VEMW Energy Lunch EU Emissions Trading Scheme: Much Progress, But Not Yet A Blueprint For The World...

32

VEMW Energy Lunch EU Emissions Trading Scheme: Much Progress, But Not Yet A Blueprint For The World Woerden, Netherlands, 24 May 2013 Vianney Schyns, Utility Support Group www.ifieceurope.org & www.usgbv.com for publications 1

-

Upload

devonte-wittie -

Category

Documents

-

view

216 -

download

0

Transcript of VEMW Energy Lunch EU Emissions Trading Scheme: Much Progress, But Not Yet A Blueprint For The World...

VEMW Energy Lunch EU Emissions Trading Scheme: Much Progress, But

Not Yet A Blueprint For The World

Woerden, Netherlands, 24 May 2013Vianney Schyns, Utility Support Group

www.ifieceurope.org & www.usgbv.com for publications

1

1. Major problems EU Climate and Energy field

2. The EU ETS for phase 3 (2013-2020)

– What were the aims of free allocation? – regulatory framework

3. EU ETS: short term issues

– Cross-sectoral correction factor (CSF), financial compensation, split of GHG

permit into more GHG installations

– Carbon Leakage List 2015-2019 (see other presentation)

4. Theory methods of allocation – EU ETS progress: industry benchmarks

5. Theory activity factor: absolute or relative or “hybrid”

6. Fundamental problems EU ETS in phase 3 (2013-2020)

7. Carbon leakage – EU Commission – academia

8. Fundamental solutions for the Structural Reform

9. Some references

2

Contents

• Natural gas and feedstock– Natural gas prices are amongst the highest in the world (next to Japan)

– Unconventional gas causes a huge disadvantage for Europe versus esp. USA;

potentially also big reserves in e.g. China

• Electricity– Electricity prices are amongst the highest in the world (next to Japan)

• Climate package is not (yet) geared to competitiveness– Inefficient overlap with EED (Energy Efficiency Directive)

– High RES costs (subsidies) for generation, upcoming issue is “capacity

mechanisms” with also high cost. Energy Intensive Industry (EII) is not shielded

from RES costs in all MSs (NL: yes, so far; Germany: to a large part). Increasing

pressure that EII must pay also (a part).

– Present EU ETS is likely to cause significant investment & production carbon

leakage

3

1. Major problems EU Climate and Energy field

• Globally

– Avoid carbon leakage (e.g. recital 24, statements Barroso, EP, Council)

• Production leakage (lower production, import product & unemployment)

• Investment leakage

– Protect competitiveness as good as possible (recital 25)

– Good global competitiveness = good resistance to energy and carbon leakage

• Within Europe: avoid distortions, improve effectiveness

– “Harmonised ETS is imperative to avoid distortions in the internal

market” (recital 8) through “Community-wide and fully-harmonised

implementing measures” (Art. 10a(1))

– Environmental effectiveness (recital 20 old, Art. 1, Art. 10a, etc.): move

away from historical grandfathering4

2.1. EU ETS: the aims of free allocation?

1. EU ETS Directive of 2003– Revised, 23 April 2009 (published OJ 5 June 2009), legally binding

2. Commission Decision on Benchmarks and Allocation Rules– Adopted 27 April 2011 (OJ 17 May 2011), legally binding (the “CIMs” *)

3. Guidance Documents on Benchmarks and Allocation Rules– Adopted 14 April 2011 and later, not legally binding

– (1) General guidance, (2) allocation methodologies, (3) data collection, (4)

verification NIMs baseline data reports, (5) carbon leakage, (6) cross boundary

heat flows, (7) new entrants / closure rules, (8) waste gases, (9) sector specific

guidance, PLUS guidance methodology report + Q&As (together 500+ pages)

4. State aid guidelines for EU ETS financial compensation– Adopted 22 May 2012 and 13 December 2012, legally binding

*) CIMs: Community-wide and fully-harmonised Implementation Measures

5

2.2. EU ETS: regulatory framework 2013-2020

• CSF might be early: perhaps < 1.0 in 2013? Causes would be:

