· Web viewCritical Success Factors of Empowerment Financing for BEE companies in South...

72

Critical Success Factors of Empowerment Financing for BEE companies in South Africa Coach: Desray Clark Research Project submitted by Syndicate 2 Oscar Siziba Gabisile Ngwenya Ivan McClean

Transcript of · Web viewCritical Success Factors of Empowerment Financing for BEE companies in South...

Critical Success Factors of Empowerment

Financing for BEE companies in South

Africa

Coach: Desray Clark

Research Project submitted by

Syndicate 2

Oscar Siziba

Gabisile Ngwenya

Ivan McClean

Matheri Kangethe

Vanitha Padayachee

TABLE OF CONTENTS

EXECUTIVE SUMMARY........................................................................................................................................................... 4

1. INTRODUCTION............................................................................................................................................................ 5

2. PURPOSE AND BENEFITS OF STUDY............................................................................................................................... 6

2.1 PROBLEM STATEMENT................................................................................................................................................................6

2 .2 OBJECTIVES OF THE INVESTIGATION /PROJECT RATIONALE................................................................................................................6

3. DEVELOPING THE FACT BASE (LITERATURE REVIEW).....................................................................................................8

3.1 MERGERS & ACQUISITIONS.........................................................................................................................................................8

3.2 COMMERCIAL BANKS IMPERATIVE IN COST EFFECTIVELY FUNDING BEE EQUITY TRANSACTIONS................................................................10

3.3 CREDIT RISK MITIGANTS...........................................................................................................................................................11

3.4 BEE FUNDING MODELS............................................................................................................................................................12

3.5 CURRENT BEE EQUITY ACQUISITION LANDSCAPE............................................................................................................................15

3.6 CONCLUSION.......................................................................................................................................................................... 17

4. METHODOLOGY/DATA COLLECTION........................................................................................................................... 19

4.1 RESEARCH METHOD AND ITS UNDERLYING CHARACTERISTICS.............................................................................................................19

4.2 DATA COLLECTION................................................................................................................................................................... 19

5. STUDY FINDINGS........................................................................................................................................................ 21

5.1 COMMERCIAL BANKS............................................................................................................................................................21

5.2 BEE COMPANIES.....................................................................................................................................................................24

5.3 COMPARISON BETWEEN BANKS AND BEE PARTNERS RESPONSES.......................................................................................................26

6. CONCLUSIONS............................................................................................................................................................ 28

7. RECOMMENDATIONS................................................................................................................................................. 28

8. REFERENCES............................................................................................................................................................... 30

APPENDIX 1 - DEFINITION OF TERMS& ASSUMPTIONS......................................................................................................... 33

DEFINITION OF TERMS....................................................................................................................................................................33

ASSUMPTIONS.............................................................................................................................................................................. 34

2

APPENDIX 2 – INTERVIEWEES............................................................................................................................................... 35

APPENDIX 3 – QUESTIONNAIRES.......................................................................................................................................... 36

INTERVIEW QUESTIONS FOR BEE COMPANIES.........................................................................................................................36

NTERVIEW QUESTIONS FOR BANKS..........................................................................................................................................38

APPENDIX 4 – INTERNATIONAL PERSPECTIVES ON EQUITY POLICIES BASED ON NETHERLANDS& KENYA VISITS....................41

NETHERLANDS.............................................................................................................................................................................. 41

Immigrants...........................................................................................................................................................................41

Gender Diversity...................................................................................................................................................................42

KENYA.........................................................................................................................................................................................43

APPENDIX 5 – HISTORY OF NETHERLANDS, KENYA SOUTH AFRICA &SWOT ANALYSIS.............................................................1

EXECUTIVE SUMMARY

BEE funding has become a very topical issue for the South African government because the

country must find ways to reduce the entrenched inequality of incomes, economic opportunities,

and access to services, left over from the years of apartheid. There is a political imperative that

the major financial institutions help redress the historically inadequate system of banking services

for the lower income market.

In recent years commercial banks in South Africa have experienced margin shrinkage, mainly as

a result of pursuing aggressive growth through new business acquisition and competition from

foreign banks. These trends and Government pressure have forced commercial banks to pay

attention to the BEE markets.

The objective of this project was to determine the critical success factors for empowerment

finance for BEE companies from the perspective of commercial banks and BEE companies. The

findings have shown that there are common themes that both BEE and Banks find to be critical in

the sustainability of BEE transactions. Among other themes, the top four were: funding costs;

quality and experience of BEE management; dividend flow and profitability of the business. The

recommendations to address these critical factors are then outlined and that if adopted would

benefit both Banks and BEE companies in overcoming current challenges associated with

funding of BEE transactions.

3

Also, this research report is expected to directly benefit commercial banks by assisting them to

understand and acquire sustainable BEE deals, thereby enhancing bank’s profitability. It should

also benefit BEE companies by assisting them in developing long term relationships with their

banks, evaluate empowerment opportunities, resulting in better service packages that meet their

business needs. The research included an international perspective comparison which was

gained by visits to Netherlands and Kenya. The countries swot analysis can be found in the

appendix.

The research was conducted as part of the Bankseta International Executive Development

Programme Europe/Kenya 2010.

4

1. INTRODUCTION

Severe limitations, historically placed on the economic activities of Black South Africans resulted

in suppressed entrepreneurship, inadequate skills to participate effectively in the economy,

limited capital accumulation, including property ownership (Mafuna, 2007).

This led to a highly marginalised and impoverished black population that cannot participate in the

economy in any meaningful way, presenting risks of possible social unrest, stagnant or declining

economic growth therefore threatening the country’s future. To mitigate these risks and ensure

blacks participate more meaningfully in the economy, Black Economic Empowerment (BEE)

policies were adopted by the newly democratic South African government (Kemp, 2008), to

facilitate a rapid and sustainable transfer of economic ownership to the black population.

Commercial banks, through financing transactions to buy stakes in companies, can play a pivotal

role in facilitating this ownership. With an average of 20 transactions per annum taking place in

key financial institutions, banks will be under continuous pressure to facilitate empowerment until

it succeeds (Lucas-Bull, 2007).

This document outlines empowerment transaction challenges, and proposes to understand the

problem through a determination of critical success factors from commercial banks and BEE

entities perspectives.

The next section of this document explains the purpose of the study, followed by a review of

literature on mergers and acquisitions, particularly BEE transactions, and thereafter examines

funding models linked to previous BEE transactions. Next is an international perspective on

empowerment experiences in Netherlands and Kenya followed by methodology applied in the

research, study findings and conclusions based on literature review and qualitative research

targeting banks, BEE companies, and BEE subject matter experts.

5

2. PURPOSE AND BENEFITS OF STUDY

This research report is expected to promote a rapid and sustainable transfer of economic

ownership to the black population through improved success level of BEE funding transactions. In

addition, commercial banks and BEE companies will both financially benefit from increased

successful transactions through effective models.

2.1 Problem Statement

The study poses three questions:

What are the critical success factors for empowerment finance for BEE companies from

the view of commercial banks?

What are the critical success factors for empowerment finance for BEE from the view of

BEE companies?

Are there any differences in the perception of critical success factors between commercial

banks and BEE companies?

2 .2 Objectives of the Investigation /Project Rationale

“Black entrepreneurs participating in BEE financing transactions borrow at unfavourable terms

and with deals remaining vulnerable to high interest rates and an economy experiencing slow

growth, ownership patterns of the economy will remain largely unchanged” (Butler, 2006). Should

the majority of the black population continue to be marginalized, the resulting social unrest would

bring disturbing consequences for businesses, and the wider social progress that is ultimately

dependent upon a flourishing private economy.

