Vermont Electric Energy Efficiency Potential Study – Draft Findings April 10, 2006.

39

Vermont Electric Energy Efficiency Potential Study – Draft Findings April 10, 2006

-

Upload

edwin-hutchinson -

Category

Documents

-

view

213 -

download

0

Transcript of Vermont Electric Energy Efficiency Potential Study – Draft Findings April 10, 2006.

Vermont Electric Energy Efficiency Potential Study –

Draft Findings

Vermont Electric Energy Efficiency Potential Study –

Draft Findings

April 10, 2006

GDS Associates, Inc. 2

Overview of PresentationOverview of Presentation

• Key findings from draft report of April 9, 2006– Load forecast for Vermont (1.5% a year before DSM,

1.0% a year after DSM)– mWh savings potential – base case– Sources of electric energy savings potential– Cost effectiveness results– Annual implementation costs– Rate impacts

• Key assumptions• Findings by Sector

GDS Associates, Inc. 3

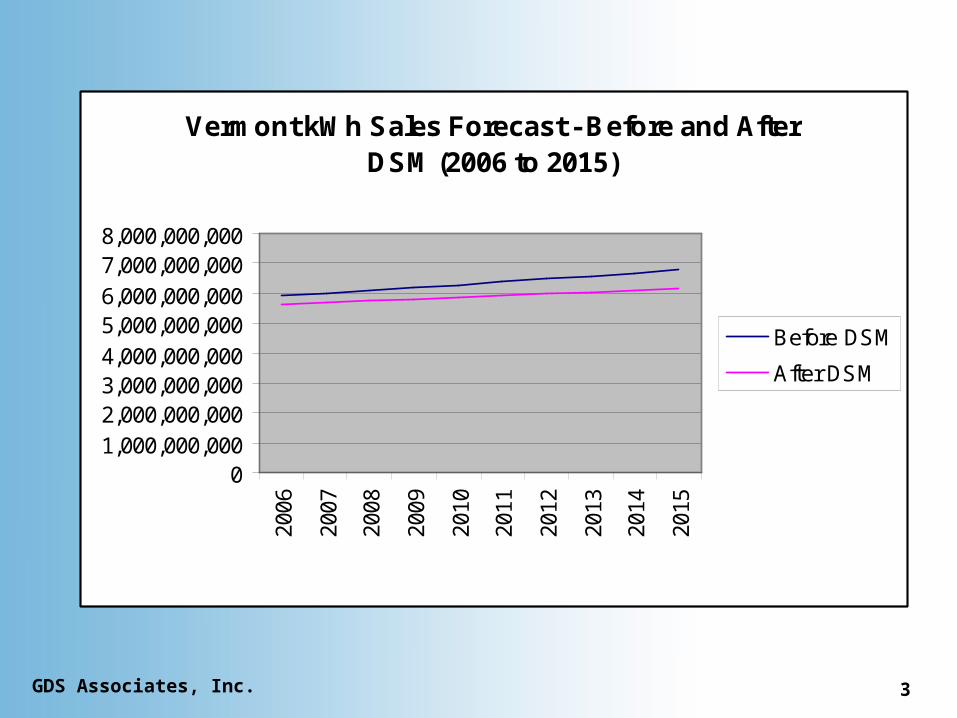

Vermont kWh Sales Forecast - Before and After DSM (2006 to 2015)

01,000,000,0002,000,000,0003,000,000,0004,000,000,0005,000,000,0006,000,000,0007,000,000,0008,000,000,000

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

Before DSM

After DSM

GDS Associates, Inc. 4

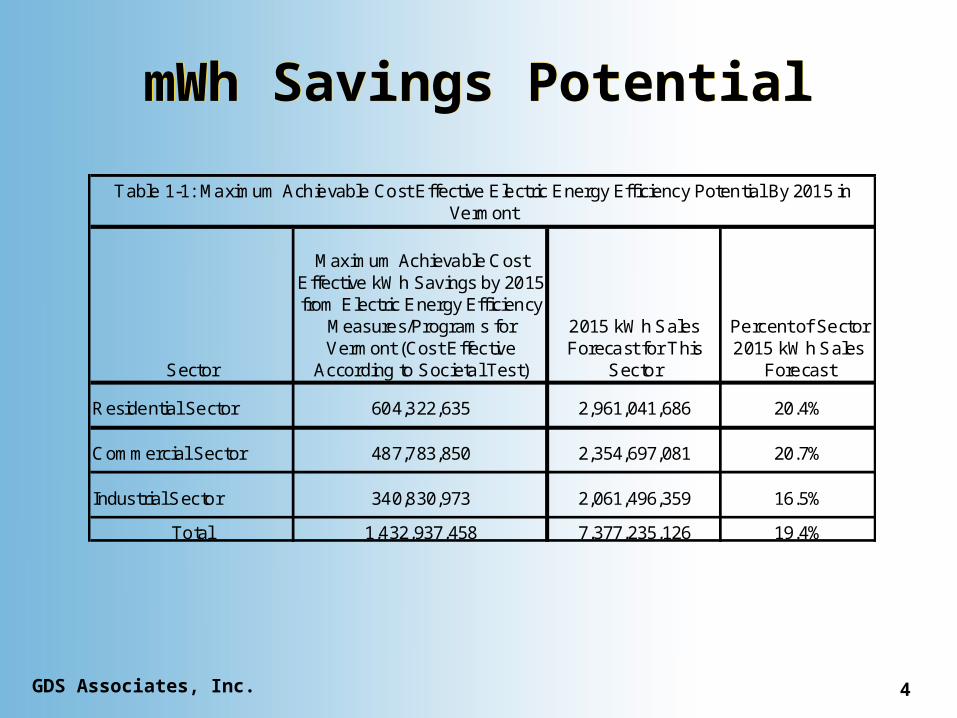

mWh Savings PotentialmWh Savings Potential

Sector

Maximum Achievable Cost Effective kWh Savings by 2015 from Electric Energy Efficiency

Measures/Programs for Vermont (Cost Effective

According to Societal Test)

2015 kWh Sales Forecast for This

Sector

Percent of Sector 2015 kWh Sales

Forecast

Residential Sector 604,322,635 2,961,041,686 20.4%

Commercial Sector 487,783,850 2,354,697,081 20.7%

Industrial Sector 340,830,973 2,061,496,359 16.5%

Total 1,432,937,458 7,377,235,126 19.4%

Table 1-1: Maximum Achievable Cost Effective Electric Energy Efficiency Potential By 2015 in Vermont

GDS Associates, Inc. 5

Key Sources of Savings Potential for Max. Ach Cost Effective Base

Case

Key Sources of Savings Potential for Max. Ach Cost Effective Base

Case• Residential – lighting, electric water

heater fuel conversion, space heat fuel conversion, standby power

• Commercial – lighting, refrigeration, cooling

• Industrial – industrial lamps and fixtures, motors

GDS Associates, Inc. 6

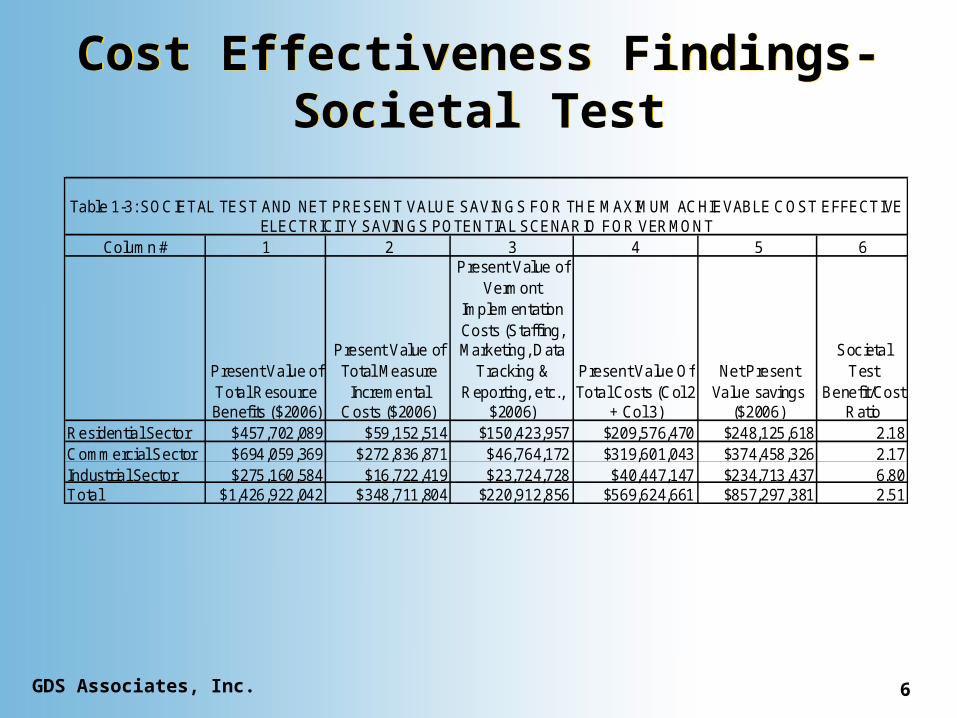

Cost Effectiveness Findings-Societal Test

Cost Effectiveness Findings-Societal Test

Column # 1 2 3 4 5 6

Present Value of Total Resource Benefits ($2006)

