Vision 2030 The UK Metals Industry's New Strategic Approach Articles/MIS printed report 2015.pdf ·...

12

Vision 2030 The UK Metals Industry's New Strategic Approach

Transcript of Vision 2030 The UK Metals Industry's New Strategic Approach Articles/MIS printed report 2015.pdf ·...

Vision 2030The UK Metals Industry'sNew Strategic Approach

The UK Metals Industry’s New Strategic Approach

11,100COMPANIES

ANNUAL TURNOVER

230,000DIRECT EMPLOYEES

750,000FURTHER JOBS SUPPORTED

£33 BN

£10.7BNGROSS VALUE ADDED

£10.7BNGROSS VALUE ADDED

UK GDPSUPPORTED

£200 BN

EMPLOYMENT COST

£7.5 BILLION

DOMINATED BYSMALL COMPANIES

21EMPLOYEESPER ENTERPRISE

£46,700GVA PER EMPLOYEE

£32,500EMPLOYMENT COST

PER HEAD

50%MORE THANUK AVERAGE

TWO-THIRDSMORE THAN UK AVERAGE

UK METALS COMPANIESWILL NEED TO RECRUIT

EVERY YEAR

AND

2,300GRADUATES

9,200APPRENTICES &TECHNICIANS

SUCCESSFULIMPLEMENTATION OF

THIS STRATEGY COULDADD UP TO

TO UK GDP

JOBS TO THE UK ECONOMY,WORTH AN EXTRA

150,000

£3-4BN

INCREASED PRODUCTION IN

EXPECTED TO PROVIDE AROUND

£2.5BN/YEAR OF ADDITIONAL OPPORTUNITIES

INFRASTRUCTUREPLAN INCLUDES

SOME £466BN OF INVESTMENT UP TO AND BEYOND 2020

By 2030, a modern and progressive UK Metals Industry willbe supplying high quality, innovative and competitivelypriced products to a wide range of customers. It will be theprincipal supplier to the UK’s main manufacturers andinfrastructure projects, and a leading global exporter.

A forward-thinking, collaborative approach to R&D will have embedded innovation throughout the industry, from the smallest firms to the largest, directed by customers’ needs.

A long-term commitment to, and involvement in, educationand training will have created a modern, specialisedworkforce. e Metals Industry will be seen as a desirableemployer able to attract the highest calibre recruits.

Metals and metal products will be at the heart of the newcircular economy, recognising their innate potential forresource-efficient reuse, remanufacture and recycling.

e industry will be represented by aMetals Council and will have workedwith government to ensure abalanced regulatory environmentthat puts UK metals firms on alevel playing field with overseascompetitors.

By delivering this vision, the UK Metals Industry aims to increase its GVA by 50% by 2030.

A Vision for 2030

Image courtesy of Pandrol UK (CBM)

The UK Metals Industry’s New Strategic Approach

e UK’s metals companies are the backbone of thenation’s manufacturing, construction andinfrastructure. e enormous value they contribute tothe UK is largely hidden. We all recognise the car wedrive, or the bridge we cross, or the aeroplane thattakes us on holiday. But most of us take for granted themyriad types of metal that are essential to these integralparts of modern life. Taken together a million jobs aredirectly or indirectly connected to the UK metalsindustry, which makes an essential direct and indirectcontribution to some £400bn of the UK’s GDP.

As importantly, the UK metals industry is a key part ofthe UK’s knowledge economy through innovation andskills development, and it plays a key role in a lowercarbon, more resource efficient UK. Metals companiesare essential to the fabric of the communities in whichthey operate.

To many, the metals industry is representative of theindustrial history of the UK, and the industry isrightly proud of its heritage. But too often thisobscures the substantial contribution it already makestoday and how it enables the economy of tomorrow.By looking at themselves and asking hard questionsabout historical patterns of investment and strategy,and by pressing policy makers in the UK and the EUto avoid repeating the mistakes of the past, we canlook to a future where metals are recognised as anessential part of a sustainable economy, and the UKcan build a metals industry with a bright future.

Recognising this potential, but also the challenges, theUK’s metals industry has come together in a commonpurpose, joining different metals and process routes,across the full spectrum of the supply chain, fromprimary manufacturing to recycling.

70 individuals, including many senior leaders fromover 50 metals companies, associated organisationsand stakeholders, such as the Advanced FormingResearch Centre, AMRC Sheffield and the trade unionCommunity representing the TUC, have workedtogether to forge a single vision for the futuredevelopment of this vital industry.

