View, Issue 15 — Designing your fiercest competitor: Mastering change by making it real

16

Issue 15 Cybersecurity Beyond the BRICS Interview with P&G’s Deb Henretta 24 34 46 Designing your fiercest competitor Mastering change by making it real page 12 view

Transcript of View, Issue 15 — Designing your fiercest competitor: Mastering change by making it real

Issue 15 Cybersecurity Beyond the BRICS

Interview with P&G’s Deb Henretta

24 34 46

Designing your fiercest competitorMastering change by making it real page 12

view

Designing your fiercest competitor Mastering change by making it real

Cover story

12 PwC View Issue 15

PwC View Issue 15 13

changed the mental model of the company: It would from now on be not only about what ran on the PC, but also the capabilities of the Internet and the tools (the Internet Explorer browser, for example) needed to fully exploit them. He was not going to let a new, fierce competitor take advantage of this technologi-cal and social trend—the Internet—and use it to beat his company.

At the time, Gates demonstrated vision, tenacity, and, ultimately, the ability to organize and execute—qualities that are even more important today. The world is more complex now than it was a decade ago. Things are changing faster because science is expanding and, most important, because feedback loops in technology, knowledge, and networks amplify learning.

Legend has it that in 1994, Bill Gates’ assistant, Steve Sonofsky, was visiting his alma mater, Cornell University. While there, he noted that Cornell was “taking full advantage of the fledgling Internet—email, course listings, international faculty collaborations, etc.—and fired off an email to his boss.”1 As a result, Gates became con-vinced that he needed to shift Microsoft’s focus toward the Internet—and fast. He sent out a long memo2 that stated that the Internet was taking off and that Microsoft would be a part of it.

Moreover, he wove this fundamental change into his story about the company. In particu-lar, he noted that the Internet was a natural extension of the desktop and part of the per-sonal computer domain. In other words, he

By John J. Sviokla and Adam J. Gutstein

John J. Sviokla is a Principal in PwC’s US Advisory practice where he serves as business leader for strategy and innovation. Principal Adam J. Gutstein is the management consulting leader in that practice.

So we won’t experience 100 years of progress in the 21st century— it will be more like 20,000 years of progress…. Ray Kurzweil

The speed of change is increasing at an alarming rate. Authors John J. Sviokla and Adam J. Gutstein argue that to prepare for accelerated change, companies need to look at five critical factors that they call the STEEP drivers: social, technological, environmental, economic, and political. Further, they maintain that management teams like yours can make these drivers of change “real” by asking leadership to “design a fiercest competitor” that could disrupt your industry. This manner of thinking and design sets the stage for actions management can take to benefit from, rather than be overwhelmed by, this rapidly changing environment.

1 http://www.cornell.edu/about/wired/.

2 This memo can be found at http://www.lettersofnote.com/2011/07/internet-tidal-wave.html.

14 PwC View Issue 15

For example, in 1990, the Human Genome Project was expected to last 15 years. However, because of advances in technology, the task was completed by 2003.3 Even the deepest experts did not understand how “the law of accelerating returns” (a phrase coined by Ray Kurzweil), which posits that “technological change is exponential,”4 works. They could not see how a combination of computer power, increased understanding, competitive access, and the knowledge network across

Figure 1: STEEP—A broad set of drivers with the potential to disrupt all industries the Steep drivers provide context In order to make sense of this accelerat-ing situation, we considered hundreds of trends, predictions, and forecasts, as well as their methods. We synthesized these forward-looking ideas into a model of five vital, interrelated drivers that we believe are the critical factors disrupting industries and recreating the lines of competition. (See Figure 1.) Understanding these core drivers and how they impact an organiza-tion is key to managing in this world of accelerating returns.

driver 1: SocialBy nature, people are social. Whether it is a friend who badmouths his car mechanic, or a distant cousin who helps get you that new job, the impact of social con-nections always has been the base upon

the Internet could make things happen much faster than expected.

In our view, in this world of faster change, it is time to examine the interlocking factors of social, technological, environmental, economic, and political change: STEEP drivers. Making these real is an exercise in creative destruction that involves a manage-ment team’s designing a fiercest competitor that could take advantage of these fast- moving trends for competitive gain.

3 http://www.ornl.gov/sci/techresources/Human_Genome/faq/faqs1.shtml.

4 http://www.kurzweilai.net/the-law-of-accelerating-returns.

