Villalonga and McGahan - College of Business at Illinois

26

Strategic Management Journal Strat. Mgmt. J., 26: 1183–1208 (2005) Published online in Wiley InterScience (www.interscience.wiley.com). DOI: 10.1002/smj.493 THE CHOICE AMONG ACQUISITIONS, ALLIANCES, AND DIVESTITURES BEL ´ EN VILLALONGA 1 * and ANITA M. MCGAHAN 2 1 Harvard Business School, Boston, Massachusetts, U.S.A. 2 School of Management, Boston University, Boston, Massachusetts, U.S.A. This paper investigates how firms choose among acquisitions, alliances, and divestitures when they decide to expand or contract their boundaries. The dataset covers 9276 deals announced and completed by 86 members of the Fortune 100 between 1990 and 2000. Our findings support explanations based on resources, transaction costs, internalization, organizational learning, social embeddedness, asymmetric information, and real options, and suggest that these theories are highly related and complementary. We find less consistent support for theories based on agency costs and asset indivisibilities. The strong role of firm attributes explains in part why firms may pre-specify whether they will pursue acquisitions, alliances, or divestitures as part of their corporate strategies. Copyright 2005 John Wiley & Sons, Ltd. INTRODUCTION This paper examines the acquisitions, alliances, and divestitures of a group of large firms during the 1990s to evaluate how these firms chose to conduct transactions that expanded and contracted their boundaries. Acquisitions, alliances, and divesti- tures are strategic alternatives along a continuum of governance modes (Williamson, 1975, 1991; Hennart, 1993): 1 Acquisitions represent greater integration at one end of the continuum, while Keywords: acquisitions; alliances; divestitures; gover- nance form; firm boundaries ∗ Correspondence to: Bel´ en Villalonga, Harvard Business School, Soldiers Field, Boston, MA 02163, U.S.A. E-mail: [email protected] 1 For instance, Child (1987) mentions the following legal forms of organization along such a continuum: firms, mutual orga- nizations (consortia) and joint ventures, subcontracting, licens- ing and franchising, and market transacting between indepen- dent traders. Contractor and Lorange (1988) provide a simi- lar ranking of various types of alliances in order of increas- ing interorganizational dependence: equity joint ventures, non- equity alliances in exploration, research and/or development, marketing alliances, know-how licensing, franchising, patent divestitures represent less integration at the other end (Klein, Crawford, and Alchian, 1978; Devlin and Bleackley, 1988; Mulherin and Boone, 2000; Sanders, 2001). In the middle of the spectrum are alliances and joint ventures, which typically confer upon firms the option for a subsequent acquisition or divestiture (Kogut, 1991; Chi, 2000; Folta and Miller, 2002). The choice to organize a particular transaction as an alliance instead of as a divesti- ture is analogous to the choice between an alliance and an acquisition; for example, when two firms negotiate to transfer rights for operating a business, the choice between an acquisition and an alliance for one of the firms amounts to a choice between a divestiture and an alliance for the firm on the other side of the transaction. Earlier empirical studies of boundary choice largely fall into three groups. A first group of studies looks at the alternative governance struc- tures that are found in a specific industry: making licensing, production/assembly/buyback agreements, and tech- nical training/start-up assistance agreements. Copyright 2005 John Wiley & Sons, Ltd. Received 13 June 2003 Final revision received 11 May 2005

Transcript of Villalonga and McGahan - College of Business at Illinois

Strategic Management JournalStrat. Mgmt. J., 26: 1183–1208 (2005)

Published online in Wiley InterScience (www.interscience.wiley.com). DOI: 10.1002/smj.493

THE CHOICE AMONG ACQUISITIONS, ALLIANCES,AND DIVESTITURES

BELEN VILLALONGA1* and ANITA M. MCGAHAN2

1 Harvard Business School, Boston, Massachusetts, U.S.A.2 School of Management, Boston University, Boston, Massachusetts, U.S.A.

This paper investigates how firms choose among acquisitions, alliances, and divestitures whenthey decide to expand or contract their boundaries. The dataset covers 9276 deals announcedand completed by 86 members of the Fortune 100 between 1990 and 2000. Our findings supportexplanations based on resources, transaction costs, internalization, organizational learning,social embeddedness, asymmetric information, and real options, and suggest that these theoriesare highly related and complementary. We find less consistent support for theories based onagency costs and asset indivisibilities. The strong role of firm attributes explains in part whyfirms may pre-specify whether they will pursue acquisitions, alliances, or divestitures as part oftheir corporate strategies. Copyright 2005 John Wiley & Sons, Ltd.

INTRODUCTION

This paper examines the acquisitions, alliances,and divestitures of a group of large firms during the1990s to evaluate how these firms chose to conducttransactions that expanded and contracted theirboundaries. Acquisitions, alliances, and divesti-tures are strategic alternatives along a continuumof governance modes (Williamson, 1975, 1991;Hennart, 1993):1 Acquisitions represent greaterintegration at one end of the continuum, while

Keywords: acquisitions; alliances; divestitures; gover-nance form; firm boundaries∗ Correspondence to: Belen Villalonga, Harvard BusinessSchool, Soldiers Field, Boston, MA 02163, U.S.A.E-mail: [email protected] For instance, Child (1987) mentions the following legal formsof organization along such a continuum: firms, mutual orga-nizations (consortia) and joint ventures, subcontracting, licens-ing and franchising, and market transacting between indepen-dent traders. Contractor and Lorange (1988) provide a simi-lar ranking of various types of alliances in order of increas-ing interorganizational dependence: equity joint ventures, non-equity alliances in exploration, research and/or development,marketing alliances, know-how licensing, franchising, patent

divestitures represent less integration at the otherend (Klein, Crawford, and Alchian, 1978; Devlinand Bleackley, 1988; Mulherin and Boone, 2000;Sanders, 2001). In the middle of the spectrum arealliances and joint ventures, which typically conferupon firms the option for a subsequent acquisitionor divestiture (Kogut, 1991; Chi, 2000; Folta andMiller, 2002). The choice to organize a particulartransaction as an alliance instead of as a divesti-ture is analogous to the choice between an allianceand an acquisition; for example, when two firmsnegotiate to transfer rights for operating a business,the choice between an acquisition and an alliancefor one of the firms amounts to a choice between adivestiture and an alliance for the firm on the otherside of the transaction.

Earlier empirical studies of boundary choicelargely fall into three groups. A first group ofstudies looks at the alternative governance struc-tures that are found in a specific industry: making

licensing, production/assembly/buyback agreements, and tech-nical training/start-up assistance agreements.

Copyright 2005 John Wiley & Sons, Ltd. Received 13 June 2003Final revision received 11 May 2005

1184 B. Villalonga and A. M. McGahan

vs. buying auto parts in the automobile industry(Monteverde and Teece, 1982), equity alliancesvs. non-equity alliances in biotechnology (Pisano,1989), in-house vs. external R&D procurementin pharmaceutical firms (Pisano, 1990), company-owned gasoline stations vs. lessee-dealer and open-dealer stations (Shepard, 1993), equity alliances vs.bilateral and unilateral non-equity alliances in tech-nology transfers (Oxley, 1997), etc. Shelanski andKlein (1995) provide a comprehensive review ofthe studies in this first group. A second group looksat the choices that firms make between acquisitionsand alliances. These choices have long been stud-ied in the context of foreign market entry (e.g.,Anderson and Gatignon, 1986; Kogut and Singh,1988; Hennart and Reddy, 1997; Shaver, 1998),but recent studies have begun to investigate themin more general terms (Dyer, Kale, and Singh,2004). A third group of studies examines jointdecisions by two or more firms to ally (see Gulati,1998, for a review) and/or to merge (Vanhaver-beke, Duysters, and Noorderhaven, 2002). Thestudies in each of these three groups use differ-ent units of analysis: the transaction, the firm, andthe dyad, respectively. As a result, each confers asomewhat different perspective on issues that arerelated to the choice of acquisitions, alliances, anddivestitures.

While there has been extensive study of thechoice to make vs. buy, there has been little studyof the choice between selling vs. buying or mak-ing. Yet there is no clear reason for this omission.As Klein et al. (1978) argue, from a transactionalperspective, both divestitures and acquisitions rep-resent reactions to changes in the transaction costscreated by specialized assets. From the perspectiveof the firm, divestitures and alliances are alterna-tive ways to contract boundaries, just as acquisitionand alliances are alternative ways to expand them.For dyads, divestitures are a way of allocating con-trol of resources between the parties. For example,suppose that a large firm controls activities or ownsassets that would be more valuable in combinationwith those of a smaller firm. The two firms havethree choices: the large firm can acquire the activi-ties and assets of the small firm; the two firms canally; or the large firm can sell its own activities andassets through a divestiture to the small firm. Whatconstitutes a divestiture for one firm in the dyad isan acquisition for the other. Volkswagen AutoEu-ropa provides a good case in point. In 1991, Fordand Volkswagen formed a joint venture in Portugal

named AutoEuropa to enter the minivan segmentof the European market. Ford was in charge ofbuilding the plant, while Volkswagen took respon-sibility for designing the product. In 1999, the twopartners agreed to have Volkswagen buy out Ford’sstake in the venture, thus creating an acquisitionfrom Volkswagen’s perspective and a divestiturefrom Ford’s perspective.

There are other important antecedents to thisstudy. An extensive literature in strategy, eco-nomics, and finance investigates the motives forcontracting firm boundaries, a practice some-times referred to as downsizing, downscoping, orrefocusing (Harrigan, 1982; Duhaime and Grant,1984; Montgomery, Thomas, and Kamath, 1984;Montgomery, 1988; Bethel and Liebeskind, 1993;Hoskisson and Hitt, 1994; Hoskisson, Johnson,and Moesel, 1994; Mitchell, 1994; John and Ofek,1995; Daley, Mehrotra, and Sivakumar, 1997;Berger and Ofek, 1999; etc.). Part of this lit-erature focuses on divestitures of prior acqui-sitions (Porter, 1987; Ravenscraft and Scherer,1987; Kaplan and Weisbach, 1992; Berger andOfek, 1996). In addition, two studies have com-pared divestitures to acquisitions. Mulherin andBoone (2000) compare the industry patterns andwealth effects of acquisitions and divestitures.Their results support synergistic over agency the-oretic explanations for acquisitions and divesti-tures, although they do not test directly for thedeterminants of the choice. Sanders (2001) viewsacquisitions and divestitures as alternative waysto increase the value of stock options, and findsevidence that executives make decisions to influ-ence the value of their personal holdings. Only afew studies examine boundary-contracting modes.Slovin, Sushka, and Ferraro (1995), Khan andMehta (1996), Nixon, Roenfeldt, and Sicherman(2000), and Powers (2004) analyze the financialdeterminants of the choice to spin-off vs. sell-off activities, but none of these studies comparesdivestitures to alternative boundary-contractingmodes.