Competitive and cost effective access to finance is important and plays a decisive role in the

long-term survival of a company. Generally BEE companies initially rely on the owners to self

6

financing before seeking external funding, which may be in the form of debt and/or equity.

External source of funding available to BEE companies mainly depend on the development of

financial markets, regulatory financial environments and the ability of financial institutions to

access a, manage and price loans for BEE companies, based on Risk.

Equity, third party debt, and vendor financing are the basic models used to fund transactions

(Lucas-Bull, 2007). Equity finance requires companies or individuals to have capital (equity) to

purchase the required asset. This takes many forms such as issuing shares in the open market to

raise finance, share swap models used in mergers and acquisitions, or borrowing from investors

who in turn take up equity in the business. Third party finance is where a buyer is financed by a

third party such a bank to acquire as asset. The third party will cost the capital based on risk. This

form of finance may require a buyer to put up collateral or cede the asset to the financier until the

debt is fully paid. Vendor financing is where the owner of the asset provides finance to the buyer

to purchase the same asset. Typically vendor financing in empowerment deals is through

convertible instruments and equity derivatives.

Commercial banks role in these transactions may include purely third party financing, or

participating in a mix of debt, equity, or vendor financing.

The competitive nature of the banking industry in South Africa requires the local banks to focus

their resources in growing their markets, thereby enhancing their profitability. For commercial

banks to successfully penetrate the BEE market, they must understand the needs of BEE clients

in order to deliver appropriate products and services thereby enhancing customer value.

The success of this project in providing clear guidelines for banks in dealing with empowerment

finance for BEE companies will result in more BEE companies being funded and still remain

attractive, profitable and sustainable to both financial institutions and BEE companies. This will

further result in job creation through new opportunities created by BEE companies, wealth

creation through equity transfers, poverty alleviation and growth in the overall economy.

7

3. DEVELOPING THE FACT BASE (LITERATURE REVIEW)

Chapter one and two served to define the objectives, the importance of the study and the study

environment. It was also indicated that existing BEE M & A funding models have not been

effective in facilitating wealth creation in previously marginalised social groups and the need to

seek address the shortcomings. In this chapter, equity funding models, particularly those used in

BEE M & A transactions are investigated. A fact base on BEE equity transactions and their

performance is also developed.

To understand challenges faced by both BEE and Banks in facilitating BEE Mergers &

Acquisitions (M & A) transactions insights were drawn through extensive literature review of

previous research.

1.

3.1 Mergers & Acquisitions

Mergers and acquisitions continue to be a highly popular form of corporate development and

wealth creation. In 2004, 30,000 acquisitions were completed globally, equivalent to one

transaction every 18 minutes. The total value of these acquisitions was $1,900 billion, exceeding

the GDP of several large countries.

Walter and Barney (1990) completed a study to determine objectives of M & As which resulted in

five broad categories namely:

To obtain and exploit economies of scale

A mechanism to deal with inter-dependencies or leverage synergies

Expand current product lines or markets

Enter a new business

8

Maximise and utilise a firm’s financial capabilities

However, in a paradox to their popularity, acquisitions appear to provide at best a mixed

performance to the broad range of stakeholders involved. While target firm shareholders

generally enjoy positive short-term returns, investors in bidding firms frequently experience share

price underperformance in the months following acquisition, with negligible overall wealth gains

for portfolio holders (Agrawal and Jaffe, 2000). Internally managers of acquiring firms report that

only 56% of their acquisitions can be considered successful against the original objectives set for

them (Schoenberg, 2006). Meanwhile, target firm executives experience considerable stress and,

on average, almost 70% depart in the five years following completion (Krug and Aguilera, 2005).

The current South African context creates opportunities and incentives for white owned

companies to achieve objectives defined by Walter and Barney (1990) when black entities are

allowed to acquire ownership stakes. For the period since South Africa’s first democratic

elections in 1994, BEE with the aim to increase black ownership of companies and subsequently

create wealth for acquirers has been an important driver behind large M & A transactions in

South Africa (Ernst & Young 2010). Over the last five years, BEE has represented a constant

proportion ~20% of all South African M & A activity over the last five years (see table1). However

BEE activity was comparatively quiet during 2009, in line with the generally depressed M & A

conditions.

Figure1: BEE transaction contribution to overall transaction value (Rbn)

Source: Ernst and Young, Mergers and Acquisitions Report, 19th Edition – A review of activity in 2009.

9

The complex phenomenon which mergers and acquisitions represent has attracted the interest

and research attention of a broad range of management disciplines encompassing the financial,

strategic, behavioural, operational and cross-cultural aspects all present of this challenging and

high risk activity.

Ultimately for acquirers, BEE entities in this case, wealth creation through increased value of the

acquired stake which is greater than acquisition costs is fundamental. Hence the ability to cost

effectively fund the acquired stake and subsequent improved financial performance of the target

company due to entry of the BEE entity represents success.

3.2 Commercial Banks imperative in cost effectively funding BEE equity

transactions

The BBBEE has seven elements which make up the scorecard with which companies measure

themselves against in order to be classified as empowered or not. These seven elements are:

Equity Ownership; Management Control; Employment Equity; Skills Development; Preferential

Procurement; Enterprise Development and Residual Element (Fauconnier&Mathur-Helm, 2008).

This research project addresses equity transfer and the role commercial banks have incost

effectively funding these acquisitions

The challenge faced by the South African banking sector is how to assist with the transformation

of the economy to ensure sustainability while achieving short term profitability objectives. In the

current South African context, where the economy’s transformation is necessary for a sustainable

South Africa, a growing black middle class presents massive opportunities. With legislated BEE

targets, it’s in the Banks best interest to seek solutions leading to successful BEE equity funding

transactions. To fund BEE equity commercial banks face a myriad of risks, which have to be

managed effectively. According to Gunnion (2005), financing remains one of the main limitations

of empowerment transactions and given the past inequalities in South Africa resulting in black

people having no equity to support the lending, no security to offer, poor credit records, and

limited training and skills (Schoombie, 2000), the challenge to banks is significant.

10

3.3 Credit Risk Mitigants

Credit risk management primarily focuses on loss avoidance and the optimisation of return on

risk. The identification of credit risk mitigants is important as it provides South African

commercial banks with insight on how to optimally structure BEE transactions. It further provides

guidelines on adopting these mitigants and thereby increasing their success rate in lending to

BEE companies. At present, this is still seen as a higher risk option mainly because the

underlying risk is not clearly understood.

Banks consider the following issues when the credit risk inherent in a single business is assessed

(Bluhm, Overbeck& Wagner, 2003):

Default probability: What is the likelihood that the business will default on its repayment

over the term of the facility?

Exposure at default: In the event of a default, how large will the outstanding exposure be?

Recovery rate: In the event of a default, what fraction of the exposure may be recovered

through bankruptcy proceedings or through some other form of settlement?

The five C’s are considered the fundamentals of successful lending:

Character refers to the borrower’s reputation and the borrower’s willingness to settle debt

obligations. In evaluating character, the borrower’s honesty, integrity and trustworthiness

are assessed. (Koch & MacDonald, 2003).

Capacity refers to the business’s ability to generate sufficient cash to repay the debt.

Capital refers to the owner’s level of investment in the business (Sinkey, 2002).

Collateral (also called security) is the asset/s that the borrower pledges to the bank to

mitigate the bank’s risk in event of default (Sinkey, 2002).

Conditions are external circumstances that could affect the borrower’s ability to repay the

amount financed.

In order to mitigate adverse selection, financial institutions subject the potential transaction to

financial and non-financial criteria. Some of the non financial factors that are considered before

entering into the transaction include the skills and expertise of the management team, the track

record, the barriers to competition, growth of potential market, the nature of the competition,

stage of company development and the uniqueness of product or service. Financial factors

11

considered when appraising a BEE deal include existing debt, cash flow and age of business.