Different thoughmany parts of theindustry are, threecore themes haveemerged from an intensiveprogramme of working groups and review:

1. Ensuring that the UK captures the most value it canfrom its manufacturing, construction andinfrastructure supply chains

2. Improving the connectivity of the metals industryto the critical ingredients for long term success,such as skills and innovation, especially for theindustry’s many smaller companies

3. Ensuring the UK metals industry is recognised asbeing at the heart of a future UK circular economy

Taken together, action under these three overarchingthemes should revitalise the UK metals industry. It will create sustainable companies ready to delivermetals and metal products to the increasinglydemanding specifications UK manufacturing is goingto rely on and companies that will be able to competewith the best in the world for the long term.

Bringing the industry together under a single voiceand working in partnership with the government andother key industrial sectors holds out the potential thatthis contribution can not only be maintained butgrown substantially.

I’d like to thank BIS for their support throughout thedevelopment of this report and to acknowledge thededicated contribution of the many people from acrossthe industry who have committed their time and effortto delivering this report.

Jon Bolton Chair, Metals Strategy Steering Group

Industry Foreword

I welcome the initiative of the Metals Forum and thewider UK metals community to produce this reportsetting out their vision for their industry. is isespecially important at a time when many companiesin the sector are facing major pressures on theirbusinesses. I have seen for myself how hard the sectoris working in order to remain competitive in such achallenging environment. is Strategy is a timelyand welcome analysis of the issues and heralds a newphase in the industry’s dialogue with Government.

e UK’s metal sectors are part of the foundation ofmany of the nation’s great, world beating supplychains – automotive, aerospace, construction andenergy to name just four. eir importance to theeconomy should not be underestimated; some 11,000companies collectively contribute or underpin £200bnof GDP and as many as a million jobs.

at is why the Government remains committed toenabling a healthy and growing metals industry in theUK and one focused on the UK’s strengths in highlyskilled manufacturing. is is essential if we are toincrease productivity, which is an important driver ofour economic success and the route to raisingstandards of living for everyone in this country.

e best way that theGovernment cancreate the rightconditions for themetals sector to flourish, first and foremost, is through a successful economyand successful metals-using industries, which is whywe will stick to our long-term economic plan. We are creating the right business environment for free enterprise and removing barriers to productivityand growth within sectors, including de-regulation,promoting fair competition and a simplified business landscape.

e Metals Strategy will provide a platform forGovernment to work with the sector on the issueswhich may hold back growth of the sector. Please beassured that where I can reasonably provide support, I will do so.

I also look forward to working with the UK MetalsCouncil in leading the sector to deliver its vision and to a long term sustainable future.