In this paper, we study a broad range of strategicoptions available to firms along the full integra-tion continuum: acquisitions (including mergers,full or majority acquisitions, and minority acquisi-tions), alliances (including joint ventures and otherequity alliances as well as non-equity alliances intechnology, R&D, manufacturing, or marketing,and licensing), and divestitures (including spin-offs and sell-offs). Our sample includes all of the

Copyright 2005 John Wiley & Sons, Ltd. Strat. Mgmt. J., 26: 1183–1208 (2005)

Acquisitions, Alliances, and Divestitures 1185

9276 acquisitions, alliances, and divestitures by 86members of the Fortune 100 during the 1990s. Byincluding deals of all three types for this groupof firms, the analysis allows us to make infer-ences about choices to change firm boundaries,that is, about the dynamics of boundary deci-sions.

Our primary analyses consider the full con-tinuum of available choices from acquisitions todivestitures, which we divide into either threeor seven discrete alternatives. The results ofthese analyses should be interpreted as condi-tional on the firm having already decided to under-take a boundary-changing transaction. Becausethe motives underlying such decisions may dif-fer between boundary-expanding and boundary-contracting decisions, we also analyze separatelythe choice between two types of decisions: thechoice between acquisition and alliances (i.e.,boundary expansion) and the choice betweenalliances and divestitures (i.e., boundary contrac-tion). We take the firm as our unit of analysisand draw on the transactional and dyadic perspec-tives by considering how firm choice is influencedby the attributes of the focal firm, the target orpartner firm, the transaction, the dyad, and therelationship between the focal firm and the trans-action.

We base our hypotheses on a variety oftheories: the resource-based view, transaction costeconomics, internalization theory, agency theory,asymmetric information, asset indivisibilities,organizational learning, and social embeddedness.All of these theories have been validatedempirically as relevant to boundary-spanningtransactions (Zajac and Olsen, 1993; Gulati, 1995;Hennart and Reddy, 1997; Capron and Mitchell,1998; Poppo and Zenger, 1998). Because thesetheories offer complementary and even coincidingpredictions, we do not treat them as competing.Our approach is to test for candidate explanationswhile controlling simultaneously for alternativetheoretical mechanisms.

THEORY AND HYPOTHESES

The analysis draws on different theoretical per-spectives to identify potential determinants of thechoice of governance mode. Because the unitof analysis is the firm, our emphasis is on theattributes of the focal firm and its interaction with

both the target/partner firm and the transaction. Wealso control for certain attributes of the transactionand of the target/partner firm in our tests of theory.Figure 1 summarizes our assessment of relevantattributes.

Focal firm attributes

Intangible resources

The dominant theoretical paradigms in thestudy of market entry modes are the resource-based view and transaction cost economics. ThePenrose–Teece view of diversification posits thata firm’s entry into new product markets resultsfrom excess capacity in valuable resources thatmay be transferable across firms but subject tomarket imperfections (Penrose 1959; Teece, 1980,1982). The internalization theory of multinationalfirms, while developed independently (Hymer,1976; Caves, 1971; Dunning, 1973), makes asimilar argument about the mechanism of entryinto new geographic markets, and has been appliedextensively in studies of foreign market entry andperformance (e.g., Anderson and Gatignon, 1986;Kogut and Singh, 1988; Morck and Yeung, 1992;Hennart and Reddy, 1997; Shaver, 1998).

This theory highlights the role of intangible cap-ital such as a firm’s technological and market-ing resources, which are particularly vulnerableto appropriation by partnering firms in alliancesor in market exchanges. As a result, firms maychoose more integrative forms of governance suchas acquisitions when their technological knowl-edge capital is highly valuable. Likewise, becausebrand capital cannot be easily shared across part-ners except through extensive internal coordina-tion of activities, advertising-intensive firms mayopt for greater integration for their transactions.Because appropriability hazards are higher amongdirect competitors, these arguments are at least aslikely to apply to horizontal expansion and con-traction of firm boundaries as they are to diversi-fication and internationalization. Thus:

Hypothesis 1a: The firm’s technologicalresources are associated with the choice ofacquisitions over alliances, and alliances overdivestitures.

Hypothesis 1b: The firm’s marketing resourcesare associated with the choice of acquisitionsover alliances, and alliances over divestitures.

Copyright 2005 John Wiley & Sons, Ltd. Strat. Mgmt. J., 26: 1183–1208 (2005)

1186 B. Villalonga and A. M. McGahan

Figure 1. Determinants of the choice among alliances, acquisitions, and divestitures

Ownership structure

Agency-theoretic arguments explain why man-agers may engage in boundary-spanning transac-tions such as acquisitions even when the trans-actions may be detrimental to shareholder value(Jensen and Meckling, 1976; Jensen, 1986). Tomaximize the assets under the firm’s control, theexecutive has an incentive to pursue acquisitionsover alliances and alliances over divestitures. Inlarge public corporations, two features of theirownership structure can be used to mitigate agencyproblems: large insider ownership, which alignsmanagerial incentives with those of other share-holders, and monitoring by large blockholderssuch as institutions (Bethel and Liebeskind, 1993;Denis, Denis, and Sarin, 1997; Sanders, 2001).

Hypothesis 2a: The level of insider ownership ofthe firm is associated with the choice of divesti-tures over alliances, and alliances over acquisi-tions.

Hypothesis 2b: The level of blockholder own-ership of the firm is associated with the choice

of divestitures over alliances, and alliances overacquisitions.

Hypothesis 2c: The level of institutional own-ership of the firm is associated with the choiceof divestitures over alliances, and alliances overacquisitions.

Acquisition, alliance, and divestiture experience

From an organizational learning perspective, thevalue generated by an acquisition or an alliancedepends on a firm’s acquisition or alliance capabil-ities, which firms develop through repeated expe-rience with these governance forms (Dyer andSingh, 1998; Haleblian and Finkelstein, 1999;Anand and Khanna, 2000; Hayward, 2002; Kale,Dyer, and Singh, 2002). The theoretical logicextends naturally to cover divestitures: firms withexperience in divestitures may be more effective atmanaging disintegration than firms without priorexperience. Allen (1998) suggests this explana-tion for Thermoelectron’s repeated success at spin-ning off and carving out equity in its activities.Under this view, a firm’s experience at manag-ing a particular governance form makes the firm

Copyright 2005 John Wiley & Sons, Ltd. Strat. Mgmt. J., 26: 1183–1208 (2005)

Acquisitions, Alliances, and Divestitures 1187

more inclined to choose the same form for futuretransactions.

Hypothesis 3a: The firm’s acquisition experienceis associated with the choice of acquisitions overboth alliances and divestitures.

Hypothesis 3b: The firm’s divestiture experienceis associated with the choice of divestitures overboth alliances and acquisitions.

Hypothesis 3c: The firm’s alliance experience isassociated with the choice of alliances over bothacquisitions and divestitures.

Prior diversification

The three theories discussed above also offerpredictions about the effect of a firm’s priorlevel of diversification on its governance choices.First, resources and transaction costs views sug-gest that corporate growth depends not only onfirm resources but also on the applicability ofresources across industries and on the potential foreconomies of scope offered by different resourcecombinations. Coase (1972) argues that internalorganization costs are likely to be higher whenthere is dissimilarity between the activities of thetransaction and of the firm because the lack of aprecedent within the firm creates greater demandson the organization’s structure. On the other hand,the greater the level of prior diversification, thegreater the likelihood of commonalities with theactivities of the transaction, and thus the greaterthe likelihood of integrating the activities ex post.

Second, agency theory suggests diversificationas a self-serving action that managers take toincrease their compensation, power, or prestige(Jensen, 1986; Jensen and Murphy, 1990), tobecome entrenched (Shleifer and Vishny, 1989), orto reduce their personal risk by reducing total firmrisk (Amihud and Lev, 1981). Thus, one wouldexpect a firm’s level of diversification to be neg-atively related to the equity ownership of bothmanagers and outside blockholders (Denis et al.,1997). Support for Hypotheses 2a–c implies thatprior diversification is also positively associatedwith the choice of an integrative governance form.

Third, because diversification almost alwaysresults from prior acquisitions, firms that arehighly diversified are also likely to have prior

acquisition experience. Hypothesis 3a also reflectsthis regularity.

The implication of all three theories with respectto diversification is therefore the following:

Hypothesis 4a: The firm’s diversification level isassociated with the choice of acquisitions overalliances, and alliances over divestitures.

On the other hand, some researchers haveexpressed the view that much of the corporaterestructuring activity that took place duringthe 1980s and 1990s was aimed at reversingthe diversification undertaken in earlier decades(Bhide, 1990; Shleifer and Vishny, 1991; Bergerand Ofek, 1996). If this effect predominated duringthe 1990s, then diversified firms would be morelikely to engage in divestitures or other forms ofdisintegration than they would be to engage infurther acquisitions.

Hypothesis 4b: The firm’s diversification levelis associated with the choice of divestitures overalliances, and alliances over acquisitions.

Attributes of the relationship between the focalfirm and the target or partner firm

Industry activity of the focal firm andpartner/target firm

Two theories yield a coinciding prediction aboutthe effect on governance choice of relatednessbetween the focal firm and the target or part-ner firm. A combination of resource-based andtransaction-cost arguments suggests that greaterrelatedness implies a lower cost of integration(Coase, 1937) because of economies of scalewithin the organization. A related version of theargument is that direct competition between thefocal and target/partner firm enhances the need forprotective (i.e., integrative) governance structuresthat will induce knowledge sharing among the part-ners (Oxley and Sampson, 2004).

Balakrishnan and Koza (1993) propose an asym-metric information theory of joint ventures thathas similar implications. In their theory, joint ven-tures are superior to acquisitions when the costs tothe acquirer of valuing the target’s assets are highdue to information asymmetries between the par-ties. This can occur when one party has the powerto appropriate rents if the other reveals privateinformation. A joint venture can mitigate the risks

Copyright 2005 John Wiley & Sons, Ltd. Strat. Mgmt. J., 26: 1183–1208 (2005)

1188 B. Villalonga and A. M. McGahan

and costs of transacting by aligning the incentivesof the two parties.