Present Value of Total Measure

Incremental Costs ($2006)

Present Value of Vermont

Implementation Costs (Staffing, Marketing, Data

Tracking & Reporting, etc.,

$2006)

Present Value Of Total Costs (Col 2

+ Col 3)

Net Present Value savings

($2006)

Societal Test

Benefit/Cost Ratio

Residential Sector $457,702,089 $59,152,514 $150,423,957 $209,576,470 $248,125,618 2.18Commercial Sector $694,059,369 $272,836,871 $46,764,172 $319,601,043 $374,458,326 2.17Industrial Sector $275,160,584 $16,722,419 $23,724,728 $40,447,147 $234,713,437 6.80Total $1,426,922,042 $348,711,804 $220,912,856 $569,624,661 $857,297,381 2.51

Table 1-3: SOCIETAL TEST AND NET PRESENT VALUE SAVINGS FOR THE MAXIMUM ACHIEVABLE COST EFFECTIVE ELECTRICITY SAVINGS POTENTIAL SCENARIO FOR VERMONT

GDS Associates, Inc. 7

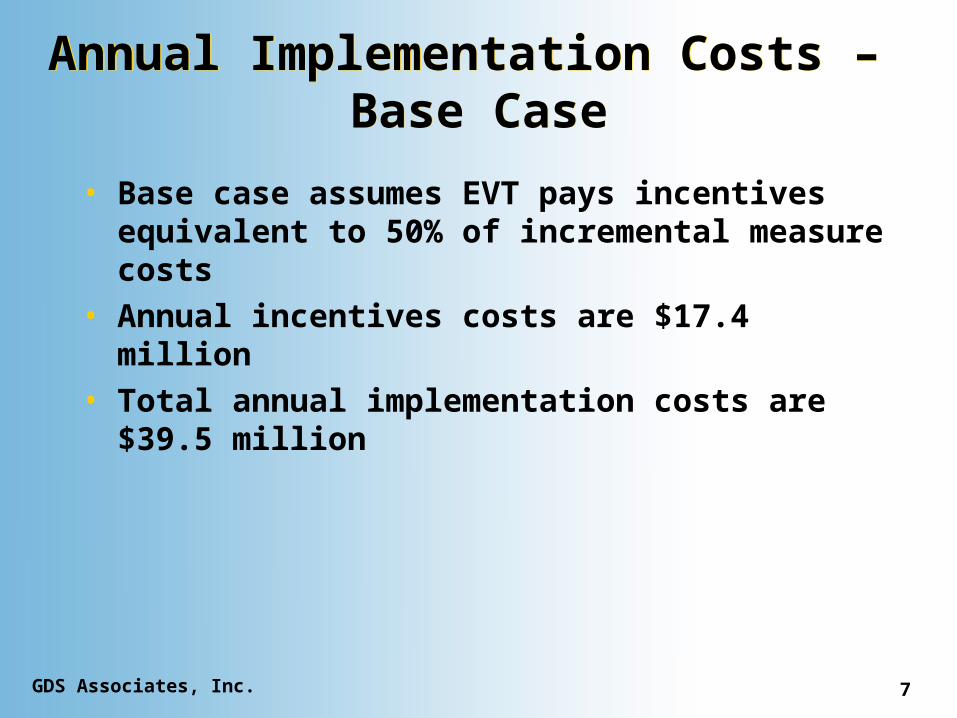

Annual Implementation Costs – Base Case

Annual Implementation Costs – Base Case

• Base case assumes EVT pays incentives equivalent to 50% of incremental measure costs

• Annual incentives costs are $17.4 million• Total annual implementation costs are

$39.5 million

GDS Associates, Inc. 8

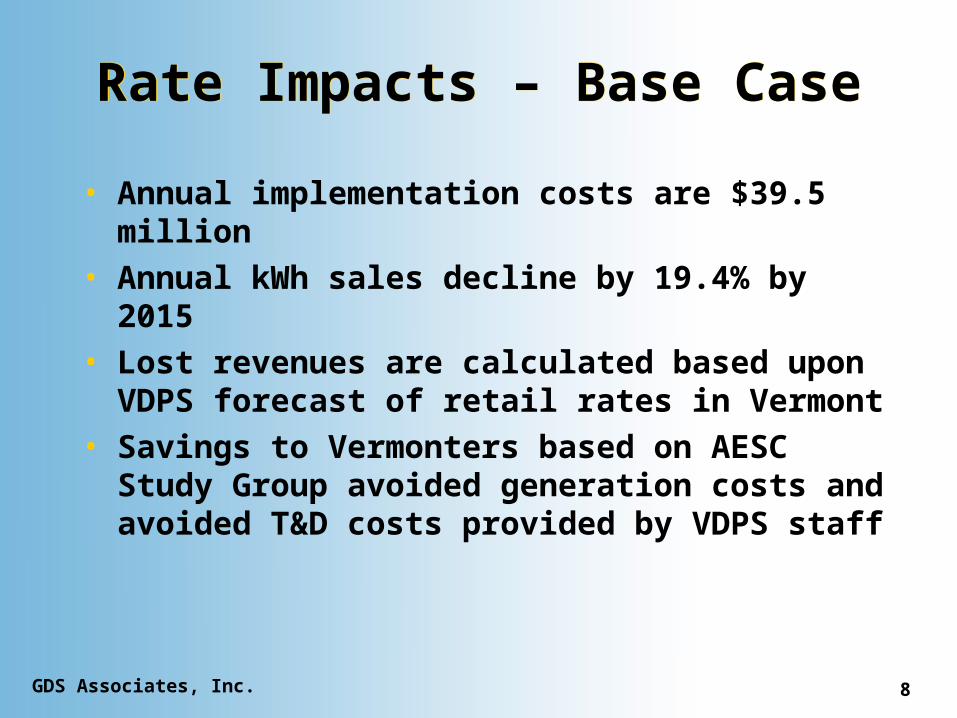

Rate Impacts – Base CaseRate Impacts – Base Case

• Annual implementation costs are $39.5 million

• Annual kWh sales decline by 19.4% by 2015• Lost revenues are calculated based upon

VDPS forecast of retail rates in Vermont• Savings to Vermonters based on AESC

Study Group avoided generation costs and avoided T&D costs provided by VDPS staff

GDS Associates, Inc. 9

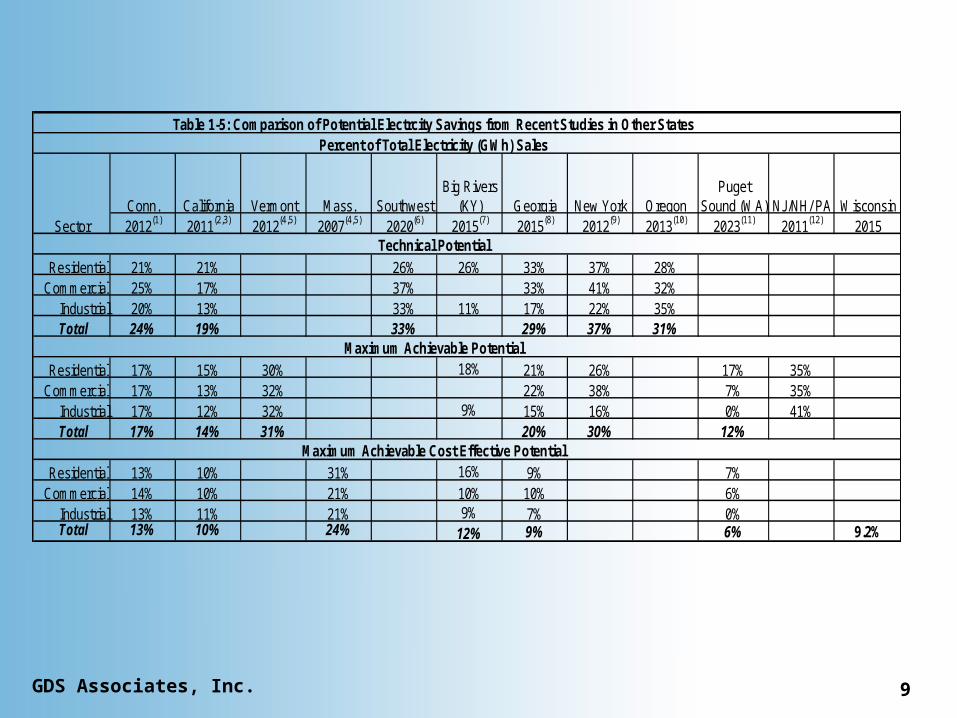

Conn. California Vermont Mass. SouthwestBig Rivers

(KY) Georgia New York OregonPuget

Sound (WA) NJ/NH/ PA Wisconsin2012(1) 2011(2,3) 2012(4,5) 2007(4,5) 2020(6) 2015(7) 2015(8) 2012(9) 2013(10) 2023(11) 2011(12) 2015

