Veresen Stock Pitch

10

VERESEN INC (TSE: VSN) Mike Chhabra October 1 st , 2015

-

Upload

mike-chhabra -

Category

Documents

-

view

218 -

download

0

description

1

Transcript of Veresen Stock Pitch

VERESEN INC (TSE: VSN)Mike Chhabra

October 1st, 2015

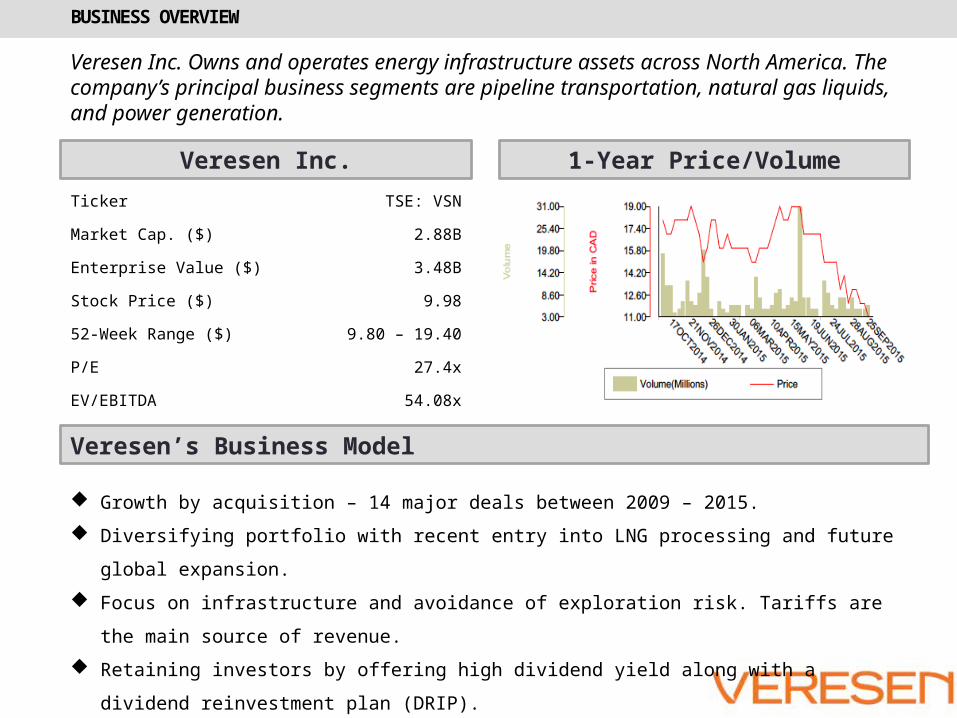

BUSINESS OVERVIEW

Veresen Inc. 1-Year Price/Volume

Veresen’s Business Model

Ticker TSE: VSN

Market Cap. ($) 2.88B

Enterprise Value ($) 3.48B

Stock Price ($) 9.98

52-Week Range ($) 9.80 – 19.40

P/E 27.4x

EV/EBITDA 54.08x

Veresen Inc. Owns and operates energy infrastructure assets across North America. The company’s principal business segments are pipeline transportation, natural gas liquids, and power generation.

Growth by acquisition – 14 major deals between 2009 – 2015.

Diversifying portfolio with recent entry into LNG processing and future global expansion.

Focus on infrastructure and avoidance of exploration risk. Tariffs are the main source of revenue.

Retaining investors by offering high dividend yield along with a dividend reinvestment plan

(DRIP).

SUMMARY OF OPERATIONS

All current operations in North America. Seeking global opportunity in LNG—Jordan Cove and Pacific Connector. Significant focus on green energy.

BUSINESS MODEL

Taking advantage of low interest rates to grow the business.

Acquisitions by cash offering.

• Majority of small acquisitions.• Cash from operations and debt financing.

Acquisitions by combination of equity and debt offering.

• Major expansion projects.• Issue of bonds and shares; high dividend yields to retain and attract investors—DRIP.

Issuing bonds at low interest rates to retire debt with high interest rates.

• Early redemption of high interest debt.• Buyback of shares.

Acquire Integrate Operate

Acquire related infrastructure.

Integration of assets.

Operations focus on lean management.

INTERNAL ANALYSIS

Strong Senior Management

History of Successful Acquisitions

Veresen Inc. has a management team with considerable amount of experience in the energy industry, as well as a proven track record of success with acquisitions.

President, CEO, and Board MemberDon Althoff has over 30 years of experienceIn leadership roles in the energy sector. All other executive/ board members comefrom diverse background including energy,financial institutions, and construction. Combinedexperience over 100 years.

Notable Senior Executives.

Donald L Althoff President/CEOElizabeth G Spomer Exec Vice PresidentKevan S King VP/Secy/Gen Counsel Theresa Jang VP:Finance/CFOThomas Day VP:OperationsDorreen Miller Director:Investor Relations

2015 Dawson area gas storage and compression assets

2014 Ruby Pipeline

2012 York Energy Centre – Wind Energy

2011 Hydroelectric projects - BC

2010 Acquired Pristine Power

2008 London Cogeneration facility

EXTERNAL ANALYSIS

Growth in LNG Exports & Future of LNG

Veresen Inc. has a management team with considerable amount of experience in the energy industry, as well as a proven track record of success with acquisitions.

Environmental resistance for new pipelines. Existing pipeline companies expected to remain over the next decade. Asia gas demand rapidly increasing—positive outlook for Jordan Cove.

INVESTMENT THESIS

High dividend with possibility of capital gain.

50% ownership of Ruby pipeline in 2014.• Strategic fit with upcoming Jordan Cove LNG Terminal.

Jordan Cove & Pacific Connector Pipeline• Access to other geographical markets.• Diversification of portfolio. Transition from inorganic growth.• FERC environmental impact statement released on September 30th, 2015 – Positive

Outlook.

Existing Assets• Attractive midstream assets with long-term contracts.• Power generation.• Stable cash flow.• Focus on infrastructure to avoid volatility.

VALUATION

Discounted Cash Flow Analysis

$ CAD MM 2015E 2016E 2017E 2018E 2019E EBIAT $49.0 $49.7 $50.2 $50.7 $51.2

Depreciation 48.8 49.6 50.0 50.5 51.1

Capex (Maintenance) (15.3) (15.5) (15.6) (15.8) (16.0)

Unlevered FCF $82.6 $83.8 $84.6 $85.5 $86.3

Discount Factor 0.96 0.88 0.81 0.75 0.69

Discounted FCF $79.2 $73.9 $68.7 $63.8 $59.3

WACC 8.7%

2019E EBITDA $121.3

Exit Multiple 16.0x

Terminal Value $1,940.0

PV Terminal Value $1,278.4

Total Equity Value $3,444.0

Fair Value per Share 14.03

Current Share Price 9.98

Implied Upside 41%

An exit multiple of 16.0x was assumed; this is in line with analyst predictionsfor Veresen.

VALUATION

COMPARABLES ANALYSIS

RISKS & CATALYSTS

RISKS CATALYSTS

Lack of experience in organic

growth.

Learning curve may be longer than

expected.

Geopolitical risk.

Govt. pressure on stringent pipeline

regulations

Demand for clean energy.

Jordan Cove LNG has a lot of

upside potential.

Absence of subsurface risk.

Less immune to greenhouse gas

effect.

Existing infrastructure with secured

contracted; provide stability in

short-medium term

Small leadership team, but very

experienced.

Primary focus on infrastructure.