Vatika Shampoo Project

64

.Soumya Ranjan Sahoo. . Asian School of Business Management . (ASBM) .Bhubaneswar. Sub-“The Availability and visibility analysis of Shampoo market in Bhubaneswar with special reference to Dabur Vatika Shampoo.”

-

Upload

toufique-kazi -

Category

Documents

-

view

357 -

download

9

Transcript of Vatika Shampoo Project

7/27/2019 Vatika Shampoo Project

http://slidepdf.com/reader/full/vatika-shampoo-project 1/64

.Soumya RanjanSahoo.

. Asian School of BusinessManagement .

(ASBM).Bhubaneswar.

Sub-“The Availability and visibility analysis of Shampoo

market in Bhubaneswar with special reference to Dabur Vatika

Shampoo.”

7/27/2019 Vatika Shampoo Project

http://slidepdf.com/reader/full/vatika-shampoo-project 2/64

Table of Contents

Acknowledgement

Executive Summary

Introduction- FMCG Industry

- Hair care Shampoo Industry In India

Company Profile of Dabur

Objectives of Study

Scope and Limitations

Research Methodology

Data Analysis and Interpretation

Findings

Suggestions

Conclusion

Bibliography

Annexure-Questionnaire

2

7/27/2019 Vatika Shampoo Project

http://slidepdf.com/reader/full/vatika-shampoo-project 3/64

INTRODUCTION

FMCG INDUSTY

FMCG refers to consumer non-durable goods required fordaily or frequent use. Typically, a consumer buys thesegoods at least once a month. FMCG industry, alternativelycalled as CPG (Consumer packaged goods) industryprimarily deals with the production, distribution and

marketing of consumer packaged goods. The Fast MovingConsumer Goods (FMCG) is those consumables which arenormally consumed by the consumers at a regular interval.Some of the prime activities of FMCG industry are selling,marketing, financing, purchasing, etc. The industry alsoengaged in operations, supply chain, production andgeneral management.

Typical Characteristics of FMCG products

• Individual products are of small value. But, all FMCG

products put together account for a significant part of

the consumer’s budget.

• The consumer keeps limited inventory of these

products and prefers to purchase them frequently, as

and when required.

3

7/27/2019 Vatika Shampoo Project

http://slidepdf.com/reader/full/vatika-shampoo-project 4/64

• Many of these products are perishable.

• The consumer spends little time on the purchase

decision. Rarely do he / she look for technical

specifications (in contrast to industrial goods).

• Brand loyalties or recommendations of reliable

retailer / dealer drive purchase decision.

• Trial of a new product i.e. brand switching is often

induced by heavy advertisement, recommendations of

the retailer or neighbors / friends.

• These products cater to necessities, comforts as well

as luxuries.

• They meet the demands of the entire cross section of

population.

• Price and income elasticity of demand varies across

products and consumers.

The Indian FMCG sector is the fourth largest sector in theeconomy with a total market size in excess of US$ 13.1billion. It has a strong MNC presence and is characterizedby a well established distribution network, intensecompetition between the organized and unorganizedsegments and low operational cost. Availability of key raw

materials, cheaper labor costs and presence across theentire value chain gives India a competitive advantage.

The FMCG market is set to treble from US$ 11.6 billion in2003 to US$ 33.4 billion in 2015. Penetration level as wellas per capita consumption in most product categories like

jams, toothpaste, skin care, hair wash etc in India is lowindicating the untapped market potential. BurgeoningIndian population, particularly the middle class and the

rural segments, presents an opportunity to makers of

4

7/27/2019 Vatika Shampoo Project

http://slidepdf.com/reader/full/vatika-shampoo-project 5/64

branded products to convert consumers to brandedproducts. Growth is also likely to come from consumer'upgrading' in the matured product categories.

FMCG Sector is expected to grow by over 60% by 2010. That will translate into an annual growth of 10% over a 5-year period. It has been estimated that FMCG sector willrise from around Rs 56,500 crores in 2005 to Rs 92,100crores in 2010. Hair care, household care, male grooming,female hygiene, and the chocolates and confectionerycategories are estimated to be the fastest growingsegments, says an HSBC report. Though the sectorwitnessed a slower growth in 2002-2004, it has been ableto make a fine recovery since then.

FMCG Category and productsHousehold Care:

- Fabric wash (laundry soaps and synthetic detergents)- Household cleaners (dish/utensil, cleaners, floor

cleaners, toilet cleaners, air fresheners, insecticidesand mosquito repellents, metal polish and furniturepolish)

Food and Health beverages:- Soft drinks- Staples/cereals- Beverages bakery products (biscuits, bread, cakes)- Snack Food

- Chocolates, ice cream, tea, coffee- Processed fruits, vegetables; dairy products- Bottled water- Branded flour, branded rice, branded sugar, juices etc.

Personal Care:- Oral care- Hair care- Skin care

- Personal wash (soaps)- Cosmetics and toiletries

5

7/27/2019 Vatika Shampoo Project

http://slidepdf.com/reader/full/vatika-shampoo-project 6/64

- Deodorants, perfumes, feminine hygiene, paper

Current FMCG Scenario

Key Drivers Concerns

Rural penetration Pricecuts/DeflationUrban demographics story Slow downin volume growthsLower input costs ConsumerDowntrading

Innovation Unraveling of Modern Trade

HAIR CARE SHAMPOO INDUSTRY

6

7/27/2019 Vatika Shampoo Project

http://slidepdf.com/reader/full/vatika-shampoo-project 7/64

The hair care market in India is valued at $200 million. It contributes

8% in the total Fmcg sector and has registered a growth of 3.8%

over the previous year. The hair care market can be segmented into

hair oils, shampoos, hair colorants & conditioners, and hair gels.

The Size of shampoo market - 930 Cr with urban areas accounting

for 80% of shampoo sold and rural areas accounting for 20% of

shampoo sold in country. The market is expected to increase due to

increased marketing by players, lower duties, and availability of

shampoos in affordable sachets. Sachet makes up to 70% and anti-

dandruff shampoo up to 20%of the total shampoo sale. This is

primarily a middle class product because more than 50% of the

population uses toilet soaps to wash hair. The penetration level isonly 30% in metros. The major players are HUL and Procter &

Gamble.

The Indian shampoo market is divided in two parts

• Cosmetic (health, shine, strength)

• Anti-dandruff

• Herbal

Brand loyalties in shampoo are not very strong. Consumers

frequently look for a change, particularly in fragrance. Major

expectations from the product are improvement in texture and

manageability, giving softness and bounce to hair, curing and

avoiding damage to the hair. Southern market is predominantly a

sachet market, accounting for 70 % of sachet volumes. In Contrast,

shampoo bottles are more popular in the Northern markets. About50 % of the shampoo bottles are sold in the Northern region alone.

The shampoo industry has lot of scope to be penetrated with all

India penetration level at 51% with urban penetration at 62% and

rural penetration at 46% till now.

Evolution of Shampoo in India

• HLL undisputed leader from the early 90’s Sunsilk launched in

1964 ( General Shampoo platform )

7

7/27/2019 Vatika Shampoo Project

http://slidepdf.com/reader/full/vatika-shampoo-project 8/64

• Clinic Plus launched in 1971 ( Family, health shampoo platform

)

• Clinic All Clear launched in 1987 ( Therapeutic AD Shampoo )

• Sunsilk re-launched in 1987 - Shampoo + Conditioner ( Beauty

platform ) with Sachet SKU

• HLL Goes rural with Sachet

• Clinic Active launched in 1991 ( with Pro Vitamin B - health

platform )

•

Sunsilk re-positioned and re-launched in 1994 (Nutracare) -Pink for dry hair, yellow for normal hair, green for oily hair and

black for long hair.

• P & G enters India in Nov 1995, with the world’s largest selling

brand - Pantene

• P & G launched its internationally acclaimed A & D shampoo H

& S in 1997 with Zinc Pyrithine (ZPT) - a unique anti-microbial

agent. There were 2 variants - regular and menthol.

• Dabur entered the shampoo market in 2000 with its premium

brand, the first natural antidandruff shampoo of India, Dabur

Vatika Antidandruff Shampoo.

8

7/27/2019 Vatika Shampoo Project

http://slidepdf.com/reader/full/vatika-shampoo-project 9/64

9

7/27/2019 Vatika Shampoo Project

http://slidepdf.com/reader/full/vatika-shampoo-project 10/64

COMPANY PROFILE

10

7/27/2019 Vatika Shampoo Project

http://slidepdf.com/reader/full/vatika-shampoo-project 11/64

Dabur India limited is the fourth largest FMCG Companyand one of India's leading Companies. It has a turnover of USD 2479 million with the largest herbal & natural portfolioin India. Building on a legacy of quality and experience forover 125 years, Dabur is today India's most trusted nameand the world's largest Ayurvedic and Natural Health CareCompany. Dabur India's FMCG portfolio today includes fourflagship brands with distinct brand identities -- Dabur asthe master brand for natural healthcare products, Vatikafor premium personal care, Hajmola for digestives, andReal for fruit-based beverages. It has over 350 plusproducts with a retail reach of 2,500,500 through 4000distributors in India.

The evolution of Dabur is quite interesting and its roottakes us back to the 19th century where it all started inBengal by a visionary by name Dr. S.K Burman, a physicianby profession. His mission was to provide effective andaffordable cure for ordinary people in far-flung villages.

With missionary zeal and fervor, Dr. Burman undertook thetask of preparing natural cures for the killer diseases of those days, like cholera, malaria and plague. Soon the newsof his medicines travelled, and he came to be known as thetrusted 'Daktar' or Doctor who came up with effectivecures. And that is how his venture Dabur got its name -derived from the Devanagri rendition of Daktar Burman.

The name is formed by joining the first half of Daktar and

Burman i.e DABUR.

11

7/27/2019 Vatika Shampoo Project

http://slidepdf.com/reader/full/vatika-shampoo-project 12/64

Founding Thoughts

"What is that life worth which cannot bring comfort to others"

The Doorstep Doctor

The story of Dabur began with a small, but

visionary endeavour by Dr. S. K. Burman, a

physician tucked away in Bengal. His mission was

to provide effective and affordable cure for ordinary

people in far-flung villages. With missionary zealand fervour, Dr. Burman undertook the task of

preparing natural cures for the killer diseases of

those days, like cholera, malaria and plague.

Soon the news of his medicines traveled, and he came to be known

as the trusted 'Daktar' or Doctor who came up with effective cures.

And that is how his venture Dabur got its name - derived from the

Devanagri rendition of Daktar Burman. Dr. Burman set up Dabur in

1884 to produce and dispense Ayurvedic medicines. Reaching out to

a wide mass of people who had no access to proper treatment. Dr.

S. K. Burman's commitment and ceaseless efforts resulted in the

company growing from a fledgling medicine manufacturer in a small

Calcutta house, to a household name that at once evokes trust and

reliability.

Vision

12

7/27/2019 Vatika Shampoo Project

http://slidepdf.com/reader/full/vatika-shampoo-project 13/64

“Dedicated to health and well being of every household”

GROWTH STRATEGY

Company History

1884

Birth of Dabur

1896 Setting up a manufacturing plant

Early

1900sAyurvedic medicines

1919 Establishment of research laboratories

1920 Expands further

1936 Dabur India (Dr. S.K. Burman) Pvt. Ltd.

1972 Shift to Delhi

1979 Sahibabad factory / Dabur Research Foundation

1986 Public Limited Company

1992 Joint venture with Agrolimen of Spain

1993 Cancer treatment

1994 Public issues

1995 Joint Ventures

1996 3 separate divisions

1997 Foods Division / Project STARS

1998 Professionals to manage the Company

13

EXPANSION

AQUISITIO

N

INNOVATIO

N

7/27/2019 Vatika Shampoo Project

http://slidepdf.com/reader/full/vatika-shampoo-project 14/64

2000 Turnover of Rs.1,000 crores

2003 Dabur demerges Pharma Business

2005 Dabur acquires Balsara

2005 Dabur announces Bonus after 12 years

2006 Dabur crosses $2 Bin market Cap, adopts US GAAP

2006 Approves FCCB/GDR/ADR up to $200 million

2007 Celebrating 10 years of Real

2007 Foray into organised retail

2007 Dabur Foods Merged With Dabur India

CORE VALUES

Ownership: This is our company. We accept personalresponsibility, and accountability to meet businessneeds.

Passion for Winning: We all are leaders in our areaof responsibility, with a deep commitment to deliver

results. We are determined to be the best at doingwhat matters most.

People Development: People are our most importantasset. We add value through result driven training, andwe encourage & reward excellence.

Consumer Focus: We have superior understanding of consumer needs and develop products to fulfill thembetter.