Political

Social Technological

Environmental

Economic

STEEPDrivers

PwC View Issue 15 15

which commerce functions. Riding atop the Internet, social networks like Facebook and LinkedIn, or user-driven review sites like Yelp! and Rotten Tomatoes, have developed and taken hold at a phenomenal pace. As pundits have noted, by population, Facebook, created only eight years ago, would be the third-largest country in the world.5

Today, social networks not only offer extensive consumer information, but also provide an infrastructure capable of shaping society’s institutions—through self-organization, fundraising, and political action. In a business context, this means that social media is reshaping the micro context of a company’s brand and services, and the macro context of politics and regulation.

networks. This enables the firm to have a live, informed conversation with its audi-ence around the clock, throughout the year. If your firm does not perform this kind of monitoring and responsiveness, there may be conversations happening about you of which you are unaware, and lack of atten-tion can allow negative perceptions or even wrong claims to fester and grow.

Trust is a significant factor in this new world. Customers are more willing to trust a peer or customer review than a company’s claims about its product or service. Numerous websites and forums bear this out. However, today, a potent factor has been added to the equation. Social networks increase the ability of online shoppers to make use of multiple distribution channels and outlets, making

Affecting the micro domainRecently, a major airline discovered how the micro context of its brand could be af-fected by the impact of social networks. A well-known celebrity who had more than 1.4 million Twitter followers was using his account to complain about the service he received. He was updating his audience in real time about his feelings. Fortunately for the airline, representatives continually monitor social media in real time to discover what people are saying about the company. As a result, they were able to view conversa-tions and complaints and to respond almost immediately to the issue that this famous, disgruntled customer had with the airline.

Social media are completely integrated with the airline’s customer contact centers, from the phone, to the Web, to social

5 Dan Fletcher, “How Facebook Is Redefining Privacy,” May 20, 2010, at http://www.time.com/time/magazine/article/0,9171,1990798,00.html.

16 PwC View Issue 15

the influence of opinion that much more powerful. For example, a recent PwC study of more than 7,000 online users around the globe found that the vast majority— 86 percent—of survey respondents shop across at least two channels, and 25 percent are using four or five.6 In this process, they often turn to social media to help them make their choices.

How are companies taking advantage of these new social developments? The savvy ones are co-creating products and services with their customers. Sports apparel manu-facturer Nike offers one example. With the Nike+ system, a small, removable elec-tronic pod is a part of the insole of the shoe. This pod, which is the size of a quarter, sends results to a smart device and allows runners to track their own training, includ-ing distance and pace. This information is automatically uploaded to a website and runners can share their routes, routines, and comments easily and quickly. This

innovative product system, with its social overlay, differentiates the shoe.

Affecting the macro domainSince the commercialization of the Internet, the number of registered non-governmental organizations has grown from 1,250 to more than 45,000,7 and today, many of these ride atop the Internet. This means that the ability of special interest groups to organize, raise funds, and take action has become much easier. More than ever, businesses need to understand who is shaping the agenda for their companies and industries.

Part of the reason that social media has grown so quickly is the result of positive feedback. That is, the more that people use the medium, add reviews, or watch online videos, the more likely they are to find some-thing useful and come back. Coming back for something useful is not different. What is new is the permanency of the network and the increasing returns it creates in terms of

its value. In a network, positive feedback drives rapid adoption, a phenomenon that we expect to continue to grow.

driver 2: technologicalWe live in a wondrous and disconcerting age. Chances are your briefcase or pocket holds one of the latest waves of technologi-cal change. Based on cellular subscriptions, there are now more than 5 billion cell phones worldwide. Almost all new cars are connected to the Internet. The Internet of Things is adding everything from insulin pumps to light switches onto the grid. Big Data allow for the decoding of human ge-nomes and the ability of computers to beat humans at chess. And these examples are in no way comprehensive.8

Connecting everything means that firms increasingly need to compete not just on the quality of their physical value chain, but also on their ability to manage their information value chain. 7-Eleven® in Japan

1

2

3

4

5

6

7

01:10:29

09:22:31

12:08:32

16:43:0524:34:4330:23:1536:12:56

6 PwC, Customers take control: How the multi-channel shopper is changing the global retail landscape, December 2011.

7 http://www.apa.org/international/united-nations/publications.aspx.