– Heat allocation from electricity generators to ETS installations

– Allocation for waste gases (esp. steel) emitted by electricity generators

• However, the present (too ambitious) top 10% benchmarks

deliver 21% reduction versus Weighted Average Efficiency

(WAE)

• Alliance of Energy Intensive Industries (AEII) letter to Mr Jos

Delbeke on 12 December 2012

6

3.1. Cross-sectoral correction factor (CSF)

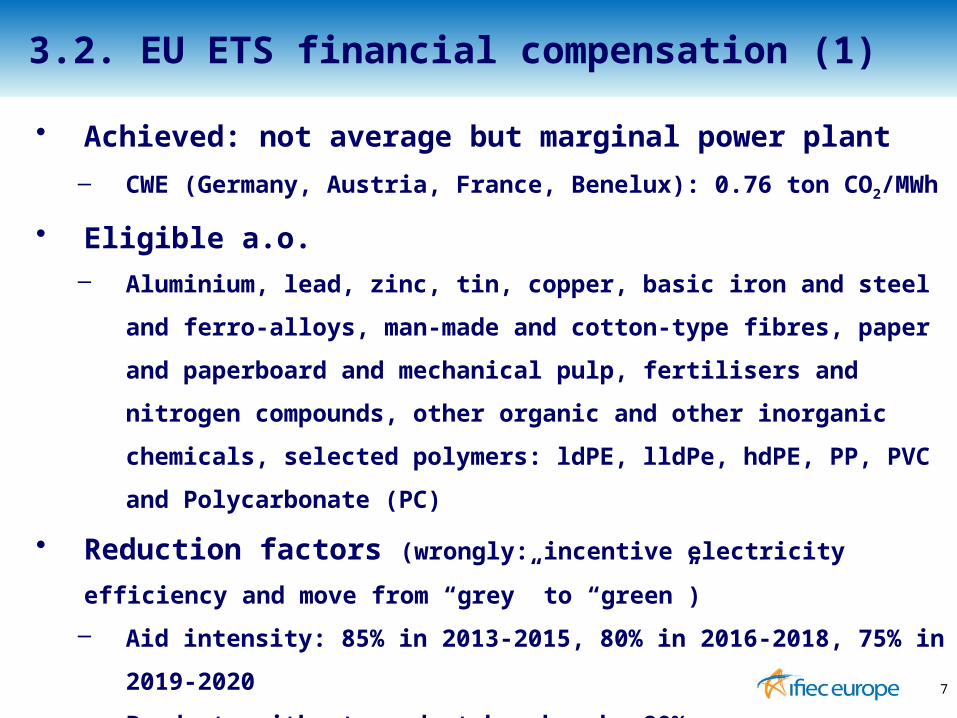

• Achieved: not average but marginal power plant

– CWE (Germany, Austria, France, Benelux): 0.76 ton CO2/MWh

• Eligible a.o.– Aluminium, lead, zinc, tin, copper, basic iron and steel and ferro-alloys,

man-made and cotton-type fibres, paper and paperboard and

mechanical pulp, fertilisers and nitrogen compounds, other organic and

other inorganic chemicals, selected polymers: ldPE, lldPe, hdPE, PP,

PVC and Polycarbonate (PC)

• Reduction factors (wrongly: incentive electricity efficiency and move

from “grey” to “green”)

– Aid intensity: 85% in 2013-2015, 80% in 2016-2018, 75% in 2019-2020

– Products without product benchmark: 80%

7

3.2. EU ETS financial compensation (1)

• Product benchmarks

– Primary aluminium, alumina, basic oxygen steel, EAF carbon steel, EAF

high alloy steel, FeSi, FeMnHC, SiMn, Cl2 (chlorine), Si metal, hyperpure

polysilicon, SiC, HVC (crackers), aromatics, carbon black, styrene,

EO/EG, zinc electrolysis, ammonia

• Production-consumption baseline (most MSs wanted actual!)