According to Meyer (2005), credit risk can be mitigated in lending to BEE companies by the

following:

Indemnity schemes providing collateral, e.g. Khula.

Providing of finance to allow a black person to take up a small shareholding and as the business performs, to increase shareholding and finance.

Establishing a proper mentorship programme and to have accredited mentors for skills transfer.

The potential for experienced retired executives to mentor BEE companies.

Partnership between the bank and the BEE company, where the bank takes an equity stake in the company.

Franchising was also deemed a risk mitigant. The franchisor provides training, assists in compiling the business plan and monitoring the business on a daily bases.

Meyer, 2005 concluded that it is evident that commercial banks currently use generic credit

policies. Although guidelines exist in lending to BEE companies; these have not yet been

incorporated into the bank’s credit policy. It is noticeable that banks need to be more involved in

this than just the lending; it needs to a total solution for the BEE company.

3.4 BEE Funding Models

Bank finance is the primary source of debt funding. Commercial banks extend credit to different

types of borrowers for many diverse purposes. A number of BEE deals involve the use of hybrid

funding mechanisms, including vendor finance, debt finance and equity investment.

The 1st wave of BEE transactions was characterised by a funding model which used the creation

of a SPV’s (Special Purpose Vehicle) to facilitate the acquiring of debt in exchange for

preference shares from the seller company to be used as security for the financier/commercial

bank funding the transaction. This arrangement was necessary because black people due to

historical reasons already detailed in Chapter1 in this report do not have the cash or the assets to

back such capital intensive transactions without the assistance of a financier. For such structures

to work high reliance is put on the performance of the share price or dividend flow resulting in a

12

highly geared structure. In theory, this works for as long as the dividend flow or the share price

appreciates at a rate higher than the funding and the capital costs of obtaining the shares,

however if share prices depreciate, transactions fail. This was the case with one of the first

notable black empowerment deal on the JSE which occurred in 1993 when New Africa

Investment Limited (NAIL) and Sanlam through Metropolitan Life, its subsidiary, pioneered the

first sizable transfer of equity and control from a wholly white owned company to black

shareholders. JSE listed companies’ shares prices declined sharply in mid-1998 due to the Asian

crisis resulting in some BEE companies including NAIL trading at a discount to net asset value.

NAIL’s share price fell from 800 cents to just below 400 cents by the end of September 1998

(Ngwenya, 2007).

In 1998 Legae Securities released research findings indicating that SPV’s financing structures

were responsible for over 50% of the black ownership on the JSE, and that an estimated 63% of

BEE ownership on the JSE would revert to financiers as the black companies were being

decimated by the markets and could no longer rely on the share price to fund their debt. The

financiers were relentless, with profits of as much as 90% of BEE companies accruing to them.

NAIL announced that it would un-bundle in late 1999 and, control of the company would flow

back into white institutional investors (Ngwenya, 2007). Other BEE companies simply collapsed

and were liquidated or de-listed.

In recent BEE transactions, there has been a realisation of the vulnerability of highly geared

structures and as a result there has been some creative thinking around how to reduce this

burden on the new black shareholders. One of these ways is the use of options. This results in a

less geared structure in that it is not an outright purchase of shares but rather an option so the

debt required from a financier/bank is less than the total notional amount of buying the shares.

The concern with this structure is that actual ownership does not transfer to black shareholders

until the end of the lock-up period when the option is exercised. The risk inherent with this

structure is the possibility of the share price to be below the strike (the price agreed upon at the

time of the deal) at the time of exercising the option which will leave the option with no value and

the black shareholders out of pocket as the funding costs/premium of the option will still have to

be settled with the financier. The Bidvest BEE deal struck with Dinatla (the BEE Consortium) in

2003 is an example. Dinatla bought a call option to purchase 15% of Bidvest at a maximum of

R60 a share. By December 2006, R2.7 billion of this debt would be due. Realising that it did not

13

have the funds to pay this debt, Dinatla announced in September 2006 that it would sell 18 million

(40%) of its 45 million shares back to Bidvest at a 30% discount to market price in order to fund

the debt (Ngwenya, 2007). This still left Dinatla with debt relating to the equity purchase of at

least R1.3 billion, for which financing was raised through Investec as part of the sale of shares

back to Bidvest. This means that Dinatla started out with a potential 15% of Bidvest, while three

years later funding forced a reduction of this stake to 9%. Should Dinatla be unable to pay

Investec in the future, more equity will possibly be given up. It thus becomes clear that Dinatla’s

final unencumbered stake will be considerably lower than the 15% quoted at the onset of the deal

in 2003 (Ngwenya, 2007). Jenny Cargill (2010) called this phenomenon the realisation principle

where the BEE partner ends up with a reduced percentage share at the end of the lock-up period.

Cargill emphasises that this consequence is not good for the Seller either as the Seller ends up

scoring less on the BEE scorecard on ownership due to now reduced BEE shareholding.

A different variation of this Option structure was used by ABSA when it concluded its deal with

BathoBonke (BEE Consortium) in 2004. BathoBonke bought an American option which could be

exercised at anytime after 2 July 2007 with the strike between R48 to R69 for the 5 year deal. At

the time of exercising the option, BathoBonke managed to only convert/purchase 5.1% of ABSA’s

ordinary shares as opposed to the potential 10% share conversion had they exercised the share

option on 1 September 2007 (Ernst & Young, 2010) when the ABSA share peaked for that period.

The disadvantage with this structure is the inability to know when the share will be at its peak.

This is always known in retrospect often once the opportunity has been missed.

So whist the deal was struck at 10% transfer of ownership, it was shown that 5 years later the

actual ownership transfer was only 5.1%.

The more recent BEE deal which seems to have created value for the BEE shareholders was the

Goldfields and Mvelaphanda which was entered into in 2004. The structure was also that of a call

option with exercise only at the end of the lock-in period. At the time of exercising the option, the

share price had appreciated by 33.1% from R89.31 to R118.90 (Ernest and Young, 2010).

Assuming that the funding costs were below 33%, this deal would create value for the BEE

partners. It should be noted that even with the creation of value in this type of structure, the BEE

shareholders were still at the mercy of the markets. The structure still depended on the share

price of Goldfields being higher at the end of the lock-in period than the time at which the deal

was struck. So indeed this structure also depends on the Bull market for it to work.

14

Based on the examples presented above, structures that are dependent on the appreciation of

the share price or the dividend flows in order to pay off the debt are unsustainable as markets are

cyclical in nature and with a downturn, it is inevitable for such structures to fail.

