Vendor Audit: I Can Too Learning Center, LLC - dds.ca.gov · DEPARTMENT OF DEVELOPMENTAL SERVICES...

19

DEPARTMENT OF DEVELOPMENTAL SERVICES AUDIT OF I CAN TOO LEARNING CENTER, LLC Programs and Services: Infant Development Program – HS0468, HS0698 Client/Parent Support Behavior Intervention Training – PS0044 Audit Period: July 1, 2011 through June 30, 2012 Audit Branch Auditors: Michael Masui, Chief of Vendor Audits Alton Kitay, Supervisor Aaron Lomanto, Lead Auditor Pardeep Deol, Auditor

Transcript of Vendor Audit: I Can Too Learning Center, LLC - dds.ca.gov · DEPARTMENT OF DEVELOPMENTAL SERVICES...

DEPARTMENT

OF

DEVELOPMENTAL SERVICES

AUDIT

OF

I CAN TOO LEARNING CENTER LLC

Programs and Services Infant Development Program ndash HS0468 HS0698

ClientParent Support Behavior Intervention Training ndash PS0044

Audit Period July 1 2011 through June 30 2012

Audit Branch

Auditors Michael Masui Chief of Vendor Audits Alton Kitay Supervisor Aaron Lomanto Lead Auditor Pardeep Deol Auditor

I CAN TOO LEARNING CENTER LLC

TABLE OF CONTENTS

Page(s)

Executive Summary 1

Background 2

Objective Scope and Methodology 2-3

Conclusion 4

Views of Responsible Officials4

Restricted Use 4

Findings and Recommendations 5-7

Attachment A-Summary of Unsupported Billings amp Failure to Bill 8-10

Attachment B-Unsupported Billings amp Failure to Bill Adjustments 11-13

Attachment C-Response from Vendor 14-15

Attachment D-Evaluation of Vendor Response 16-17

ii

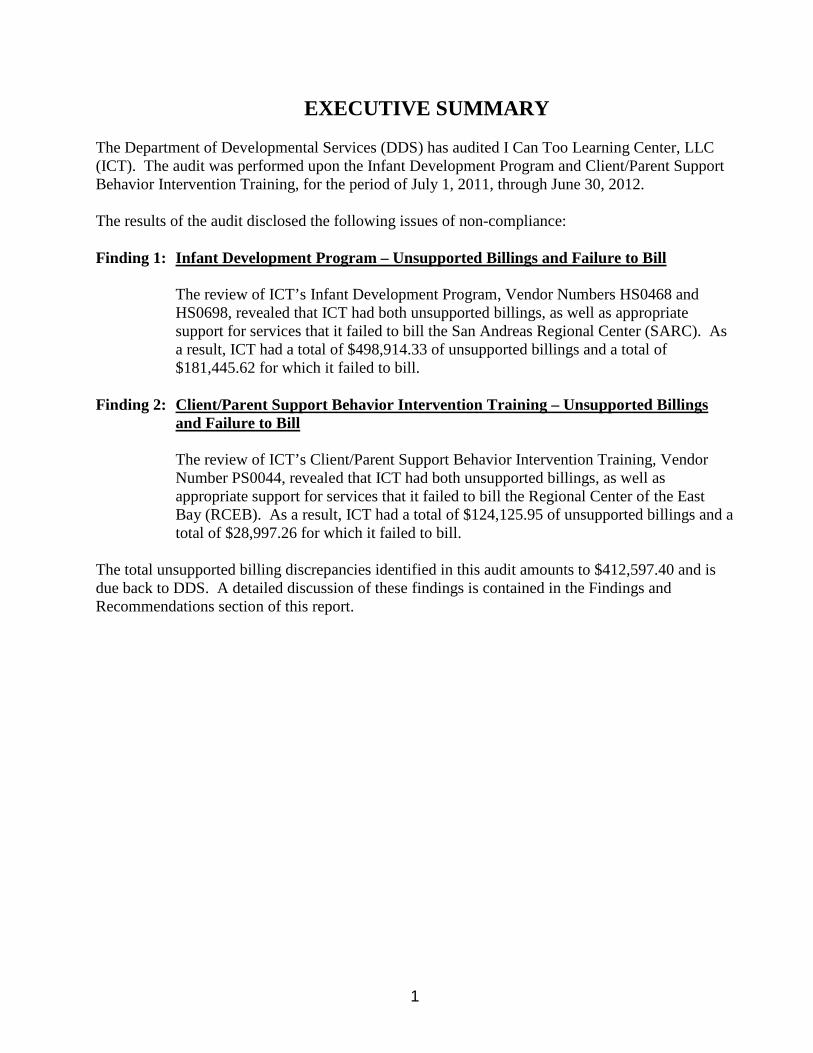

EXECUTIVE SUMMARY

The Department of Developmental Services (DDS) has audited I Can Too Learning Center LLC (ICT) The audit was performed upon the Infant Development Program and ClientParent Support Behavior Intervention Training for the period of July 1 2011 through June 30 2012

The results of the audit disclosed the following issues of non-compliance

Finding 1 Infant Development Program ndash Unsupported Billings and Failure to Bill

The review of ICTrsquos Infant Development Program Vendor Numbers HS0468 and HS0698 revealed that ICT had both unsupported billings as well as appropriate support for services that it failed to bill the San Andreas Regional Center (SARC) As a result ICT had a total of $49891433 of unsupported billings and a total of $18144562 for which it failed to bill

Finding 2 ClientParent Support Behavior Intervention Training ndash Unsupported Billings and Failure to Bill

The review of ICTrsquos ClientParent Support Behavior Intervention Training Vendor Number PS0044 revealed that ICT had both unsupported billings as well as appropriate support for services that it failed to bill the Regional Center of the East Bay (RCEB) As a result ICT had a total of $12412595 of unsupported billings and a total of $2899726 for which it failed to bill

The total unsupported billing discrepancies identified in this audit amounts to $41259740 and is due back to DDS A detailed discussion of these findings is contained in the Findings and Recommendations section of this report

1

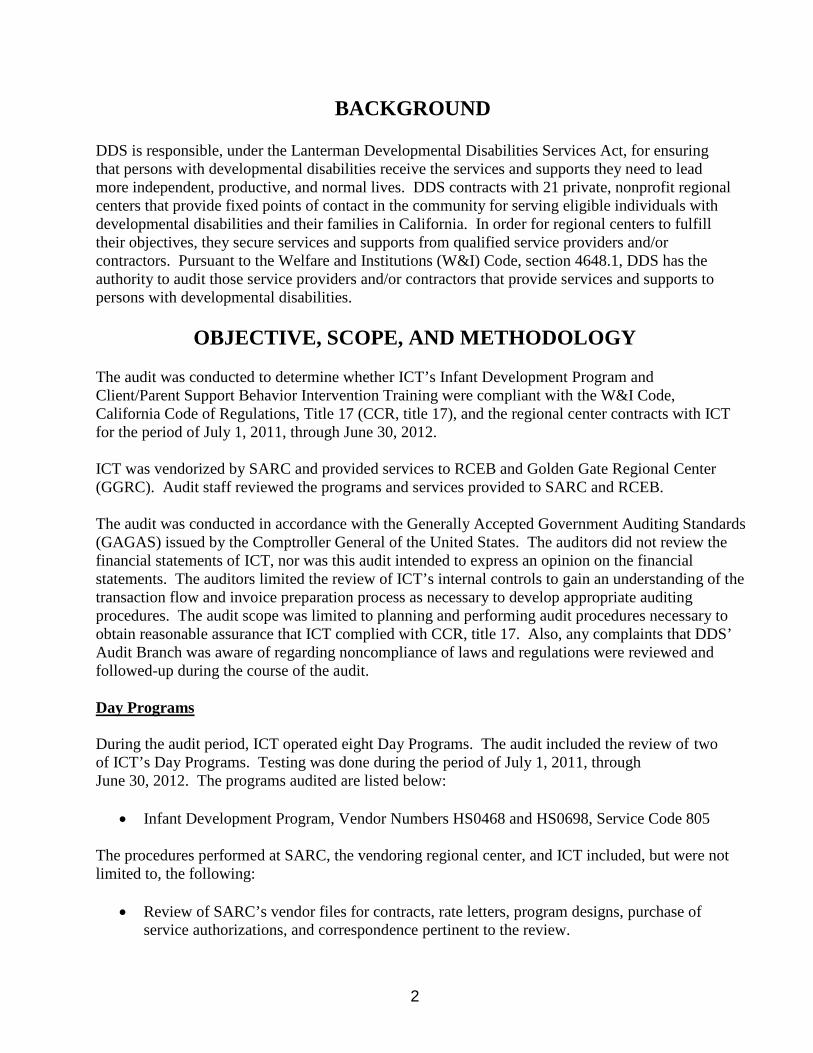

BACKGROUND

DDS is responsible under the Lanterman Developmental Disabilities Services Act for ensuring that persons with developmental disabilities receive the services and supports they need to lead more independent productive and normal lives DDS contracts with 21 private nonprofit regional centers that provide fixed points of contact in the community for serving eligible individuals with developmental disabilities and their families in California In order for regional centers to fulfill their objectives they secure services and supports from qualified service providers andor contractors Pursuant to the Welfare and Institutions (WampI) Code section 46481 DDS has the authority to audit those service providers andor contractors that provide services and supports to persons with developmental disabilities

OBJECTIVE SCOPE AND METHODOLOGY

The audit was conducted to determine whether ICTrsquos Infant Development Program and ClientParent Support Behavior Intervention Training were compliant with the WampI Code California Code of Regulations Title 17 (CCR title 17) and the regional center contracts with ICT for the period of July 1 2011 through June 30 2012

ICT was vendorized by SARC and provided services to RCEB and Golden Gate Regional Center (GGRC) Audit staff reviewed the programs and services provided to SARC and RCEB

The audit was conducted in accordance with the Generally Accepted Government Auditing Standards (GAGAS) issued by the Comptroller General of the United States The auditors did not review the financial statements of ICT nor was this audit intended to express an opinion on the financial statements The auditors limited the review of ICTrsquos internal controls to gain an understanding of the transaction flow and invoice preparation process as necessary to develop appropriate auditing procedures The audit scope was limited to planning and performing audit procedures necessary to obtain reasonable assurance that ICT complied with CCR title 17 Also any complaints that DDSrsquo Audit Branch was aware of regarding noncompliance of laws and regulations were reviewed and followed-up during the course of the audit

Day Programs

During the audit period ICT operated eight Day Programs The audit included the review of two of ICTrsquos Day Programs Testing was done during the period of July 1 2011 through June 30 2012 The programs audited are listed below

bull Infant Development Program Vendor Numbers HS0468 and HS0698 Service Code 805

The procedures performed at SARC the vendoring regional center and ICT included but were not limited to the following

bull Review of SARCrsquos vendor files for contracts rate letters program designs purchase of service authorizations and correspondence pertinent to the review

2

bull Interview of SARCrsquos staff for vendor background information and to obtain prior vendor audit reports

bull Interview of ICTrsquos staff and management to gain an understanding of its accounting procedures and processes for SARC billings

bull Review of ICTrsquos serviceattendance records to determine if ICT had sufficient and appropriate evidence to support the direct care services billed to SARC

ClientParent Support Behavior Intervention Training

During the audit period ICT operated one ClientParent Support Behavior Intervention Training The audit included the review of ICTrsquos ClientParent Support Behavior Intervention Training Vendor Number PS0044 Service Code 048 Testing was done during the period of July 1 2011 through June 30 2012