Residential 21% 21% 26% 26% 33% 37% 28%

Commercial 25% 17% 37% 33% 41% 32% Industrial 20% 13% 33% 11% 17% 22% 35%

Total 24% 19% 33% 29% 37% 31%

Residential 17% 15% 30% 18% 21% 26% 17% 35%

Commercial 17% 13% 32% 22% 38% 7% 35% Industrial 17% 12% 32% 9% 15% 16% 0% 41%

Total 17% 14% 31% 20% 30% 12%

Residential 13% 10% 31% 16% 9% 7%

Commercial 14% 10% 21% 10% 10% 6% Industrial 13% 11% 21% 9% 7% 0%

Total 13% 10% 24% 12% 9% 6% 9.2%

Table 1-5: Comparison of Potential Electrcity Savings from Recent Studies in Other StatesPercent of Total Electricity (GWh) Sales

Sector

Maximum Achievable Cost Effective Potential

Technical Potential

Maximum Achievable Potential

GDS Associates, Inc. 10

Key Assumptions Key Assumptions

• New benefit/cost screening model• Line losses• Reserve margin• Electric avoided costs and fossil fuel

prices• Externality adders• Maximum achievable penetration rate for

efficiency measures

GDS Associates, Inc. 11

New Benefit-Cost Screening Model

New Benefit-Cost Screening Model

• Built by GDS Associates over the past five years

• Operates in an Excel environment• Has been approved by regulators in other

States• Can handle over 110 energy efficiency

measures• User-friendly and easy to use

GDS Associates, Inc. 12

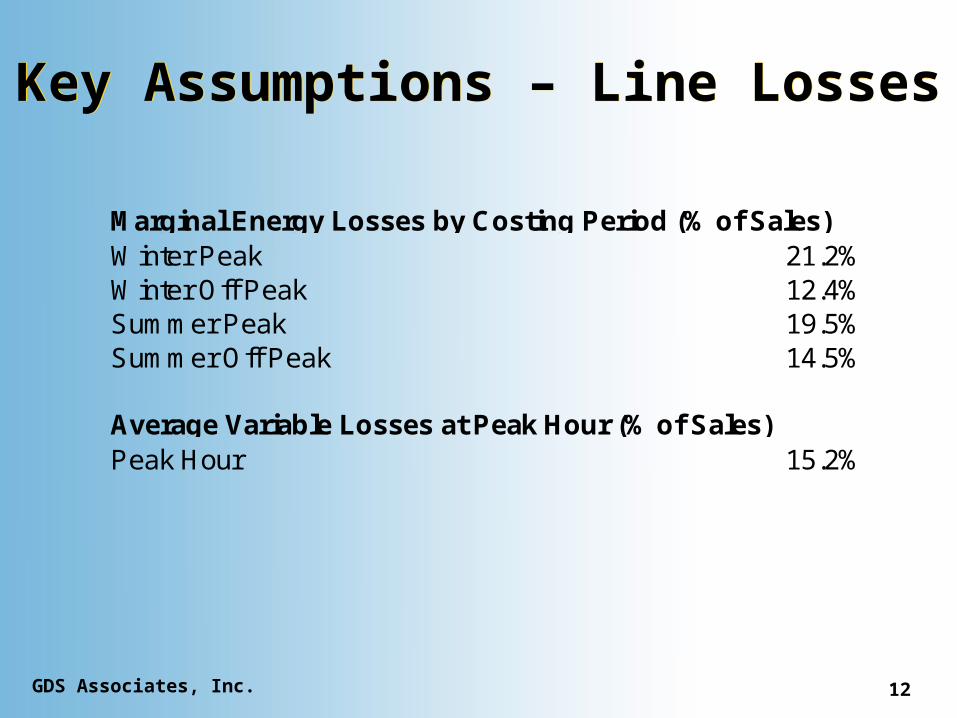

Key Assumptions – Line LossesKey Assumptions – Line Losses

Marginal Energy Losses by Costing Period (% of Sales)Winter Peak 21.2%Winter Off Peak 12.4%Summer Peak 19.5%Summer Off Peak 14.5%

Average Variable Losses at Peak Hour (% of Sales)Peak Hour 15.2%

GDS Associates, Inc. 13

Key Assumptions for Electric Avoided Costs

Key Assumptions for Electric Avoided Costs

• Electric generation avoided costs for Vermont – from December 2005 AESC Study Group report

• Fossil fuel prices - from December 2005 AESC Study Group report

• T&D avoided capacity costs – from VDPS ($163 per kW in 2005 dollars)

• Reserve margin of 13.8% provided by VDPS staff

GDS Associates, Inc. 14

Key Assumptions for Externality Adders for Vermont Societal TestKey Assumptions for Externality Adders for Vermont Societal Test

• Non – energy benefits adder of $.0081 per kWh saved (in 2005 dollars) applied to electricity savings

• Non – energy benefits adder for fossil fuel savings obtained from VDPS staff

• Costs of electric energy efficiency measures reduced by 10%

GDS Associates, Inc. 15

Key Assumptions for Maximum Penetration of Efficiency

Measures

Key Assumptions for Maximum Penetration of Efficiency

Measures

• Maximum penetration rate of 80% for base case where incentives of 50% of incremental cost are paid (base case)

• Maximum penetration rate of 85% for base case where incentives of 100% of incremental cost are paid (high incentives case)

Residential Sector Findings

Residential Sector Findings

April 10, 2006

GDS Associates, Inc. 17

Vermont Residential SectorVermont Residential Sector

• Much has already been accomplished in VT

• EVT has already saved a significant amount of electric energy and demand

• This is equivalent to a significant percentage of 2005 annual kWh sales in Vermont

GDS Associates, Inc. 18

Residential Savings SummaryResidential Savings Summary

• Significant cost effective electricity savings potential still exists

• Important to understand how electricity is used in the residential sector

• Residential sector is forecast to have the fastest kWh sales growth for 2006 to 2015 (1.6%)

• Majority of savings potential is in lighting and electric water heater fuel conversion

GDS Associates, Inc. 19

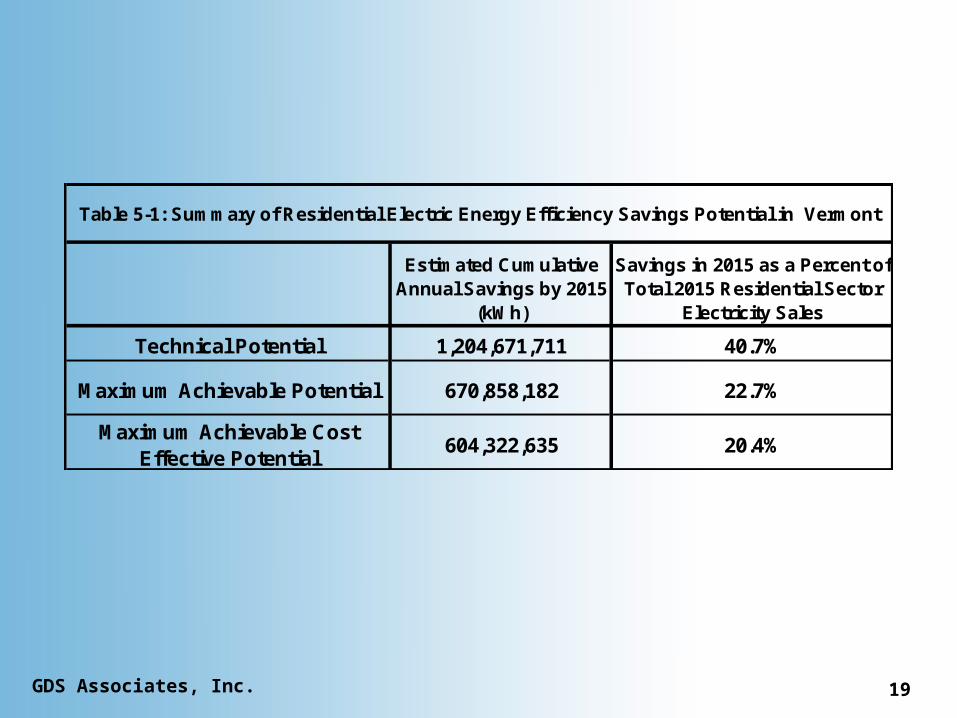

Estimated Cumulative Annual Savings by 2015

(kWh)

Savings in 2015 as a Percent of Total 2015 Residential Sector

Electricity Sales

Technical Potential 1,204,671,711 40.7%

Maximum Achievable Potential 670,858,182 22.7%

Maximum Achievable Cost Effective Potential

604,322,635 20.4%

Table 5-1: Summary of Residential Electric Energy Efficiency Savings Potential in Vermont