8 The Internet of Things is “a new kind of network that will allow sensor-enabled physical objects—appliances in your home, products in a factory, cars in a city—to talk to one another, the same way people communicate over the Internet.” See Time’s “Best Inventions of 2008” at http://www.time.com/time/specials/packages/article/0,28804,1852747_1854195_1854158,00.html #ixzz1m0tJ9Ghn. “Big Data” refers to “massive amounts of data” that “are analyzed with massively parallel computers.” Read the full definition at http://www.pcmag.com/encyclopedia_term/0,2542,t=Big+Data&i=62849,00.asp.

PwC View Issue 15 17

has such great control over its informa-tion value chain that it tells store managers how to restock to meet the demand of the breakfast crowd, the lunch rush, the afternoon snacker, the evening shopper, and the late-night eater. The company is able to drive more sales because its information value chain allows it to slice the store in time increments, thereby creating more virtual square footage through information.

General Electric’s aircraft engine business has more information about the behavior of the engine on the wing that it tracks in its command center than the pilots have in the cockpit. By being able to track this information in real time, GE can provide customers with more analysis and preven-tative maintenance, thereby increasing up-time. Most important, by having a technological connection to the engine in flight, GE can sell “power by the hour” and provide airlines with a service whereby they pay only for those hours of engine use

they consume while GE worries about own-ing, providing, and maintaining the asset. We see a growing number of companies using this technology-based advantage to enhance their products, create new and better services, and retain customers.

driver 3: environmentalFrom a business perspective, eco-friendliness used to be primarily about reputation. That no longer is the case. Today, there is pressure on every industry to deal with power, water, and general environmental impact.

CEOs are recognizing that sustainability is as important to competitiveness as it is to image, permeating every aspect of an organization, from talent recruitment to innovation. In fact, according to our 14th Annual Global CEO Survey, 64 percent of respondents agree or strongly agree that an important part of their innovation strategy is to develop products or services that are environmentally friendly.

In short, in an increasingly competitive market, eco-friendliness is a differentiator, and more and more firms are recognizing the need to determine the implications of environmental matters for themselves, their customers, and their locations.

Consider MBA Polymers, for example, a company that has taken a potential eco-disaster—discarded post-consumer plastic—and turned it into a successful enterprise. When founder and plastics engineer Mike Biddle discovered that, for a variety of reasons, very little plastic was being recycled, he set out to find a solution. He developed a 30-step plastics recycling system that results in a product that requires less than one-tenth of the energy needed to make new plastic from crude oil. As a consequence of an innovative, eco-friendly solution, MBA Polymers has grown to include plants in China, Austria, and the United Kingdom, with plans to open additional plants in the future.

