VIA A11 NV - IFLR. · PDF fileVIA A11 NV (incorporated as a public limited liability company...

181

VIA A11 NV (incorporated as a public limited liability company (société anonyme/naamloze vennootschap) under the laws of Belgium and registered with the Belgian legal entities register under number 0547.978.239) €577,900,000 4.49 per cent. Secured Amortising Bonds due 2045 Issue price: 100 per cent. The €577,900,000 4.49 per cent. Secured Amortising Bonds due 2045 (the Bonds ) are issued by Via A11 NV a Belgian limited liability company ( société anonyme/naamloze vennootschap ), having its registered office at Tragel 60, 9308 Hofstade-Aalst Belgium and registered with the legal entities register ( RPM/RPR) under number 0547.978.239 (the Issuer) and will be constituted by a bond trust deed (the Bond Trust Deed) to be dated on or about 20 March 2014 (the Issue Date ) between the Issuer and Deutsche Trustee Company Limited as bond trustee (the Bond Trustee, which expression shall include its successors as bond trustee for the holders of the Bonds for the time being (the Bondholders )). Interest accrues on the Bonds at a rate of 4.49 per cent. per annum from (and including) the Issue Date. Interest is payable from and including the Issue Date to and including 31 March 2018, quarterly in arrear on 31 March, 30 June, 30 September and 31 December and thereafter, from and including 30 September 2018, semi-annually in arrear on 31 March and 30 September in each year (each a Payment Date ), the first Payment Date will be 31 March 2014. The Bonds will be redeemed in instalments on each Payment Date from and including 31 March 2018. To the extent not previously redeemed or purchased and cancelled, the Bonds will be redeemed in full on 30 September 2045 (the Final Redemption Date ). The Bonds will be issued on the Issue Date. A portion of the Bonds (the Initial Issue Bonds) will be subscribed and paid for on the Issue Date by the Bond Purchasers. The remaining portion of the Bonds (the Forward Purchase Bonds) will be subscribed and paid for by the Deutsche Bank AG, London Branch (Deutsche Bank) on the Issue Date and then sold back to the Issuer. Certain Bond Purchasers will purchase certain of the Forward Purchase Bonds on each Bond Purchase Date in accordance with the terms of an agreement dated 18 March 2014 between, inter alia, the Issuer, Deutsche Bank and the Bond Purchasers (the Bond Purchase Agreement). On the Issue Date, the Issuer will also issue €287,509,000 4.49 per cent. unlisted partly paid notes (the PP Notes ) to certain investors. Those investors may elect to purchase the remaining Forward Purchase Bonds rather than pay-up the PP Notes. The European Investment Bank (EIB or the PBCE Provider) has undertaken to issue a letter of credit (the PBCE Letter of Credit) in accordance with the terms of a letter of credit and reimbursement deed between the Issuer, the Bond Trustee and the PBCE Provider dated the Issue Date (the PBCE Agreement ) (as described in “ Description of the PBCE Letter of Credit ”). The PBCE Letter of Credit is not a guarantee but it is a form of subordinated credit enhancement in relation to the Bonds and the Bonds are not guaranteed by the PBCE Provider and the PBCE Letter of Credit is not a guarantee within the meaning of the Commission Regulation (EC) 809/2004. Under the terms of the PBCE Agreement, the PBCE Provider will undertake to make amounts available under the PBCE Letter of Credit in an amount up to the the PBCE Maximum Balance (a) to fund PBCE Funding Shortfalls; (b) to meet scheduled interest and principal payments in relation to the Bonds (other than those held by the Issuer) and the PP Notes; (c) if certain PBCE Rebalancing Events occur to meet mandatory partial redemption amounts due in respect of the Bonds and the PP Notes; or (d) to meet certain accelerated payments in relation to the Bonds and the PP Notes. The Issuer is a special purpose vehicle whose principal purposes are, inter alia, to issue the Bonds and to design, build, finance and maintain the A11 road in Bruges in accordance with the provisions of an agreement to be entered into between the Flemish Region (the Authority) and the Issuer on or around the Issue Date (the DBFM Agreement ). Via Brugge NV ( HoldCo) is a special purpose vehicle established for the principal purpose of holding 60.67% of the shares in the Issuer. The remaining 39.33% of the shares in the Issuer are held by Via-Invest Vlaanderen NV, a company ultimately controlled by the Authority ( Via- Invest ). Via-Invest and HoldCo (together the Shareholders ) are the sole shareholders of the Issuer. The Bondholders will have no recourse to any shareholder of HoldCo or Via-Invest other than for the amount of any equity contribution on or prior to the Issue Date and the Shareholder Loans or to the Authority other than in respect of the rights of the Issuer under the DBFM Agreement, which are secured in favour of the Security Trustee. The obligations of the Issuer under the Bonds will be secured in favour of Deutsche Trustee Company Limited as security trustee (the Security Trustee, which expression shall include its successors for the time being). In accordance with a security trust and intercreditor agreement (the STID) to be entered into by, inter alia, the Issuer, the Shareholders, DG Infra + NV, Inframan NV, Jan De Nul NV, Asfalt Wegenis En Bouwwerken NV, Aclagro NV, Algemene Aannemingen Van Laere NV, Franki Construct NV and Via-Invest Vlaanderen NV (the Shareholder Lenders ), the Bond Trustee, the PBCE Provider, the Bond Purchasers, the PP Noteholders and the Security Trustee, the Transaction Security (as defined below) will be held by the Security Trustee for itself and on behalf of the Bondholders, the PP Noteholders, the PBCE Provider and the other Secured Creditors (as defined below) (see “ Description of the Finance Documents”). Pursuant to the STID, certain rights of the PBCE Provider against the Issuer under the PBCE Agreement are subordinated to rights of the Bondholders against the Issuer under the Bonds. However, no Enforcement Action (including acceleration of the Bonds) will be permitted, in the circumstances set out in Condition 8.2 (Events of Default ) of the Bonds. The Issuer will be required to redeem the Bonds in part prior to the Final Redemption Date upon the occurrence of a PBCE Rebalancing Event and may redeem the Bonds prior to the Final Redemption Date in full (but not in part only) upon the occurrence of certain tax-related events. The Issuer may also voluntarily redeem the Bonds prior to the Final Redemption Date in whole or in part provided that it pays the applicable Voluntary Redemption Make-Whole Amount (see Condition 4 (Redemption, Purchase and Cancellation ) of the Bonds). Application has been made to the Commission de Surveillance du Secteur Financier (the CSSF) in its capacity as competent authority under the Prospectus Act 2005 dated 10 July 2005 on prospectuses for securities, as amended (the Prospectus Act 2005) to approve this document as a prospectus for the purposes of Directive 2003/71/EC, as amended. The CSSF assumes no responsibility for the economic and financial soundness of the transactions contemplated by this Prospectus or the quality or solvency of the Issuer in accordance with Article 7(7) of the Prospectus Act 2005. Application has also been made to the Luxembourg Stock Exchange for the listing of the Bonds on the Official List of the Luxembourg Stock Exchange and admission to trading on the Luxembourg Stock Exchange’s regulated market. References in this Prospectus to Bonds being listed (and all related references) shall mean that such Bonds have been admitted to trading on the Luxembourg Stock Exchange’s regulated market and have been admitted to the Official List of the Luxembourg Stock Exchange. The Luxembourg Stock Exchange’s regulated market is a regulated market for the purposes of the Markets in Financial Instruments Directive (Directive 2004/39/EC). The Bonds are expected to be rated A3 by Moody’s Investor Services Limited (Moody’s ) on the Issue Date. Moody’s is established in the European Union and is registered under the Regulation (EC) No. 1060/2009 (as amended) (the CRA Regulation). As such Moody’s is included in the list of credit rating agencies published by the European Securities and Markets Authority on its website (at http://www.esma.europa.eu/page/List-registered-and-certified-CRAs) in accordance with the CRA Regulation. A security rating is not a recommendation to buy, sell or hold securities and may be subject to suspension, reduction or withdrawal at any time by the assigning rating organisation. The Bonds will be issued in dematerialised form in accordance with Article 468 and following of the Belgian Code of Companies and will be represented by a book-entry in the records of the X/N System operated by the National Bank of Belgium (the NBB) and will be credited to the accounts held with the X/N System by Euroclear Bank SA/NV (Euroclear) for credit by Euroclear to the securities accounts of their subscribers. Prior to the final Bond Purchase Date, the Bonds shall be credited to and held with the securities accounts of the relevant holders at Euroclear. Following the final Bond Purchase Date, the Bonds shall be eligible to be credited to securities accounts of the holders with Euroclear or Clearstream Banking S.A. (Clearstream, Luxembourg) or other X/N System participants for credit by Euroclear, Clearstream, Luxembourg or other X/N System

Transcript of VIA A11 NV - IFLR. · PDF fileVIA A11 NV (incorporated as a public limited liability company...