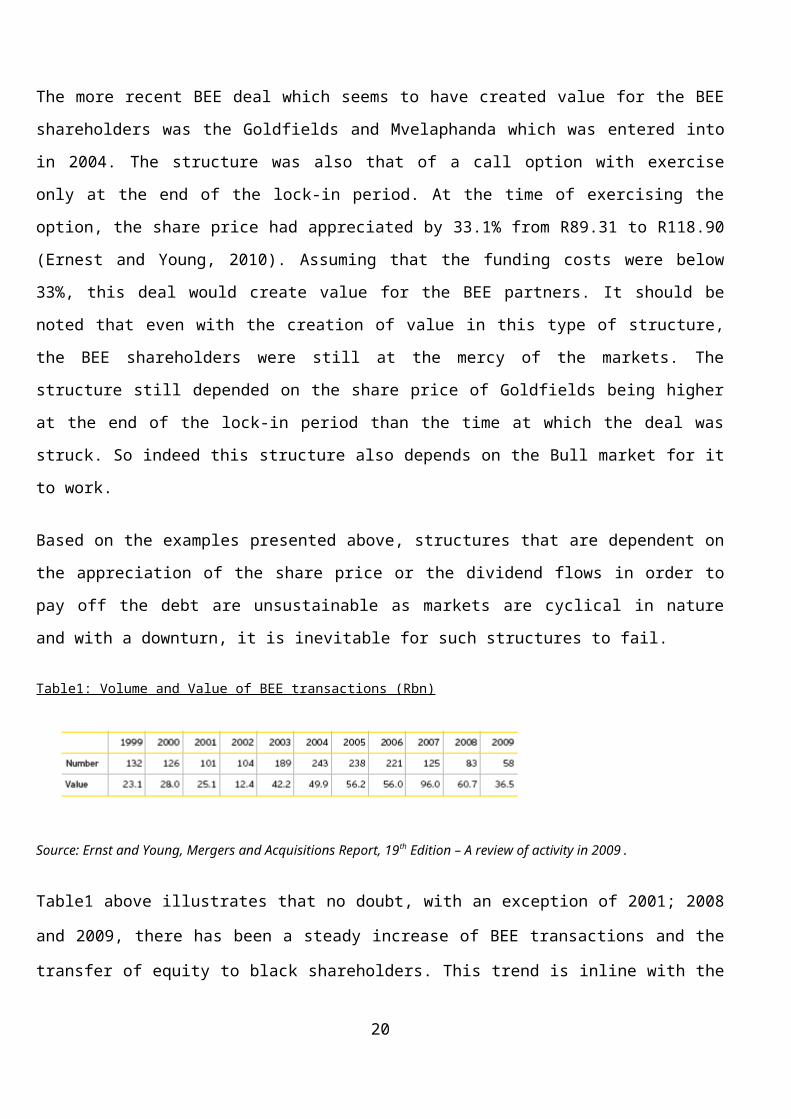

Table1: Volume and Value of BEE transactions (Rbn)

Source: Ernst and Young, Mergers and Acquisitions Report, 19th Edition – A review of activity in 2009.

Table1 above illustrates that no doubt, with an exception of 2001; 2008 and 2009, there has been

a steady increase of BEE transactions and the transfer of equity to black shareholders. This trend

is inline with the sentiment from private business that BEE is an imperative to the success and

stability of the democratic South Africa (KPMG BEE Survey, 2009), however, the question

becomes, is the acquisition of such equity a success or failure when it is measured against the

objectives of the BBBEE Act of 2003 which is that of distributing the wealth of the South African

economy to the broader base of the previously disadvantage population.

3.5 Current BEE equity acquisition landscape

According to President Jacob Zuma at the opening address to the inaugural meeting of the

President's Broad-Based Black Economic Empowerment (BBBEE) council in 4 February 2010,

the percentage of black-owned companies registered at the Johannesburg Stock Exchange is

disappointingly low. In a parliamentary committee briefing in 2009, Philisiwe Buthelezi, chief

executive of the National Empowerment Fund (NEF), said that there was an upward movement of

impairments reported in development finance institutions and the private banking sector linked to

BEE companies. It was also reported that the sustainability of existing BEE deals has been hit by

the global credit crunch and cash flow positions of BEE companies have been at their weakest

since 2000 and this has had serious implications on issues such as loan repayments and loan

write-offs. In addition, debt to equity ratios has been at their highest and this affects how

companies pay for deals.

15

According to rating agency, Empowerdex, an estimated R41bn worth of BEE deals were

decimated in the past two years (Mabotja, 2009) due to un-conducive market conditions spawned

by the ongoing economic recession. Last year, (2008), empowerment deals sealed by JSE-listed

companies declined fivefold to R13bn, compared to R66bn the previous year. The slowdown in

the momentum of empowerment deal-making has prompted financial engineers to raise serious

concerns about the prospects of this important drive. Itumeleng Kgaboesele, CEO of Sphere,

holds the view that the Achilles’ heel for empowerment remains the funding mechanisms

employed in the acceleration and implementation of this drive.

BEE partners have traditionally relied on structured finance instruments that allow them to borrow

money to invest with little or no equity or collateral of their own. This historic landscape of BEE

deal making has yielded mixed results for third party funders and recipients of funds. Morne Van

Der Merwe, a senior director at Werksmans Attorney, a firm specialising in the construction of

empowerment funding models is of the view that many of the BEE deals struck in recent years

after painstaking negotiations may have to be renegotiated to ensure they do not fail (Mabotja,

2009).

Mining in particular faces significant challenges. Last year, (2009) the Industrial Development

Corporation (IDC) spent about R700m on redeeming the bank debts of BEE companies in the

mining industry whose loans had been called in by banks (Lange, 2010). On several occasions

the IDC had been asked to become shareholders in mining transactions where bank loans were

being called in.

The success of any modern economy is dependent on its ability to grow and sustain an

environment conducive for entrepreneurship to emerge and thrive. Entrepreneurs contribute to

economic growth and job creation through the establishment of new business. In South Africa,

the Task Group of the Policy Board for Financial Services and Regulation (2002) has recognised

the major contribution BEE deals make towards the socio-political stability of the country.

Subsequently, they have advocated for the government to create a framework that provides an

enabling environment in which BEE deals can flourish.

According to Fauconnier and Mathur-Helm (2008), there is an increased effort on ensuring

genuine and sustainable broad based BEE in South Africa, essentially to implement suitable

funding structures that are not superficial fronting arrangements. Fauconnier and Mathur-Helm

16

(2008) further suggest that many BEE transactions have failed since inception due to complex,

elaborate and unsustainable funding structures, which include the use of hybrid funding

instruments, debt finance, vendor finance and equity finance. Successfully implemented BEE

transactions have similarities when scrutinising their funding structures which included the use of

SPV’s, mezzanine funding, issuing of preference shares, vendor finance, use of dividend income

to service the debt of the BEE investor and sustainable cash flows.

The BEE stakeholders including the company sellers of such stakes have realised the

vulnerability of such funding structures as those described above. Such funding structures do not

advance the BEE agenda instead when they fail, the stake either gets bought back by the white

previous owners or the financiers take over the shares ceded as security for the funding and

structuring costs associated with the transaction.

3.6 Conclusion

Generally, BEE lending is perceived to be high risk and this research focuses on lending models

that can be applied by commercial banks in the lending decision when equity investments are

considered for BEE classified companies. Banks are the custodians of a nation’s savings and

cannot afford to make poor lending decisions as it has a direct impact on multiple stakeholders.

This research outlines empowerment transaction challenges, and proposes to understand the

problem through a determination of critical success factors from commercial banks and BEE

entities perspectives. This will promote a rapid and sustainable transfer of economic ownership to

the black population through improved success level of BEE funding transactions. In addition,

commercial banks and BEE companies will both financially benefit from increased successful

transactions through effective models.

In light of the above, it is an imperative to determine critical success factors for BEE Funding

models in order to ensure the success of BEE. This research project embarked on this to provide

a set of factors that answer this question.

The success or failure of a BEE deal goes back to inception of the business concept, more

specifically in the structuring of the deal. The challenge in structuring a BEE deal usually lies in

overcoming a number of problems associated with the lack of funding, the integrity, track record

17

and leadership skills of management and the possibility for high returns and an exit. With all this

in mind, it is not easy to forget that the relevant industry regulators are becoming more focused

on ensuring sustainable, genuine broad based empowerment.

The research includes the investigation of credit policies that are being applied by commercial

banks in South Africa when financing BEE transactions and the credit assessment models

applied by these commercial banks when assessing BEE funding. On completion of the

investigation on the credit policies and credit assessment models, a set of credit risk mitigants will

be identified that can be applied in order to improve the success and sustainability of these BEE

transactions.

