Venture Capital in Spain by Stage of Development

21

68 JOURNAL OF SMALL BUSINESS MANAGEMENT Journal of Small Business Management 2007 45(1), pp. 68–88 Venture Capital in Spain by Stage of Development by Tomás Ramón Pintado, Domingo García Pérez de Lema, and Howard Van Auken This paper examines the investment decisions of 51 Spanish venture capital firms by stage of development. The results showed that venture capitalists ranked evalua- tion criteria related to the characteristics of the entrepreneurs, manager background, and management team experience as more important than market and product char- acteristics. Factors affecting the required rate of return were more important for the early-stage firms than for late-stage firms. Discounted cash flow analysis is the most frequently used valuation method. Private venture capital firms invest more during late development stages, while public venture capital firms invest more during the early stages. The results can be used by firms seeking venture capital, venture capital firms, consultants, and support agencies that provide capital-acquisition assistance. By gaining insight into decision criteria and processes, firms can develop better and more targeted materials to attract capital. Venture capital firms can use the infor- mation from this study to better understand their decision processes, individually and relative to competitors. Consultants and support agencies can use the informa- tion to provide better advice to both firms and venture capital firms. Information is this study could easily be built into training programs for both new and existing busi- nesses. Finally, the results can also be incorporated directly into university courses that include material related to venture capital. Tomás Ramón Pintado is professor in the Department of Accounting and Finance at the Politechnical University of Cartagena and coordinator of SMEs. Domingo García Pérez de Lema is head of The Department of Accounting and Finance at the Politechnical University of Cartagena and coordinator of SMEs Economic Observatory in the Murcia region of Spain. Howard Van Auken is professor of management at Iowa State University. Address correspondence to: Howard Van Auken, 3363 Gerdin Building, Iowa State Univer- sity, Ames, IA 50011. Tel: (515) 294-2478. E-mail: [email protected]. Introduction Venture capital (VC) is important to many Spanish SMEs that are rapidly growing or that are developing high- risk products. Traditional financing sources are commonly unavailable as financial institutions are reluctant to provide risk capital and personal equity is often consumed during the early

Transcript of Venture Capital in Spain by Stage of Development

68 JOURNAL OF SMALL BUSINESS MANAGEMENT

Journal of Small Business Management 2007 45(1), pp. 68–88

Venture Capital in Spain by Stage ofDevelopmentby Tomás Ramón Pintado, Domingo García Pérez de Lema, and Howard Van Auken

This paper examines the investment decisions of 51 Spanish venture capital firmsby stage of development. The results showed that venture capitalists ranked evalua-tion criteria related to the characteristics of the entrepreneurs, manager background,and management team experience as more important than market and product char-acteristics. Factors affecting the required rate of return were more important for theearly-stage firms than for late-stage firms. Discounted cash flow analysis is the mostfrequently used valuation method. Private venture capital firms invest more duringlate development stages, while public venture capital firms invest more during theearly stages. The results can be used by firms seeking venture capital, venture capitalfirms, consultants, and support agencies that provide capital-acquisition assistance.By gaining insight into decision criteria and processes, firms can develop better andmore targeted materials to attract capital. Venture capital firms can use the infor-mation from this study to better understand their decision processes, individuallyand relative to competitors. Consultants and support agencies can use the informa-tion to provide better advice to both firms and venture capital firms. Information isthis study could easily be built into training programs for both new and existing busi-nesses. Finally, the results can also be incorporated directly into university coursesthat include material related to venture capital.

Tomás Ramón Pintado is professor in the Department of Accounting and Finance at the

Politechnical University of Cartagena and coordinator of SMEs.

Domingo García Pérez de Lema is head of The Department of Accounting and Finance at

the Politechnical University of Cartagena and coordinator of SMEs Economic Observatory in

the Murcia region of Spain.

Howard Van Auken is professor of management at Iowa State University.

Address correspondence to: Howard Van Auken, 3363 Gerdin Building, Iowa State Univer-

sity, Ames, IA 50011. Tel: (515) 294-2478. E-mail: [email protected].

IntroductionVenture capital (VC) is important to

many Spanish SMEs that are rapidlygrowing or that are developing high-

risk products. Traditional financingsources are commonly unavailable asfinancial institutions are reluctant toprovide risk capital and personal equityis often consumed during the early

PINTADO, PÉREZ DE LEMA, AND VAN AUKEN 69

stages of company operations (VanAuken 2001). Venture capital can fundproduct development, marketing, expan-sion, turnaround, employee buyout, andacquisition. Venture capital investmentcan position the firm to obtain additionalcapital through the venture capitalist’sexperience, expanded network of con-tacts, enhanced market creditability, andstronger financial position (Ruhnka andYoung 1997). Gupta and Sapienza (1994)suggest that venture capitalists add valueto a firm by bringing investors and entre-preneurs together in an efficient manner,making better investment decisions thanlimited partners would make, and pro-viding nonfinancial assistance that inturn promotes survival. Zacharakis andMeyer (2000) pointed out that VC-backedventures have higher survival rates thannonVC-backed ventures.

Understanding the nature and processof VC investment decisions can improvethe likelihood that a firm will be suc-cessful in raising funds. Stage of devel-opment, risk of the venture, backgroundof the owners, geographic location, andexit opportunities affect the venture capitalists’ assessment of risk and returnpotential (Van Auken 2001). Under-standing these issues will enable compa-nies to develop better proposals andnegotiate more effectively with venturecapitalists (Timmons and Spinelli 2004).

The creation of an active VC marketthat facilitates the financing of early-stage and high technology ventures hasbeen a high priority for economic poli-tics (Da Rin, Nicodano, and Sembenelli2005). Early-stage companies that attractVC investment can take advantage of theVC’s experience, knowledge, under-standing of the entrepreneurial process,and network of relationships (Repulloand Suarez 2004; Lindsey 2003; Lerner1995). Late-stage companies that attractVC capital have less opportunity to takeadvantage of these VC contributions(Michelacci and Suarez 2004).

The tendency of the VC in Europe incomparison with Asia countries and theUnited States is to invest in more in late-stage projects (Allen and Song 2003).This takes place in a higher intensity inSpain, where the investments in earlystages only represented 4.2 percent ofthe invested volume and 21.9 percent ofthe number of operations in 2003 (ASCRI2004). Spanish SMEs have traditionallyexperienced problems accessing mediumand long-term financing. Public VC fundswere established to provide funding forSMEs, particularly start-ups who couldpotentially contribute high added value.Regional governments are especiallyinterested in establishing regional VCfunds to promote regional economicdevelopment.

This paper fills a gap in VC researchby examining VC investing in Spain.Specifically, the study examined the rela-tionship between the stage of develop-ment and investment decisions of 51Spanish VC firms. Little research hasbeen completed on Spanish VC, espe-cially on VC investing in relation to stageof firm development. Venture capitalinvesting in Spain has increased fourfoldsince 1997, and much of this growth hasbeen achieved through internationalcapital inflows. In 1999–2000, theSpanish government developed eco-nomic initiatives to spur VC investing(Tejado 2003). Gaining insight into thedecision criteria and processes ofSpanish VC decisions can assist furtherdevelopment of government policy thatfacilitates VC investing. A better under-standing of VC investing can helpSpanish firms to develop better and moretargeted materials to attract capital.Venture capital firms can use the infor-mation from this study to better under-stand their decision processes, both inisolation as well as in relation to theircompetitors.