VIA A11 NV (incorporated as a public limited liability company (société anonyme/naamloze vennootschap) under the laws of Belgium

and registered with the Belgian legal entities register under number 0547.978.239)

€577,900,000 4.49 per cent. Secured Amortising Bonds due 2045

Issue price: 100 per cent. The €577,900,000 4.49 per cent. Secured Amortising Bonds due 2045 (the Bonds) are issued by Via A11 NV a Belgian limited liability company (société anonyme/naamloze vennootschap), having its registered office at Tragel 60, 9308 Hofstade-Aalst Belgium and registered with the legal entities register (RPM/RPR) under number 0547.978.239 (the Issuer) and will be constituted by a bond trust deed (the Bond Trust Deed) to be dated on or about 20 March 2014 (the Issue Date) between the Issuer and Deutsche Trustee Company Limited as bond trustee (the Bond Trustee, which expression shall include its successors as bond trustee for the holders of the Bonds for the time being (the Bondholders)).

Interest accrues on the Bonds at a rate of 4.49 per cent. per annum from (and including) the Issue Date. Interest is payable from and including the Issue Date to and including 31 March 2018, quarterly in arrear on 31 March, 30 June, 30 September and 31 December and thereafter, from and including 30 September 2018, semi-annually in arrear on 31 March and 30 September in each year (each a Payment Date), the first Payment Date will be 31 March 2014. The Bonds will be redeemed in instalments on each Payment Date from and including 31 March 2018. To the extent not previously redeemed or purchased and cancelled, the Bonds will be redeemed in full on 30 September 2045 (the Final Redemption Date).

The Bonds will be issued on the Issue Date. A portion of the Bonds (the Initial Issue Bonds) will be subscribed and paid for on the Issue Date by the Bond Purchasers. The remaining portion of the Bonds (the Forward Purchase Bonds) will be subscribed and paid for by the Deutsche Bank AG, London Branch (Deutsche Bank) on the Issue Date and then sold back to the Issuer. Certain Bond Purchasers will purchase certain of the Forward Purchase Bonds on each Bond Purchase Date in accordance with the terms of an agreement dated 18 March 2014 between, inter alia, the Issuer, Deutsche Bank and the Bond Purchasers (the Bond Purchase Agreement).

On the Issue Date, the Issuer will also issue €287,509,000 4.49 per cent. unlisted partly paid notes (the PP Notes) to certain investors. Those investors may elect to purchase the remaining Forward Purchase Bonds rather than pay-up the PP Notes.

The European Investment Bank (EIB or the PBCE Provider) has undertaken to issue a letter of credit (the PBCE Letter of Credit) in accordance with the terms of a letter of credit and reimbursement deed between the Issuer, the Bond Trustee and the PBCE Provider dated the Issue Date (the PBCE Agreement) (as described in “Description of the PBCE Letter of Credit”). The PBCE Letter of Credit is not a guarantee but it is a form of subordinated credit enhancement in relation to the Bonds and the Bonds are not guaranteed by the PBCE Provider and the PBCE Letter of Credit is not a guarantee within the meaning of the Commission Regulation (EC) 809/2004. Under the terms of the PBCE Agreement, the PBCE Provider will undertake to make amounts available under the PBCE Letter of Credit in an amount up to the the PBCE Maximum Balance (a) to fund PBCE Funding Shortfalls; (b) to meet scheduled interest and principal payments in relation to the Bonds (other than those held by the Issuer) and the PP Notes; (c) if certain PBCE Rebalancing Events occur to meet mandatory partial redemption amounts due in respect of the Bonds and the PP Notes; or (d) to meet certain accelerated payments in relation to the Bonds and the PP Notes.

The Issuer is a special purpose vehicle whose principal purposes are, inter alia, to issue the Bonds and to design, build, finance and maintain the A11 road in Bruges in accordance with the provisions of an agreement to be entered into between the Flemish Region (the Authority ) and the Issuer on or around the Issue Date (the DBFM Agreement).

Via Brugge NV (HoldCo) is a special purpose vehicle established for the principal purpose of holding 60.67% of the shares in the Issuer. The remaining 39.33% of the shares in the Issuer are held by Via-Invest Vlaanderen NV, a company ultimately controlled by the Authority (Via-Invest). Via-Invest and HoldCo (together the Shareholders) are the sole shareholders of the Issuer. The Bondholders will have no recourse to any shareholder of HoldCo or Via-Invest other than for the amount of any equity contribution on or prior to the Issue Date and the Shareholder Loans or to the Authority other than in respect of the rights of the Issuer under the DBFM Agreement, which are secured in favour of the Security Trustee.

The obligations of the Issuer under the Bonds will be secured in favour of Deutsche Trustee Company Limited as security trustee (the Security Trustee, which expression shall include its successors for the time being). In accordance with a security trust and intercreditor agreement (the STID ) to be entered into by, inter alia, the Issuer, the Shareholders, DG Infra + NV, Inframan NV, Jan De Nul NV, Asfalt Wegenis En Bouwwerken NV, Aclagro NV, Algemene Aannemingen Van Laere NV, Franki Construct NV and Via-Invest Vlaanderen NV (the Shareholder Lenders), the Bond Trustee, the PBCE Provider, the Bond Purchasers, the PP Noteholders and the Security Trustee, the Transaction Security (as defined below) will be held by the Security Trustee for itself and on behalf of the Bondholders, the PP Noteholders, the PBCE Provider and the other Secured Creditors (as defined below) (see “ Description of the Finance Documents”). Pursuant to the STID, certain rights of the PBCE Provider against the Issuer under the PBCE Agreement are subordinated to rights of the Bondholders against the Issuer under the Bonds. However, no Enforcement Action (including acceleration of the Bonds) will be permitted, in the circumstances set out in Condition 8.2 (Events of Default) of the Bonds.

The Issuer will be required to redeem the Bonds in part prior to the Final Redemption Date upon the occurrence of a PBCE Rebalancing Event and may redeem the Bonds prior to the Final Redemption Date in full (but not in part only) upon the occurrence of certain tax-related events. The Issuer may also voluntarily redeem the Bonds prior to the Final Redemption Date in whole or in part provided that it pays the applicable Voluntary Redemption Make-Whole Amount (see Condition 4 (Redemption, Purchase and Cancellation) of the Bonds).

Application has been made to the Commission de Surveillance du Secteur Financier (the CSSF) in its capacity as competent authority under the Prospectus Act 2005 dated 10 July 2005 on prospectuses for securities, as amended (the Prospectus Act 2005) to approve this document as a prospectus for the purposes of Directive 2003/71/EC, as amended. The CSSF assumes no responsibility for the economic and financial soundness of the transactions contemplated by this Prospectus or the quality or solvency of the Issuer in accordance with Article 7(7) of the Prospectus Act 2005. Application has also been made to the Luxembourg Stock Exchange for the listing of the Bonds on the Official List of the Luxembourg Stock Exchange and admission to trading on the Luxembourg Stock Exchange’s regulated market.

References in this Prospectus to Bonds being listed (and all related references) shall mean that such Bonds have been admitted to trading on the Luxembourg Stock Exchange’s regulated market and have been admitted to the Official List of the Luxembourg Stock Exchange. The Luxembourg Stock Exchange’s regulated market is a regulated market for the purposes of the Markets in Financial Instruments Directive (Directive 2004/39/EC).

The Bonds are expected to be rated A3 by Moody’s Investor Services Limited (Moody’s) on the Issue Date. Moody’s is established in the European Union and is registered under the Regulation (EC) No. 1060/2009 (as amended) (the CRA Regulation). As such Moody’s is included in the list of credit rating agencies published by the European Securities and Markets Authority on its website (at http://www.esma.europa.eu/page/List-registered-and-certified-CRAs) in accordance with the CRA Regulation. A security rating is not a recommendation to buy, sell or hold securities and may be subject to suspension, reduction or withdrawal at any time by the assigning rating organisation.

The Bonds will be issued in dematerialised form in accordance with Article 468 and following of the Belgian Code of Companies and will be represented by a book-entry in the records of the X/N System operated by the National Bank of Belgium (the NBB) and will be credited to the accounts held with the X/N System by Euroclear Bank SA/NV (Euroclear) for credit by Euroclear to the securities accounts of their subscribers. Prior to the final Bond Purchase Date, the Bonds shall be credited to and held with the securities accounts of the relevant holders at Euroclear. Following the final Bond Purchase Date, the Bonds shall be eligible to be credited to securities accounts of the holders with Euroclear or Clearstream Banking S.A. (Clearstream, Luxembourg) or other X/N System participants for credit by Euroclear, Clearstream, Luxembourg or other X/N System

Page 2

participants to the securities accounts of their subscribers.