This research project attempted to expand on the current Literature by carrying out research work

to determine the critical success factors for BEE funding models and provide recommendations.

18

4. METHODOLOGY/DATA COLLECTION

This chapter describes the methodology that was followed to test the propositions suggested in

the preceding chapter. Leedy and Ormrod (2005) noted that in addition to a researcher choosing

a workable research problem, the following needs to be considered: the types of data to be

analysed relating to the problem; and the means of collecting and interpreting these data. The

chapter starts off with a description of the chosen method and its implications for this research.

This is followed by descriptions of the processes that were used in data collection, analysis and

interpretation.

3

4.1 Research method and its underlying characteristics

A qualitative research methodology was applied in this research specifically, the descriptive

survey was used. According to Leedy and Ormrod (2005) this research problem lends itself well

to qualitative research. Another reason for not doing quantitative research is that commercial

banks have different reasons and take on BEE funding approaches, mostly due to their unique

strategies and therefore benchmarks are likely to differ significantly among banks, the same will

apply to BEE clients.

4.2 Data collection

Data was collected through face-to-face interviews. The critical incidence technique was used in

developing the semi-structured questionnaires that were used to guide the interviews. Face to

face interviews were conducted with the major banks which are prominent in the funding of BEE

equity acquisition transactions in South Africa. Additionally, BEE companies were interviewed to

determine their perspective. The aim was to understand the challenges faced by the industry and

19

success achieved in these transactions in order to establish the current views of what is critical

for a BEE transaction to be successful for both the banks and companies.

The material gathered for the purpose of this research was transcribed and coded as per themes

that emerged from analysis. The data was then subjected to content analysis, to identify certain

themes that emerged from the data. A summary of results is presented in tabular form in section

5 (see tables 2 and 3). The following steps were followed in conducting the content analysis

The coding procedure to evaluate the critical success factors was a frequency count of

how many times these factors were mentioned by the respondents.

The characteristics were combined and presented in detailed tables contained in Section 5

(table 4)

A description of patterns that the data reflects is then presented in the section of the

research where interpretation of data is set out.

20

5. STUDY FINDINGS

2.

3.

4

5.1 Commercial Banks

The interview process with financial institutions revealed certain common trends as well as

marked differences on Individual responses.

Banks do not as general rule apply different credit policies to BEE transactions. They are viewed

as a subset of the overall “Merger and Acquisition” credit policies. Where the M&A activities are

on smaller unlisted companies, the evaluation differs dramatically from listed companies where

each transaction is independently evaluated.

Although listed companies were discussed, the focuses of our interviews were on the unlisted or

private companies. Subsequent findings from the interviews unless specifically noted will refer to

private companies.

The size of transactions involved varies from R5 million to R400 million with the overall exposure

being limited per institution depending on institutional risk appetite (these figures were not

divulged).

Volumes of BEE transactions have tapered down over the past 2 years with figures ranging from

10 to 20 deals in 2010. Of these deals the banks agree that the majority of the deals are

approved with FNB putting the figure at around 95%.

21

The following key elements are considered in the due diligence process for funding (not

exhaustive)

Financials – Who are the Auditors of the Audited Financials – these have to be reputable

Cash-flows – Business has to pass the solvency test over the tenure of the deal

Consistency – There has to be consistency in the income statement figures over the

years, no escalated growth patterns in the year of the sale for instance

Sales & Purchase agreement has to be in place and must make sense

Financial Forecast and Cash Flow stress testing.

As equity finance is riskier than debt funding, BEE transactions are considered riskier by the

bank. In general, it was found that 100 % funding was requested as BEE companies did not have

collateral to offer. In light of this equity funding is not attractive to Banks as holding regulatory

capital is too expensive for Banks. For every R1 lent out, the Banks are expected to hold R1 as

capital for these equity deals.

Default rates and failure of BEE deals are reported as low by the banks. A number of the deals

are restructured when the cash flows are inadequate to cover the debt. The actual success of the

BEE partner servicing the debt against the original agreement is not reflected by the banks. It

does however appear as if the banks are more willing to look at restructuring finance for BEE

deals.

The most preferred funding model used by the banks is the ‘NewCo structure’, often called a

section 34 structure. In this structure the BEE partner is buying into the business. The Target

Company and the BEE come together and agree to form a new company called NewCo. The

Bank then lends to this NewCo. The Credit evaluation is purely based on the cash flows of this

NewCo. Bank leverages/optimises the balance sheet of the NewCo.

When asked to rank the most important aspects which we determined from the literature review,

the banks ranked the following in order of importance for consideration on credit granting as

depicted in the table below.(Each participant ranked factors from 1 to 8, with points allocated

accordingly. The ranks were then totalled with minimum total score indicating most important,

minimum of 4 and max of 32)

22

Table 2: Summary of Banks Rank order of critical success factors as determined from Literature

Critical success factors from Literature reviewRank Order Score

· Quality and experience of BEE management 1 12

· Profitability of target entity 2 14

· Pricing (funding costs) 3 17

· Security 4 18

· Dividend flow 5 18

· Mutual benefit 6 19

· Value creation 7 23

· Share price 8 31

The most valuable finding from the interview process is indicated in the response to the following

question: What do you consider as must have’s in approving a BEE deal with your BEE client?

The individual responses varied, but a clear theme was emerging:

There must be a willing buyer and a willing seller.

The expectations of the BEE partner and the Seller must be aligned.

The culture of the organisation and the BEE partners must be conducive. (the trust and

culture blend).

The BEE partner must not be paying an inflated value for the share.

The new partners must add value to the company (BEE must not just be an asset swap).

Outgoing management must be committed to the success of the transaction.

23

There must be an honest an open partnership. The notion of BEE as a get rich quick as

the silent partner is almost a certainty to failure.

More should be done to facilitate BEE transactions. The role banks play is limited and that

BEE partners need assistance in:

• Company valuation (paying a fair price).

• Enterprise development

• Contractual legalities

• Mentorship

5.2 BEE Companies

Interviews with companies brought to the fore the preferred funding models, the impact of the

financial crisis and the latest deals brought on to their books. Covered also were the problems

that impede BEE deals.

In general, it was found that 100% funding was requested as BEE companies did not have

collateral to offer. First problem is that Banks take 100% downside risk but BEE legislation

requires that upside benefits be shared with the BEE partner, a ratio of 49 to 51. Since Banks got

the short end of the stick in the early 2000’s for this structure, they no longer fund 100% debt.

Banks now fund eg: 80% senior debt with 20% equity stakes into these deals. This leads to the

problem of capital requirements for equity deals being more expensive than normal or senior debt

and is expected to get even more expensive with the implementation of Basel 2. Currently for

every R1 that is lent out, the bank has to keep R1 in capital. To date, the Reserve Bank is not

relaxing these capital requirements. One Bank revealed that numerous attempts to apply for

concessions to the Reserve Bank to reduce this capital requirement for BEE equity deals have

been made in the past and have all been rejected. The Reserve Bank is of the view that Banks

are deposit takers and should protect depositors’ money and not gamble with injecting it into

equity deals. In light of this, BEE equity funding is not attractive to Banks.

A problem which was also highlighted in our literature review was lengthy lock-in periods, this

does not allow the BEE partner to exit when profitable to do so, this results in an artificial market

24

where shareholders cannot exercise economic gain which leaves BEE partners cash flow

constrained for years and not allowing opportunity for growth or acquisition of other assets.

More recently funding structures require what is termed “unencumbered equity portion”. This is

the partner’s contribution that has not been borrowed in any shape or form but really is his own

funds. Model is doomed as few BEE partners have the cash to do this.

