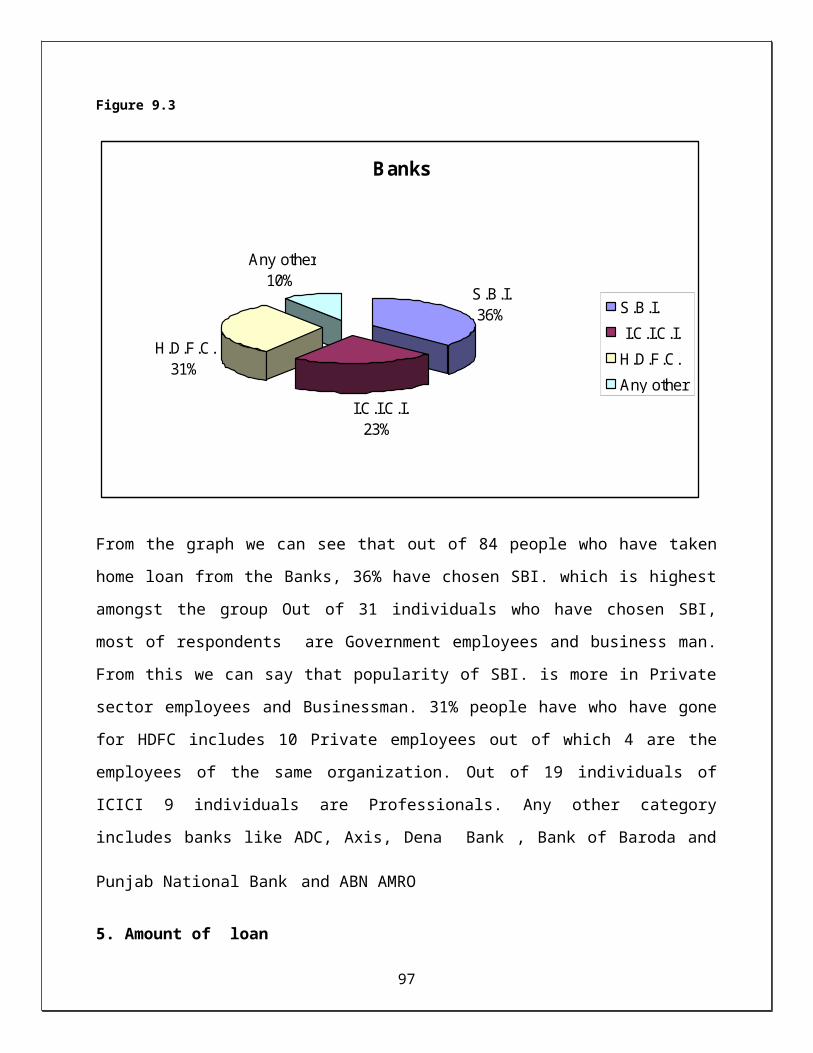

retawprojects.comretawprojects.com/uploads/In-Depth_Study_of_Housing... · Web viewSBI Home Finance...

166

1

-

Upload

duongkhanh -

Category

Documents

-

view

214 -

download

0

Transcript of retawprojects.comretawprojects.com/uploads/In-Depth_Study_of_Housing... · Web viewSBI Home Finance...

1

1. Retail Banking Industry Profile

Retail Banking Industry in India

covers industry segments like housing loan, auto loan, personal loan, education loan, consumer

durable loan, credit card, debit cards, bank assurance and the regular operation of the banks. The

major players(including Public, Private, and Foreign sector) in the Indian Banking Industry

includes Bank of Baroda, State Bank of India, Canara Bank, Punjab National Bank, HDFC

Bank, ICICI Bank, Kotak Mahindra Bank, Citibank, Standard Chartered Bank, HSBC Bank,

ABN AMRO Bank, American Express, etc.

During 2006-07, gross credit extended by Indian commercial banks grew by 34.83% to touch

INR 19,495 billion. Retail credit constitutes about 25% of the total credit and has grown by

28.0% to INR 4,218.3billion The annual growth in bank credit to the commercial sector is at

25.4% as on March 31, 2007 and was lower than 27.2% against previous year. Until 2010, retail

banking is expected to grow at a CAGR of 28% to touch a figure of INR9, 700 billion.

India's retail-banking assets are expected to grow at the rate of 18% a year over the next four

years (2006-2010). Housing loan accounts for major chunk of retail loan.

Pension fund industry in India grew at a CAGR of 122.44% from 1999-00 to 2007-08.

In terms of ownership, debit cards are more in number than credit cards but in terms of

transactions, use of credit cards is more prevalent than debit cards.

The ATM outlets in India increased at a rate of 28.09% from March 2007 to March 2008.

Outstanding Education loan segment is expected to grow at 36.41% till March 2009 from

March 2007 onwards to cross Rs. 27000 Crore Mark.

Two-wheeler finance industry is projected to forge ahead at a CAGR of 14.21% till

2009-10 from 2005-06.

2

Indian Mutual Fund industry witnessed a growth of 49.88% from May 2007 to May

2008, and a higher 215.61% growth was recorded in closed ended schemes.

Increasing number of millionaires in India is increasing the scope of Wealth Management

Services.

Bankable households in India are estimated to move up at a CAGR of 28.10% during

2007-2011.

India's retail-banking assets are expected to grow at the rate of 18% a year over the next

four years (2006-2010). Housing loan account for major chunk of retail loan.

3

4

2. Housing Finance sector in India

Industry Classification

Life cycle position

Housing finance as a financial service is relatively young in India. The growth in housing and housing finance activities in recent years reflect the buoyant state of the housing finance market in India. The real estate sector is the second largest employment generator in the country.

In 1970, the state set up the Housing and Urban Development Corporation (HUDCO) to finance housing and urban infrastructure activities, in 1977, the Housing Development Finance Corporation (HDFC) was the first housing finance company in the private sector to be set up in India.

Currently there are 29 HFCs approved for refinance assistance from NHB.

The following types of home loans are generally available in the market:

Home Equity Loans: A form of finance to the customer by way of mortgage of existing property to the financier for taking a loan for some other purpose. The current market value of the property is the basis for providing home equity loans.

Home Extension Loans: The purpose of this loan is the extension of existing houses tike the addition of rooms, toilet facilities etc. Such loans fall under the category of home loans.

Home Improvement Loans: These loans are provided mainly for repairs and maintenance of existing houses- These could include internal and external repairing, waterproofing and roofing, complete interior renovation, tiling and flooring etc.

Home Purchase Loans: Finance provided for the purchase of ready-made houses.

Land Purchase Loans: These loans are being provided for the purchase of land for the purpose

of construction of residential houses.Private housing finance sector is also doing very well in

catering the need for housing finance. Dewan Housing Finance Corporation Ltd. is one of the

best options in private housing finance sector. Having 22 branches all over the country and

dealing in the market for more then 15 years, the group is well established in the market. Rural

housing finance is one of the best schemes in India offered by Dewan Housing. With most

competitive interest rates in private sector housing finance market, and personalized finance is

made available to informal sectors besides formal sector like service class.

5

HUDCO is a powerful government organization. Financing state government for infrastructural

development is the main aim. But ever since it has entered individual housing finance sector, the

entire scenario has changed. The main war of interest rates has actually begun when HUDCO

has started giving housing finance for 11.5 % and after deductions the interest rates comes to

8.81%.

After NHB, many housing finance companies looked at HUDCO for refinancing their proposals.

Hometrust Ltd., a company by Gujarat Ambuja Group, Global Housing finance Ltd., a syndicate

of reputed builders, Weizmann Homes Ltd., a company from Weizmann Finance Ltd., Maharishi

Housing Finance Corporation Ltd., a company from Maharishi Group, are also catering to

housing finance sector. SBI Home finance Ltd., a subsidiary of SBI, PNB Housing Finance Ltd.,

a subsidiary of PNB is also doing very good business. SBI Home Finance Ltd. is doing little bit

slow for the time being but PNB Housing Finance Ltd. has recently opened its new branch near

Shoppers Stop, Andheri. BOB Housing Finance Ltd., a subsidiary of Bank of Baroda also having

very attractive housing finance schemes. Can Fin Homes, very aggressive subsidiary of Canara

Bank in Southern India, is also doing very good job in Western parts of the country.

Nationalized banks are coming in a very big way into housing finance market. SBI, an oldest

financial institution and bankers for majority of Indians have entered with interest rates of

12.24 %. PNB has crossed Rs. 50 crore alone in Mumbai region for housing finance in very

short period of time.