The Bonds will be accepted for clearance through the X/N System, and are accordingly subject to the applicable Belgian clearing regulations, including: the Belgian law of 6 August 1993 on transactions in certain securities, its implementing Belgian Royal Decrees of 26 May 1994 and 14 June 1994 and the rules of the X/N System and its annexes, as issued or modified by the NBB from time to time (the laws, decrees and rules mentioned in this Clause, in each case as modified or replaced from time to time, being referred to herein as the NBB System Regulations).

The Bonds will governed by English law save that any matter relating to the title to, and dematerialised form of, the Bonds will be governed by the laws of Belgium. The Bonds are intended to be held in a manner which will allow Eurosystem eligibility. This does not mean that the Bonds will be recognised as eligible collateral for Eurosystem monetary policy and intra-day credit operations by the Eurosystem either upon issue or at any or all times during their life. Such recognition will depend upon, inter alia, satisfaction of the Eurosystem eligibility criteria.

An investment in Bonds involves certain risks. Prospective investors should have regard to the factors described in the section “Risk Factors” on page 22.

Global Co-ordinator

Deutsche Bank

Joint Lead Managers

Bayern LB Belfius Bank Deutsche Bank

The date of this Prospectus is 20 March 2014

Page 3

IMPORTANT INFORMATION

This Prospectus comprises a prospectus for the purposes of Article 5.3 of Directive 2003/71/EC (the Prospectus Directive) as amended (which includes the amendments made by Directive 2010/73/EU to the extent that such amendments have been implemented in a relevant Member State of the European Economic Area).

The Issuer accepts responsibility for the information contained in this Prospectus. To the best of the knowledge of the Issuer (having taken all reasonable care to ensure that such is the case) the information contained in this Prospectus is in accordance with the facts and does not omit anything likely to affect the import of such information.

The Issuer, having made all reasonable enquiries, confirms that this Prospectus contains all material information with respect to the Issuer, the Project and the Bonds (including all information which, according to the particular nature of the Issuer, the Project and of the Bonds, is necessary to enable investors to make an informed assessment of the assets and liabilities, financial position, profits and losses and prospects of the Issuer and of the rights attaching to the Bonds), that the information contained or incorporated in this Prospectus is true and accurate in all material respects and is not misleading, that the opinions and intentions expressed in this Prospectus are honestly held and that there is no other fact the omission of which would make this Prospectus or any of such information or the expression of any such opinion or intention misleading.

None of Deutsche Bank, Belfius Bank SA/NV and Bayerische Landesbank (together the Joint Lead Managers), the Bond Trustee, the Security Trustee, the PBCE Provider, the Bond Custodian, the Project Agent, the Account Bank, the Account Operator, the Authority or Via-Invest has independently verified the information contained herein. Accordingly, no representation, warranty or undertaking, express or implied, is made and no responsibility or liability is accepted by the Joint Lead Managers, the Bond Trustee, the Security Trustee, the Bond Custodian, the PBCE Provider, the Project Agent, the Account Bank, the Account Operator, the Authority or Via-Invest as to the accuracy or completeness of the information contained in this Prospectus or any other information provided by the Issuer in connection with the offering of the Bonds. None of the Joint Lead Managers, the Bond Trustee, the Security Trustee, the Bond Custodian, the PBCE Provider, the Project Agent, the Account Bank, the Account Operator, the Authority or Via-Invest accepts liability in relation to the information contained in this Prospectus or any other information provided by the Issuer in connection with the offering of the Bonds or their distribution.

No person is or has been authorised by the Joint Lead Managers, the Issuer, the Bond Trustee, the Security Trustee, the Bond Custodian, the PBCE Provider, the Project Agent, the Account Bank, the Account Operator, the Authority or Via-Invest to give any information or to make any representation not contained in or not consistent with this Prospectus or any other information supplied in connection with the offering of the Bonds and, if given or made, such information or representation must not be relied upon as having been authorised by the Issuer, the Joint Lead Managers, the Bond Trustee, the Security Trustee, the Bond Custodian, the PBCE Provider, the Project Agent, the Account Bank, the Account Operator, the Authority or Via-Invest.

Neither this Prospectus nor any other information supplied in connection with the offering of the Bonds (a) is intended to provide the basis of any credit or other evaluation or (b) should be considered as a recommendation by the Issuer, the Joint Lead Managers, the Bond Trustee, the Security Trustee, the Bond Custodian, the PBCE Provider, the Project Agent, the Account Bank, the Account Operator, the Authority or Via-Invest that any recipient of this Prospectus or any other information supplied in connection with the offering of the Bonds should purchase any Bonds. Each investor contemplating purchasing any Bonds should make its own independent investigation of the financial condition and affairs and its own appraisal of the creditworthiness of the Issuer. Neither this Prospectus nor any other information supplied in connection with the offering of the Bonds constitutes an offer or invitation by or on behalf of the Issuer, the Joint Lead Managers, the Bond Trustee, the Security Trustee, the Bond Custodian, the PBCE Provider, the Project Agent, the Account Bank, the Account Operator, the Authority or Via-Invest to any person to subscribe for or to purchase any Bonds.

Neither the delivery of this Prospectus nor the offering, sale or delivery of the Bonds shall in any circumstances imply that the information contained herein concerning the Issuer, any Shareholder or the Project is correct at any time subsequent to the date hereof or that any other information supplied in connection with the offering of the Bonds (whether contained in this Prospectus or otherwise) is correct as of any time subsequent to the date indicated in the document containing the same. The Joint Lead Managers, the Bond Trustee, the Security Trustee, the Bond Custodian, the PBCE Provider, the Project Agent, the Account Bank, the Account Operator, the Authority and Via-Invest expressly do not undertake to review the financial condition or affairs of the Issuer during the life of the Bonds or to advise any investor in the Bonds of any information coming to their attention.

This Prospectus does not constitute an offer to sell or the solicitation of an offer to buy the Bonds in any jurisdiction to any person to whom it is unlawful to make the offer or solicitation in such jurisdiction. The distribution of this Prospectus and the offer or sale of Bonds may be restricted by law in certain jurisdictions. The Issuer, the Joint Lead Managers, the Bond Trustee, the Security Trustee, the Bond Custodian, the PBCE Provider, the Project Agent, the Account Bank, the Account Operator, the Authority and Via-Invest do not represent that this Prospectus may be lawfully distributed, or that the Bonds

Page 4

may be lawfully offered, in compliance with any applicable registration or other requirements in any such jurisdiction, or pursuant to an exemption available thereunder, or assume any responsibility for facilitating any such distribution or offering. In particular, no action has been taken by the Issuer, the Joint Lead Managers, the Bond Trustee, the Security Trustee, the Bond Custodian, the PBCE Provider, the Project Agent, the Account Bank, the Account Operator, the Authority or Via-Invest which is intended to permit a public offering of the Bonds or the distribution of this Prospectus in any jurisdiction where action for that purpose is required. Accordingly, no Bonds may be offered or sold, directly or indirectly, and neither this Prospectus nor any advertisement or other offering material may be distributed or published in any jurisdiction, except under circumstances that will result in compliance with any applicable laws and regulations. Persons into whose possession this Prospectus or any Bonds may come must inform themselves about, and observe, any such restrictions on the distribution of this Prospectus and the offering and sale of Bonds.

The Bonds may not be a suitable investment for all investors. Each potential investor in the Bonds must determine the suitability of that investment in light of its own circumstances. In particular, each potential investor may wish to consider, either on its own or with the help of its financial and other professional advisers, whether it:

(i) has sufficient knowledge and experience to make a meaningful evaluation of the Bonds, the merits and risks of investing in the Bonds and the information contained in this Prospectus or any applicable supplement;

(ii) has access to, and knowledge of, appropriate analytical tools to evaluate, in the context of its particular financial situation, an investment in the Bonds and the impact the Bonds will have on its overall investment portfolio;

(iii) has sufficient financial resources and liquidity to bear all of the risks of an investment in the Bonds, including Bonds where the currency for principal or interest payments is different from the potential investor’s currency;

(iv) understands thoroughly the terms of the Bonds and is familiar with the behaviour of financial markets; and

(v) is able to evaluate possible scenarios for economic, interest rate and other factors that may affect its investment and its ability to bear the applicable risks.