The procedures performed at SARC the vendoring regional center and ICT included but were not limited to the following

bull Review of SARCrsquos vendor files for contracts rate letters program designs purchase of service authorizations and correspondence pertinent to the review

bull Interview of SARCrsquos staff for vendor background information and to obtain prior vendor audit reports

bull Interview of ICTrsquos staff and management to gain an understanding of its accounting procedures and processes for RCEB billings

bull Review of ICTrsquos serviceattendance records to determine if ICT has sufficient and appropriate evidence to support the direct care services billed to RCEB

3

CONCLUSION

Based upon items identified in the Findings and Recommendations section ICT did not comply with the requirements of CCR title 17

VIEWS OF RESPONSIBLE OFFICIALS

DDS issued a draft audit report on February 11 2014 The findings in the report were discussed at a formal exit conference with Lani Fritts ICTrsquos Managing Director on February 19 2014 Subsequent to the meeting Mr Fritts responded on March 17 2014 that ICT would submit documents to support additional hours of service

RESTRICTED USE

This report is solely for the information and use of DDS Department of Health Care Services SARC RCEB and ICT This restriction is not intended to limit distribution of this report which is a matter of public record

4

FINDINGS AND RECOMMENDATIONS

Finding 1 Infant Development Program ndash Unsupported Billings and Failure to Bill

The review of ICTrsquos Infant Development Program Vendor Numbers HS0468 and HS0698 for the period of July 1 2011 through June 30 2012 revealed that ICT had both unsupported billings as well as appropriate support for services that it failed to bill to SARC

Unsupported billings occurred due to a lack of appropriate documentation to support the units of service billed to SARC The failure to bill occurred when ICT had appropriate supporting documentation but it did not bill SARC The following are the discrepancies identified

ICT was not able to provide appropriate supporting documentation for 565837 hours of services billed for Vendor Number HS0468 and 131950 hours of services billed for Vendor Number HS0698 The lack of documentation resulted in unsupported billings to SARC in the amount of $42415143 for Vendor Number HS0468 and $7476290 for Vendor Number HS0698 The total unsupported billings amounted to $49891433

In addition ICT provided appropriate supporting documentation for 219286 hours of service for Vendor Number HS0468 and 30125 hours of service for Vendor Number HS0698 but was not billed to SARC This resulted in an unbilled amount of $16437676 for Vendor Number HS0468 and $1706886 for Vendor Number HS0698 The total failure to bill amounted to $18144562

As a result $31746871 is due back to DDS for the unsupported billings (See Attachment A)

CCR title 17 section 54326(a)(3) and (10) states

ldquo(a) All vendors shall

(3) Maintain records of services provided to consumers in sufficient detail to verify delivery of the units of service billed

(10) Bill only for services which are actually provided to consumers and which have been authorized by the referring regional centerhelliprdquo

Also CCR title 17 section 50604(d) and (e) states

ldquo(d) All service providers shall maintain complete service records to support all billinginvoicing for each regional center consumer in the programhellip

(e) All service providersrsquo records shall be supported by source documentationrdquo

5

Recommendation ICT must reimburse to DDS the $31746871 for the unsupported billings In addition ICT should develop and implement policies and procedures to ensure that proper documentation is maintained to support the amounts billed to SARC

ICTrsquos Response Lani Fritts ICTrsquos Managing Director stated via letter to Edward Yan DDSrsquo Audit Manager dated March 17 2014 that ICT had additional documentation to provide that would support some of the billings A copy of the letter is enclosed as Attachment C

Finding 2 ClientParent Support Behavior Intervention Training ndash Unsupported Billings and Failure to Bill

The review of ICTrsquos ClientParent Support Behavior Intervention Training Vendor Number PS0044 for the period of July 1 2011 through June 30 2012 revealed that ICT had both unsupported billings as well as appropriate support for services that it failed to bill to RCEB

Unsupported billings occurred due to a lack of appropriate documentation to support the units of service billed to RCEB The failure to bill occurred when ICT had appropriate supporting documentation but it did not bill RCEB The following are the discrepancies identified

ICT was not able to provide appropriate supporting documentation for 250128 hours of services billed The lack of documentation resulted in unsupported billings to RCEB in the amount of $12412595

In addition ICT provided appropriate supporting documentation for 69693 hours of service but was not billed to RCEB This resulted in an unbilled amount of $2899726

As a result $9512869 is due back to DDS for the unsupported billings (See Attachment A)

CCR title 17 section 54326(a)(3) and (10) states

ldquo(a) All vendors shall

(3) Maintain records of services provided to consumers in sufficient detail to verify delivery of the units of service billed

(10) Bill only for services which are actually provided to consumers and which have been authorized by the referring regional centerhelliprdquo

6

Also CCR title 17 section 50604(d) and (e) states

ldquo(d) All service providers shall maintain complete service records to support all billinginvoicing for each regional center consumer in the programhellip

(e) All service providersrsquo records shall be supported by source documentationrdquo

Recommendation ICT must reimburse to DDS the $9512869 for the unsupported billings In addition ICT should develop and implement policies and procedures to ensure that proper documentation is maintained to support the amounts billed to RCEB

ICTrsquos Response Lani Fritts ICTrsquos Managing Director stated via letter to Edward Yan DDSrsquo Audit Manager dated March 17 2014 that ICT had additional documentation to provide that would support some of the billings A copy of the letter is enclosed as Attachment C

7

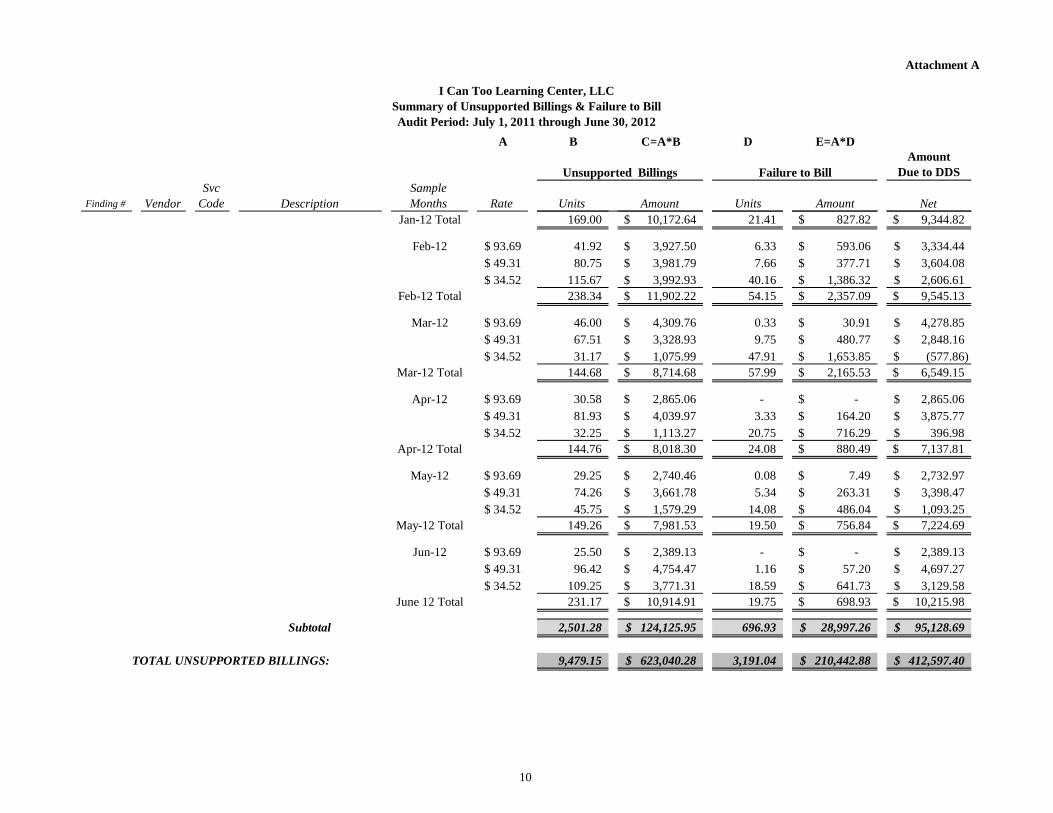

Attachment A

Finding 1

Vendor Svc

Code Description Infant Development Program HS0468 805

I Can Too Learning Center LLC Summary of Unsupported Billings amp Failure to Bill Audit Period July 1 2011 through June 30 2012

Sample Months

Jul-11 Aug-11 Sep-11 Oct-11 Nov-11 Dec-11 Jan-12 Feb-12 Mar-12 Apr-12 May-12 Jun-12

A

Rate

$ 7496 $ 7496 $ 7496 $ 7496 $ 7496 $ 7496 $ 7496 $ 7496 $ 7496 $ 7496 $ 7496 $ 7496

B C=AB

Units Amount

54825 4109682 $ 76357 5723721 $ 57808 4333288 $ 46574 3491186 $ 45232 3390592 $ 17533 1314274 $ 21192 1588552 $ 47033 3525594 $ 42742 3203940 $ 42058 3152668 $ 49075 3678662 $ 65408 4902984 $

Unsupported Billings

D E=AD

Units Amount

3125 234250 $ 10225 766466 $

4367 327350 $ 20067 1504222 $ 21642 1622284 $ 42092 3155216 $ 20008 1499800 $ 23317 1747842 $ 20592 1543576 $ 19125 1433610 $ 19717 1477986 $ 15009 1125074 $

Failure to Bill Amount

Due to DDS

Net

3875432 $ 4957255 $ 4005938 $ 1986964 $ 1768308 $

(1840942) $ 88752 $

1777752 $ 1660364 $ 1719058 $ 2200676 $ 3777910 $

Subtotal 565837 42415143 $ 219286 16437676 $ 25977467 $

1 Infant Development Program HS0698 805 Jul-11

Aug-11 Sep-11 Oct-11 Nov-11 Dec-11 Jan-12 Feb-12 Mar-12 Apr-12 May-12 Jun-12

$ 5666 $ 5666 $ 5666 $ 5666 $ 5666 $ 5666 $ 5666 $ 5666 $ 5666 $ 5666 $ 5666 $ 5666

8750 10625 13050 13000 10800 10600 16875 12675 11450

8100 9575 6450

495775 $ 602012 $ 739413 $ 736580 $ 611928 $ 600596 $ 956138 $ 718166 $ 648758 $ 458947 $ 542520 $ 365457 $

3675 2800

300 2400 3350 1175 1225 2400 3425 5375 2375 1625

208226 $ 158648 $

16998 $ 135985 $ 189812 $

66576 $ 69408 $

135984 $ 194061 $ 304548 $ 134568 $

92072 $

287549 $ 443364 $ 722415 $ 600595 $ 422116 $ 534020 $ 886730 $ 582182 $ 454697 $ 154399 $ 407952 $ 273385 $

Subtotal 131950 7476290 $ 30125 1706886 $ 5769404 $

Infant Development Program Total 697787 49891433 $ 249411 18144562 $ 31746871 $

8

Attachment A

I Can Too Learning Center LLC Summary of Unsupported Billings amp Failure to Bill Audit Period July 1 2011 through June 30 2012