The next section of the paper providesan overview of VC investing. Section 3presents a description of the data and

methods used in data analysis. Section 4explains the results of the analysis, andthe final section provides summaryresults and conclusions.

Venture CapitalInvestmentsStage of Development

Lam (1991) recognized the impor-tance of analyzing investments accordingto the stage of development by statingthat VC investments relative to the stageof development provide important infor-mation on company value. Venturecapital investment of capital is similar tobuying an option to participate in thesubsequent stages of company develop-ment. The company’s stage of develop-ment directly impacts the VC’sinvestment analysis, especially as relatedto the risk assessment and return potential (Carter and Van Auken 1994).Venture capitalists would require higherexpected rates of return for early-stageinvestments as compared to late-stageinvestments due to the greater risk exposure.

Venture capitalists typically specializeby stage of development and geographi-cal location. Specializing by stage ofdevelopment allows them to balanceinvestment risk, portfolio diversification,and return potential. Investing in specificgeographical locations permits greateropportunity to influence and advise firms in which they invest (Cano andCazorla 1998; Carter and Van Auken1994; Barry 1994; Norton and Tenen-baum 1993). Gupta and Sapienza (1992)show that VC firms that specialized in theearly stage of development prefer lessdiversification and close geographicproximity to the firms in which theyinvest than VC firms that invest in latestages. Larger VC firms often invest inmultiple stages of development and alarger geographic area to manage riskexposure through diversification (Canoand Cazorla 1998).

InformationThe flow of information between the

venture capitalist and the entrepreneur isone of the more important elementsaffecting negotiations and investment.Several alternative approaches, includinginformation asymmetry, signaling, andagency theory, have been used to under-stand the role of information in con-summating the investment decision.Information asymmetry has been cited asone of the more important factors in theacquisition of capital by small firms(Landstrom 1992). Expecting theexchange of all knowledge about aventure is unrealistic, particularly in viewof the specific knowledge embedded inthe skills and capabilities of thefounders. Asymmetrical information isgreater in the early stages of develop-ment than in later stages because of the difficulty of assessing performance in earlier stages (Sahlman 1990).Information asymmetry is potentially aneven greater problem for firms involvedin technological innovation than other firms because of the uncertainty of market forecasts and long productdevelopment lead times (Van Auken2001).

Even with a superior business con-cept and a competent team, new ventures are likely to be underfundedunless they can effectively communi-cate the appropriate information topotential investors (Busenitz, Fiet, andMoesel, 2005). Problems associated with information asymmetry can,however, be mitigated through interac-tions between the venture capitalist and the entrepreneur (Sapienza andGupta 1994). The venture capitalists’due diligence of the investment proposal is an important step in mini-mizing information asymmetry (Gompers1995). Several researchers (Admati and Pfleiderer 1994; Lerner 1994; Chan1983) proposed models to overcomeproblems stemming from asymmetricalinformation.

70 JOURNAL OF SMALL BUSINESS MANAGEMENT

The presence of asymmetric informa-tion is a fundamental assumption of signaling theory. In the absence of infor-mation, decision-makers often look tovarious indicators as signals of futureoutcomes. Information asymmetry mayallow the entrepreneur to engage inopportunistic behavior that is inconsis-tent with the goals of the investor. Oneof the critical challenges for a newventure team is to provide signals toventure capitalists that overcome infor-mation asymmetry (Busenitz et al. 2005;Deeds, Decarolis, and Coombs 1997).Appropriate signals can allow new ventures to communicate both firm value and owner commitment to poten-tial investors (Arthurs and Busenitz,2003).

Agency problems can occur as theresult of incongruent goals and differentrisk preferences between an owner anda venture capitalist (Arthurs and Busenitz2003). Entrepreneurs may, for example,exaggerate the viability of the businessto obtain favorable financing terms(Amit, Brander, and Zott 1998). Land-strom (1992) used agency theory to showthat information asymmetry results insmall firms having greater difficulty inraising capital because of higher moni-toring costs, bonding costs, and residualloss potential, as compared to largerfirms.

Quality and amount of informationmay depend on the firm’s stage of devel-opment (Van Auken 2001). Both venturecapitalists and entrepreneurs should rec-ognize that agency problems and signal-ing issues may vary by stage ofdevelopment. One method that venturecapitalists often use to manage agencyand signaling issues is that of specializ-ing by stage of development (Cano andCazorla 1998; Gupta and Sapienza 1992).Specialization allows them to developand provide expanded networks andbetter understand their risk exposure(Carter and Van Auken 1994; Norton andTenenbaum 1993).

Proposal EvaluationSeveral studies have examined due

diligence of proposals (Fried and Hisrich1994; MacMillan, Siegel, and Subba-narasimha 1985; Tyebjee and Bruno1984). Due diligence assesses the impacton the venture’s risk and return charac-teristics of issues related to the manage-ment team, product, market potential,and legal concerns (Manigart et al. 1998;Wright, Robbie, and Ennew 1997; Friedand Hisrich 1994). The valuation of pro-posals includes two distinct aspects. Dealorigination, or the first contact betweenthe owner and venture capitalist, is oftenarranged through financial mediators,and other venture capitalists. Due dili-gence of material in the business plan isa common initial aspect of deal origina-tion. Deal screening, the next step in pro-posal evaluation, evaluates issues relatedto location, size, industry, and stage ofdevelopment, to filter proposals thatmerit serious consideration. This evalua-tion often focuses on matters related tothe quality of the company as well as theachievement of the venture capitalist’sinvestment goals (Manigart et al. 2002;Wright and Robbie 1996; MacMillan,Siegel, and Subbanarasimha 1985;Tyebjee and Bruno 1984). Accountinginformation is an especially importantevaluation tool of VC investments inEurope (Manigart, Wright, and Des-brières 1998).

Venture Capital Decision Process

Figure 1 shows the VC decisionprocess and may provide insight intowhy venture capitalists specialize in par-ticular niches and focus on specificsources/types of information. Selectionof specific investments is the culminationof issues associated with both the marketneeds and venture capitalists skills.Venture capitalists will invest in marketniches where they can add the mostvalue to both their potential portfolio

PINTADO, PÉREZ DE LEMA, AND VAN AUKEN 71

72 JOURNAL OF SMALL BUSINESS MANAGEMENT

and the firm. Selection of the marketniche is, however, predicated on thenature of market (for example, entrepre-neur’s demand for capital) and theventure capitalist’s comparative advan-tage (Wright and Robbie 1998). Theanalysis of opportunities in differentniches may require different types ofinformation as well as different analyti-cal methods (Harvey and Lusch 1995).

Venture capital financing may beviewed as an expensive funding solutionto projects with high potential returns,but also substantial asymmetric informa-tion problems and potentially highagency costs (Timmons and Spinelli2004; Landstrom 1992). Venture capital-ists face numerous constraints, includinglimits on time, financial resources, and

information. Venture capitalists would beexpected to invest in market niches (forexample, geographic, stage of develop-ment, and industry) and use informationsources that produce the most gainsgiven these constraints.