Rt Hon Anna Soubry Minister of State, Small Business, Industry and Enterprise

Ministerial Foreword

1

The UK Metals Industry’s New Strategic Approach

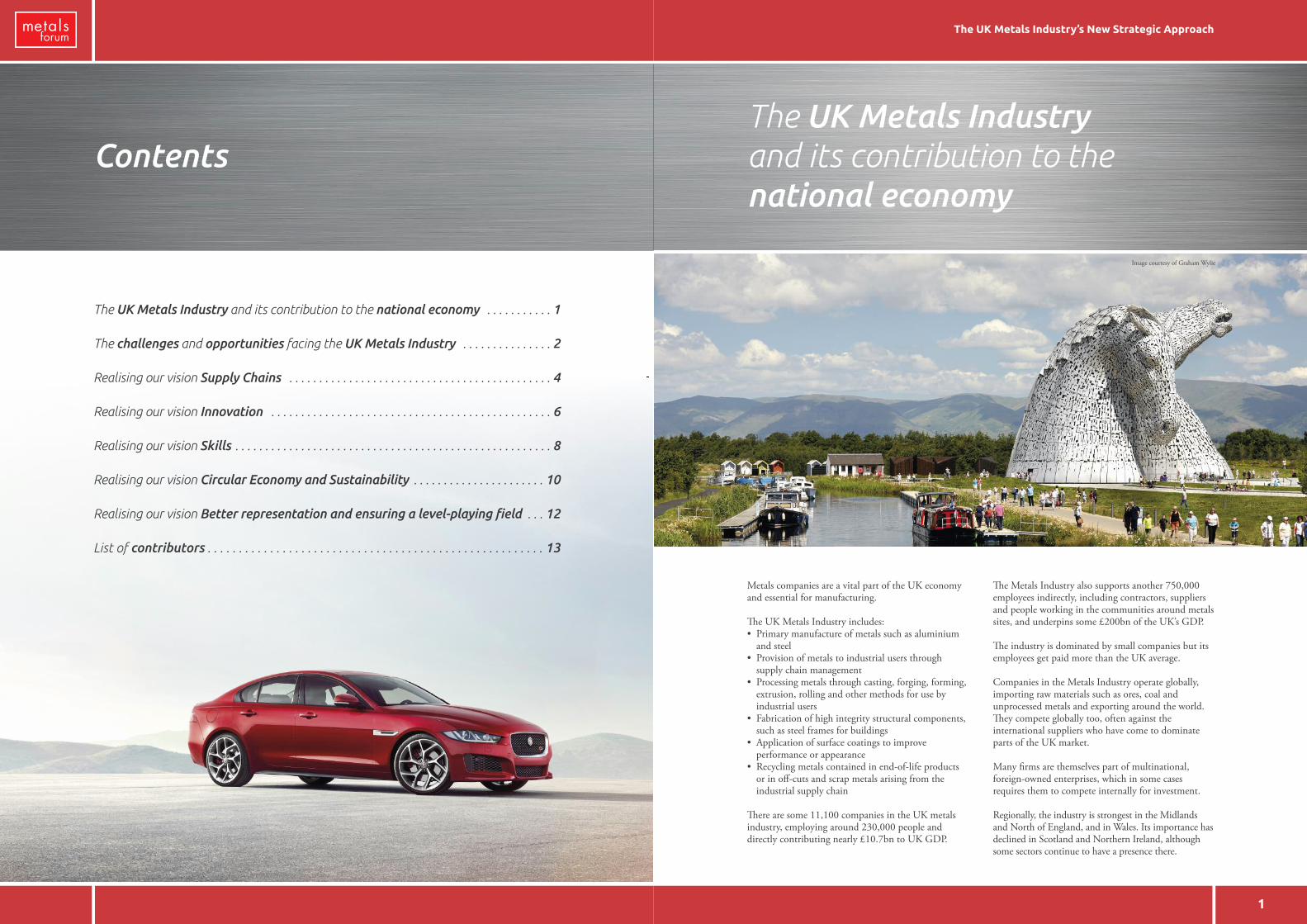

Metals companies are a vital part of the UK economyand essential for manufacturing.

e UK Metals Industry includes: • Primary manufacture of metals such as aluminium

and steel• Provision of metals to industrial users through

supply chain management• Processing metals through casting, forging, forming,

extrusion, rolling and other methods for use byindustrial users

• Fabrication of high integrity structural components,such as steel frames for buildings

• Application of surface coatings to improveperformance or appearance

• Recycling metals contained in end-of-life productsor in off-cuts and scrap metals arising from theindustrial supply chain

ere are some 11,100 companies in the UK metalsindustry, employing around 230,000 people anddirectly contributing nearly £10.7bn to UK GDP.

e Metals Industry also supports another 750,000employees indirectly, including contractors, suppliersand people working in the communities around metalssites, and underpins some £200bn of the UK’s GDP.

e industry is dominated by small companies but itsemployees get paid more than the UK average.

Companies in the Metals Industry operate globally,importing raw materials such as ores, coal andunprocessed metals and exporting around the world.ey compete globally too, often against theinternational suppliers who have come to dominateparts of the UK market.

Many firms are themselves part of multinational,foreign-owned enterprises, which in some casesrequires them to compete internally for investment.

Regionally, the industry is strongest in the Midlandsand North of England, and in Wales. Its importance hasdeclined in Scotland and Northern Ireland, althoughsome sectors continue to have a presence there.

The UK Metals Industryand its contribution to the national economy

Image courtesy of Graham Wylie

Contents

The UK Metals Industry and its contribution to the national economy . . . . . . . . . . . 1

The challenges and opportunities facing the UK Metals Industry . . . . . . . . . . . . . . . 2

Realising our vision Supply Chains . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

Realising our vision Innovation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

Realising our vision Skills . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

Realising our vision Circular Economy and Sustainability . . . . . . . . . . . . . . . . . . . . . . 10

Realising our vision Better representation and ensuring a level-playing field . . . 12

List of contributors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

3

The UK Metals Industry’s New Strategic Approach

Regulation

e metals industry feels it has been at the whim ofsuccessive UK governments with varied approaches tofiscal, industrial, trade, energy and environmentalpolicy from laissez-faire to actively interventionist.

