Vietnamese Bank Valuation

29

Present by: HOANG HAI NGUYEN [email protected] Vietnamese Bank Valuation John Von Neumann Institute - VNUHCM November - 2013 Nguyen Vietnamese Bank 1

-

Upload

nguyen-hoang -

Category

Economy & Finance

-

view

320 -

download

1

Transcript of Vietnamese Bank Valuation

Present by: HOANG HAI NGUYEN [email protected]

Vietnamese Bank Valuation

John Von Neumann Institute - VNUHCM

November - 2013

Nguyen Vietnamese Bank Valuation 1

Table of Content

• Motivation• Objectives• Literature review• Model specification• Results & Discussion• Conclusion & Perspective

Nguyen Vietnamese Bank Valuation 2

Motivation

• Valuing financial service firms is difficult.

• The top of the list of valuation issue [1]

• More banks listed on stock exchanges (VN – 18%) [*].

• Need the framework for valuing bank.

Nguyen Vietnamese Bank Valuation 3[*]: Own calculation at 01/11/2013

• Review the current bank industry practice• Review the literature on the topic of firm

valuation• Propose a framework for valuing bank• Discuss practical implication• Indicate areas for further research in the

future

Nguyen Vietnamese Bank Valuation 4

Objectives

• Problem 1: Operating business is special.

• Problem 2: most banks operate under a regulatory framework.

Nguyen Vietnamese Bank Valuation 5

Problem

• Business structure• Value-relevant specifics

Nguyen Vietnamese Bank Valuation 6

Bank Specifies in Context of Valuation

Nguyen Vietnamese Bank Valuation 7

AssetsNon-banks Banks

Liability & shareholders' equity

Non-hanks Banks

Property, plant and equipment 25% 1% Equity capital and reserves 18% 8%

Investments 13% 2% Provisions 20% 1%

Inventories 23% n/a Liabilities 62% 91%

Receivables 33% 74% Trade payables 12% n/a

from customers 15% 49%Liabilities to financial

institutions 20% 29%

from credit institutions n/a 25% Liabilities to non-banks n/a 38%

Other receivables 18% 0% Securitized loans n/a 23%

Investment securities 3% 19% Other liabilities 30% 5%

Cash and cash equivalents 4% 1%

Other assets 0% 2%

Total assets 100% 100% Total assets 100% 100%

Bank Specifies in Context of Valuation (cont.)

Source: (Gross,2006)

Structure of the balance sheet of banks vs. non-banks

Nguyen Vietnamese Bank Valuation 8

Structure of the income statement of banks vs. non-banks

Bank Specifies in Context of Valuation (cont.)

RevenuesNon-Banks Banks Expenses

Non-Banks Banks

Sales 93% n/a Supplies expense 61% n/a

Change in inventories 1% n/a Staff expense 16% 10%

Interest income 1% 83% Other administrative expenses n/a 7%

Income from provisions n/a 7% Depreciation 4% 7%

Income from securities & investments n/a 4% - on fixed assets & intangible 4% 1%

Net income from financing business n/a 1%

Provisions on receivable & securities n/a 5%

Other income 5% 5% Interest expense 2% 71%

Tax charges 3% 1%

Other expenses 14% 4%

Total income 100% 100% Total expense 100% 100%Source: (Gross,2006)

• Business structure of banks• Value-relevant specifics of banks– Specific role of financing and risk-taking– Bank-specific laws and regulations– Specifics of the operating business

Nguyen Vietnamese Bank Valuation 9

Bank Specifies in Context of Valuation

Nguyen Vietnamese Bank Valuation 10

Valuation methods and their application for banks

Four approaches [2] [3] [4] Applications Requirements

Asset-based approach Valuing individual financial investments

Market-oriented approach Valuing bank - Information is easily accessible- Comparable assets is not limited

Cash flow-oriented approach

Valuing bank - The cash flows of a bank are easily estimated

Residual Income-oriented approach

Valuing bank - The return on invested capital- The cost of capital

⁻ The equity approach [1][4]