LIC housing finance Ltd., is one of the largest and oldest housing finance institute, is offering

one of the best services in the industry. Having its branches all over India, it offers variety of

loans like housing finance for new purchases, re-constructions, renovations, NRI housing finance

etc. GIC Housing Finance Ltd., a company from the house of General Insurance Company is

also having very strong clientele in recent years. A silent company, but very vibrant in its

performance, is also gearing for new land marks in the industry.

Last but not the least, HDFC, one of the best housing finance company in the country is all set to

take on the challenges of housing finance sector. With reduced interest rates, the company is

6

having its name as synonymous as, housing finance. Gruh Finance, a subsidiary of HDFC is also

giving very good business in Gujarat.

Table2. 1

Bank name

Interest Type

Interest Rates for various loan amount

Actionupto 5 lakh

5-20 lakh

20-30 lakh

30-50 lakh

50-75 lakh

>75 lakh

83 Sample Results based on default inputs.

Allahabad Bank Fixed 12.25 12.25 12.25 12.25 12.75 12.75

Axis Bank Floating 8.75 8.75 8.75 9.25 NA NA

Axis Bank Fixed 14 14 14 14 NA NA

Bank of Baroda Floating 9 9 9 9.75 9.75 9.75

Bank of India Star Home Loan - Floating Floating 9.25 9.25 9.25 10.25 11 11

Bank of Maharashtra Floating 9.25 9.25 9.25 9.75 9.75 9.75

Bank of Maharashtra- Festive offer Floating 8 8 8 8.25 8.25 8.25

Bank of Rajasthan Fixed 9 9 9 9 9 9

Bank of Rajasthan Floating 7.5 7.5 7.5 8 8 8

Canara Bank Fixed 11.5 11.5 11.5 11.75 11.75 11.75

Canara Bank Floating 9.25 9.25 9.25 10 10 10

HDFC Floating 8.75 8.75 8.75 9 9.25 9.25

HDFC Fixed 14.25 14.25 14.25 14.25 14.25 14.25

HSBC Bank Floating 9.0 - 9.0 - 9.0 - 9.0 - 9.0 - 9.0 -

7

14.0 14.0 14.0 14.0 14.0 14.0

ICICI Bank Floating 8.75 8.75 8.75 9 9.5 9.5

ICICI Bank Fixed 16 16 16 16 16 16

IDBI Bank Fixed 11 11 11 11 11 11

IDBI Bank Special Scheme Floating 8.25 8.25 8.25 8.25 8.25 8.25

IDBI Home Finance Floating 8.25 8.25 8.25 8.25 8.25 8.25

IDBI Home Finance Fixed 13.75 13.75 NA NA NA NA

Indian Bank Floating 9.75 9.75 10 10.5 10.5 10.5

Indian Overseas Bank Floating 8.75 8.75 8.75 10.25 NA NA

J & K Bank Floating 11.5 11.5 12.25 12.25 12.25 NA

Kotak Bank Floating 8.5 8.5 8.5 8.5 8.5 NA

LIC Fix-o-Floaty Floating 8.9 8.9 8.9 8.9 8.9 8.9

LIC Housing Finance Floating 9.75 9.75 9.75 9.75 9.75 9.75

Moneyline Credit Ltd Floating 15 15 15 15 15 15

Oriental Bank of Commerce Floating 9.25 9.25 9.5 10.25 10.25 10.25

Oriental Bank of Commerce Fixed 10.25 10.25 10.5 NA NA NA

PNB Housing Finance Ltd Floating 9.5 9.5 10 10 10 10

PNB Housing Finance Ltd Fixed 13 13 13 13 13 13

Punjab & Sind Bank Floating 8.25 8.25 8.5 10 10 10

Punjab National Bank Fixed 10.5 10.5 10.75 10.75 10.75 10.75

8

Punjab National Bank Floating 9.25 9.25 9.75 9.75 9.75 9.75

Punjab National Bank- Festive offer (Fixed) Fixed 8.5 8.5 8.5 8.5 8.5 8.5

Punjab National Bank- Festive offer (Floating) Floating 8.5 8.5 8.5 8.5 NA NA

Reliance Home Finance Floating 8.25 8.25 8.25 8.25 8.25 8.25

SBBJ Advantage Home Loan Fixed NA NA NA NA 8 8

SBBJ Advantage Home Loan Floating NA NA NA NA 8 8

SBBJ Easy Home Loan Fixed 8 8 8 8 NA NA

SBBJ Easy Home Loan Floating 8 8 8 8 NA NA

SBI Floating 9.75 9.75 9.75 10.25 10.25 10.5

SBI Advantage Home Loan Fixed NA NA NA NA 8 8

SBI Advantage Home Loan Floating NA NA NA NA 8 8

SBI Easy Home Loan Fixed 8 8 8 8 NA NA

SBI Easy Home Loan Floating 8 8 8 8 NA NA

South Indian Bank Fixed 12.75 12.75 12.75 13.5 13.5 13.5

9

Few Housing Finance Companies & Banks of India Housing Development Finance Corporation Limited (HDFC)

Housing Development Finance Corporation Ltd (HDFC) is one of the leaders in the

Indian housing finance market with almost 37% market share. Serves more than 26 lakh

customers across the nation, HDFC also offers customized solutions that fit to the need of

the customer. In the FY 2008, it registered a net profit of Rs. 2,282.54 crore. It also

registered a net profit of Rs. 663.94 crore in the quarter ended September 30, 2009.

State Bank of India Home Finance (SBI)

State Bank of India is another major player in the Indian housing finance market with

almost 16% of the market share. The SBI Housing Loan schemes are specifically

designed to meet the varied requirements of the customers. It offers home loan for

various purposes including new house/flat, purchase of land,

renovation/alteration/extension of existing house/flat etc. SBI Home Finance registered a

net profit of Rs. 24.63 crore in the year ended March 31, 2009.

LIC Housing Finance Limited

LIC Housing Finance is another major player in housing finance sector in India with

almost 13% of market share. Promoted by Life Insurance Corporation of India, LICHFL

has an extensive distribution network with a strong brand presence. Recently, the

company has been awarded “Consumer Superbrand 2009/10 Status” by Superbrands

Council. In the last financial year (ended on March 31, 2009), LICHFL earned a net

profit of Rs. 387.19 crore, comparing to Rs. 279.14 in the previous FY. It also registered

a net profit of Rs. 171.25 crore in the quarter ended on September 30, 2009.

10

ICICI Home Finance Company Limited

ICICI is a leading housing finance company in India with almost 6% market share. It

offers various types of home loans for its customers which may have tenure up to 20

years. The home loan interest rate is connected to the ICICI Bank Floating Reference

Rate (FRR/PLR). Here it can be added here that, the PLR has been reduced to 14.75%

from its previous rate of 15.25% since June 4, 2009. As on January 23, 2009, ICICI HFC

has 1416 branches with an asset of Rs. 3,74,410 crore. As on December 31, 2008, the

company has a net worth of Rs. 50,035 crore.

Dewan Housing Finance Corporation Limited (DHFL)

Dewan Housing Finance Corporation Limited is one of the largest housing finance

solution providers in India with an extensive network of 74 branches, 78 service centers

and 35 camps spread across the nation. The company registered a net profit of Rs.

8,631.83 lacs in 2008-09, comparing to a net profit of Rs. 8,257.74 lacs in the previous

financial year. In the quarter ended on September 30, 2009, DHFL earned a profit (after

tax) of Rs. 3,751.09 lacs.

11

12

3. The Housing Finance System in India

The following chart shows the financial institutes, banks and other specific institutes involved in financing the people for the houses.

13

Figure 3. 1

The following institutes are providing different Home Loan product to the different class of the

people in the society and conduct the activity of financing and refinancing in the sector.

1. Scheduled Commercial Banks

2. Housing Finance Companies

14

3. Scheduled Cooperative Banks (Scheduled State Co-operative Banks, Scheduled District

Cooperative Banks and Scheduled Urban Cooperative Banks)

4. Agriculture and Rural Development Banks

5. State Level Apex Co-operative Housing Finance Societies

Scheduled Commercial Banks

The SCBs have the largest network of branches and are also the largest mobilizer of savings in

the country. Since housing finance becomes a part of the 40 per cent Priority Sector lending, it

makes business sense for banks to undertake this activity. Moreover, a favorable tax and

regulatory regime, act as catalyst for doing business in this sector. Further, the earmarking of 3

per cent of incremental deposits of SCBs to finance housing activities has ensured availability of

adequate funds for housing activities. Security by way of mortgage of property and robust

demand has been major considerations for banks to lend to this sector.