Finding Vendor Svc

Code Description Sample Months

A

Rate

B C=AB

Units Amount

Unsupported Billings

D E=AD

Units Amount

Failure to Bill Amount

Due to DDS

Net

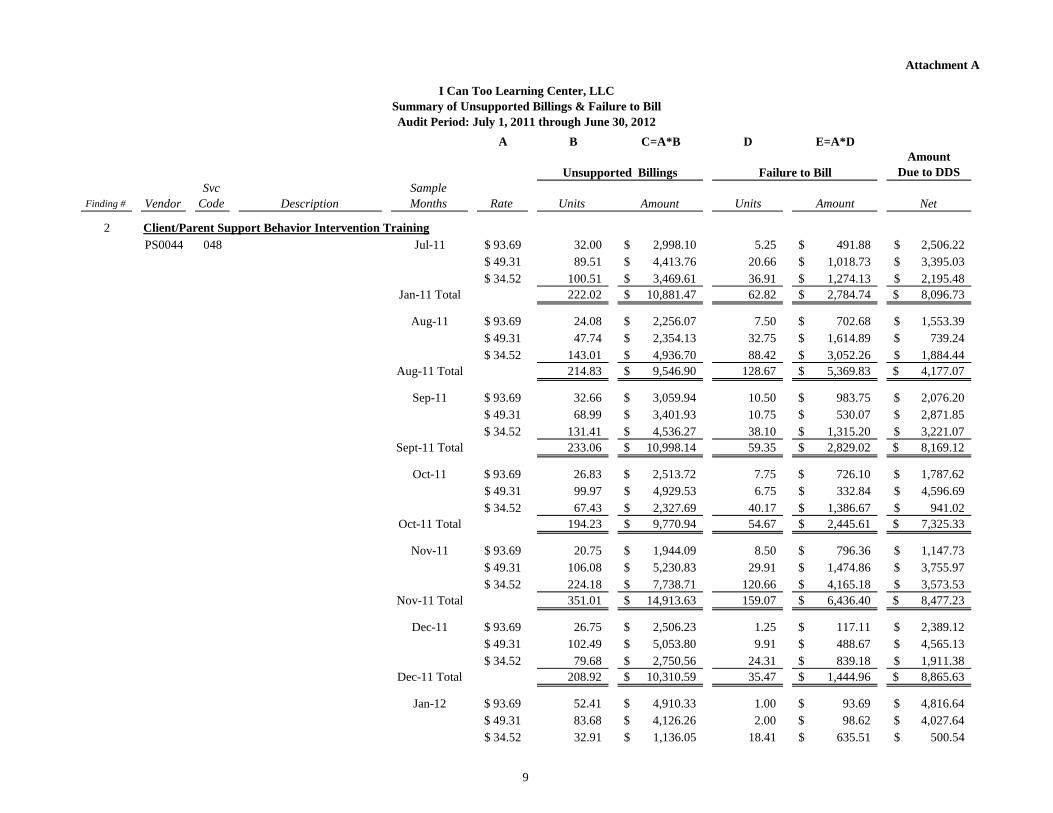

2 ClientParent Support Behavior Intervention Training PS0044 048 Jul-11

Jan-11 Total

$ 9369 $ 4931 $ 3452

3200 8951

10051 22202

299810 $ 441376 $ 346961 $

1088147 $

525 2066 3691 6282

49188 $ 101873 $ 127413 $ 278474 $

250622 $ 339503 $ 219548 $ 809673 $

Aug-11

Aug-11 Total

$ 9369 $ 4931 $ 3452

2408 4774

14301 21483

225607 $ 235413 $ 493670 $ 954690 $

750 3275 8842

12867

70268 $ 161489 $ 305226 $ 536983 $

155339 $ 73924 $

188444 $ 417707 $

Sep-11

Sept-11 Total

$ 9369 $ 4931 $ 3452

3266 6899

13141 23306

305994 $ 340193 $ 453627 $

1099814 $

1050 1075 3810 5935

98375 $ 53007 $

131520 $ 282902 $

207620 $ 287185 $ 322107 $ 816912 $

Oct-11

Oct-11 Total

$ 9369 $ 4931 $ 3452

2683 9997 6743

19423

251372 $ 492953 $ 232769 $ 977094 $

775 675

4017 5467

72610 $ 33284 $

138667 $ 244561 $

178762 $ 459669 $

94102 $ 732533 $

Nov-11

Nov-11 Total

$ 9369 $ 4931 $ 3452

2075 10608 22418 35101

194409 $ 523083 $ 773871 $

1491363 $

850 2991

12066 15907

79636 $ 147486 $ 416518 $ 643640 $

114773 $ 375597 $ 357353 $ 847723 $

Dec-11

Dec-11 Total

$ 9369 $ 4931 $ 3452

2675 10249

7968 20892

250623 $ 505380 $ 275056 $

1031059 $

125 991

2431 3547

11711 $ 48867 $ 83918 $

144496 $

238912 $ 456513 $ 191138 $ 886563 $

Jan-12 $ 9369 $ 4931 $ 3452

5241 8368 3291

491033 $ 412626 $ 113605 $

100 200

1841

9369 $ 9862 $

63551 $

481664 $ 402764 $

50054 $

9

Attachment A

I Can Too Learning Center LLC Summary of Unsupported Billings amp Failure to Bill Audit Period July 1 2011 through June 30 2012

Finding Vendor Svc

Code Description Sample Months

Jan-12 Total

A

Rate

B C=AB

Units Amount

Unsupported Billings

16900 1017264 $

D E=AD

Units Amount

Failure to Bill

2141 82782 $

Amount Due to DDS

Net 934482 $

Feb-12

Feb-12 Total

$ 9369 $ 4931 $ 3452

4192 8075

11567 23834

392750 $ 398179 $ 399293 $

1190222 $

633 766

4016 5415

59306 $ 37771 $

138632 $ 235709 $

333444 $ 360408 $ 260661 $ 954513 $

Mar-12

Mar-12 Total

$ 9369 $ 4931 $ 3452

4600 6751 3117

14468

430976 $ 332893 $ 107599 $ 871468 $

033 975

4791 5799

3091 $ 48077 $

165385 $ 216553 $

427885 $ 284816 $ (57786) $

654915 $

Apr-12

Apr-12 Total

$ 9369 $ 4931 $ 3452

3058 8193 3225

14476

286506 $ 403997 $ 111327 $ 801830 $

-333

2075 2408

-$ 16420 $ 71629 $ 88049 $

286506 $ 387577 $

39698 $ 713781 $

May-12

May-12 Total

$ 9369 $ 4931 $ 3452

2925 7426 4575

14926

274046 $ 366178 $ 157929 $ 798153 $

008 534

1408 1950

749 $ 26331 $ 48604 $ 75684 $

273297 $ 339847 $ 109325 $ 722469 $

Jun-12

June 12 Total

$ 9369 $ 4931 $ 3452

2550 9642

10925 23117

238913 $ 475447 $ 377131 $

1091491 $

-116

1859 1975

-$ 5720 $

64173 $ 69893 $

238913 $ 469727 $ 312958 $

1021598 $

Subtotal 250128 12412595 $ 69693 2899726 $ 9512869 $

TOTAL UNSUPPORTED BILLINGS 947915 62304028 $ 319104 21044288 $ 41259740 $

10

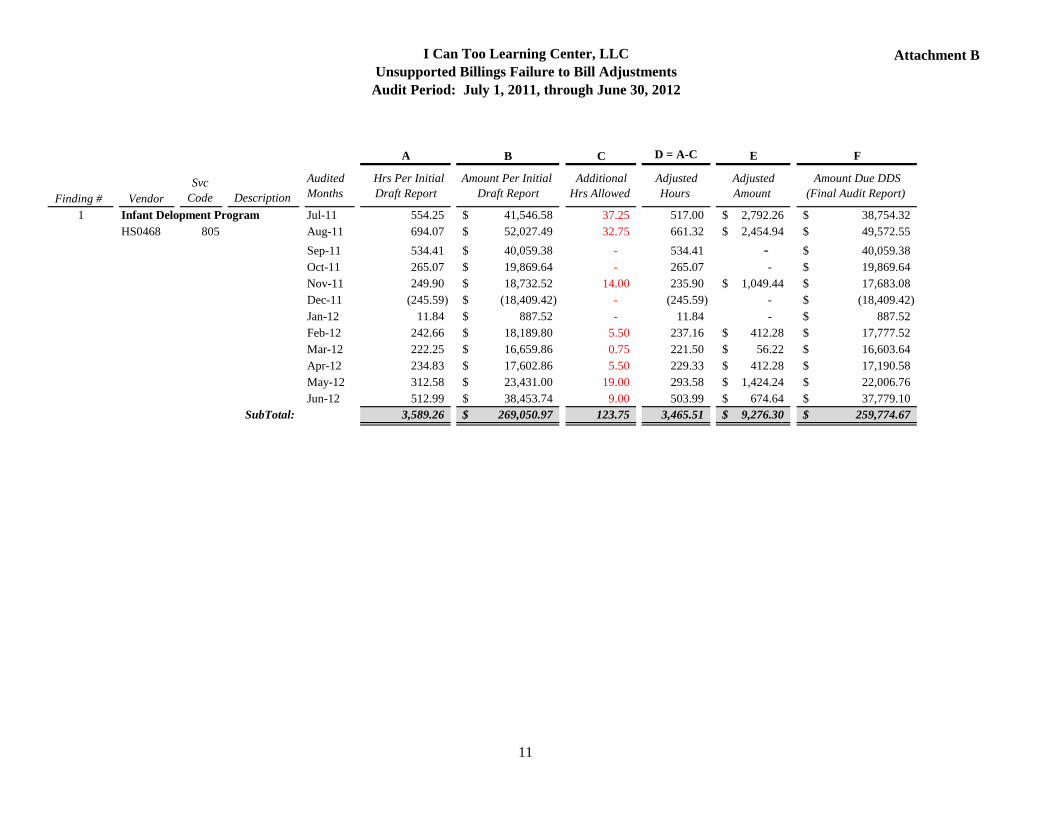

I Can Too Learning Center LLC Attachment B Unsupported Billings Failure to Bill Adjustments

Audit Period July 1 2011 through June 30 2012

A B C D = A-C E F

Finding 1

Vendor Svc

Code Description Infant Delopment Program HS0468 805

Audited Months

Jul-11 Aug-11 Sep-11 Oct-11 Nov-11 Dec-11 Jan-12

Hrs Per Initial Draft Report

55425 69407 53441 26507 24990

(24559) 1184

Amount Per Initial Draft Report

4154658 $ 5202749 $ 4005938 $ 1986964 $ 1873252 $

(1840942) $ 88752 $

Additional Hrs Allowed

3725 3275

--

1400 --

Adjusted Hours

51700 66132 53441 26507 23590

(24559) 1184

Adjusted Amount

279226 $ 245494 $

--

104944 $ --

Amount Due DDS (Final Audit Report)