On the environment, the UK has been keen to be seenas a leader in environmental policy, and tended tointerpret and enforce EU regulations more strictlythan other countries, which can put metals firms at adisadvantage.

As a low-profit industry, the Metals Industry has notbenefitted particularly from recent reductions incorporation tax. At the same time, we have seen anincrease in the taxes and charges hitting our cost base,such as business rates, which make it harder tocompete with some other parts of Europe.

Opportunities

On the other hand,the government’srenewed focus onmanufacturing, emphasis on re-establishing UK supply chains, and commitment toinfrastructure development are hugely welcome andvery significant for our industry.

e UK has ambitious plans to develop newgenerations of world-leading cars, aircraft and otherproducts, and for a major upgrade of its energy andtransport infrastructure, all of which will create extrademand for metals.

Reshoring and increased production in the UKautomotive sector, for instance, is expected to providearound £2.5bn/year of additional opportunities for theMetals Industry, while the UK’s latest nationalinfrastructure plan includes some £466bn ofinvestment up to and beyond 2020.

ese plans are reliant on metals; if these are notprovided domestically a substantial part of their valuewill be lost to the economy.

e move towards a more circular economy is also anopportunity for our industry. Metals are endlesslyreusable and recyclable, and become increasinglyattractive from a life-cycle perspective the more timesthey are reused or recycled. Circular economy businessmodels like remanufacture and product leasing may alsogive UK metals firms a competitive edge by helpingthem build closer relationships with their customers.

Achieving the Metals Industry’s vision for 2030 willrequire considerable change within the sector,including new working practices, additional investmentand a more outward-facing attitude. Full and activesupport from policymakers will also be essential.

Within each of our core themes from the 2030 visions,there are a range of sub-targets, actions andrecommendations.

Image courtesy of Tata Steel

Image courtesy of voestalpine Metsec (CBM)

2

The challenges andopportunities facing the UK Metals Industry

For generations the UK was a world leader in themetals sector, refining, processing and manufacturingmetals and metal products that were exported aroundthe world. But international change and globalisationhave caused its global market share to declinesignificantly over the last forty years and even domesticdemand has been increasingly met by imports.

As a result, important parts of the metals supply chainare located overseas and some key markets now seeminaccessible to smaller UK firms.

At the same time, recession and changes ingovernment support have upset training practices inthe industry, deterred new recruits and resulted in anageing workforce.

ere have been positive trends too, with decades oftechnological developments making metals productionmuch more efficient, less labour-intensive, and cleanerand more environmentally friendly.

Nonetheless, metals manufacture remains a very capital-intensive business with long-investment cycles leavingfirms vulnerable to changeable and unpredictablegovernment policies. Some of the most expensiveequipment in the sector is expected to run almostcontinuously for up to 12 years before refurbishment andmight not be replaced for more than 20 years. Once UKplants are closed they are rarely re-opened or replaced.

Image courtesy of Tata Steel

Image courtesy of Severfield plc

5

The UK Metals Industry’s New Strategic Approach

Encourage more local content by:

Finding new ways to incentivise end users toincreasingly source locally.

Working with government and infrastructureproviders to develop public procurement practices andpolicies that work more in favour of UK supplierswithout contravening legal frameworks.

Organising a joint UK Metals Industry / governmentPR campaign to celebrate significant UK Metalscontent examples.

Enable fitter supply chains by working withgovernment and LEPs to improve logistics andtelecommunications systems.

Commitments sought frompolicymakers:

1. A seat for the UK Metals Industry on the IndustryStrategy Council or its equivalent and specificinclusion of metals in horizontal supply chainindustrial strategy work.

2. To set andmonitor targetlevels of UK contentin public, and publiclyenabled, infrastructureprojects and find legally compliant ways to facilitate use of local content through for example, local economic benefit clauses.Explanations should be provided when measuredcontent falls significantly below target.

3. Work with the industry to celebrate significant UK metals content examples.

Initial targets:

By 2016, UK Metals Industry representation to thestrategy councils of all the industries prioritised in theindustrial strategy, and the UK Metals Industry to have aseat on the Industrial Strategy Council or its equivalent.

By the end of 2016, procurement policy for publiclyfunded infrastructure to reflect the value of locallysourced materials, and publicly enabled infrastructureprojects to have targets to source at least 50% ofmaterials locally.

Image courtesy of Sheffield Forgemasters

4

Rationale: e sector needs to engage more closelywith its key customers, ensure even the smallestcompanies at the opposite ends of supply chains areaware of their needs, and that those needs can be morethan met.