Legal investment considerations may restrict certain investments. The investment activities of certain investors are subject to legal investment laws and regulations, or review or regulation by certain authorities. Each potential investor should consult its legal advisers to determine whether and to what extent (a) Bonds are legal investments for it, (b) Bonds can be used as collateral for various types of borrowing and (c) other restrictions apply to its purchase or pledge of any Bonds. Financial institutions should consult their legal advisers or the appropriate regulators to determine the appropriate treatment of Bonds under any applicable risk-based capital or similar rules.

The Bonds have not been and will not be registered under the U.S. Securities Act of 1933, as amended (the Securities Act), or with any securities regulatory authority of any state or other jurisdiction of the United States and the Bonds may not be offered, sold or delivered within the United States or to, or for the account or benefit of, U.S. persons (as defined in Regulation S under the Securities Act (Regulation S)), except pursuant to an exemption from, or in a transaction not subject to, the registration requirements of the Securities Act and any other applicable securities laws. Each purchaser of the Bonds will be deemed to have made the representations described in “Subscription and Sale”.

Page 5

FINANCIAL MODEL

Summary information derived from the results of the financial model in relation to the Project (the Financial Model) which is set out in Appendix 1 of this Prospectus (the Summary Financial Model Information) does not constitute a projection or prediction. A financial model simply illustrates hypothetical results that are mathematically derived from specified assumptions. In addition, the Financial Model shows cash flows available for debt service and does not model individual financial performance under the assumptions set forth therein. Although the revenues, operating, maintenance and capital costs, interests rates and taxes have been modelled in alignment with the Issuer’s most accurate expectation of the Project’s performance as at the date of this Prospectus, it can be expected that these will almost certainly differ from those assumed for the purposes of the Financial Model. Accordingly, actual performance and cash flows for any future period will almost certainly differ from those shown by the results of the Financial Model.

The inclusion of the Summary Financial Model Information herein should not be regarded as a representation by the Issuer or any other person that the results contained in the Financial Model will be achieved. In addition, the Summary Financial Model Information contained herein does not, and does not purport to, restate the Financial Model in its entirety. Prospective investors in the Bonds are cautioned not to place undue reliance on the Financial Model, the Summary Financial Model Information or summary information derived therefrom and should make their own independent assessment of the future results of operations, cash flows and financial condition.

The Summary Financial Model Information was prepared by the Issuer. The Issuer confirms that the Summary Financial Model Information has been accurately reproduced and that, as far as the Issuer is aware and is able to ascertain from the Financial Model, no facts have been omitted which would render the Summary Financial Model Information, in the context of the information contained in the Financial Model, inaccurate or misleading.

Page 6

FORWARD LOOKING STATEMENTS

Certain statements contained in this Prospectus, including any forecasts, projections, descriptions or statements regarding the possible future results of operations, any statement preceded by, followed by or including the words “believes”, “expects”, “plans” or “will” or similar expressions, and other statements that are not historical facts, are or may constitute “forward-looking statements”. Since such statements are inherently subject to risks and uncertainties, actual results may differ from those expressed or implied by such forward-looking statements including, without limitation, any projections included as part of the Summary Financial Model Information prepared by the Issuer and set out in Appendix 1. Although the Issuer believes that the projections contained in this Prospectus are reasonable as at the date of this Prospectus, the Issuer cannot give any assurance that such projections will prove to have been correct.

Important factors that could cause actual results to differ from such projections are disclosed in this Prospectus, including, without limitation, those contained in the section entitled “Risk Factors” and any such projection is qualified in its entirety accordingly.

Each investor in the Bonds offered in this Prospectus will be deemed to have represented and agreed that it has read and understood the description of the assumptions and uncertainties underlying the projections that are set forth in this Prospectus and to have acknowledged that the Issuer is under no obligation to update the information and do not intend to do so.

Save as expressly provided under the terms of the Transaction Documents, the Issuer does not undertake any obligation to release publicly any revision to such forward-looking statements after the date of this Prospectus to reflect later events or circumstances or to reflect the occurrence of unanticipated events. These cautionary statements should be considered in connection with any written or oral forward-looking statements that the Issuer may issue in the future.

All descriptions of documents referred to in this Prospectus are qualified in their entirety by reference to the terms of the original documents.

Page 7

PRESENTATION OF INFORMATION

The Issuer has obtained market and industry data and other statistical information used throughout this Prospectus from its own research, surveys or studies conducted by third parties, independent industry or general publications and other published independent sources. Where information has been sourced from a third party, such as industry publications and surveys that generally state that they have obtained information from sources believed to be reliable, but do not guarantee the accuracy and completeness of such information, Issuer confirm that such information has been accurately reproduced and, as far as it is aware and are able to ascertain from such information, no facts necessary for the review of such information for the purpose for which it was included herein have been omitted which would render the reproduced information inaccurate or misleading. While the Issuer believes that these industry publications and surveys are reliable, the Issuer has not independently verified such data, and does not make any representations as to the accuracy of such information. Similarly, the Issuer believes that their internal research is reliable, but it has not been verified by any independent sources.

Certain figures included in this Prospectus have been subject to rounding adjustments. Accordingly, figures shown as totals in certain tables may not be an exact arithmetic aggregation of the numbers that precede them. Percentage figures included in this Prospectus have not in all cases been calculated on the basis of such rounded figures but on the basis of such amounts prior to rounding. For this reason, certain percentage amounts in this Prospectus may vary from those obtained by performing the same calculations using the figures in the relevant financial statements. Certain other amounts that appear in this Prospectus may not sum due to rounding.

Any information available on any website referred to in this Prospectus shall not form part of this Prospectus.

DEFINED TERMS

All capitalised terms used in this Prospectus and not otherwise defined in this Prospectus (including the Conditions) have the meanings assigned to them in the Glossary.

LON29133735/2+

Page 8

CONTENTS

Page

OVERVIEW OF THE PROJECT .................................................................................................................................. 9

OVERVIEW OF THE BONDS.................................................................................................................................... 13

TRANSACTION STRUCTURE.................................................................................................................................. 21

RISK FACTORS ........................................................................................................................................................ 22

USE OF PROCEEDS.................................................................................................................................................. 38

DESCRIPTION OF THE ISSUER................................................................................................................................ 39

DESCRIPTION OF THE SHAREHOLDERS .............................................................................................................. 43

DESCRIPTION OF THE PROJECT DOCUMENTS.................................................................................................... 52

DESCRIPTION OF THE FINANCE DOCUMENTS ................................................................................................... 76

DESCRIPTION OF THE PBCE PROVIDER.............................................................................................................. 110

DESCRIPTION OF THE PBCE LETTER OF CREDIT ............................................................................................... 111

CONDITIONS OF THE BONDS................................................................................................................................ 115

CLEARING .............................................................................................................................................................. 137

TAXATION.............................................................................................................................................................. 138

SUBSCRIPTION AND SALE.................................................................................................................................... 143

GLOSSARY ............................................................................................................................................................. 147

GENERAL INFORMATION..................................................................................................................................... 172

APPENDIX 1 SUMMARY FINANCIAL MODEL INFORMATION ................................................................ 174

Page 9

OVERVIEW OF THE PROJECT

This overview highlights selected information appearing elsewhere in this Prospectus. This overview does not contain all of the information that is important to prospective investors in the Bonds or that prospective investors should consider in making an investment decision and is qualified in its entirety by, and should be read in conjunction with, the more detailed information, including information in the appendices hereto, appearing elsewhere in this Prospectus. Prospective investors should carefully consider the information set forth under “Risk Factors” herein. In addition, certain statements are forward-looking statements which involve risks and uncertainties. See “Forward Looking Statements”.

Background

On 8 April 2010, the Authority, Agentschap Wegen & Verkeer (represented for the purposes of the bid procedure by Via-Invest Vlaanderen NV (Via-Invest)), invited tenders for the design, build, finance and maintenance of the Road (as defined below) (the Project).

Via Brugge NV, a consortium made up of Ondernemingen Jan De Nul NV, Aswebo NV, Aclagro NV, Algemene Aannemingen Van Laere NV, Franki Construct NV and DG Infra+ NV, was selected as “preferred bidder” on 21st December 2012. Via Brugge NV submitted the building permit file on 8 May 2013. The building permit (the Building Permit) was issued on 25 October 2013 and all environmental permits have been issued (the last of which, relating to 2 bridges), was granted on 20 January 2014). The challenge period of one month relating to such permits has expired without any claim against the issue of permits being made.

The Project

The Project is part of the Flemish "Missing Link" package of Public Private Partnership (PPP) projects. It involves the design, build, finance and maintenance of the A11 road connection / port bypass ("havenrandweg") between the provincial N49 (the Natiënlaan, at the Westkapelle residential district in Knokke) and the N31 (at the Blauwe Toren in Bruges) (the Road).