GDS Associates, Inc. 20

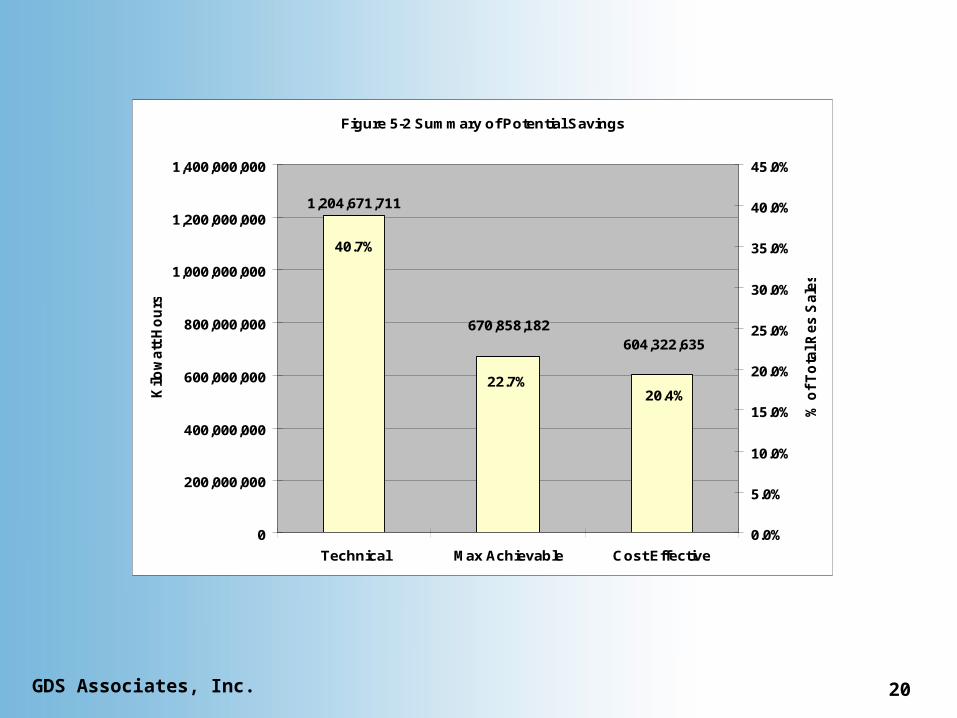

Figure 5-2 Summary of Potential Savings

1,204,671,711

670,858,182604,322,635

20.4%22.7%

40.7%

0

200,000,000

400,000,000

600,000,000

800,000,000

1,000,000,000

1,200,000,000

1,400,000,000

Technical Max Achievable Cost Effective

Kilo

wa

tt H

ou

rs

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

% o

f T

ota

l Re

s S

ale

s

GDS Associates, Inc. 21

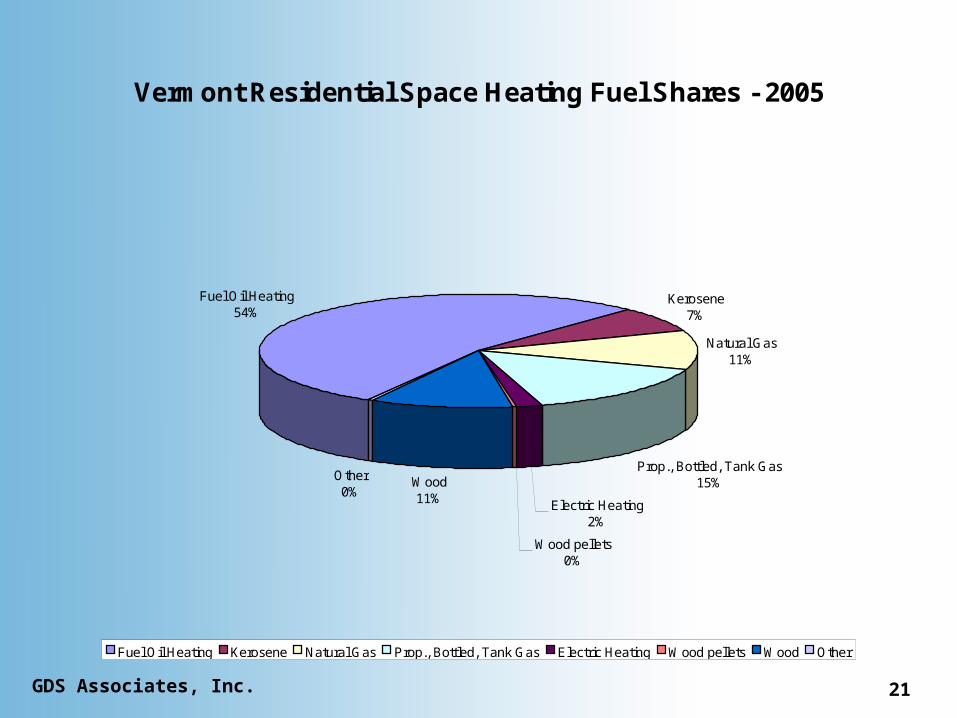

Vermont Residential Space Heating Fuel Shares - 2005

Fuel Oil Heating54%

Kerosene7%

Natural Gas11%

Prop., Bottled, Tank Gas15%

Electric Heating2%

Wood pellets0%

Wood11%

Other0%

Fuel Oil Heating Kerosene Natural Gas Prop., Bottled, Tank Gas Electric Heating Wood pellets Wood Other

GDS Associates, Inc. 22

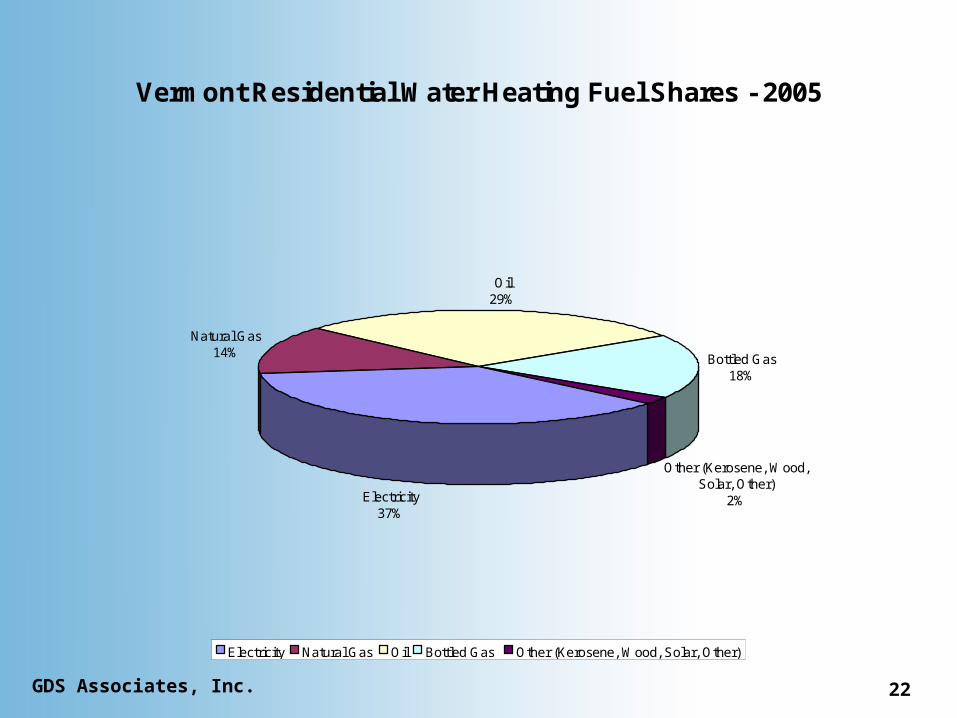

Vermont Residential Water Heating Fuel Shares - 2005

Electricity37%

Natural Gas14%

Oil29%

Bottled Gas 18%

Other (Kerosene, Wood, Solar, Other)

2%

Electricity Natural Gas Oil Bottled Gas Other (Kerosene, Wood, Solar, Other)

GDS Associates, Inc. 23

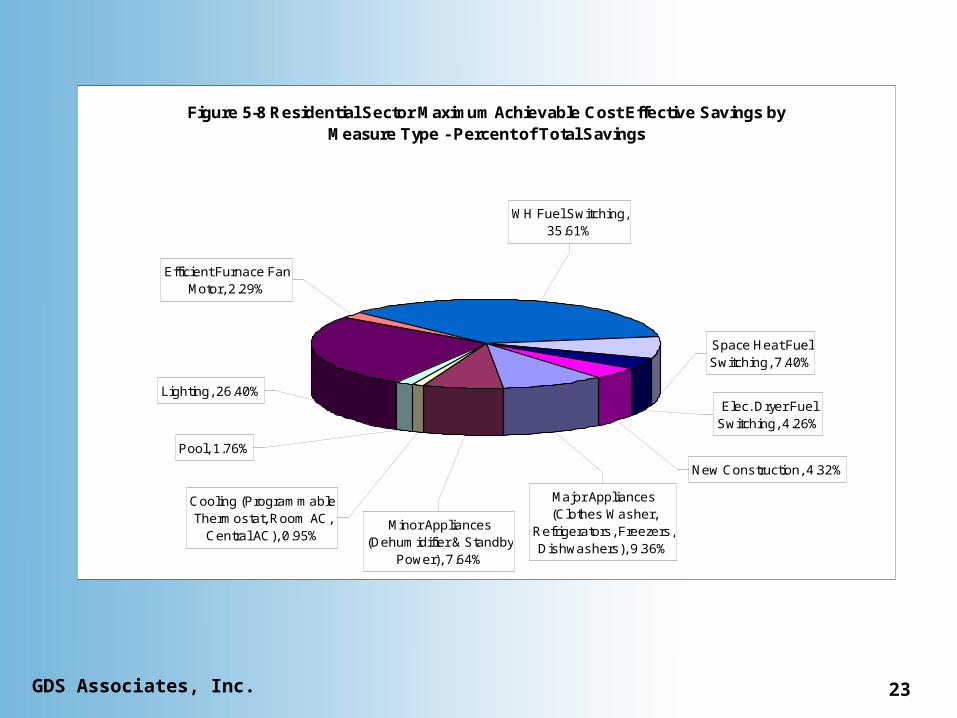

Figure 5-8 Residential Sector Maximum Achievable Cost Effective Savings by Measure Type - Percent of Total Savings