Team Work: We work together on the principle of mutual trust & transparency in a boundary-lessorganization. We are intellectually honest inadvocating proposals, including recognizing risks.

Innovation: Continuous innovation in products &processes is the basis of our success.

14

7/27/2019 Vatika Shampoo Project

http://slidepdf.com/reader/full/vatika-shampoo-project 15/64

Integrity: We are committed to the achievement of business success with integrity. We are honest withconsumers, with business partners and with eachother.

STRATEGIC INTENT

Focus on growing our core brands across categories,reaching out to new geographies, within and outsideIndia, and improve operational efficiencies by

leveraging technology

Be the preferred company to meet the health andpersonal grooming needs of our target consumers withsafe, efficacious, natural solutions by synthesizing ourdeep knowledge of Ayurveda and herbs with modernscience

Provide our consumers with innovative products within

easy reach

Build a platform to enable Dabur to become a globalAyurvedic leader

Be a professionally managed employer of choice,attracting, developing and retaining quality personnel

Be responsible citizens with a commitment to

environmental protection

Provide superior returns, relative to our peer group, toour shareholders

Business Structure

15

7/27/2019 Vatika Shampoo Project

http://slidepdf.com/reader/full/vatika-shampoo-project 16/64

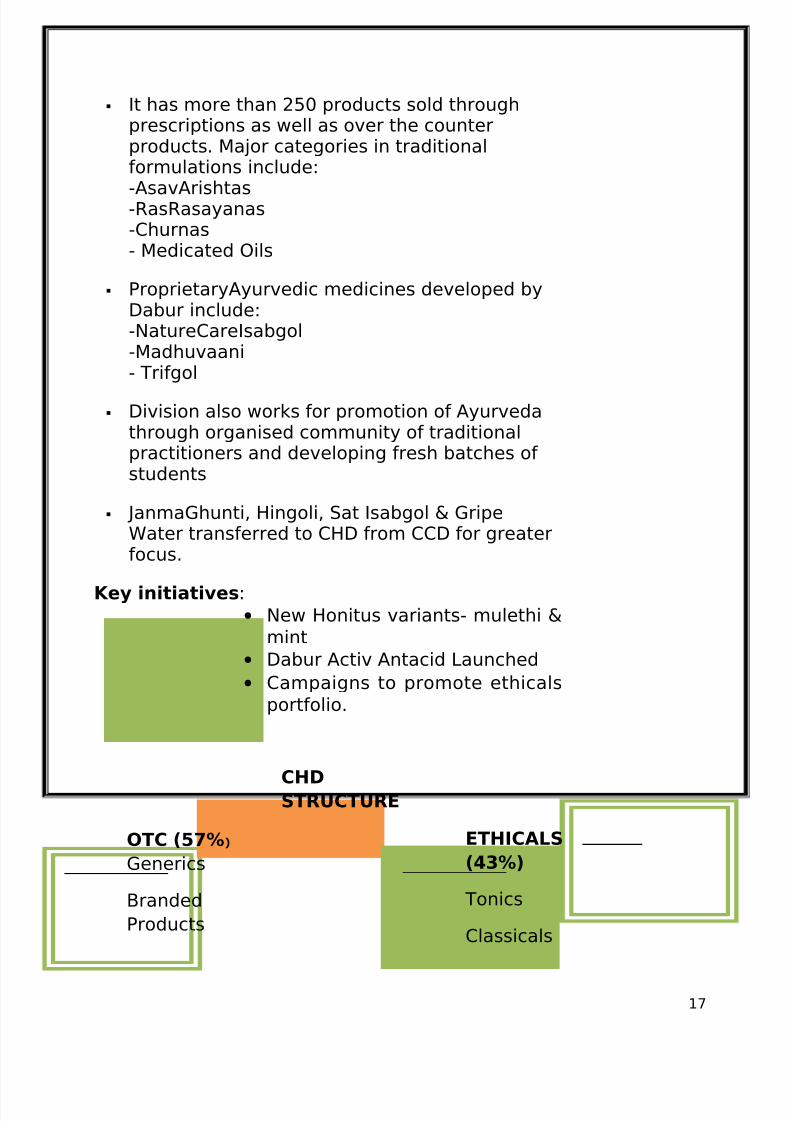

CONSUMER HEALTH DIVISION

Consumer Health Division dealing with classical Ayurvedic

medicines

16

7/27/2019 Vatika Shampoo Project

http://slidepdf.com/reader/full/vatika-shampoo-project 17/64

It has more than 250 products sold throughprescriptions as well as over the counterproducts. Major categories in traditionalformulations include:

-AsavArishtas-RasRasayanas-Churnas- Medicated Oils

ProprietaryAyurvedic medicines developed byDabur include:-NatureCareIsabgol-Madhuvaani

- Trifgol

Division also works for promotion of Ayurvedathrough organised community of traditionalpractitioners and developing fresh batches of students

JanmaGhunti, Hingoli, Sat Isabgol & GripeWater transferred to CHD from CCD for greaterfocus.

Key initiatives:

• New Honitus variants- mulethi &

mint

• Dabur Activ Antacid Launched

• Campaigns to promote ethicals

portfolio.

17

OTC (57% )

Generics

Branded

Products

CHD

STRUCTURE

ETHICALS

(43%)

Tonics

Classicals

7/27/2019 Vatika Shampoo Project

http://slidepdf.com/reader/full/vatika-shampoo-project 18/64

INTERNATIONAL HEALTH DIVISION

IBD continued its strong growth reporting 43.3% growth during9MFY09.

Robust performance in GCC and North African Markets.GCC 47%

Dabur Egypt 85%North Africa 96%Bangladesh 52%Nepal 14%

Key Category Drivers for growth are Hair Cream, Toothpaste,Hamamzaithand Olive Oil.

Strong New Product Development rolls out continues: Amla

Hair Cream and new variants of shampoos being launched inQ4.

New markets opened during the quarter are Lebanon, Turkey,Mauritania and China

Key Initiatives

•

1980’s: DIL Started as an Exporter. Focus on Order fulfillmentthrough India Mfg.

• Early 90’s: Set up a franchisee at Dubai in 1989. Demand

generation led to setting up of mfg in Dubai & Egypt.

• 1995-2000: Renamed franchisee as Dabur International Ltd.

Local operations further strengthened. Set up new mfg

facilities in Nigeria, RAK & Bangladesh.

18

7/27/2019 Vatika Shampoo Project

http://slidepdf.com/reader/full/vatika-shampoo-project 19/64

• Now: Building scale-18% of overall Dabur Sales (9MFY09).High

Levels of Localization & Global Supply chain.

CONSUMER CARE DIVISION

CCD, dealing with FMCG Products relating to Personal Care andHealth Care

Leading brands -

Dabur - The Health Care Brand Vatika-Personal Care Brand

Anmol- Value for Money Brand

Hajmola- Tasty Digestive Brand

and Dabur Amla, Chyawanprash and Lal DantManjan with Rs.100 crore turnover each

19

7/27/2019 Vatika Shampoo Project

http://slidepdf.com/reader/full/vatika-shampoo-project 20/64

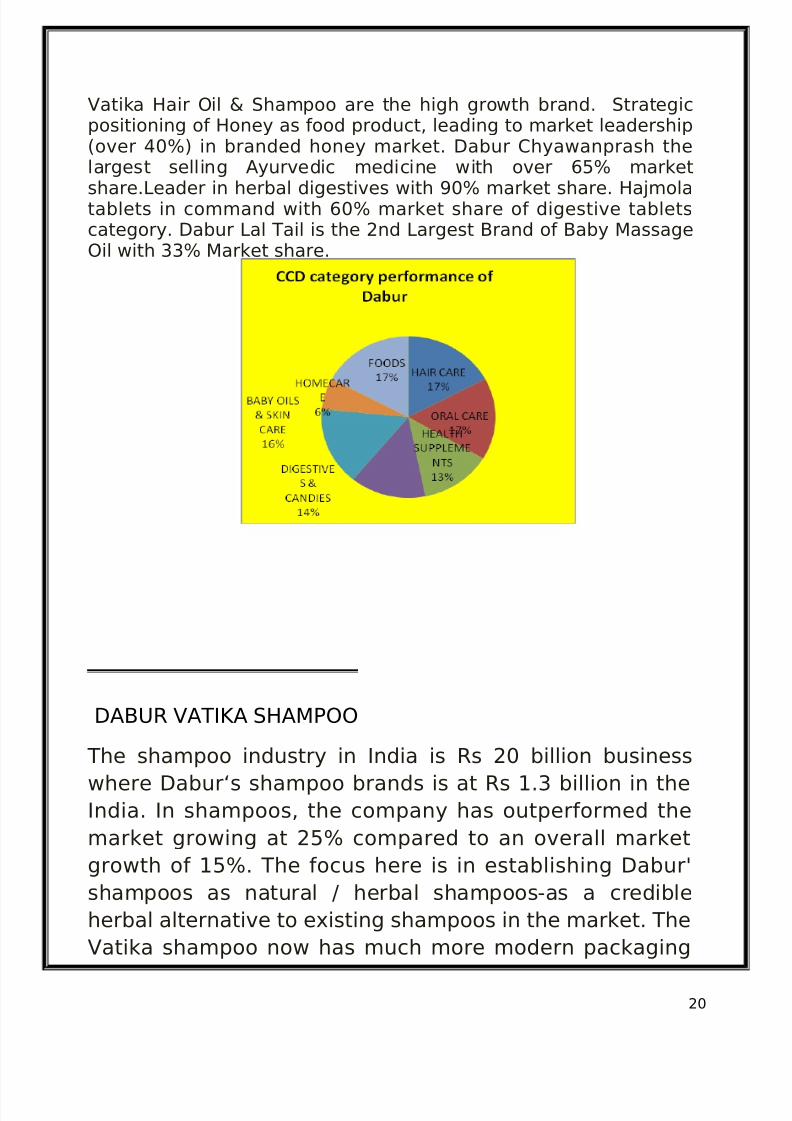

Vatika Hair Oil & Shampoo are the high growth brand. Strategicpositioning of Honey as food product, leading to market leadership(over 40%) in branded honey market. Dabur Chyawanprash thelargest selling Ayurvedic medicine with over 65% market

share.Leader in herbal digestives with 90% market share. Hajmolatablets in command with 60% market share of digestive tabletscategory. Dabur Lal Tail is the 2nd Largest Brand of Baby MassageOil with 33% Market share.

DABUR VATIKA SHAMPOO

The shampoo industry in India is Rs 20 billion businesswhere Dabur‘s shampoo brands is at Rs 1.3 billion in the

India. In shampoos, the company has outperformed the

market growing at 25% compared to an overall market

growth of 15%. The focus here is in establishing Dabur'

shampoos as natural / herbal shampoos-as a credible

herbal alternative to existing shampoos in the market. The

Vatika shampoo now has much more modern packaging

20

7/27/2019 Vatika Shampoo Project

http://slidepdf.com/reader/full/vatika-shampoo-project 21/64

and communication. The newly launched Vatika Black

Shine Shampoo has been well received in the market.

Strong performance of Vatika range of shampoos with a growth of 34% duringQ3 and 32.2% during FY09.

Vatika shampoos growing at double thecategory growth of 19% (Value-April-December 08)

Volume Market Share up from 5% to 6.3% andValue Market Share up from 5.1% to 5.9%

The focus of this initiative is to continue rapid growth inrevenue and profits leveraging three key strategic drivers- Expansion, Acquisition and Innovation. In this roadmap,while Dabur will continue to be positioned as an herbalspecialist leveraging its knowledge and credentials, it willalso widen its business canvass by extending its productsand organization capabilities to service the entire 'Healthand Wellness' space.

Vatika in Hindi means ‘garden’. The brand attempts to liveup to the promises – beauty and nature – that areassociated with its very name. Starting with theseassociations Vatika has assiduously built a brand thatdelivers on all these values through its various productofferings. Vatika products contain natural ingredients thathave been blended together through scientific processesat Dabur’s in-house research laboratories.

ALL ABOUT DABUR VATIKA

Vatika is a brand that espouses traditional wisdom about

21

7/27/2019 Vatika Shampoo Project

http://slidepdf.com/reader/full/vatika-shampoo-project 22/64

health in a modern format. It believes that nature hasperennial answers to day-to-day health issues, particularlywhen it comes to hair care and skin care. In a world wheremodern living causes untold stress the Vatika brand holdsout the promise of providing natural ingredients thatrejuvenate and safeguard the human body in anextraordinary way. This concept is put to work throughcontemporary, modern products, offered by Vatika.

The Vatika woman is young, contemporary, educated,multi-faceted, achievement-driven and confident. It is inthe Vatika brand that she sees a true reflection of her ownpersonal ideals.

The green-and-white colours, used in its packaging, reflectthe brands’ natural ancestry and give it a premium look.