– 7-year period 2005-2011, allowed minus one year

– Significant capacity extension (reduction): physical change & 10%

capacity increase (legally not required: 2 highest months in 3 or 6

months after start-up = “start of normal operations”)

– Germany: actual production (max), banking if actual < baseline!

8

3.2. EU ETS financial compensation (2)

• Applicable EUA forward price

– “The simple average of the daily one-year forward EUA prices (closing offer

prices) for delivery in December of the year for which the aid is granted, as

observed in a given EU carbon exchange from 1 January to 31 December of the

year preceding the year for which the aid is granted.”

– “For example, for aid granted for 2016, it is the simple average of the December

2016 EUA closing offer prices observed from 1 January 2015 to 31 December

2015 in a given EU carbon exchange.”

• Eligible volume NL

– 17 TWh ( 17% of total electricity use), 33% of auction revenues (may

rise to e.g. 37% after a possible set-aside)

• This financial compensation is maximum (MS can do less)

9

3.2. EU ETS financial compensation (3)

• Allowed by Commission, less distortions versus other

Member States

– Optimisation of baseline years (median 2005-2008 or median 2009-2010)

– Much easier to get allowances for significant capacity extensions;

criteria: 10% extension or 50,000 allowances and at least 5% extension

10

3.3. Split GHG permit into more GHG installations

1. Auctioning

2. Free allocation, historical grandfathering (basis historical

emissions), like EU ETS phase 1 (2005-2007), phase 2 (2008-2012)

3. Free allocation, benchmark based

– Static benchmarking: allocation = benchmark x historical production

– Dynamic benchmarking: allocation = benchmark x actual production

4. Hybrids, like EU ETS phase 3 (2013-2020):

– Auctioning for electricity production, static benchmarking for direct

emissions of industry, possible financial compensation for the

indirect (electricity) emissions (restricted, inherently unstable)

11

4. Theory: methods of allocation (1)

• Auctioning: only if applied globally (otherwise carbon leakage)

– Generally regarded as ideal system: most effective & efficient

– Production & product carbon price signal

• Production: incentive to reduce emissions for manufacturing installations

• Product: carbon cost fully in variable costs of each product

– Higher product price lower market demand (price elasticity of demand)

– Inter-product competition lower carbon products win market share

– Note, dynamic benchmarking: same production carbon price signal

• Carbon costs also variable costs, carbon cost difference between 2

manufacturing plants: same as for auctioning (unlike static systems)

• Auctioning & dynamic BM: same in following of market dynamics: win/lose

market share, growth and shrinkage on firm level (unlike static systems)

12

4. Theory: methods of allocation (2)

• Free allocation, historical grandfathering

– EU ETS, phase 1 (2005-2007) and phase 2 (2008-2012)

– Considered in the 7 Chinese ETS pilots

• EU ETS experience: historical grandfathering was a failure

Baseline years include crisis years, shut downs, expansions

High polluters are rewarded (high allocation), disadvantage for modern

efficient plants (no reward of early action) as scarcity increases

Uncertainty for expansions, complex rules, barriers & risks for growth

Huge windfall profits for electricity producers (opportunity costs)

“Update” problem: investment to reduce emission lower allocation later,

so operators delay abatement (discount of carbon price signal)

13

4. Theory: methods of allocation (3)

• Free allocation, static benchmarking

– For industry, EU ETS, phase 3 (2013-2020)

• EU ETS experience: progress, but still huge problems

Baseline years for historical production include crisis years, shut downs,

expansions: historical production tells nothing about the future

Uncertainty for expansions, complex rules, barriers & risks for growth

(see reference 4)

The important “update” problem: disappeared, problem solved

14

4. Theory: methods of allocation (4)

• The European Union achieved benchmarks for phase 3

– Leading support role by Ecofys/Fraunhofer and industry federations

– 52 benchmarks: chemicals (15), Paper & pulp (11), ceramics incl.