Housing Finance Companies

To boost the housing sector there is a need to regulate and have a greater access of credit for

housing. Thus a good housing finance system is imperative. Housing Finance Companies (HFC)

need to be recognized as a part of total financial system and should be given a level playing

field.

Amidst liberalization certain provisions of the Company’s Act 1956, such as, restrictions on

interoperate loans and deposits continue to discriminate Housing Finance Companies against

other non-banking financial companies. Also certain tax laws, such as deduction of tax at

sources, restrictions on acceptance of cash as deposits are disadvantages to HFC. The Reserve

Bank of India has put housing finance on priority core sector lending. In the developed

countries, the flow of housing finance a substantial share of total financial system. In fact, the

savings for housing is among the single largest source of funds in their entire financial system.

Schedule Cooperative Banks

15

The concept of Co-operatives as an institutional mechanism for satisfying various needs of the

people is premised on the principles of ‘self-help’ as well as ‘collective–effort.’ Scheduled State

Co-operative Banks, Scheduled District Cooperative Banks and Scheduled Urban Cooperative

Banks come under heading of the Schedule Cooperative Banks. Housing cooperatives have a

prominent place in the cooperative movement in the country. Today, it is estimated that there are

over 92,000 primary housing cooperatives with over 6.5 million members.

The co-operative sector has played an important role in providing housing to its members and

has made a significant impact across the country. The cooperative sector is expected to play a

lead role, particularly in land acquisition, allotment of land and housing sites to encourage group

housing and development of amenities in their projects, as envisaged in the National Housing

and Habitat Policy. The National Co-operative Housing Federation (NCHF) was established as

an apex organization for coordinating, guiding and promoting cooperative housing activities in

the country.

Agriculture and Rural Development Banks

Keeping in view the housing shortage in rural areas, a few state governments, after suitable

legislative amendments, have permitted the Agriculture and Rural Development Banks (ARDBs)

to lend for housing. As the ARDBs do not fall under the category of either SCBs or specialized

housing finance institutions, NHB formulated a scheme to subscribe to special rural housing

debentures floated by ARDBs, backed by the mortgages originated by them, in order to extend

financial assistance to this category of institutions.

State Level Apex Co-operative Housing Finance Societies

Apex Co-operative Housing Finance Societies (ACHFS) at the state level are affiliated to The

National Co-operative Housing Federation (NCHF) of India, which looks after their growth

strategies, policy formulations and evolving housing programmes besides inter-facing with

various institutions to channel finances for these Societies for onward lending to the ultimate

16

borrowers. In addition, NCHF also helps the ACHFS in improving their financial, organizational

and technical capabilities.

The primary housing co-operatives functioning at the grass root level are supported by 25

ACHFS all over the country with a membership of over 6.5 million. These ACHFS represent

about 92,000 housing co-operatives all over the country out of which, about 31,000 housing co-

operatives are affiliated to state level ACHFS for getting financial assistance.

17

4. Issues with the Housing Finance sector in IndiaAggressive approach may lead to defaults

Growing competition coupled with reduction in risk weights on housing loans has led the

lending institutions to adopt aggressive practices including very high loan has led the lending

18

institutions to adopt aggressive practices including very high loan to value loans, softening of

collateral requirements, competitive pricing etc. with such an aggressive approach being

followed may lead to increase in the default rates.

Cost of funds

The prevailing interest rate war has resulted in constant downward revision of interest rates.

Further, the spreads are increasingly becoming thin as the lending rates are fast nearing the cost

of funds. While during 1993-94, the interest rate on housing loans were in the range of 17-18%

the same right now are in the range of 7%-8.5%. This may lead to erosion of profitability in the

long run.

Security Deficit due to norms

Many primary lending institutions are making terms and conditions of sanction flexible and

liberal, thus enabling the borrowers to avail the loans even more than value of security for long

tenure of 20 to 25 years. The large quantum of institutional finance in the property transactions

may lead to the problem of security deficit.

Due diligence Issues

Increasingly, there have been instances of dilution in due diligence on the part of lenders.

Sometimes, loans are sanctioned without strictly complying with laid down rules, systems and

procedures. This situation arises primarily out of fierce competitive pressures. It is observed that

the growing customer expectations force the Prime Lending Institutes to compromise due to

diligence, field verification process and appraisal norms, in a rush to sanction the loan at the

earliest.

Lack of Uniformity of norms amongst industry players

While banks and HFCs are the prominent players, HFCs face few constraints. The regulatory

norms stipulate 10% capital adequacy for banks whereas the same is 12% for HFCs. Further,

banks have access to lower cost retail funds compared to HFCs. Uniformity in norms and hence

19

a level playing field has to be ensured for a healthy housing finance system. These are newer

challenges which need to be addressed and resolved in times to come.

Industry Fragmentation

The fragmented nature of the housing finance industry is a major impediment for its further

growth. Despite this, the industry has managed to grow mainly due to consistent decline in

interest rates, tax incentives given by the government and changing income profile of the Indian

middle class population.

Conflicting Interests

While the private housing finance institutions are required to abide by the guidelines of the

NHB, the general financial institutions, which include the commercial banks, follow the

guidelines set by the RBI. Today, both these sections are competing with each other for the same

housing pie but their functioning and lending practices seem to bear no similarity.

ALM

Asset liability mismatch is one of the biggest risks housing finance institutions are confronted

with. Funding of long term loans with short term deposits, leads to a mismatch between assets

and liabilities that can be overcome by adopting appropriate asset liability management (ALM)

techniques.

20

Future Outlook

The onset of year 2010 has brought in some good news for those who are dreaming of a 'home'

with home loan rates as well as property rates spiraling downwards.

The considerable reduction in rates is already beginning to affect deposit rates and will soon lead

to a fresh round of rate cuts for both deposits and loans. In fact home seekers are likely to see

single digit interest rates for regular 20 year home loans (not just for those below Rs. 20 lacs) in

this quarter from at least the PSU banks.

Recently announced stimulus package by the Government entails consumers seeking home loans

between Rs. 5 lacs+upto Rs. 20 lacs a fixed interest rate (for 5 years) of 9.25% and nil

processing and pre-payment fees and free life insurance to boot. However it cannot solve the

issue of lack of risk appetite in the banks. Clearly, the banks want to play safe. On the other hand

consumers The significant reduction in interest rates is likely to result in some increase in

demand for such properties. Notwithstanding some corrections, property prices in popular areas

continue to be unaffordable and we are unlikely to see new demand emerging till the prices reach

some kind of equilibrium. So the number of consumers who will take advantage of this package

is unlikely to be very high. Only if the property rates drop by between 20-25% in the middle and

high-end home segments, one can expect a spurt in the business.

In the meanwhile RBI can make the home loan seeker better equipped by issuing the licenses to

Credit Bureaus so that the consumer's right to his own credit report can be activated. This will

have a significantly positive effect on credit sensitivity in the country and bring home to the

consumer the benefits of paying their bills on time as well as the cost of not paying them on

time. Also make the necessary operational changes in Section 138 of the Negotiable instruments

act to ensure so that people realize the seriousness of issuing cheques and the impact of

dishonoring them. Finally, activate the Mortgage guarantee scheme so that the effective down

payment can be brought down in a home purchase.This will raise the customer's confidence level

and this is the need of the hour! Clearly all things going right we should see a spurt in business

in the last quarter of the year which is also traditionally a large demand quarter. Also await a

further reduction in property prices before they will act on the property purchase decision.

21

22

5. Research Proposal

Objectives

Macro Objective

To imbibe a broad knowledge regarding Housing Finance Sector.

Micro Objective

1. To study the preference and satisfaction level of the customers regarding Housing

Finance providers.

2. To study the Home Loan process in ICICI Housing Finance.

Scope

We have taken the Housing Finance as the product of Retail Banking sector. This project has

helped to know the macro factors affecting the Housing Finance sector in India. When it comes

to micro factors, customer satisfaction, preference and behavioral aspects regarding the Housing

Finance are the out puts of the live research. The study of the Home Loan Process at ICICI

Housing Finance has helped us to get practical exposure of operation hierarchy of Home Loan

Process.

Research Methodology

Data Source:-

Primary data:

Information collected though the survey of consumers of the bank

Secondary data:

Industry portals, company websites, magazines, newspapers, trade journals, other financial

data provided by the bank required for the study.

23

Research Approach:-

We have used the Survey Research to collect the primary data, as it is best suited for descriptive

research.