These also help Vatika stand out in the clutteredenvironment of Indian retail. In this category whereplayers talk about chemicals – ZPTO, Ketakenazole etc –

Vatika Anti-Dandruff Shampoo has capitalised on theconsumers’ fear of chemicals by showcasing the efficacyof lemon to eliminate dandruff – with no ill effects on thehair.

The product innovation was fed by the vital consumerinsight that many women in contemporary India areworried about hair problems caused by urban pollution,

frequent change of diet due to geographical mobility andother factors. Beset by modern-day hair problems, theyare far more inclined to rely on home-grown remedies.

Dabur Vatika offers a wide range of hair care shampoo-Vatika Dandruff control, Vatika Black shine & Vatikasmooth & silky shampoo. All these shampoo serve for avariety of Hair problems faced by the consumers and a

very strong alternative for the chemical & medicatedshampoos available in the market.

22

7/27/2019 Vatika Shampoo Project

http://slidepdf.com/reader/full/vatika-shampoo-project 23/64

“Removes Dandruff loves hair”

Vatika Dandruff Control Shampoo removes dandruff without

being violent on hair. Discover non-violence, the new beauty

mantra captured in Vatika Dandruff Control shampoo range.

Enriched with the goodness of nature, Vatika gently removes

100% dandruff and prevents recurrence, without causing anydamage to hair. So what you get is dandruff-free, beautiful hair.

That's the power of non-violence.

“Beautiful Hair Naturally”

Vatika Smooth & Silky Shampoo is a natural shampoo that

conditions from deep within, while gently cleansing and nourishing

the hair. Its offers the gentle & caring touch of nature that leave

the hair soft, silky and radiant. It has the perfect balance of natural

ingredients like Henna, Green Almonds and Shikakai that turn dull

& lifeless hair into smooth & silky without damaging them.

23

7/27/2019 Vatika Shampoo Project

http://slidepdf.com/reader/full/vatika-shampoo-project 24/64

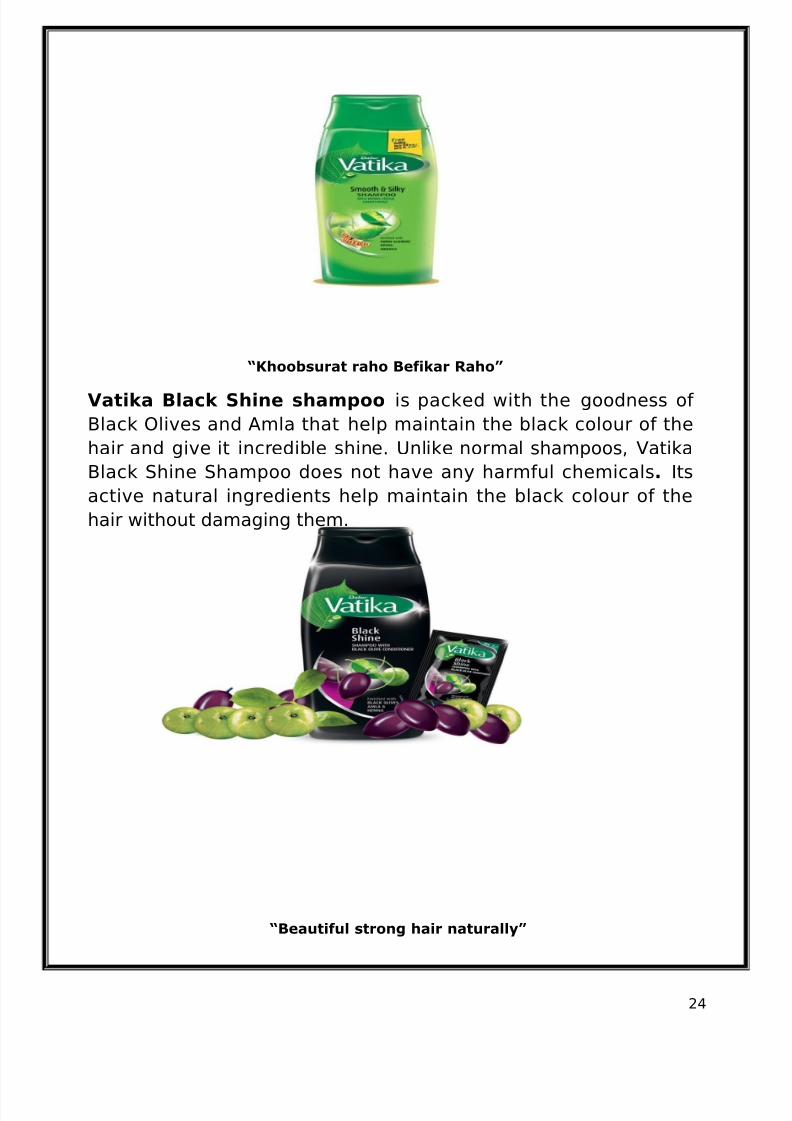

“Khoobsurat raho Befikar Raho”

Vatika Black Shine shampoo is packed with the goodness of

Black Olives and Amla that help maintain the black colour of the

hair and give it incredible shine. Unlike normal shampoos, Vatika

Black Shine Shampoo does not have any harmful chemicals. Its

active natural ingredients help maintain the black colour of the

hair without damaging them.

“Beautiful strong hair naturally”

24

7/27/2019 Vatika Shampoo Project

http://slidepdf.com/reader/full/vatika-shampoo-project 25/64

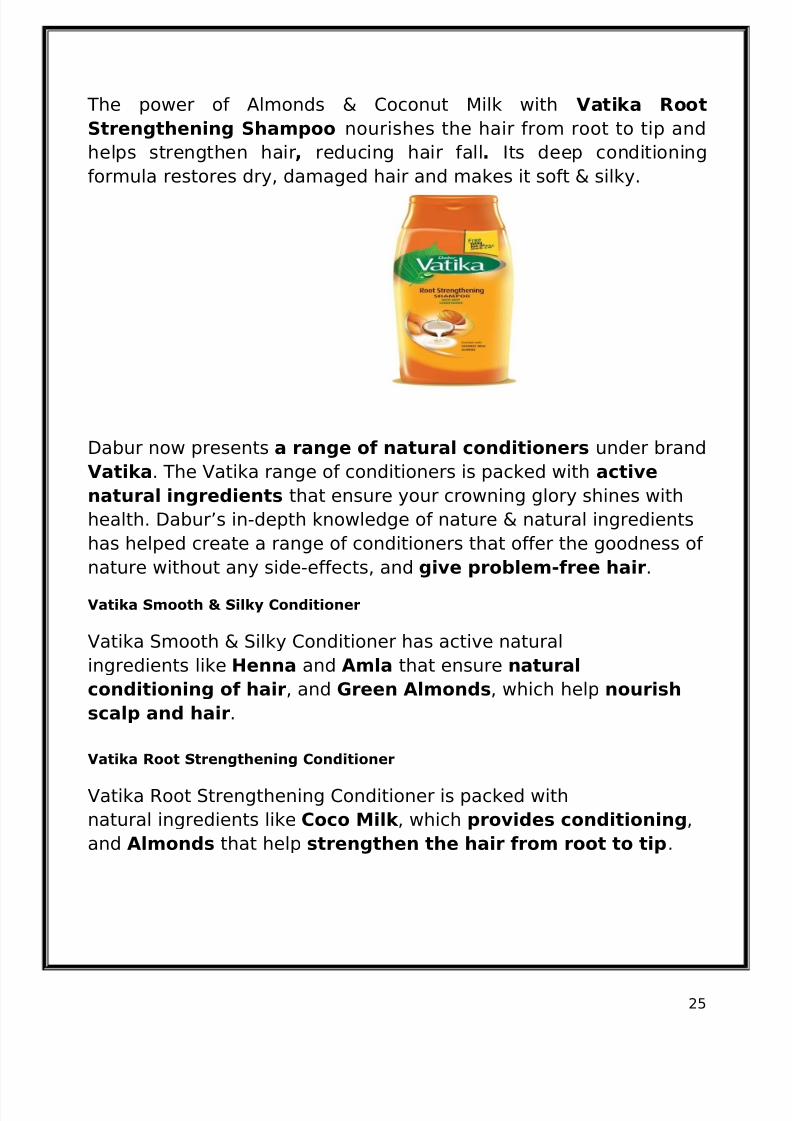

The power of Almonds & Coconut Milk with Vatika Root

Strengthening Shampoo nourishes the hair from root to tip and

helps strengthen hair, reducing hair fall. Its deep conditioning

formula restores dry, damaged hair and makes it soft & silky.

Dabur now presents a range of natural conditioners under brand

Vatika. The Vatika range of conditioners is packed with active

natural ingredients that ensure your crowning glory shines with

health. Dabur’s in-depth knowledge of nature & natural ingredients

has helped create a range of conditioners that offer the goodness of

nature without any side-effects, and give problem-free hair.

Vatika Smooth & Silky Conditioner

Vatika Smooth & Silky Conditioner has active natural

ingredients like Henna and Amla that ensure natural

conditioning of hair, and Green Almonds, which help nourish

scalp and hair.

Vatika Root Strengthening Conditioner Vatika Root Strengthening Conditioner is packed with

natural ingredients like Coco Milk , which provides conditioning,

and Almonds that help strengthen the hair from root to tip.

25

7/27/2019 Vatika Shampoo Project

http://slidepdf.com/reader/full/vatika-shampoo-project 26/64

Distribution network

26

7/27/2019 Vatika Shampoo Project

http://slidepdf.com/reader/full/vatika-shampoo-project 27/64

The distribution network of Dabur India Limited is a very

simple but effective distribution network spreading across

various channels providing for an in depth coverage

facilitating the products to reach the consumers. Theproducts come from factory to the D.C situated in each

state of India and then the distribution divides into URBAN

DISTRIBUTION, RURAL DISTRIBUTION and MODERN TRADE.

URBAN DISTRIBUTION

The urban distribution basically needs various stockiest

who are responsible to reach the market regions of a place. They collect the stocks from the stockiest and supply to

wholesalers, semi wholesalers and retailers which finally

reaches the customers. The market regions are divided into

BEAT PLANS which consist of various areas to be covered

through distribution process. This beat plans consist of

BEAT TYPES which deal with WHOLESALE & LINEWISE

divisions for products that would help in efficientdistribution.

Objectives of the study

All companies are having their own planning and businessstrategies but the company who is having the best, is themost successful company among its competitors. So thecompany can get success within its competitors byapplying best and effective marketing strategies.

The Primary objective of the project was tounderstand the prevailing market conditions of Dabur Vatika Shampoo in Hair-care shampoo marketsegment in the area of Bhubaneswar through amarket survey.

27

7/27/2019 Vatika Shampoo Project

http://slidepdf.com/reader/full/vatika-shampoo-project 28/64

To attain this objective various other sub objectives are

needed to be achieved. These are listed below.

• To analyze the Availability & Visibility of various brands

of shampoo with special reference to Dabur Vatika

Shampoo in Bhubaneswar.

• To find out the Market share of Dabur Vatika Shampoo

in terms of Sales and other brands of shampoo in

Bhubaneswar.• To analyze the consumer preference to various brands

of Shampoo through the Retailers.

• To analyze Sales & Promotion of Dabur Vatika

Shampoo & other Shampoo’s

• To analyze the level of service provided by the

Stockiest of the various brands of Shampoo available

in the Retail market

• Finally, to carry out a competitor analysis of the

various brands of Shampoo for various aspects of

service provided.

Scope and Limitations

28

7/27/2019 Vatika Shampoo Project

http://slidepdf.com/reader/full/vatika-shampoo-project 29/64

SCOPE:

• The study has been done for the hair care-shampoo

market by studying the market condition through the

retailers’ point of view so more or less it helps in

understanding the consumer preference towards the

shampoo market with special reference to Dabur

Vatika shampoo.

• The study can help in analyzing certain weak point,

improving on which a company can overcome the low

sales of Dabur Vatika Shampoo but only in the

Bhubaneswar region covering the areas Saheed

nagar,Unit 3& 4 , Rasulgarh ,Jaydev vihar,C.S .Pur.

LIMITATIONS:

• The study is based on the perception, ideas and

preferences of the respondent (retailers), which are

complex in nature and depend upon subjectivity of the

individual.

• At times there was lack of cooperation from

respondent for research.

29

7/27/2019 Vatika Shampoo Project

http://slidepdf.com/reader/full/vatika-shampoo-project 30/64

• The research was carried out in certain parts of

Bhubaneswar only therefore findings and suggestions

are limited to those parts only.

RESEARCH METHODOLOGY

“Marketing research is a systematic problem analysis, model building and fact finding for the purpose of important decision

making and control in the marketing of goods and services.”