Page 10

The main line of the missing link is approximately 13 km long and is part of the Trans-European Transport Network (TEN-T). It will create a fast connection between the port of Bruges-Zeebrugge with the hinterland, as well as improving recreational access to the west coast and optimising access to the Bruges regional urban area. The Road will be aligned south west – north east and connected through three junctions to the underlying road network. In the south west, the A11 will be connected to the N31 (in the direction of Bruges and Zeebrugge). The existing junction with the Blankenbergsesteenweg will be adjusted. In the north east, at the junction with the Natiënlaan, the access to the port of Bruges-Zeebrugge from the N49 will be improved. Roughly halfway along the A11 route, a junction complex will be created allowing access to the eastern part of the port. Over the Boudewijn Canal a new twin movable bridge will be built on the A11 that will guarantee continued access for sea-going ships to the inner harbour.

The Project incorporates nearly 90 civil engineering structures, including twin bascule bridges, a viaduct and three tunnels. Via Brugge intends to design and construct the Infrastructure (primarily consisting of the main road) and Third Party Infrastructure (primarily consisting of adjacent cycle paths and connecting roads) within 41.5 months (3.5 years). The Infrastructure is then to be maintained for 30 years.

The Principal Project Parties

The Contractor (the Issuer)

The design, build, finance and maintenance of the Road will be managed by the Issuer, a special purpose vehicle owned by Via Brugge NV (60.67 %) and Via-Invest (39.33 %).

Via Brugge NV is a special purpose vehicle recently incorporated under Belgian law, owned by a consortium of seven shareholders: Ondernemingen Jan De Nul NV (Jan De Nul), Asfalt-, Wegenis- en Bouwwerken NV (Aswebo), Aclagro NV (Aclagro), Inframan NV (Inframan ), Algemene Aannemingen Van Laere NV (Van Laere), Franki Construct NV (Franki ) and DG Infra+ NV (DG Infra+ ) (together the Consortium).

The members of the Consortium have together both local and international civil and road construction experience and expertise. In particular, in 2011 members of the Consortium reached financial close on the Via-Invest Vlaanderen NV PPP road project "Kempen north-south missing link" (Jan De Nul and Aswebo) and "R4 Gent" (DG Infra+), and both projects are currently under construction, with the respective Consortium members working closely with Via-Invest.

Via-Invest is a shareholder in the Issuer, with 51% of its shares held by the government-owned independent investment company PMV and 49% of its shares held by Agentschap Wegen & Verkeer.

Page 11

The Sub-Contractors

The parties to the EPC Contract are the Issuer and a joint venture vehicle composed of (i) Jan De Nul, (ii) Van Laere, (iii) Aswebo, (iv) Aclagro and (v) Franki (the EPC Contractor).

The parties to the Maintenance Contract are the Issuer and a joint venture vehicle composed of (i) Jan De Nul, (ii) Van Laere, (iii) Aswebo, (iv) Aclagro, and (v) Franki (the MTC Contractor ).

The MTC Contractor and the EPC Contractor comprise the same parties, which should limit issues as regards to the interface between construction and maintenance.

Under Belgian law, a “tijdelijke handelsvennootschap” or joint venture vehicle (a JVV ) is a temporary (commercial) partnership whose partners are jointly and severally liable for the JVV’s obligations.

The Maintenance Contract includes the possibility for the MTC Contractor to set-up a special purpose vehicle (Maintain Co) in the form of a limited liability company under Belgian law, prior to the Availability Date, on conditions to be specified by the Issuer and the Financiers in order to bring the Issuer into a position that is neither better nor worse than if the Maintenance Contract were not transferred to Maintain Co.

Contractual Structure

Overview

The Project follows the internationally recognised DBFM (Design, Build, Finance and Maintain) structure, pursuant to which the Authority will enter into the DBFM Agreement with the Issuer.

The Issuer in turn will enter into the EPC Contract and the Maintenance Contract. These contracts are back-to-back with the provisions of the DBFM Agreement for the design and construction of the Infrastructure and the Third Party Infrastructure, and the maintenance of the Infrastructure, respectively. The EPC Contract therefore passes (subject to agreed liability caps) to the EPC Contractor the design and construction risks, liabilities and obligations assumed by the Issuer in the DBFM Agreement, and the Maintenance Contract passes (subject to agreed liability caps) to the MTC Contractor the risks, liabilities and obligations of the Issuer contained in the DBFM Agreement which relate to the repair, maintenance and hand-back of the Infrastructure. See the section entitled Description of Project Documents for further information.

Independent Technical Review

The design, construction and maintenance proposals developed by Via Brugge NV have been independently reviewed by Steer Davies Gleave (in that capacity, the Technical Adviser) which has been appointed to act as independent technical adviser to Via Brugge NV.

Design and Construction

The design and construction of the Infrastructure and Third Party Infrastructure is to be undertaken by the EPC Contractor in accordance with the terms of the EPC Contract. The EPC Contract operates on a fixed-price, fixed-term, lump-sum, turnkey basis, back-to-back with the provisions of the DBFM Agreement and supported by a construction performance security package.

The specification for the works (the Technical Specification) is that provided by the Authority and supplemented by Via Brugge NV during the procurement process, and the Issuer will not permit any variation from the Technical Specification unless it is approved by the Authority. The Authority has opted for an integral approach, whereby traffic related, ecological, landscape and spatial aspects must be considered in a satisfactory manner in the development of the Road. This implies, inter alia, the taking of necessary action to mitigate the effects on the environment, the fitting into the landscape of the main road, qualitative solutions for interactions with and modifications of underlying networks.

Jan De Nul as main shareholder in the EPC Contractor and MTC Contractor is taking the lead management of the Project, meaning that key management functions such as project director, process manager, engineering manager, lead project managers and accounting manager will be performed by experienced Jan De Nul persons.

Construction works are estimated to start on 21 March 2014, with a total construction period of 41.5 months, this gives a target Completion Date of 5 September 2017. At this point, the Road shall be complete and a Completion Certificate should be issued to the Issuer.

Page 12

The design phase commenced in June 2013 and preparation works such as those relating to relocation of cables and ducts, archaeological investigations and geotechnical investigations have been proceeding since April 2013.

Operation and Maintenance

Maintenance of the Infrastructure is to be undertaken by the MTC Contractor for a 30-year period in accordance with the terms of the Maintenance Contract.

The Maintenance Contract obligations are back-to-back with the provisions of the DBFM Agreement and supported by a construction performance security package.

The Issuer's principal obligation under the Maintenance Contract is payment of the agreed sums representing the Maintenance Fee. These sums are indexed quarterly in accordance with a specific price revision formula in line with the price revision formula applicable to the availability payments under the DBFM Agreement (see Remuneration of the Issuer below).

Major maintenance primarily comprises renewal of asphalt wearing course at 15 year intervals, renewal of structural asphalt at 24 years, renewal of asphalt base in slow lane at 24 years, road markings at 3 year intervals, painting bascule bridges at 6 year intervals, renewal of tunnel lighting at years 12 and 24 and revision of hydraulic jacks of bascule bridges at year 20.

The Maintenance Reserve Account in the Original Financial Model is designed to ensure that funds will be available when necessary for the Issuer to fulfil its payment obligations in relation to heavy maintenance under the DBFM Agreement.

Remuneration of the Issuer

As from the Availability Date, when the Infrastructure is completed (which is expected to be 5 September 2017), the DBFM Agreement grants the Issuer the right to receive periodic availability payments (“Beschikbaarheidsvergoeding”), payable quarterly, amounting to 90% of full availability payments. The remaining 10% of availability payments is only payable from the Completion Date (when both the Infrastructure and Third Party Infrastructure are completed).

Availability payments are linked to meeting performance and quality targets. Accordingly, the Project must be operated and maintained to certain standards, with various penalties deductible if these standards are not fully met.

The Project, therefore, carries construction and availability risk for the Issuer. However, no traffic demand risk element is contained in the DBFM Agreement.

Page 13

OVERVIEW OF THE BONDS

The following overview does not purport to be complete and is taken from, and qualified in its entirety by, the remainder of the Prospectus and the terms and conditions of the Bonds set out in the section entitled “Terms and Conditions of the Bonds” (the Conditions).

Words and expressions defined in the Conditions shall have the same meanings in this section. If such words and expressions used in this section are not defined in the Conditions, they shall have the meaning given to them in the “Glossary”.

Issuer: Via A11 NV a Belgian public limited liability company (naamloze vennootschap/société anonyme) (see “Description of the Issuer”).

Initial Shareholders: Via Brugge NV, and Via-Invest.

Bond Trustee: Deutsche Trustee Company Limited.