New Construction, 4.32%

Pool, 1.76%

Cooling (Programmable Thermostat, Room AC,

Central AC), 0.95%Minor Appliances

(Dehumidifier & Standby Power), 7.64%

Elec. Dryer Fuel Switching, 4.26%

Major Appliances (Clothes Washer,

Refrigerators, Freezers, Dishwashers), 9.36%

Space Heat Fuel Switching, 7.40%

WH Fuel Switching, 35.61%

Efficient Furnace Fan Motor, 2.29%

Lighting, 26.40%

Commercial Sector Findings

Commercial Sector Findings

April 10, 2006

GDS Associates, Inc. 25

Commercial Sector SummaryCommercial Sector Summary

• Significant cost effective electricity savings potential still exists

• Important to understand how electricity is used in the commercial sector

• Commercial sector is forecast to have the slowest growth for 2006 to 2015 (0.5% a year)

• Majority of savings potential is in lighting and refrigeration end uses

GDS Associates, Inc. 26

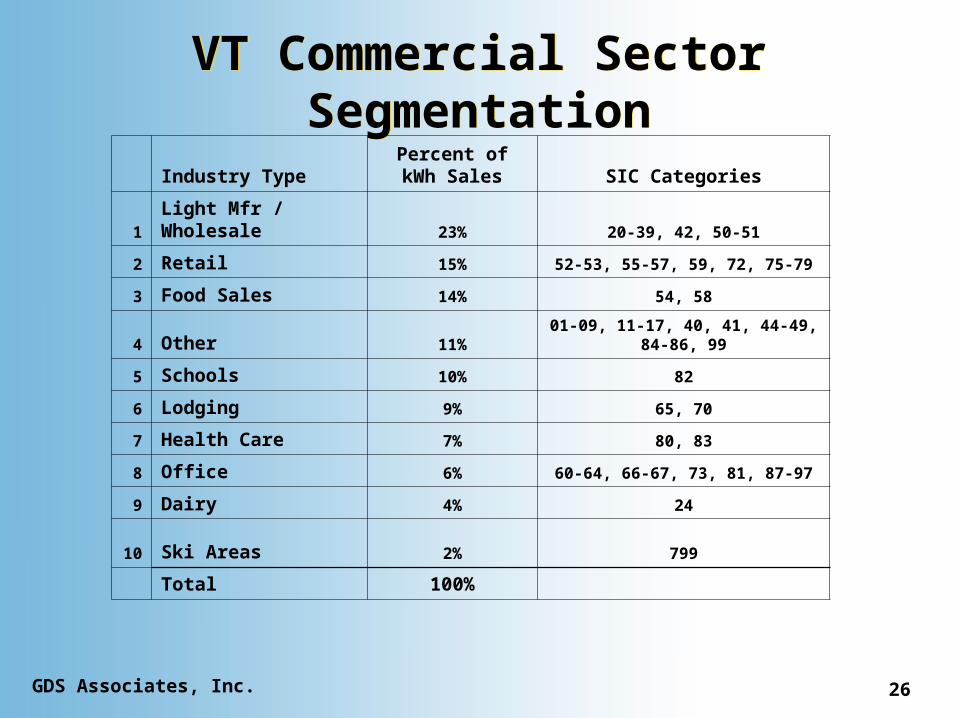

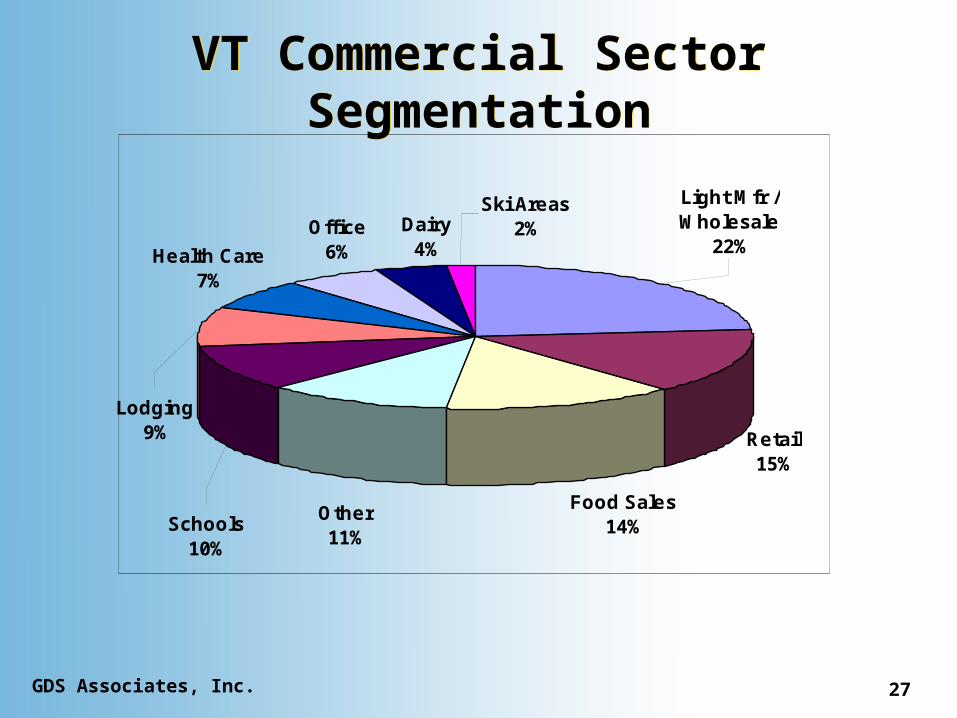

VT Commercial Sector Segmentation

VT Commercial Sector Segmentation

Industry TypePercent of kWh

Sales SIC Categories

1 Light Mfr / Wholesale 23% 20-39, 42, 50-51

2 Retail 15% 52-53, 55-57, 59, 72, 75-79

3 Food Sales 14% 54, 58

4 Other 11% 01-09, 11-17, 40, 41, 44-49, 84-86, 99

5 Schools 10% 82

6 Lodging 9% 65, 70

7 Health Care 7% 80, 83

8 Office 6% 60-64, 66-67, 73, 81, 87-97

9 Dairy 4% 24

10 Ski Areas 2% 799

Total 100%

GDS Associates, Inc. 27

VT Commercial Sector Segmentation

VT Commercial Sector Segmentation

Retail15%

Food Sales14%

Ski Areas2%

Light Mfr / Wholesale

22%

Other11%

Health Care7%

Lodging9%

Schools10%

Office6%

Dairy4%

GDS Associates, Inc. 28

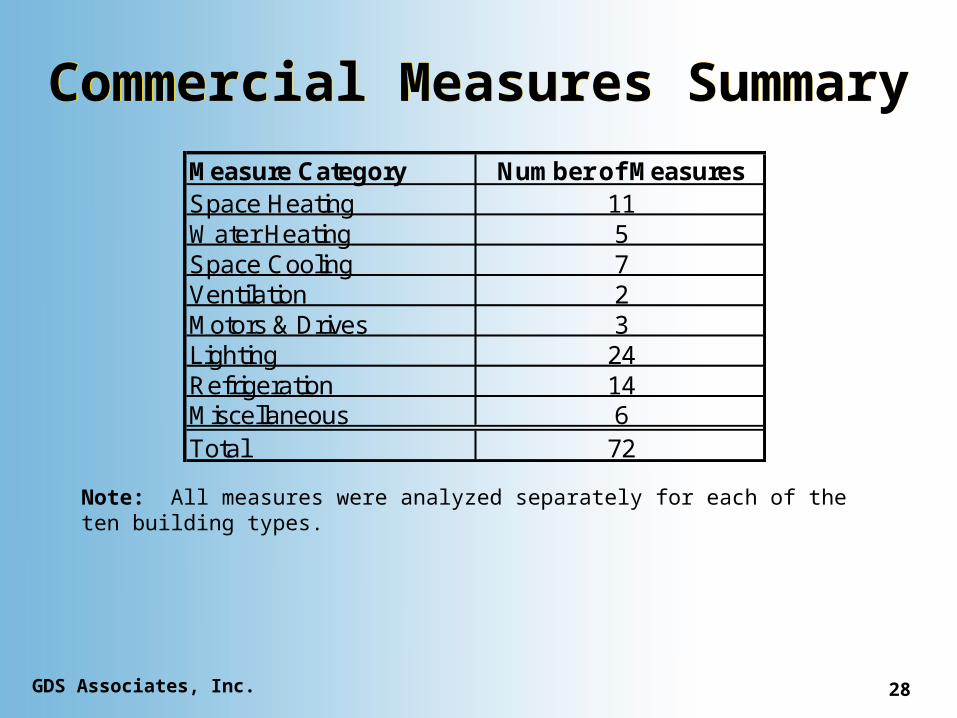

Commercial Measures Summary

Commercial Measures Summary

Measure Category Number of MeasuresSpace Heating 11Water Heating 5Space Cooling 7Ventilation 2Motors & Drives 3Lighting 24Refrigeration 14Miscellaneous 6Total 72

Note: All measures were analyzed separately for each of the ten building types.