-

Phillip Kotler

Marketing research plays an important role in the processof marketing starting with market component of the totalmarketing tasks. It helps the firm to acquire a betterunderstanding of the consumers, the competition and themarketing environment. Research extends knowledgeabout a particular case through the researcher who buildsup a wealth of knowledge through their research findings.

It is a step-by-step logical process, which involves:

Defining a problem

Laying the objectives of the research

Sources of data

Methods of data collection

30

7/27/2019 Vatika Shampoo Project

http://slidepdf.com/reader/full/vatika-shampoo-project 31/64

Tabulation of data

Data analysis & tabulation

Conclusions & recommendations

Research Plan

The Primary objective of the project was to understand the

prevailing market conditions of in Hair-care shampoo

market in chosen areas of Bhubaneswar with special

reference to Dabur Vatika Shampoo through a marketsurvey. What is the trend in shampoo market and brand

awareness of Dabur Vatika Shampoo.

Nature of Research

Pure and applied research

Pure research is taken for the sake of knowledge without

any intention to apply it in practice. It is undertaken out of

intellectual curiosity or inquisitiveness. It lays the

foundation for applied research. Applied research is carried

on to find solution to a real-life problem so it is problemoriented and action oriented.

Exploratory research

Exploratory research is preliminary study of an unfamiliar

problem about which the researcher has little or no

knowledge at all. It is done at two levels- first, the discovery

31

7/27/2019 Vatika Shampoo Project

http://slidepdf.com/reader/full/vatika-shampoo-project 32/64

of variables in the situation. Second, is the discovery of

relationship between the variables.

Experimental research

It is designed to assess the effects of particular variables on

a phenomenon by keeping the other variables constant or

controlled.

Descriptive research

A descriptive study is a fact finding investigation aimed at

identifying the various characteristics of a problem understudy but it does not deal with testing of hypothesis. Data

are collected by using observation, interviewing and mail

questionnaire.

My project involved descriptive research of study

Data Collection

The descriptive nature of research necessitates collection

of primary data from retailers through market survey,

personal interview technique was used and interview was

conducted through structured questionnaire the question

was asked in prearranged manner. The market research

was conducted over a period of 60 days. Data wastabulated, analyzed and suggestion and recommendation

were given.

Sources of data:

Data refers to a collection of natural phenomena,

descriptors, including the results of experience, observation

or a set of premises. This may consist of nos., words or

32

7/27/2019 Vatika Shampoo Project

http://slidepdf.com/reader/full/vatika-shampoo-project 33/64

images particularly as measurements or observations of a

set of variables.

There are two sources of data:

• Primary Source

• Secondary Source

Primary Source

Data obtained from the first hand by the researcher iscalled the primary data. This data is that the researcher

collects himself. It is reliable way to collect data as it

requires researcher to interact with the source and extract

information. It allows the learner to access original &

unedited information.

Its methods are -

SurveysObservationsQuestionnaireExperiments

I collected data using the primary method by interviewingthe retailers through a structured questionnaire.

Secondary Source:

Secondary data refers to the data available in some form oranother and may include the result of the previouslyperformed research or the available materials. Secondarysources take the role of analyzing, explaining & combiningthe information from the primary source with additional

information.

33

7/27/2019 Vatika Shampoo Project

http://slidepdf.com/reader/full/vatika-shampoo-project 34/64

Its sources are-

INTERNAL SOURCE EXTERNAL SOURCE

Sales Records InternetMarketing activities Standardized Sources- Store audits, CPP, etc.Cost Information Electronic PublishedData

Distribution Report Printed Published DataFeed back

The secondary source for my project is collected from

Dabur India Ltd website and by the data given by Mr.

Dheeman Bhattarcharya, the Regional Sales Manager of

Dabur India for Orissa. I was also provided with needed

information from Senior Sales Officer, Bhubaneswar

Research instrument

The Research instrument chosen for conducting the survey

was structured questionnaire as shown in the annexure.

The questionnaire includes open ended as well as close

ended question, few open ended question were included to

obtain the perception of the retailers.

Sampling Technique

The procedure by which some members of a given

population are selected as representatives of the entire

population.

34

7/27/2019 Vatika Shampoo Project

http://slidepdf.com/reader/full/vatika-shampoo-project 35/64

Probability sampling: ones in which members of the

population have a known chance (probability) of being

selected

Non-probability sampling: instances in which the

chances (probability) of selecting members from the

population are unknown. The project involves non-

probability sampling technique

• Quota Sampling: samples that set a specific number

of certain types of individuals to be interviewed. Often

used to ensure that convenience samples will havedesired proportion of different respondent classes.

My sample technique involved quota sampling as I was

provided five beat areas with definite number of retail

outlets to be covered in my project.

Sampling units

Sampling units were geographical area of Bhubaneswarwhich were divided into four market beat plan.

Geographical areas visited:1.Saheed nagar.

2. Unit -3& 4.3.Rasulgarh –Laxmi, Palasuni.4. Jaydev Vihar-Bda,Mayfair,M .Vihar,A.Vihar.5.C.S Pur- Damana,Saileshri Vihar,Niladri vihar.

The retailers visited during the survey were consideredthe sampling units.

Sample Size

35

7/27/2019 Vatika Shampoo Project

http://slidepdf.com/reader/full/vatika-shampoo-project 36/64

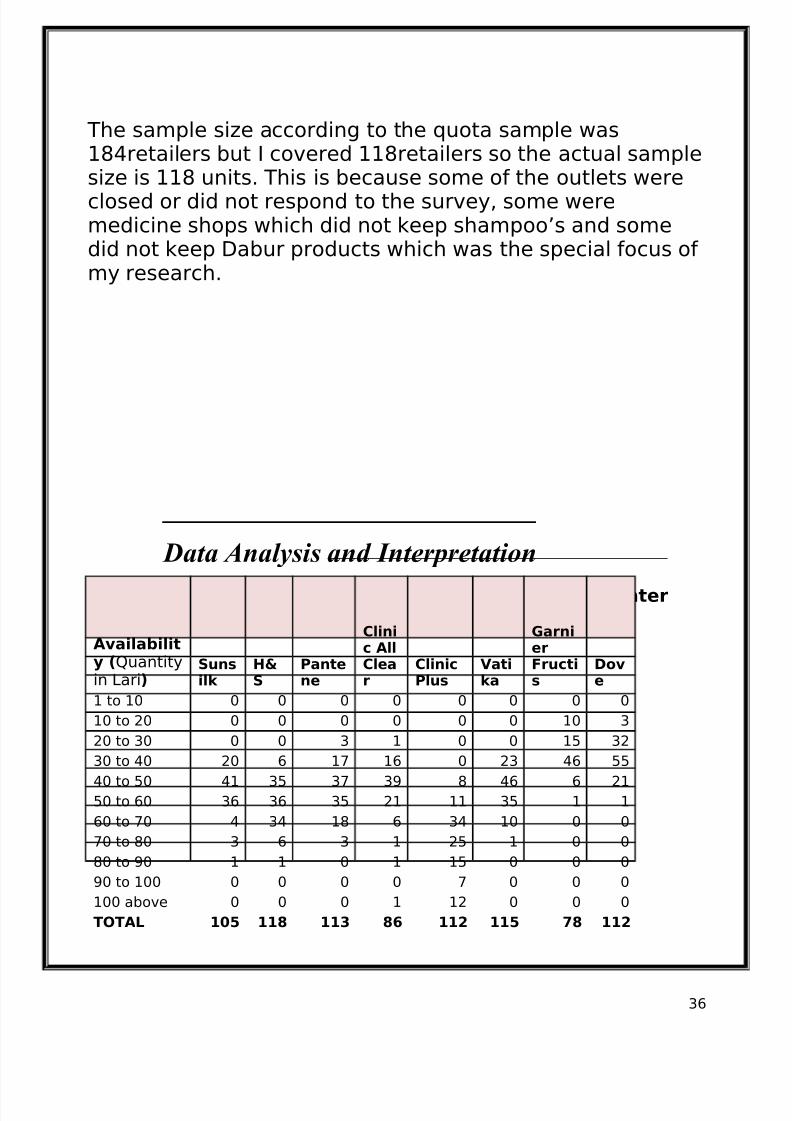

The sample size according to the quota sample was184retailers but I covered 118retailers so the actual samplesize is 118 units. This is because some of the outlets wereclosed or did not respond to the survey, some weremedicine shops which did not keep shampoo’s and somedid not keep Dabur products which was the special focus of my research.

Data Analysis and Interpretation

Shampoo available in the counter

Availability (Quantityin Lari)

Sunsilk

H&S

Pantene

Clinic AllClear

ClinicPlus

Vatika

GarnierFructis

Dove

1 to 10 0 0 0 0 0 0 0 0

10 to 20 0 0 0 0 0 0 10 3

20 to 30 0 0 3 1 0 0 15 32

30 to 40 20 6 17 16 0 23 46 5540 to 50 41 35 37 39 8 46 6 21

50 to 60 36 36 35 21 11 35 1 1

60 to 70 4 34 18 6 34 10 0 0

70 to 80 3 6 3 1 25 1 0 0

80 to 90 1 1 0 1 15 0 0 0

90 to 100 0 0 0 0 7 0 0 0

100 above 0 0 0 1 12 0 0 0

TOTAL 105 118 113 86 112 115 78 112

36

7/27/2019 Vatika Shampoo Project

http://slidepdf.com/reader/full/vatika-shampoo-project 37/64

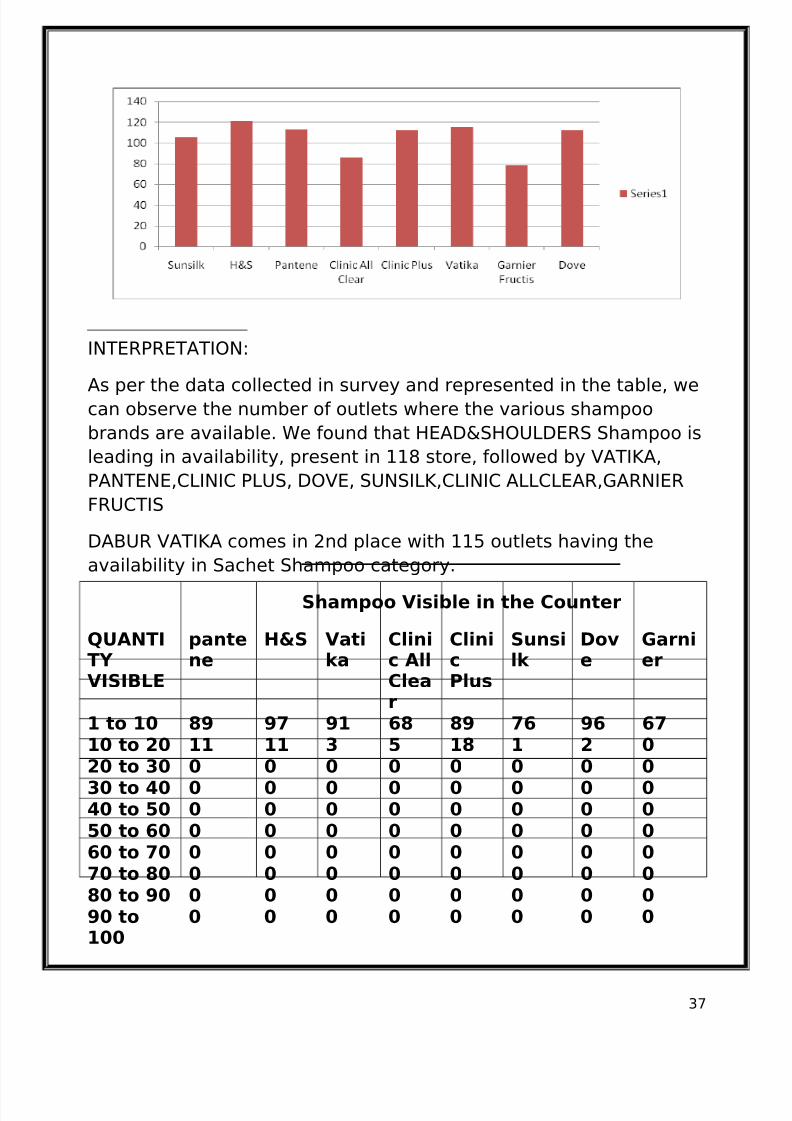

INTERPRETATION:

As per the data collected in survey and represented in the table, we

can observe the number of outlets where the various shampoo

brands are available. We found that HEAD&SHOULDERS Shampoo is

leading in availability, present in 118 store, followed by VATIKA,

PANTENE,CLINIC PLUS, DOVE, SUNSILK,CLINIC ALLCLEAR,GARNIER

FRUCTIS

DABUR VATIKA comes in 2nd place with 115 outlets having the

availability in Sachet Shampoo category.