Security Trustee: Deutsche Trustee Company Limited.

Principal Paying Agent: Belfius Bank SA/NV.

Account Bank: Deutsche Bank AG, Brussels Branch.

Account Operator Deutsche Bank AG, London Branch.

Project Agent: Deutsche Bank AG, London Branch.

PBCE Provider: European Investment Bank (see “Description of the PBCE Provider”).

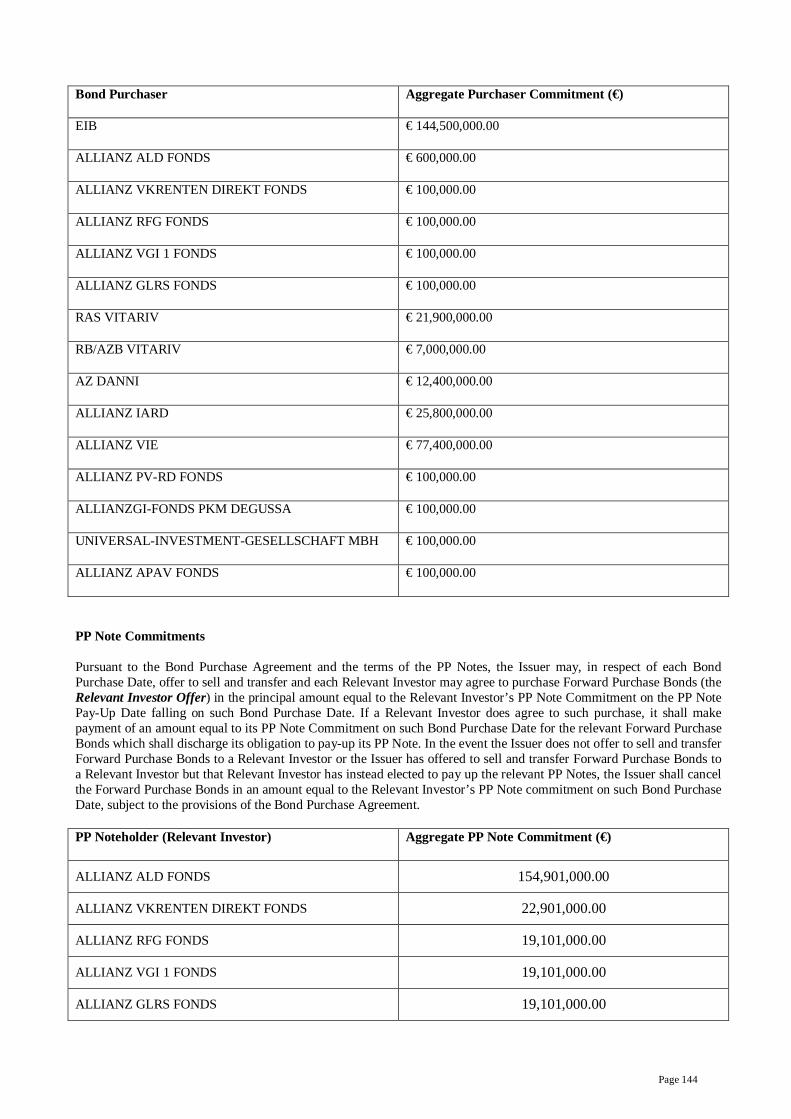

Bond Purchasers European Investment Bank, Allianz IARD, Allianz Vie and Allianz Global Investors Europe GmbH acting on behalf of Allianz Ald Fonds, Allianz Vkrenten Direkt Fonds, Allianz RFG Fonds, Allianz VGI 1 Fonds, Allianz GLRS Fonds, Allianz PV-RD Fonds, Allianzgi-Fonds PKM Degussa, Universal-Investment-Gesellschaft MBH and Allianz Apav Fonds, and Allianz S.p.A. acting in the interests of Ras Vitariv, RB/AZB Vitariv and AZ Danni (together, the Original Bond Purchasers).

Description of Bonds: €577,900,000 4.49 per cent. Secured Amortising Bonds due 2045, to be issued by the Issuer on the Issue Date.

Issue Date: 20 March 2014.

Issue Process and Use of Proceeds:

The Bonds will be issued on the Issue Date. Pursuant to the terms of the Bond Purchase Agreement the Initial Issue Bonds will be subscribed and paid for on the Issue Date by the Bond Purchasers and the Forward Purchase Bonds will be subscribed and paid for on issue by Deutsche Bank and then on the Issue Date will be repurchased by the Issuer and transferred to Deutsche Bank AG, London Branch (the Bond Custodian) to be held for and on behalf of the Issuer. Pursuant to the Bond Purchase Agreement, certain of the Bond Purchasers have agreed to purchase the Forward Purchase Bonds from the Issuer on each Bond Purchase Date. The Issuer will use the proceeds of sale of the Initial Issue Bonds on the Issue Date and the proceeds received on sale of the Forward Purchase Bonds on each Bond Purchase Date to fund the Project Costs. (see “Use of Proceeds” below).

Form and Denomination of the Bonds:

The Bonds will be issued in dematerialised form in denominations of €100,000. The Bonds will be issued in dematerialised form in accordance with Article 468 and following of the Belgian Code of Companies will be are represented by a book-entry in the records of the X/N System operated by the National Bank of Belgium (the NBB) and will be credited to the accounts held with the X/N System by Euroclear, Clearstream, Luxembourg or other X/N

Page 14

System participants for credit by Euroclear, Clearstream, Luxembourg or other X/N System participants to the securities accounts of their subscribers.

The Bonds will be accepted for clearance through the X/N System, and are accordingly subject to the applicable Belgian clearing regulations, including the NBB System Regulations.

Up to and including the final Bond Purchase Date, the Bonds shall be credited to and held with the securities accounts of the relevant holders at Euroclear. Following the final Bond Purchase Date, the Bonds shall be eligible to be credited to securities accounts of the holders held with Euroclear, Clearstream, Luxembourg or other participants in the X/N System.

Final Redemption Date: 30 September 2045.

Average life: 20.69 years.

Bond Trust Deed: The Bonds will be constituted by, and issued subject to, the Bond Trust Deed (see “Description of the Finance Documents”).

PBCE Letter of Credit: The PBCE Provider will undertake to make available the PBCE Letter of Credit, in an amount up to the PBCE Maximum Balance, as a form of subordinated credit enhancement in relation to the Bonds and the PP Notes under, and in accordance with the terms of, the PBCE Agreement. Under the terms of the PBCE Agreement, the PBCE Provider has undertaken to make available amounts under the PBCE Letter of Credit in the following circumstances (subject in all cases to the PBCE Available Amount):

(a) PBCE Funding Shortfall: to make payment either of certain cash shortfalls, or in respect of Debt Service on the Bonds and the PP Notes (if the Technical Adviser reasonably believes that the PBCE Longstop Date can be met and certain other conditions are satisfied) following a PBCE Funding Shortfall during the Construction Phase;

(b) Debt Service: to make scheduled interest and principal payments in relation to the Bonds and PP Notes if there is insufficient cash available to the Issuer for such purposes;

(c) PBCE Rebalancing Events: if a PBCE Rebalancing Event (as defined below) occurs, during the Availability Phase, to make payment of mandatory partial redemption amounts in respect of the Bonds and PP Notes; or

(d) Accelerated Payments: provided no PBCE Rebalancing has previously occurred, to make accelerated payments (excluding any make-whole amount, costs or indemnities associated therewith) in relation to the Bonds and PP Notes if there is insufficient cash available to the Issuer for such purposes following acceleration of the Bonds,

all as more particularly described in the PBCE Agreement (see the section entitled “Description of the PBCE Letter of Credit”).

PP Notes: On the Issue Date, the Issuer will issue €287,509,000 4.49 per cent. unlisted partly paid notes to certain investors (the PP Noteholders and Relevant Investors). On issue each PP Note will be paid up as to €1,000.

The PP Notes shall rank pari passu with the Bonds. The PP Notes will not be listed.

Pursuant to the terms and conditions of the PP Notes, the PP Noteholders shall pay-up the PP Notes in specified amounts on dates corresponding to the Bond

Page 15

Purchase Dates (PP Note Pay-Up Dates).

If the Issuer offers Forward Purchase Bonds to the Relevant Investors prior to any Bond Purchase Date in a principal amount equal to the amount to be paid-up on such PP Note Pay-Up Date and the Relevant Investor accepts such offer, the obligation to pay up the relevant PP Notes shall be discharged by purchasing such Forward Purchase Bonds on such date.