A related view has been articulated with respectto divestitures: spin-offs and other forms of divesti-ture create value because they reduce informationasymmetries between the firm and the market. Ifspecialized firms are better able to convey infor-mation about their operating efficiency and futureprospects when they are stand-alone entities thanwhen they are divisions of a larger firm, conglom-erates and vertically integrated firms may be ableto create value through spin-offs and divestitures.In support of this view, Krishnaswami and Sub-ramaniam (1999) find that firms that engage inspin-offs have higher levels of information asym-metry than a matched sample of firms, and that theasymmetry decreases significantly after the spin-off. Gilson et al. (2001) show that conglomeratestock break-ups through spin-offs, equity carve-outs, and tracking stock offerings generate a sig-nificant increase in coverage by specialized ana-lysts and a 30–50 percent improvement in ana-lyst forecast accuracy for parent and subsidiaryfirms.

Research in both streams suggests proxying thelevel of information asymmetry by assessing dis-similarities in the parties’ SIC codes. Their predic-tions yield a general asymmetric information-basedhypothesis of governance choice that is consis-tent with the hypothesis of the resource-based andtransaction-costs arguments:

Hypothesis 5: The relatedness between the focalfirm and the target (or partner) firm is associ-ated with the choice of acquisitions overalliances, and alliances over divestitures.

Size balance

Hennart’s (1988) ‘digestibility’ theory argues thatjoint ventures may create value when neither ofthe partnering firms can ‘digest’ the other due tothe diseconomies of scale or scope that wouldarise if an acquisition were to occur. Hennartand Reddy (1997) find that, in their sample, jointventures are relatively more likely than acquisi-tions when the partners are in the same industry.They interpret this result as consistent with Hen-nart’s (1988) digestibility hypothesis but inconsis-tent with Balakrishnan and Koza’s (1993) infor-mation asymmetries hypothesis (reformulated inthis paper as Hypothesis 5). Their interpretation

has been challenged by Reuer and Koza (2000a),who argue that the two theories are complemen-tary rather than competing (see also Hennart andReddy, 2000; Reuer and Koza, 2000b). Hennartand Reddy (2000) offer one possible reconciliationof this debate by acknowledging that proximity inSIC codes is a better proxy for information asym-metries than it is for the digestibility of the target’sassets to the acquirer. As an alternative measure ofdigestibility, we propose the size balance betweenthe two firms, which we define as the ratio of thesales of the smaller firm to the sales of the largerfirm. This measure also addresses the concern thatone solution to digestibility problems is to havethe indigestible partner fully acquire the digestibleone (Hennart and Reddy, 2000; Reuer and Koza,2000a): The more balanced in size partners are,the more difficult it becomes for any of them tobe digested by the other. Using this proxy, wereformulate Hennart’s digestibility hypothesis asfollows:

Hypothesis 6: The size balance between thefocal firm and the target (or partner) firm isassociated with the choice of divestitures overalliances, and alliances over acquisitions.

Prior alliances

Several theories suggest that prior relationshipsbetween the focal firm and the target or part-ner are important to governance choices. Socialembeddedness theory suggests, and empirical evi-dence has confirmed, that two firms are morelikely to engage in an alliance when they havea history of prior alliances between them (Pow-ell, 1990; Gulati, 1998; Podolny and Page, 1998).The embeddedness of firms in social networksenhances trust, which can be promoted by priorties. Real options theory suggests that firms witha history of prior alliances or minority acquisi-tions are more likely to engage subsequently inalliances because prior alliances create valuableoptions (Kogut, 1991; Folta and Miller, 2002).Chi (2000) further argues that alliances also conferupon firms a valuable option to engage in a sub-sequent divestiture. In addition, the literature oncorporate refocusing shows that firms often divestor spin off formerly acquired divisions, whichsuggests that dyadic ties of an acquisitive naturemay also affect future governance choices (Porter,1987; Ravenscraft and Scherer, 1987; Bhide, 1990;

Copyright 2005 John Wiley & Sons, Ltd. Strat. Mgmt. J., 26: 1183–1208 (2005)

Acquisitions, Alliances, and Divestitures 1189

Kaplan and Weisbach, 1992; Berger and Ofek,1996, 1999).

All of these theories predict that firms are morelikely to engage in deals of any type (acquisi-tions, alliances, and divestitures) when they have ahistory of dyadic ties between them. Social embed-dedness theory yields an even more specific pre-diction: prior alliances are more likely to resultin subsequent alliances than they are to result ineither acquisitions or divestitures because the trustcreated by prior alliances enables firms to reduceappropriability hazards (Gulati, 1995):

Hypothesis 7: The number of prior alliancesbetween the firm and the target (or partner)firm is positively associated with the choice ofalliances over both acquisitions and divestitures.

Real options theory predicts that prior allianceswill give rise to acquisitions or divestitures onlywhen the value of the option makes it worthwhileto exercise it. Hence, if Hypothesis 7 is supported,the evidence will be consistent with both theories.If it is not, the evidence will still be consistent withreal options theory but not with social embedded-ness theory.

Attributes of the transaction and of the firm

Relatedness in SIC codes between the firm and thetransaction

Resource-based and transaction-cost argumentssuggest that firms are more likely to chooseintegrative governance forms when the activitiesthat are subject to the transaction are similar to thefirm’s established activities (Coase, 1937; Penrose,1959). The asymmetric information theory of firmboundaries contraction extends the prediction todivestitures:2

Hypothesis 8: The relatedness between the firmand the activity that is subject to the transactionis associated with the choice of acquisitions overalliances, and alliances over divestitures.

2 As stated in Hypothesis 5, the asymmetric information theoryof joint ventures makes the same prediction about the similarityin activities between the partner firms. Unlike other governanceforms, the activities of the joint venture need not be the sameas those of the partner firm. Therefore, we use the asymmetricinformation theory of boundary expansion to justify Hypothesis5 but not Hypothesis 8.

Governance specialization

Implicit in Hypotheses 3a–c is the assumptionthat there are negative or no experience spilloversacross governance forms. For instance, Hypothe-sis 3c predicts that a firm with a long history ofalliances will be more likely to choose an allianceover other governance forms than a firm that hasno alliance experience but is otherwise identicalto the former. It also predicts that a firm willbe more likely to choose an alliance the morealliances it has engaged in before. But if thelessons learned by the firm at managing alliancescan also be applied to acquisitions, the firm may beequally likely to engage in acquisitions based onits experience. Zollo and Reuer (2001) provide evi-dence of spillovers from alliances to acquisitions.One question that remains open is whether thesespillovers are symmetric across governance forms.For instance, it may be that acquisitions providefirms with valuable learning that can inform theevaluation and implementation of future alliances,but not vice versa.

To address this question we introduce the con-cept of governance specialization, which measuresthe degree to which a firm has repeatedly engagedin deals of the current type. As a result, gover-nance specialization captures whether a firm showsevidence of pursuing a program of acquisitions,alliances, or divestitures.

If experience spillovers are symmetric acrossgovernance forms, the following will hold:

Hypothesis 9a: The firm’s governance special-ization is insignificantly associated with thechoice of governance form.

If, on the other hand, governance form experiencespillovers are asymmetric, one of the followinghypotheses will be supported:

Hypothesis 9b: The firm’s governance special-ization is associated with the choice of acquisi-tions over alliances, and alliances over divesti-tures.

Hypothesis 9c: The firm’s governance special-ization is associated with the choice of divesti-tures over alliances, and alliances over acquisi-tions.

Copyright 2005 John Wiley & Sons, Ltd. Strat. Mgmt. J., 26: 1183–1208 (2005)

1190 B. Villalonga and A. M. McGahan

Hypothesis 9b will be supported if spe-cialization is more important for boundary-expanding transactions such as acquisitions thanfor boundary-contracting transactions such asdivestitures. Conversely, Hypothesis 9c will besupported if specialization is more important forboundary-contracting transactions. Hypothesis 9awill be supported if governance specialization isnot more important to deals of any particulartype, or if specialization is more important toalliances.

Recency of experience

A related question to the symmetry and sign ofexperience spillovers is the relative importanceof the experience effects hypothesized in 3a–c.Regardless of a firm’s experience with a gover-nance form, the recency of a firm’s experiencewith deals of the current type may reflect rele-vant learning. For instance, it may be that a firmcontemplating a transaction may lean toward analliance because of learning from a recent alliance,regardless of whether it is pursing a program ofalliances. To address this question we develop thenotion of recency of same-form governance experi-ence—the proximity in time between the deal thatis the subject of the governance choice and the lastdeal of the same form undertaken by the firm. Thismeasure differs from governance specialization inthat it captures only the amount of time since thelast deal of the same type. For example, for twofirms, each with the same high degree of special-ization in divestitures, the ‘deal recency’ variablesimply captures the elapsed time since the mostrecent divestiture.

The following hypotheses test for these possibil-ities. Hypotheses 10a and 10b will be supported iflearning effects are more important in acquisitionsand alliances, respectively.

Hypothesis 10a: The recency of the firm’s same-form governance experience is associated withthe choice of acquisitions over alliances, andalliances over divestitures.

Hypothesis 10b: The recency of the firm’s same-form governance experience is associated withthe choice of divestitures over alliances, andalliances over acquisitions.

Target/partner attributes

Target/partner firm’s intangible resources

The resource-based view offers boundary choicepredictions based not only on the focal firm’sresources but also on those of the target. The focalfirm diversifies and expands not only in search ofopportunities to exploit its existing resources andcapabilities (Penrose, 1959), but also in search ofnew resources that may complement its existingbase (Chatterjee, 1990). Hence:

Hypothesis 11a: The target (or partner) firm’stechnological resources are associated with thechoice of acquisitions over alliances, andalliances over divestitures.

Hypothesis 11b: The target (or partner) firm’smarketing resources are associated with thechoice of acquisitions over alliances, andalliances over divestitures.

Transaction attributes

Market transaction costs and internalorganization costs

Transaction cost theory stipulates that a firmchooses to acquire assets when the ongoingcosts of conducting business in the market arehigher than the costs of organizing activitieswithin the firm (Coase, 1937; Williamson, 1975,1985). Empirical tests typically use one of twoproxies for high market costs: uncertainty in therelevant market, or the degree of specificity of theasset or activity being exchanged. As Shelanskiand Klein (1995) argue, uncertainty leads tohierarchical governance only in the presence ofasset specificity. Therefore the interaction betweenuncertainty and asset specificity may be a betterproxy for the costs of transacting through themarket. One possible measure of uncertainty thatis generic across industries is the variability inprofits of the target or partner/firm. Measuringasset specificity in a multi-industry setting isdifficult, however, because what makes assetsspecific to a given activity typically differs acrossactivities. We propose the use of the percentageof employees in the focal firm’s industry that areengineers as a measure of human asset specificity.Nevertheless, we caution that this variable mayalso be indicative of the firm’s knowledge

Copyright 2005 John Wiley & Sons, Ltd. Strat. Mgmt. J., 26: 1183–1208 (2005)

Acquisitions, Alliances, and Divestitures 1191

capital and hence be a proxy for combinedresource-based/transaction-costs arguments ratherthan for transaction cost theory alone.

