproduced or distributed without prior written consent. © Industrial Info Resources, Inc. 1-713-783-5147

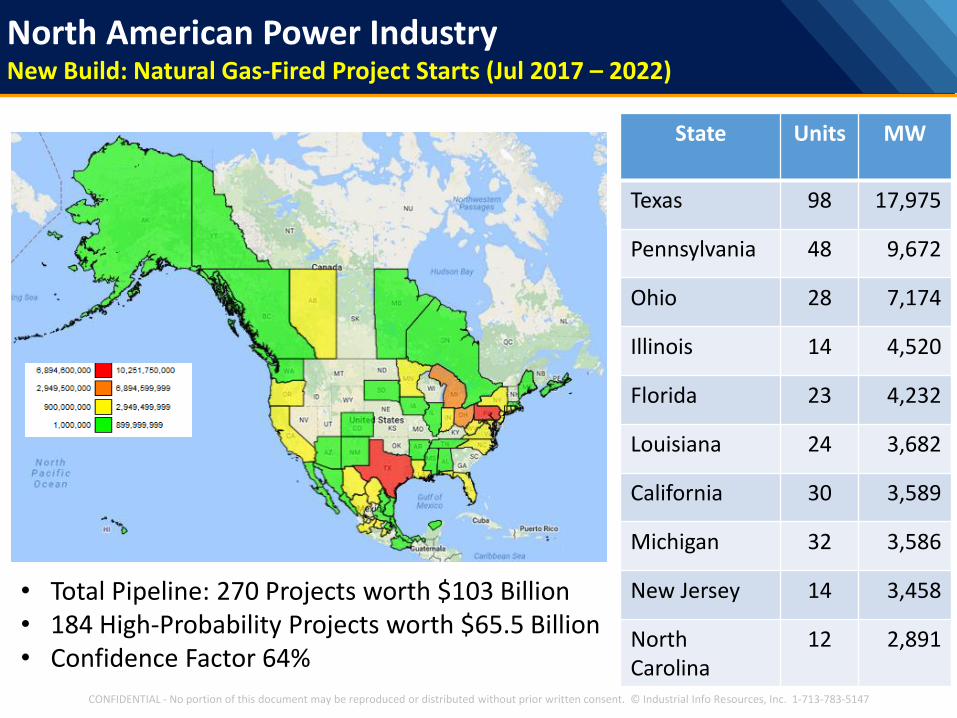

State Units MW

Texas 98 17,975

Pennsylvania 48 9,672

Ohio 28 7,174

Illinois 14 4,520

Florida 23 4,232

Louisiana 24 3,682

California 30 3,589

Michigan 32 3,586

New Jersey 14 3,458

NorthCarolina

12 2,891

• Total Pipeline: 270 Projects worth $103 Billion• 184 High-Probability Projects worth $65.5 Billion• Confidence Factor 64%

North American Power IndustryNew Build: Natural Gas-Fired Project Starts (Jul 2017 – 2022)

CONFIDENTIAL - No portion of this document may be reproduced or distributed without prior written consent. © Industrial Info Resources, Inc. 1-713-783-5147

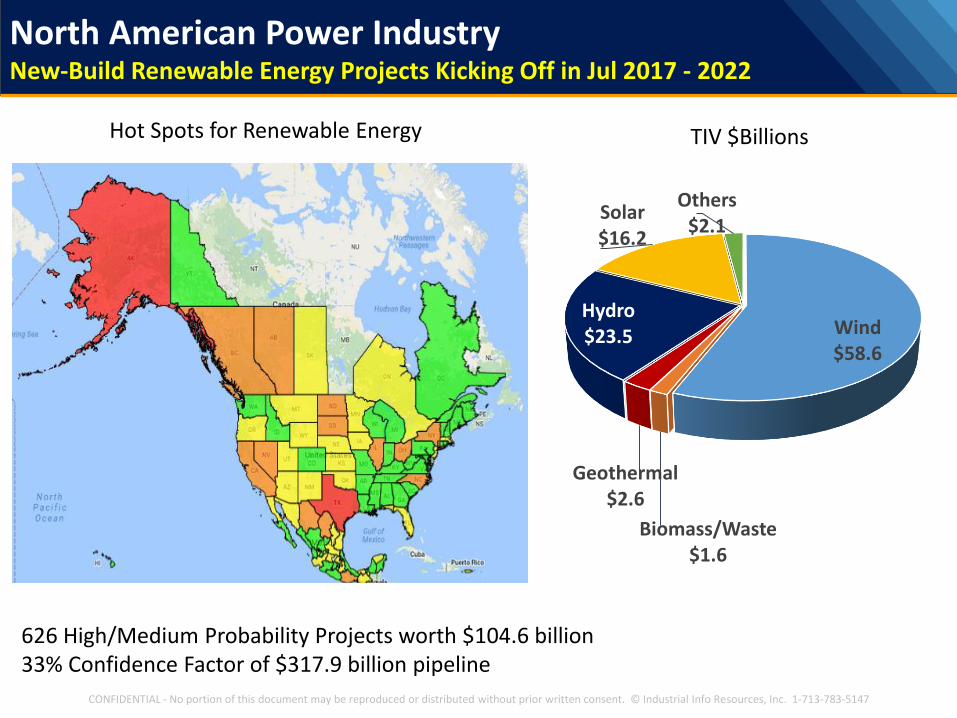

North American Power IndustryNew-Build Renewable Energy Projects Kicking Off in Jul 2017 - 2022