Shampoo Visible in the Counter

QUANTITY VISIBLE

pantene

H&S Vatika

Clinic AllClear

ClinicPlus

Sunsilk

Dove

Garnier

1 to 10 89 97 91 68 89 76 96 6710 to 20 11 11 3 5 18 1 2 0

20 to 30 0 0 0 0 0 0 0 030 to 40 0 0 0 0 0 0 0 040 to 50 0 0 0 0 0 0 0 050 to 60 0 0 0 0 0 0 0 060 to 70 0 0 0 0 0 0 0 070 to 80 0 0 0 0 0 0 0 080 to 90 0 0 0 0 0 0 0 090 to100

0 0 0 0 0 0 0 0

37

7/27/2019 Vatika Shampoo Project

http://slidepdf.com/reader/full/vatika-shampoo-project 38/64

100Above

0 0 0 0 0 0 0 0

TOTAL 100 108 94 73 107 77 98 67

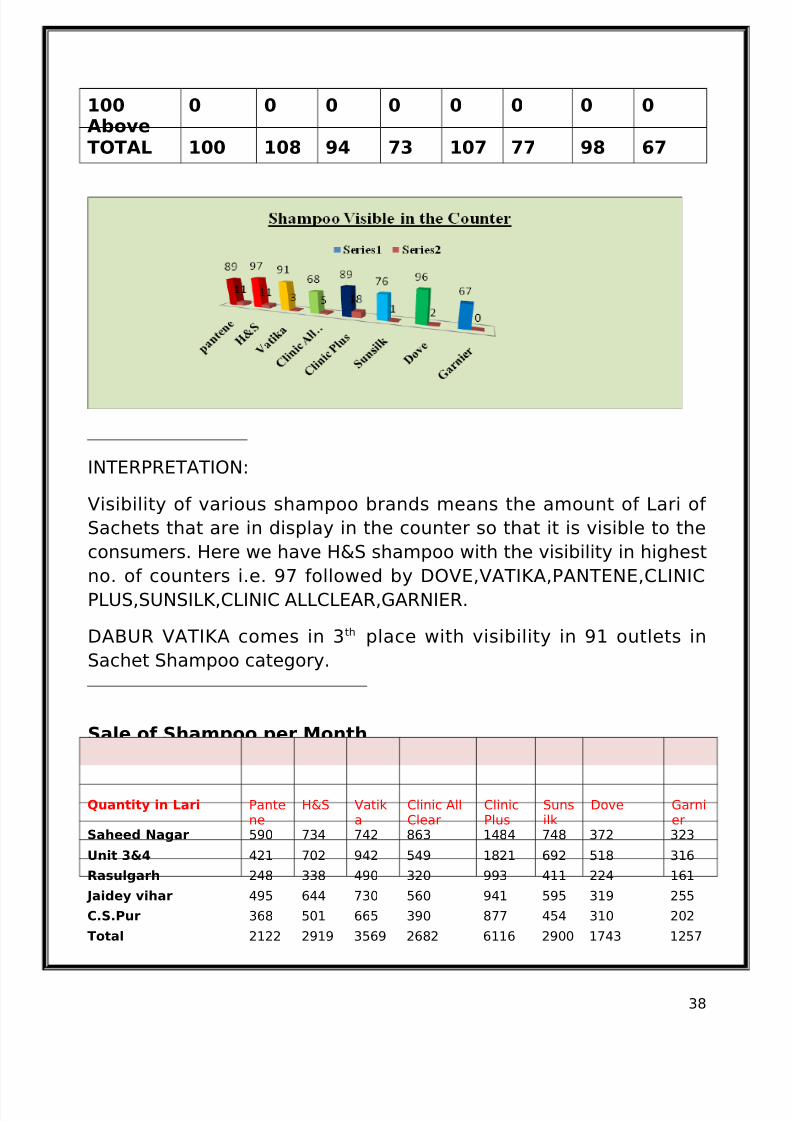

INTERPRETATION:

Visibility of various shampoo brands means the amount of Lari of

Sachets that are in display in the counter so that it is visible to the

consumers. Here we have H&S shampoo with the visibility in highest

no. of counters i.e. 97 followed by DOVE,VATIKA,PANTENE,CLINIC

PLUS,SUNSILK,CLINIC ALLCLEAR,GARNIER.

DABUR VATIKA comes in 3th place with visibility in 91 outlets in

Sachet Shampoo category.

Sale of Shampoo per Month

Quantity in Lari Pantene

H&S Vatika

Clinic AllClear

ClinicPlus

Sunsilk

Dove Garnier

Saheed Nagar 590 734 742 863 1484 748 372 323

Unit 3&4 421 702 942 549 1821 692 518 316

Rasulgarh 248 338 490 320 993 411 224 161

Jaidey vihar 495 644 730 560 941 595 319 255

C.S.Pur 368 501 665 390 877 454 310 202

Total 2122 2919 3569 2682 6116 2900 1743 1257

38

7/27/2019 Vatika Shampoo Project

http://slidepdf.com/reader/full/vatika-shampoo-project 39/64

INTERPRETATION:

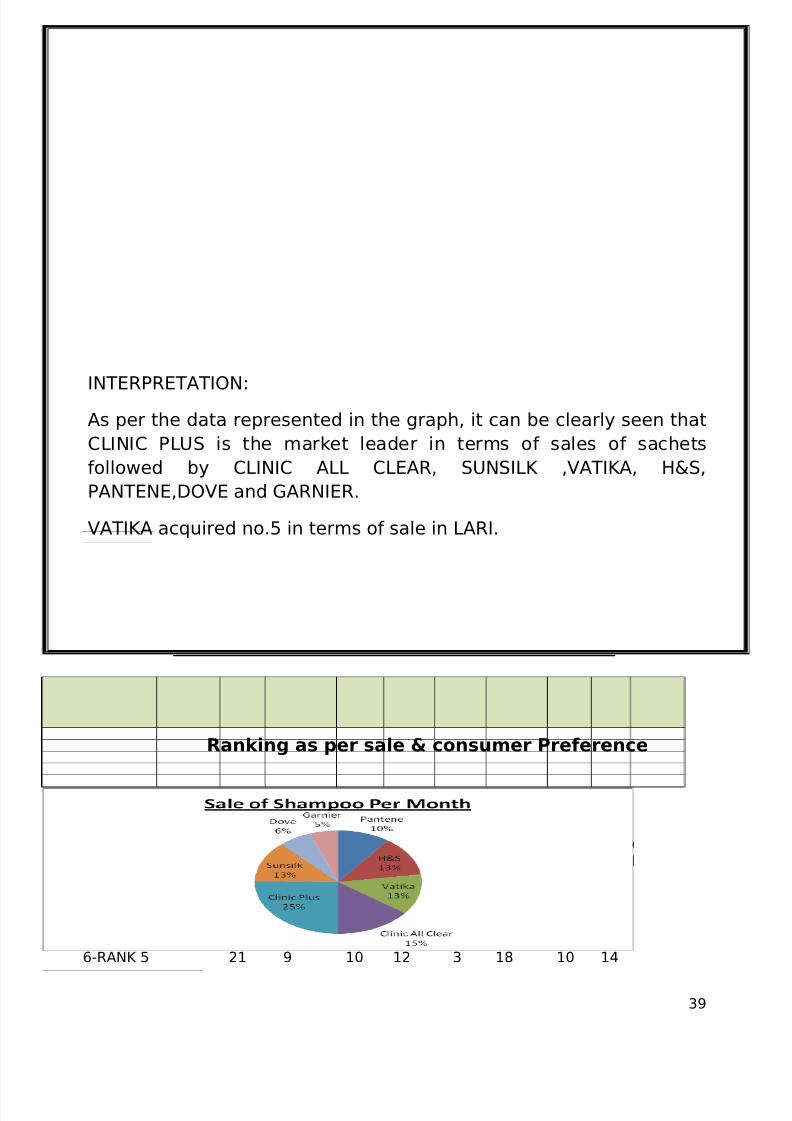

As per the data represented in the graph, it can be clearly seen that

CLINIC PLUS is the market leader in terms of sales of sachets

followed by CLINIC ALL CLEAR, SUNSILK ,VATIKA, H&S,

PANTENE,DOVE and GARNIER.

VATIKA acquired no.5 in terms of sale in LARI.

Ranking as per sale & consumer Preference

Ratings-Ranking

Sunsilk

H&S

Pantene

ClinicAllClear

ClinicPlus

Vatika

GarnierFructis

Dove

Chik

Others

10-RANK 1 3 24 1 0 53 1 6 6 0 0

9-RANK 2 19 31 7 6 10 9 5 8 0 1

8-RANK 3 19 13 13 4 15 9 6 16 1 0

7-RANK 4 20 15 11 15 6 18 5 9 0 0

6-RANK 5 21 9 10 12 3 18 10 14 0 0

39

7/27/2019 Vatika Shampoo Project

http://slidepdf.com/reader/full/vatika-shampoo-project 40/64

5-RANK 6 4 2 22 23 3 17 6 17 0 0

4-RANK 7 5 2 20 24 4 14 11 12 1 0

3-RANK 8 2 0 8 11 1 8 28 10 0 0

2-RANK 9 0 0 0 0 0 1 0 2 9 0

1-RANK 10 0 0 0 0 0 0 0 0 2 0

INTERPRETATION:

The rankings of various Shampoo brands are done according toresponse from 118 retail outlets. CLINIC PLUS has been rated the

most preferred shampoo brand with 53 from 118 outlets

Dabur Vatika is rated rank 1 only by one outlet.

Analysis of Dabur Vatika

Quality of services provided bydistributors

Frequency of salesmanvisit

Excellent

VeryGood Good Fair Poor

Saheed Nagar 3 16 4 2 1

40

7/27/2019 Vatika Shampoo Project

http://slidepdf.com/reader/full/vatika-shampoo-project 41/64

Unit 3&4 1 12 8 8 1

Rasukgarh 3 8 1 2 0

Jaydev vihar 0 14 5 4 1

C.S Pur 2 10 8 1 3

Total 9 60 26 17 6

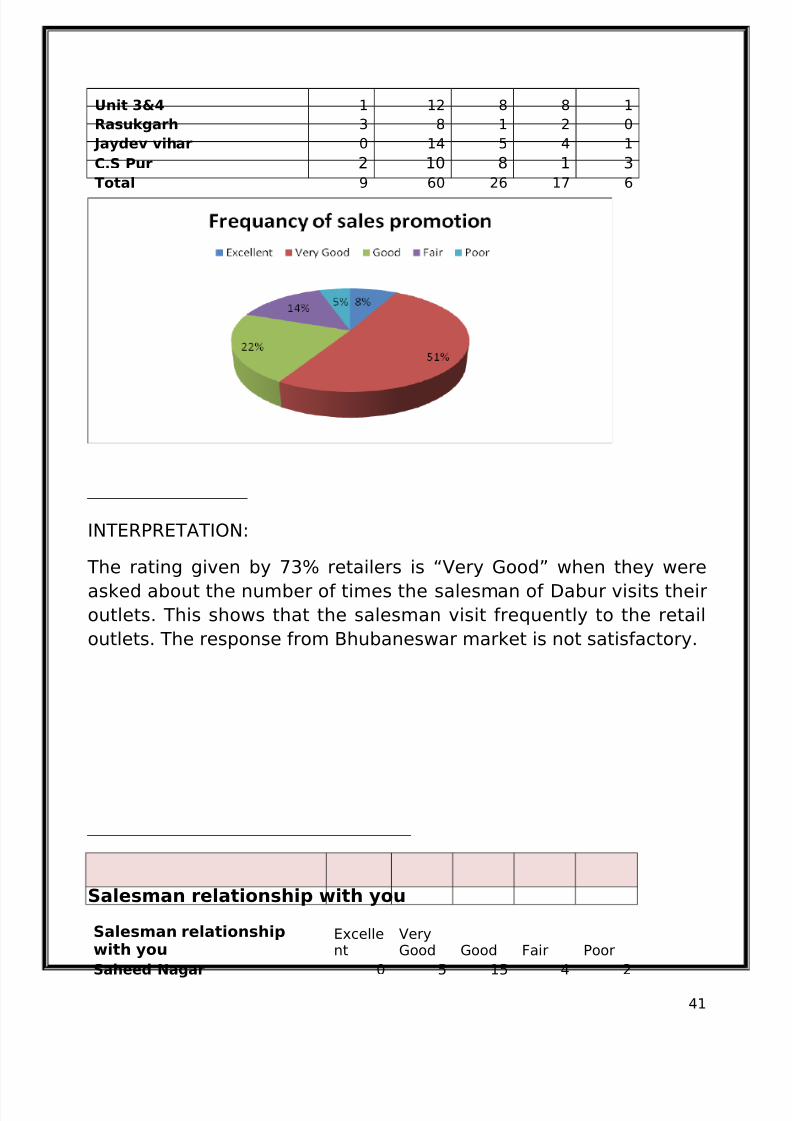

INTERPRETATION:

The rating given by 73% retailers is “Very Good” when they wereasked about the number of times the salesman of Dabur visits their

outlets. This shows that the salesman visit frequently to the retail

outlets. The response from Bhubaneswar market is not satisfactory.