Private venture capitalists should con-sider at least two issues when selectingthe desired market niche in which to spe-cialize and invest. The first issue, dealflow, is related to the availability andquality of investment opportunities. Thesecond, the comparative advantage ofthe venture capitalist, could be, forexample, skills in evaluating unproventechnologies, appraising market demandfor new products, assessing the manage-rial talent of the entrepreneur, providingthe advice and support needed to grow

Entrepreneurs Demand for Venture Capital Financing

Venture Capitalist’s Comparative Advantage

Selection of Niches in which Venture Capitalist can Add Most Value

Selection of Best Information Sources and Methods To Evaluate Firms in Niche

Analysis of Alternative Firms

Investment Decision

Figure 1Venture Capital Process

the business rapidly, or other areas.Given the set of opportunities and theircomparative advantage, the venture cap-italist should invest in the niche(s) wherethey can add the most value (Wright,Robbie, and Ennew 1997). The impor-tance of investing in high-technologyfirms is part of this market niche selec-tion issue. Another aspect of the nicheselection may be deciding whether tofocus on early- or late-stage firms.

Once the VC firm identifies the marketniche(s) where they can offer the mostvalue and that provides that highestpotential return on investment. Theinvestment opportunities would subse-quently be analyzed using the mostuseful tools and available information. Ifaccurate information was costless andtime constraints did not exist, thenventure capitalists could evaluate all pro-posals. However, these conditions do notexist because information is costly andall information may not be revealed.Moreover, the time devoted to projectanalysis would limit the time to analyzeother projects or advice existing firms inthe venture capitalist’s portfolio. Venturecapitalists would be expected to selectinformation sources and types of infor-mation that offer the greatest largestvalue in analyzing firms within theirniche.

MethodologySample and Questionnaire

The sample consisted of the 63 firmsregistered in Asociación Española deEntidades de Capital-Riesgo (SpanishAssociation of VC Firms). A total of 51usable questionnaires were returned,providing a response rate of 80.95percent. A postal survey followed by tele-phone call was used to gather the data.

The questionnaire was developed andpretested in early 2001. A pretest of thequestionnaire was completed by econo-mists with experience in business valua-tion and financial risk and by venture

capitalists with experience in projectevaluation. Comments and suggestionsresulting from the pretest were incorpo-rated into the questionnaire as was nec-essary. Data were collected during Marchto June 2001.

The first section of the questionnairecollected information on the characteris-tics of the VC company and proposalevaluation. These questions included (1)type of VC company (VC firm, VC man-agement company, regional/industrialdevelopment society, and other); (2)source of capital (private versus public);(3) amount of funds managed (<6 millioneuros, 6–15 million euros, 15–30 millioneuros, and >30 million euros); (4)average evaluation time for accepted pro-posal (<1 month, 1–3 months, 3–6months, >6 months); (5) evaluation timefor rejected proposal (<1 month, 1–3months, 3–6 months, >6 months); and (6)percentage of rejected proposals (<30,31–50, 51–80, and >80); (7) number ofproposals received each year; and (8)percentage of investments during pastthree years by stage of development(seed, start-up, expansion, and maturity).

The next section of the questionnairecollected information on 12 aspects ofproposal evaluation. Questions included(1) source of first contact (from the VCfirm versus from the entrepreneur); (2)frequency (1–5 scale, 1 = never and 5 =always) of source of referral (venturecapitalist’s reputation, manager ofanother of VC company’s investment, VCcompany’s consultant, other VC’sinvestor, VC’s pursuit of new investment,state-owned company, other businessperson, financial institution, financingmediators, and other); (3) frequency ofventure capitalist expectations duringfirst contact (1–5 scale, 1 = never and 5= always) (interview of owner, informa-tion on position of company withinindustry, business plan, managementteam resume, and other); (4) ranking ofimportance (1–5 Likert scale, 1 = notimportant and 5 = very important) of

PINTADO, PÉREZ DE LEMA, AND VAN AUKEN 73

factors affecting acceptance or rejectionof proposal during initial screening (hightechnology company, viability of project,quality of management team, exit oppor-tunity, stage of development, and geo-graphic location); and (5) ranking ofimportance (1–5 Likert scale, 1 = notimportant and 5 = very important) ofinformation sources that are used to eval-uate proposals (financial press, inter-views with other owners in the economicsector, interviews with company man-agers, interviews with other companypersonnel, government statistics, salesand market information, product infor-mation, other VC firms, external account-ants or auditors, business plan cash flowprojections, business plan situationanalysis, business plan profits/losses,business plan global coherence, timeschedule, and management team’sresumes).

Additional questions in this sectionincluded: (6) required rate of return bystage of development; (7) ranking ofimportance (1–5 scale, 1 = not importantand 5 = very important) of VC firm’sfinancial requirements (minimum prof-itability independent of type of firm,minimum profitability depends on char-acteristics of investment, debt-to-equityratio falls within standard limits, debt-to-equity ratio appropriate to project risk,and required return depends on natureof investment); (8) ranking of factors(1–5 scale, 1 = not important and 5 = veryimportant) causing the VC firm to changetarget rate of return (expected time toexit, size of investment, industry condi-tions, economic conditions, changes inprofitability of equity market, changes inprofitability of debt market profitability,changes in interest rates, amount ofexpected from investment, industry/sector, geographic region, round offinancing, preplanned exit); (9) rankingof importance (1–5 scale, 1 = not impor-tant and 5 = very important) of entre-preneur attributes (honest/integrity,management team, work experience,

knowledge of the sector, leadershipskills, understanding of company objec-tives); (10) ranking of importance (1–5scale, 1 = not important and 5 = veryimportant) of product or services char-acteristics (proven product success,product’s stage of life cycle, marketingstrategy, high-tech product); (11) rankingof importance (1–5 scale, 1 = not impor-tant and 5 = very important) of marketcharacteristics (target has high potentialgrowth rate, company able to create anew market for product, high potentialgrowth rate of potential clients, VC firm’sexperience in market); and (12) fre-quency of use (1–5 scale, 1 = never and5 = always) of valuation methods (bookvalue, replacement value, discountedfuture cash flows, price earnings ratio(historic basis), price earnings ratio(prospective basis), recent industryprices, and industry ratios).

MethodologyThe data were initially summarized by

use of univariate statistics (means andfrequencies) to provide a better under-standing of the respondents and charac-teristics of the responding companies.The sample was subsequently segmentedinto two categories: early-stage (seed andstart-up phases) and late-stage firms(expansion, bridge, etc. phases). Theearly- and late-stage classification wasused by Allen and Song (2003) and DaRin, Nicodano, and Sembenelli (2005).

The nonparametric Mann–Whitney U-test and contingency tables were used toidentify differences between the cate-gories relative to stage of development.A nonparametric test was used becausethe assumption of normality of the pop-ulation distribution may not be valid.Yates’ correction for continuity was alsoused with the Pearson’s chi-square test(tables matrices are 2 × 2).

The development of risk capital inSpain occurred in stages that could becharacterized by a prevalence of publicinvestments in companies that were in

74 JOURNAL OF SMALL BUSINESS MANAGEMENT

PINTADO, PÉREZ DE LEMA, AND VAN AUKEN 75

the seed and start-up phases of develop-ment. Currently, private initiative is moreimportant for companies in the maturestages of development, although thepublic initiative continues to be relativelyimportant.

