Vision 2014: The Evolving Landscape of Customer Management

20

©2014 Experian Information Solutions, Inc. All rights reserved. Experian and the marks used herein are service marks or registered trademarks of Experian Information Solutions, Inc. Other product and company names mentioned herein are the trademarks of their respective owners. No part of this copyrighted work may be reproduced, modified, or distributed in any form or manner without the prior written permission of Experian. Experian Public. The evolving landscape of customer management Gordon Cameron PNC Scott Henry Experian #vision2014

-

Upload

experian -

Category

Data & Analytics

-

view

101 -

download

1

description

"Expanding data and the need to identify and act on the value of greater customer information have significantly affected customer decisioning. Cross-selling, exposure management, risk-based pricing and relevancy scoring can all be refined with the power of greater customer information — and new revenue streams can be created. However, effectively harnessing this information requires an integrated approach to data, customer and analytics processes. This session will provide Experian’s point of view on the direction many of our key accounts are looking to in next-generation decisioning.

Transcript of Vision 2014: The Evolving Landscape of Customer Management

© 2014 Experian Information Solutions, Inc. All rights reserved. Experian and the marks used herein are service marks or registered trademarks of Experian Information Solutions, Inc.

Other product and company names mentioned herein are the trademarks of their respective owners. No part of this copyrighted work may be reproduced, modified, or distributed in

any form or manner without the prior written permission of Experian. Experian Public.

The evolving landscape of customer management

Gordon Cameron PNC

Scott Henry Experian

#vision2014

2 © 2014 Experian Information Solutions, Inc. All rights reserved. Experian Public.

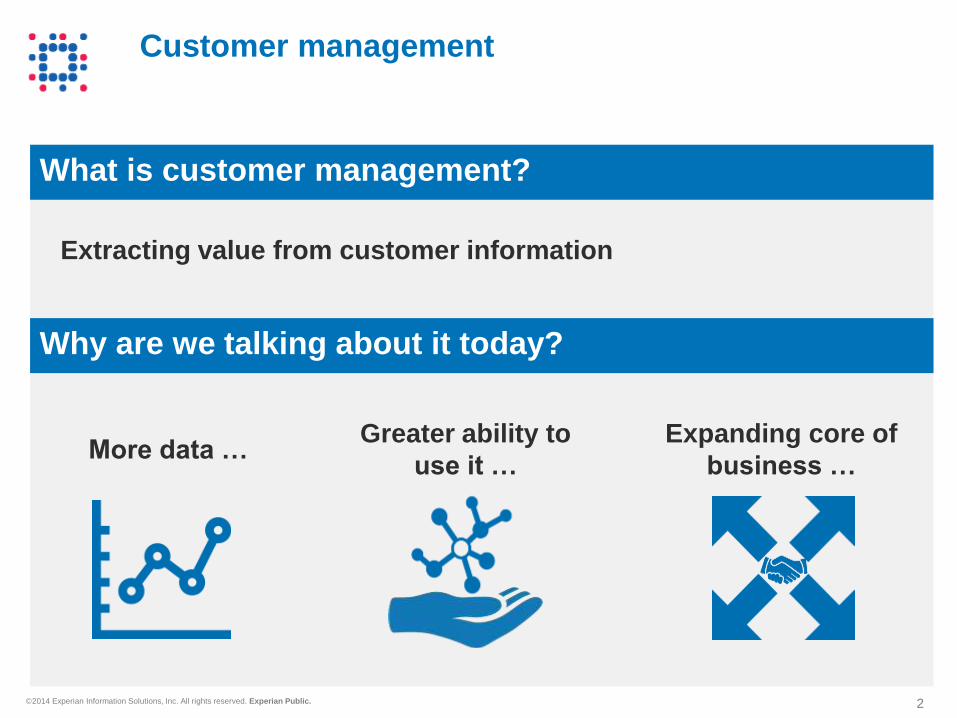

Customer management

Why are we talking about it today?

What is customer management?

Extracting value from customer information

More data … Greater ability to

use it …

Expanding core of

business …

3 © 2014 Experian Information Solutions, Inc. All rights reserved. Experian Public.