Hypothesis 12a: The interaction between uncer-tainty and asset specificity is associated withthe choice of acquisitions over alliances, andalliances over divestitures.

Likewise, we use the number of managers asa percentage of employees in the target/partnerfirm’s industry as a proxy for the internal organi-zation costs associated to integrating the target intothe focal firm. Transaction cost economics recog-nizes that the costs of market exchange are onlyrelevant determinants of the optimal governancechoice after netting out the costs of internal orga-nization. Thus, even if transaction costs are high,a firm may choose to conduct an alliance overan acquisition if the cost of integrating the tar-get firm’s activities is even higher than the cost ofmarket exchange (Kogut and Singh, 1988; Masten,Meehan, and Snyder, 1991; Hennart and Reddy,1997).

Hypothesis 12b: The internal organization costsof integrating the target firm into the focal firmare associated with the choice of divestituresover alliances, and alliances over acquisitions.

DATA AND SAMPLE

The sample represents 9276 acquisitions, alliances,and divestitures announced and completed by 86members of the Fortune 100 between 1990 and2000.3 Each of the 86 firms engaged in a variety ofdeals over the period, which allows us to evaluatethe importance of transaction and target/partnerattributes while controlling for firm attributes. Weconstruct the dataset through the process describedbelow.

First, we select the 86 firms in the 1990 Fortune100 that: (a) were publicly traded on one or moreU.S. stock exchanges; (b) engaged in at least onealliance during the period; and (c) engaged in atleast one acquisition or divestiture.

3 The dataset was drawn from the same sources as in McGahanand Villalonga (2003). The main difference is that the dataset inthe prior paper contained 7714 deals, whereas this paper reportson 9276 deals. The reason is that the prior dataset excluded dealsfor which the stock market reaction could not be assessed.

Second, we draw information from the SDCJoint Ventures and Alliances database on alliancesannounced and completed between January 1,1990, and December 31, 1999 by the 86 firms inour database, including alliances that involved anyof their subsidiaries.

Third, we draw information from the SDC’sMergers and Acquisitions database on acquisi-tions announced and completed between January1, 1990, and December 31, 1999, by the 86 firmsand by any of their subsidiaries. This category,‘acquisitions,’ includes deals classified by SDCas mergers, acquisitions, acquisitions of majorityinterest, acquisitions of partial interest, acquisi-tions of remaining interest, acquisitions of assets,or acquisitions of certain assets.

Fourth, we draw information from the SDC’sMergers and Acquisitions database on the divesti-tures announced and completed during the periodby the 86 firms and by any of their sub-sidiaries. The ‘divestitures’ category includesdeals classified by SDC as divestitures, spin-offsand carve-outs.4 It also includes seven ‘mega-divestitures’ in which the entire sample firmwas sold: Daimler–Chrysler, Compaq–DigitalEquipment, Exxon–Mobil, Boeing–McDonnellDouglas, Kimberly Clark–Scott Paper, Jeffer-son Smurfit–Stone Container, Kohlberg KravisRoberts–Borden.

Fifth, we eliminate duplicate observations on thesame deal arising from repeated announcements ofa single deal, from deals that are associated withmore than one governance form (alliance, acquisi-tion and/or divestiture), and from simple reportingerrors in SDC. Thus, any given deal will appearonly once in our dataset unless the partner/targetfirm is also one of our sample firms, in which casethe deal will appear twice and the focal and target

4 A divestiture is tracked in SDC when there is a loss of majoritycontrol, the parent company is losing a majority interest in thetarget, or the target company is disposing of assets. A spin-off is the tax-free distribution of shares by a company of aunit, subsidiary, division, or another company’s stock, or anyportion thereof, to its shareholders. SDC tracks spin-offs of anypercentage. In contrast, in a carve-out, the new company’s sharesare distributed or sold to the public via an IPO. Carve-outs aretracked in SDC only if they represent 100 percent of the unit,subsidiary division or other company. Note that we exclude anyobservation that was not a divestiture, spin-off, or carve-out.In particular, we do not include changes in a firm’s ownershipstructure created by a firm’s Employee Stock Ownership Plan, ormore generally by the acquisition of partial or remaining interestin one of the sample firms (or in a subsidiary) that does notrepresent a divestiture.

Copyright 2005 John Wiley & Sons, Ltd. Strat. Mgmt. J., 26: 1183–1208 (2005)

1192 B. Villalonga and A. M. McGahan

firm will switch roles. For instance, three of the‘mega-divestitures’ mentioned above also appearin our sample as acquisitions: Exxon–Mobil (amega-divestiture for Mobil but an acquisition forExxon), Boeing–McDonnell Douglas, and Kim-berly Clark–Scott Paper.

Sixth, because SDC alliance dates are unreliable(Anand and Khanna, 2000; McGahan and Villa-longa, 2003), we verify the alliance dates reportedby SDC using the Lexis–Nexis and the Dow JonesNews Retrieval Service (DJNRS). We could notfind news information on 8 percent of the alliancesand relied on the SDC data for these observa-tions. For 62 percent of all alliances, the SDC dateswere the same as those reported by the news ser-vices. When discrepancies arose, we used the datereported by the news service rather than by SDC.In 21 percent of cases, the news date was ear-lier than the date reported by SDC. In 10 percentof cases, the news date was later than the datereported by SDC.

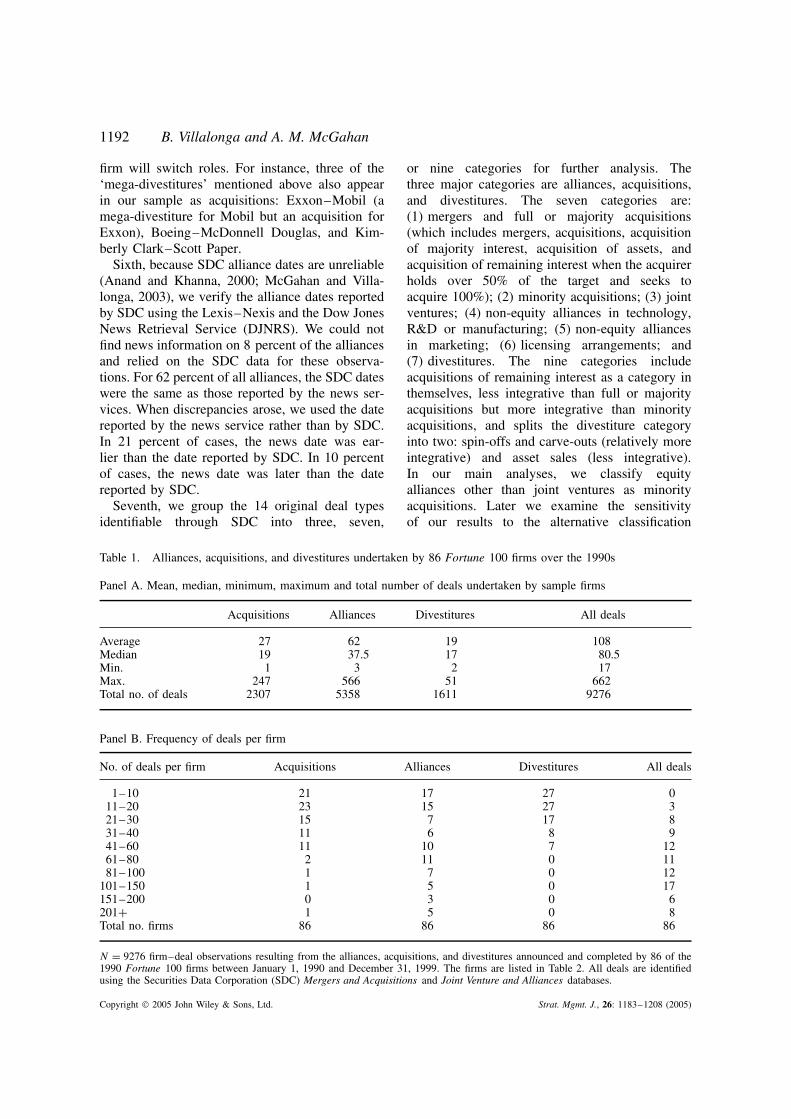

Seventh, we group the 14 original deal typesidentifiable through SDC into three, seven,

or nine categories for further analysis. Thethree major categories are alliances, acquisitions,and divestitures. The seven categories are:(1) mergers and full or majority acquisitions(which includes mergers, acquisitions, acquisitionof majority interest, acquisition of assets, andacquisition of remaining interest when the acquirerholds over 50% of the target and seeks toacquire 100%); (2) minority acquisitions; (3) jointventures; (4) non-equity alliances in technology,R&D or manufacturing; (5) non-equity alliancesin marketing; (6) licensing arrangements; and(7) divestitures. The nine categories includeacquisitions of remaining interest as a category inthemselves, less integrative than full or majorityacquisitions but more integrative than minorityacquisitions, and splits the divestiture categoryinto two: spin-offs and carve-outs (relatively moreintegrative) and asset sales (less integrative).In our main analyses, we classify equityalliances other than joint ventures as minorityacquisitions. Later we examine the sensitivityof our results to the alternative classification

Table 1. Alliances, acquisitions, and divestitures undertaken by 86 Fortune 100 firms over the 1990s

Panel A. Mean, median, minimum, maximum and total number of deals undertaken by sample firms

Acquisitions Alliances Divestitures All deals

Average 27 62 19 108Median 19 37.5 17 80.5Min. 1 3 2 17Max. 247 566 51 662Total no. of deals 2307 5358 1611 9276

Panel B. Frequency of deals per firm

No. of deals per firm Acquisitions Alliances Divestitures All deals

1–10 21 17 27 011–20 23 15 27 321–30 15 7 17 831–40 11 6 8 941–60 11 10 7 1261–80 2 11 0 1181–100 1 7 0 12

101–150 1 5 0 17151–200 0 3 0 6201+ 1 5 0 8Total no. firms 86 86 86 86

N = 9276 firm–deal observations resulting from the alliances, acquisitions, and divestitures announced and completed by 86 of the1990 Fortune 100 firms between January 1, 1990 and December 31, 1999. The firms are listed in Table 2. All deals are identifiedusing the Securities Data Corporation (SDC) Mergers and Acquisitions and Joint Venture and Alliances databases.