Research Instrument:-

We have used the questionnaire as our research instrument. In which close-ended and open-

ended questions have help to understand consumer preference and behavior more clearly.

Sampling Plan:-

Sample Unit : One Home Loan Taker

Sampling Size : consumers

Sampling Method : Simple Random Sampling

Contact Method:-

Out of the four method of primary data collection namely mail questionnaire, telephone

interview, personal interview and online interview; we will be using personal interview and

telephone interview , so that we can ask more questions.

Limitations

As it is the questionnaire survey, there are chances of bias answers.

We have taken simple random sampling because population survey is not possible.

Sampling plan is limited to Ahmedabad region only.

Limited time period to conduct the project

Limited information was available from company side.

24

25

6. Guidelines for the Sanctioning Process

Here are the basic guidelines which every loan provider has to accept and follow before

sanctioning any loan in India.

Basic qualifications for a home loan (Resident Indian)

(I) A resident Indian is eligible for a home loan if he satisfies the following

conditions :

1. He must be earning a regular monthly income.

2. If he is from the salaried class, then he should a minimum of 5 years of service left.

3. Above 21 years of age at the commencement of the loan

4. Below 65 when the loan matures

5. If he is a business person or a professional or a self employed individual, then his age

should be less than 58 years at the time of applying for the loan.

6. The property that he wishes to purchase/construct should have a clear and marketable

title.

(II) Documents required to be submitted at the time of application

There are certain sets of documents that need to be submitted at the time of application. The

documents sets will vary according to individual status- either resident or non-resident in India,

as also the type of loan that an individual may want to avail of.

Resident Indian

(a) Salaried Individual

26

Salary slip/Form 16A

A photocopy of the first and last pages of ration card or copy of PAN /telephone/

electricity bills.

A photocopy of Investments (FD certificates, Shares, any fixed asset, etc) or any other

documents supporting the financial background of the borrower

A photocopy of LIC policies with the latest premium payment receipts (if any)

Photographs (as applicable)

A photocopy of bank statement for the last six months.

(b) Self employed or businessman

A brief introduction of business/profession

Balance sheet, profit & loss account and statement of income with Income Tax returns

for the last 3 years certified by the Chartered Accountant

A photocopy of advance tax payments (if applicable)

A photocopy of registration certificate of establishment under shops and establishments

Act/factories Act

A photocopy of registration certificate for deduction of profession tax (if Applicable)

Bank statements of current and saving accounts for the last six months

A photocopy of certificate of practice (if applicable)

A photocopy of any bank loan (if applicable)

A photocopy of the first and last pages of the Ration card or a copy of

PAN/telephone/electricity bills

A photocopy of investments (FD certificates, shares, any other fixed assets)

27

(c) If flat is purchased from builder

Original copy of your agreement with the builder

7/12 extract of your agreement with the builder

Copy of N.A. permission for the land from the collector

Search and title report (with the details of the documents) for the last 30 years

Development agreement between the owner of land and the builder

Copy of the order under the urban land ceiling Act

Copy of building plans sanctioned by the competent authority

Commencement certificate granted by the corporation / Nagar Palika

Building completion certificate (if available)

The latest receipts of taxes paid

Partnership deed or memorandum of association of the builder firm

(d) If the property is being purchased in a co-operative society

Original share certificate of the society

Allotment letter from the society in your name

Copy of the lease deed, if executed

Certificate of the registration of the society

Copy of the bye-laws of the society

No objection certificate from the society

7/12 extract or property register card in the society’s name

28

Copy of N.A permission for the land from the collector

Search and title report (with the details of documents) for the last 30 years

Copy of order under the urban land ceiling Act

Copy of the building plans sanctioned by the competent authority

Commencement certificate granted by the corporation / Nagar Palika

The latest receipts of tax paid

Original Agreement to assign/ Deed of assignment

(e) If constructing on own land

Original sale deed of land and extract of index 2

7/12 extract or property register card in your name

Copy of N.A permission for land from the collector

Search and title report (with the details of documents) for the last 30 years

Copt of order under urban land ceiling Act

Copy of the building plans sanctioned by the competent authority

Building permission granted by corporation / Nagar Palika

The latest receipts of taxes paid

Estimate of cost of construction certified by the architect

Non-residents

(a) Income Documents

29

Employment contract (if the contract is in any language other than English, the same has

to be translated into English and arrested by the employer/Indian Embassy)

Certified copy of the latest salary slips of the past 6 months

Identity card issued from the current employer

Continuous discharge certificate, if applicable

Latest work permit

Visa stamped on passport

NRE bank account passbook sheets

Overseas bank account statements for the past 6 months

Bio-data covering educational qualifications, age job experience, nature of profession/

business with necessary proof

Power of attorney in favour of local representative in India, if required Guarantor forms

along with net worth proof / income proof. Number of guarantors as per the norms of the

company. The guarantors should be related to the applicant(s)

(b) Property documents: purchase of a flat from the builder/promoter

Title deeds of the builder/land owner for a period of at least 13 years

Development agreement between the builder and land owner if applicable

Power of attorney executed in favour of the builder, if applicable

Non-encumbrance certificate for the past 13 years

The khata certificate (basic document indicating ownership of property as entered in the

register of the government authorities)

Up-to-date tax paid receipts of the property

30

A sanctioned plan and Licence

An agreement for sale and a construction agreement with the borrower

(c) In case of purchase of house from second owner

Title deeds of land owner for a period of at least 13 years

Non-encumbrance certificate for the past 13 years

Khata certificate

Up to date tax paid receipts of the property

Sanctioned plan and license

Agreement for sale in favour of the applicant(s)

Valuation report from the qualified valuers

(d) Incase of repairs/ renovation/ extension of house/ flat

Title deeds of land owner for a period of at least 13 years

Non-encumbrance certificate for the past 13 years

Khata certificate

Up to date of tax paid receipts of the property

Sanctioned plan and license for the extension

Agreement for sale in favour of the applicant(s)

Estimates of costs from the qualified engineer

31

(e) Personal Documents

1 passport size photograph

1 copy of your passport/ PAN card/ Driving License/ school leaving certificate/ birth

certificate/ LIC policy/ bankers sign verification

1 copy of last months telephone bill / ration card (first and last page) / title deed

property / rental agreement / driving license

(III) Loan amount eligibility

The maximum amount that a resident Indian can borrow from housing finance companies is

75% - 85% of the project cost. Subject to this condition, the borrowers repayment capacity takes

into consideration factors such as income, age, qualifications, number of dependants, spouse’s

income, assets, liabilities, stability and continuity of occupation and saving history. Loans

beyond the above mentioned limits can be considered by the housing finance companies

depending on the merits of the case.

(IV) Documents required to be submitted after sanction

Apart from the various documents to be submitted at the time of application of loan, there are

further documents to be given to the housing finance company once the loan is sanctioned.

Tri-partite agreement between the borrower, builder and housing finance company

Proof of investment of margin money

Loan papers by the applicants

Guarantee agreements with sureties

Post dated Cheques

Original documents executed with the builder or previous owner

No objection certificate from the builder to mortgage the property in favour of the

housing finance company

32

No objection certificate from other housing finance companies if the builder has availed a

project loan

No objection certificate from the co-operative housing society

Share certificate of housing society

33

34

8. Home Loan: The Process

From applying for a home loan to getting it involves various stages. These are:

Step 1: Application form

Step 2: Personal Discussion

Step 3: Bank's Field Investigation

Step 4: Credit appraisal by the bank and loan sanction

Step 5: Offer Letter

Step 6: Submission of legal documents & legal check

Step 7: Technical / Valuation check

Step 8: Valuation

Step 9: Registration of property documents

Step 10: Signing of agreements and submitting post-dated cheques

35

Step 11: Disbursement

1. Applying for a loan

Filling up the application form is the first step. The look of an application form may differ from

bank to bank, but nearly 80 per cent of the information they need is similar. Most of this is

basically personal and professional information, details of applicants financial assets and

liabilities and the details of the property (if finalized) including the estimated cost and the means

of financing the same.

Documents to submit:

While submitting the application form, every bank asks for several documents. And most banks

these days provide doorstep service, so that applicant doesn't have to spend time visiting their

office to submit the documents. However, some banks still insist on the customer visiting their

offices at least once.

Proof of income:

This will need to be backed up by proof such as copies of last three years Income Tax returns

(along with copies of Computation of Income/Annual accounts, if any), Form 16/Form 16A, last

three months salary slips, copies of the last 6 months statements of all applicant’s active bank

accounts in which applicant’s salary/business income details are reflected, etc. Other documents

that applicant need to provide with application form include age proof, address proof and

identification proof. Applicant may also be asked to give applicant’s employment details.