GDS Associates, Inc. 29

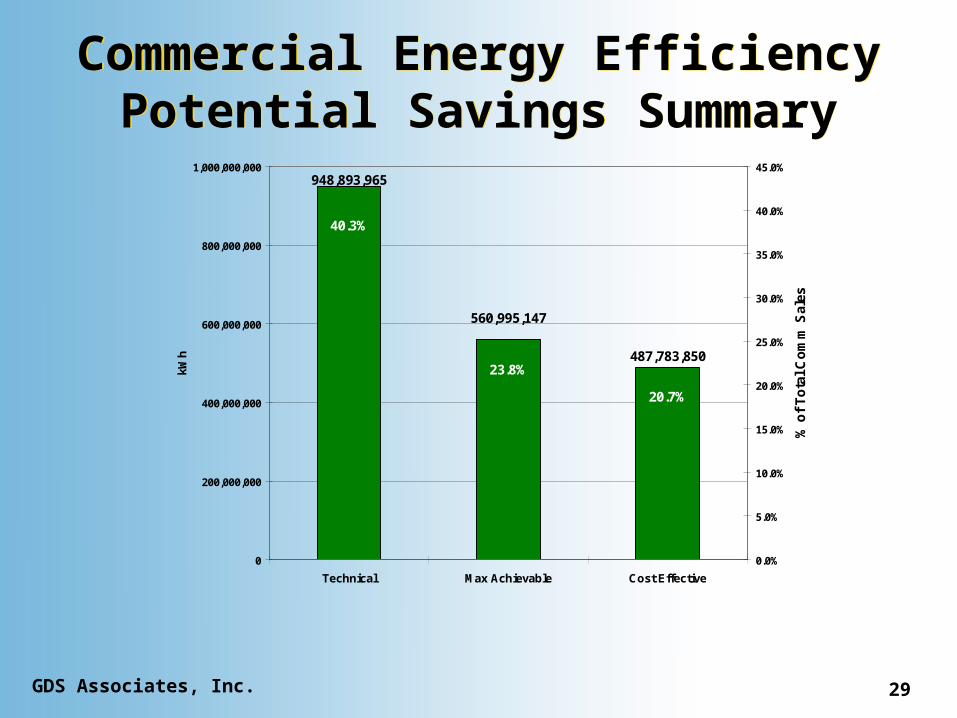

Commercial Energy Efficiency Potential Savings Summary

Commercial Energy Efficiency Potential Savings Summary

487,783,850

560,995,147

948,893,965

40.3%

23.8%

20.7%

0

200,000,000

400,000,000

600,000,000

800,000,000

1,000,000,000

Technical Max Achievable Cost Effective

kWh

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

% o

f T

ota

l C

om

m S

ales

GDS Associates, Inc. 30

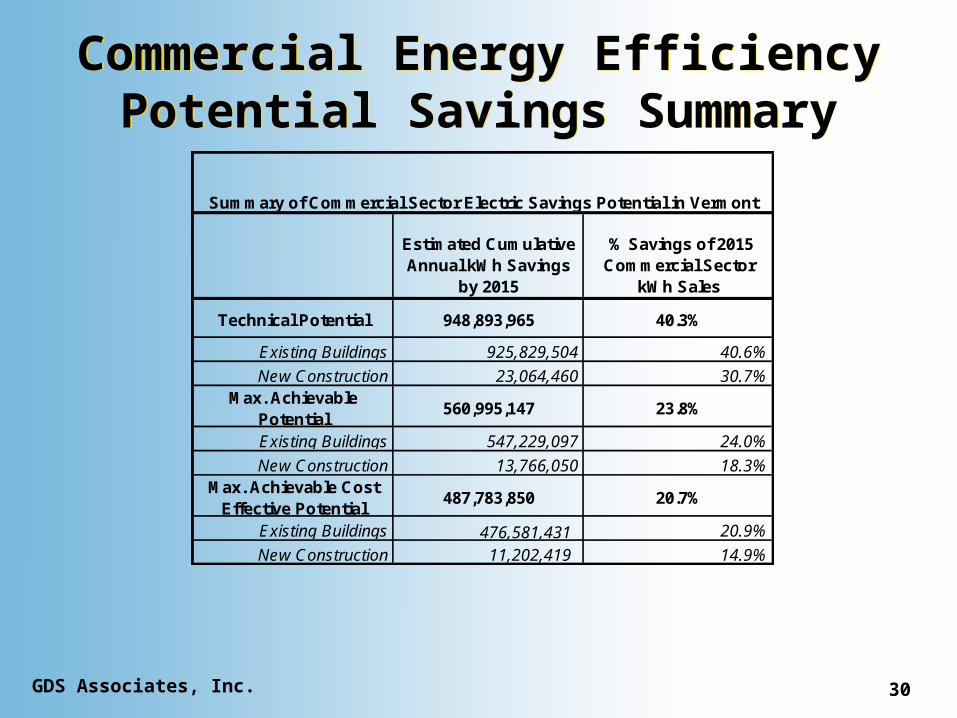

Commercial Energy Efficiency Potential Savings Summary

Commercial Energy Efficiency Potential Savings Summary

Estimated Cumulative Annual kWh Savings

by 2015

% Savings of 2015 Commercial Sector

kWh Sales

Technical Potential 948,893,965 40.3%

Existing Buildings 925,829,504 40.6%

New Construction 23,064,460 30.7%Max. Achievable

Potential560,995,147 23.8%

Existing Buildings 547,229,097 24.0%

New Construction 13,766,050 18.3%Max. Achievable Cost

Effective Potential487,783,850 20.7%

Existing Buildings 476,581,431 20.9%

New Construction 11,202,419 14.9%

Summary of Commercial Sector Electric Savings Potential in Vermont

GDS Associates, Inc. 31

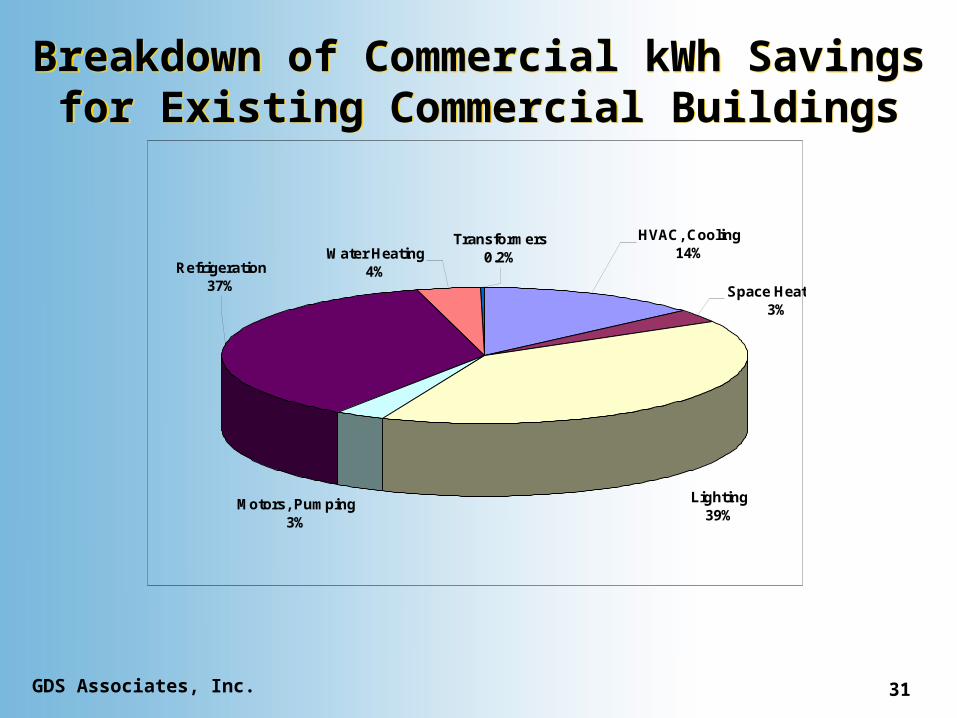

Breakdown of Commercial kWh Savings for Existing Commercial

Buildings

Breakdown of Commercial kWh Savings for Existing Commercial

Buildings

Motors, Pumping3%