3875432 $ 4957255 $ 4005938 $ 1986964 $ 1768308 $

(1840942) $ 88752 $

SubTotal

Feb-12 Mar-12 Apr-12 May-12 Jun-12

24266 22225 23483 31258 51299

358926

1818980 $ 1665986 $ 1760286 $ 2343100 $ 3845374 $

26905097 $

550 075 550

1900 900

12375

23716 22150 22933 29358 50399

346551

41228 $ 5622 $

41228 $ 142424 $

67464 $ 927630 $

1777752 $ 1660364 $ 1719058 $ 2200676 $ 3777910 $

25977467 $

11

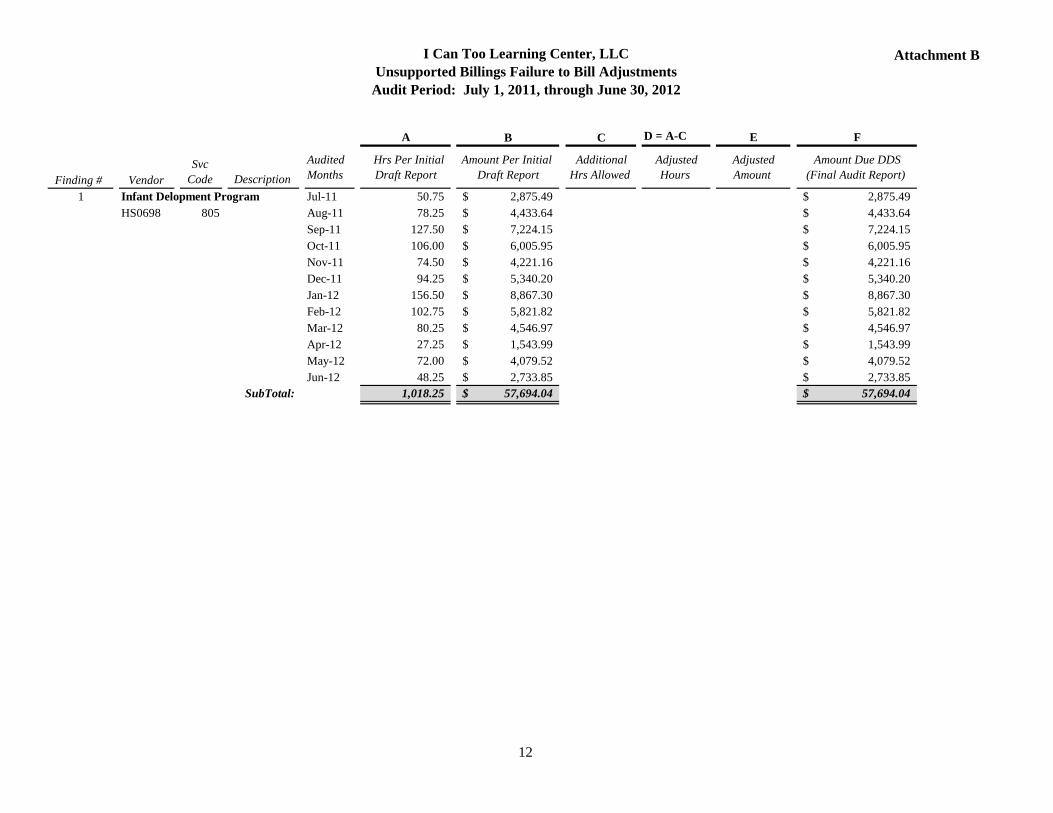

I Can Too Learning Center LLC Attachment B Unsupported Billings Failure to Bill Adjustments

Audit Period July 1 2011 through June 30 2012

A B C D = A-C E F

Finding 1

Vendor Svc

Code Description Infant Delopment Program HS0698 805

SubTotal

Audited Months

Jul-11 Aug-11 Sep-11 Oct-11 Nov-11 Dec-11 Jan-12 Feb-12 Mar-12 Apr-12 May-12 Jun-12

Hrs Per Initial Draft Report

5075 7825

12750 10600

7450 9425

15650 10275

8025 2725 7200 4825

101825

Amount Per Initial Draft Report

287549 $ 443364 $ 722415 $ 600595 $ 422116 $ 534020 $ 886730 $ 582182 $ 454697 $ 154399 $ 407952 $ 273385 $

5769404 $

Additional Hrs Allowed

Adjusted Hours

Adjusted Amount

Amount Due DDS (Final Audit Report)

287549 $ 443364 $ 722415 $ 600595 $ 422116 $ 534020 $ 886730 $ 582182 $ 454697 $ 154399 $ 407952 $ 273385 $

5769404 $

12

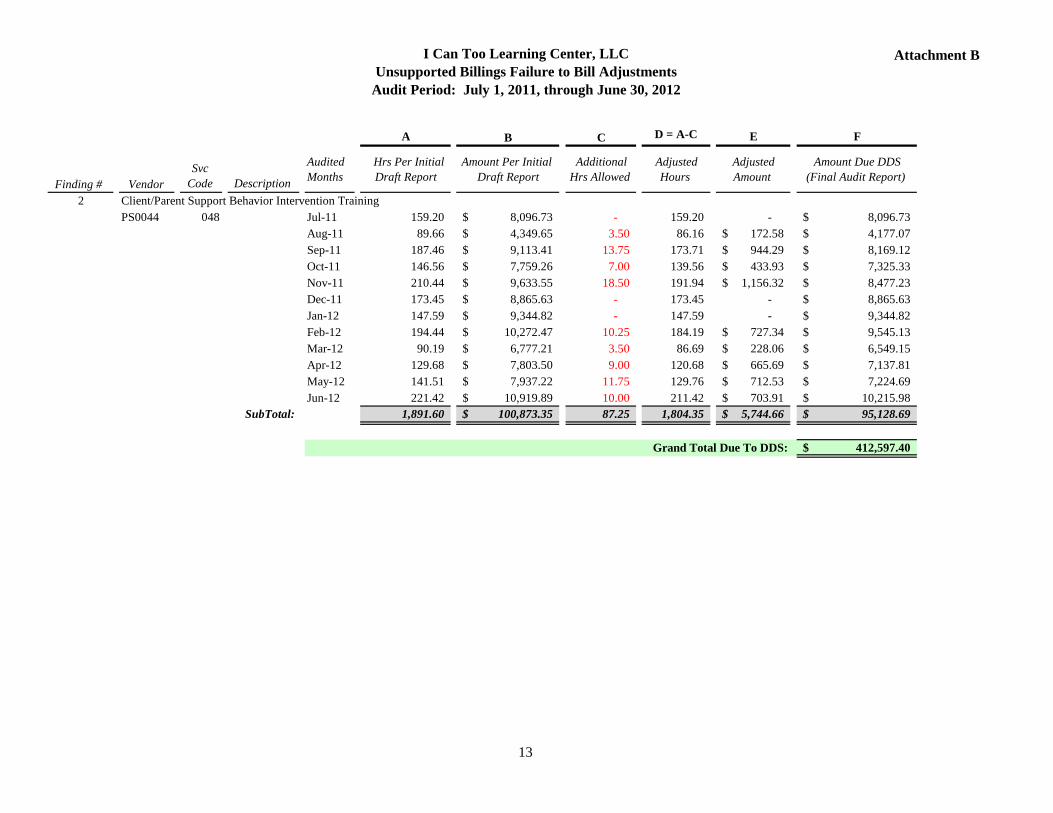

I Can Too Learning Center LLC Attachment B Unsupported Billings Failure to Bill Adjustments

Audit Period July 1 2011 through June 30 2012

A B C D = A-C E F

Audited Hrs Per Initial Amount Per Initial Additional Adjusted Adjusted Amount Due DDS Svc Months Draft Report Draft Report Hrs Allowed Hours Amount (Final Audit Report) Finding Vendor Code Description

2 ClientParent Support Behavior Intervention Training PS0044 048 Jul-11 15920 $ 809673 - 15920 - $ 809673

Aug-11 8966 $ 434965 350 8616 $ 17258 $ 417707 Sep-11 18746 $ 911341 1375 17371 $ 94429 $ 816912 Oct-11 14656 $ 775926 700 13956 $ 43393 $ 732533 Nov-11 21044 $ 963355 1850 19194 $ 115632 $ 847723 Dec-11 17345 $ 886563 - 17345 - $ 886563 Jan-12 14759 $ 934482 - 14759 - $ 934482 Feb-12 19444 $ 1027247 1025 18419 $ 72734 $ 954513 Mar-12 9019 $ 677721 350 8669 $ 22806 $ 654915 Apr-12 12968 $ 780350 900 12068 $ 66569 $ 713781 May-12 14151 $ 793722 1175 12976 $ 71253 $ 722469 Jun-12 22142 $ 1091989 1000 21142 $ 70391 $ 1021598

SubTotal 189160 $ 10087335 8725 180435 $ 574466 $ 9512869

Grand Total Due To DDS $ 41259740

13

Attachment C

March 172014

Edward Y an Manager Department of Developmental Services Audit Branch 1600 9th St Room 230 MS 2-10 Sacramento CA 95814

Re Official Response to I Can Too Learning Center LLC Draft Audit Report

Dear Mr Yan

Thank you for the release of the draft audit report and the review conducted February 19 2014 with the I Can TooTrumpet Behavioral Health team

We have three fonnal responses to the draft report

bull For sessions in which some clinical documentation andor parent verification was

available I Can Too was given only partial credit for sessions In total this represented

1050 hours of credit Ve believe pay record data associated with those sessions in which we can tie an employees schedule to billed hours to their payroll stubs should constitute full allowance for the entirety of those sessions This will significantly

increase the number of hours accepted Per a follow-up meeting withAl Kitay and Pardeep D eol on Tuesday March 41

h (prior to which we submitted significant data backshy

up regarding one specific consumer) we were given approval to submit that

documentation as back-up and receive credit for the additional hours VIe will provide a

separate addendum to this letter Nith the total ofhours consumers and $s that we plan to submit for which we are requesting inclusion

bull During the audit exit meeting Al and Pardeep indicated that we had documentation that

counted toward supported billing for several consumers during the months of the audit period but a purchase of service (PO S) was not in the Sand Andreas Regional Center (SARC) system to bill these services Per Aland Pardeeps suggestion Ve have found a

copy of the POS andor initial referral email for the consumer from the SARC service coordinator Ve intend to contact SARC directly to bill these services per A1 and Pardeeps advice but have also submitted these documents to you for review as well

bull More generally we b elieve that DDS should all ow payroll records (pay-stubs V-2s

etc) to substantiate that sessions took place even when clinical source documentation cmmot be produced A record ofpayment to an employee for the same hours associated with a consumers services in a given month is a reasonable indication that a staff was paid for time (documented in our schedulingpayroll systems) as billable time spent with that particular consumer We believe this is a fair and reasonable proxy to those billable

14services havin g been provided

T

1401 Parkmoor Ave Suite 208 San Jose CA 95126

Attachment C

In the 14 days foll owing the March 3rd follmv-up meeting we have been pulling together extensive payroll schedule and pay stub documenta6on to support the follow-up Ve request a 30 day extension of response (to April 19 20 14) to allow us to provide all remaining documentation By its nature thi s is a very time and energy intensive process- pulling data on hundreds of staffmembers hundreds of consumers across the 1-year audit time-frame and from several different source data systems We appreciate your consideration

J Frankli~ Managing Director I Can Too Learning CenterTrumpet Behavioral Health

15

1401 Parkmoor Ave Suite 208 San Jose CA 95126

Attachment D

DEPARTMENT OF DEVELOPMENTAL SERVICES EVALUATION OF

I CAN TOOrsquoS RESPONSE

As part of the audit process I Can Too Learning Center LLC (ICT) was afforded the opportunity to respond to the draft audit report and provide a written response to each finding identified therein The draft audit report was issued on February 11 2014 The Audit Branch received ICTrsquos response on March 17 2014

DDS evaluated ICTrsquos written response to the draft audit report upon receipt and determined that ICT disagreed with the audit findings DDS determined that although ICTrsquos response did not identify which programs were being discussed the comments were all in relation to Vendor Number HS0468 Provided below are excerpts from ICTrsquos response and DDSrsquo evaluation of the response (See Attachment C to the final audit report for the full text of ICTrsquos response)

Finding 1 Infant Development Program - Unsupported Billings and Failure to Bill

ICT argues the following in response to this finding

Unsupported Billing ldquoFor sessions in which some clinical documentation andor parent verification was available I Can Too was given only partial credit for sessions In total this represented 1050 hours of credit We believe pay record data associated with those sessions in which we can tie an employeersquos schedule to billed hours to their payroll stubs should constitute full allowance for the entirety of those sessionsrdquo

In instances where service billings were considered to be unsupported by DDS due to inadequate source documentation DDS did consider payroll records as support and gave ICT credit when it could tie the payroll to services provided to specific consumers An example is when source documentation included a date employee name and consumer name but no length of time for the session In this instance payroll was used to determine length of time for the session

ldquoDuring the audit exit meeting Al and Pardeep indicated that we had documentation that counted toward supported billing for several consumers during the months of the audit period but a purchase of service (POS) was not in the Sand [sic] Andreas Regional Center (SARC) system to bill those servicesrdquo

DDS determined that there was evidence that services were provided for which payment was not made by the regional center Further analysis revealed that the reason the payment was not received was that there was no authorization in the system CCR title 17 requires that before payments can be made the services must be authorized and the services must be provided Since the services were not authorized at the time of the audit DDS was unable to net those services against the unsupported services DDS suggested that ICT discuss those services with the regional center