Age proof:

Copy of school leaving certificate/Driving license/Passport/ration card/PAN card/Election

Commission's card/etc.

Address proof:

Similar documents need to be provided to prove that applicant is actually staying at his/her

current address.

36

Identification proof:

Same as above, but with photograph. Sometimes, the same document if it contains a photograph,

the current residential address and the correct age can be the proof for all 3 things.

Employment details:

If applicant’s company is not well-known, then a short summary about the nature of the

company, its business lines, its main customers, its competitors, number of offices, number of

employees, turnover, profit, etc may be needed. Usually, the company profile that is available on

the standard website of the company is enough.

Financial check:

All the income-related documents submitted by applicant serve a specific purpose. The lending

institution uses them to study financial status. The bank statements are scrutinized for:

Level of activity in the case of self-employed persons, this gives a very good clue about

the extent of business activities.

Average bank balance a cursory glance at the average bank balances maintained in a

savings bank account speaks volumes about the spending/saving habits of any individual.

Cheque returns a small charge debited by bank in the statement indicates that a cheque

issued by applicant was returned by applicant’s bank. Many such cheque returns can have

a negative impact on applicant’s loan sanction.

Cheque bounces if cheques deposited by applicant are returned by the issuer's bank, they

will be visible in applicant’s bank statement and again, banks have specific norms as to

how many such returns are acceptable in a period of one year.

Regular periodic payments the existence of periodic payments to other finance

companies/banks etc. indicate an existing liability and applicant will need to provide full

details to the lender.

Applicant’s investments also come under the scanner.

37

This helps the bank to estimate applicant’s ability to pay the down payment as well as

applicant’s savings habit.

Processing Fee:

Along with the application form and the credit documents, banks ask for a processing fee. This

fee varies from bank to bank, but is usually around 0.25% to 0.50% of the total loan amount. The

agent dealing with applicant earns a commission from the bank, which to some extent is also

affected by the amount of fees paid.

Most banks have flexible fee structures, and it is advisable that applicant negotiate hard to find

out the bank's minimum possible fees though it is unlikely that a bank will agree to provide a

loan without any upfront fee at all. Some banks have zero upfront fee loans, but that advantage

may be negated as their other charges such as legal charges and 'stamp duty is normally higher.

This fee is collected to maintain applicant’s loan account, and includes work like sending

Income Tax certificates every year, maintaining post-dated cheques, etc.

2. Personal discussion

After applicant has formally and successfully completed the application process, all applicants

have to do is wait till the home finance institution evaluates applicant’s papers. The wait

normally lasts only a day or two or sometimes even less. However, some banks insist on meeting

applicant after receiving the application form, and before the loan sanction. This is to gather

more details about applicant that may not be mentioned in the application form and to reassure

them of applicant’s repayment capacity.

3. Field Investigation

Thousands of people apply for loans everyday. And however eager a bank is to complete its

targets, every loan is a risk. So, it is only natural that it confirms or validates the details applicant

38

provides. The bank checks all applicant’s information including applicant’s existing residential

address, applicant’s place of employment, employer credentials (if applicant work for a small

organization), residence and work telephone numbers. Representatives are sent to applicant’s

workplace or residence to verify the details.

Even the references applicant has provided in the application form are checked out. While this

may sound irritating and an invasion of his/her privacy, banks are forced to undertake validation

in the absence of any credit bureau. Once applicant’s credentials are validated, it helps establish

trust between applicant and the bank.

4. Credit appraisal and loan sanction

This is the make-or-break stage. If the bank is not convinced about applicant’s credentials,

applicant’s application may get rejected. If it is satisfied, it sanctions applicant’s loan.

The bank or the home financier establishes applicant’s repayment capacity based on applicant’s

income, age, qualifications, experience, employer, nature of business (if self employed), etc, and

based on these, works out applicant’s maximum loan eligibility, and the final loan amount is

communicated to applicant. The bank then issues a sanction letter. This letter may either be an

unconditional letter, or may have certain terms and conditions mentioned, which applicant have

to fulfill before the loan disbursal.

5. Offer letter

← Once the loan is sanctioned, the banks sends applicant an offer letter mentioning the following

details:

o Loan amount

o Rate of Interest

o Whether fixed or variable rate of interest linked to a reference rate

39

o Tenure of the loan

o Mode of repayment

o If the loan is under some special scheme, then the details of the scheme

o General terms and conditions of the loan

o Special conditions, if any

Acceptance copy

If applicant agree with what is mentioned in the offer letter from the bank, applicant will have to

sign a duplicate letter of the same for the bank's records. Earlier, banks used to charge

administrative fees along with the offer letter. However, with rising competition, administrative

fees have virtually disappeared from the home loan market.

6. The legal angle: Property and papers

Now, the focus of the bank’s activities shifts from applicant to the property applicant intends to

buy. Once applicant select his/her property, need to hand over the entire set of original

documents pertaining to applicant’s property to the bank so that it can keep them as security for

the loan amount given to applicant.

The title documents of applicant’s seller, which prove the seller\'s title including the chain of title

documents if he is not the first owner. NOCs from the legal owners such as cooperative housing

societies, statutory development authorities, the lessor of the land in the case of leasehold land,

etc. NOCs are not required where the property is situated on freehold land and the entire land is

being transferred along with the structure.

These documents remain in the bank's custody until the loan is fully repaid.

Legal check

40

Every bank conducts a legal check on applicant’s documents to validate their authenticity. Even

the draft sale documents that applicant will be entering into with seller will be scrutinised.

The documents are sent to a lawyer in their panel (either in-house or outsourced) for a thorough

scrutiny. The lawyer's report either gives a go-ahead if documents are clear, or it may ask for a

further set of documents. In the latter case, applicant is expected to hand over the additional

documents to the bank for a clear title.

7. Technical / Valuation check

Banks are extremely careful about the property they plan to finance. They send an expert to visit

the premises applicant intend to purchase. This expert could either be a bank employee or he

could belong to a firm of architects or civil engineers.

Site visit: The site visits to applicant’s property are conducted to verify the following:

In case of under construction property: Stage of construction is the same as that mentioned in the payment notice given to applicant by the builder.

o Quality of construction

o Satisfactory progress of work.

o Layout of flats and area of property is within permissions granted by the

governing authority.

o The builder has the requisite certificates to start construction at the site.

o Valuation of the property in relation to other deals in the surrounding areas.

In case of ready/resale construction

41

o External / internal maintenance of the property.

o The age of the building.

o Will the building last the loan tenure? This has a direct bearing on applicant’s

loan eligibility, since the loan tenure will be restricted to the maximum age of the

property as decided by the bank's engineer and this will impact applicant’s loan

eligibility.

o Quality of construction.

o Surrounding area (development).

o Whether the builder has received the requisite certificates for handing over

possession of the flat.

o There is no existing lien or mortgage on the property.

o Valuation of the property in relation to other deals in the surrounding areas.

o These inspections are carried out to protect consumer interests in terms of

construction quality, adherence to local laws, approved building plans, etc. A

technical inspection also lets the bank understand the progress of construction so

as to release the staggered disbursements.

8. Valuation: Reality check

Since housing loans are cheaper than other loans, there have been cases where individuals have

shown purchase of properties from related entities at inflated prices to obtain cheap loans. Since

the risk associated with diversion of funds is higher than if the loan was used for genuine

purposes, banks carry out an independent valuation to find out whether the transaction is in line

with the existing market price of the area.

42

Valuation of real estate as a profession is still in its infancy in India and is still non-standardised.

In many cases, the valuer determines the value of the property at an amount that is lower than the

documented cost of the property and this would result in the loan amount being lower, since the

bank funds a certain percentage of the cost or valuation of the property, whichever is lower.

This practice has led to severe consumer issues in an increasing number of cases, as the

valuation is normally done only after the consumer takes a sanction (by paying a fee) and after

identifying and committing to buy the property.

The valuation issue rarely arises when a property is purchased through a reputed builder directly

or if the property is pre approved. In both the cases, the banks would have already completed the

valuation and therefore, applicant can safely assume that there is no difference between the

documented cost of the property and the bank's valuation amount.

9. Registration: Sealing the deal

After the legal and technical / valuation check, the draft documents as cleared by the lawyer need

to be finalized and signed and the stamping and registration of the documents need to be done.

Also, if any NOCs are pending, these need to be obtained in the format approved by the bank's

lawyer.