Another finding has been the applying of account sweeping facilities by Banks to service debt

leaving the BEE partners with no cash flow to survive and unable to buy into other economic

opportunities. Banks still resort to account sweeping of cash even when covenant has been met.

Three of the four Banks interviewed confirmed that sweeping of accounts is applied even after

covenant has been met.

All the interviewees agreed that for the country, it is essential that BEE be successful. There is a

general sense that not enough is being done to facilitate these transactions and that NGO’s, DTI

and business partners need to take a more active role in achieving this.

When asked to rank the most important aspects which we determined from the literature review,

the respondent’s from BEE companies interviewed ranked the following in order of importance

for consideration on credit granting as depicted in the table below. (Each participant ranked

factors from 1 to 8, with points allocated accordingly. The ranks were then totalled with minimum

total score indicating most important, minimum of 4 and max of 32)

Table 3: Summary of BEE respondents Rank order of critical success factors as determined from Literature

Critical success factors from Literature reviewRank Order Score

· Profitability of target entity 1 7

· Dividend flow 2 10

· Pricing (funding costs) 3 11

· Value creation 4 19

· Mutual benefit 5 20

25

· Security 6 21

· Quality and Experience of BEE management 7 26

· Share price 8 30

A final sentiment from the interviews on the way forward – Only Education will resolve the issue

of wealth distribution and enterprise development. Government must create an environment for

these to flourish. Banks or BEE will not solve this. (These sentiments are echoed in Trick or Treat

by Jenny Cargill 2010)

5.3 Comparison between Banks and BEE partners responses

As can be seen by the tables in this section,(tables 2 and 3) there is a disparity between what the

banks rank as most important and the BEE respondents rank as most important.

There are areas where the companies and the banks are aligned. What appears in the top four of

both lists is Profitability and Pricing. These 2 key variables will form the basis for any common

ground. That BEE companies do not see “Quality and experience of Management” as important,

is a misnomer as they themselves believe that they have the ability to add a positive contribution

to the future growth of the company. As such we can say that 3 of the top 4 factors between BEE

respondents and banks are aligned. Dividend Flow also ranks highly on BEE and in top 4 overall.

This alignment is more apparent if we sum the scores of both respondents and then rank order

the result. (see highlighted yellow)

Table 4: Collation of Banks and BEE summaries of critical success factors as determined by literature

Critical success factors from Literarure reviewRank Order Score

Profitability of target entity 1 21

Pricing (Funding Costs) 2 28

26

Dividend flow 3 28

Quality and experience of BEE management 4 38

Security 5 39

Mutual benefit 6 39

Value creation 7 42

Share price 8 61

It is now clear that the top 4 success factors as indicated in table 4 must be in place for there to

be any meaningful basis of funding by the banks and acceptance thereof by the BEE partner.

Share price on both rankings is last as the interviewees focus was biased towards non listed

companies.

27

6. CONCLUSIONS

Based on the research findings, of the eight critical success factors, four: namely pricing

(funding costs), quality and management experience of BEE partners, profitability and

dividend flow linked to the target entity were viewed as the most critical by both banks and

BEE companies.

7. RECOMMENDATIONS

Below are the recommendations that could be adopted by the Banking industry; the BEE

companies and other stakeholders involved in BEE transactions. If implemented, this could go

a long way in improving the sustainability of BEE transactions through such funding models.

The role of Government in reducing BEE funding costs (pricing)

The research findings have shown that 100% debt funding or equity funding of BEE

transactions by commercial Banks is unsustainable due to high regulatory capital that banks

need to hold for such equity deals which then results in very high funding costs. This funding

model is not optimal for both banks and BEE companies. Government can play a role in terms

of offering guarantees to commercial banks for BEE transactions for the equity portion of the

transaction. The presence of this guarantee will enable the banks to fund 100% of these deals

without assuming 100% of the risk. The risk could be shared 70-30% between the bank and

the government respectively. This will allow the banks to classify this guaranteed portion of

debt as senior debt instead of equity hence reducing the capital requirement to 10%. This will

result in cheaper funding of these BEE transactions thus ensuring sustainability of the

transaction and the survival of the BEE company.

Quality and management experience of BEE partners

The findings have shown that both Banks and BEE companies place a lot of importance

on the quality of management in BEE transactions. Funding models should incorporate

operational involvement of BEE partners as one of the CP’s (condition precedence) to

28

ensure that the BEE partners understands the industry and that skills transfer and capacity

building takes place. Another CP could be to introduce a lock-in period for the outgoing

Dividend Flow

Both the Banks and BEE companies rated dividend flow as critical as it generates the cash

flow needed to service the debt. The findings have shown that Banks apply sweeping of

accounts i.e. all cash flow available go into servicing the debt. It is recommended that

Banks should allow portion of dividend back into the BEE business for growth – no

sweeping should be applied to BEE companies once covenant is met. Allow a percentage

of the dividend back into the business instead of the entire dividend going to service debt.

This will allow growth for the BEE partner to get involved in other economic activities or

invest back into the business. Banks need to play a collaborative role in this model.

Sustainable Profitability of the business is crucial

It is of utmost importance for banks and BEE companies to ensure that the target company

is a viable going concern that can generate profits even after acquisition by the BEE

partners. BEE partners should ensure that valuations are not overstated in order not to

over-pay. This also increases prospects for healthy dividend flow that can be applied to

acquisition debt-repayment and re-investments.

If the above recommendations are considered, the probability of success in BEE funding

by commercial banks will increase, causing more transactions. In addition, the government

objectives of sustainable wealth creation amongst the black population and general

economic growth will be achieved.

6

29

8. REFERENCES

Agrawal, A., and Jaffe, J. (2000). ‘The post merger performance puzzle’, Advances in

Mergers and Acquisitions, 1, pp. 119-156.

Bluhm, C.,Overbeck, L., and Wagner, C. (2003).An Introduction to Credit Risk Modelling.

New York: CRC Press Company.

Cargill, J., (2010), Trick or Treat: Rethinking Black Economic Empowerment, Jacana

Media (Pty) Ltd.

Chweya, L., (2006): Paper Presented at the ‘Mijadala on Social Policy, Governance and

Development in Kenya’ sponsored by Development Policy Management Forum on 26

October 2006 at Holiday Inn, Nairobi.

De Lange, J. (2010). IDC spent R700m on BEE debt. Fin 24 (Online).

http://www.fin24.com/Companies/IDC-spent-R700m-on-BEE-debt-20100204

Ernst & Young. (2010).Mergers and Acquisitions: A Review of Activity for the year 2009,

19th Edition, Transaction Advisory services.

Fauconnier, A.,&Mathur-Helm, B. (2008).Black economic empowerment in South Africa

mining industry: A case study of Exxaxo Limited. University of Stellenbosch Business

School, September 2008.

Gunnion S. (2005). A new look at empowerment, Real Business in Business Day. 22-02-

2005:1

Kemp, K. (2008). Implementation of Black Economic Empowerment in South Africa’s

Economy. In A. Muhamed, J. Muliru, A. Corradi and T. Davis (eds). An Exercise in World

Making 2008. Netherlands: Institute of Social Studies, 157 – 163.

30

Koch T. W., &MacDonald, S. (2003).Bank Management, 5th edition. Ohio: South-Western

Thompson Learning.

KPMG, (2009). Are We There, Yet? 2009 BEE Survey.2009 KPMG Services (Proprietary)

Limited.

Krug, J., and Aguilera, R. (2005). ‘Top management team turnover in mergers and

acquisitions’, Advances in Mergers and Acquisitions, 4, pp. 121-149.