plaster/gypsum/plasterboard (7), steel industry (6), cement industry incl.

lime/dolime (5), glass (4) aluminium (2), refineries & aromatics (2)

• EU ETS lessons

– A correct technical definition is feasible in a reasonable time

– Stringency of the benchmark is an important framework choice

• EU ETS: “top 10%” benchmarks (average of 10% best installations)

• Australian ETS: weighted average benchmarks, better for competitiveness

– More stringent benchmarks: not better for the environment, to the

contrary: higher incentive carbon leakage lower overall efficiency 15

4. EU ETS achievement: industry benchmarks

• Introduction names & concepts: absolute, relative, hybrid – Absolute schemes, cap & trade in narrow sense

• Permit trading (environmental economists’ literature), ex-ante fixed caps per

firm or auctioning; includes static benchmarking (see reference 5)

• Aims: certainty environmental outcome, they claim as most efficient system

because of (product) carbon price signal – price elasticity of demand

– Relative schemes

• Credit trading (environmental economists’ literature), ex-post to actual

production; other names: baseline-and-credit, performance standard rate

(PSR), rate-, intensity-, output-based; includes dynamic benchmarking

• Our claim: auctioning = “relative” (BM x actual production, BM = 0)

• Aims: avoid carbon leakage, avoid competitive distortions (winning/losing

market share), avoid barriers & risks for growth (see references 2 & 3)

– A hybrid: relative for firms, absolute cap for total (see references 2 & 3)

16

5. Theory: absolute or relative or “hybrid” (1)

• What is best? Difficult subject, analyse via “elimination”• Level 1: absolute caps give certainty of environmental

outcome, relative caps do not; often expressed

– E.g. by Koutstaal et al (CATEP, 2002), EU Commission e.g. in Decision

(2003) on Dutch NOx ETS, EU ETS Directive demands “absolute” for

linking trading schemes (but: position is softening)

– However “absolute” is no guarantee, some targets “can’t be done”:

• Who could have foreseen the immense Chinese growth 10 years ago?

• If absolute would be guaranteed: why not set -85% for 2020, or for 2025?

– Canada (2007): “World Resources Institute noted in a 2006 report, ‘for environmental

performance, what matters overall is that targets are set at reasonably stringent levels

and subsequently are met. This may be achieved with absolute or intensity targets.’”

17

5. Theory: absolute or relative or “hybrid” (2)

• Level 1: issues about ex-ante absolute caps

– Illusion: supply-demand balance predictable for e.g. 10 years ahead?

– Will Europe recover from the crisis? Or remain depressed for 10

years? Or something in between?

– Or: what will happen if Europe recovers from the crisis and economic

growth becomes much higher than expectation? (explosion to very

high carbon price)

18

5. Theory: absolute or relative or “hybrid” (3)

• Level 2: carbon price signal – carbon leakage – windfalls

– Climate Strategies / Carbon Trust, Öko-Institut and many other

environmental economists: actual production is solution to avoid

carbon leakage, but not acceptable because of loss of carbon price

signal (meant: product carbon price signal), “with relative caps

product prices are inefficient” (Koutstaal) – price elasticity of demand

– However: avoidance of carbon leakage and avoidance of possibility

of windfall profits (ref. CE Delft) and maintenance of product carbon

price signal are conflicting objectives, mutually exclusive

• Carbon leakage >> elasticity profit (Carbon Trust)

• Carbon leakage is inefficient, total loss for the environment

(see reference 3, Trilogy Study)