We are interested in analyzing therelationship between the stage of devel-opment and source of capital (private orpublic), size of funds managed, and hightechnology firm and geographic location.Two models using Wald’s stepwise logis-tic regressions were used in the analyses.This method is used because the vari-ables may not be normally distributed.

Model 1: SD = a0 + b1CAP + b2SIZE + eModel 2: SD = a0 + b1HT + b2GEO + e,

where SD = Stage of development (0 =early-stage and 1 = late-stage)

CAP = Source of capital (0 = private and1 = public)

SIZE = Amount of funds managed (1 =<6 million euros, 2 = 6–15 millioneuros, 3 = 15–30 million euros, and 4= >30 million euros)

HT = High-technology business (1–5scale, 1 = not important and 5 =important)

GEO = Geographic location (1–5 scale, 1= not important and 5 = important).

ResultsCharacteristics of Firm and Fund

Table 1 provides background infor-mation on the VC firm and proposal eval-uation. Approximately two-thirds of thefirms obtained capital from privatesources and the remaining one-thirdobtained capital from public funds. Thefirst contact between the VC firm andentrepreneur was almost always (82percent of the time) made by the VC firm.Over one-half (60.8 percent) of the VCfirms evaluate more than 100 proposalsper year. The majority of the VC firmsrespond relatively quickly to proposals.Approximately 56.9 percent of the firmsrespond in less than one month to pro-

posals that are rejected, while approxi-mately 72 percent of the firms respondin less than three months to proposalsthat are accepted.

Table 1 also shows a comparison ofthe background information relative tofirms that primarily invest in companiesin early versus late stages of develop-ment. A significantly higher percentageof VC firms invest in later-stage compa-nies than in early-stage companies, andthe difference is statistically significantwhether the VC funds come primarilyfrom private or public sources. The tablealso shows significant differencesbetween the percentage of proposalssubmitted by early- and late-stage firmsrelative to the number of proposalsreceived each year by the VC firm. Firmsreceiving fewer than 100 proposals peryear receive a significantly higher per-centage of proposals from firms in theearly stages of development than fromfirms in the late stages of development.Firms receiving more than 100 proposalsper year receive a significantly higherpercentage of proposals from firms in thelate stage of development than fromfirms in the early stages of development.No other statistically significant differ-ences between VC firm characteristicsrelative to stage of development areevident in the table.

Initial Contact between VentureCapital Firm and Entrepreneur

Table 2 shows the mean frequency ofmethod through which the first contactis established between the VC firm andentrepreneurs. The two most frequentmethods, the venture capitalist’s searchfor new investments (mean = 3.37) andcontacts through financing intermedi-aries (mean = 3.35), were the only twomethods of contact with a mean fre-quency of use above 3.0. The two leastfrequent methods of establishing firstcontact are through state-owned compa-nies (mean = 2.16) and the VC firm’swork with other firms (mean = 2.34). All

76 JOURNAL OF SMALL BUSINESS MANAGEMENT

other methods clustered between meansof 2.96 (other businessmen) and 2.52(firm managers).

The rankings of two methods of estab-lishing first contact differed significantlyrelative to stage of development of entre-preneur’s firm. Financing intermediarieswere used significantly more for the latestage of development firms, while state-owned companies were used signifi-cantly more for the early stage ofdevelopment firms.

Importance of Venture Capitalists’Evaluation Criteria

Table 3 shows the evaluation criteriaused by the venture capitalists in theirinitial screening of proposals. The top

three criteria, each of which had a meanranking above 4.0, were viability ofproject (mean = 4.94), quality of man-agement team (mean = 4.88), and exitopportunity (mean = 4.29). The standarddeviation (S.D.) of these criteria becamesmaller as the mean use became higher.This suggests greater consensus on theimportance of the most important crite-ria than on those less important. Theleast important criteria were high tech-nology (mean = 2.45), geographical loca-tion of firm (mean = 2.83), and firm’sstage of development (mean = 3.55).

Table 3 also shows the mean rankingsof importance of the evaluation criteriaby stage of development. The relativerankings are generally similar in both

Table 1Comparisons of Characteristics of Venture Capital Firms:Percentages and Chi-Square Tests of Significance (n = 51)

Variables Percentage of Firms Stage of Development

Source of Venture Capital Early Stage Late StagePrivate Capital 66.7 14.7** 85.3**Public Capital 33.3 33.3** 52.9**

Makes First ContactVenture Capital Firm 18.0 30.8 13.5Entrepreneur 82.0 69.2 86.5

Number of Proposals per Year< 100 60.8 84.6* 52.6*> 100 39.2 15.4* 47.4*

Average Time to Respond toa Rejected Proposal

< 1 month 56.9 53.8 57.91–3 months 43.1 46.2 42.1

Average Time to Respond toan Accepted Proposal

< 3 months 72.5 76.9 71.13–6 months 27.5 23.1 28.9

*Significant at 10 percent.**Significant at 5 percent.

***Significant at 1 percent.

PINTADO, PÉREZ DE LEMA, AND VAN AUKEN 77

Table 2Reasons for First Contact between Venture Capital Firmand Entrepreneur: Means and Standard Deviations (S.D.)of All Firms Mann–Whitney Test of Differences between

Means by Stage of Development (n = 51)

Reason for Contact All Firms Stage of Development

Mean S.D.Early Late

Venture Capital’s Pursuit of New Investments 3.37 0.82 3.15 3.45Financing Mediators 3.35 1.11 2.27*** 3.66***Other Businessmen 2.96 0.92 2.83 3.00Referral from Financial Institution 2.90 1.05 2.83 2.92Venture Capital Firm’s Other Investment 2.71 1.05 2.27 2.84Venture Capital’s Consultants 2.69 0.85 2.45 2.76Firm Managers 2.52 0.74 2.75 2.44Venture Capitalist’s Work with Other Firms 2.34 0.81 2.18 2.39State-Owned Companies 2.16 1.09 2.83*** 1.91***

*Significant at 10 percent.**Significant at 5 percent.

***Significant at 1 percent.

Table 3Ranking of Importance of Factors Affecting Evaluation of

Initial Screening of Proposal Mean and Standard Deviationof All Firms and Mann–Whitney Test of Differencesbetween Means by Stage of Development (n = 51)

Evaluation Criteria All Firms Stage of Development

Mean S.D.Early Late

Viability of Project 4.94 0.24 4.83* 4.97*Quality of Management Team 4.88 0.33 4.77 4.92Exit Opportunity 4.29 0.87 4.00 4.38Development Stage of Firm 3.55 0.79 3.46 3.58Geographical Location of Firm 2.83 1.58 4.08*** 2.37***Project on High Technology 2.45 1.17 3.31*** 2.14***

*Significant at 10 percent.**Significant at 5 percent.

***Significant at 1 percent.

78 JOURNAL OF SMALL BUSINESS MANAGEMENT

categories. The main difference is thatgeographic location is ranked as beingmuch more important when the firm isin the early stage of development (mean= 4.08) than when it is in a later stage ofdevelopment (mean = 2.37). Venture capitalists are probably more attentive toearly-stage firms because of their greaterrisk of failure and therefore may preferthat early-stage firms be located in closerproximity.