Security: The Bondholders (and the other Secured Creditors) will have the benefit of the following security granted by the Issuer, the Shareholders and the Shareholder Lenders in favour of the Security Trustee (together, the Transaction Security):

(a) security granted by the Issuer over its rights in respect of the Transaction Documents to which it is a party, credit rights deriving from its bank accounts, rights over its receivables and other rights as listed in the Issuer Security Documents;

(b) security granted by the Shareholder Lenders in respect of rights over its receivables in connection with the Shareholder Loan Agreements; and

(c) security granted by HoldCo and Via-Invest over their respective shares held in the Issuer.

The rights of the Bond Trustee to take Enforcement Action in respect of the Transaction Security will be restricted by the provisions of the STID (see the section entitled “Description of the Finance Documents – Security Trust and Intercreditor Deed - Enforcement Action”).

Secured Creditors: The Secured Creditors will be the Security Trustee, the Bond Trustee, the Bondholders, the PP Noteholders, the PBCE Provider, the Principal Paying Agent, each Paying Agent, the Project Agent, the Bond Custodian, the Bond Purchasers, the Account Operator and the Account Bank.

STID: The Bonds will be subject to, and have the benefit of the STID (see “Description of the Finance Documents”). The STID will regulate (i) the claims of the Secured Creditors; (ii) the exercise, acceleration and enforcement of rights by the Secured Creditors; (iii) the rights of the Secured Creditors to instruct the Security Trustee; and (iv) the giving of consents and waivers and the making of modifications to the Security Documents, the Common Terms Agreement and the other Transaction Documents including, in particular, the basis on which votes of the Secured Creditors will be counted for the purpose of determining whether the Security Trustee may provide consents or waivers or approve modifications.

The STID will provide for decisions to be made according to certain majorities and quorums. Decisions may be Discretion Matters, Ordinary Voting Matters, Extraordinary Voting Matters or QC Voting Matters and each type of decision is subject to different requirements as to majorities and/or quorums. Under the STID, certain rights of the PBCE Provider against the Issuer under the PBCE Agreement are subordinated to rights of the Bondholders against the Issuer under the Bonds.

Enforcement Action (including acceleration of the Bonds) will not be permitted:

(a) in circumstances where there is no amount available for drawing under the PBCE Letter of Credit, without the prior written consent of the PBCE Provider as a result of a DSCR Default or MRA Default if the most recent PBCE PLCR is equal to or greater than 1.20:1; or

(b) as a result of:

(i) a DSCR Default;

(ii) an MRA Default; or

Page 16

(iii) a failure to pay on the due date any amount payable pursuant to a Finance Document at the place at and in the currency in which it is expressed to be payable,

if any amount remains available for drawing under the PBCE Letter of Credit; or

(c) without the prior written consent of the PBCE Provider, in circumstances where a drawing under the PBCE Letter of Credit for a PBCE Funding Shortfall is requested by the Issuer pursuant to Part B of Schedule 5 of the Common Terms Agreement before the PBCE Longstop Date, in relation to any Event of Default which was subsisting, or had occurred, and of which Bond Creditors had notice as at the date of such notice by the Issuer to the Bond Trustee pursuant to Part B of Schedule 5 of the Common Terms Agreement.

The decision to take Enforcement Action may only be taken by holders of Qualifying Debt (which includes (i) the outstanding principal amount of the Bonds, (ii) the Outstanding Purchaser Commitments (as defined below) under the Bond Purchase Agreement, (iii) amounts paid up on the PP Notes and outstanding commitments to pay up the PP Notes and (iv) drawn and outstanding principal amounts under the PBCE Letter of Credit) passing a QC Resolution (see Condition 8.2 (Events of Default)).

The STID will also provide for the ranking (in point of payment) of the claims of the Secured Creditors following the taking of Enforcement Action.

Interest Payments: Interest will accrue on the Bonds at a rate of 4.49 per cent. per annum from (and including) the Issue Date. Interest is payable:

(a) from and including the Issue Date to and including 31 March 2018, quarterly in arrear each 31 March, 30 June, 30 September and 31 December; and

(b) thereafter, from and including 30 September 2018, semi-annually in arrear on 31 March and 30 September in each year,

(each a Payment Date).

Scheduled Redemption of the Bonds:

The Bonds will be redeemed in instalments on each Payment Date from and including 31 March 2018 (see Condition 4.2 (Redemption, Purchase and Cancellation - Scheduled Redemption)). To the extent not previously redeemed, the Bonds will be redeemed at their Principal Amount Outstanding on the Final Redemption Date.

Optional redemption of the Bonds:

On giving not fewer than 30 nor more than 60 days’ notice to the Bondholders, the Principal Paying Agent and the Bond Trustee, the Issuer may (subject to the satisfaction of certain conditions) in accordance with the Conditions redeem the Bonds in whole or in part on any Payment Date at their Principal Amount Outstanding together with accrued and unpaid interest and the applicable Voluntary Redemption Make-Whole Amount (see Condition 4.3 (Redemption, Purchase and Cancellation - Optional Redemption)).

Optional redemption for tax reasons; illegality:

On giving not fewer than 30 but not more than 60 days’ notice to (among others) the Bondholders and the Bond Trustee, the Issuer may, in accordance with the Conditions, redeem all, but not some only, of the Bonds at their Principal Amount Outstanding together with accrued and unpaid interest on the date set out in the circumstances in the circumstances set out below (subject to satisfaction of certain conditions):

(a) where the Issuer is or will be obliged to make any withholding or deduction from payments and pay additional amounts in respect of the

Page 17

Bonds pursuant to Condition 6 (Taxation); or

(b) it is illegal for the Bonds to remain outstanding or unlawful for the Issuer to perform its obligations under the Finance Documents; and

(c) despite using all reasonable endeavours to avoid the event described in (a) or (b) above, the Issuer is unable to do so.

See Condition 4.4 (Redemption, Purchase and Cancellation - Optional Redemption for Tax Reasons; Illegality).

Mandatory Redemption of the Bonds:

The Issuer shall, subject to certain conditions, redeem the Bonds (in whole or in part) on the relevant Payment Date next following the occurrence of a PBCE Rebalancing Event (see Condition 4.5 (Mandatory Redemption - PBCE Rebalancing Event)).

A PBCE Rebalancing Event will be deemed to have occurred in respect of a Payment Date, during the Availability Phase, if on such Payment Date, the PBCE Letter of Credit has been drawn to pay Debt Service, and:

(a) the BLCR as at that Payment Date is below 1.10:1; or

(b) on that Payment Date, the sum of:

(i) the amount of the PBCE Letter of Credit drawn to pay Debt Service (as calculated in accordance with Clause 1.4 of Part C (Debt Service Procedure and PBCE Drawing Mechanism for Debt Service Shortfalls) of the Common Terms Agreement), plus

(ii) all amounts previously drawn under the PBCE Letter of Credit and not repaid by the Issuer pursuant to Clause 4.1(a)(i) (Reimbursement) of the PBCE Agreement,

exceeds an amount equal to 50 per cent. of the Debt Service falling due on that Payment Date; or

(c) there has been a drawing under the PBCE Letter of Credit to pay Debt Service in respect of the previous three consecutive Payment Dates; or

(d) if:

(i) the PBCE Rebalancing Historic DSCR as at that Payment Date is 0.85:1, or below;

(ii) the PBCE Provider confirms in writing not later than 30 Business Days following that Payment Date to the Issuer, Bond Trustee and the Project Agent that, in its discretion, it wishes to designate a PBCE Rebalancing Event on the immediately following Payment Date in respect of which the PBCE Rebalancing Historic DSCR was 0.85:1, or below; and

(iii) the PBCE Provider has not delivered a further notice in writing prior to the day which is the 25th Business Day prior to the next Payment Date to the Issuer, the Bond Trustee and the Project Agent confirming that it is revoking such previous designation on the basis that the Issuer has demonstrated to its satisfaction that the PBCE Rebalancing Historic DSCR will no longer be less than 0.85:1 on the next Payment Date,

provided that no PBCE Rebalancing Event shall be deemed to have occurred as a

Page 18

result of paragraphs (a) or (d) above for so long as a dispute is continuing in relation to any Assumption or calculation relating to the BLCR level or the PBCE Rebalancing Historic DSCR level which has not been finally determined in accordance with the provisions of the Finance Documents.

Following the occurrence of a PBCE Rebalancing Event, the Issuer shall, on giving not fewer than 5 nor more than 15 days’ notice to the Bondholders (in accordance with Condition 11 (Notices)), to the Principal Paying Agent and to the Bond Trustee, redeem the Bonds in part on the next Payment Date following the occurrence of the PBCE Rebalancing Event in an amount equal to the Bondholders’ Proportion of the PBCE Rebalancing Amount. Such amount shall be applied to reduce the Principal Amount Outstanding of each Bond and applied to reduce each remaining Amortisation Amount pro rata in accordance with Condition 4.2 (Scheduled Redemption).