CONFIDENTIAL - No portion of this document may be reproduced or distributed without prior written consent. © Industrial Info Resources, Inc. 1-713-783-5147

Wind $58.6

Biomass/Waste$1.6

Geothermal $2.6

Hydro$23.5

Solar$16.2

Others$2.1

TIV $BillionsHot Spots for Renewable Energy

626 High/Medium Probability Projects worth $104.6 billion33% Confidence Factor of $317.9 billion pipeline

327 High-Probability Projects worth $25.9 Billion70%+ Confidence factor of $38.3 Billion Pipeline

North American Power IndustryIn-Plant Capital Projects – Construction Start 2017 - 2022

Market Region Environmental Modernization Repower Closure Other In-Plant Capital

West Coast $41 $54 $3,261 $1,423 $2,096

Ontario $600 $8,413 $2,418

Great Lakes $2,296 $150 $669 $239 $1,202

Southeast $1,974 $612 $228 $49 $737

Rocky Mountains $1,714 $25 $15 $72 $1,049

Midwest $1,300 $520 $104 $154

Western Canada $980 $430 $30 $708

Southwest $376 $3 $37 $2 $353

Mid Atlantic $674 $60 $25 $200 $275

Northeast $143 $252 $32 $640

New England $344 $1,260 $93

Atlantic Canada $38

Total $10,442 $10,267 $4,517 $3,381 $9,763

TIV $ Millions

CONFIDENTIAL - No portion of this presentation may be reproduced without prior written consent. © 2017 Industrial Info Resources, Inc. 1-713-783-5147

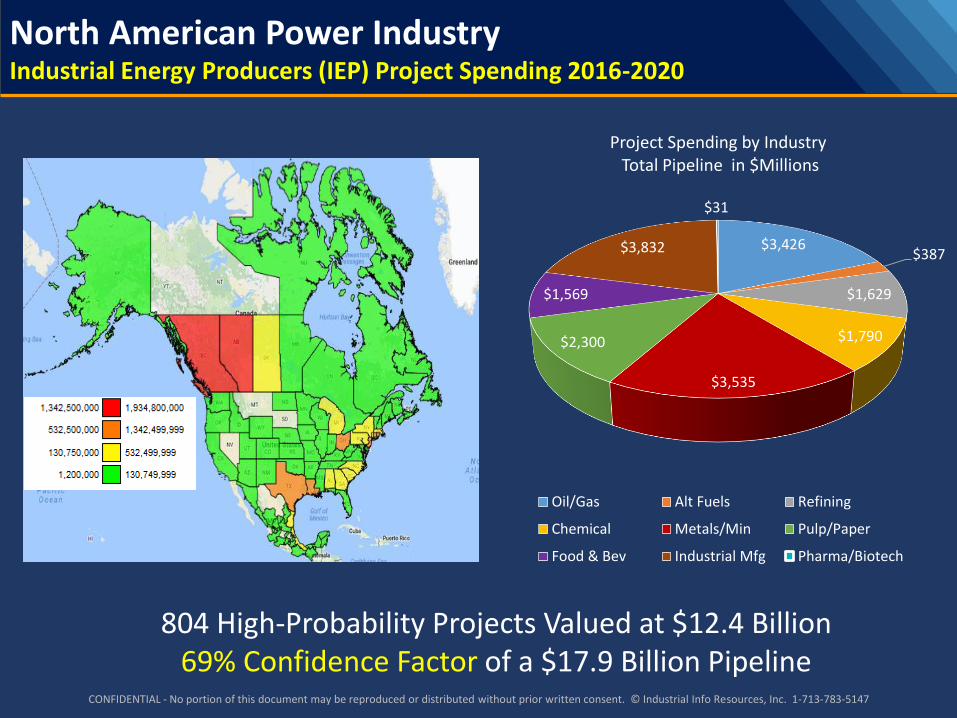

$3,426$387

$1,629

$1,790

$3,535

$2,300

$1,569

$3,832

$31

Project Spending by IndustryTotal Pipeline in $Millions

Oil/Gas Alt Fuels Refining

Chemical Metals/Min Pulp/Paper

Food & Bev Industrial Mfg Pharma/Biotech

804 High-Probability Projects Valued at $12.4 Billion69% Confidence Factor of a $17.9 Billion Pipeline

North American Power IndustryIndustrial Energy Producers (IEP) Project Spending 2016-2020

CONFIDENTIAL - No portion of this document may be reproduced or distributed without prior written consent. © Industrial Info Resources, Inc. 1-713-783-5147