Two other significant differencesbetween early- and late-stage firms’ eval-uation criteria mean rankings of impor-tance are evident in Table 3. The viabilityof the project is more important for late-stage firms (mean = 4.97) than for early-stage firms (mean = 4.83). Time tomarket, viability, and exit opportunitiesmay be easier to assess and thus morerelevant for late-stage firms. Also, theimportance of the degree of technology

is more important for early-stage (mean= 3.31) than for late-stage firms (mean =2.14). Although relatively unimportantfor both categories of firms, technologyis more important for early-stage than forlate-stage firms.

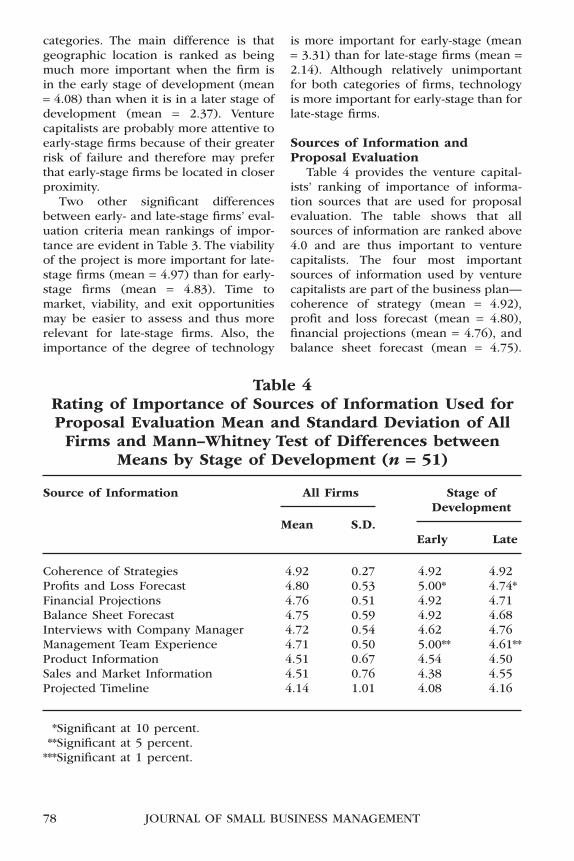

Sources of Information andProposal Evaluation

Table 4 provides the venture capital-ists’ ranking of importance of informa-tion sources that are used for proposalevaluation. The table shows that allsources of information are ranked above4.0 and are thus important to venturecapitalists. The four most importantsources of information used by venturecapitalists are part of the business plan—coherence of strategy (mean = 4.92),profit and loss forecast (mean = 4.80),financial projections (mean = 4.76), andbalance sheet forecast (mean = 4.75).

Table 4Rating of Importance of Sources of Information Used forProposal Evaluation Mean and Standard Deviation of AllFirms and Mann–Whitney Test of Differences between

Means by Stage of Development (n = 51)

Source of Information All Firms Stage ofDevelopment

Mean S.D.Early Late

Coherence of Strategies 4.92 0.27 4.92 4.92Profits and Loss Forecast 4.80 0.53 5.00* 4.74*Financial Projections 4.76 0.51 4.92 4.71Balance Sheet Forecast 4.75 0.59 4.92 4.68Interviews with Company Manager 4.72 0.54 4.62 4.76Management Team Experience 4.71 0.50 5.00** 4.61**Product Information 4.51 0.67 4.54 4.50Sales and Market Information 4.51 0.76 4.38 4.55Projected Timeline 4.14 1.01 4.08 4.16

*Significant at 10 percent.**Significant at 5 percent.

***Significant at 1 percent.

PINTADO, PÉREZ DE LEMA, AND VAN AUKEN 79

This finding supports the central impor-tance of a good business plan whenseeking VC. The sources of informationranked as being least important (but stillranked as important) were projectedtimeline (mean = 4.14), experience of themanagement team (mean = 4.71), salesand market information (mean = 4.51),and product information (mean = 4.51).The generally low standard deviationssuggest relatively high agreement of therankings among the venture capitalists.

Table 4 also reports means for rank-ings of importance of the sources ofinformation for the evaluation of early-and late-stage companies. Mean rankingsof importance are generally similar forthe two types of companies. The mostnoticeable differences are that profitsand losses from the business plan are asignificantly (10 percent significancelevel) more important source of infor-mation for early-stage firms (mean =5.00) than for late-stage firms (mean =4.74). Additionally, the managementteam is a significantly more importantsource of information for early-stage(mean = 5.00) than for late-stage (mean= 4.61) firms. The significantly higherrankings of importance are likely a resultof longer time to market and profitabil-ity for early-stage than for late-stagefirms. Management experience is veryimportance in leading the firm throughthe development and market entryphases.

Assessment of Required Rate of Return

Table 5 provides a description of twoaspects of the venture capitalists’ assess-ment of required rate of return. Panel Ashows venture capitalists’ required ratesof return on investment relative to stageof development. The results indicate thata higher percentage of venture capitalistsrequire higher rates of return on invest-ments in earlier stages than in laterstages of development. Correspondingly,a higher percentage of VC firms require

lower rates of return on investments inlater stages of development. This resultis consistent with financial theory thatstates that higher risk investments (forexample, early-stage firms) shouldprovide higher expected returns and thatlower risk investments (for example, late-stage firms) should provide lowerexpected returns.

Panel B of Table 5 shows the meanranking of importance of factors affect-ing venture capitalists’ assessment of therequired rate of return on proposedinvestments. All factors of evaluationwere ranked relatively high (all above3.0) in importance by the venture capi-talists. The factor ranked highest inimportance was that the minimumrequired return depends on the charac-teristics of the investment (mean = 4.20).This assessment suggests that therequired return will vary relative to thegeneral characteristics of the proposal.This finding may be consistent withPanel A in that a proposal with charac-teristics that suggest greater risk wouldlikely have a higher required rate ofreturn, whereas proposals with charac-teristics that suggest less risk wouldlikely have a lower required rate ofreturn. Notably, the two lowest-rankedfactors are that the required rate ofreturn does not depend on the charac-teristics of the proposal (mean = 3.20)and that the debt-to-equity depends on risk (mean = 3.14). The low rankingson these factors suggest that specific criteria are not as important as a general risk assessment during proposalreview.

Panel B shows mean rankings by thefirms’ stage of development. The impor-tance of proposal evaluation criteria issimilar for both categories of firms. Inmost cases, however, factors affecting therequired rate of return were more impor-tant for evaluating early-stage firms thanlate-stage firms. Two significant differ-ences between early- and late-stagefirms’ assessment of factors affecting

80 JOURNAL OF SMALL BUSINESS MANAGEMENT

required return are that (1) acceptabledebt-to-equity ratio varies by risk beingsignificantly more important in early-stage (mean = 4.38) than in late-stagefirms (mean = 3.75), and (2) debt-to-equity ratio being within standard limitsis significantly more important for early-stage (mean = 3.85) than late-stage(mean = 2.89) firms. These resultssuggest that proposal evaluation isdependent on venture characteristics,analysis of risk is more important in the

early than the late stage of development,and debt levels impact the assessment ofrequired rate of return.