Government can also help by reviewing procurementpolicies to ensure they support domestic suppliers asmuch as possible. Existing approaches frequently focussolely on headline price, ignoring the additionalbenefits local suppliers bring to the UK economy.

Proposed actions:

Supply chain integration:

e UK Metals Industry will work with governmentand other sectors with industrial strategies tounderstand the opportunities arising in their industries,and tailor our capabilities and future investment totheir needs. e initial focus will be on Automotive,Nuclear Energy, Offshore Wind, Construction,Aerospace and Rail Supply and on smaller companiesin the metals sector. is will include a full analysis ofeach supply chain to see where the current gaps are andwhat can be done to fill them.

Opportunities for greater take up of supply chain-levelcollaboration projects will also be explored.

“By 2030, a modern and progressive UK Metals Industry will be supplyinghigh quality, innovative and competitively priced products to a wide rangeof customers. It will be the principal supplier to the UK’s mainmanufacturers and infrastructure projects, and a leading global exporter.”

Image courtesy of Airbus

Image courtesy of ALFED

Realising our vision

SupplyChains

The UK Metals Industry’s New Strategic Approach

1.2. Achieving coordination and connection:

1.2.1. Establish a virtual coordination hub tofacilitate information exchange throughsupply chains and provide expertise andguidance on innovation and accessingnew markets to SMEs. is would alsoattempt to drive the development ofregional clusters of associated industriesthat can cooperate on innovation and across-industry view of opportunitiesarising in major new industrialdevelopments such as the Internet ofings and the development of additivelayer manufacturing.

1.3. Moving the perception dial:

1.3.1 e outcome of the previous twomeasures will be communicated aswidely as possible to encourage moreparticipants and build on successes.

2. Develop proposals for better funding frameworks forlarge-scale breakthrough technology demonstration,working where necessary with other sectors, andlook for cross-sector opportunities for clustering, eg for Carbon Capture and Storage (CCS).

Commitmentssought from UKpolicymakers:

1. To contribute resources to theUK Metals Industry’s efforts to widenparticipation in R&D.

2. Incorporate the UK Metals Industry’s virtual hubinto the High Value Manufacturing (HVM)Catapult network.

3. To re-examine current support for R&D,particularly for smaller companies and in relation tolocal delivery.

4. Lead EU work on better funding frameworks forlarge-scale breakthrough technology demonstration.

Initial targets:

First SME collaboration pilot commenced by end2015. Ten SMEs should also have been supportedthrough the use of R4I and ten more throughapplication of I2SMEs.

7

Image courtesy of Pandrol UK (CBM)

Image courtesy of Advanced Forming Research Centre

6

Rationale: Process and product innovation is vital ifthe UK Metals Industry is to regain ground against itsrivals, many of whom can currently produce basicproducts more cheaply.

However, AFRC research shows most companies in thesector do not see R&D as important due to the costand perceived high rate of failure. Many demand a veryrapid payback from investments which means R&Dcannot compete against other business improvements.

On the whole, small firms also have a restricted viewof the demands of OEMs and Tier 1 suppliers and feelunable to engage with such large firms and competewith their overseas suppliers.

Government’s innovation support mechanisms arepatchy and poorly coordinated, and not well-suited tosmaller companies. Small firms also find it difficult toparticipate in signature programmes such as Catapult.

Proposed actions:

1. e UK Metals Industry has developed a three-partaction plan to address risk aversion among SMEs,bring about coordination and new connections inthe sector, and changing wider attitudes to R&D:

1.1. Addressing risk aversion:

1.1.1. Readiness for Innovation diagnostic(R4I) – A tool for assessing thecapability of a company to implementinnovation successfully. It will use astandard set of factors that are known toinfluence the process.

1.1.2. Innovations to SMEs (I2SMEs) - Aplanning framework to help companiesidentify and manage risk in innovation.is will be based around thetechniques already used in largercompanies but tailored specifically toSMEs and projects with shorttimescales. We believe this will be thefirst tool of its type specifically designedfor SMEs.

1.1.3. SME collaboration projects – ese willbring together groups of companies tocollaborate on particular short termprojects. It will aim to demonstrate thebenefits of innovation to SMEs as wellas providing successful outcomes to theprojects themselves.

“A forward-thinking, collaborative approach to R&D will haveembedded innovation throughout the industry, from the smallest firmsto the largest, directed by customers’ needs.”