⁻ Residual Income model⁻ Need to adjust

Nguyen Vietnamese Bank Valuation 11

Selection

Nguyen Vietnamese Bank Valuation 12

Model specification

Market value

Invested Capital

Future value

creation

Market value observed in the market

Intrinsic value

Economic Equity

Value of Residual Income

Intrinsic value estimated by model

• Using equity approach, Residual Income model,

• Residual Income is defined by Equation[2]:

RI = Op. Earnings - k x EE (1)• Intrinsic value of bank[2]

IV = EE + PV(RI) (2)

Nguyen Vietnamese Bank Valuation 13

Structure of the Model

RI: Residual IncomeOp. Earning: Operating Earningk: cost of equity

IV: Intrinsic valueEE: Economic EquityPV(RI): Present value of Residual Income

Intrinsic value

Economic Equity

Value of Residual Income

• Calculation of Economic Equity– Charter equity, reserves, sum of intangible, deferred taxesEconomic Equity = Charter equity + Sum of intangible + reserves + deferred taxes

• Calculation of Residual Income

– RI increases at a certain perpetual growth rate g– PV(RI) can be expressed as :

Nguyen Vietnamese Bank Valuation 14

Structure of the Model (cont.)

(3)

t t+2t+1 …𝑅𝐼 𝑡+1 𝑅𝐼 𝑡+2

𝑃𝑉 (𝑅𝐼 )

t+m𝑅𝐼 𝑡+𝑚𝑅𝐼 𝑡

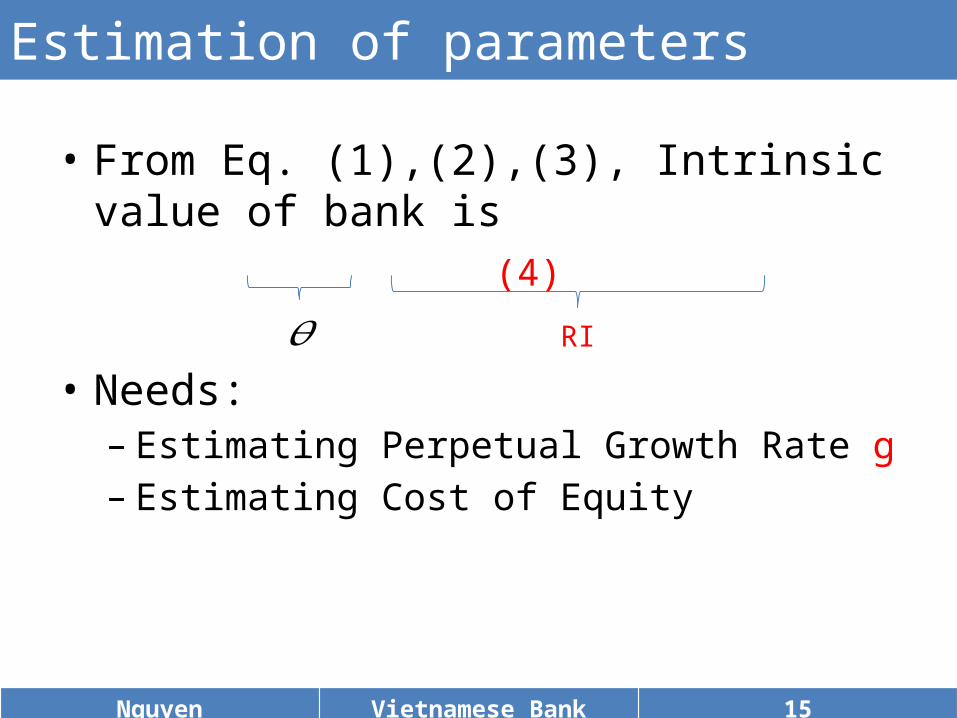

• From Eq. (1),(2),(3), Intrinsic value of bank is (4)

• Needs:– Estimating Perpetual Growth Rate g– Estimating Cost of Equity

Nguyen Vietnamese Bank Valuation 15

Estimation of parameters

RI𝜃

Value of firm cannot be larger than value of economic (GDP).