Importance of Owner, Product,and Market

The venture capitalists’ rankings ofimportance (overall and by stage ofdevelopment) of criteria for owner,product, and market characteristics areshown in Table 6. All characteristics ofthe owner are ranked as being very

Table 5Required Rate of Return and Factors Affecting Required

Rate of Return Relative to Stage of Development (n = 51)

Panel A: Required Rate of Return by Stage of DevelopmentPercentages and Chi-Square Tests of Significance

Required All Firms Stage of Development

Return

Early Late Stage Early (percent) Late (percent)(percent)

Stage (percent)

Early-Stage Late-Stage Early-Stage Late-Stage(percent)

Investments Investments Investments Investments

< 15 12.2 8.5 27.3** 6.7** 20.0* 5.4*

15–25 12.2 57.4 18.2** 10.0** 80.0* 51.4*

26–35 19.5 29.8 36.4** 13.3** 0* 37.8*

> 35 56.1 4.3 18.2** 70.0** 0* 5.4*

Panel B: Factors Affecting Required Rate of Return Mean and Standard Deviation of All Firms and Mann–Whitney Test of Differences between Means by

Stage of Development

Factor All Firms Stage of

Development

Mean S.D.

Early Late

Depends on Characteristics of Investment 4.20 0.99 4.31 4.16

Debt-to-Equity Ratio Depends on Risk 3.92 1.04 4.38** 3.75**

Total Yield Depends on Investment 3.92 1.06 3.85 3.94

Does Not Depend on Characteristics of Investment 3.20 1.02 3.31 3.17

Debt-to-Equity Ratio within Standard Limits 3.14 1.22 3.85** 2.89**

*Significant at 10 percent.

**Significant at 5 percent.

***Significant at 1 percent.

PINTADO, PÉREZ DE LEMA, AND VAN AUKEN 81

important (honesty/integrity = 4.84,knowledge of the sector = 4.75, workexperience = 4.69, management team =4.49, leadership skills = 4.42, and under-standing company objectives = 4.36). Therelatively low S.D.s suggest high agree-ment among the respondents.

Three of the product characteristicsranked as important (proven productsuccess = 4.44, product stage of life cycle= 4.14, and marketing strategy = 4.0) are

also ranked relatively similarly. The rela-tively small and similar S.D.s of theserankings suggest consistency of rankingof importance among the respondents.The importance of the product being ori-ented toward high technology (mean =2.86) was ranked considerably lowerthan other factors. Market issues relatedto the product are much more importantthan whether the product is orientedtoward high technology.

Table 6 Ranking of Importance of Characteristics of Owner,

Product, and Market: Means and Standard Deviations ofAll Firms and Mann–Whitney Test of Differences between

Means by Stage of Development (n = 51)

All Firms Stage of Development

Mean S.D.Early Late

OwnerHonesty and Integrity 4.84 0.37 4.85 4.84Knowledge of the Sector 4.75 0.44 4.92* 4.68*Work Experience 4.69 0.55 4.92* 4.61*Management Team 4.49 0.58 4.46 4.50Leadership Skills 4.42 0.67 4.42 4.42Understands Company Objectives 4.36 0.66 4.46 4.32

ProductProven Product Success 4.44 0.76 4.31 4.49Product’s Stage of Life Cycle 4.14 0.74 4.38 4.06Marketing Strategy 4.00 0.73 4.08 3.97High-Tech Product 2.86 1.15 3.77*** 2.53***

MarketTarget Market Has High Potential 4.45 0.58 4.62 4.39

Growth RateCompany Able to Create a New Market 3.98 0.76 3.77 4.05

for ProductHigh Potential Growth Rate of Potential 3.96 0.80 3.85 4.00

ClientsVenture Capital Firm’s Experience in Market 3.39 0.98 3.00 3.53

*Significant at 10 percent.**Significant at 5 percent.

***Significant at 1 percent.

82 JOURNAL OF SMALL BUSINESS MANAGEMENT

Market-related factors are generallyranked as being less important thanowner and product characteristics. Theexception is “target market has highpotential growth” (mean = 4.45). Marketpotential is directly related to futuremarket demand, revenue forecasts, and,thus, profit potential. Due diligence ofthe proposal would be incompletewithout assessing market potential.Ability to create a new market for theproposed product (mean = 3.98), highpotential customer growth rate (mean =3.96), and firm’s market experience(mean = 3.39) are also important criteriawhen venture capitalists evaluate firms.

Table 6 also compares the mean rank-ings of the importance of owner,product, and market characteristics forthe entire sample and by stage of devel-opment. The table shows that several ofthe mean rankings differ significantlyaccording to stage of development. Theimportance of the product being ori-

ented toward high technology is signifi-cantly more important for investments inearly-stage firms (mean = 3.77) than forlate-stage firms (mean = 2.53). Althougha much riskier investment, venture capi-talists believe that investments in hightechnology are much more important forearly-stage than for late-stage firms. Twoowner characteristics (knowledge of the industrial sector and work experi-ence) were weakly more significant forfirms in the early stage than for those inthe late stage of development. No otherstatistically significant differences wereevident between the two categories offirms.

Methods Used to ValueEntrepreneurial Firm

Table 7 shows how frequently sevencompany valuation methods were used.Discounted cash flow analysis, which isbased on finance theory associated witha firm’s risk and return characteristics, is

Table 7Mean Ranking of Importance of Method Used to Value

Company Means and Standard Deviations of All Firms andMann–Whitney Test of Differences between Means by Stage

of Development (n = 51)

All Firms Stage ofDevelopment

Mean S.D.Early Late

Discounted Future Cash Flows 4.20 0.94 4.15 4.21Price Earnings Ratio (Prospective Basis) 3.80 1.22 3.23* 4.00*Recent Prices in Industry 3.72 1.09 3.00*** 3.97***Ratios Unique to Industry 3.68 1.24 2.92*** 3.95***Price Earnings Ratio (Historic Basis) 3.56 1.22 3.08* 3.74*Book Value 2.62 1.41 3.23* 2.41*Replacement Value 2.24 1.03 2.77* 2.06*

*Significant at 10 percent.**Significant at 5 percent.

***Significant at 1 percent.

PINTADO, PÉREZ DE LEMA, AND VAN AUKEN 83

Table 8Correlations and Significance (in Parentheses) among Type

of Capital and Size (n = 51)

Variables Type of Capital VC Size VC

Type of VC 1.000Size of VC −0.279 (0.048) 1.000

Correlations and Significance (in parentheses) among High-Technology Business and Geographic Location

(n = 51)

Variables High-Technology GeographicBusiness Location

High-Technology Business 1.000Geographic Location 0.356 (0.014) 1.000

used most frequently (mean = 4.20). Thefrequency of use of four other methods(price earnings ratio—forecast values[3.80], recent prices in the industry [3.72],ratio analysis [3.68], and price earningsratio—historical values [3.56]) were verysimilar. Book value [mean = 2.62] andreplacement value [mean = 2.24] wereused much less frequently.

A comparison of the frequency of usebetween early- and late-stage firms indi-cates several significant differences.Almost every difference between the twocategories of firms shows that the valua-tion technique is used more frequentlywhen the firm is in the later stage asopposed to the early stage of develop-ment. The only exception is that replace-ment value is used significantly lessfrequently when the firm is in the laterather than in the early stage of devel-opment. No significant difference isevident in the use of discount cash flowbetween the two categories of firms.

A Wilcoxin chi-square test evaluateddifferences between mean frequencies ofuse of valuation methods. The most sig-nificant findings from these tests (notpresented in a table) are that discountedcash flow is used significantly more often(1 percent level of significance) andreplacement value is used significantlyless often (1–5 percent level of signifi-cance) than other valuation methods.Discounted cash flow is clearly favored,and replacement value is obviously notpreferred to value firms.