Leedy, P.D., andOrmrod, J.E. (2005).Practical Research: Planning and Design, Seventh

Edition, Upper Saddle River: Merrill Prentice Hall.

Lucas-Bull, W. (2007). From Politics to Business. In Mangcu, X., G. Marcus, K. Shubane

and A. Hadland (eds). Visions of Black Economic Empowerment. Johannesburg: Jacana

Press, 132-146.

Mafuna, E. (2007). From Politics to Business. In Mangcu, X., G. Marcus, K. Shubane and

A. Hadland (eds). Visions of Black Economic Empowerment. Johannesburg: Jacana

Press, 31-37.

Meyer, P.G., (2005): The determination of credit risk mitigation in lending to Black

Economic Empowerment (BEE) companies, from a banker’s perspective. Graduate School

of Business Leadership; University of South Africa, November 2005.

Ngwenya, F.S.(2007). Success and Failures of BBBEE – A critical Assessment. MBA

Thesis:Stellenbocsh University, December 2007.

Schoenberg, R. (2006). ‘Measuring the performance of corporate acquisitions: An

Empirical Comparison of Alternative Metrics’, British Journal of Management.

31

Schoombie A. (2000). Banking for the poor: The success and failures of South African

Banks, in Poverty, Prosperity and Progress, Wellington, New Zealand, November 17-12,

2001. http://www.devnet.org.nz/pdf

Sinkey J.F. (2002).Commercial Bank Financial Management in the Financial-Services

Industry, 6th edition. New Jersey: Prentice Hall.

Statistics SA, (2010). 1st quarter published results of Statistics SA,

2010http://www.statssa.gov.za/publications/statskeyfindings.asp?PPN=P0441&SCH=4661

Walter,G.A., and Barney, J.A. (1990). 'Management objectives in mergers and

acquisitions', Strategic Management Journal, 11, 1990, pp. 79-86.

32

APPENDICES

APPENDIX 1 - DEFINITION OF TERMS& ASSUMPTIONS

Definition of terms

The following definitions are relevant to this research:

BEE – as defined in the Broad-Based Black Economic Empowerment legislation means

the economic empowerment of all black people, including women, workers, youth, people

with disabilities and people living in rural areas, through diverse but integrated socio-

economic strategies.

BEE Transaction - all transactions for the acquisition, by black people, of direct ownership

in an existing or new entity (other than an SME) in the financial or any other sector of the

economy; and joint ventures with, debt financing of or other form of credit extension to,

and equity investments in BEE companies (other than SMEs).

BEE companies – all Black empowered/influenced/women-empowered companies

Empowerment Finance - means the provision of finance for or investment in Targeted

investments and BEE transactions. The focus of this research will be on BEE Transactions

only.

Financial Institutions - means banks, long -term insurers, short -term insurers, re-

insurers, managers of formal collective investment schemes in securities, investment

managers and other entities that manage funds on behalf of the public, including

retirement funds and members of any exchange licensed to trade equities or financial

instruments in this country and entities listed as part of the financial index of a licensed

exchange. Any other institution in the financial sector, including licensed exchanges, may

opt in.

33

Commercial Banks– are defined as commercial or merchant banks that sell banking services

and products to large corporate (companies). They provide services and products such

overdrafts, medium term loans, long-term loans, debtor finance, treasury products such as letters

of credit, cash management products, corporate

Assumptions

The following were the assumptions made :

All referral to Legislation/Statutory Acts and the Financial Sector Charter (FSC) refer to

the currently available versions at the time of publishing the final report.

Interviewees are knowledge experts in their own fields simply by their title and the position

they assume in their organisations.

34

APPENDIX 2 – INTERVIEWEES

Bank Respondent's Name Designation

First National Bank-Commercial Banking Sipho Mdanda Leverage Finance - Senior Debt Lending

Nedbank Business Banking Bridgette Ryders Senior Debt Provision-Special Assets

ABSA - Commercial Banking Peter Swart Head of Credit

SBSA: Corporate and Investment Banking David Redwick Head of Strategic Finance and Acquisitions

SBSA: Corporate and Investment Banking Mohale Masithela Head of BEE

Industry Expert Respondent's Name Designation

BEE specialist Jenny CargillAuthor of Trick or Treat, Investment Advisor on BEE

Assistant Professor on Diversity Dr Betina Szkudlarek University of Rotterdam

Equity Funding Expert Sandile Hlope Director of BEE, KPMG

M&A Expert Dave Thayser Director of M&A, Ernest & Young

BEE Company Respondent's Name Designation

Thebe Resources Mpilo Shelembe CEO

Indigo African Legend Mashude Tshivase Executive Chairman

Vito Retailers Group Brian Skosana CEO

Euromatic Plastop (PTY) Ltd Garl Wolman Financial Director

35

APPENDIX 3 – QUESTIONNAIRES

INTERVIEW QUESTIONS FOR BEE COMPANIES

36

37

Interview schedule to be used for BEE companies

SECTION A COMPANY DETAILS:

Name of the Company:

Physical address

Nature of business/industry (SIC)

No. of Employees:

Company Turn-over

Respondent’s designation:

Company’s Main Bankers:

Other Bankers:

SECTION B: Incident Description – Specific transaction

concluded

We would like to discuss your BEE transaction – can you give us a

brief overview of your business and an explanation summarising

the details of the deal?

What insights can you share with us about the funding structure of

the deal?

Please explain what role the Bank played in the funding structure of

the deal

Were there any challenges associated with the funding structure of

this deal?

What were the critical criteria this deal had to meet in order to get

credit approval from the Bank?

What were the critical criteria for your company to consider this deal

successful?

Were there any issues that you believe might have been overlooked

in achieving the optimum funding structure for this deal?

INTERVIEW QUESTIONS FOR BANKS

Interview schedule to be used

A COMPANY DETAILS:

1. Name of the Bank:

38

2. Physical address

3. Respondent’s designation:

4. Respondent’s Role:

5. No of BEE deals in 2010:

SECTION B: General

6. What Credit Policy is applied to BEE funding?

7. How often do you receive BEE funding/credit applications?

8. How many of these get approved?

9. What are the key elements you look for when conducting a due

diligence exercise for BEE deals?

10.Drawing from your experience, how do BEE transactions risk profile

compare to other similar transactions?

11.What percentage of your NPL makes up BEE transactions?

12.What funding models or mechanisms are prevalent in your bank for

funding BEE transactions?

13.What do you consider as critical (must haves) in approving a BEE

deal with your BEE client?

SECTION C: Specific

14. Can you share some insights into the latest deal you have

approved?

39

15. Do you consider the following to be critical (must haves) for bank to

secure a BEE deal (the list will not be made available to the client to

avoid influencing the respondent’s response in the above question).

Ranking to be used.

Profitability

Value creation and mutual benefit

Value creation

Share price

Dividend flow

Security

Pricing

Quality and Experience of BEE management

16. In your opinion, what attracts BEE companies to your Bank?

17. Have you recently lost a BEE transaction to your competitor, and if

so why?

In your opinion, what needs to change for BEE deals to be sustainable

and mutually beneficial to the bank and customer?

40

41

APPENDIX 4 – INTERNATIONAL PERSPECTIVES ON EQUITY

POLICIES BASED ON NETHERLANDS& KENYA VISITS

Netherlands and Kenya have attempted to implement equity policies with varying degrees of

success:

NetherlandsIn a South African context, BEE policy is aimed at broadening the economic base of the country;

stimulating further economic growth, creating employment and enhancing the economic

participation of Black people (South Africa. Info, 2008 & DTI, 2006). Since its implementation the

program has become legislation, demanding companies to comply. BEE is supposed to provide

equal chances to all, and improve the living conditions of all South Africans. (Afrique du Sud,

2010).