Customer management elements

1

2

3 4

5

Data

Listen and

detect

Decision

management Offer

presentation

Feedback

loop

Enterprise customer data

Unique ID Payment history

Transactions Eligible offers

Bureau data Response history

4 © 2014 Experian Information Solutions, Inc. All rights reserved. Experian Public.

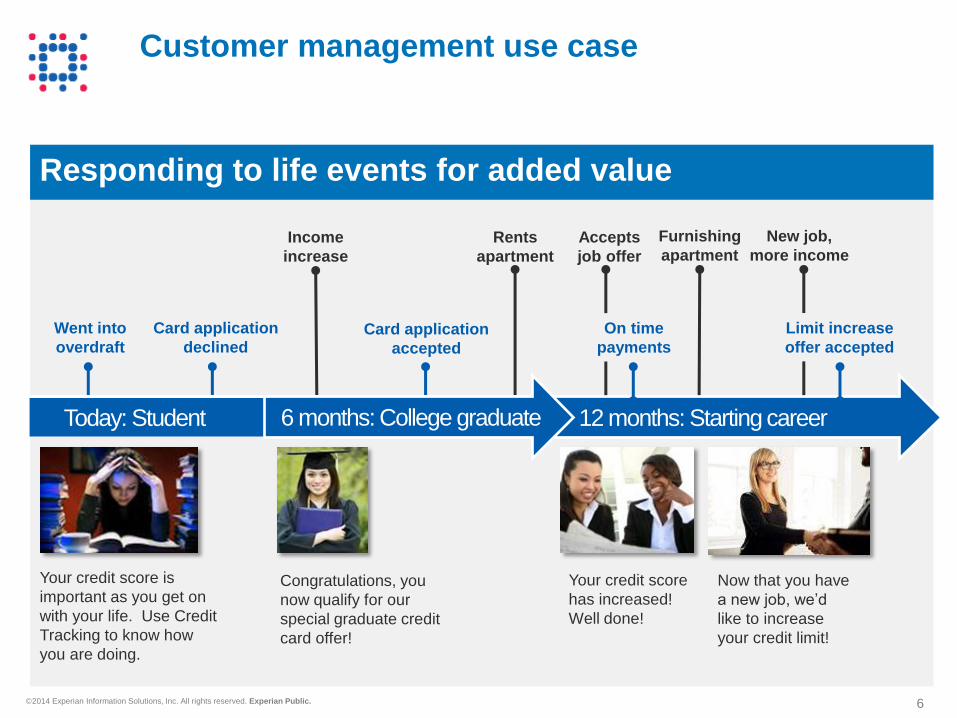

Went into

overdraft

Card application

declined

Today: Student

Customer management use case

Your credit score is

important as you get on

with your life. Use Credit

Tracking to know how

you are doing.

Responding to life events for added value

5 © 2014 Experian Information Solutions, Inc. All rights reserved. Experian Public.

Customer management use case

Congratulations, you

now qualify for our

special graduate credit

card offer!

Your credit score is

important as you get on

with your life. Use Credit

Tracking to know how

you are doing.

Responding to life events for added value

Went into

overdraft

Card application

declined

Today: Student

Rents

apartment

Income

increase

Card application

accepted

6 months: College graduate Today: Student

6 © 2014 Experian Information Solutions, Inc. All rights reserved. Experian Public.

Customer management use case

Your credit score

has increased!

Well done!

Congratulations, you

now qualify for our

special graduate credit

card offer!

Your credit score is

important as you get on

with your life. Use Credit

Tracking to know how

you are doing.

Now that you have

a new job, we’d

like to increase

your credit limit!

Responding to life events for added value

Went into

overdraft

Card application

declined

Today: Student 6 months: College graduate

Rents

apartment

Income

increase

Card application

accepted

Accepts

job offer

New job,

more income

Furnishing

apartment

Limit increase

offer accepted

On time

payments

12 months: Starting career 6 months: College graduate

7 © 2014 Experian Information Solutions, Inc. All rights reserved. Experian Public.

Optimize current business and extend customer relationships

Using unique customer insight, grow

outside of your traditional business:

Market external propositions

Enter adjacencies

Increase cross sell revenue through

lifestyle triggers

Optimize offer pricing

Reduce turnover through optimising

attrition models

Enhance pre-delinquency models

Improve current

business

REFINE

Extend customer

relationships

TRANSFORM

8 © 2014 Experian Information Solutions, Inc. All rights reserved. Experian Public.