10. Signing the home loan agreement: In black & white

All borrowers need to sign the home loan agreement. Applicant also needs to submit post-dated

cheques for the first 36 months (if that is the agreed mode of repayment). The original property

documents have to be handed over to the bank at this stage. Some banks also create a document

43

recording the handing over of the property documents to them as security for the due repayment

of the home loan.

This document is also called a memorandum of entry and attracts significant stamp duty

depending on the amount of the loan in some states. The stamp duty payable on such a

memorandum is naturally recovered from applicant.

Not all banks create this memorandum and hence the stamp duty may or may not be payable,

depending on the practice of the specific bank. However, even where no such memorandum of

entry is created, the state government concerned may, in the future, demand a stamp duty on the

loan transaction, which naturally is recoverable from applicant as per the home loan agreement

signed by applicant.

11. Disbursement

After the bank has ensured that the property is legally and technically clear, all the original

documents pertaining to transfer of ownership of property in applicant’s favor have been

submitted and all the necessary loan agreements have been executed. Applicant will now

actually receive the cheque in his/her hand. Before the big moment arrives, applicant need to

submit documents to prove that applicant has paid his/her personal contribution towards the

property, since banks normally finance only up to 85-90 % of the total cost of the house.

In case applicant is expecting money from other sources to fund his/her own contribution, need

to provide sufficient evidence for the same. It is only after submitting this proof that the bank

will release part-disbursement of the loan.

The cheque will be in the name of the reseller (for resale flats), builder, society or the

development authority. It is only in exceptional circumstances, that is, if applicant provides

documents to support that he/she has made an excess payment from his/her own account then,

the cheque will be handed over to applicant directly by the bank.

Disbursement in stages

44

Usually, loans are disbursed on the basis of the stage of construction of the property. So, in case

of resale or ready possession properties, the disbursement is full and final. However, in case of

under-construction properties, the payment is made in parts, also known as part-disbursement.

Each option would have different disbursement processes.

1. Part disbursement: When a loan is partly disbursed, the bank does not start EMIs

immediately, since it is calculated on the total loan amount at a particular rate of interest and for

a given tenure. Moreover, it normally does not start breaking up the installments into its

principal and interest components until the entire loan amount is disbursed.

To overcome this difficulty, banks charge simple interest on the partly disbursed loan amount.

For instance, if applicant have a sanctioned loan of Rs10 lakh, but the property is under

construction and the bank has disbursed only Rs4 lakh, applicant will be charged a simple

interest only on the disbursed amount. This process continues until the final disbursement takes

place. The simple interest paid is called Pre-EMI interest or PEMI.

At this stage, banks may take only around three to six post-dated cheques on account of PEMI.

2. Full and final disbursement: If it is a ready-possession property, the bank disburses the

entire loan amount in favor of either the reseller or the builder.

Post Disbursement Relationship

The final disbursement does not end applicant’s relationship with the bank. In fact, it is just the

beginning. And there are various issues / situations that arise in between the beginning of the

relationship and its end.

These include:

oPayment Receipt

oRepayment

o Income tax certificate

45

oPrepayment

oLoan preclosure/satisfaction

Payment receipt :

Once the bank hands over the pay order to applicant, applicant in turn are expected to hand it

over to the reseller or the builder. Applicant should get a receipt from them for the payment and

hand it back to the bank, as it will become part of applicant’s mortgage documentation.

Share certificates: In case applicant’s property is part of a society, applicant will need to get the

flat transferred to applicant’s name by asking the society to issue the share certificate in

applicant’s name and recording the transfer of ownership in their books. This normally happens

at the first AGM/EGM after the sale transaction. This transferred share certificate also happens

to be a part of the mortgage documentation and has, therefore, to be handed over to the bank

after the transfer takes place.

Repayment:

The loan is generally repaid by equated monthly installments, using post-dated cheques. Banks

usually ask for 12, 24 or 36 PDCs, after which applicant need to repeat the process until

applicant have repaid the loan. Some banks may also insist on a cheque for an amount equivalent

to the loan outstanding at the end of PDC period to ensure timely replenishment of PDCs for the

next 12, 24 or 36 months as the case may be.

In case applicant’s installments are to be deducted against applicant’s salary, applicant needs a

letter from applicant’s employer accepting this arrangement and directly remitting the amount to

the bank every month. This is possible only if applicant’s organisation has an arrangement with

the bank for all employees.

46

Some banks allow applicant to give standing instructions to the bank where applicant have

applicant’s savings/current account to deduct money each month crediting applicant’s home loan

account.

Another possible mode of payment is by cash or demand draft (not all banks offer this).

Applicant can deposit the EMI every month at the bank's office.

Income Tax certificate:

Every bank issues an income tax certificate that serves as requisite proof to let applicant avail of

tax benefits that accrue on repayment of a home loan. This will typically contain the total

amount of interest and capital repaid during the year. This is mandatory to claim the tax benefit

in respect of self-occupied property. Applicant will have to file this with applicant’s tax returns

and submit this to applicant’s employer or chartered accountant to calculate applicant’s tax

liability.

Prepayment

Applicant can prepay a loan either in part or in full at any given point of time. Applicant can also

prepay it even when it is only partly disbursed. However, most banks have an upper limit on the

number of times a person can prepay his loan in a year as well as on the minimum amount

applicant can prepay each time. Until recently, banks charged a penalty for part or full

prepayment. But increased competition has forced most banks to allow partial prepayment at nil

charge. Most banks levy a prepayment charge if applicant make full repayment and ask for

release of applicant’s property documents.

Loan pre-closure- satisfaction

Applicant also has the option of completely repaying the loan at any time. Of course, each bank

has its conditions for preclosure. Also, the loan will get completely paid off on the expiry of the

tenure of the loan if applicant has paid all installments on time.

47

Once applicant has completely repaid his/her loan, ensure that the entire set of original property

documents is handed back to applicant. Applicant should also ask the bank for a No-Objection

Certificate saying the account has been cleared. As an option, the bank may issue a consent letter

stating that the property is now free from mortgage.

If applicant has guarantors, the bank will issue a separate letter for each of the guarantors stating

that their liability has come to an end. Only after applicant receive these documents can applicant

say that the property is now completely free of mortgage.

At this stage, in some cases, applicant may discover that the original documents have yet not

been received by the bank from the registrar. In such cases, applicant will need to follow up with

the registrar and get the documents from them directly by showing them a copy of the bank's

clearance certificate.

Sometimes (and we must stress only sometimes) the bank may misplace applicant’s original

property documents leading to avoidable stress. In fact, the bank may claim that these documents

were never given to them at all. Hence the importance of insisting on a proper receipt of title

documents while handing them over to the bank.

Remember that receipt will come in very useful when the loan is fully paid off. Also, it is

extremely useful when applicant want to shift applicant’s loan to a new lender.

48

49

9. Home Loan in ICICI Housing Finance

Products in ICICI Housing Finance

ICICI Bank Home loans provide not just the most competitive interest rates & best level of

service, but also products designed to cater to the specific needs of consumer. Home Loans are

provided to individuals to own a residential property

Land Loans

Land loans give an opportunity for individual customer to purchase a residential plot of land to

do self- construction. Thus, customer can invest now in a plot of land & build in future. The

Land loan can be financed only within municipal limits of HUB locations or in case of direct

allotment outside municipal limits by DA.

Land Loan can be availed by Resident Indian whether Salaried or Self-Employed and also by

Non- Resident Indian.

Home Improvement Loans

Home Improvement Loan is offered to facilitate improvement of a self-owned dwelling unit to

existing or new customer. HIL considers a range of facilities internal or external to the structure

without increase in the living pace. Thus, a customer can add or improve facilities to his

dwelling unit with a loan at Home Equity Loan rate of interest. Home Improvement Loan can be

availed by Resident Indian whether salaried or Self-Employed.

Office Premises Loans

Office Premises Loan can be used for purchase, construction, extension & also for improvement

(at the time of acquisition of office premises. It creates an opportunity to extend loans to self-

employed individuals to house their profession or business giving a permanent address for

50

generating steady flow of income. The product can also include the estimate of renovation at the

time of purchase of the property. This loan is especially meant for self-employed professionals

like Doctors, Architects etc.

Home Loans can be availed by Resident Indian who is Self-Employed and also by Non-

Resident Indian who are Salaried.

EMI under Construction

EMI under Construction is offered for structuring a home loan to enable individuals to

commence his EMI in a partly disbursed under construction project. Commencement of EMI

ensures re-payment towards principal amount leading to savings in interest and faster repayment

of the loan. The EMI paid is as per the sanctioned loan amount and remains constant during the

tenure of the loan. The tenure of the loan keeps moving up with additional amount being

disbursed.