Logistic Regression AnalysisSpearman correlations (shown in

Table 8) between the independent vari-ables were used to determine significantrelationships between the variables. Thecorrelation coefficients indicate a lowrelationship between the variables. Mul-ticollinearity should, thus, not be aproblem.

84 JOURNAL OF SMALL BUSINESS MANAGEMENT

Table 9 shows the results of the Logitregression analysis that examined therelationship between stage of develop-ment (dependent variable) and (1) VCcharacteristics (type of capital and size)(model 1), and (2) investment prefer-ences (high-technology business andgeographic location) (model 2). The joint

significance of the variables is acceptedby the likelihood and Hosmer andLemeshow tests (model 1: χ2 = 7.112;sig.: 0.212; model 2: χ2 = 0.216; sig.:0.898). The Cox and Snell R2 and Nagelk-erke R2 also show good fit. In model 1,the results indicate that the coefficientsfor type of capital (−1.746) is significant

Table 9Logit Regression Results: MODEL 1

Stage of Development versus Type of Capital and Size (n = 51)

Independent Variables Regression Wald Significance Exp (B)Coefficient

Type of capital −1.746 4.792 0.029 0.174Size 0.954 8.147 0.004 2.597Constant 0.910 0.466 0.495 2.484Model FitOmnibus Test of Model: χ2 = 15.775 0.000−2 Log Likelihood = 42.126Cox and Snell R2 = 0.266Nagelkerke R2 = 0.392Hosmer—Lemeshow test: χ2 = 7.112 0.21282.4 percent correct classification

Logit Regression Results: MODEL 2Stage of Development versus High-Tech and Geographical Situation (n = 51)

Independent Variables Regression Wald Significance Exp (B)Coefficient

High Tech −1.802 4.943 0.026 0.165Geographic Location −1.840 5.088 0.024 0.159Constant 2.559 13.465 0.000 12.926Model FitOmnibus Test of Model: χ2 = 15.195 0.001−2Log Likelihood = 40.238Cox and Snell R2 = 0.276Nagelkerke R2 = 0.399Hosmer—Lemeshow test: χ2 = 0.216 0.89883.0 percent correct classification

PINTADO, PÉREZ DE LEMA, AND VAN AUKEN 85

at 5 percent. The coefficient for size(0.954) is significant at 1 percent. Venturecapital companies that invest more oftenin late-stage companies are mainlyprivate and larger firms than those thatinvest primarily in early-stage compa-nies. Model 2 results indicate that thecoefficients for high-tech (−1.802) andgeographic location (−1.840) are sig-nificant at 5 percent. Venture capital companies that invest more often in late-stage companies give less impor-tance to the geographical localizationand whether the company is high tech-nology when valuing proposals than VCcompanies that invest more often inearly-stage companies.

ConclusionsThis study examined the investment

decisions of a sample of 51 Spanish VC firms. More insight into decision criteria and processes can enable firmsto develop more targeted strategies to attract VC and to aid VC firms to better understand investment decisionprocesses. An important contribution ofthe study is the empirical evidence onthe venture capitalists’ decisions relativeto firms’ stage of development. Thecurrent Spanish venture market is heavilybiased toward mature expansion-phase firms in traditional sectors, withlittle investment in technology-basedstart-ups (Tejado 2003). This lack ofinvestment diversification may restrictfuture economic development and competitiveness.

The findings provided insight intoseveral areas of the Spanish entrepre-neur—VC relationship. Approximatelytwo-thirds of the Spanish VC firms obtaincapital from private sources. Over one-half evaluate more than 100 proposalsper year. The majority of the Spanish VCfirms respond quickly to proposals,while most invest in late-stage compa-nies. Venture capital firms receivingfewer than 100 proposals per year

receive a higher proportion of proposalsfrom early-stage companies, while VCfirms receiving more than 100 proposalsper year receive proportionately moreproposals from late-stage companies.The top three criteria for evaluating pro-posals were viability of project, quality ofmanagement team, and exit opportunity.The relative importance of the rankingsis generally similar for early- and late-stage companies. All sources of informa-tion used for proposal evaluation wereranked as being important for both cat-egories of firms.

The first contact, typically initiated bythe VC firm, most commonly occurredthrough the venture capitalist’s search for new investments and through financ-ing intermediaries. Financing inter-mediaries were used significantly more often to initiate contact with late-stagefirms, while state-owned companies were used significantly more often to initiate contact with early-stage firms.Private VC firms invest more during the late development stages, while pub-lic VC firms invest more during the early stages. High technology and loca-tion are more important initial screen-ing criteria for early VC firms than forlate VC firms. Characteristics of theentrepreneur, manager background,and management team experience wereconsistently more important evaluationcriteria than market and product characteristics.

Two finance-related issues that wereexamined in the study were expectedrate of return and proposal valuationmethods. The results showed that ahigher percentage of VC firms required ahigher rate of return on investment inearly-stage than late-stage of develop-ment firms. This result is consistent withfinancial theory that states that high-riskinvestments (for example, early stagefirms) should be associated with highexpected returns and that low-riskinvestments (for example, late-stage

86 JOURNAL OF SMALL BUSINESS MANAGEMENT

firms) should be associated with lowexpected returns (Timmons and Spinelli2004). Evaluation factors affecting therequired rate of return were generallyranked as being more important forearly-stage than late-stage firms. Two sig-nificant differences between the assess-ments of early- and late-stage firms’expected return are that the acceptabledebt-to-equity ratio and “debt-to-equityratio being within standard limits” aremore important in the analysis of early-than late-stage firms. This is consistentwith proposal evaluation being depend-ent on the venture characteristics andwith risk being a more important crite-rion in the early than in the late stagesof development (Tyebjee and Bruno1984). The valuation method used mostoften was discounted cash flow analysis.Logit regression analysis indicated thatVC companies that invest more often inearly-stage companies (1) are smallerand acquire resources from public organ-izations and (2) place greater emphasison the geographic location and techno-logical intensity than those that investprimarily in late-stage companies whenevaluating a company.

The results can be used by govern-ment policymakers, firms seeking VC, VCfirms, consultants, and support agenciesthat provide capital-acquisition assis-tance. A greater understanding of VCdecision-making can assist in the devel-opment of government policies thatpromote VC investing. New governmentpolicies could promote investment diver-sification into industry segments not cur-rently receiving high VC investments.Better insight into the decision processesof venture capitalists can enable firms toprepare better capital-acquisition strate-gies. The more comprehensive industry-wide perspective can enhance a VC firm’sinvestment analysis policies and proce-dures. The greater insight into capitalacquisition and investment analysis canenable consultants and support agenciesto improve the advice they give to com-

panies and VC firms. Information is thisstudy could easily be built into businesstraining programs and be incorporatedinto university classes that include mate-rial related to VC.

The study has several limitations thatprovide avenues for potential futureresearch. Because the sample was rela-tively small, future studies could includemore firms. A larger sample size mayallow comparison by type of investment,stage of development, or size of invest-ment. Such a study could include empir-ical test to determine whether therelationships in Figure 1 are valid invarious countries. The data were also col-lected at a single point in time. A longi-tudinal study could provide evidence onthe changes in evaluation over time.Future studies could expand the scope ofresearch to include postinvestment activ-ities and could compare investment deci-sions among venture capitalists in Spain,the United States, and the UnitedKingdom.