Customer management

in financial services

Gordon Cameron

PNC

Executive Vice President,

Chief Consumer Credit Officer

9 © 2014 Experian Information Solutions, Inc. All rights reserved. Experian Public.

Bulk mailings

Large, difficult to

access systems

Smaller banks still

relying on paper

Drive to digital

Consolidated

marketing files –

moving toward

integrated customer

information systems

Bank mergers

Integrated systems

Large institutions

working to digest

acquisitions

Big Data talk track

Understanding the

New Normal of

consumers,

competition and

regulation

1990s Early 2000s Late 2000s 2010s

Large scale technology investment as a tier differentiator

Understanding customers is levelling the playing field

Financial services timeline

10 © 2014 Experian Information Solutions, Inc. All rights reserved. Experian Public.

The goal is to turn customer data into actionable insight that drives a scalable, sustainable and compliant customer relationship agenda

Harvesting insights and opportunities within the customer base

R A P I D LY E V O LV I N G C O N S U M E R

Macro environmental changes

Household balance sheets

Demographics

The economy

B E S T D AT A I S H A R D T O

A N A LY Z E

Deposit account data

Transaction data online and

credit card

Customer “career path”

11 © 2014 Experian Information Solutions, Inc. All rights reserved. Experian Public.

The big picture of consumer balance sheets

Home prices are

stable to increasing

across most markets

Household debt ratios

are returning to long term

trend line

12 © 2014 Experian Information Solutions, Inc. All rights reserved. Experian Public.

Demographics will shape the customer landscape profoundly over the next half decade

Estimated Change in Population Distribution w ith Current Spend

Distribution

-20%

-10%

0%

10%

20%

30%

40%

50%

<25 25-34 35-44 45-54 55-64 65-74 >=75

Age Group

Delta 2010/2020

Population

DistributionSpend Distribution

Average Score at Time of Inquiry

620

640

660

680

700

720

740

760

780

Overall Auto Mortgage Bankcard

Asset Class

Sco

re

2006 2010 2013

Demographic changes are

shaping the future of

spending and consumption

Credit seeking customers are

returning to long term trends

after a period of austerity

13 © 2014 Experian Information Solutions, Inc. All rights reserved. Experian Public.

Income segmentation Using DDA data to its best potential

Challenge

Identify patterns in transaction data that we did not know before, or we could not see

before, that can help increase customer value

Analytic solution Test and learn approach

Customer behavior analysis

Segmentation analysis of DDA

customers by unique

deposit/income streams

Development of triggers based on

behavioral changes

DDA based models for income

predictions

Outcomes:

Significant predictive value

in analyzing the

transactions and their

associated footprints

Better understanding of

Risk, depth of customer

relationship profile and a

set of tactics to address

changes

14 © 2014 Experian Information Solutions, Inc. All rights reserved. Experian Public.

Transaction level data

Point of sale /

payments

Merchant

Geography /

proximity

Amount

Web

Credit cards

Point of sale

ATM

Internet transactions

Debit cards

ACH payments

ACH deposits

Income statements

Purchases

Checking accounts

Open lines of credit

New loan

originations

Payments

Other loans

Teller transactions

Platform visits

Branch

15 © 2014 Experian Information Solutions, Inc. All rights reserved. Experian Public.

Transaction level analytic techniques

The periodic nature of deposit and

payment information can be

understood through non traditional

techniques like Fourier series

Borrowing from other disciplines we

can determine appropriate signal

filtering mechanisms (example:

Schmitt triggers and hysteresis)

16 © 2014 Experian Information Solutions, Inc. All rights reserved. Experian Public.

Categorization of customer behavior

Comb Shaped Filter

0

200

400

600

800

1000

1200

1400

1600

Auto

Payment

CreditCard Mortgage Credit Card Cable/phone Cell Phone Insurance Transfer to

savings

0

X 4 X 3 X 1 X 2

XX 3 4 XX 2 4 XX 1 4 XX 2 3 XX 1 3 XX 1 2

XXX 1 2 3 XXX 2 3 4

1

XXX 1 2 4 XXX 1 3 4

Comb shaped filtering provides

a baseline of behavior and

information-theoretic

compression opportunities

The customer “career path”

creates something similar to a

Boolean Lattice structure and

provides deep insight in to

profit potential and product

offer cadence

17 © 2014 Experian Information Solutions, Inc. All rights reserved. Experian Public.