19

5. Theory: absolute or relative or “hybrid” (4)

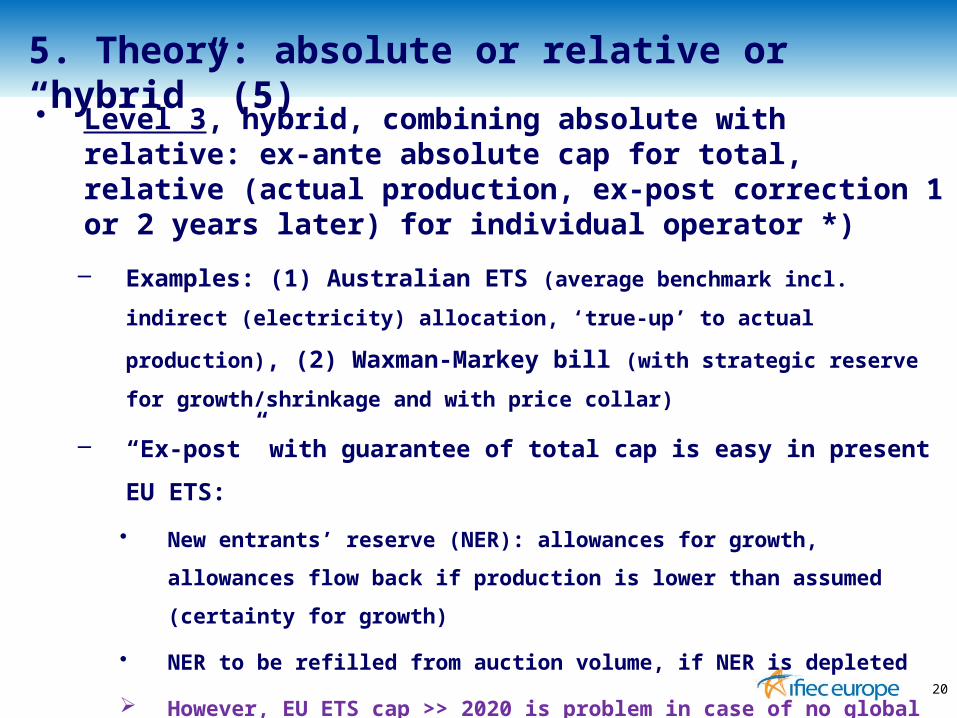

• Level 3, hybrid, combining absolute with relative: ex-ante absolute cap for total, relative (actual production, ex-post correction 1 or 2 years later) for individual operator *)

– Examples: (1) Australian ETS (average benchmark incl. indirect (electricity)

allocation, ‘true-up’ to actual production), (2) Waxman-Markey bill (with

strategic reserve for growth/shrinkage and with price collar)

– “Ex-post” with guarantee of total cap is easy in present EU ETS:

• New entrants’ reserve (NER): allowances for growth, allowances flow back if

production is lower than assumed (certainty for growth)

• NER to be refilled from auction volume, if NER is depleted

However, EU ETS cap >> 2020 is problem in case of no global ETS by 2020

*) Fischer (Resources of the Future), Quirion (CIRED a.o.), Loske / Schyns (see reference 2 & 3)

20

5. Theory: absolute or relative or “hybrid” (5)

• Wide agreement on ideal system long-term

– Auctioning, but then also global rules: what (not) to do with revenues

(otherwise allocation problems are reintroduced via backdoor)

– Global cap, one single carbon price

– Probably also: some supply response – e.g. with carbon banks, auction

reserve price, maximum price

– Same & clever ETS coverage, avoid incentive lack by “ETS borders”