Realising our vision

Innovation

Image courtesy of Advanced Forming Research Centre

9

The UK Metals Industry’s New Strategic Approach

3. Fill the current gaps in provision by:

3.1 Supporting the education sector by usingexperienced employees as trainers to pass ontheir skills to the next generation of employeesand fill gaps in provision. is might be doneon a part-time or full-time basis with suchemployees seconded to relevant schools,colleges or other training providers.

Commitments sought from UKpolicymakers:

1. To work with the Metals Industry to examine andaddress its skills needs and reduce any futuremismatch.

2. Improving the supply of candidates:

2.1. To put a greater emphasis on practical subjectsand other forms of work-based learning inschools and to ensure materials, includingmetals, is incorporated into the curriculum.

2.2. “Educate the educators” by ensuring youngpeople have access to an independent careersadviser who has knowledge of theopportunities available in the metals industry.ere must also be clarity about the steps astudent can take from starting as an apprenticeto degree-level pathways.

2.3. Extend the current Destination Measures tothe activity of school leavers after two yearsand to track the pathways they have taken.

3. Increase awarenessof trainingopportunities amongemployers and ensure whatis available is fit for purpose:

3.1 Put employers in the driving seat so they areable to demand local and relevant trainingprovision that meets the industry’s needs.

3.2 Continue to roll-out Apprenticeship Trailblazersspecifically targeting employers in the MetalsIndustry, giving them the responsibility fordesigning and developing apprenticeshipstandards that meet their needs.

3.3 Provide greater support and more responsiveprovision for companies needing to re-skill andup-skill their existing workforce.

3.4 “Bite-size” courses offering modular trainingavailable at lower cost.

4. Fill the current gaps in provision by:

4.1. Ensuring the continued roll-out of EmployerOwnership of Skills initiatives to support theMetals Industry to deliver specialist training in-house with a more flexible, modular-basedapproach to learning.

4.2. Make it easier for employers to seek fundingand accreditation for tailored in-house training,making them less reliant on third parties.

4.3. Develop qualifications and programmes oftraining outside of apprenticeships, focusing onareas such as supply chain management,leadership and general management training.

Initial targets:

To recruit and train through a partnership approach the2,300 graduates and 9,200 apprentices and techniciansthe industry is thought to require each year, aiming forcapacity to reach 50% of this level (at least 6,000people) by 2018 and 100% by 2025.

Image courtesy of voestalpine Metsec (CBM)

Image courtesy of Advanced Forming Research Centre

Image courtesy of Wilkinson Eyre

Architects

8

Rationale: To meet expected replacement demand andour wider ambitions for growth, we need to attract asteady flow of new entrants into the sector and retainand retrain those within the sector to acquire thespecific skills required for the future.

Meeting this requirement will not be without itschallenges. e sector is not seen as an attractive careerchoice for young people. In addition, there has beenan erosion of the vocational education and traininglandscape over the last few decades.

ere has been little or no focus on practical skills inschools, with a huge decline in the number of youngpeople taking practical subjects such as Design andTechnology together with the downgrading ofDiplomas, including those relevant to the metals sector.

Training for schools leavers is fragmented, oftenuncoordinated and does not meet companies’ needs.is is especially true of smaller companies which areless able to demand relevant and responsive provisionfrom training providers. Provision relevant to the metalssector has suffered as a result of some training providersnot being responsive to industry demands and nothaving the capacity or resource to invest in the facilitiesand specialist staff needed to teach relevant courses.

Some of the skills we require are generic, leaving themetals sector competing with not only other industrialsectors but those outside of the industrial sector.

Where more specific skills-sets are required, forexample metallurgy, degree-level provision andtherefore students are in short supply.

e replacement rate for an industry employingaround 230,000 people would be 5,000-6,000 a year.To support our ambitions for growth we haveestimated we need around 2,300 graduates a year and9,200 apprentices and technicians.

Successful implementation of this strategy could add50,000 high quality jobs in the UK’s metals companiesand up to 100,000 jobs in the wider economy, worthan extra £3-4bn to UK GDP by 2030.

Proposed actions:1. Improving the supply of candidates:

1.1. Work with government to re-focus parts of theschool curriculum to place a greater focus onmaterials and particularly metals, and providebetter careers advice.

1.2. Encourage universities to retain metallurgy as aseparate discipline at degree level.

2. Increase awareness of training opportunities amongemployers and ensure what is available is fit forpurpose:

2.1. Raise awareness of relevant platforms thatallow UK metals companies, particularlySMEs, to find advice and guidance onapprenticeships, and relevant brokeringinitiatives that match potential candidates tovacancies.