18 PwC View Issue 15

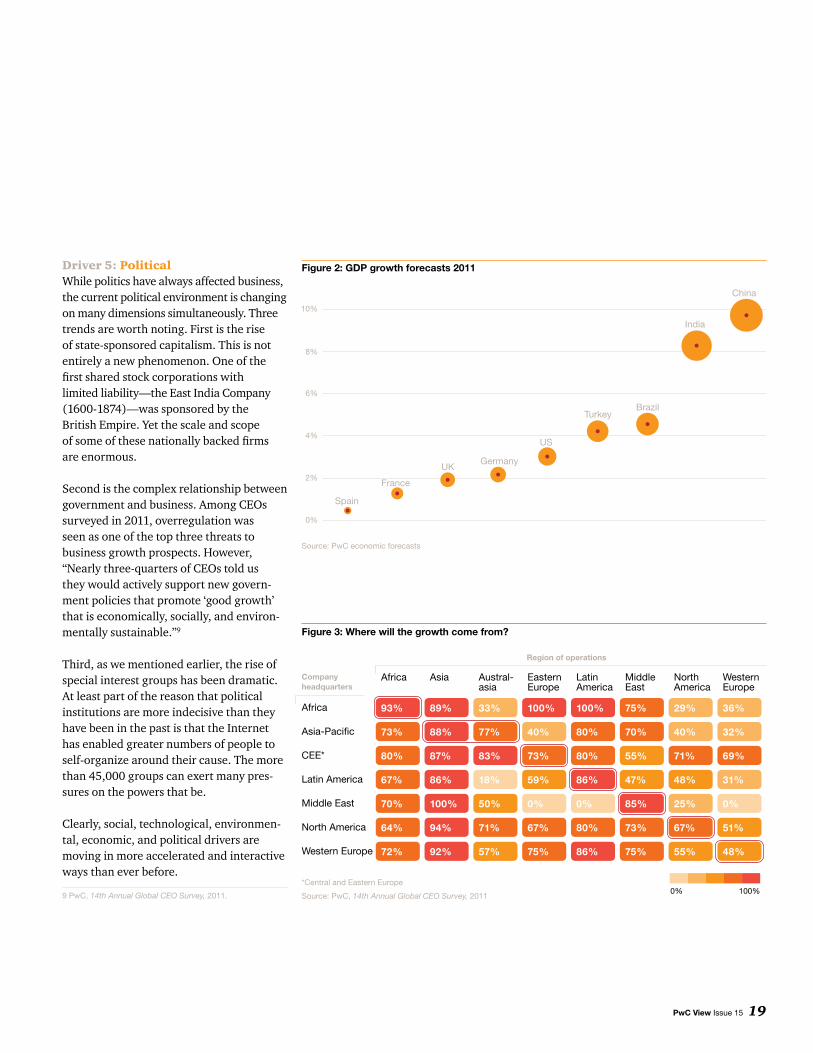

driver 4: economicEvidence points to the fact that the developing world is growing at a faster pace than the developed world. (See Figure 2.)

Most companies not only expect to grow in their home markets, but also intend to expand in other countries. Firms headquar-tered in the developed world want to grow in the developing world and vice versa. (See Figure 3.) Because there will be intensive competition both in developed as well as in emerging markets, companies need to understand how to manage a global supply base while meeting the needs of their local markets.

In our view, the need to grow will drive companies to manage their costs in a glob-ally efficient manner. This is evident in that almost every major company is establishing research and development centers around the globe and sourcing from an ever-wider base of global suppliers. For example, a large multi-level marketing company we worked with had standardized its core products and business concepts around the world. At the same time, it was important to meet the local variations in a number of markets. Therefore, the products that the company stocked and the business model it followed differed country by country. The Internet is an infrastructure that enables simultaneous standardization of some capabilities and localization of others. Again, this trend is accelerating as a combination of more open trade and the Internet enables a worldwide platform for commerce.

86%of more than 7,000 online users surveyed shop across at least two channels.

Other companies also have taken advantage of the demand for eco-friendly products and services. Some, like LIFESAVER® systems, deal with the needs of the here and now. LIFESAVER has developed a bottle-based (and therefore portable) water purifica-tion system that instantly creates potable water by filtering toxins and other impuri-ties and has filled a need that ranges from humanitarian efforts resulting from natural disasters to individuals traveling to locations

where drinkable water may not be readily available. Others, like Nanoholdings LLC, have their sights firmly fixed on the future. Nanoholdings is using cutting-edge nano-technology to approach energy generation in new, environmentally friendly ways.

Whether focusing on today or tomorrow, eco-friendly business is here to stay and sure to grow, offering significant opportu-nities for success through innovation.

PwC View Issue 15 19

Figure 3: Where will the growth come from?

0%

2%

4%

6%

8%

10%

China

India

BrazilTurkey

US

GermanyUK

France

Spain

driver 5: politicalWhile politics have always affected business, the current political environment is changing on many dimensions simultaneously. Three trends are worth noting. First is the rise of state-sponsored capitalism. This is not entirely a new phenomenon. One of the first shared stock corporations with limited liability—the East India Company (1600-1874)—was sponsored by the British Empire. Yet the scale and scope of some of these nationally backed firms are enormous.

Second is the complex relationship between government and business. Among CEOs surveyed in 2011, overregulation was seen as one of the top three threats to business growth prospects. However, “Nearly three-quarters of CEOs told us they would actively support new govern-ment policies that promote ‘good growth’ that is economically, socially, and environ-mentally sustainable.”9

Third, as we mentioned earlier, the rise of special interest groups has been dramatic. At least part of the reason that political institutions are more indecisive than they have been in the past is that the Internet has enabled greater numbers of people to self-organize around their cause. The more than 45,000 groups can exert many pres-sures on the powers that be.

Clearly, social, technological, environmen-tal, economic, and political drivers are moving in more accelerated and interactive ways than ever before.