• Example: full bio-based manufacturing plant should not be ‘non-ETS’ (such

as now in the EU ETS), this removes the incentive

21

5. Theory: absolute or relative or “hybrid” (6)

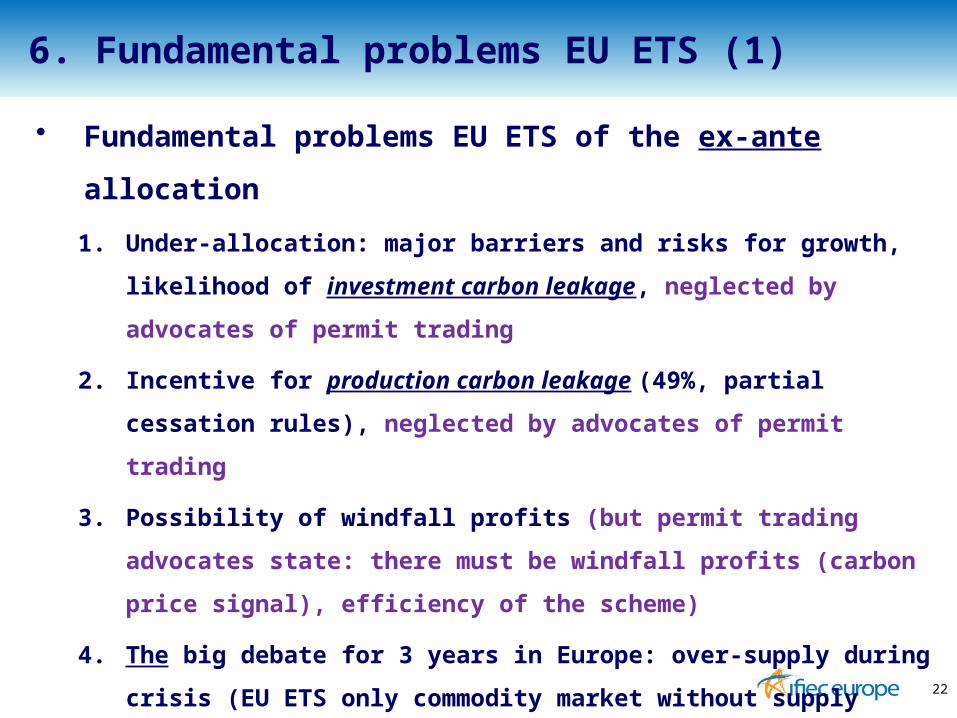

• Fundamental problems EU ETS of the ex-ante allocation

1. Under-allocation: major barriers and risks for growth, likelihood of

investment carbon leakage, neglected by advocates of permit trading

2. Incentive for production carbon leakage (49%, partial cessation rules),

neglected by advocates of permit trading

3. Possibility of windfall profits (but permit trading advocates state: there

must be windfall profits (carbon price signal), efficiency of the scheme)

4. The big debate for 3 years in Europe: over-supply during crisis (EU ETS

only commodity market without supply response) – backloading / set-

aside is conceptually questionable, no structural solution

22

6. Fundamental problems EU ETS (1)

• Carbon Leakage List, assessments each 5 years: uncertainty

• NER limited (sufficient for 1.2% annual growth), (yet) no NER for after 2020

• Unstable, unpredictable and restricted financial compensation: restricted in

terms of (1) coverage of sectors and (2) with reduction factors

• The too stringent “top 10%” immediately in 2013, moves down with cross-

sectoral correction factor CSF (when?) and for new investments with linear reduction

factor LRF, both with 1.74% points per year (70.4% in 2030, 53.0% in 2040)

23

6. Fundamental problems EU ETS (2) – killers

• Various kinds of production carbon leakage by “ex-ante”

– Structural incumbent production carbon leakage: selling allowances

creates more value than Gross Value Added (GVA)

• GVA w/o ETS moves up and down (tight – less tight supply-demand ratio)

• Problem increases over time (CSF), moves from quartile 4 to quartile 3 to

WAE plants and so forth

• CO2 break-even prices generally in the range of € 40-80/ton

– Arbitrage production carbon leakage: a producer arbitrages between

producing in Europe and producing outside Europe while covering

transportation costs into Europe by sales of allowances

• CO2 break-even prices: generally € 25-35/ton until as low as € 15-25/ton

• Also rather low break-even prices for new plants: investment carbon leakage

24

6. Fundamental problems EU ETS (3)

• Error in Impact Assessment (23-1-2008) of EU ETS Directive,

“free allocation does the trick”

– Analysis of allocation options (pages 120-122): (1) harmonised

grandfathering, (2) fully harmonised benchmarking, (3) Hybrid approach:

harmonised benchmarking only for large emitters, (3) relative performance

benchmarking, the latter with the addition “This option does not mean that

allocations will be adjusted to actual production (ex-post adjustments)”.