The log normal process- Firm: - Economic:

Applying Ito’s lemmaWe have limitation of perpetual growth rate of firm

Nguyen Vietnamese Bank Valuation 16

Estimation of Perpetual Growth Rate

𝜇𝐹<𝜇𝐸+12

(𝜎 𝐹2 −𝜎𝐸

2 ) (7)

1 13 25 37 49 61 73 85 97 1090.001

0.01

0.1

1

10

100

1000

10000

Economic Firm

• From (1),(2),(3), Intrinsic value of bank is (4)

• Needs:– Estimating Perpetual Growth Rate g– Estimating Cost of Equity -> using CAPM model

)

Nguyen Vietnamese Bank Valuation 17

Estimation of Cost of Equity

RI𝜃

• Selected markets• Financial factors• Market data• Economic factors

Nguyen Vietnamese Bank Valuation 18

DATASET

Market data

Economic factors

Financial factors

Model

Nguyen Vietnamese Bank Valuation 19

Selected Markets

Characteristics Australia Vietnam

Type of market Developed Frontier

Size Large Small

Volatility Low High

Policy Low risk High risk

Information Transparent Lack of information

Selected marketsFinancial factorsMarket dataEconomic factors

Own table

No. Full Name Transaction Name CodeMarket cap.

(bil. VND)

First Day of Trading

1Asia Commercial Joint Stock Bank

ACB ACB 15,002.71 11/21/2006

2Vietnam Joint Stock Commercial Bank for Industry and Trade

VIETINBANKCTG 64,669.66 07/16/2009

3Vietnam Export Import Commercial Joint Stock Bank (Vietnam Eximbank)

EXIMBANKEIB 18,162.26 10/27/2009

4Sai Gon Thuong Tin Commercial Joint Stock Bank

SACOMBANK STB 19,308.45 12/07/2006

5Joint Stock Commercial Bank For Foreign Trade of Vietnam

VIETCOMBANK VCB 64,887.68 30/06/2009

No.

Full Name CodeMarket cap.

(mil. A$)Rank

1Australia and New Zealand Banking Group

ANZ 59,030 3

2 Commonwealth Bank CAB 84,540 13 National Australia Bank NAB 52,730 44 Westpac Banking Corporation WBC 64,560 2

Nguyen Vietnamese Bank Valuation 20

Selected Markets (cont.)

Selected markets– Australia– Vietnam

Nguyen Vietnamese Bank Valuation 21

DATASET

Economic factors– GDP growth rate– Risk-free rate– Risk Premium

Financial factors– Annual financial reports– Adjusted profit, capital,

and number of shares

Market data– Close price.– Market Index:

• Australia market: ASX200

• Vietnam market: Banking Index

Results

Nguyen Vietnamese Bank Valuation 22

The results

Market data

Economic factors

Australia’s Banks

Vietnam’s Banks

Financial factors

Model

Nguyen Vietnamese Bank Valuation 23

Australia’s Banks

19891991

19931995

19971999

20012003

20052007

20092011

0

5

10

15

20

25

30

35ANZ

Modelled Price Traded Price1992

19931994

19951996

19971998

19992000

20012002

20032004

20052006

20072008

20092010

20112012

0

10

20

30

40

50

60CAB

Modelled Price Traded Price

19891991

19931995

19971999

20012003

20052007

20092011

05

101520253035404550

NAB

Modelled Price Traded Price1989

19911993

19951997

19992001

20032005

20072009

20110

5

10

15

20

25

30

35WBC

Modelled price Traded Price

Nguyen Vietnamese Bank Valuation 24

Australia’s Banks (cont.)

0 5 10 15 20 25 30 350

5

10

15

20

25

30

35

f(x) = 0.923033382703708 x + 0.606548389088504

ANZ

0 10 20 30 40 50 600

10

20

30

40

50

60

f(x) = 0.866433485430815 x + 2.87103456034985

CBA

0 5 10 15 20 25 30 35 40 450

10

20

30

40

50

f(x) = 1.0414725692756 x + 0.3151313559732R² = 0.893952153000979

NAB

0 5 10 15 20 25 30 350

5

10

15

20

25

30

f(x) = 0.900373629009221 x + 0.771940698500252R² = 0.942464866008935

WBC

Nguyen Vietnamese Bank Valuation 25

Vietnam’s Banks

2009 2010 2011 20120

5

10

15

20

25

30

35

40ACB

Modelled Price Traded Price2009 2010 2011 2012

0

5

10

15

20

25CTG

Modelled Price Traded Price

2009 2010 2011 20120

2

4

6

8

10

12

14

16

EIB

Modelled Price Traded Price2009 2010 2011 2012

0

5

10

15

20

25

30

35VCB

Modelled Price Traded Price

Nguyen Vietnamese Bank Valuation 26

Vietnam’s Banks (cont.)