Salesman relationship with you

Salesman relationship

with you

Excelle

nt

Very

Good Good Fair PoorSaheed Nagar 0 5 15 4 2

41

7/27/2019 Vatika Shampoo Project

http://slidepdf.com/reader/full/vatika-shampoo-project 42/64

Unit 3&4 1 10 14 4 1

Rasulgarh 2 5 5 2 0

Jaydev Vihar 0 4 15 3 2

C.s pur 0 2 10 5 7

Total 3 26 59 18 12

INTERPRETATION:

The rating given by 50% retailers is “Good” when they were askedabout the behavior and relationship maintained by the salesman of Dabur Vatika with them. This shows that the salesman have a goodrelationship with the retailers.

Providing all schemes & discounts

Providing all schemes &discounts

Excellent

VeryGood

Good Fair Poor

Saheed Nagar 0 2 8 6 10unit 3&4 0 3 8 8 5Rasulgarh 1 2 4 6 1

Jaydev vihar 0 0 7 5 12

C .S PUR 0 2 3 4 15 Total 1 9 30 29 43

INTERPRETATION:

The rating given by 38% retailers is “POOR” which shows that theretailers are not getting proper schemes and discounts for DaburVatika Shampoo.

Credit facility provided by distributor

Credit facility provided bydistributor

Excellent

VeryGood Good Fair Poor

Saheed Nagar 1 5 10 5 3

Unit 3&4 0 4 8 5 7

Rasulgarh 2 2 3 4 2

Jaydev vihar 0 3 6 5 10

C. s pur 0 0 5 8 11

Total 3 14 32 27 33

INTERPRETATION:

42

7/27/2019 Vatika Shampoo Project

http://slidepdf.com/reader/full/vatika-shampoo-project 43/64

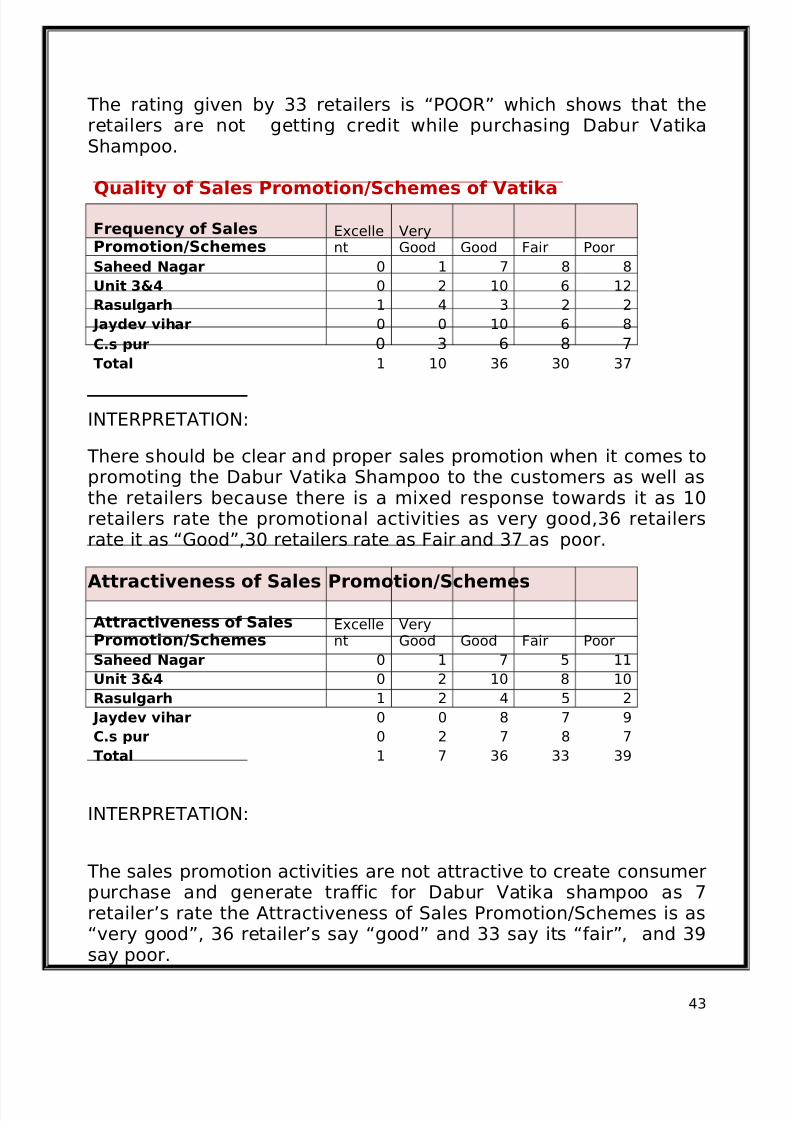

The rating given by 33 retailers is “POOR” which shows that theretailers are not getting credit while purchasing Dabur VatikaShampoo.

Quality of Sales Promotion/Schemes of Vatika

Frequency of SalesPromotion/Schemes

Excellent

VeryGood Good Fair Poor

Saheed Nagar 0 1 7 8 8

Unit 3&4 0 2 10 6 12

Rasulgarh 1 4 3 2 2

Jaydev vihar 0 0 10 6 8

C.s pur 0 3 6 8 7

Total 1 10 36 30 37

INTERPRETATION:

There should be clear and proper sales promotion when it comes topromoting the Dabur Vatika Shampoo to the customers as well asthe retailers because there is a mixed response towards it as 10retailers rate the promotional activities as very good,36 retailersrate it as “Good”,30 retailers rate as Fair and 37 as poor.

Attractiveness of Sales Promotion/Schemes

Attractiveness of SalesPromotion/Schemes

Excellent

VeryGood Good Fair Poor

Saheed Nagar 0 1 7 5 11

Unit 3&4 0 2 10 8 10

Rasulgarh 1 2 4 5 2

Jaydev vihar 0 0 8 7 9

C.s pur 0 2 7 8 7

Total 1 7 36 33 39

INTERPRETATION:

The sales promotion activities are not attractive to create consumerpurchase and generate traffic for Dabur Vatika shampoo as 7retailer’s rate the Attractiveness of Sales Promotion/Schemes is as“very good”, 36 retailer’s say “good” and 33 say its “fair”, and 39

say poor.

43

7/27/2019 Vatika Shampoo Project

http://slidepdf.com/reader/full/vatika-shampoo-project 44/64

Innovativeness of Sales Promotion/schemes

Innovativeness of SalesPromotion/schemes

Excellent

VeryGood Good Fair Poor

Saheed nagar 0 2 8 7 9

Unit 3&4 0 0 10 8 3

Rasulgarh 1 2 3 4 4

Jaydev vihar 0 0 10 4 10

C.s pur 0 2 6 5 11

Total 1 6 37 28 37

INTERPRETATION:

The sales promotion activities are not innovative to createconsumer purchase and generate traffic for Dabur Vatika shampooas 37 retailer’s rate the Innovativeness of Sales Promotion/Schemesis as “good”, 28 retailer’s say “Fair” and 37 say its “poor”.

Response to Competitors Schemes

Response to CompetitorsSchemes

Excellent

VeryGood Good Fair Poor

Saheed Nagar 0 2 8 6 10Unit 3&4 0 1 12 9 9

Rasulgarh 0 3 4 5 2

Jaydev vihar 0 0 5 5 14

C.s pur 0 2 7 8 7

TOTAL 0 8 36 33 42

INTERPRETATION:

The response of 42 retailers was “POOR”,33 say “FAIR”,36 say

“GOOD” and 8 “VERY GOOD” which implies that when it comes to

introduction of more schemes and immediate response of Dabur

towards the marketing activities and strategies of competitor

shampoo brands of HUL, P&G and Garnier is NOT adequate.

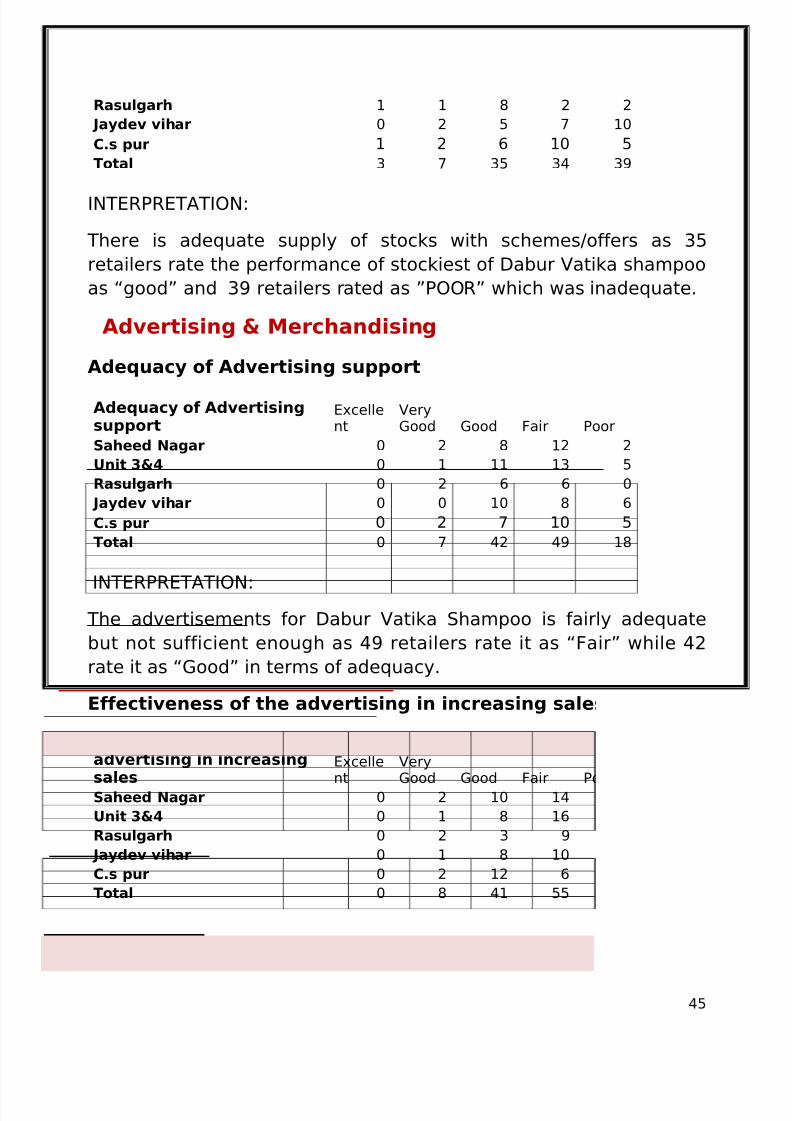

Sufficient supply of stocks with Schemes/offers

Sufficient supply of stocks withSchemes/offers

Excellent

VeryGood Good Fair Poor

Saheed Nagar 1 2 6 8 9Unit 3&4 0 0 10 7 13

44

7/27/2019 Vatika Shampoo Project

http://slidepdf.com/reader/full/vatika-shampoo-project 45/64

Rasulgarh 1 1 8 2 2

Jaydev vihar 0 2 5 7 10

C.s pur 1 2 6 10 5

Total 3 7 35 34 39

INTERPRETATION:

There is adequate supply of stocks with schemes/offers as 35

retailers rate the performance of stockiest of Dabur Vatika shampoo

as “good” and 39 retailers rated as ”POOR” which was inadequate.

Advertising & Merchandising

Adequacy of Advertising support

Adequacy of Advertisingsupport

Excellent

VeryGood Good Fair Poor

Saheed Nagar 0 2 8 12 2

Unit 3&4 0 1 11 13 5

Rasulgarh 0 2 6 6 0

Jaydev vihar 0 0 10 8 6

C.s pur 0 2 7 10 5

Total 0 7 42 49 18

INTERPRETATION:

The advertisements for Dabur Vatika Shampoo is fairly adequate

but not sufficient enough as 49 retailers rate it as “Fair” while 42

rate it as “Good” in terms of adequacy.

Effectiveness of the advertising in increasing sales

Effectiveness of the

advertising in increasingsales

Excellent

VeryGood Good Fair Poor

Saheed Nagar 0 2 10 14 2

Unit 3&4 0 1 8 16 5

Rasulgarh 0 2 3 9 0

Jaydev vihar 0 1 8 10 5

C.s pur 0 2 12 6 4

Total 0 8 41 55 16

INTERPRETATION:

45

7/27/2019 Vatika Shampoo Project

http://slidepdf.com/reader/full/vatika-shampoo-project 46/64

The advertisements for Dabur Vatika Shampoo are “poor” to “very

good” when it comes to increasing sales as 16 retailers’ rate it as

“poor” and 8 retailers rate it as “very good”.