– Wrong conclusion (page 122): “Since the number of allowances to be

allocated for free is rather determined according to the option chosen as set

out in the preceding section, all options have similar effects as regards

environmental effectiveness and their potential to avoid carbon leakage.”

• Ex-ante allocation is in fact an inbuilt incentive for carbon leakage

25

7.1. Carbon leakage – European Commission

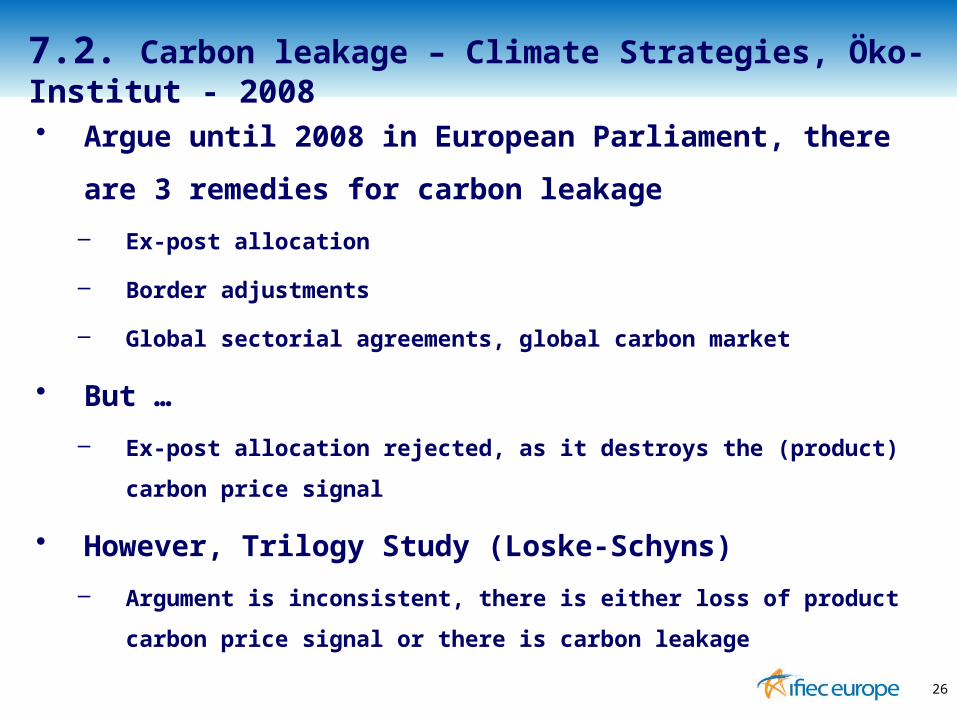

• Argue until 2008 in European Parliament, there are 3 remedies

for carbon leakage

– Ex-post allocation

– Border adjustments

– Global sectorial agreements, global carbon market

• But …

– Ex-post allocation rejected, as it destroys the (product) carbon price signal

• However, Trilogy Study (Loske-Schyns)

– Argument is inconsistent, there is either loss of product carbon price signal

or there is carbon leakage

26

7.2. Carbon leakage – Climate Strategies, Öko-Institut - 2008

• As from 2009, the same 3 remedies for carbon leakage apply

– Ex-post allocation now recommended, next to (preferably)

– Border adjustments

– And of course: global sectorial agreements, global carbon market

• E.g. Climate Strategies– Dröge (2009), page 42

– “Thus, if free allocation of allowances is used to address carbon leakage

under a cap and trade system, it has to be linked to the existence,

availability or production of the installation. …”

• E.g. Grantham-CCCEP (2013) (incl. Öko-Institut), page 42

– “the impact on leakage of production … to non-EU regions is less under

output-based allocation”