16

Attachment D

DEPARTMENT OF DEVELOPMENTAL SERVICES EVALUATION OF

I CAN TOOrsquoS RESPONSE

ldquoMore generally we believe that DDS should allow payroll records (pay-stubs W-2rsquos etc) to substantiate that sessions took place even when clinical source documentation cannot be producedrdquo

Billings are consumer specific while payroll is employee specific Payroll does not indicate whether a service was provided to a consumer Therefore without collaborating evidence it is unknown if direct consumer services were provided

DDSrsquo Conclusion

Subsequent to the receipt of this response ICT provided DDS with documents to support billings that were previously unsupported DDS accepted documents that supported an additional 12375 hours for Vendor Number HS0468 These adjustments are reflected in this report (See Attachment B Page 11) However ICTrsquos response did not address its policies and procedures going forward DDS recommends that ICT develop and implement policies and procedures to ensure that proper documentation is maintained to support its billings to the regional centers A future audit may be conducted by DDS to ensure that DDSrsquo recommendation has been fully implemented

Finding 2 ClientParent Support Intervention Training - Unsupported Billings and Failure to Bill

ICT did not provide an argument in response to this finding however the supporting documentation provided subsequently included support for finding 2 DDS accepted the additional documentation

DDSrsquo Conclusion

Subsequent to the receipt of this response ICT provided DDS with documents to support billings that were previously unsupported DDS accepted documents that supported an additional 8725 hours for Vendor Number PS0044 These adjustments are reflected in this report (See Attachment B Page 13) However ICTrsquos response did not address its policies and procedures going forward DDS recommends that ICT develop and implement policies and procedures to ensure that proper documentation is maintained to support its billings to the regional centers A future audit may be conducted by DDS to ensure that DDSrsquo recommendation has been fully implemented

17

I CAN TOO LEARNING CENTER LLC

TABLE OF CONTENTS

Page(s)

Executive Summary 1

Background 2

Objective Scope and Methodology 2-3

Conclusion 4

Views of Responsible Officials4

Restricted Use 4

Findings and Recommendations 5-7

Attachment A-Summary of Unsupported Billings amp Failure to Bill 8-10

Attachment B-Unsupported Billings amp Failure to Bill Adjustments 11-13

Attachment C-Response from Vendor 14-15

Attachment D-Evaluation of Vendor Response 16-17

ii

EXECUTIVE SUMMARY

The Department of Developmental Services (DDS) has audited I Can Too Learning Center LLC (ICT) The audit was performed upon the Infant Development Program and ClientParent Support Behavior Intervention Training for the period of July 1 2011 through June 30 2012

The results of the audit disclosed the following issues of non-compliance

Finding 1 Infant Development Program ndash Unsupported Billings and Failure to Bill

The review of ICTrsquos Infant Development Program Vendor Numbers HS0468 and HS0698 revealed that ICT had both unsupported billings as well as appropriate support for services that it failed to bill the San Andreas Regional Center (SARC) As a result ICT had a total of $49891433 of unsupported billings and a total of $18144562 for which it failed to bill

Finding 2 ClientParent Support Behavior Intervention Training ndash Unsupported Billings and Failure to Bill

The review of ICTrsquos ClientParent Support Behavior Intervention Training Vendor Number PS0044 revealed that ICT had both unsupported billings as well as appropriate support for services that it failed to bill the Regional Center of the East Bay (RCEB) As a result ICT had a total of $12412595 of unsupported billings and a total of $2899726 for which it failed to bill

The total unsupported billing discrepancies identified in this audit amounts to $41259740 and is due back to DDS A detailed discussion of these findings is contained in the Findings and Recommendations section of this report

1

BACKGROUND

DDS is responsible under the Lanterman Developmental Disabilities Services Act for ensuring that persons with developmental disabilities receive the services and supports they need to lead more independent productive and normal lives DDS contracts with 21 private nonprofit regional centers that provide fixed points of contact in the community for serving eligible individuals with developmental disabilities and their families in California In order for regional centers to fulfill their objectives they secure services and supports from qualified service providers andor contractors Pursuant to the Welfare and Institutions (WampI) Code section 46481 DDS has the authority to audit those service providers andor contractors that provide services and supports to persons with developmental disabilities

OBJECTIVE SCOPE AND METHODOLOGY

The audit was conducted to determine whether ICTrsquos Infant Development Program and ClientParent Support Behavior Intervention Training were compliant with the WampI Code California Code of Regulations Title 17 (CCR title 17) and the regional center contracts with ICT for the period of July 1 2011 through June 30 2012

ICT was vendorized by SARC and provided services to RCEB and Golden Gate Regional Center (GGRC) Audit staff reviewed the programs and services provided to SARC and RCEB

The audit was conducted in accordance with the Generally Accepted Government Auditing Standards (GAGAS) issued by the Comptroller General of the United States The auditors did not review the financial statements of ICT nor was this audit intended to express an opinion on the financial statements The auditors limited the review of ICTrsquos internal controls to gain an understanding of the transaction flow and invoice preparation process as necessary to develop appropriate auditing procedures The audit scope was limited to planning and performing audit procedures necessary to obtain reasonable assurance that ICT complied with CCR title 17 Also any complaints that DDSrsquo Audit Branch was aware of regarding noncompliance of laws and regulations were reviewed and followed-up during the course of the audit

Day Programs

During the audit period ICT operated eight Day Programs The audit included the review of two of ICTrsquos Day Programs Testing was done during the period of July 1 2011 through June 30 2012 The programs audited are listed below

bull Infant Development Program Vendor Numbers HS0468 and HS0698 Service Code 805

The procedures performed at SARC the vendoring regional center and ICT included but were not limited to the following

bull Review of SARCrsquos vendor files for contracts rate letters program designs purchase of service authorizations and correspondence pertinent to the review

2

bull Interview of SARCrsquos staff for vendor background information and to obtain prior vendor audit reports

bull Interview of ICTrsquos staff and management to gain an understanding of its accounting procedures and processes for SARC billings

bull Review of ICTrsquos serviceattendance records to determine if ICT had sufficient and appropriate evidence to support the direct care services billed to SARC

ClientParent Support Behavior Intervention Training

During the audit period ICT operated one ClientParent Support Behavior Intervention Training The audit included the review of ICTrsquos ClientParent Support Behavior Intervention Training Vendor Number PS0044 Service Code 048 Testing was done during the period of July 1 2011 through June 30 2012

The procedures performed at SARC the vendoring regional center and ICT included but were not limited to the following

bull Review of SARCrsquos vendor files for contracts rate letters program designs purchase of service authorizations and correspondence pertinent to the review

bull Interview of SARCrsquos staff for vendor background information and to obtain prior vendor audit reports

bull Interview of ICTrsquos staff and management to gain an understanding of its accounting procedures and processes for RCEB billings

bull Review of ICTrsquos serviceattendance records to determine if ICT has sufficient and appropriate evidence to support the direct care services billed to RCEB

3

CONCLUSION

Based upon items identified in the Findings and Recommendations section ICT did not comply with the requirements of CCR title 17

VIEWS OF RESPONSIBLE OFFICIALS

DDS issued a draft audit report on February 11 2014 The findings in the report were discussed at a formal exit conference with Lani Fritts ICTrsquos Managing Director on February 19 2014 Subsequent to the meeting Mr Fritts responded on March 17 2014 that ICT would submit documents to support additional hours of service

RESTRICTED USE

This report is solely for the information and use of DDS Department of Health Care Services SARC RCEB and ICT This restriction is not intended to limit distribution of this report which is a matter of public record

4

FINDINGS AND RECOMMENDATIONS

Finding 1 Infant Development Program ndash Unsupported Billings and Failure to Bill

The review of ICTrsquos Infant Development Program Vendor Numbers HS0468 and HS0698 for the period of July 1 2011 through June 30 2012 revealed that ICT had both unsupported billings as well as appropriate support for services that it failed to bill to SARC

Unsupported billings occurred due to a lack of appropriate documentation to support the units of service billed to SARC The failure to bill occurred when ICT had appropriate supporting documentation but it did not bill SARC The following are the discrepancies identified

ICT was not able to provide appropriate supporting documentation for 565837 hours of services billed for Vendor Number HS0468 and 131950 hours of services billed for Vendor Number HS0698 The lack of documentation resulted in unsupported billings to SARC in the amount of $42415143 for Vendor Number HS0468 and $7476290 for Vendor Number HS0698 The total unsupported billings amounted to $49891433

In addition ICT provided appropriate supporting documentation for 219286 hours of service for Vendor Number HS0468 and 30125 hours of service for Vendor Number HS0698 but was not billed to SARC This resulted in an unbilled amount of $16437676 for Vendor Number HS0468 and $1706886 for Vendor Number HS0698 The total failure to bill amounted to $18144562

As a result $31746871 is due back to DDS for the unsupported billings (See Attachment A)

CCR title 17 section 54326(a)(3) and (10) states

ldquo(a) All vendors shall

(3) Maintain records of services provided to consumers in sufficient detail to verify delivery of the units of service billed

(10) Bill only for services which are actually provided to consumers and which have been authorized by the referring regional centerhelliprdquo

Also CCR title 17 section 50604(d) and (e) states

ldquo(d) All service providers shall maintain complete service records to support all billinginvoicing for each regional center consumer in the programhellip

(e) All service providersrsquo records shall be supported by source documentationrdquo

5

Recommendation ICT must reimburse to DDS the $31746871 for the unsupported billings In addition ICT should develop and implement policies and procedures to ensure that proper documentation is maintained to support the amounts billed to SARC

ICTrsquos Response Lani Fritts ICTrsquos Managing Director stated via letter to Edward Yan DDSrsquo Audit Manager dated March 17 2014 that ICT had additional documentation to provide that would support some of the billings A copy of the letter is enclosed as Attachment C

Finding 2 ClientParent Support Behavior Intervention Training ndash Unsupported Billings and Failure to Bill

The review of ICTrsquos ClientParent Support Behavior Intervention Training Vendor Number PS0044 for the period of July 1 2011 through June 30 2012 revealed that ICT had both unsupported billings as well as appropriate support for services that it failed to bill to RCEB

Unsupported billings occurred due to a lack of appropriate documentation to support the units of service billed to RCEB The failure to bill occurred when ICT had appropriate supporting documentation but it did not bill RCEB The following are the discrepancies identified

ICT was not able to provide appropriate supporting documentation for 250128 hours of services billed The lack of documentation resulted in unsupported billings to RCEB in the amount of $12412595

In addition ICT provided appropriate supporting documentation for 69693 hours of service but was not billed to RCEB This resulted in an unbilled amount of $2899726

As a result $9512869 is due back to DDS for the unsupported billings (See Attachment A)

CCR title 17 section 54326(a)(3) and (10) states

ldquo(a) All vendors shall

(3) Maintain records of services provided to consumers in sufficient detail to verify delivery of the units of service billed

(10) Bill only for services which are actually provided to consumers and which have been authorized by the referring regional centerhelliprdquo

6

Also CCR title 17 section 50604(d) and (e) states

ldquo(d) All service providers shall maintain complete service records to support all billinginvoicing for each regional center consumer in the programhellip

(e) All service providersrsquo records shall be supported by source documentationrdquo

Recommendation ICT must reimburse to DDS the $9512869 for the unsupported billings In addition ICT should develop and implement policies and procedures to ensure that proper documentation is maintained to support the amounts billed to RCEB

ICTrsquos Response Lani Fritts ICTrsquos Managing Director stated via letter to Edward Yan DDSrsquo Audit Manager dated March 17 2014 that ICT had additional documentation to provide that would support some of the billings A copy of the letter is enclosed as Attachment C