Refrigeration37%

HVAC, Cooling14%

Transformers0.2%Water Heating

4%

Lighting39%

Space Heating3%

GDS Associates, Inc. 32

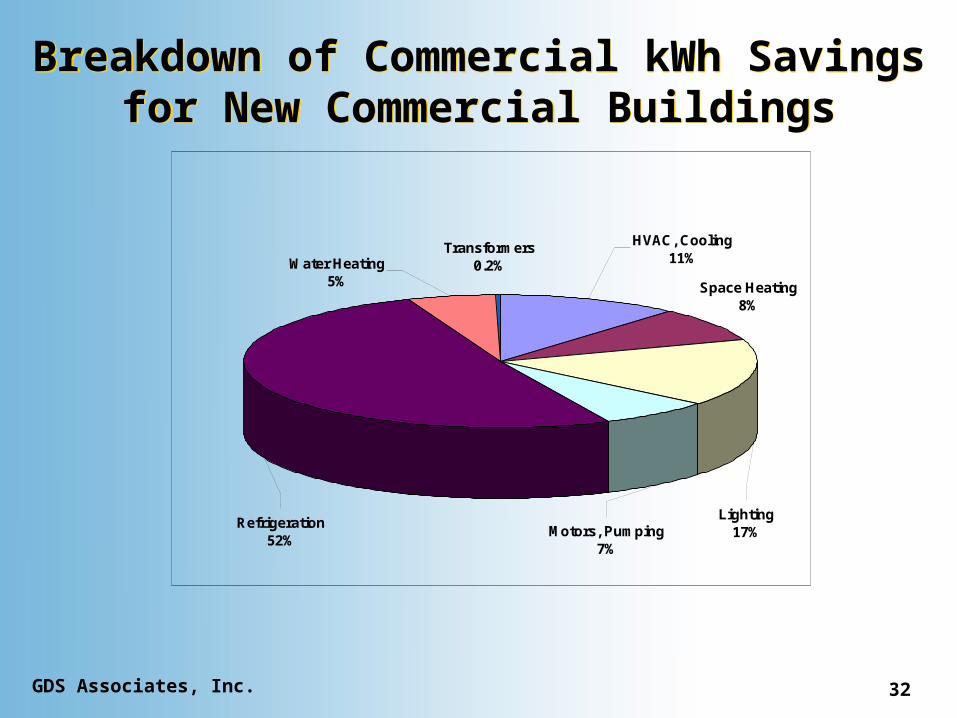

Breakdown of Commercial kWh Savings for New Commercial Buildings

Breakdown of Commercial kWh Savings for New Commercial Buildings

Motors, Pumping7%

Refrigeration52%

HVAC, Cooling11%

Transformers0.2%Water Heating

5%

Lighting17%

Space Heating8%

GDS Associates, Inc. 33

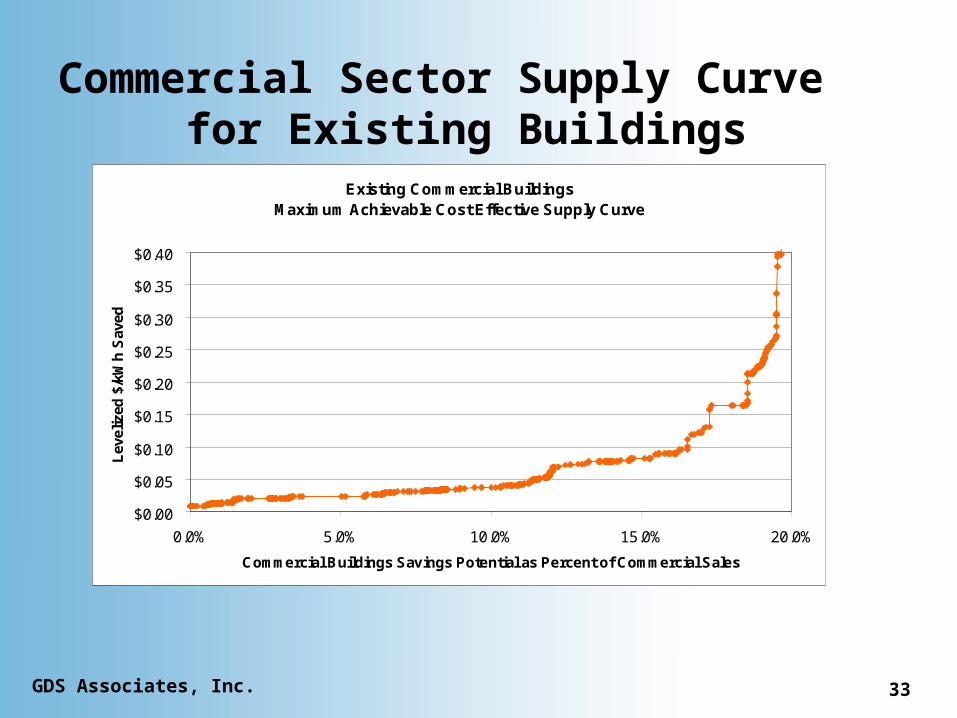

Commercial Sector Supply Curve for Existing Buildings

Existing Commercial Buildings Maximum Achievable Cost Effective Supply Curve

$0.00

$0.05

$0.10

$0.15

$0.20

$0.25

$0.30

$0.35

$0.40

0.0% 5.0% 10.0% 15.0% 20.0%

Commercial Buildings Savings Potential as Percent of Commercial Sales

Lev

eliz

ed $

/kW

h S

aved

GDS Associates, Inc. 34

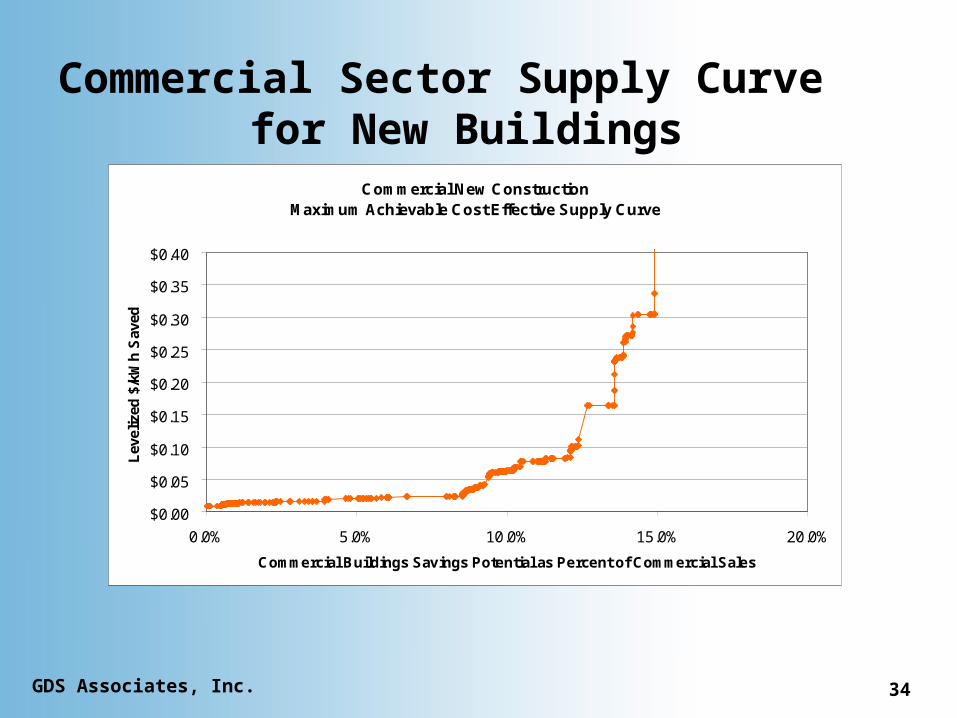

Commercial Sector Supply Curve for New Buildings

Commercial New ConstructionMaximum Achievable Cost Effective Supply Curve

$0.00

$0.05

$0.10

$0.15

$0.20

$0.25

$0.30

$0.35

$0.40

0.0% 5.0% 10.0% 15.0% 20.0%

Commercial Buildings Savings Potential as Percent of Commercial Sales

Lev

eliz

ed $

/kW

h S

aved

Industrial Sector Findings

Industrial Sector Findings

April 10, 2006

GDS Associates, Inc. 36

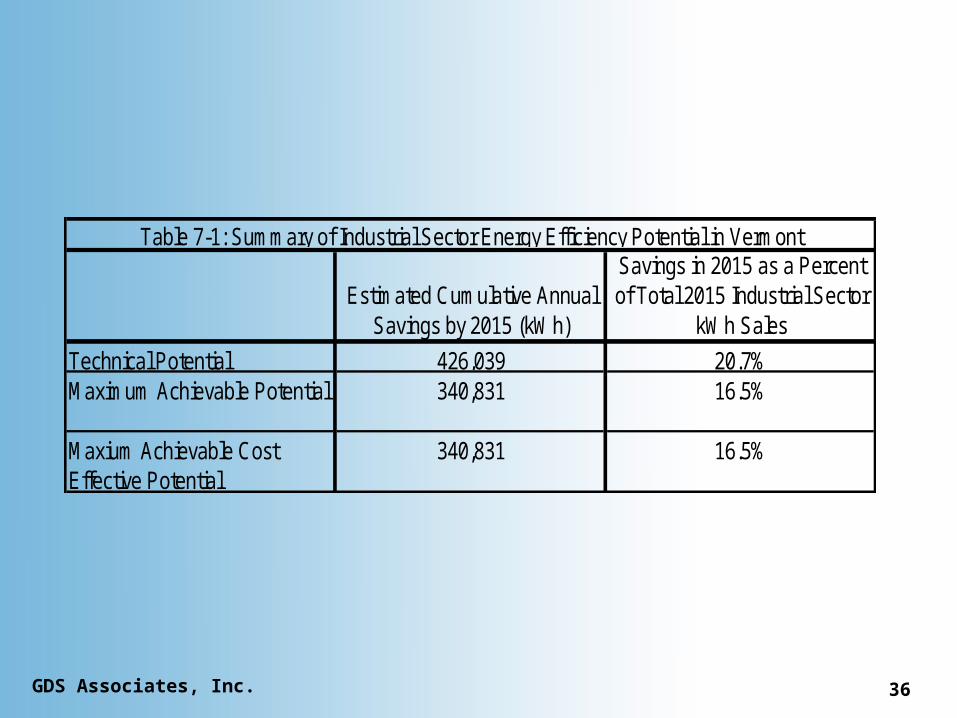

Estimated Cumulative Annual Savings by 2015 (kWh)