2.2. Encourage smaller company participation inapprenticeships through greater awareness ofGroup Training Associations that support themetals sector.

2.3. Work with government to ensure the continuedroll-out of the Employer Ownership of Skillsinitiatives to support the metals sector to deliverspecialist training in-house with a more flexible,modular-based approach to learning.

Realising our vision

Skills

“A long-term commitment to, and involvement in, education and trainingwill have created a modern, specialised workforce. e Metals Industry willbe seen as a desirable employer able to attract the highest calibre recruits.”

11

The UK Metals Industry’s New Strategic Approach

Commitments sought from UKpolicymakers:

1. Incorporate true cradle-to-cradle sustainabilitytools, such as LCA and carbon footprint assessment,in public procurement.

2. Recognise and promote metals as a permanentmaterial and maximise their use in a future circulareconomy.

3. Develop a regulatory system that supports andencourages the use of responsibly produced UK-based metals products and aids re-use,remanufacture and recycling.

4. To take forward the Industrial Decarbonisation andEnergy Efficiency Roadmap to 2050 for the steelsector over 2015 and 2016, and develop it into acomprehensive action plan.

5. Consider the roll out of similar decarbonisationroadmaps to other industrial sectors, includingother metals sectors.

Initial targets:

By 2017, establish an accredited circulareconomy standard as a keydriver for materials efficiencyacross the product lifecycle.

To have investigated the proposal for a 2050 low carbonroadmap for the metal sector by the end of 2016.

In the absence of direct government support, thiscould be an independent Metals Council project forlater endorsement by government.

For the metals sector to strongly support the draftingof a new EU circular economy package, including:• e establishment of sectoral and material-based

recycling targets.• Improved recycling definitions.• Harmonized calculations and reporting methods.• A 2025 target for ending the landfilling of

recyclable waste.• e harmonisation of ecodesign criteria.

Image courtesy of Grainger and Worrall

Image courtesy of Metal Packaging Manufacturers Association

10

Rationale: Policymakers are keen to move towards a more circular economy, replacing the use of virginresources and discard of end-of-life products withsystems based on repair, re-use, remanufacture and recycling.

Metals are an excellent fit with this agenda as they arewell-suited to reuse, remanufacture and endlesslyrecyclable, amortising the initial energy used in theirextraction over many generations of products.

However, capturing the full environmental benefits ofmetal products also requires good product design toensure components can be easily disassembled and asupportive regulatory environment.

Proposed actions:

1. To work with government and other industrialsectors to develop actions in support of creating acircular economy, including:

1.1. More widespread use of Life Cycle Analysis(LCA) and carbon footprinting methods thatreflect the real value of metals.

1.2. Promotion of metals as a material capable oftrue recycling and re-use instead of down-cycling into less valuable products.

1.3. Advocating product design strategies that aideventual separation and re-use or recycling.

1.4. More appropriate definitions of wastes andprocess by-products, particularly those deemedas hazardous wastes, to maximise re-use andrecycling of metals and process by-products.

1.5. Measures to support increased resourceefficiency and responsible sourcing, includingworking with supply chains and providing themwith guidance on best practice (eg BES6001)

1.6. Full participation in UK 2050 low-carbonroadmap project and European resourceefficiency agenda.

2. To develop a sustainability best practice exchangefor the UK Metals Industry, aimed particularly atsmaller companies.

Realising our vision

Circular Economy and Sustainability

“Metals and metal products will be at the heart of the new circulareconomy, recognising their innate potential for resource-efficient reuse,remanufacture and recycling.”

Image courtesy of BMRA

12

Rationale: A Metals Council led by senior industryfigures would help deliver the metal sector's newstrategic approach and ensure it leads to a sustainablegrowth-led future for the industry.

It would also improve the way the UK Metals Industrycommunicates its messages and enable it to speak withauthority to government, other industries, and educators.

e industry is often put at a disadvantage toEuropean and other competitors when it comes to taxand environmental policies. Other issues where moresupport from policymakers is needed includeinternational competition for raw materials,prevention of dumping, and access to finance.

Proposed actions:

1. CEO-level commitment and engagement with theMetals Industry's new strategic approach.

2. Metals Council formed to drive forward the newstrategic approach.

3. Work with government to ensure that taxation,regulation and the UK’s energy and carbon policyframework supports long-term economicsustainability as well as environmentalresponsibility and is appropriately tailored to theMetals Industry’s needs.