Adequacy of shop-based material like posters, stickers,danglers etc

Adequacy of shop-basedmaterial

Excellent

VeryGood Good Fair Poor

Saheed Nagar 0 2 4 5 13

Unit 3&4 0 1 5 7 17

Rasulgarh 0 2 4 3 5

Jaydev vihar 0 0 5 7 12

C.s pur 0 2 4 5 13

Total 0 7 22 27 60

INTERPRETATION:

There is insufficiency in shop-based materials as 33 retailers haveresponded “Poor” when it comes to shop-based materials for DaburVatika Shampoo.

Quality of Media advertising

Quality of Mediaadvertising

Excellent

VeryGood Good Fair Poor

Saheed Nagar 0 2 3 10 9

Unit 3&4 0 0 5 12 13Rasulgarh 0 1 3 3 7

Jaydev vihar 0 0 2 10 12

C.s pur 0 0 3 6 15

Total 0 3 16 41 56

INTERPRETATION:

The quality of media advertisements is “poor” to “fair” as 56retailers rated it as “poor” and 41 retailers rated it as “Fair”.

46

7/27/2019 Vatika Shampoo Project

http://slidepdf.com/reader/full/vatika-shampoo-project 47/64

Frequency of merchandising

Frequency of merchandising

Excellent

VeryGood Good Fair Poor

Saheed Nagar 0 3 6 5 15Unit 3&4 0 1 4 8 17

Rasulgarh 0 2 3 2 7

Jaydev vihar 0 0 5 8 11

C.s pur 0 0 3 8 13

Total 0 6 21 31 63

INTERPRETATION:

There is merchandising problem for Vatika shampoo as the 63retailers rate it as “Poor”

Quality of merchandising

Quality of merchandisingExcellent

VeryGood Good Fair Poor

Saheed Nagar 0 2 4 8 12

Unit 3&4 0 1 5 11 13

Rasulgarh 0 1 3 2 8 Jaydev vihar 0 0 2 10 12

C.s pur 0 1 5 8 10

Total 0 5 19 39 55

INTERPRETATION:

The quality of merchandising for Vatika shampoo is also not good asthe 55 retailers rate it as “Poor”.

47

7/27/2019 Vatika Shampoo Project

http://slidepdf.com/reader/full/vatika-shampoo-project 48/64

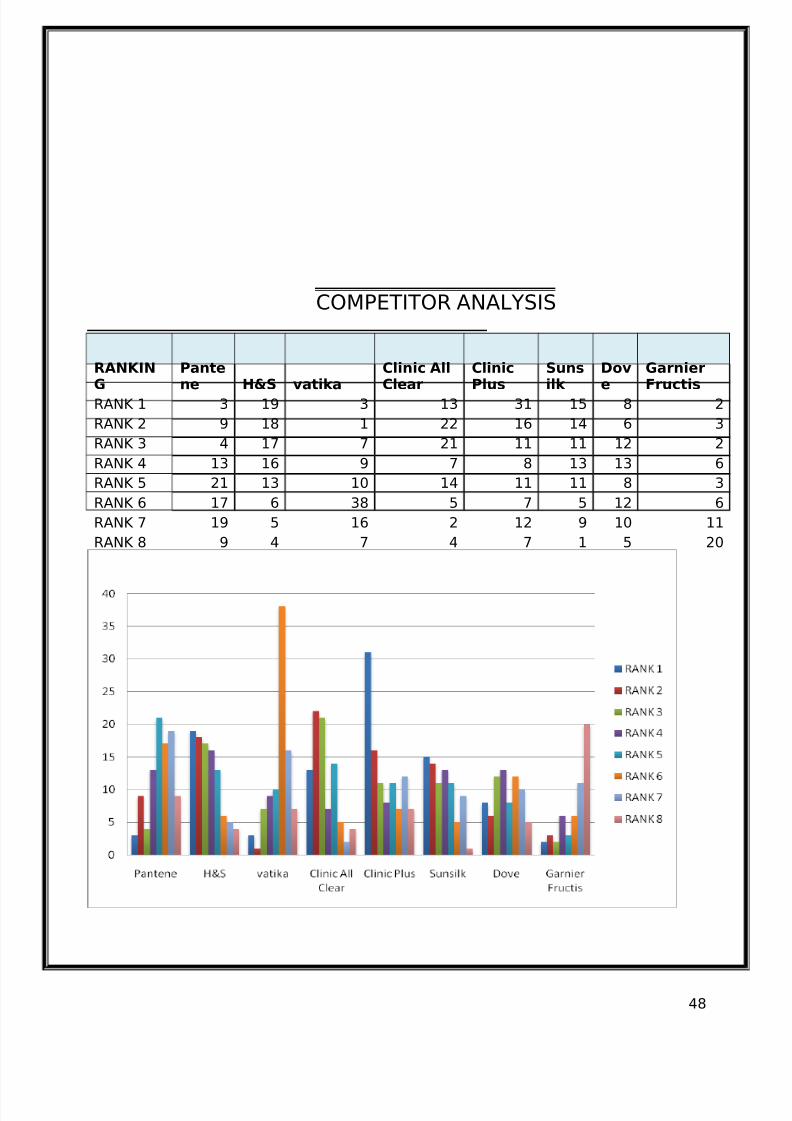

COMPETITOR ANALYSIS

Frequency of Sales Promotion/SchemesRANKIN

G

Pante

ne H&S vatika

Clinic All

Clear

Clinic

Plus

Suns

ilk

Dov

e

Garnier

Fructis

RANK 1 3 19 3 13 31 15 8 2

RANK 2 9 18 1 22 16 14 6 3

RANK 3 4 17 7 21 11 11 12 2

RANK 4 13 16 9 7 8 13 13 6

RANK 5 21 13 10 14 11 11 8 3

RANK 6 17 6 38 5 7 5 12 6

RANK 7 19 5 16 2 12 9 10 11

RANK 8 9 4 7 4 7 1 5 20

48

7/27/2019 Vatika Shampoo Project

http://slidepdf.com/reader/full/vatika-shampoo-project 49/64

INTERPRETATION:

From the interpretation of the data, we come to know that Clinicplus and Clinic Allclear are on no.1 and no.2 respectively. Head &Shoulders, Sunsilk, Pantene are ranked after them.Dabur Vatika is ranked at no.6 that means it needs extra effort topenetrate the market.

Attractiveness of Sales Promotion/Schemes]RANKIN

G

Pante

ne H&S vatika

Clinic All

Clear

Clinic

Plus

Suns

ilk

Do

ve

Garnier

FructisRANK 1 3 19 3 11 30 13 7 2

RANK 2 9 18 1 19 17 14 8 3

RANK 3 4 17 7 21 12 10 6 2

RANK 4 13 16 9 7 8 11 10 6

RANK 5 21 13 10 13 10 5 6 3

RANK 6 17 6 38 4 7 6 11 6

RANK 7 19 5 16 1 11 7 8 11

RANK 8 9 4 7 2 7 3 5 20

49

7/27/2019 Vatika Shampoo Project

http://slidepdf.com/reader/full/vatika-shampoo-project 50/64

INTERPRETATION:

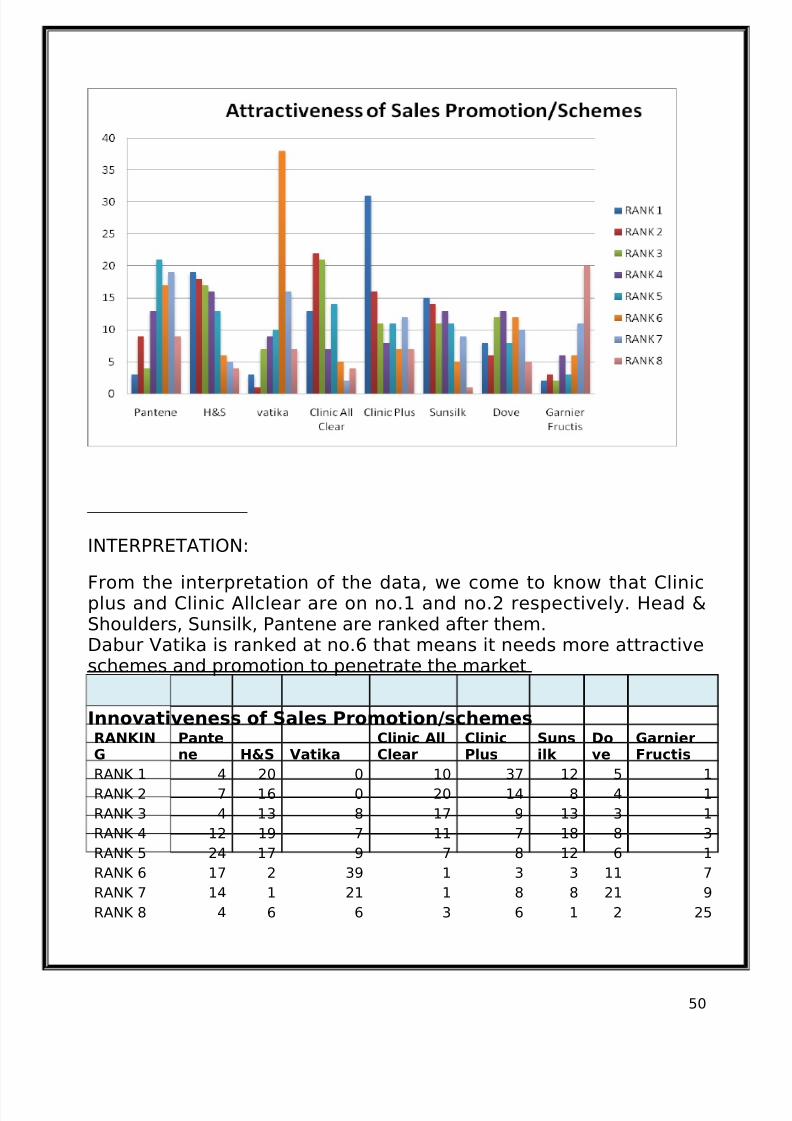

From the interpretation of the data, we come to know that Clinicplus and Clinic Allclear are on no.1 and no.2 respectively. Head &Shoulders, Sunsilk, Pantene are ranked after them.Dabur Vatika is ranked at no.6 that means it needs more attractiveschemes and promotion to penetrate the market

Innovativeness of Sales Promotion/schemesRANKIN

G

Pante

ne H&S Vatika

Clinic All

Clear

Clinic

Plus

Suns

ilk

Do

ve

Garnier

FructisRANK 1 4 20 0 10 37 12 5 1

RANK 2 7 16 0 20 14 8 4 1

RANK 3 4 13 8 17 9 13 3 1

RANK 4 12 19 7 11 7 18 8 3

RANK 5 24 17 9 7 8 12 6 1

RANK 6 17 2 39 1 3 3 11 7

RANK 7 14 1 21 1 8 8 21 9

RANK 8 4 6 6 3 6 1 2 25

50

7/27/2019 Vatika Shampoo Project

http://slidepdf.com/reader/full/vatika-shampoo-project 51/64

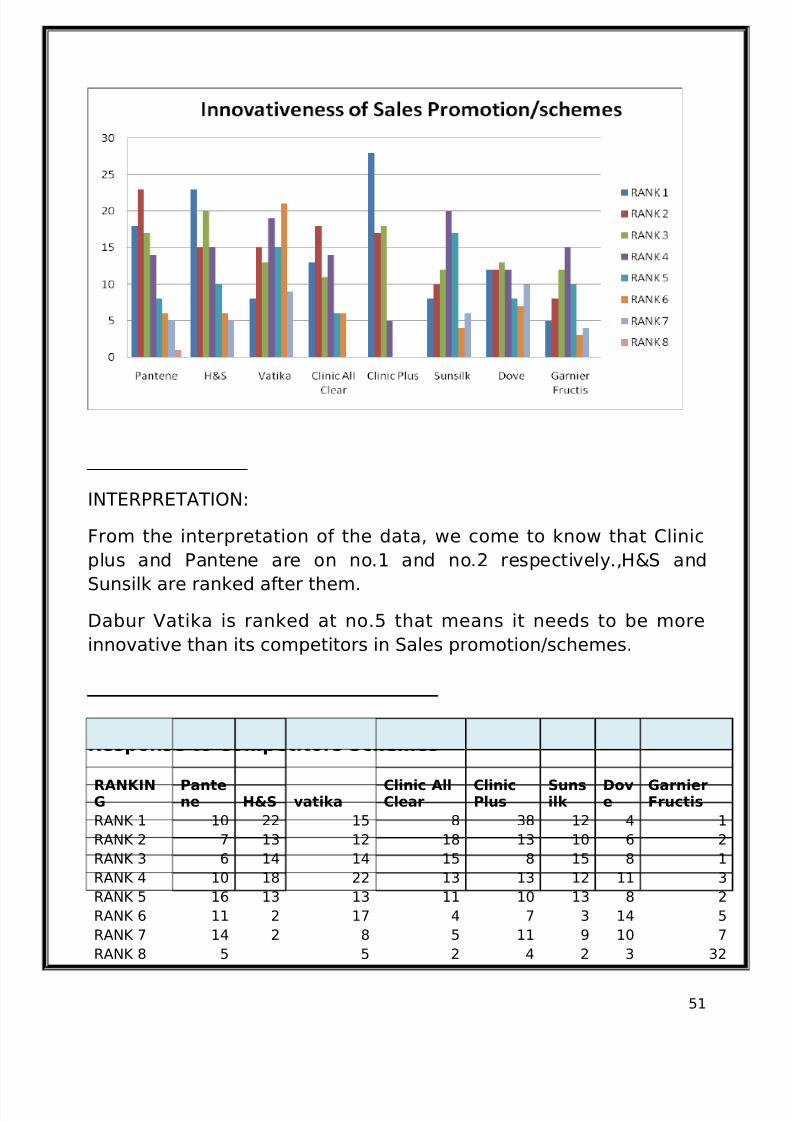

INTERPRETATION:

From the interpretation of the data, we come to know that Clinic

plus and Pantene are on no.1 and no.2 respectively.,H&S andSunsilk are ranked after them.