7

Attachment A

Finding 1

Vendor Svc

Code Description Infant Development Program HS0468 805

I Can Too Learning Center LLC Summary of Unsupported Billings amp Failure to Bill Audit Period July 1 2011 through June 30 2012

Sample Months

Jul-11 Aug-11 Sep-11 Oct-11 Nov-11 Dec-11 Jan-12 Feb-12 Mar-12 Apr-12 May-12 Jun-12

A

Rate

$ 7496 $ 7496 $ 7496 $ 7496 $ 7496 $ 7496 $ 7496 $ 7496 $ 7496 $ 7496 $ 7496 $ 7496

B C=AB

Units Amount

54825 4109682 $ 76357 5723721 $ 57808 4333288 $ 46574 3491186 $ 45232 3390592 $ 17533 1314274 $ 21192 1588552 $ 47033 3525594 $ 42742 3203940 $ 42058 3152668 $ 49075 3678662 $ 65408 4902984 $

Unsupported Billings

D E=AD

Units Amount

3125 234250 $ 10225 766466 $

4367 327350 $ 20067 1504222 $ 21642 1622284 $ 42092 3155216 $ 20008 1499800 $ 23317 1747842 $ 20592 1543576 $ 19125 1433610 $ 19717 1477986 $ 15009 1125074 $

Failure to Bill Amount

Due to DDS

Net

3875432 $ 4957255 $ 4005938 $ 1986964 $ 1768308 $

(1840942) $ 88752 $

1777752 $ 1660364 $ 1719058 $ 2200676 $ 3777910 $

Subtotal 565837 42415143 $ 219286 16437676 $ 25977467 $

1 Infant Development Program HS0698 805 Jul-11

Aug-11 Sep-11 Oct-11 Nov-11 Dec-11 Jan-12 Feb-12 Mar-12 Apr-12 May-12 Jun-12

$ 5666 $ 5666 $ 5666 $ 5666 $ 5666 $ 5666 $ 5666 $ 5666 $ 5666 $ 5666 $ 5666 $ 5666

8750 10625 13050 13000 10800 10600 16875 12675 11450

8100 9575 6450

495775 $ 602012 $ 739413 $ 736580 $ 611928 $ 600596 $ 956138 $ 718166 $ 648758 $ 458947 $ 542520 $ 365457 $

3675 2800

300 2400 3350 1175 1225 2400 3425 5375 2375 1625

208226 $ 158648 $

16998 $ 135985 $ 189812 $

66576 $ 69408 $

135984 $ 194061 $ 304548 $ 134568 $

92072 $

287549 $ 443364 $ 722415 $ 600595 $ 422116 $ 534020 $ 886730 $ 582182 $ 454697 $ 154399 $ 407952 $ 273385 $

Subtotal 131950 7476290 $ 30125 1706886 $ 5769404 $

Infant Development Program Total 697787 49891433 $ 249411 18144562 $ 31746871 $

8

Attachment A

I Can Too Learning Center LLC Summary of Unsupported Billings amp Failure to Bill Audit Period July 1 2011 through June 30 2012

Finding Vendor Svc

Code Description Sample Months

A

Rate

B C=AB

Units Amount

Unsupported Billings

D E=AD

Units Amount

Failure to Bill Amount

Due to DDS

Net

2 ClientParent Support Behavior Intervention Training PS0044 048 Jul-11

Jan-11 Total

$ 9369 $ 4931 $ 3452

3200 8951

10051 22202

299810 $ 441376 $ 346961 $

1088147 $

525 2066 3691 6282

49188 $ 101873 $ 127413 $ 278474 $

250622 $ 339503 $ 219548 $ 809673 $

Aug-11

Aug-11 Total

$ 9369 $ 4931 $ 3452

2408 4774

14301 21483

225607 $ 235413 $ 493670 $ 954690 $

750 3275 8842

12867

70268 $ 161489 $ 305226 $ 536983 $

155339 $ 73924 $

188444 $ 417707 $

Sep-11

Sept-11 Total

$ 9369 $ 4931 $ 3452

3266 6899

13141 23306

305994 $ 340193 $ 453627 $

1099814 $

1050 1075 3810 5935

98375 $ 53007 $

131520 $ 282902 $

207620 $ 287185 $ 322107 $ 816912 $

Oct-11

Oct-11 Total

$ 9369 $ 4931 $ 3452

2683 9997 6743

19423

251372 $ 492953 $ 232769 $ 977094 $

775 675

4017 5467

72610 $ 33284 $

138667 $ 244561 $

178762 $ 459669 $

94102 $ 732533 $

Nov-11

Nov-11 Total

$ 9369 $ 4931 $ 3452

2075 10608 22418 35101

194409 $ 523083 $ 773871 $

1491363 $

850 2991

12066 15907

79636 $ 147486 $ 416518 $ 643640 $

114773 $ 375597 $ 357353 $ 847723 $

Dec-11

Dec-11 Total

$ 9369 $ 4931 $ 3452

2675 10249

7968 20892

250623 $ 505380 $ 275056 $

1031059 $

125 991

2431 3547

11711 $ 48867 $ 83918 $

144496 $

238912 $ 456513 $ 191138 $ 886563 $

Jan-12 $ 9369 $ 4931 $ 3452

5241 8368 3291

491033 $ 412626 $ 113605 $

100 200

1841

9369 $ 9862 $

63551 $

481664 $ 402764 $

50054 $

9

Attachment A

I Can Too Learning Center LLC Summary of Unsupported Billings amp Failure to Bill Audit Period July 1 2011 through June 30 2012

Finding Vendor Svc

Code Description Sample Months

Jan-12 Total

A

Rate

B C=AB

Units Amount

Unsupported Billings

16900 1017264 $

D E=AD

Units Amount

Failure to Bill

2141 82782 $

Amount Due to DDS

Net 934482 $

Feb-12

Feb-12 Total

$ 9369 $ 4931 $ 3452

4192 8075

11567 23834

392750 $ 398179 $ 399293 $

1190222 $

633 766

4016 5415

59306 $ 37771 $

138632 $ 235709 $

333444 $ 360408 $ 260661 $ 954513 $

Mar-12

Mar-12 Total

$ 9369 $ 4931 $ 3452

4600 6751 3117

14468

430976 $ 332893 $ 107599 $ 871468 $

033 975

4791 5799

3091 $ 48077 $

165385 $ 216553 $

427885 $ 284816 $ (57786) $

654915 $

Apr-12

Apr-12 Total

$ 9369 $ 4931 $ 3452

3058 8193 3225

14476

286506 $ 403997 $ 111327 $ 801830 $

-333

2075 2408

-$ 16420 $ 71629 $ 88049 $

286506 $ 387577 $

39698 $ 713781 $

May-12

May-12 Total

$ 9369 $ 4931 $ 3452

2925 7426 4575

14926

274046 $ 366178 $ 157929 $ 798153 $

008 534

1408 1950

749 $ 26331 $ 48604 $ 75684 $

273297 $ 339847 $ 109325 $ 722469 $

Jun-12

June 12 Total

$ 9369 $ 4931 $ 3452

2550 9642

10925 23117

238913 $ 475447 $ 377131 $

1091491 $

-116

1859 1975

-$ 5720 $

64173 $ 69893 $

238913 $ 469727 $ 312958 $

1021598 $

Subtotal 250128 12412595 $ 69693 2899726 $ 9512869 $

TOTAL UNSUPPORTED BILLINGS 947915 62304028 $ 319104 21044288 $ 41259740 $

10

I Can Too Learning Center LLC Attachment B Unsupported Billings Failure to Bill Adjustments

Audit Period July 1 2011 through June 30 2012

A B C D = A-C E F

Finding 1

Vendor Svc

Code Description Infant Delopment Program HS0468 805

Audited Months

Jul-11 Aug-11 Sep-11 Oct-11 Nov-11 Dec-11 Jan-12

Hrs Per Initial Draft Report

55425 69407 53441 26507 24990

(24559) 1184

Amount Per Initial Draft Report

4154658 $ 5202749 $ 4005938 $ 1986964 $ 1873252 $

(1840942) $ 88752 $

Additional Hrs Allowed

3725 3275

--

1400 --

Adjusted Hours

51700 66132 53441 26507 23590

(24559) 1184

Adjusted Amount

279226 $ 245494 $

--

104944 $ --

Amount Due DDS (Final Audit Report)

3875432 $ 4957255 $ 4005938 $ 1986964 $ 1768308 $

(1840942) $ 88752 $

SubTotal

Feb-12 Mar-12 Apr-12 May-12 Jun-12

24266 22225 23483 31258 51299

358926

1818980 $ 1665986 $ 1760286 $ 2343100 $ 3845374 $

26905097 $

550 075 550

1900 900

12375

23716 22150 22933 29358 50399

346551

41228 $ 5622 $

41228 $ 142424 $

67464 $ 927630 $

1777752 $ 1660364 $ 1719058 $ 2200676 $ 3777910 $

25977467 $

11

I Can Too Learning Center LLC Attachment B Unsupported Billings Failure to Bill Adjustments

Audit Period July 1 2011 through June 30 2012

A B C D = A-C E F

Finding 1

Vendor Svc

Code Description Infant Delopment Program HS0698 805

SubTotal

Audited Months

Jul-11 Aug-11 Sep-11 Oct-11 Nov-11 Dec-11 Jan-12 Feb-12 Mar-12 Apr-12 May-12 Jun-12

Hrs Per Initial Draft Report

5075 7825

12750 10600

7450 9425

15650 10275

8025 2725 7200 4825

101825

Amount Per Initial Draft Report

287549 $ 443364 $ 722415 $ 600595 $ 422116 $ 534020 $ 886730 $ 582182 $ 454697 $ 154399 $ 407952 $ 273385 $

5769404 $

Additional Hrs Allowed

Adjusted Hours

Adjusted Amount

Amount Due DDS (Final Audit Report)

287549 $ 443364 $ 722415 $ 600595 $ 422116 $ 534020 $ 886730 $ 582182 $ 454697 $ 154399 $ 407952 $ 273385 $

5769404 $

12

I Can Too Learning Center LLC Attachment B Unsupported Billings Failure to Bill Adjustments

Audit Period July 1 2011 through June 30 2012

A B C D = A-C E F

Audited Hrs Per Initial Amount Per Initial Additional Adjusted Adjusted Amount Due DDS Svc Months Draft Report Draft Report Hrs Allowed Hours Amount (Final Audit Report) Finding Vendor Code Description

2 ClientParent Support Behavior Intervention Training PS0044 048 Jul-11 15920 $ 809673 - 15920 - $ 809673

Aug-11 8966 $ 434965 350 8616 $ 17258 $ 417707 Sep-11 18746 $ 911341 1375 17371 $ 94429 $ 816912 Oct-11 14656 $ 775926 700 13956 $ 43393 $ 732533 Nov-11 21044 $ 963355 1850 19194 $ 115632 $ 847723 Dec-11 17345 $ 886563 - 17345 - $ 886563 Jan-12 14759 $ 934482 - 14759 - $ 934482 Feb-12 19444 $ 1027247 1025 18419 $ 72734 $ 954513 Mar-12 9019 $ 677721 350 8669 $ 22806 $ 654915 Apr-12 12968 $ 780350 900 12068 $ 66569 $ 713781 May-12 14151 $ 793722 1175 12976 $ 71253 $ 722469 Jun-12 22142 $ 1091989 1000 21142 $ 70391 $ 1021598

SubTotal 189160 $ 10087335 8725 180435 $ 574466 $ 9512869

Grand Total Due To DDS $ 41259740

13

Attachment C

March 172014

Edward Y an Manager Department of Developmental Services Audit Branch 1600 9th St Room 230 MS 2-10 Sacramento CA 95814