EMI under Construction can be availed by Resident Indian whether Salaried or Self-Employed

and also by Non- Resident Indian.

Balance Transfer

Balance Transfer is a facility offering the customer a choice to transfer the outstanding balance

of the loan availed for better terms & conditions. Balance Transfer helps to move from higher

rate of interest to lower rate of interest or increase in loan component as Top up. BT is possible

only from loans taken from HFCs approved by NHB for refinance, Banks or employer Loans

taken from Central or State Government. Balance Transfer can be availed by Resident Indian

whether salaried or Self-Employed

MoneySaver

Money Saver account is a home loan account with transaction facility. The account holder can

deposit & withdraw to the extent of balance maintained. On the commencement of EMI the

interest will be calculated on the outstanding debit balance. Thus, the home loan account holder

51

maintaining large balance in the Money Saver account can save on the interest paid by faster

repayment. This means one can pay less & repay loan faster.

This product can be offered only in case of first and final disbursement – Part disbursement cases

cannot be offered this product. MoneySaver would be available at Floating Rates only & Fixed

EMI per lac per month would be applicable. IT certificate in the case of MoneySaver is not

issued. Money Saver can be availed by Resident Indian whether salaried or Self-Employed

Top Up Loan

Top Up Loan can be availed time and again for various personal requirement based on value of

the property. It offers the customer additional funds against the security of the same property. To

avail Top Up loan, the vintage of at least six months is required for the loan availed. The basic

eligibility emerges with good repayment track record. The end use letter is essential to be

collected.

The End use of Top Up Loans can be

Furnishing of home

Consumer durable

Child’s education

Daughter’s marriage

Family holiday

Vehicle

Any other personal requirement of the borrower provided it is not speculative or illegal in nature.

This product is applicable to fully disbursed cases with no post- disbursement document

pending. This product is priced more than base home loan rates but lower than any personal loan

rates. Top Up Loan can be availed by Resident Indian whether Salaried or Self-Employed.

Loan on Phone

52

Loan On Phone is a pre-sanctioned loan. Its is based on the existing relationship of the customer

with ICICI Bank. The biggest advantage is that the customer can get the loan with minimum

documentation. Good banking transactions and repayment records becomes a strength for

availing loans in future. Loan on Phone can be availed by Resident Indian whether salaried or

Self-Employed

Home Equity Loan

Loan against property gives the owner of residential or commercial premises to leverage on the

value of the property. It offers the ability to unlock funds gives the advantage of looking at the

asset as a source of security bringing liquidity and retaining ownership. In case of HEL the

property should be self occupied by one of income considered applicants. The security of the

property ensures competitive rate of interest. The interest component of the EMI paid by SEP /

SENP can be booked as expenses in their P & L

Home Equity Loans are provided for many personal requirements of the customer viz. –

Marriage

Child Education

Business

Purchase of Property (Where mortgage is not possible)

Improvement of Property

Medical Treatment

Home Equity Loans can be availed by Resident Indian who is Self-Employed and also by Non-

Resident Indian who are Salaried.

Property Overdraft

The overdraft facility from ICICI Bank Home Loans allows you to borrow money against your

self-occupied property. The overdraft facility comes with a multi-city cheque book and phone

banking facility. The customer is charged interest only for the amount that he withdraws from

53

the account. Whenever he deposits funds into the account, they go towards reducing the

outstanding balance in the account.

It offers the following benefits:-

Generating capital against property (R) or ( C) for business or personal use

Convenience of Pre - Sanctioned limit and draw as you need

Pay interest on the amount drawn and for days utilized

Convenience of depositing & withdrawing like any Current Account

Benefit of Cheque Book & Phone banking

Fast Processing and door-step service

Multi-city cheque book and phone banking facility

Property Overdraft can be availed by Resident Indian who is Self-Employed

Lease Rental Discounting

Lease Rental Discounting helps to raise funds against the future expected rentals of self owned

commercial property. The property should be occupied by the Lessee. Similar to Home Equity

Loans, LRD can be provided for any personal requirements of the customer viz. –

Marriage

Child Education

Business

Purchase of Property (Where mortgage is not possible)

Improvement of Property

Medical Treatment

54

Lease Rental Discounting can be availed by Resident Indian whether salaried or Self-Employed

55

Eligibility Norms for Home Loans

Home Loans can be availed by Resident Indian whether salaried or Self-Employed and also by

Non- Resident Indian who are Salaried. For resident Indians the following are the eligibility

norms

One must be at least 21 years of age when the loan is sanctioned.

The loan must terminate before or when one turns 65 years of age or before retirement,

whichever is earlier.

One must be employed or self-employed with a regular source of income

Factors affecting Home Loan Amount

ICICI Housing Finance provides home loan suited as per client’s needs. The home loan amount

depends on client’s repayment capability and is restricted to a maximum of 85% of the cost of

the property or the cost of construction as applicable. Repayment capacity takes into

consideration factors such as income, age, qualifications, number of dependants, spouse's

income, assets, liabilities, stability, continuity of occupation and savings history.

However, there are ways by which clients can enhance their eligibility

If client’s spouse is earning, put him/her as a co-applicant. The additional income shall be

included to enhance loan amount. Incidentally, if there are any co-owners they must

necessarily be co-applicants.

Fiancée's income can also be considered for sanctioning the loan on combined income.

The disbursement of the loan, however, will be done only after the proof of marriage is

submission.

Providing additional security like bonds, fixed deposits and LIC policies may also help to

enhance eligibility.

56

While there is no need for a guarantor, it could be that having one might enhance credibility. If

so, loan officer would provide clients with the necessary details.

The final amount to be sanctioned will depend on your repayment capacity. However, what you

ultimately are entitled to will have to conform within the limits fixed for each loan.

Also, when the company looks at the total cost, registration charges, transfer charges and stamp

duty costs are included.

Home Loan Interest Rates for Resident Indians

With varied offering of house loans and home finance, ICICI Housing Finance gives an

opportunity to select the perfect home loan as per needs of clients. Clients are availed with-

Adjustable Rate Home Loan

Fixed Rate Home Loan

Combination of the above two

Step Up Repayment Facility (SURF)

SURF is a variant to enhance the eligibility of a young professionally qualified home loan

customer with out increasing monthly outflow as EMI. The structuring considers a notional

percentage increase in income & offers options of graded increase in EMI over the tenure of the

loan contracted.

The tenure is divided in three parts

Primary being lowest EMI

Secondary

Tertiary being highest EMI

57

The following are the features of SURF

Higher eligibility of loan amount with lower EMI

Graded increase in EMI considering future increase in Income

Suited for young professionals.

SURF can be availed by Resident Indian whether Salaried or Self-Employed Professionals.

Flexible Installment Plan (FLIP)

FLIP is a variant for structuring enhanced eligibility of home loan applicants with varying tenure

of income source. This repayment facility is given when income is going to reduce after certain

time during the loan tenure due to one of the borrowers retiring before loan maturity. The EMI

payable becomes affordable based on individual income source and also matching the family

cash flow. This variant is offered typically to family members joining as applicants like husband

& wife or father & son with varying tenure of service Period / Age norm.

FLIP has the following features

FLIP considers income of two applicants and offers step down repayment facility

One of the applicants should have service period till the end of the tenure of the loan

FLIP would have two different EMIs during the tenure of the loan

Normally the first EMI would be based on the combined income

The second EMI would be smaller & based on the lower income with longer tenure of the

applicant

FLIP can be availed by Resident Indian whether salaried or Self-Employed and also by Non-

Resident Indian who is Salaried.

Part Fixed, Part Floating

58

A product that offers the dual benefit of fixed rate loans as well as floating rate loans. With this

product, a customer can book part of his loan under a fixed rate plan and the other part under a

floating rate plan. Thus, he can minimize the impact of any adverse changes in the interest rate

regimes and at the same time, avail of any benefits that may come by way of favorable changes.

Part Fixed, Part Floating can be availed by Resident Indian whether salaried or Self-Employed

and also by Non- Resident Indian who is Salaried.

SmartFix Home Loans

3 years fixed and floating rate thereafter. A product that offers the safety of fixed rates plus the

advantages of floating rates. The Smart Fix enables the customer to lock at fixed rate of interest

today with the contract to move to a floating rate on a subsequent date. For the first 3 years you

get a fixed interest rate. From the fourth year, your loan gets switched to the prevailing floating

interest rate. Thus, a customer gets an opportunity to observe the interest rate movement over a

period of time and expects to benefit in the bargain

Smart Fix can be availed by Resident Indian whether salaried or Self-Employed.