Copyright 2005 John Wiley & Sons, Ltd. Strat. Mgmt. J., 26: 1183–1208 (2005)

Acquisitions, Alliances, and Divestitures 1193

Table 2. Total number of deals for each firm in the sample

Firm name Acquisitions Alliances Divestitures All deals

Abbott Laboratories 13 64 4 81Alcoa 23 24 6 53Allied-Signal 47 63 27 137Amerada Hess 9 11 12 32American Home Products 24 84 16 124Amoco 3 15 10 28Anheuser-Busch 7 25 8 40Apple Computer 4 152 2 158Archer Daniels Midland 39 9 3 51Ashland Oil 38 16 20 74Atlantic Richfield 21 35 41 97Baxter International 26 62 13 101Boeing 8 54 7 69Borden 9 3 23 35Bristol-Myers-Squibb 19 82 20 121Campbell Soup 16 9 24 49Caterpillar 13 24 3 40Chevron 12 61 51 124Chrysler 10 48 22 80Coastal 27 30 5 62Coca-Cola 34 50 8 92Colgate-Palmolive 18 9 7 34Conagra 36 18 19 73Cooper Industries 46 3 11 60Deere 14 9 5 28Digital Equipment 9 193 18 220Dow Chemical 42 104 37 183Du Pont de Nemours 52 181 49 282Eastman Kodak 31 126 41 198Emerson Electric 37 10 10 57Exxon 2 72 10 84Ford Motor 88 126 29 243General Dynamics 6 17 10 33General Electric 247 259 50 556General Mills 8 9 6 23General Motors 106 268 45 419Georgia-Pacific 13 6 12 31Goodyear Tire & Rubber 12 12 10 34H.J. Heinz 44 14 15 73Hewlett-Packard 30 343 18 391Honeywell 3 40 7 50IBM 65 566 31 662International Paper 42 9 22 73Johnson & Johnson 37 85 21 143Kimberly-Clark 19 11 14 44Litton Industries 25 14 19 58Lockheed 23 106 14 143LTV 3 10 4 17McDonnell Douglas 1 38 10 49Merck 7 67 7 813M 19 49 19 87Mobil 22 85 48 155Monsanto 27 64 27 118Motorola 44 271 24 339NCR 4 11 3 18Northrop 11 14 4 29

(continued overleaf )

Copyright 2005 John Wiley & Sons, Ltd. Strat. Mgmt. J., 26: 1183–1208 (2005)

1194 B. Villalonga and A. M. McGahan

Table 2. (Continued )

Firm name Acquisitions Alliances Divestitures All deals

Occidental Petroleum 17 27 32 76Pepsico 44 66 22 132Pfizer 21 64 16 101Philip Morris 48 37 35 120Phillips Petroleum 12 48 18 78PPG Industries 31 21 13 65Procter & Gamble 37 52 40 129Quaker Oats 7 4 17 28Ralston Purina 12 10 5 27Raytheon 27 44 25 96Reynolds Metals 17 12 20 49RJR Nabisco 21 5 14 40Rockwell International 21 71 16 108Sara Lee 63 12 23 98Scott Paper 3 5 13 21Stone Container 8 3 7 18Tenneco 37 41 21 99Texaco 22 88 31 141Texas Instruments 17 141 20 178Textron 49 17 17 83TRW 16 50 24 90Union Carbide 14 49 22 85Unisys 14 88 6 108United Technologies 48 95 15 158Unocal 8 25 24 57USX–Marathon 14 32 25 71W.R. Grace 40 31 36 107Weyerhaeuser 19 6 16 41Whirlpool 6 13 4 23

of equity alliances as (or together with) jointventures.

Finally, we extract information on firm attributesand on target/partner firm attributes from the Com-pustat Research and Active files, the CompustatBusiness-Segment Reports, CRSP, the Occupa-tional Employment Survey of the Bureau of LaborStatistics, and Compact Disclosure. The sample weuse for our probit analyses encompasses the 4058deals for which we have information on partnersand targets.

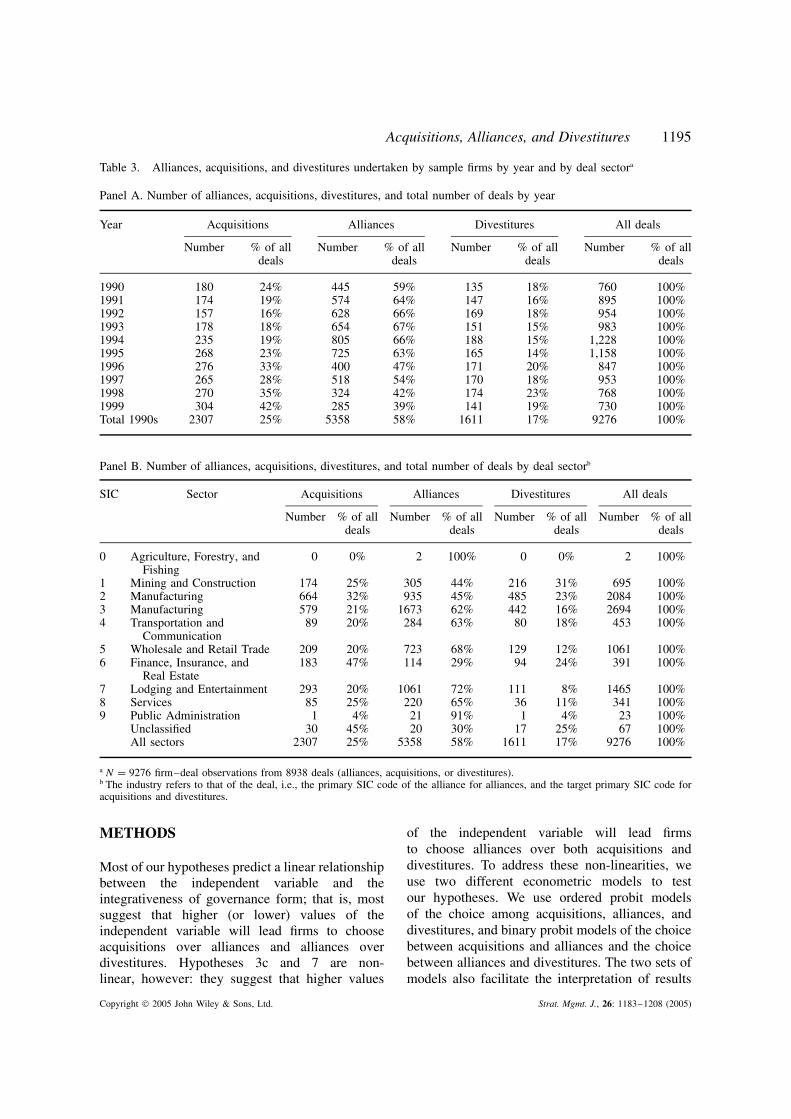

Tables 1–3 describe the screened data set. PanelA of Table 1 indicates that 5358 of the deals inthe sample (or 56%) are alliances, 2307 (26%) areacquisitions, and 1611 (18%) are divestitures. Thesample firms engaged in an average of 108 deals,of which 27 were acquisitions, 62 were alliances,and 19 were divestitures. Panel B shows that thedistribution of the number of firms doing deals ofeach type is skewed.

Table 2 lists the number of alliances, acqui-sitions, and divestitures for each firm over the

sample period. As the table shows, some firmsused mixed governance strategies, while othersspecialized in one particular governance form.IBM pursued more deals of all types than anyother firm (662). LTV Steel pursued fewer dealsthan any other firm (17). General Electric didthe most acquisitions (247). IBM did the mostalliances (566). Chevron did the most divesti-tures (51), followed closely by General Electric(50).

Table 3 shows deals by year and economic sec-tor. Panel A shows that the number of acquisi-tions grew over the sample period, while the num-ber of alliances and divestitures peaked in 1994.Panel B shows the distribution of deals by indus-try (where the industry is that of the deal, i.e.,the primary SIC code of the alliance for alliances,and the primary SIC code of the target for acqui-sitions and divestitures). The most deals of alltypes were in manufacturing. The fewest dealsoccurred in the agriculture, forestry and fishingsector.

Copyright 2005 John Wiley & Sons, Ltd. Strat. Mgmt. J., 26: 1183–1208 (2005)

Acquisitions, Alliances, and Divestitures 1195

Table 3. Alliances, acquisitions, and divestitures undertaken by sample firms by year and by deal sectora

Panel A. Number of alliances, acquisitions, divestitures, and total number of deals by year

Year Acquisitions Alliances Divestitures All deals

Number % of alldeals

Number % of alldeals

Number % of alldeals

Number % of alldeals

1990 180 24% 445 59% 135 18% 760 100%1991 174 19% 574 64% 147 16% 895 100%1992 157 16% 628 66% 169 18% 954 100%1993 178 18% 654 67% 151 15% 983 100%1994 235 19% 805 66% 188 15% 1,228 100%1995 268 23% 725 63% 165 14% 1,158 100%1996 276 33% 400 47% 171 20% 847 100%1997 265 28% 518 54% 170 18% 953 100%1998 270 35% 324 42% 174 23% 768 100%1999 304 42% 285 39% 141 19% 730 100%Total 1990s 2307 25% 5358 58% 1611 17% 9276 100%

Panel B. Number of alliances, acquisitions, divestitures, and total number of deals by deal sectorb

SIC Sector Acquisitions Alliances Divestitures All deals

Number % of alldeals

Number % of alldeals

Number % of alldeals

Number % of alldeals

0 Agriculture, Forestry, andFishing

0 0% 2 100% 0 0% 2 100%

1 Mining and Construction 174 25% 305 44% 216 31% 695 100%2 Manufacturing 664 32% 935 45% 485 23% 2084 100%3 Manufacturing 579 21% 1673 62% 442 16% 2694 100%4 Transportation and

Communication89 20% 284 63% 80 18% 453 100%

5 Wholesale and Retail Trade 209 20% 723 68% 129 12% 1061 100%6 Finance, Insurance, and

Real Estate183 47% 114 29% 94 24% 391 100%

7 Lodging and Entertainment 293 20% 1061 72% 111 8% 1465 100%8 Services 85 25% 220 65% 36 11% 341 100%9 Public Administration 1 4% 21 91% 1 4% 23 100%

Unclassified 30 45% 20 30% 17 25% 67 100%All sectors 2307 25% 5358 58% 1611 17% 9276 100%

a N = 9276 firm–deal observations from 8938 deals (alliances, acquisitions, or divestitures).b The industry refers to that of the deal, i.e., the primary SIC code of the alliance for alliances, and the target primary SIC code foracquisitions and divestitures.