Savings in 2015 as a Percent of Total 2015 Industrial Sector

kWh Sales

Technical Potential 426,039 20.7%Maximum Achievable Potential 340,831 16.5%

Maxium Achievable Cost Effective Potential

340,831 16.5%

Table 7-1: Summary of Industrial Sector Energy Efficiency Potential in Vermont

GDS Associates, Inc. 37

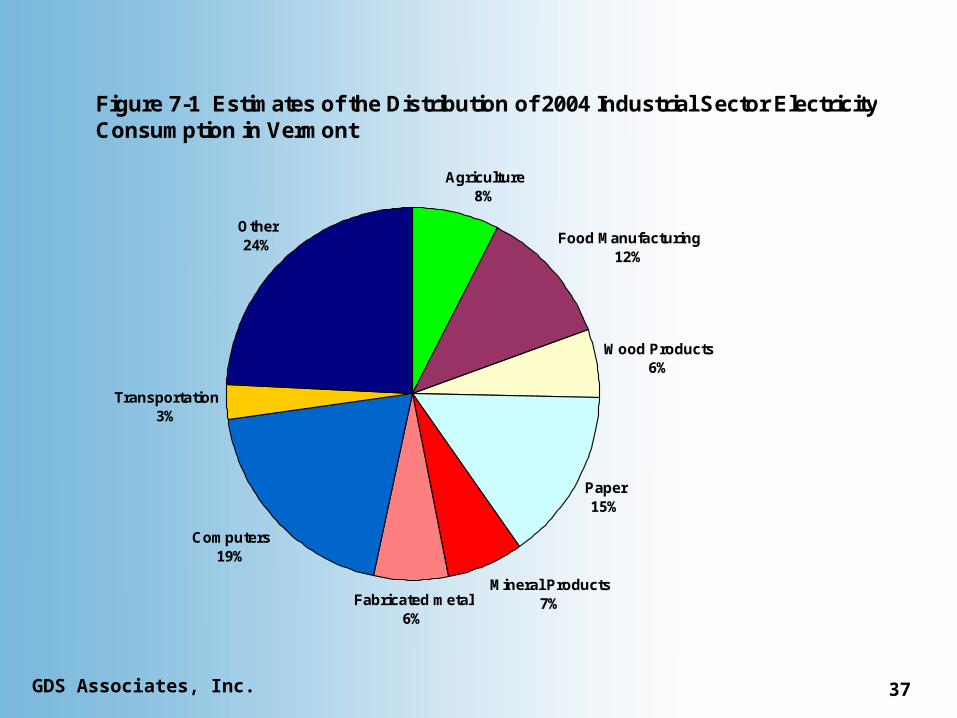

Figure 7-1 Estimates of the Distribution of 2004 Industrial Sector Electricity Consumption in Vermont

Agriculture8%

Food Manufacturing12%

Wood Products6%

Paper15%

Mineral Products7%Fabricated metal

6%

Computers19%

Transportation3%

Other24%

GDS Associates, Inc. 38

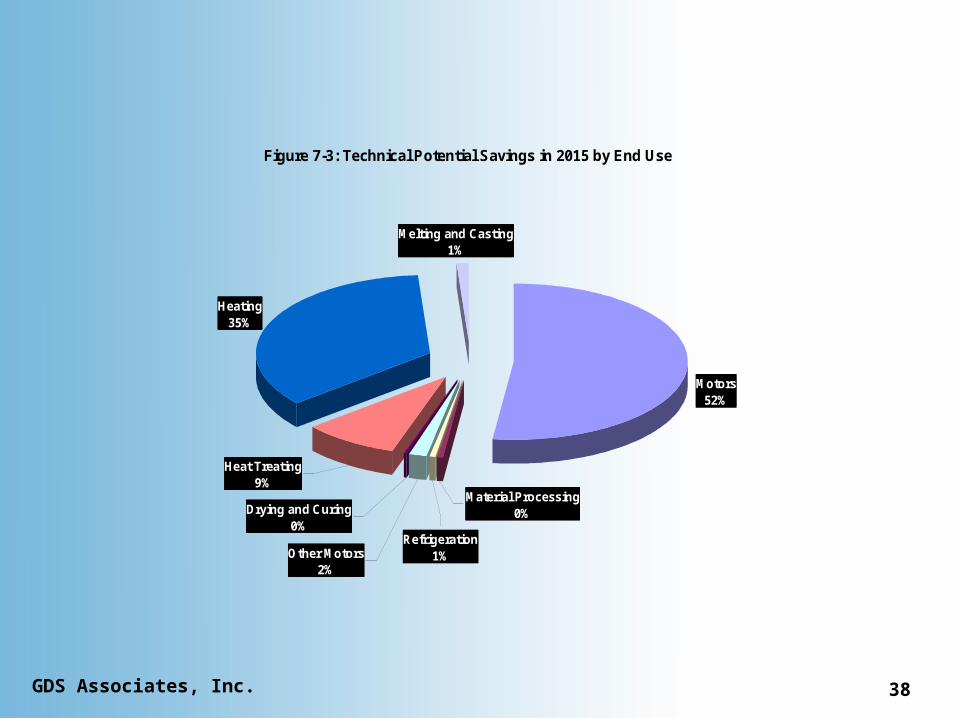

Figure 7-3: Technical Potential Savings in 2015 by End Use

Motors52%

Heating35%

Melting and Casting1%

Heat Treating9%

Refrigeration1%

Drying and Curing0%

Other Motors2%

Material Processing0%

GDS Associates, Inc. 39

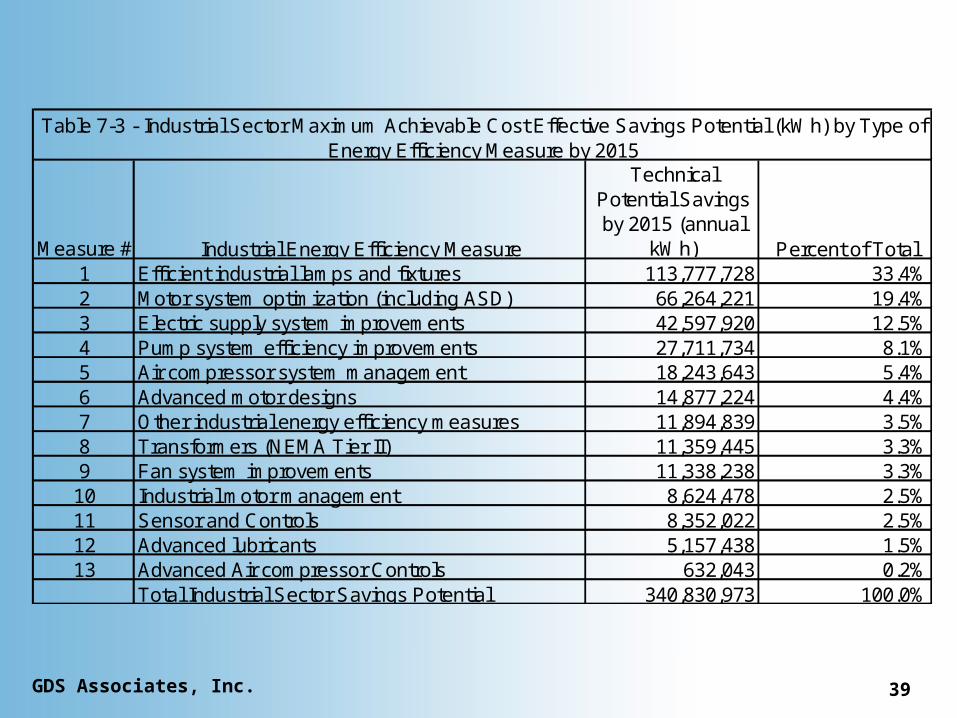

Measure # Industrial Energy Efficiency Measure

Technical Potential Savings by 2015 (annual

kWh) Percent of Total1 Efficient industrial lamps and fixtures 113,777,728 33.4%2 Motor system optimization (including ASD) 66,264,221 19.4%3 Electric supply system improvements 42,597,920 12.5%4 Pump system efficiency improvements 27,711,734 8.1%5 Air compressor system management 18,243,643 5.4%6 Advanced motor designs 14,877,224 4.4%7 Other industrial energy efficiency measures 11,894,839 3.5%8 Transformers (NEMA Tier II) 11,359,445 3.3%9 Fan system improvements 11,338,238 3.3%10 Industrial motor management 8,624,478 2.5%11 Sensor and Controls 8,352,022 2.5%12 Advanced lubricants 5,157,438 1.5%13 Advanced Air compressor Controls 632,043 0.2%

Total Industrial Sector Savings Potential 340,830,973 100.0%

Table 7-3 - Industrial Sector Maximum Achievable Cost Effective Savings Potential (kWh) by Type of Energy Efficiency Measure by 2015