Re Official Response to I Can Too Learning Center LLC Draft Audit Report

Dear Mr Yan

Thank you for the release of the draft audit report and the review conducted February 19 2014 with the I Can TooTrumpet Behavioral Health team

We have three fonnal responses to the draft report

bull For sessions in which some clinical documentation andor parent verification was

available I Can Too was given only partial credit for sessions In total this represented

1050 hours of credit Ve believe pay record data associated with those sessions in which we can tie an employees schedule to billed hours to their payroll stubs should constitute full allowance for the entirety of those sessions This will significantly

increase the number of hours accepted Per a follow-up meeting withAl Kitay and Pardeep D eol on Tuesday March 41

h (prior to which we submitted significant data backshy

up regarding one specific consumer) we were given approval to submit that

documentation as back-up and receive credit for the additional hours VIe will provide a

separate addendum to this letter Nith the total ofhours consumers and $s that we plan to submit for which we are requesting inclusion

bull During the audit exit meeting Al and Pardeep indicated that we had documentation that

counted toward supported billing for several consumers during the months of the audit period but a purchase of service (PO S) was not in the Sand Andreas Regional Center (SARC) system to bill these services Per Aland Pardeeps suggestion Ve have found a

copy of the POS andor initial referral email for the consumer from the SARC service coordinator Ve intend to contact SARC directly to bill these services per A1 and Pardeeps advice but have also submitted these documents to you for review as well

bull More generally we b elieve that DDS should all ow payroll records (pay-stubs V-2s

etc) to substantiate that sessions took place even when clinical source documentation cmmot be produced A record ofpayment to an employee for the same hours associated with a consumers services in a given month is a reasonable indication that a staff was paid for time (documented in our schedulingpayroll systems) as billable time spent with that particular consumer We believe this is a fair and reasonable proxy to those billable

14services havin g been provided

T

1401 Parkmoor Ave Suite 208 San Jose CA 95126

Attachment C

In the 14 days foll owing the March 3rd follmv-up meeting we have been pulling together extensive payroll schedule and pay stub documenta6on to support the follow-up Ve request a 30 day extension of response (to April 19 20 14) to allow us to provide all remaining documentation By its nature thi s is a very time and energy intensive process- pulling data on hundreds of staffmembers hundreds of consumers across the 1-year audit time-frame and from several different source data systems We appreciate your consideration

J Frankli~ Managing Director I Can Too Learning CenterTrumpet Behavioral Health

15

1401 Parkmoor Ave Suite 208 San Jose CA 95126

Attachment D

DEPARTMENT OF DEVELOPMENTAL SERVICES EVALUATION OF

I CAN TOOrsquoS RESPONSE

As part of the audit process I Can Too Learning Center LLC (ICT) was afforded the opportunity to respond to the draft audit report and provide a written response to each finding identified therein The draft audit report was issued on February 11 2014 The Audit Branch received ICTrsquos response on March 17 2014

DDS evaluated ICTrsquos written response to the draft audit report upon receipt and determined that ICT disagreed with the audit findings DDS determined that although ICTrsquos response did not identify which programs were being discussed the comments were all in relation to Vendor Number HS0468 Provided below are excerpts from ICTrsquos response and DDSrsquo evaluation of the response (See Attachment C to the final audit report for the full text of ICTrsquos response)

Finding 1 Infant Development Program - Unsupported Billings and Failure to Bill

ICT argues the following in response to this finding

Unsupported Billing ldquoFor sessions in which some clinical documentation andor parent verification was available I Can Too was given only partial credit for sessions In total this represented 1050 hours of credit We believe pay record data associated with those sessions in which we can tie an employeersquos schedule to billed hours to their payroll stubs should constitute full allowance for the entirety of those sessionsrdquo

In instances where service billings were considered to be unsupported by DDS due to inadequate source documentation DDS did consider payroll records as support and gave ICT credit when it could tie the payroll to services provided to specific consumers An example is when source documentation included a date employee name and consumer name but no length of time for the session In this instance payroll was used to determine length of time for the session

ldquoDuring the audit exit meeting Al and Pardeep indicated that we had documentation that counted toward supported billing for several consumers during the months of the audit period but a purchase of service (POS) was not in the Sand [sic] Andreas Regional Center (SARC) system to bill those servicesrdquo

DDS determined that there was evidence that services were provided for which payment was not made by the regional center Further analysis revealed that the reason the payment was not received was that there was no authorization in the system CCR title 17 requires that before payments can be made the services must be authorized and the services must be provided Since the services were not authorized at the time of the audit DDS was unable to net those services against the unsupported services DDS suggested that ICT discuss those services with the regional center

16

Attachment D

DEPARTMENT OF DEVELOPMENTAL SERVICES EVALUATION OF

I CAN TOOrsquoS RESPONSE

ldquoMore generally we believe that DDS should allow payroll records (pay-stubs W-2rsquos etc) to substantiate that sessions took place even when clinical source documentation cannot be producedrdquo

Billings are consumer specific while payroll is employee specific Payroll does not indicate whether a service was provided to a consumer Therefore without collaborating evidence it is unknown if direct consumer services were provided

DDSrsquo Conclusion

Subsequent to the receipt of this response ICT provided DDS with documents to support billings that were previously unsupported DDS accepted documents that supported an additional 12375 hours for Vendor Number HS0468 These adjustments are reflected in this report (See Attachment B Page 11) However ICTrsquos response did not address its policies and procedures going forward DDS recommends that ICT develop and implement policies and procedures to ensure that proper documentation is maintained to support its billings to the regional centers A future audit may be conducted by DDS to ensure that DDSrsquo recommendation has been fully implemented

Finding 2 ClientParent Support Intervention Training - Unsupported Billings and Failure to Bill

ICT did not provide an argument in response to this finding however the supporting documentation provided subsequently included support for finding 2 DDS accepted the additional documentation

DDSrsquo Conclusion

Subsequent to the receipt of this response ICT provided DDS with documents to support billings that were previously unsupported DDS accepted documents that supported an additional 8725 hours for Vendor Number PS0044 These adjustments are reflected in this report (See Attachment B Page 13) However ICTrsquos response did not address its policies and procedures going forward DDS recommends that ICT develop and implement policies and procedures to ensure that proper documentation is maintained to support its billings to the regional centers A future audit may be conducted by DDS to ensure that DDSrsquo recommendation has been fully implemented

17

EXECUTIVE SUMMARY

The Department of Developmental Services (DDS) has audited I Can Too Learning Center LLC (ICT) The audit was performed upon the Infant Development Program and ClientParent Support Behavior Intervention Training for the period of July 1 2011 through June 30 2012

The results of the audit disclosed the following issues of non-compliance

Finding 1 Infant Development Program ndash Unsupported Billings and Failure to Bill

The review of ICTrsquos Infant Development Program Vendor Numbers HS0468 and HS0698 revealed that ICT had both unsupported billings as well as appropriate support for services that it failed to bill the San Andreas Regional Center (SARC) As a result ICT had a total of $49891433 of unsupported billings and a total of $18144562 for which it failed to bill

Finding 2 ClientParent Support Behavior Intervention Training ndash Unsupported Billings and Failure to Bill

The review of ICTrsquos ClientParent Support Behavior Intervention Training Vendor Number PS0044 revealed that ICT had both unsupported billings as well as appropriate support for services that it failed to bill the Regional Center of the East Bay (RCEB) As a result ICT had a total of $12412595 of unsupported billings and a total of $2899726 for which it failed to bill

The total unsupported billing discrepancies identified in this audit amounts to $41259740 and is due back to DDS A detailed discussion of these findings is contained in the Findings and Recommendations section of this report

1

BACKGROUND

DDS is responsible under the Lanterman Developmental Disabilities Services Act for ensuring that persons with developmental disabilities receive the services and supports they need to lead more independent productive and normal lives DDS contracts with 21 private nonprofit regional centers that provide fixed points of contact in the community for serving eligible individuals with developmental disabilities and their families in California In order for regional centers to fulfill their objectives they secure services and supports from qualified service providers andor contractors Pursuant to the Welfare and Institutions (WampI) Code section 46481 DDS has the authority to audit those service providers andor contractors that provide services and supports to persons with developmental disabilities

OBJECTIVE SCOPE AND METHODOLOGY

The audit was conducted to determine whether ICTrsquos Infant Development Program and ClientParent Support Behavior Intervention Training were compliant with the WampI Code California Code of Regulations Title 17 (CCR title 17) and the regional center contracts with ICT for the period of July 1 2011 through June 30 2012

ICT was vendorized by SARC and provided services to RCEB and Golden Gate Regional Center (GGRC) Audit staff reviewed the programs and services provided to SARC and RCEB

The audit was conducted in accordance with the Generally Accepted Government Auditing Standards (GAGAS) issued by the Comptroller General of the United States The auditors did not review the financial statements of ICT nor was this audit intended to express an opinion on the financial statements The auditors limited the review of ICTrsquos internal controls to gain an understanding of the transaction flow and invoice preparation process as necessary to develop appropriate auditing procedures The audit scope was limited to planning and performing audit procedures necessary to obtain reasonable assurance that ICT complied with CCR title 17 Also any complaints that DDSrsquo Audit Branch was aware of regarding noncompliance of laws and regulations were reviewed and followed-up during the course of the audit

Day Programs

During the audit period ICT operated eight Day Programs The audit included the review of two of ICTrsquos Day Programs Testing was done during the period of July 1 2011 through June 30 2012 The programs audited are listed below

bull Infant Development Program Vendor Numbers HS0468 and HS0698 Service Code 805

The procedures performed at SARC the vendoring regional center and ICT included but were not limited to the following

bull Review of SARCrsquos vendor files for contracts rate letters program designs purchase of service authorizations and correspondence pertinent to the review

2

bull Interview of SARCrsquos staff for vendor background information and to obtain prior vendor audit reports

bull Interview of ICTrsquos staff and management to gain an understanding of its accounting procedures and processes for SARC billings

bull Review of ICTrsquos serviceattendance records to determine if ICT had sufficient and appropriate evidence to support the direct care services billed to SARC

ClientParent Support Behavior Intervention Training

During the audit period ICT operated one ClientParent Support Behavior Intervention Training The audit included the review of ICTrsquos ClientParent Support Behavior Intervention Training Vendor Number PS0044 Service Code 048 Testing was done during the period of July 1 2011 through June 30 2012

The procedures performed at SARC the vendoring regional center and ICT included but were not limited to the following

bull Review of SARCrsquos vendor files for contracts rate letters program designs purchase of service authorizations and correspondence pertinent to the review

bull Interview of SARCrsquos staff for vendor background information and to obtain prior vendor audit reports

bull Interview of ICTrsquos staff and management to gain an understanding of its accounting procedures and processes for RCEB billings

bull Review of ICTrsquos serviceattendance records to determine if ICT has sufficient and appropriate evidence to support the direct care services billed to RCEB

3

CONCLUSION

Based upon items identified in the Findings and Recommendations section ICT did not comply with the requirements of CCR title 17

VIEWS OF RESPONSIBLE OFFICIALS

DDS issued a draft audit report on February 11 2014 The findings in the report were discussed at a formal exit conference with Lani Fritts ICTrsquos Managing Director on February 19 2014 Subsequent to the meeting Mr Fritts responded on March 17 2014 that ICT would submit documents to support additional hours of service

RESTRICTED USE

This report is solely for the information and use of DDS Department of Health Care Services SARC RCEB and ICT This restriction is not intended to limit distribution of this report which is a matter of public record

4

FINDINGS AND RECOMMENDATIONS

Finding 1 Infant Development Program ndash Unsupported Billings and Failure to Bill

The review of ICTrsquos Infant Development Program Vendor Numbers HS0468 and HS0698 for the period of July 1 2011 through June 30 2012 revealed that ICT had both unsupported billings as well as appropriate support for services that it failed to bill to SARC