27

7.3. Carbon leakage – Climate Strategies, Öko-Institut - 2009

• Avoid carbon leakage = ensure global competitiveness = support Europe

2020 Strategy for Growth and Jobs (industry from 16% to 20% of GDP)

1. Rethink total cap and allocation to industry if by or soon after 2020

there is no global participation with equal carbon burdens

2. Unstable, unpredictable restricted financial compensation, move to

unrestricted indirect allocation, complementary to direct allocation

3. Carbon Leakage List: assessments each 5 years, move to more

certainty: e.g. by comparison electricity, gas and feedstocks and

comparison EU ETS with ETSs outside EU

4. NER: define for after 2020 and guarantee to refill from auction

volume if depleted, no auctioning of left overs

28

8. Fundamental solutions EU ETS (1)

• Avoid carbon leakage = ensure global competitiveness = support Europe

2020 Strategy for Growth and Jobs (industry from 16% to 20% of GDP)

5. Stringent “top 10%” immediately in 2013, move to Weighted Average

Efficiency (WAE) benchmarks

6. CSF and LRF to be replaced by a realistic ILRF (Industry Linear

Reduction Factor) of e.g. 0.8% points per year (‘sliding path’

allocation taking into account technological possibilities, stringent

targets need time & resources)

– Fallbacks: no ILRF but state-of-the art technology! (until … CCS, etc.)

7. Ex-ante allocation, move to ex-post, eliminates barriers & risks for

growth, creates recession-proof system

• Abandon Guidance Docs, move to legally binding rules, simplify rules

29

8. Fundamental solutions EU ETS (2)

• Operational details ex-post allocation per installation

1. Initial allocation = benchmark x historical production median 2005-

2008 or 2009-2010

2. If actual production < historical, surplus flows to NER

3. If actual production > historical, shortage taken from NER

4. Surplus NER end trading period is not auctioned but kept in reserve

for future industrial growth

5. Any shortage of the NER is refilled from the auction volume

• The ex-post correction is also applicable for the “fallback”

benchmarks (heat, fuel, process emissions)

• The ex-post correction can be done in year n+1 or n+2

30

8. Fundamental solutions EU ETS (3)

• Ex-post – last worry of the Commission, DG Climate Action

Director General Jos Delbeke concluded on the stakeholder meeting

of 19 April 2013 that a supply response will indeed be considered, but

that “ex-post” on installation level is not doable because that would

require huge efforts and time to scrutinise and approve the allocation

annually, as is now being undertaken

However, this worry is taken into account

CIMs Art. 23 requires stepwise ex-post adjustments (-50% for 50%-

75% production shrinkage, etc.), while initial allocation is untouched

The proposed (advanced) approach requires ex-post adjustments to

any (higher or lower) production level, while initial allocation is also

untouched

31

8. Fundamental solutions EU ETS (4)

1. “Climate change challenges and the search for a sustainable policy”, Schyns (2005),

a.o. about absolute or relative targets

2. “The IFIEC method for the allocation of CO2 allowances in the EU Emissions Trading

Scheme”, by Ecofys (2008), a.o. electricity benchmark as alternative for auctioning

3. Trilogy Study: “The benefits and feasibility of an ETS based on benchmarks and

actual production”, Loske, Schyns (2008), about ensuring the total cap in an intensity

based scheme & carbon leakage, possible windfall profits and the product- and the

production carbon price signal

4. “A reality check of the EU Emissions Trading Scheme; Does it allow growth – the

major objective of the EU industry policy?”, Brouwers, Stalmans, Schyns (2012),

detailed study of CIMs & Guidance Documents: major barriers & risks for growth

5. “Tradable Permits versus Tradable Credits: A Survey and Analysis”, Nentjes,

Woerdman (2012), a comprehensive ETS history & a comparison of ex-ante (absolute)

fixed emission caps per firm with (relative) ex-post systems32

7. Some References