METHODS

Most of our hypotheses predict a linear relationshipbetween the independent variable and theintegrativeness of governance form; that is, mostsuggest that higher (or lower) values of theindependent variable will lead firms to chooseacquisitions over alliances and alliances overdivestitures. Hypotheses 3c and 7 are non-linear, however: they suggest that higher values

of the independent variable will lead firmsto choose alliances over both acquisitions anddivestitures. To address these non-linearities, weuse two different econometric models to testour hypotheses. We use ordered probit modelsof the choice among acquisitions, alliances, anddivestitures, and binary probit models of the choicebetween acquisitions and alliances and the choicebetween alliances and divestitures. The two sets ofmodels also facilitate the interpretation of results

Copyright 2005 John Wiley & Sons, Ltd. Strat. Mgmt. J., 26: 1183–1208 (2005)

1196 B. Villalonga and A. M. McGahan

as conditional on different decisions by a firm: tochange boundaries, to expand boundaries, or tocontract boundaries, respectively. The purpose isto evaluate candidate explanations for the choiceamong acquisitions, alliances, and divestitures.

The dependent variable in the ordered probitmodels is an indicator variable called ‘governanceform’ that takes on a series of ordinal values(see McKelvey and Zavoina, 1975, and Oxley,1997, for statistical details on the estimation tech-nique). Higher values indicate higher degrees ofintegration along the market–hierarchies contin-uum. We use alternative measures of this vari-able to test formally for the appropriate level ofaggregation or disaggregation of the governancecontinuum into discrete structural alternatives. Inthe three-category ordered probit model, the gov-ernance form variables is set to two if the transac-tion involves a merger or acquisition (majority orminority), one if the transaction involves any kindof non-equity alliance or joint venture, and zero ifthe transaction involves a divestiture of any type.In the remaining ordered probit models, the gover-nance form variable takes one of seven values foreach of the categories listed earlier, ranging fromsix for mergers and full or majority acquisitions,to zero for divestitures.

The ordering is similar in the binary probit mod-els: in the model of boundary expansion, the gover-nance form variable equals one for acquisition andzero for alliances. In the probit model of bound-ary contraction, the dependent variable equals onefor alliances and zero for divestitures. Thus, in allmodels, a positive coefficient on any of the inde-pendent variables can be interpreted as a higherprobability that the firm will choose to organize thetransaction through a more integrative governanceform.

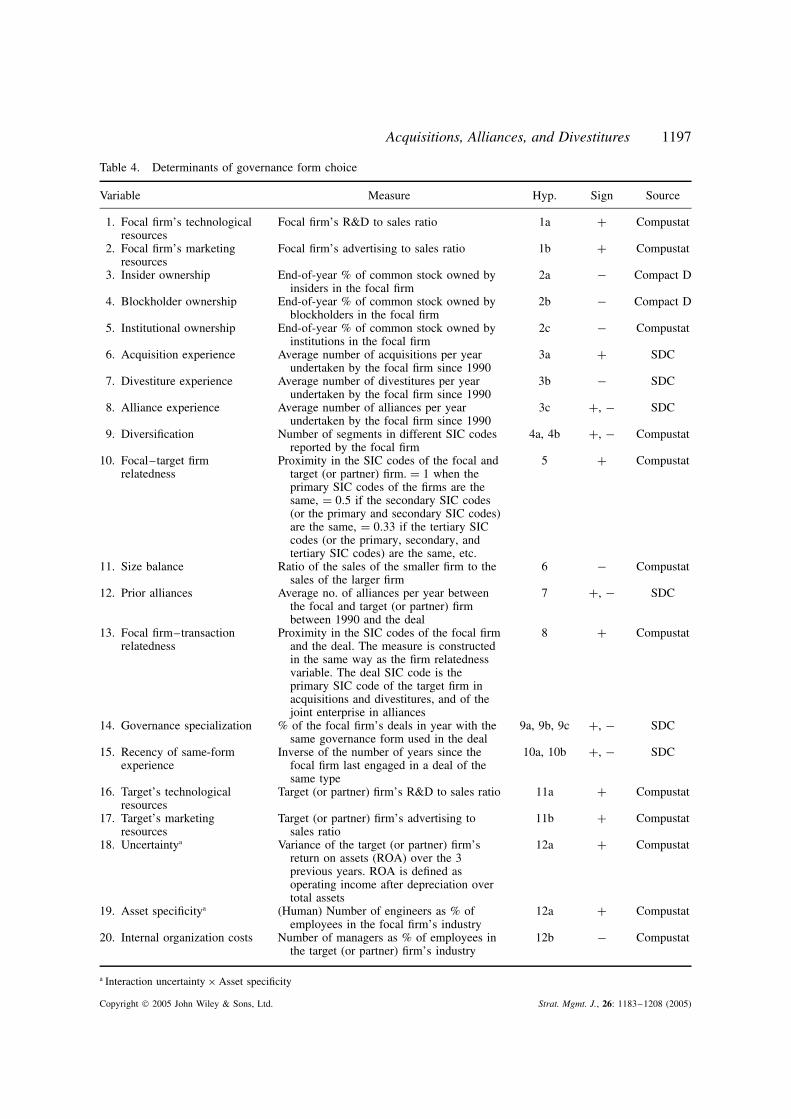

Table 4 contains a description of each indepen-dent variable together with the hypothesis it servesto test, its predicted sign, and the data source. Thecorrelation matrix is reported in Table 5.

RESULTS AND DISCUSSION

Choices among the full continuum ofboundary-changing governance forms

Table 6 presents the results of our ordered probitanalyses linking attributes to governance choices.These results should be interpreted as conditionalon a firm’s decision to change its boundaries

through expansion or contraction. The first col-umn shows the results when the dependent variable(which represents governance form) takes threepossible values (for acquisitions, alliances, anddivestitures). The second column shows results forthe seven-value construction of the dependent vari-able.

In both models, the focal firm’s technologi-cal resources are significantly associated with thechoice of acquisitions over alliances and alliancesover divestitures, as predicted by Hypothesis 1a.This result provides support for the resource-based, transaction-cost, and internalization argu-ments, and is consistent with prior evidence fromstudies of foreign market entry mode (e.g., Kogutand Singh, 1988; Morck and Yeung, 1992). LikeMorck and Yeung (1992), however, we find sup-port for these arguments in the R&D intensity (ortechnological resources) variable, but not in theadvertising intensity (or marketing resources) vari-able, which is statistically non-significant in bothof our probit models. Hence, Hypothesis 1b is notsupported in our analysis. The effects of the tar-get firm’s technological and marketing resources(Hypotheses 11a and 11b) are not statistically sig-nificant.

The ownership structure variables show onlymixed support for agency theory. On the one hand,institutional ownership is significantly associatedwith the choice of divestitures over alliances andalliances over acquisitions in both probit regres-sions, as predicted by Hypothesis 2c. Blockholderownership has a negative sign, as predicted byHypothesis 2b, but is not statistically significant.On the other hand, insider ownership has a positivesign, and is statistically significant in the three-governance-form model, which runs contrary tothe prediction of Hypothesis 2a. Our results aboutthe effect of ownership structure on governancechoice suggest that blockholders, particularly insti-tutional blockholders, do exercise a monitoringrole in preventing executives from empire build-ing through excessive acquisitions. Yet the con-centration of stock in the hands of executives hasthe opposite effect of leading to further expan-sion of the firm’s boundaries through acquisitions,and/or less boundary contraction through divesti-tures. One possible explanation for this finding isthat equity ownership by insiders beyond certainlevels may have an entrenchment effect rather thanan incentive-alignment effect (Morck, Shleifer, andVishny, 1988).

Copyright 2005 John Wiley & Sons, Ltd. Strat. Mgmt. J., 26: 1183–1208 (2005)

Acquisitions, Alliances, and Divestitures 1197

Table 4. Determinants of governance form choice

Variable Measure Hyp. Sign Source

1. Focal firm’s technologicalresources

Focal firm’s R&D to sales ratio 1a + Compustat

2. Focal firm’s marketingresources

Focal firm’s advertising to sales ratio 1b + Compustat

3. Insider ownership End-of-year % of common stock owned byinsiders in the focal firm

2a − Compact D

4. Blockholder ownership End-of-year % of common stock owned byblockholders in the focal firm

2b − Compact D

5. Institutional ownership End-of-year % of common stock owned byinstitutions in the focal firm

2c − Compustat

6. Acquisition experience Average number of acquisitions per yearundertaken by the focal firm since 1990

3a + SDC

7. Divestiture experience Average number of divestitures per yearundertaken by the focal firm since 1990

3b − SDC

8. Alliance experience Average number of alliances per yearundertaken by the focal firm since 1990

3c +, − SDC

9. Diversification Number of segments in different SIC codesreported by the focal firm

4a, 4b +, − Compustat

10. Focal–target firmrelatedness

Proximity in the SIC codes of the focal andtarget (or partner) firm. = 1 when theprimary SIC codes of the firms are thesame, = 0.5 if the secondary SIC codes(or the primary and secondary SIC codes)are the same, = 0.33 if the tertiary SICcodes (or the primary, secondary, andtertiary SIC codes) are the same, etc.

5 + Compustat

11. Size balance Ratio of the sales of the smaller firm to thesales of the larger firm

6 − Compustat

12. Prior alliances Average no. of alliances per year betweenthe focal and target (or partner) firmbetween 1990 and the deal

7 +, − SDC

13. Focal firm–transactionrelatedness

Proximity in the SIC codes of the focal firmand the deal. The measure is constructedin the same way as the firm relatednessvariable. The deal SIC code is theprimary SIC code of the target firm inacquisitions and divestitures, and of thejoint enterprise in alliances

8 + Compustat

14. Governance specialization % of the focal firm’s deals in year with thesame governance form used in the deal

9a, 9b, 9c +, − SDC

15. Recency of same-formexperience

Inverse of the number of years since thefocal firm last engaged in a deal of thesame type

10a, 10b +, − SDC

16. Target’s technologicalresources

Target (or partner) firm’s R&D to sales ratio 11a + Compustat

17. Target’s marketingresources

Target (or partner) firm’s advertising tosales ratio

11b + Compustat

18. Uncertaintya Variance of the target (or partner) firm’sreturn on assets (ROA) over the 3previous years. ROA is defined asoperating income after depreciation overtotal assets

12a + Compustat

19. Asset specificitya (Human) Number of engineers as % ofemployees in the focal firm’s industry

12a + Compustat

20. Internal organization costs Number of managers as % of employees inthe target (or partner) firm’s industry

12b − Compustat

a Interaction uncertainty × Asset specificity

Copyright 2005 John Wiley & Sons, Ltd. Strat. Mgmt. J., 26: 1183–1208 (2005)

1198 B. Villalonga and A. M. McGahan

Tabl

e5.