$2.9$3.2

$4.2

$3.5$3.6

$3.2

0

100

200

300

400

500

600

700

800

$0.0

$0.5

$1.0

$1.5

$2.0

$2.5

$3.0

$3.5

$4.0

$4.5

2013 2014 2015 2016 2017 2018

Scheduled Outages

TIV Project Count

504 516 513323

147

466633 557

696

315

325

490 500 572

180

0

2

4

6

8

10

12

14

0

500

1,000

1,500

2,000

2013 2014 2015 2016 2017

Coal NuclearNatural Gas RenewablesFuel Oil

Unplanned Outages

$ B

illio

ns

Pro

ject

Co

un

t

Tota

l Ou

tage

s

Avg

Day

s O

fflin

e

• Maintenance activity for scheduled outages trending upward for 2017

• Extended maintenance cycles and deferred outages becoming more common

US Power IndustryScheduled and Unplanned Outage Activity

CONFIDENTIAL - No portion of this document may be reproduced or distributed without prior written consent. © Industrial Info Resources, Inc. 1-713-783-5147

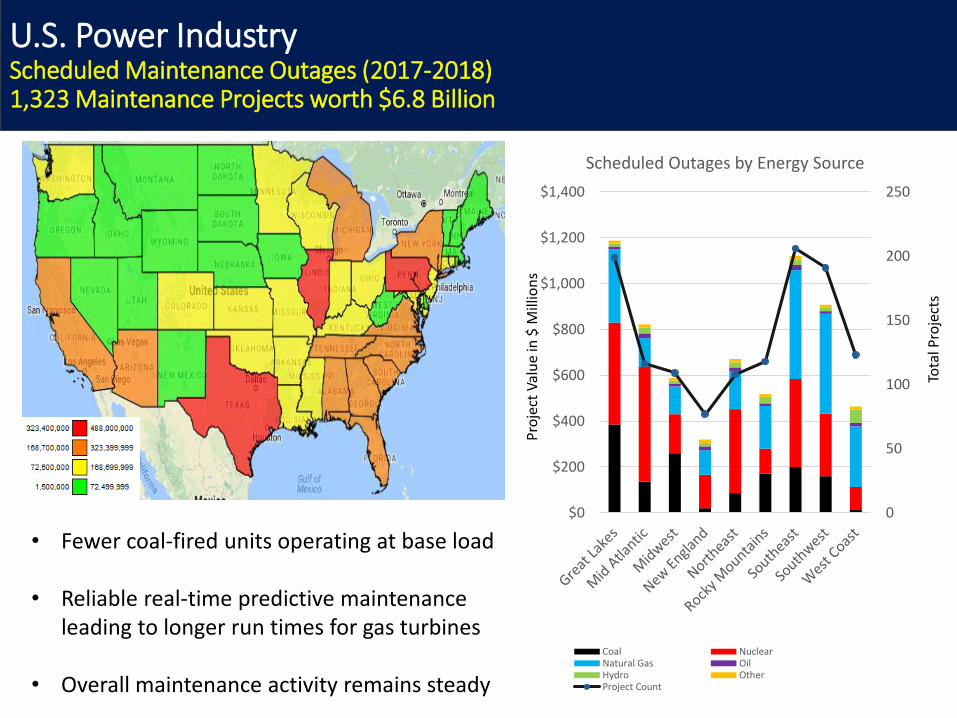

U.S. Power IndustryScheduled Maintenance Outages (2017-2018)1,323 Maintenance Projects worth $6.8 Billion

0

50

100

150

200

250

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

Scheduled Outages by Energy Source

Coal NuclearNatural Gas OilHydro OtherProject Count

Pro

ject

Val

ue

in $

Mill

ion

s

Tota

l Pro

ject

s

• Fewer coal-fired units operating at base load

• Reliable real-time predictive maintenance leading to longer run times for gas turbines

• Overall maintenance activity remains steady

• Industrial, Commercial, Educational Institutions and Government entities are expanding micro-grid capabilities.

• Healthy outlook for energy storage technologies.

• Development of distributed generation continues to increase.

• More development of combined heat and power sources on the horizon.

• Grid operators and generation companies alike continue with cybersecurity programs.

• Development of small modular reactors proceeds for future beyond 2020.

North American Power IndustryOngoing and Emerging Trends

CONFIDENTIAL - No portion of this document may be reproduced or distributed without prior written consent. © Industrial Info Resources, Inc. 1-713-783-5147

• Transformation of the power industry continues.

• New-build generation continues to be led by natural gas-fired power plants and renewable energy sources.

• Investment in the coal and nuclear sectors continues to be centered around in-plant capital and maintenance.

• More project spending directed toward environmental regulations.

• Emerging trends continue to open new doors.

North American Power IndustryOutlook Conclusions

CONFIDENTIAL - No portion of this document may be reproduced or distributed without prior written consent. © Industrial Info Resources, Inc. 1-713-783-5147