Netherlands is faced with the challenge of diversity, predominantly, discrimination against

immigrants and gender diversity.

Immigrants

The following are our findings after discussions with Dr.Betina Szkudlarek, assistant professor at

the Erasmus University in Rotterdam

In the mid-1960s, most migrant workers entered the Netherlands from the southern and eastern

Mediterranean countries, notably Morocco and Turkey. A few years later, the Dutch government

formalized the recruitment practices by bilateral agreements with the sending countries. The

Dutch and the sending societies and the migrants themselves expected this migration to be

temporary.

In fact, most labourers from southern Europe (Italy, Spain and Greece) returned to their home

countries after a couple years of work in the Dutch industry. However, during the 1970s

Moroccan and Turkish migration shifted into more permanent settlement of these ‘guest workers’

and their families.

42

Although the Dutch authorities called for the recruitment to stop, immigration from Morocco and

Turkey continued in the 1970s in the form of family reunification and later in the 1980s onwards in

the form of family formation. As a result of large scale family reunification more female migrants

entered the Netherlands and as a consequence the sex ratio became gradually more balanced.

Now with second generation Moroccan and Turkish immigrants in the system there are issues

about acceptability into society. There is a distinct “separation” in society with immigrants being

referred to as “non-allentogs” and the ethnic Dutch population as “allentogs”. Further distinction is

evident in the residential areas of these groups; both groups live in different residential areas and

in their community. However on the positive side, businesses are now realizing the potential of

this market and are recruiting Moroccans and Turkish immigrants to service this market.

Gender Diversity

The following extract are conclusions from Mary van der Boon, who is principal of trans-cultural

management firm global tmc international, President of the European Professional Women’s

Network-Amsterdam and PhD candidate in Organisational Behaviour on the topic of Systemic

Bias in Organisations at Amsterdam Business School, University of Amsterdam.

Countless surveys and studies have come to the same conclusion: gender diversity in the

Netherlands, particularly the streaming of women to top positions in business, government and

universities, lags sorely behind other European countries. A common myth in the Netherlands is

that companies who appoint woman are taking more risks.

Corporations have to make the appointments and then back their (female) appointees all the way,

making it clear that no insubordination will be tolerated. There isn’t any visible mechanism

(process) that holds women back (perhaps only the resistance from middle management. This

group is nervously hanging onto their own positions, and won’t easily let women through). Top

managers will perhaps have to give women a helping hand by breaking through this resistance.

The concept of ’systemic bias’ is ingrained in every organisation. This occurs when certain

behaviours and characteristics ¬ often those of background, ethnicity, personality, gender, age; in

43

short, things over which people have no choice or control are encouraged and rewarded in an

organisation. The preference is very subtle, but extends from recruitment approaches (where is

the organisation looking for its new talent, for instance, and what kind of candidate applies?) to

promotion (who is placed on the fast track and in management development programmes, and

who is asked for key overseas jobs?) and leadership (what kind of diversity exists in the top

200?).

Most organisations unconsciously favour those who look, act and feel like the present leadership,

and they in turn are usually clones of the leaders before them. With senior management boards

of any organisation in the Netherlands there is virtually NO change over time. Down to the ties

they are wearing.

It is simplistic, therefore, to assume that the problem lies in a middle-management bottleneck.

The problem lies in engrained, hidden and very powerful bias inherent in every process in the

organisation. It takes incredible courage to undertake the change management initiatives

necessary to enact serious improvements in an organisation. Very few organisations have this

courage.

Kenya

Re-distribution of wealth in Kenya after colonial dominations did not evolve to create a broadly

empowered population but only benefited a few. The anti-colonial nationalist leaders and the

African population in general were in agreement about the colonial economic domination of the

African population, but differed on how to restore equity in the economic sphere once

independence was achieved (Chweya, 2006). The African population and a few leftist nationalists

like Bildad Kaggia expected redistribution of land in the former White Highlands as well as other

economic opportunities in the commercial, services, and manufacturing sectors in favour of the

poor and the “land-less”. But the right wing bulk of the KANU leadership like Jomo Kenyatta

seemed to favour redistribution to a new African bourgeoisie; that is, to individuals able to pay for

the land and other means of capitalist production that the colonial bourgeoisie had opened. New

African elite emerged through the process of Africanization of both the economy (land ownership,

commerce, industry) and state apparatuses including the bureaucracy thereby establishing a link

44

between state power, state resources and accumulation. In the end, Kenya adopted a system

that was neither free market nor socialist and the development of capitalism was halted except for

a few.

The departure of European participation in agrarian, commercial, and industrial activities left

behind a vacuum that called upon new local, indigenous elite to fill. While Africanization of

ownership of the means of production was effected rapidly, the emergent class of African elite

lacked the characteristics of the European elite, especially skills, capital, and relevant culture of

accumulation resulting in stalled development.

In addition, nationalization of the economy was undertaken through the establishment of public

enterprises as a framework for wealth creation and production. While public enterprises (PE)

served more purposes than just capital accumulation, the generation of wealth was crucial and

was not necessarily antagonistic to the fulfilment of the other goals of PE. However, public

enterprises failed to spearhead development because the state mixed non-capitalist

considerations with capitalist undertakings, especially political patronage. The state treated PE as

a source of cash for political operations and employment to favoured individuals.

Therefore the turn of independence did not result in the beginning of widespread wealth

redistribution and growth due to failed state policies that favoured the elite, while promoting

subsistence peasant production and petty entrepreneurship.

45

APPENDIX 5 – HISTORY OF NETHERLANDS, KENYA SOUTH AFRICA &SWOT ANALYSIS

The Netherlands Kenya South Africa

HISTORY The Netherlands has been historically been

made up of the Dutch population until the mid

60’s when the Dutch Government signed a

bilateral agreements with countries like

Morocco and Turkey to allow migrant workers

into the country. Some of these migrant

workers never went back to their original

countries and instead established permanent

homes and as a result, there has been a

second generation of non-indigenous Dutch

population which is making a significant size

(ca 20%) of the total Dutch population today.

This non-indigenous group has been

classified as the Multi-Cultural Group.

Because of the growing numbers in this

population group and hence the increased

economic activity in this segment, Marketers

and Financial Institutions alike have taken

note of the potential of this “emerging” market

segment as a new growth area for their

products. Certain Banks visited have

Kenya got her independence from

Colonial rule in 1963. They have since

had 3 democratic presidents with the

current parliament being made up of a

coalition government following a

contested election in December 2007

which resulted in a series of violence

attacks which left more than 800 people

dead. These series of violence sent a

shocking wave to the international

community which resulted in Kenya’s

GDP dropping to its lowest level in

history. Tourism which makes up 63%

of GDP dropped by .. as the

international community issued travel

warnings to Kenya. The economy is on

the recovery following a formation of a

coalition government after some

intervention from key international

figures like Kofi Anan. Kenya had a

referendum which introduced a new

South Africa’s 1st democratic elections were

held in 1994 following Nelson Mandela’s

release in 1990. Nelson Mandela was sworn

in as South Africa’s first democratically

elected President. Since European settlers

first arrived in South Africa with Jan van

Riebeeck on April 6 1652, the rights and the

wellbeing of the indigenous Black population

had been placed second to racial superiority

of the minority groups, first by the Dutch, then

by the British colonisation and then by

Apartheid under Afrikaner minority Rule.

Under Apartheid Government, racism was

institutionalized and put into law by the

enacting of various Acts aimed at

disenfranchising the Black majority

population. Amongst these was the Group

Areas Act No 41 of 1950 which divided urban

areas into racially segregated zones. Black

people were separated and prevented from

owning land or residing in designated ‘white’