The interest rate on ICICI Bank Home Loans is linked to the ICICI Bank Floating Reference

Rate (FRR)/PLR. As per earlier communication, FRR/PLR was increased by 0.75 % on June

30th 2008. Subsequent to this change, as per recent announcement, the FRR/PLR has been

further increased by 0.75% effective from July 31st 2008. The FRR has gone up from 13.50% to

14.25% & PLR has gone up from 15.50% to 16.25%. For all the Adjustable Rate Home Loan

customers, both the above changes will be effective from July 31st 2008.

Insurance Plans for your Home Loan

Introducing exclusive Home Insurance plans, that can provide cover to your Home loan in the

face of any unforeseen event happening to your life. In case of any of these happenings, your

family will have the support of the insurance cover to pay for the outstanding Home loan,

without being burdened by the loan EMI's.

59

ICICI Housing Finance presents “HomeSafePlus“& “HomeAssure/HealthAssure“ two exclusive

and innovative insurance plans to insure your Home Loan.

HomeSafePlus –

Insurance cover for HomeSafePlus provided by ICICI Lombard General Insurance Company.

Key Benefits of HomeSafePlus

No medical checkup

Comprehensive insurance plan for individual, home and its contents

Single premium long-term insurance plan

Premium paid for the Critical Illness cover is eligible for tax benefits u/s 80D of the

Income Tax Act

Sum Insured remains constant throughout the policy period (loan O/S amount to come to

bank, rest goes to individual)

Multiple applicants can be covered under the same loan

Simple application form

HomeAssure/HealthAssure -

Insurance cover for HomeAssure/HealthAssure provided by ICICI Prudential Life Insurance

Company.

Key Benefits of HomeAssure/HealthAssure

Life Cover from HomeAssure for the entire home loan tenure

Critical Illness cover from life threatening illnesses like cancer, coronary artery bypass,

heart attack, kidney failure, stroke, major organ transplant

Special non-medical limits only for ICICI Bank Home Loans customers

60

Dual benefit to customers, Life Cover from HomeAssure and Critical Illness Cover from

HealthAssure

Dual tax benefits, Section 80C benefits under HomeAssure, Section 80D benefits under

HealthAssure

Simplified claim procedure

61

Home Assure Premium Chart: Premium as a % of the Loan amount

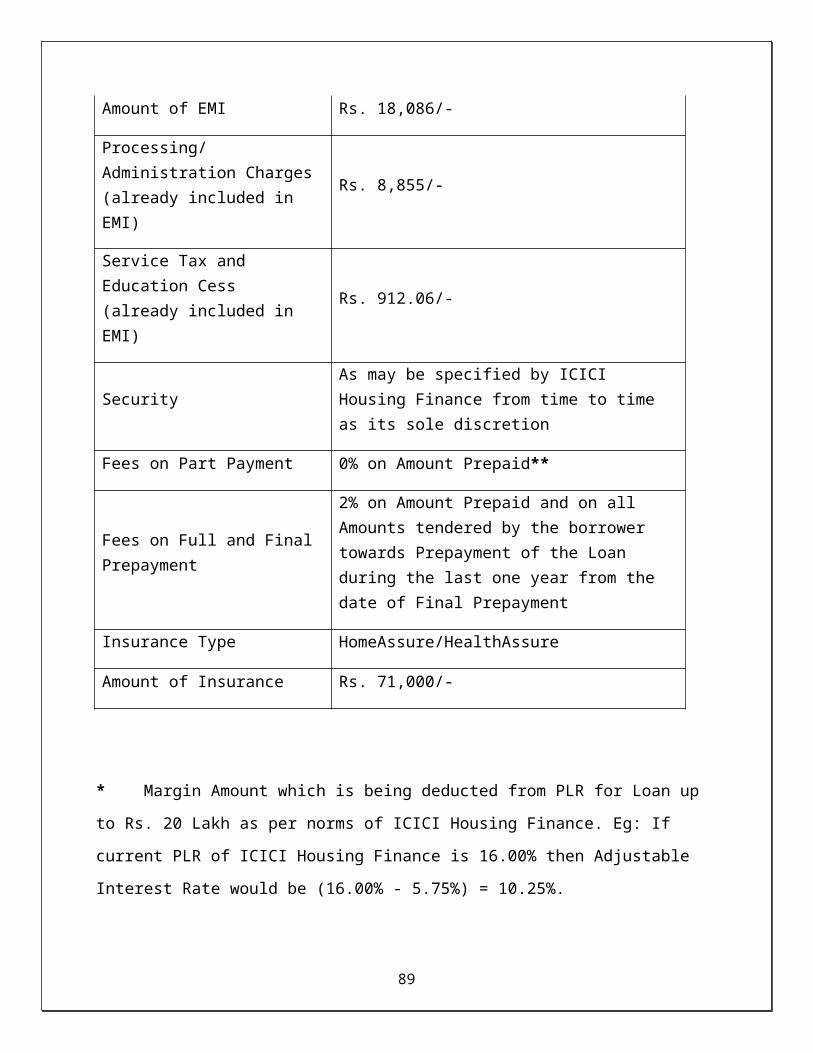

Table 8. 1

Age/Term 2 3 4 5 6 7 8 9 10 11

18-30 0.381 0.484 0.589 0.695 0.802 0.91 1.023 1.136 1.254 1.364

31-35 0.421 0.545 0.673 0.805 0.944 1.088 1.239 1.396 1.559 1.715

36-40 0.547 0.719 0.899 1.086 1.283 1.49 1.708 1.939 2.185 2.424

41-45 0.752 1.002 1.269 1.554 1.861 2.188 2.538 2.913 3.313 3.701

46-50 1.163 1.567 2.002 2.468 2.969 3.504 4.074 4.681 5.324 5.941

51-55 1.82 2.465 3.153 3.882 4.66 5.489 6.375 7.326 8.346 9.341

56-60 2.709 3.692 4.76 5.92 7.18 8.541 10.004 11.585 13.302 14.996

Age/Term 12 13 14 15 16 17 18 19 20 21

18-30 1.488 1.614 1.746 1.882 2.022 2.167 2.319 2.476 2.641 2.813

31-35 1.89 2.072 2.264 2.465 2.677 2.99 3.135 3.384 3.646 3.922

36-40 2.694 2.983 3.289 3.612 3.955 4.318 4.701 5.104 5.527 5.969

41-45 4.146 4.617 5.114 5.638 6.189 6.768 7.378 8.019 8.694 9.409

46-50 6.646 7.392 8.182 9.021 9.912 10.857 11.855 12.911 14.034 15.228

51-55 10.49 11.715 13.022 14.422 15.926 17.545 19.285 21.156 NA NA

56-60 16.988 19.158 21.517 NA NA NA NA NA NA NA

Age/Term 22 23 24 25 26 27 28 29 30

18-30 2.994 3.184 3.383 3.592 3.812 4.042 4.284 4.536 4.798

31-35 4.213 4.513 4.839 5.174 5.524 5.888 6.269 6.666 7.081

36-40 6.433 6.917 7.426 7.959 8.518 9.105 9.718 10.359 11.032

41-45 10.159 10.949 11.78 12.654 13.578 14.556 15.589 16.68 NA

46-50 16.501 17.856 19.298 NA NA NA NA NA NA

62

Home Loan Process at ICICI Housing Finance

First of all individual who is interested in taking Home Loan, is provided with all information

regarding different products of ICICI Housing Finance. He/She is given information regarding

general norms of availing the facility of Home Loan.

1. If client is interested and eligible for getting Home Loan, He/She is

asked to submit all the required documents.

2. File of all necessary documents of client is getting sourced by the

Back-Office people and Client ID is given to the file of client.

3. If any document is remaining to be submitted then, query is

conveyed to the client. Client is asked to submit the remaining

documents so that the file can be moved ahead.

4. Team of officials called “Risk Containing Unit” (RCU)

properly verifies the documents given by the client and if there is

any query, it is communicated to the Back Office people.

63

5. Property for which Loan is taken is properly identified by the

Professional Evaluation Team of the ICICI Housing Finance. There

are two types of property evaluation conducted by the Professional

Evaluation Team mentioned below..

1) Technical Evaluation- Eg: Layout plan, Building premises etc.

2) Resale (Legal) Evaluation- Eg: Legality of documents of

previous owner, legality of property etc.

6. Afterwards credibility of client is verified by “Credit Processing