ReferencesAdmati, A., and P. Pfleiderer (1994).

“Robust Financial Contracting and theRole of Venture Capitalists,” Journal ofFinance 49, 371–402.

Allen, F. and W.L. Song (2003). “VentureCapital and Corporate Governance,”The Warton Financial InstitutionsCenter, Working Paper 03–05, Univer-sity of Pennsylvania, Philadelphia,September.

Amit, R., J. Brander, and C. Zott (1998).“Why Do Venture Capital Firms Exist?Theory and Canadian Evidence,”Journal of Business Venturing 13,441–466.

Arthurs, J. and L. Busenitz (2003). “Theo-retical Foundations of the VentureCapitalist/Entrepreneurs Relationship:Current Issues and Future Directions,”Entrepreneurship: Theory and Prac-tice 28(2), 145–162.

ASCRI (2004). Capital Riesgo Y PrivateEquity En España. Madrid: Asociación

Española De Entidades De CapitalRiesgo.

Barry, C. (1994). “New Directions inResearch on Venture Capital Finance,”Financial Management 23(3), 3–15.

Busenitz, L., J. Fiet, and D. Moesel (2005).“Signaling in Venture Capitalist-NewVenture Team Funding Decisions:Does It Indicate Long-Term VentureOutcomes?” Entrepreneurship: Theoryand Practice 29(1), 1–12.

Cano, C., and L. Cazorla (1998). “Elmodelo andaluz de capital riesgo:situación actual y perspectivas. Unacomparación a escala nacional,”Revista de Estudios Regionales 51,121–143.

Carter, R., and H. Van Auken (1994).“Venture Capital Firms’ Preferencesfor Projects in Particular StagesofDevelopment,” Journal of Small Busi-ness Management 32(1), 60–74.

Chan, Y. (1983). “On the Positive Role ofFinancial Intermediation in Allocationof Venture Capital in a Market withImperfect Information,” The Journal ofFinance 38(5), 1543–1561.

Da Rin, M., G. Nicodano, and A. Sem-benelli (2005). “Public Policy and theCreation of Active Venture CapitalMarkets,” Working Paper Series n°.430, January, European Central Bank,Madrid.

Deeds, D., D. Decarolis, and J. Coombs(1997). “The Impact of Firm-SpecificCapabilities on the Amount of CapitalRaised in a Initial Public Offering: Evi-dence from the Biotechnology Indus-try,” Journal of Business Venturing 12,31–46.

Fried, V., and R. Hisrich (1994). “Towarda Model of Venture Capital InvestmentDecision Making,” Financial Manage-ment 23(3), 28–37.

Gompers, P. (1995). “Optimal Investment,Monitoring, and the Staging ofVenture Capital,” Journal of Finance50(5), 1461–1489.

Gupta, A., and H. Sapienza (1994).“Determinants of Venture Capital

Firms’ Preferences Regarding theIndustry Diversity and GeographicScope of Their Investments,” Journalof Business Venturing 7, 347–362.

Harvey, M., and R. Lusch (1995).“Expanding the Nature and Scope ofDue Diligence,” Journal of BusinessVenturing 10(1995), 5–21.

Lam, S. (1991). “Venture Capital Financ-ing: A Conceptual Framework,”Journal of Business Finance andAccounting 18(2), 137–149.

Landstrom, H. (1992). “The Relationshipbetween Private Investors and SmallFirms: An Agency Perspective,” Entre-preneurship and Regional Develop-ment 9, 199–223.

Lerner, J. (1994). “The Syndication ofVenture Capital Investments,” Finan-cial Management 23(3), 16–27.

——— (1995). “Venture capitalists andthe oversight of private firms,” Journalof Finance 50(1), 301–318.

Lindsey, L. (2003). “The Venture Capital Keiretsu Effect: An Empirical Analysis of Strategic Alliances AmongPortfolio Firms,” Mimeo, Stanford University.

Macmillan, I., R. Siegel, and P. Subba-narasimha (1985). “Criteria Used byVenture Capitalists to Evaluate NewVenture Proposals,” Journal of Busi-ness Venturing 1, 119–128.

Manigart, S., K. De Waele, M. Wright, K.Robbie, P. Desbrières, H. Sapienza,and A. Beekman (2002). “Determi-nants of Required Return in VentureCapital Investment: A Five-CountryStudy,” Journal of Business Venturing17, 291–312.

Manigart, S., M. Wright, K. Robbie, P.Desbrières, and K. De Waele (1998).“Venture Capitalists’ Appraisal ofInvestment Projects: An EmpiricalEuropean Study,” Entrepreneurship:Theory & Practice 21(4), 29–43.

Michelacci, C., and J. Suarez (2004).“Business Creation and the StockMarket,” Review of Economic Studies71(2), 459–481.

PINTADO, PÉREZ DE LEMA, AND VAN AUKEN 87

88 JOURNAL OF SMALL BUSINESS MANAGEMENT

Norton, E., and B. Tenenbaum (1993).“Specialization Versus Diversificationas a Venture Capital Investment Strat-egy,” Journal of Business Venturing 8,431–442.

Repullo, R., and J. Suarez (2004).“Venture Capital Finance: A SecurityDesign Approach,” Review of Finance8, 75–108.

Ruhnka, J., and J. Young (1997). “AVenture Capital Model of the Devel-opment Process for New Ventures,”Journal of Business Venturing 12,167–184.

Sahlman, W. (1990). “The Structure andGovernance of Venture Capital Orga-nizations,” Journal of Financial Eco-nomics 27, 473–521.

Sapienza, H., and A. Gupta (1994).“Impact of Agency Risks and TaskUncertainty of Venture Capitalist-CEOInteraction,” Academy of ManagementJournal 37(6), 1618–1632.

Tejado, R. (2003). “Venture Capital PolicyReview: Spain,” Working Paper2003/18, Organization for EconomicCooperation and Development,Madrid.

Timmons, J., and S. Spinelli (2004). “NewVenture Creation,” 6th ed. Boston:Irwin McGraw-Hill.

Tyebjee, T., and A. Bruno (1984). “AModel of Venture Capitalist Invest-ment Activity,” Management Science30, 1051–1066.

Van Auken, H. (2001). “Financing SmallTechnology-Based Companies: TheRelationship between Familiarity with Capital and Ability to Price andNegotiate Investment,” Journal ofSmall Business Management 30(3),240–258.

Wright, M., and K. Robbie (1996).“Venture Capitalists, Unquoted EquityInvestment Appraisal and the Role ofAccounting Information,” Accountingand Business Research 26(2),153–168.

——— (1998). “Venture Capital andPrivate Equity: A Review and Synthe-sis,” Journal of Business Finance andAccounting 25(5), 306–356.

Wright, M., K. Robbie, and C. Ennew(1997). “Venture Capitalists and SerialEntrepreneurs,” Journal of BusinessVenturing 12(3), 161–249.

Zacharakis, A., and D. Meyer (2000).“The Potential of Actuarial Models Can They Improve the Venture Capital Investment Decision?” Journalof Business Venturing 15(4), 323–346.