9 PwC, 14th Annual Global CEO Survey, 2011.

Figure 2: GDP growth forecasts 2011

Source: PwC economic forecasts

Source: PwC, 14th Annual Global CEO Survey, 2011

*Central and Eastern Europe

33%

40%

29%

40%

25%

36%

32%

31%18%

0% 0% 0%50%

57%

59%

55%

47% 48%

55%

51%

48%

93% 89%

88%

87%

86%

100%

94%

92%

100% 100%

86%

85%

83%

86%

Companyheadquarters

Africa

Asia-Pacific

CEE*

Latin America

Middle East

North America

Western Europe

Region of operations

Africa

0% 100%

Asia Austral- asia

Eastern Europe

Latin America

Middle East

North America

Western Europe

73%

80%

67%

70%

64%

72%

77%

71%

73%

67%

75%

80%

80%

80%

75%

70%

73%

75%

71%

67%

69%

20 PwC View Issue 15

Designing your fiercest competitor: addressing the Steep drivers in your business

organization. A mental model is a picture of how the world actually works. It is based on data, relationships, and everyday experiences. While mental models are somewhat imprecise, subject to change, and inconsistent, they also are prone to creativity and/or flashes of insight.

Let’s take an example from the airline industry to illustrate how mental models work. Executives at an airline brought with them a mental model of the experi-ence of flying with their organization that was composed of elements such as sup-port, innovation, trust, transparency, and quality. However, stories about the flying experience on this airline were propagat-ing across social networks via social media, forever changing management’s notion of how traditional media work. Data on interactions with, for example, gate agents, flight attendants, and baggage handlers also affected the mental image, as did

While it is easy to consider the STEEP driv-ers in an abstract manner, it’s not as easy to confront them in concrete and immediate ways—that is, in ways that really can have an impact on your company. As any leader knows, organizational change depends on winning people’s minds and hearts. In order to begin a process of change, people need to be affected on both a rational and an emotional level. An abstract consider-ation of change that somehow is not very meaningful today will not get that job done. What’s needed is a technique that brings an immediacy to change and that leads to concrete action steps to deal with it. An exercise that facilitates designing your fiercest competitor is one such technique. (See Figure 4.)

Altering the mental modelEveryone who works for, buys from, does business or interacts in any way with a company forms a mental model of that

PwC View Issue 15 21

moments of truth, those profound experi-ences with a company—good or bad—that can remain with consumers for years.

Anticipating a fiercest competitor can have the same impact with regard to altering a mental model. It is critical that manage-ment teams learn how to design such a competitor in order to envision how new entities might enter their market and dis-rupt their business.

One way to do this is to ask management to imagine that they have been fired from their own firm and given access to capital and tal-ent. Most executives know their company’s weaknesses—the soft underbelly, if you will—and where the opportunities lie in a market for a firm that can move with a new model. This exercise helps senior executives

Figure 4: A fiercest competitor exercise

Alter your mental model Imagine scenarios involving disruptive, greenfield competitors

Apply insights gained

get out of their old mental habits and imag-ine new ways to compete.

Developing scenariosOnce this is accomplished, the fact base from the STEEP drivers relevant to the company’s industry can be used to imagine a couple of scenarios that jump-start a worrisome conversation. For example, if you are Apple, as a starting point, you might imagine what happens to your video business if Microsoft were to buy Netflix and do a distribution deal with Facebook. Or if you are a prop-erty and casualty insurance company, you might imagine what would happen if Google teamed up with an investment house that was willing to create a retail insurance prod-uct, and it used Google’s search expertise to help in underwriting and sales. Under these hypothetical circumstances, Google could

facilitate the creation of a new-age insurance firm. In conducting exercises of this sort, we often suggest that the fiercest competitor be imagined as a greenfield firm because it helps the senior team be unconstrained by current capabilities, organizational culture, performance standards, and norms.

As Clay Christensen has pointed out, compa-nies are often blind-sided by firms that take advantage of emerging trends and serve a lower price/underserved market.10 In short, we are asking executives to design disruptive competitors. We find that by doing this fierc-est competitor exercise, the STEEP drivers become real in a context senior management can understand and find motivating on a rational and an emotional level.

10 The Innovator’s Dilemma, Harvard Business School Press, 1997.

22 PwC View Issue 15

be building relationships. STEEP drivers uncover new complementors, channel players, and emerging third parties.