DNA – The core building blocks

Dynamic Needs-based Attributes (DNA)

Leverages position and momentum

rather than static profiling

Multiple objective functions

Attempts to understand and identify

changes in behavior more rapidly as

well as estimate likely future changes

This is the foundation around which we create strategies

18 © 2014 Experian Information Solutions, Inc. All rights reserved. Experian Public.

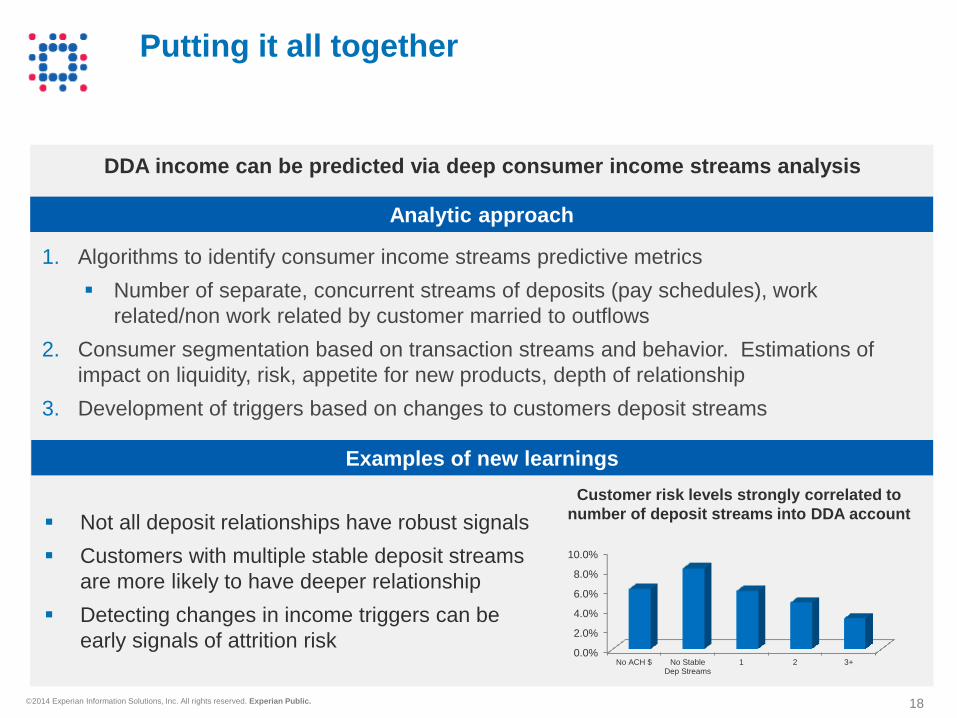

Putting it all together

1. Algorithms to identify consumer income streams predictive metrics

Number of separate, concurrent streams of deposits (pay schedules), work

related/non work related by customer married to outflows

2. Consumer segmentation based on transaction streams and behavior. Estimations of

impact on liquidity, risk, appetite for new products, depth of relationship

3. Development of triggers based on changes to customers deposit streams

Examples of new learnings

Not all deposit relationships have robust signals

Customers with multiple stable deposit streams

are more likely to have deeper relationship

Detecting changes in income triggers can be

early signals of attrition risk

Customer risk levels strongly correlated to

number of deposit streams into DDA account

DDA income can be predicted via deep consumer income streams analysis

Analytic approach

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

No ACH $ No StableDep Streams

1 2 3+

19 © 2014 Experian Information Solutions, Inc. All rights reserved. Experian Public.

For additional information, please contact:

Hear the latest from Vision 2014

in the Daily Roundup:

www.experian.com/vision/blog

@ExperianVision | #vision2014

Follow us on Twitter

20 © 2014 Experian Information Solutions, Inc. All rights reserved. Experian Public.

Visit the Experian Expert Bar to learn more about

the topics and products covered in this presentation.