The PBCE Rebalancing Amount shall be an amount equal to the available amounts under the PBCE Letter of Credit drawn down on the Payment Date next following the occurrence of the PBCE Rebalancing Event (less, if any, the amount to be drawn down under the PBCE Letter of Credit to pay Debt Service on such Payment Date).

Bondholders’ Proportion means the proportion which the Principal Amount Outstanding of the Bonds bears to the aggregate Principal Amount Outstanding of the Bonds and the PP Notes.

Common Terms Agreement: The Issuer, the PBCE Provider, the Bond Trustee, the Security Trustee, the Project Agent, the Account Operator and the Account Bank will enter into a common terms agreement on the Issue Date (the Common Terms Agreement) pursuant to which the Secured Creditors will have the benefit of common representations, covenants and events of default.

Project Accounts: The Issuer will be required to maintain the Proceeds Account, the Insurance Proceeds Account, the Maintenance Reserve Account, the Debt Service Reserve Account and the Distributions Account with the Account Bank in accordance with the terms of the Account Bank Agreement and the Common Terms Agreement.

Debt Service Reserve Account: The Issuer will be required to maintain a minimum balance in the Debt Service Reserve Account (or DSRA) with the Account Bank, which balance, on satisfaction of certain conditions, will be available to make payments in respect of the Bonds. The DSRA Required Balance equals, on each Test Date after the final Bond Purchase Date, the aggregate of all scheduled interest payments and principal payments in respect of the Bonds until (and including) the next Payment Date. (See “Description of the Finance Documents – Common Terms Agreement – Debt Service Reserve Account”).

Maintenance Reserve Account: The Issuer will be required to maintain a minimum balance in the Maintenance Reserve Account with the Account Bank, which balance, if needed will be available to make payments in respect of lifecycle maintenance expenditure. The MRA Required Balance equals, the amount shown in the Operating Financial Model as the credit balance that should be maintained on the Maintenance Reserve Account, being:

(a) 100 per cent. of the lifecycle maintenance costs during the next 12 months commencing on the Test Date in respect of which the Operating Financial Model was prepared;

(b) 66.67 per cent. of the lifecycle maintenance costs during the period from the date that is 12 months after the Test Date in respect of which the Operating Financial Model was prepared to (but excluding) the date that is 24 months after the Test Date in respect of which the Operating Financial Model was prepared; and

Page 19

(c) 33.33 per cent. of the lifecycle maintenance costs during the period from the date that is 24 months after the Test Date in respect of which the Operating Financial Model was prepared to (but excluding) the date that is 36 months after the Test Date in respect of which the Operating Financial Model was prepared.

See “Description of the Finance Documents – Common Terms Agreement– Maintenance Reserve Account”.

Status of the Bonds: The Bonds are direct, secured and unconditional obligations of the Issuer and (subject as provided above) will rank pari passu, without any preference among themselves and with the PP Notes.

Meetings of Bondholders: The Conditions and the Bond Trust Deed contain provisions for calling meetings of Bondholders to consider matters affecting their interests generally. Subject to the provisions of the STID, these provisions permit defined majorities to bind all Bondholders including Bondholders who did not attend (or were not represented) and did not vote at the relevant meeting and Bondholders who abstained or voted in a manner contrary to the majority.

Modification, Waiver and Substitution:

The Bond Trustee may without the consent of Bondholders, agree to, and direct the Security Trustee to agree to, any modification of (subject to certain exceptions), or to the waiver or authorisation of any breach or proposed breach of, any of the provisions of Bonds or the other Finance Documents in the circumstances contemplated by and subject to the Conditions, the Bond Trust Deed and the STID.

Withholding Tax and additional amounts:

The Issuer will pay such additional amounts as may be necessary in order that the net amounts received by each Bondholder after withholding or deduction for any taxes imposed by tax authorities in Belgium upon payments made by or on behalf of the Issuer in respect of the Bonds, shall equal the amount which would have been receivable in respect of the Bonds in the absence of any such withholding or deduction, subject to customary exceptions, as described in Condition 6 (Taxation).

Listing, approval and admission to trading:

Application has been made to the CSSF to approve this Prospectus as a prospectus and to the Luxembourg Stock Exchange for the listing of the Bonds on the Official List of the Luxembourg Stock Exchange and admission to trading on the Luxembourg Stock Exchange’s regulated market.

Governing law: The Bonds (other than any matter relating to title to, and the dematerialised form of, the Bonds), the Bond Trust Deed, the Common Terms Agreement, the PBCE Letter of Credit, the PBCE Agreement, the Account Bank Agreement, the Bond Custody Agreement, the Project Agent Services Agreement, the Bond Purchase Agreement, the PP Notes, the PP Note Subscription Agreement and the STID and any non-contractual obligation arising out of or in connection with them will be governed by, and construed in accordance with, English law. Certain of the Security Documents, the Clearing Agreement and other Transaction Documents and any matter relating to title to, and the dematerialised form of, the Bonds will be governed by Belgian law.

Credit Ratings: The Bonds are expected, upon issue, to be rated A3 by Moody’s. A security rating is not a recommendation to buy, sell or hold securities and may be subject to revision, suspension or withdrawal at any time by the assigning rating organisation.

Risk Factors: There are certain factors that may affect the Issuer’s ability to fulfil its obligations under the Bonds. In addition, there are certain factors which are material for the purpose of assessing the market risks associated with the Bonds. These include the fact that the Bonds may not be a suitable investment for all investors and certain market risks. See “Risk Factors” below.

Page 20

Page 21

TRANSACTION STRUCTURE

The following structure diagram does not purport to be complete and is taken from, and is qualified in its entirety by, the remainder of this Prospectus. Words and expressions defined elsewhere in this Prospectus shall have the same meanings in this structure diagram. The following diagram sets out the current ownership structure of the Issuer and also illustrates major contractual relationships currently in place for the Project and its financing.

Page 22 ( ( ( (

RISK FACTORS

The Issuer believes that the following factors may affect its ability to fulfil its obligations under the Bonds. All of these factors are contingencies which may or may not occur and the Issuer is not in a position to express a view on the likelihood of any such contingency occurring.

In addition, factors which are material for the purpose of assessing the market risks associated with the Bonds are listed below.

The Issuer believes that the factors described below represent the principal risks inherent in investing in the Bonds, but the inability of the Issuer to pay interest, principal or other amounts on or in connection with the Bonds may occur for other reasons which may not be considered significant risks by the Issuer based on information currently available to it or which it may not currently be able to anticipate. Prospective investors should also read the detailed information set out elsewhere in this Prospectus and reach their own views prior to making any investment decision.

Factors with respect to the Project Documents

Reliance on other parties

Risks that are not specifically and expressly borne by the Authority (or any successor thereto) under the DBFM Agreement are borne by the Issuer. Some of these risks are passed on in whole or in part (and subject to limits on liability) to insurers, the EPC Contractor under the EPC Contract or the MTC Contractor under the Maintenance Contract, with interfaces between the EPC Contractor and the MTC Contractor being dealt with in the Interface and Coordination Contract. However, to the extent that the Authority, the insurers, the EPC Contractor or the MTC Contractor fail to meet their obligations in respect of risks that have been assumed by them, or claims by the Issuer exceed the insured amounts or limits on liability, or such risks are not effectively passed on by the Issuer, the Issuer will continue to bear these risks. These risks might affect the Issuer's ability to meet its payment obligations under the Bonds.

Direct agreements and step-in rights

Any material change made to a public procurement contract will require a new tender. Case law (from the European Court of Justice, the Pressetext case) suggests that a full new procurement procedure is required in the case of a material change to the initial contract, in particular, if there are changes to the scope and content of the rights and obligations of the parties. This may be the case if the amended terms are likely to have had an influence on the outcome of the award procedure, had they formed a part of the initial procedure, or if a contractor who is awarded a contract by an authority is substituted by a different contractor.

It is therefore possible that the Issuer's replacement, upon the Security Trustee exercising its step-in and cure rights under the Authority Direct Agreement, may qualify as a material change to the DBFM Agreement, requiring a new tender process. This could be a ground for setting aside the DBFM Agreement with the replacement DBFM contract party or as ineffective. The time limit for such a claim to be made is 30 days after the publication of the notice in the Official Journal, or 6 months after the new contract is concluded (if no notice was published). The prospect of the DBFM Agreement being set aside on this basis might adversely affect the ability of the Security Trustee, on behalf of the Finance Parties (which includes the Noteholders), to exercise its step-in and cure rights under the Authority Direct Agreement.