Third, and the most difficult, is that the senior team begins to have ideas for disrup-tive business designs. The problem for the CEO is that few organizations have the right talent, organizational structure, and funding to build a truly disruptive competi-tor—but it can be done.

Determining success—a caveatWhile some businesses are poised to extend their existing models to the next wave of change to meet the challenge of a fiercest competitor, success is neither easy nor assured. When the trends portend a disruptive competitor, we have found few—if any—companies that successfully created disruptive business models within their own organizations. The winners usually devise a way to “hot-house” the new business model.

Launching new products at Green Mountain Coffee®

Applying the insightsThe critical leadership question is this: What does one do with the insights that are generated from a fiercest competitor design exercise? The output usually comes in three forms. (See Figure 5.)

First, most executive teams immediately find places in their business where they need to accelerate existing initiatives or eliminate them so as to focus on the present and future rather than on the past. For example, after a fiercest competitor workshop at one major insurance company, management chose the former approach. They amped up their direct-to-consumer strategy because they saw its weakness in that channel much more clearly. A differ-ent firm saw that it needed to create a new product to blunt a possible strategic weak-ness if and when inflation returns.

Second, senior teams pursue partnerships with outside firms with which they should

At Green Mountain Coffee Roasters, anticipating its fiercest competitor means applying innovation energy at all levels of the organization. The ultimate goal? To generate a revenue stream that grows by 15 percent per year through the introduc-tion of new hit products.

However, according to Kevin Hartley, Vice President of Strategy at Green Mountain, this is easier said than done. “While critical to the launching of hit products, innovation is not for wimps. It’s ugly, and in large or-ganizations, it collides with the status quo.” What’s needed, he says, is “an understand-ing of the dynamics of the organization,

coupled with an infrastructure that enables innovation and, consequently, the launch-ing of hit products.” By bringing together quality coffee and a unique single-serve delivery system, the Keurig K-Cup single-serve brewer is a home run for Green Mountain and is today, as Hartley describes it, “the fastest-growing consumer product in the US, except for the iPad.”

Success, however, doesn’t just happen. It requires infrastructures suitable to the launching of global hit products, including individuals who are drivers of innovation, suitable gatekeepers, and assets that are aligned with opportunities.

Accelerate or eliminate existing initiatives

Pursue new partnerships

Develop disruptive business designs

Figure 5: Creating a disruptive business model

PwC View Issue 15 23

Hartley refers to individuals who drive innovation as producers. “A producer,” he says, “takes an idea and rams it through until it exists in the physical world. Produc-ers are change agents who never give up. Rather, they take decision makers through the processes needed to make great new products real. They lay the groundwork for infrastructures that enable creation.”

When it comes to launching new hit prod-ucts, every large organization has internal adjudicators or gatekeepers who can prevent an idea from reaching its potential. “The solution,” says Hartley, “is to use world-class adjudicators, preferably from outside the organization, who are knowledgeable about

Finally, when launching a global hit product, it’s important that assets equal opportuni-ties. Says Hartley, “If you have a vision of a global hit product, your assets—human and financial—must be appropriately sized to the opportunity. If you’re not going to do that, you should just forget about innovation.”

The team at Green Mountain Coffee practices what they preach. But they are not resting on their laurels. According to Hartley, they intend to apply these principles to achieving their ultimate objective: “We want to be the world’s largest single-serve beverage company,” he says. “And new global hit products will help us get there.”

While some businesses are poised to extend their existing models to the next wave of change to meet the challenge of a fiercest competitor, success is neither easy nor assured.

One way is to establish disruptive innova-tions as separate organizational entities with their own funding and leadership and with a plan to integrate them after they grow to scale. If there is a relationship to the parent, it is usually arm’s length, at least until the division grows large enough to stand on its own. At that time, it is reintegrated. This is how IBM entered the personal computer business in the 1980s, and it was how W.W. Grainger created a market-leading online capability, Grainger.com, in the mid 1990s. Bottom line: The more disruptive the business model is to the parent company, the greater “distance” it needs from the core.