Unsupported billings occurred due to a lack of appropriate documentation to support the units of service billed to SARC The failure to bill occurred when ICT had appropriate supporting documentation but it did not bill SARC The following are the discrepancies identified

ICT was not able to provide appropriate supporting documentation for 565837 hours of services billed for Vendor Number HS0468 and 131950 hours of services billed for Vendor Number HS0698 The lack of documentation resulted in unsupported billings to SARC in the amount of $42415143 for Vendor Number HS0468 and $7476290 for Vendor Number HS0698 The total unsupported billings amounted to $49891433

In addition ICT provided appropriate supporting documentation for 219286 hours of service for Vendor Number HS0468 and 30125 hours of service for Vendor Number HS0698 but was not billed to SARC This resulted in an unbilled amount of $16437676 for Vendor Number HS0468 and $1706886 for Vendor Number HS0698 The total failure to bill amounted to $18144562

As a result $31746871 is due back to DDS for the unsupported billings (See Attachment A)

CCR title 17 section 54326(a)(3) and (10) states

ldquo(a) All vendors shall

(3) Maintain records of services provided to consumers in sufficient detail to verify delivery of the units of service billed

(10) Bill only for services which are actually provided to consumers and which have been authorized by the referring regional centerhelliprdquo

Also CCR title 17 section 50604(d) and (e) states

ldquo(d) All service providers shall maintain complete service records to support all billinginvoicing for each regional center consumer in the programhellip

(e) All service providersrsquo records shall be supported by source documentationrdquo

5

Recommendation ICT must reimburse to DDS the $31746871 for the unsupported billings In addition ICT should develop and implement policies and procedures to ensure that proper documentation is maintained to support the amounts billed to SARC

ICTrsquos Response Lani Fritts ICTrsquos Managing Director stated via letter to Edward Yan DDSrsquo Audit Manager dated March 17 2014 that ICT had additional documentation to provide that would support some of the billings A copy of the letter is enclosed as Attachment C

Finding 2 ClientParent Support Behavior Intervention Training ndash Unsupported Billings and Failure to Bill

The review of ICTrsquos ClientParent Support Behavior Intervention Training Vendor Number PS0044 for the period of July 1 2011 through June 30 2012 revealed that ICT had both unsupported billings as well as appropriate support for services that it failed to bill to RCEB

Unsupported billings occurred due to a lack of appropriate documentation to support the units of service billed to RCEB The failure to bill occurred when ICT had appropriate supporting documentation but it did not bill RCEB The following are the discrepancies identified

ICT was not able to provide appropriate supporting documentation for 250128 hours of services billed The lack of documentation resulted in unsupported billings to RCEB in the amount of $12412595

In addition ICT provided appropriate supporting documentation for 69693 hours of service but was not billed to RCEB This resulted in an unbilled amount of $2899726

As a result $9512869 is due back to DDS for the unsupported billings (See Attachment A)

CCR title 17 section 54326(a)(3) and (10) states

ldquo(a) All vendors shall

(3) Maintain records of services provided to consumers in sufficient detail to verify delivery of the units of service billed

(10) Bill only for services which are actually provided to consumers and which have been authorized by the referring regional centerhelliprdquo

6

Also CCR title 17 section 50604(d) and (e) states

ldquo(d) All service providers shall maintain complete service records to support all billinginvoicing for each regional center consumer in the programhellip

(e) All service providersrsquo records shall be supported by source documentationrdquo

Recommendation ICT must reimburse to DDS the $9512869 for the unsupported billings In addition ICT should develop and implement policies and procedures to ensure that proper documentation is maintained to support the amounts billed to RCEB

ICTrsquos Response Lani Fritts ICTrsquos Managing Director stated via letter to Edward Yan DDSrsquo Audit Manager dated March 17 2014 that ICT had additional documentation to provide that would support some of the billings A copy of the letter is enclosed as Attachment C

7

Attachment A

Finding 1

Vendor Svc

Code Description Infant Development Program HS0468 805

I Can Too Learning Center LLC Summary of Unsupported Billings amp Failure to Bill Audit Period July 1 2011 through June 30 2012

Sample Months

Jul-11 Aug-11 Sep-11 Oct-11 Nov-11 Dec-11 Jan-12 Feb-12 Mar-12 Apr-12 May-12 Jun-12

A

Rate

$ 7496 $ 7496 $ 7496 $ 7496 $ 7496 $ 7496 $ 7496 $ 7496 $ 7496 $ 7496 $ 7496 $ 7496

B C=AB

Units Amount

54825 4109682 $ 76357 5723721 $ 57808 4333288 $ 46574 3491186 $ 45232 3390592 $ 17533 1314274 $ 21192 1588552 $ 47033 3525594 $ 42742 3203940 $ 42058 3152668 $ 49075 3678662 $ 65408 4902984 $

Unsupported Billings

D E=AD

Units Amount

3125 234250 $ 10225 766466 $

4367 327350 $ 20067 1504222 $ 21642 1622284 $ 42092 3155216 $ 20008 1499800 $ 23317 1747842 $ 20592 1543576 $ 19125 1433610 $ 19717 1477986 $ 15009 1125074 $

Failure to Bill Amount

Due to DDS

Net

3875432 $ 4957255 $ 4005938 $ 1986964 $ 1768308 $

(1840942) $ 88752 $

1777752 $ 1660364 $ 1719058 $ 2200676 $ 3777910 $

Subtotal 565837 42415143 $ 219286 16437676 $ 25977467 $

1 Infant Development Program HS0698 805 Jul-11

Aug-11 Sep-11 Oct-11 Nov-11 Dec-11 Jan-12 Feb-12 Mar-12 Apr-12 May-12 Jun-12

$ 5666 $ 5666 $ 5666 $ 5666 $ 5666 $ 5666 $ 5666 $ 5666 $ 5666 $ 5666 $ 5666 $ 5666

8750 10625 13050 13000 10800 10600 16875 12675 11450

8100 9575 6450

495775 $ 602012 $ 739413 $ 736580 $ 611928 $ 600596 $ 956138 $ 718166 $ 648758 $ 458947 $ 542520 $ 365457 $

3675 2800

300 2400 3350 1175 1225 2400 3425 5375 2375 1625

208226 $ 158648 $

16998 $ 135985 $ 189812 $

66576 $ 69408 $

135984 $ 194061 $ 304548 $ 134568 $

92072 $

287549 $ 443364 $ 722415 $ 600595 $ 422116 $ 534020 $ 886730 $ 582182 $ 454697 $ 154399 $ 407952 $ 273385 $

Subtotal 131950 7476290 $ 30125 1706886 $ 5769404 $

Infant Development Program Total 697787 49891433 $ 249411 18144562 $ 31746871 $

8

Attachment A

I Can Too Learning Center LLC Summary of Unsupported Billings amp Failure to Bill Audit Period July 1 2011 through June 30 2012

Finding Vendor Svc

Code Description Sample Months

A

Rate

B C=AB

Units Amount

Unsupported Billings

D E=AD

Units Amount

Failure to Bill Amount

Due to DDS

Net

2 ClientParent Support Behavior Intervention Training PS0044 048 Jul-11

Jan-11 Total

$ 9369 $ 4931 $ 3452

3200 8951

10051 22202

299810 $ 441376 $ 346961 $

1088147 $

525 2066 3691 6282

49188 $ 101873 $ 127413 $ 278474 $

250622 $ 339503 $ 219548 $ 809673 $

Aug-11

Aug-11 Total

$ 9369 $ 4931 $ 3452

2408 4774

14301 21483

225607 $ 235413 $ 493670 $ 954690 $

750 3275 8842

12867

70268 $ 161489 $ 305226 $ 536983 $

155339 $ 73924 $

188444 $ 417707 $

Sep-11

Sept-11 Total

$ 9369 $ 4931 $ 3452

3266 6899

13141 23306

305994 $ 340193 $ 453627 $

1099814 $

1050 1075 3810 5935

98375 $ 53007 $

131520 $ 282902 $

207620 $ 287185 $ 322107 $ 816912 $

Oct-11

Oct-11 Total

$ 9369 $ 4931 $ 3452

2683 9997 6743

19423

251372 $ 492953 $ 232769 $ 977094 $

775 675

4017 5467

72610 $ 33284 $

138667 $ 244561 $

178762 $ 459669 $

94102 $ 732533 $

Nov-11

Nov-11 Total

$ 9369 $ 4931 $ 3452

2075 10608 22418 35101

194409 $ 523083 $ 773871 $

1491363 $

850 2991

12066 15907

79636 $ 147486 $ 416518 $ 643640 $

114773 $ 375597 $ 357353 $ 847723 $

Dec-11

Dec-11 Total

$ 9369 $ 4931 $ 3452

2675 10249

7968 20892

250623 $ 505380 $ 275056 $

1031059 $

125 991

2431 3547

11711 $ 48867 $ 83918 $

144496 $

238912 $ 456513 $ 191138 $ 886563 $

Jan-12 $ 9369 $ 4931 $ 3452

5241 8368 3291

491033 $ 412626 $ 113605 $

100 200

1841

9369 $ 9862 $

63551 $

481664 $ 402764 $

50054 $

9

Attachment A

I Can Too Learning Center LLC Summary of Unsupported Billings amp Failure to Bill Audit Period July 1 2011 through June 30 2012

Finding Vendor Svc

Code Description Sample Months

Jan-12 Total

A

Rate

B C=AB

Units Amount

Unsupported Billings

16900 1017264 $

D E=AD

Units Amount

Failure to Bill

2141 82782 $

Amount Due to DDS

Net 934482 $

Feb-12

Feb-12 Total

$ 9369 $ 4931 $ 3452

4192 8075

11567 23834

392750 $ 398179 $ 399293 $

1190222 $

633 766

4016 5415

59306 $ 37771 $

138632 $ 235709 $

333444 $ 360408 $ 260661 $ 954513 $

Mar-12

Mar-12 Total

$ 9369 $ 4931 $ 3452

4600 6751 3117

14468

430976 $ 332893 $ 107599 $ 871468 $

033 975

4791 5799

3091 $ 48077 $

165385 $ 216553 $

427885 $ 284816 $ (57786) $

654915 $

Apr-12

Apr-12 Total

$ 9369 $ 4931 $ 3452

3058 8193 3225

14476

286506 $ 403997 $ 111327 $ 801830 $

-333

2075 2408

-$ 16420 $ 71629 $ 88049 $

286506 $ 387577 $

39698 $ 713781 $

May-12

May-12 Total

$ 9369 $ 4931 $ 3452

2925 7426 4575

14926

274046 $ 366178 $ 157929 $ 798153 $

008 534

1408 1950

749 $ 26331 $ 48604 $ 75684 $

273297 $ 339847 $ 109325 $ 722469 $

Jun-12

June 12 Total

$ 9369 $ 4931 $ 3452

2550 9642

10925 23117

238913 $ 475447 $ 377131 $

1091491 $

-116

1859 1975

-$ 5720 $

64173 $ 69893 $

238913 $ 469727 $ 312958 $

1021598 $

Subtotal 250128 12412595 $ 69693 2899726 $ 9512869 $

TOTAL UNSUPPORTED BILLINGS 947915 62304028 $ 319104 21044288 $ 41259740 $

10

I Can Too Learning Center LLC Attachment B Unsupported Billings Failure to Bill Adjustments

Audit Period July 1 2011 through June 30 2012

A B C D = A-C E F

Finding 1

Vendor Svc

Code Description Infant Delopment Program HS0468 805

Audited Months

Jul-11 Aug-11 Sep-11 Oct-11 Nov-11 Dec-11 Jan-12

Hrs Per Initial Draft Report

55425 69407 53441 26507 24990

(24559) 1184

Amount Per Initial Draft Report