Cor

rela

tion

mat

rix

12

34

56

78

910

1112

1314

1516

1718

19

1.Fo

cal

firm

’ste

chno

logi

cal

reso

urce

s1.

00

2.Fo

cal

firm

’sm

arke

ting

reso

urce

s0.

341.

003.

Insi

der

owne

rshi

p−0

.06

−0.0

81.

004.

Blo

ckho

lder

owne

rshi

p−0

.17

−0.1

30.

531.

005.

Inst

itutio

nal

owne

rshi

p−0

.23

−0.1

7−0

.08

0.03

1.00

6.A

cqui

sitio

nex

peri

ence

0.29

−0.0

1−0

.15

−0.2

6−0

.17

1.00

7.D

ives

titur

eex

peri

ence

0.01

0.07

−0.0

30.

11−0

.15

−0.1

51.

008.

Alli

ance

expe

rien

ce0.

670.

040.

01−0

.17

−0.2

60.

48−0

.15

1.00

9.D

iver

sific

atio

n0.

03−0

.01

−0.0

3−0

.02

0.02

0.04

0.24

−0.0

71.

0010

.Fo

cal–

targ

etfir

mre

late

dnes

s0.

060.

04−0

.04

−0.0

1−0

.04

0.05

−0.0

20.

02−0

.12

1.00

11.

Size

bala

nce

−0.0

4−0

.04

0.03

0.01

0.01

−0.0

1−0

.04

−0.0

10.

090.

131.

0012

.Pr

ior

allia

nces

0.26

0.04

0.09

0.00

−0.0

70.

270.

000.

010.

070.

130.

201.

0013

.Fo

cal

firm

–tr

ansa

ctio

nre

late

dnes

s−0

.04

−0.0

4−0

.04

0.02

0.07

−0.1

3−0

.13

−0.0

1−0

.04

0.11

0.02

0.04

1.00

14.

Gov

erna

nce

spec

ializ

atio

n−0

.18

−0.1

10.

100.

090.

06−0

.13

−0.1

5−0

.02

−0.0

50.

060.

030.

060.

021.

0015

.R

ecen

cyof

sam

e-fo

rmgo

v.ex

peri

ence

0.16

0.05

0.00

−0.0

4−0

.09

0.18

0.13

0.03

−0.0

10.

020.

000.

09−0

.04

0.14

1.00

16.

Targ

et’s

tech

nolo

gica

lre

sour

ces

0.05

0.00

0.05

0.03

0.00

0.09

0.00

0.01

0.09

0.12

0.48

0.38

0.00

0.02

0.03

1.00

17.

Targ

et’s

mar

ketin

gre

sour

ces

0.01

0.02

−0.0

10.

000.

000.

020.

01−0

.02

0.07

0.09

0.40

0.16

0.01

0.01

0.00

0.57

1.00

18.

Unc

erta

inty

×A

sset

spec

ifici

ty0.

05−0

.03

0.01

0.00

0.02

0.04

−0.0

5−0

.02

0.01

−0.0

2−0

.04

0.06

−0.0

20.

020.

030.

01−0

.02

1.00

19.

Inte

rnal

orga

niza

tion

cost

s0.

08−0

.02

0.02

0.02

0.02

0.07

0.05

−0.0

10.

030.

04−0

.03

0.02

−0.0

10.

000.

020.

06−0

.02

0.07

1.00

Copyright 2005 John Wiley & Sons, Ltd. Strat. Mgmt. J., 26: 1183–1208 (2005)

Acquisitions, Alliances, and Divestitures 1199

Table 6. Ordered probit analysis of governance form choicea

Variable Hyp. 3 governance formvaluesb

7 governance form valuesc

Coeff. t-statistic Coeff. t-statistic

Focal firm’s technological resources 1a 5.E-05 2.67∗∗∗ 4.E-05 2.34∗∗

Focal firm’s marketing resources 1b 6.E-07 0.02 1.E-05 0.40Insider ownership 2a 0.006 2.37∗∗ 0.001 0.28Blockholder ownership 2b −0.003 −1.47 −0.001 −0.74Institutional ownership 2c −0.004 −2.34∗∗ −0.003 −1.97∗∗

Acquisition experience 3a 0.022 7.37∗∗∗ 0.027 9.91∗∗∗

Divestiture experience 3b −0.028 −4.20∗∗∗ −0.029 −4.77∗∗∗

Alliance experience 3c −0.005 −3.29∗∗∗ −0.007 −5.77∗∗∗

Diversification 4 0.093 24.31∗∗∗ 0.081 23.76∗∗∗

Focal firm-target firm relatedness 5 0.334 6.52∗∗∗ 0.230 5.01∗∗∗

Size balance 6 0.458 4.19∗∗∗ 0.276 2.85∗∗∗

Prior alliances 7 −0.161 −8.20∗∗∗ −0.105 −5.94∗∗∗

Focal firm–transaction relatedness 8 0.147 1.99∗∗ 0.198 2.94∗∗∗

Governance specialization 9a,b 0.293 3.30∗∗∗ 0.606 7.43∗∗∗

Recency of same-form experience 10a,b −0.272 −3.37∗∗∗ 0.088 1.21Target’s technological resources 11a 2.E-05 0.48 −1.E-06 −0.03Target’s marketing resources 11b 1.E-04 1.39 1.E-04 1.50Uncertainty × Asset specificity 12a 0.251 2.60∗∗∗ −0.019 −0.22Internal organization costs 12b −0.028 −2.92∗∗∗ −0.021 −2.46∗∗

Cutpoint no. 1 −0.807 −4.83∗∗∗ −0.431 −2.86∗∗∗

Cutpoint no. 2 1.200 7.16∗∗∗ −0.343 −2.28∗∗

Cutpoint no. 3 −0.045 −0.30Cutpoint no. 4 0.808 5.32∗∗∗

Cutpoint no. 5 1.513 9.96∗∗∗

Cutpoint no. 6 1.666 10.96∗∗∗

Log likelihood −3343 −6435No. of observations 4058 4058Prob. >χ 2 0.000 0.000Pseudo R2 0.127 0.071

a The dependent variable is an ordinal variable called ‘governance form’, where higher values indicate higher degrees of integration.Huber/White/Sandwich robust standard errors are in parentheses. ∗∗∗ p < 0.01; ∗∗ p < 0.05; ∗ p < 0.10b Governance form takes one of three values: 2 for mergers and acquisitions, 1 for alliances and joint ventures, 0 for divestitures.c Governance form takes one of seven values: 6 for mergers and full or majority acquisitions; 5 for minority acquisitions; 4 for jointventures; 3 for non-equity alliances in technology, R&D or manufacturing; 2 for non-equity alliances in marketing; 1 for licensingarrangements; and 0 for spin-offs and divestitures.

The focal firm’s acquisition and divestiture expe-rience are significantly associated with the choiceof deals of the same type. These findings providesupport for Hypotheses 3a and 3b about the sig-nificance of experience effects, and are consistentwith organizational learning theory and with priorevidence about acquisition and divestiture capa-bilities (Allen, 1998; Haleblian and Finkelstein,1999; Hayward, 2002). The focal firm’s allianceexperience is negatively and significantly associ-ated with more integrative governance choices.Because Hypothesis 3c posits that alliance expe-rience favors the choice of alliances over bothacquisitions and divestitures, it can only be testedusing our binary probit models; thus we defer

until later the discussion of the alliance experienceresults.

The firm’s diversification level has a positivesign and is highly significant in both regressions.As explained in the development of Hypothesis4a, this result can be explained by the combinedresources–transaction costs view as well as byagency theory and by organizational learning argu-ments about acquisition capabilities. However, theresult is inconsistent with the view that diversifiedfirms are more likely than focused firms to engagein divestitures (and not in any further acquisitions)to reverse their earlier diversification strategy.

All the attributes of the focal firm–partner/targetfirm dyad are statistically significant, as are those

Copyright 2005 John Wiley & Sons, Ltd. Strat. Mgmt. J., 26: 1183–1208 (2005)

1200 B. Villalonga and A. M. McGahan

of the relationship between the focal firm and thetransaction itself. As predicted by Hypothesis 5,the effect of relatedness (measured by proximityin SIC codes) between the two firms is positive.Hypothesis 8, about the relatedness between theactivities of the focal firm and the transaction, isalso supported. These results are consistent withthe combined resources–transaction costs viewthat the cost of integration is lower the greater thesimilarity in activities between the partnering firmsor between the focal firm and the goods or servicesbeing exchanged (Coase, 1972). It is also consis-tent with the theory and findings in Balakrishnanand Koza (1993), Krishnaswami and Subramaniam(1999), and Gilson et al. (2001) about informa-tion asymmetries leading to boundary-contractingchoices. If, as Hennart and Reddy (1997, 2000)argue, the proximity in SIC codes between the part-ners is a proxy for digestibility and a way to testHennart’s (1988) indivisibilities theory against theasymmetric information view, our results can beseen as supportive of the latter and not of the for-mer. To the extent that the size balance betweenthe partnering firms is an alternative proxy fordigestibility, our finding that size balance has apositive effect on the choice of integrative gover-nance is also difficult to reconcile with Hennart’sviews.

The focal firm’s governance specialization isassociated with the choice of acquisitions overalliances, and alliances over divestitures, whichsupports Hypothesis 9b but not Hypotheses 9a or9c. This finding indicates that experience spilloversare asymmetric across governance forms. Inparticular, governance specialization is importantfor moves toward greater integration, but not viceversa. This means that the knowledge acquiredby conducting acquisitions tends to be specializedto future acquisitions, but that the knowledgeacquired on alliances and divestitures is fungibleand applies across both deal types. In other words,the lessons learned by firms in prior alliances maybe applicable to divestitures but not to acquisitions,which is consistent with Zollo and Reuer’s (2001)finding of a negative spillover effect of allianceexperience on acquisition performance for lowexperience levels. Zollo and Reuer also find thatthe spillover effect is a function of the decisionsmade in the post-acquisition phase regardingthe level of integration and the replacementof top management. The importance of post-acquisition integration to the overall success of

acquisitions—i.e., the strategy implementationphase—may thus be the reason why governancespecialization is critical for acquisitions but not somuch for other governance forms.