There are, however, always the exceptions that prove the rule. Though it’s not the norm, with strong leadership and proper guidance, disruptive business models can be incubated closer to home. Cases in point: Schwab Online and Green Mountain Coffee. Schwab Online was created within the

overall Schwab structure and eventually became the core of the new Schwab. Likewise, Green Mountain Coffee has been able to incubate radical inventions within its core business. (See the sidebar below.)

deriving valueWhile workshops can be intellectually stimulating and encourage teamwork, if value is not the result, the entire exercise is in vain. If you are going to extract eco-nomic value from the fiercest competitor design effort, you must look to accelerate key internal initiatives, constrain others,

create new partnerships, and, in the case of truly fierce designs, avoid being seduced by the hope that you can incubate this new model within your own firm without appropriate distance between the old and the new. History shows that successful companies will kill the new idea with kind-ness if they are kept too close. Like a rogue relative, a new idea needs time to develop and mature before returning to the fold. If your organization lacks the courage to give new ideas a chance to thrive and grow, the market will give birth to your worst night-mare. If it has that courage and exploits it to the fullest, you will succeed.

the ideas they are judging. The key is to avoid the tyranny of the check mark—the naysayers who insist, ‘Yeah, we tried that, it didn’t work.’” Often, when new products founder, the blame rests with the internal adjudicators. Because they’re judging new products, they may lack adequate knowl-edge of the customer or the market. Big ideas can get so diluted prior to execution that they barely resemble the original con-cept. As Hartley points out, “If you want to set an infrastructure for launching hit prod-ucts, the purity and power of the idea has to be exposed to the consumer.” Anything less will result in failure.

52 PwC View Issue 15

editorial

Editorial Director Tom Craren

Managing Editor Gene Zasadinski

Assistant Managing EditorChristine Wendin

View points Editor Angela Pham

Contributing EditorsMike Brewster Emily Church Cecily Dixon Susan Eggleton Benjamin Isgur Sandy Lutz Susan Poole Anand Rao Bill Sand Jamie Yoder

online

Jeffrey Dreiblatt Adiba Khan Scott Schmidt Jack Teuber

design

Odgis + Company

Creative Director Janet Odgis

Senior DesignerBanu Berker

DesignersRhian Swierat T. Chloé Bartholomew

Contributors

We thank the following individuals for their contributions to this issue of View:

Caroline Calkins-Heine Steve Lechner Alfred Peguero Daryl Walcroft

photography

AP Images

Brian Bielmann

Corbis Images

Bill Gallery

Getty Images

Andreas Herzau/Laif/Redux

iStockphoto

Vincent Lafloret

Chen Ming/Xinhua/Eyevine/Redux

Tommaso Rada/4See/Redux

Reuters Pictures

Brian Smale

Stephen Wilkes

viewIssue 15

To request additional copies of View or to comment: www.pwc.com/view.

PwC firms help organisations and individuals create the value they’re looking for. We’re a network of firms with 169,000 people in more than 158 countries who are committed to deliver quality in assurance, tax and advisory services. Tell us what matters to you and find out more by visiting us at http://www.pwc.com/.

© 2012 PwC. All rights reserved. PwC refers to the PwC network and/or one or more of its member firms, each of which is a separate legal entity. Please see www.pwc.com/structure for further details. This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors.

The information contained in this document is for general guidance on matters of interest only. The application and impact of laws can vary widely based on the specific facts involved. Given the changing nature of laws, rules, and regu lations, there may be omissions or inaccuracies in information contained in this document. Before making any decision or taking any action, you should consult a competent professional adviser. Although we believe that the infor mation contained in this document has been obtained from reliable sources, PricewaterhouseCoopers is not responsible for any errors or omissions contained herein or for the results obtained from the use of this information.

View magazine is printed at an ISO 14001:2004 certified plant with Forest Stewardship Council (FSC) Chain of Custody certification (BVCOC-080903). It was printed with the use of renewable wind power resulting in nearly zero volatile organic compound (VOC) emissions. The paper used is 10 percent recycled minimum with postconsumer waste.

By printing at a facility that uses wind-generated electricity:

6,440 lbs of greenhouse gases were prevented

equivalent to 5,588 miles not driven in a year

equivalent to planting 438 trees

By using postconsumer recycled fiber in lieu of virgin fiber:

105,932 gallons of wastewater flow was saved

12,070 lbs of solid waste was not generated

32,676 lbs net of greenhouse gases was prevented

158,000,000 BTUs of energy was not consumed

Source: Environmental Defense Fund paper calculator

www.pwc.com/view

Rear view

Are you designing a disruptive business model to keep your fiercest competitor at bay?

Alter your mental model Apply insights gained Imagine scenarios involving disruptive, greenfield competitors