Commitments sought from UKpolicymakers:

1. Ministerial-level commitment and engagement withthe UK Metals Industry's new strategic approach.

2. To utilise the new Metals Council as a coreconsultative body and offer occasional Ministerialpresence at enhanced meetings of the Metals Council.

3. To ensure a fair and fit-for-purpose taxation andregulatory landscape that reflects the particularcharacteristics of the UK Metals Industry.

Initial targets:

Metals Council established in 2015.

Establish and track objective measures of internationalcompetitiveness for key parts of the metals industry by 2016.

Realising our vision

Better representation andensuring a level-playing field

“e industry will be represented by a Metals Council and will have workedwith government to ensure a balanced regulatory environment that putsUK metals firms on a level playing field with overseas competitors.”

Image courtesy of Galvanizers’ Association

17

The UK Metals Industry’s New Strategic Approach

Lee Adcock OutokumpuSimon Alexander Sheffield Forgemasters

Engineering LtdJohn Baker SSI UKPaul Barker British Stainless Steel AssociationGeraldine Bolton Confederation of British

MetalformingJon Bolton TATA Steel EuropeJames Booth Smiths Metal CentresRoz Bulleid EEFJane Campion Mabey BridgeGraeme Carus EMRMike Castellucci Hadley IndustriesCorina Cato Billington StructuresPeter Corfield National Association of Steel

Service CentresJo Davies SSI UKHenry Dickinson Norton AluminiumJohn Dowling British Constructional Steelwork

AssociationMartin Drinkall KierMartin Dudley omas Dudley Ltd (Dudley)James Ellis Celsa SteelDeirdre Fox TATA Steel Ian Goldsmith ConsultantIan Halstead Confederation of British

MetalformingPaul Harvey Böhler Uddeholm (Voest Alpine)Ian Hetherington British Metals Recycling AssociationRupert Hodges Metals ForumJames Hughes AMRC University of SheffieldAlasdair Jackson Recycle Lives Iqbal Johal Galvanizers’ AssociationPeter Johnson KierNeil Lawley Afon Tinplate Co LtdPatrick Lawson Maybey BridgeDavid Leggett MetsecColin Leighfield BE Wedge Holdings LtdPeter Lennon TATA Steel EuropeNorman Lett Ball Trading UK

Chris MacDonald Materials Processing InstituteArchie MacPherson AFRCSarah McCann-Bartlett British Constructional Steelwork

AssociationMichele McNeill William KingChris Meredith Amari Metals LtdSteve Morley Sertec GroupTim Morris TATA Steel EuropeNick Mullen Metal Packaging Manufacturers

AssociationPam Murrell Cast Metals FederationDavid New Lean Engineering and

Manufacturing AcademyAdrian Nicklin Confederation of British

MetalformingDavid Ollier TATA SteelColin Parker Black Country ConsortiumSimon Pike TATA Steel Adrian Platt BEFESA Salt SlagsPeter Quinn TATA Steel Phil Rawnson MRT Castings Ltd (Andover)Roy Rickhuss CommunityIan Rodgers UK SteelAidan Ruddock Crown Food EuropeChrissie Sabine OutokumpuWill Savage Aluminium FederationDavid Scott TATA Steel UKGraham Small AMRC Training CentreWilliam Smith Galvanizers’ AssociationMike Smith AtotechGareth Stace UK SteelCarl Tomlinson Tomburn LtdBen Towe Hadley IndustriesIan Walsh Saint Gobain PAM UK Ltd

(Ilkeston) Nigel Ward Nickel InstituteChris Woolridge Wedge Group GalvanizingAndrew Worley William KingBarry Yeomans Hadley Industries

List of contributors

Metals Forumwww.metalsforum.org

07939 722 447

Aluminium Federationwww.alfed.org.uk

0121 601 6363

British Constructional Steelwork Associationwww.steelconstruction.org

020 7839 8566

British Metals Recycling Associationwww.recyclemetals.org

01480 455 249

British Stainless Steel Associationwww.bssa.org.uk0114 292 2638

Cast Metals Federationwww.castmetalsfederation.com

0121 601 6390

Confederation of British Metalformingwww.britishmetalforming.com

0121 601 6350

Galvanizers Associationwww.galvanizing.org.uk

0121 355 8838

Metal Packaging Manufacturers Associationwww.mpma.org.uk

0118 978 8433

National Association of Steel Service Centreswww.nass.org.uk0121 200 2288

UK Steelwww.eef.org.uk/uksteel

020 7654 1518