2009 2010 2011 2012 (5,000)

-

5,000

10,000

15,000

20,000

25,000

30,000

ACB

Residual Income Capital

Year

Bank's value (mil. VND)

2009 2010 2011 2012 -

10,000

20,000

30,000

40,000

50,000

60,000

70,000

CTG

Residual Income Capital

Year

Bank's value (mil. VND)

2009 2010 2011 2012 (5,000)

-

5,000

10,000

15,000

20,000

25,000

EIB

Residual Income Capital

Year

Bank's value (mil. VND)

2009 2010 2011 2012 -

10,000

20,000

30,000

40,000

50,000

60,000

70,000

VCB

Residual Income Capital

Year

Bank's value (mil. VND)

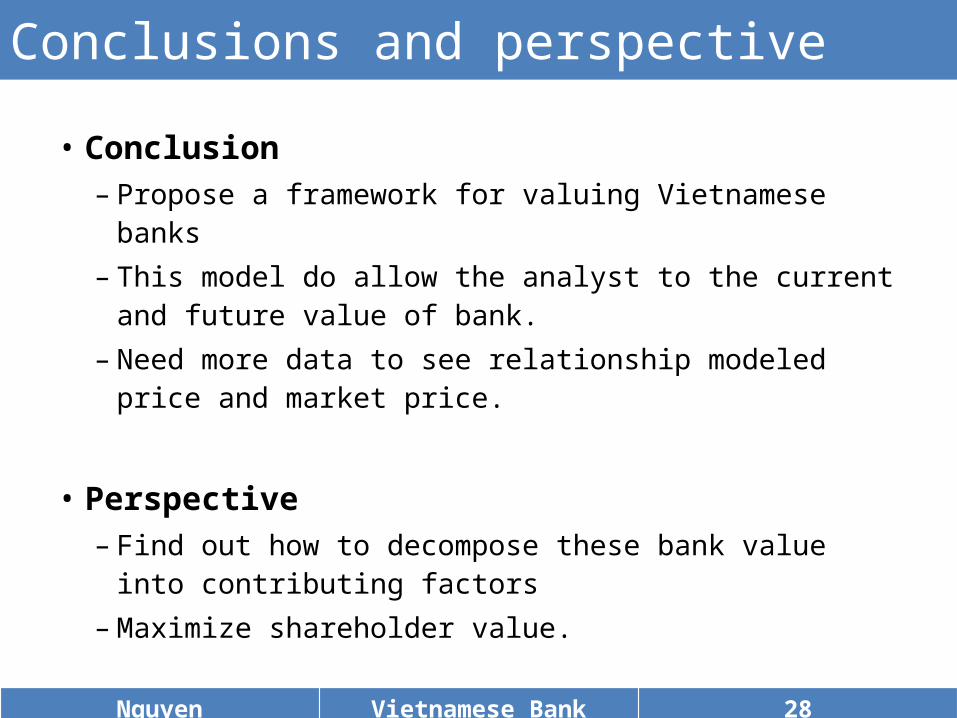

• Appreciate model for valuing banks is residual income model.

• Estimating parameters of Residual income model for Vietnam market.

• Bank value is effected by external factors (rf,b) and internal factors (Capital, Profit ).

Nguyen Vietnamese Bank Valuation 27

Findings

• Conclusion– Propose a framework for valuing Vietnamese banks– This model do allow the analyst to the current and

future value of bank.– Need more data to see relationship modeled price

and market price.

• Perspective– Find out how to decompose these bank value into

contributing factors– Maximize shareholder value.

Nguyen Vietnamese Bank Valuation 28

Conclusions and perspective

THANK FOR YOUR ATTENTION

![[Bank of America] Hybrid ARM MBS - Valuation and Risk Measures](https://static.fdocuments.in/doc/165x107/55205dca4979590a3f8b4684/bank-of-america-hybrid-arm-mbs-valuation-and-risk-measures.jpg)