Our findings also suggest that firms canlearn valuable lessons from acquisitions thatcan be applied to subsequent alliances anddivestitures—perhaps of the same units that wereacquired earlier. The latter is consistent withthe evidence in Porter (1987), Ravenscraft andScherer (1987), and Kaplan and Weisbach (1992)indicating that between one third and one halfof acquisitions are later divested. As Kaplan andWeisbach (1992) show, divested acquisitions arenot in themselves evidence of failures.

We find that the recency of the focal firm’sexperience is less influential for acquisitions thanit is for alliances or divestitures. This meansthat learning between deals is more potent atthe non-integrative end of the spectrum. Firmsare more likely to choose a divestiture if theyhave recently divested or an alliance if theyhave recently allied. Yet they are no more likelyto choose an acquisition if they have recentlyacquired. In the hypothetical case in which a firmhad engaged in deals of all three types with equalrecency, the findings imply a greater likelihoodthat a less integrative governance form would bechosen. The learning effects underlying alliancecapabilities are more persistent than those thatunderlie acquisition capabilities, and the learn-ing effects underlying divestiture capabilities lastlonger than those that underlie alliance capabili-ties.

The interaction between uncertainty and assetspecificity is positive and significant. This is sup-portive of Hypothesis 12a and is consistent withprior empirical evidence on transaction cost the-ory as reviewed in Shelanski and Klein (1995).The results also indicate that internal organi-zational costs—as measured by the percentageof the target/partner’s industry employment asmanagers—are associated with less integrativechoices, which is also consistent with a transac-tion–cost hypothesis (Hypothesis 12b) and withthe evidence in Masten et al. (1991). Despite this,our measures are coarse proxies for the vari-ables that they represent, and therefore lend them-selves to alternative interpretations such as theresources–transaction costs view that underlies ourHypotheses 1a and 1b.

Copyright 2005 John Wiley & Sons, Ltd. Strat. Mgmt. J., 26: 1183–1208 (2005)

Acquisitions, Alliances, and Divestitures 1201

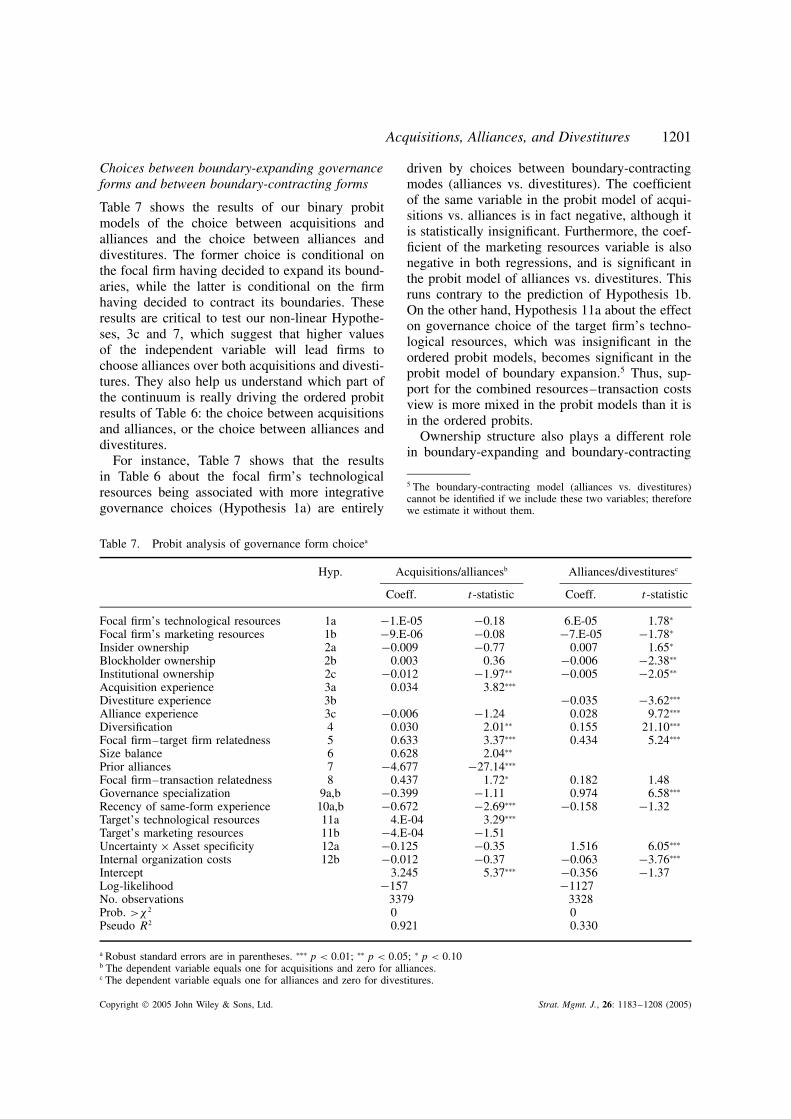

Choices between boundary-expanding governanceforms and between boundary-contracting forms

Table 7 shows the results of our binary probitmodels of the choice between acquisitions andalliances and the choice between alliances anddivestitures. The former choice is conditional onthe focal firm having decided to expand its bound-aries, while the latter is conditional on the firmhaving decided to contract its boundaries. Theseresults are critical to test our non-linear Hypothe-ses, 3c and 7, which suggest that higher valuesof the independent variable will lead firms tochoose alliances over both acquisitions and divesti-tures. They also help us understand which part ofthe continuum is really driving the ordered probitresults of Table 6: the choice between acquisitionsand alliances, or the choice between alliances anddivestitures.

For instance, Table 7 shows that the resultsin Table 6 about the focal firm’s technologicalresources being associated with more integrativegovernance choices (Hypothesis 1a) are entirely

driven by choices between boundary-contractingmodes (alliances vs. divestitures). The coefficientof the same variable in the probit model of acqui-sitions vs. alliances is in fact negative, although itis statistically insignificant. Furthermore, the coef-ficient of the marketing resources variable is alsonegative in both regressions, and is significant inthe probit model of alliances vs. divestitures. Thisruns contrary to the prediction of Hypothesis 1b.On the other hand, Hypothesis 11a about the effecton governance choice of the target firm’s techno-logical resources, which was insignificant in theordered probit models, becomes significant in theprobit model of boundary expansion.5 Thus, sup-port for the combined resources–transaction costsview is more mixed in the probit models than it isin the ordered probits.

Ownership structure also plays a different rolein boundary-expanding and boundary-contracting

5 The boundary-contracting model (alliances vs. divestitures)cannot be identified if we include these two variables; thereforewe estimate it without them.

Table 7. Probit analysis of governance form choicea

Hyp. Acquisitions/alliancesb Alliances/divestituresc

Coeff. t-statistic Coeff. t-statistic

Focal firm’s technological resources 1a −1.E-05 −0.18 6.E-05 1.78∗

Focal firm’s marketing resources 1b −9.E-06 −0.08 −7.E-05 −1.78∗

Insider ownership 2a −0.009 −0.77 0.007 1.65∗

Blockholder ownership 2b 0.003 0.36 −0.006 −2.38∗∗

Institutional ownership 2c −0.012 −1.97∗∗ −0.005 −2.05∗∗

Acquisition experience 3a 0.034 3.82∗∗∗

Divestiture experience 3b −0.035 −3.62∗∗∗

Alliance experience 3c −0.006 −1.24 0.028 9.72∗∗∗

Diversification 4 0.030 2.01∗∗ 0.155 21.10∗∗∗

Focal firm–target firm relatedness 5 0.633 3.37∗∗∗ 0.434 5.24∗∗∗

Size balance 6 0.628 2.04∗∗

Prior alliances 7 −4.677 −27.14∗∗∗

Focal firm–transaction relatedness 8 0.437 1.72∗ 0.182 1.48Governance specialization 9a,b −0.399 −1.11 0.974 6.58∗∗∗

Recency of same-form experience 10a,b −0.672 −2.69∗∗∗ −0.158 −1.32Target’s technological resources 11a 4.E-04 3.29∗∗∗

Target’s marketing resources 11b −4.E-04 −1.51Uncertainty × Asset specificity 12a −0.125 −0.35 1.516 6.05∗∗∗

Internal organization costs 12b −0.012 −0.37 −0.063 −3.76∗∗∗

Intercept 3.245 5.37∗∗∗ −0.356 −1.37Log-likelihood −157 −1127No. observations 3379 3328Prob. >χ 2 0 0Pseudo R2 0.921 0.330

a Robust standard errors are in parentheses. ∗∗∗ p < 0.01; ∗∗ p < 0.05; ∗ p < 0.10b The dependent variable equals one for acquisitions and zero for alliances.c The dependent variable equals one for alliances and zero for divestitures.

Copyright 2005 John Wiley & Sons, Ltd. Strat. Mgmt. J., 26: 1183–1208 (2005)

1202 B. Villalonga and A. M. McGahan

decisions. In the former, only institutionalownership is significant and has the negative signpredicted by agency theory (Hypothesis 2c). In thelatter, all three variables are significant, includingblockholder ownership, which was insignificant inthe ordered probit models, but is now negativeand significant in support of Hypothesis 2b. Thepositive sign of insider ownership shows thatthe results that were contrary to agency theoryin Table 6 are entirely attributable to the choicebetween alliances and divestitures. Consistent withagency theory and with earlier evidence of theincentive alignment role played by insider equityownership, firms are less likely to engage in

acquisitions the higher is the ownership stakeof those insiders, although the coefficient is notstatistically significant. While event study evidenceshows that spin-offs and divestitures tend tocreate value for shareholders (Rosenfeld, 1984;Jain, 1985; Daley et al., 1997; Krishnaswami andSubramaniam, 1999), there is similar evidenceof positive abnormal returns to joint venturesand alliances (McConnell and Nantell, 1985;Koh and Venkatraman, 1991; Chan et al., 1997;Das, Sen, and Sengupta, 1998). The case for anagency explanation to managers’ preference foralliances over divestitures is therefore weaker thanit is for managers’ preference for acquisitions,

Table 8. Ordered probit analysis of governance form choice on alternative categoriesa

Variable Hyp. 3 governance form valuesb 9 governance form valuesc

Coeff. t-statistic Coeff. t-statistic

Focal firm’s technological resources 1a 5.E-05 2.65∗∗∗ 4.E-05 2.39∗∗