Dabur Vatika is ranked at no.5 that means it needs to be more

innovative than its competitors in Sales promotion/schemes.

Response to Competitors Schemes

RANKING

Pantene H&S vatika

Clinic AllClear

ClinicPlus

Sunsilk

Dove

GarnierFructis

RANK 1 10 22 15 8 38 12 4 1

RANK 2 7 13 12 18 13 10 6 2

RANK 3 6 14 14 15 8 15 8 1

RANK 4 10 18 22 13 13 12 11 3

RANK 5 16 13 13 11 10 13 8 2

RANK 6 11 2 17 4 7 3 14 5

RANK 7 14 2 8 5 11 9 10 7

RANK 8 5 5 2 4 2 3 32

51

7/27/2019 Vatika Shampoo Project

http://slidepdf.com/reader/full/vatika-shampoo-project 52/64

INTERPRETATION:

From the interpretation of the data, we come to know that Clinic

plus and Clinic allclear are on no.1 and no.2 respectively. Sunsilk,

Head & Shoulders, Pantene are ranked after them. Basically HUL &

P&G are very good in keeping their market share by responding

quickly to other competitor schemes.

Dabur Vatika is ranked at no.6 followed by Dove & Garnier Fructis

shampoo.

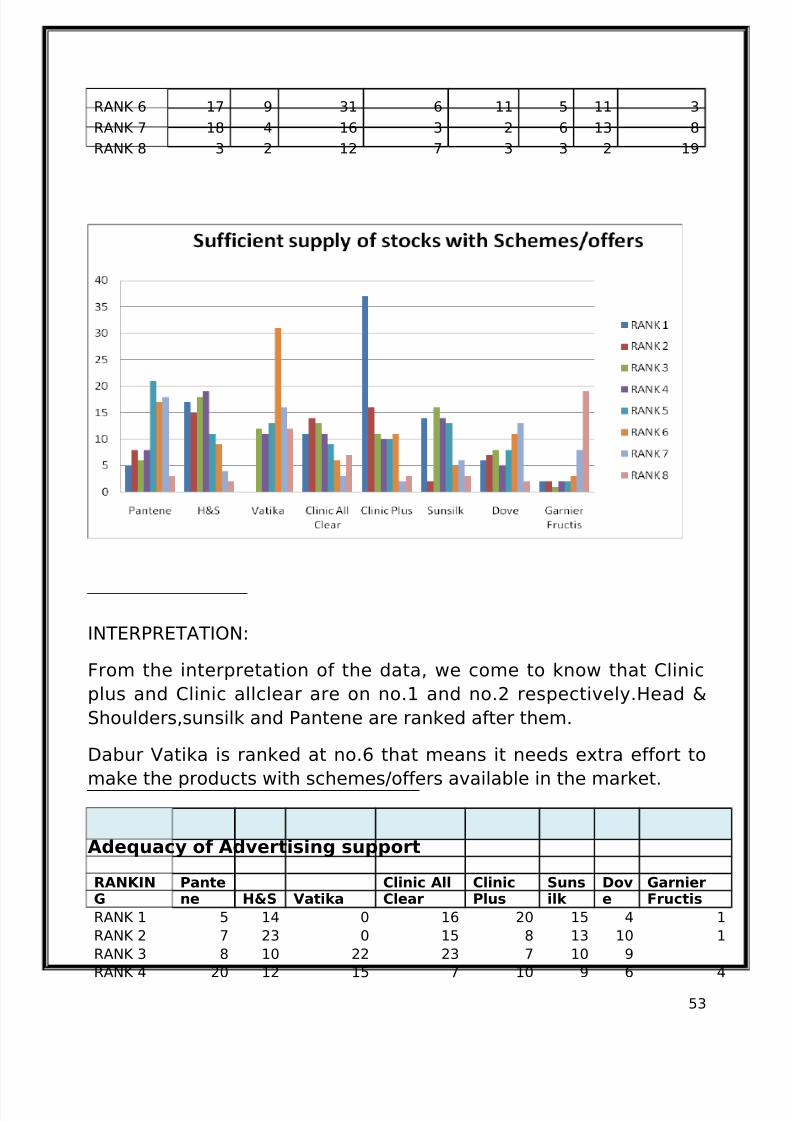

Sufficient supply of stocks with Schemes/offers

RANKING

Pantene H&S Vatika

Clinic AllClear

ClinicPlus

Sunsilk

Dove

GarnierFructis

RANK 1 5 17 0 11 37 14 6 2

RANK 2 8 15 0 14 16 2 7 2

RANK 3 6 18 12 13 11 16 8 1

RANK 4 8 19 11 11 10 14 5 2

RANK 5 21 11 13 9 10 13 8 2

52

7/27/2019 Vatika Shampoo Project

http://slidepdf.com/reader/full/vatika-shampoo-project 53/64

RANK 6 17 9 31 6 11 5 11 3

RANK 7 18 4 16 3 2 6 13 8

RANK 8 3 2 12 7 3 3 2 19

INTERPRETATION:

From the interpretation of the data, we come to know that Clinic

plus and Clinic allclear are on no.1 and no.2 respectively.Head &

Shoulders,sunsilk and Pantene are ranked after them.

Dabur Vatika is ranked at no.6 that means it needs extra effort tomake the products with schemes/offers available in the market.

Adequacy of Advertising support

RANKING

Pantene H&S Vatika

Clinic AllClear

ClinicPlus

Sunsilk

Dove

GarnierFructis

RANK 1 5 14 0 16 20 15 4 1

RANK 2 7 23 0 15 8 13 10 1

RANK 3 8 10 22 23 7 10 9RANK 4 20 12 15 7 10 9 6 4

53

7/27/2019 Vatika Shampoo Project

http://slidepdf.com/reader/full/vatika-shampoo-project 54/64

RANK 5 16 20 18 10 7 5 15 1

RANK 6 15 10 21 11 6 11 5 11

RANK 7 18 0 14 1 15 5 9 29

RANK 8 5 0 4 0 20 7 5 34

INTERPRETATION:

When it comes to advertising Clinic plus and Head & Shoulders are

no.1 and no.2 respectively. Clinic all clear is no.3 followed by

Pantene, sunsilk and Dabur are on no.6 after that Garnier fructis

and Dove ranked at 7 and 8 respectively.

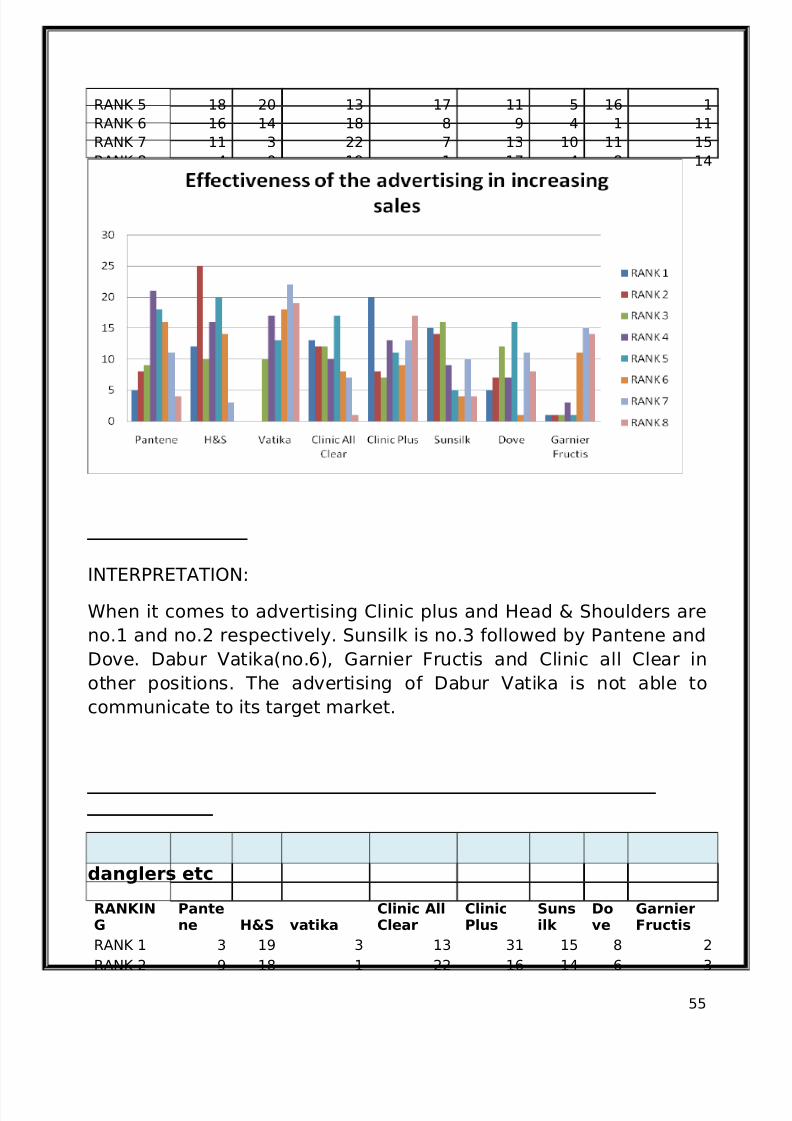

Effectiveness of the advertising in increasing sales

RANKING

Pantene H&S Vatika

Clinic AllClear

ClinicPlus

Sunsilk

Dove

GarnierFructis

RANK 1 5 12 0 13 20 15 5 1

RANK 2 8 25 0 12 8 14 7 1

RANK 3 9 10 10 12 7 16 12 1

RANK 4 21 16 17 10 13 9 7 3

54

7/27/2019 Vatika Shampoo Project

http://slidepdf.com/reader/full/vatika-shampoo-project 55/64

RANK 5 18 20 13 17 11 5 16 1

RANK 6 16 14 18 8 9 4 1 11

RANK 7 11 3 22 7 13 10 11 15

RANK 8 4 0 19 1 17 4 8 14

INTERPRETATION:

When it comes to advertising Clinic plus and Head & Shoulders are

no.1 and no.2 respectively. Sunsilk is no.3 followed by Pantene and

Dove. Dabur Vatika(no.6), Garnier Fructis and Clinic all Clear in

other positions. The advertising of Dabur Vatika is not able to

communicate to its target market.

Adequacy of shop-based material like posters, stickers,

danglers etc

RANKING

Pantene H&S vatika

Clinic AllClear

ClinicPlus

Sunsilk

Dove

GarnierFructis

RANK 1 3 19 3 13 31 15 8 2RANK 2 9 18 1 22 16 14 6 3

55

7/27/2019 Vatika Shampoo Project

http://slidepdf.com/reader/full/vatika-shampoo-project 56/64

RANK 3 4 17 7 21 11 11 12 2

RANK 4 13 16 9 7 8 13 13 6

RANK 5 21 13 10 14 11 11 8 3

RANK 6 17 6 38 5 7 5 12 6

RANK 7 19 5 16 2 12 9 10 11RANK 8 9 4 7 4 7 1 5 20

INTERPRETATION:

From the interpretation of the data, we come to know that Clinic

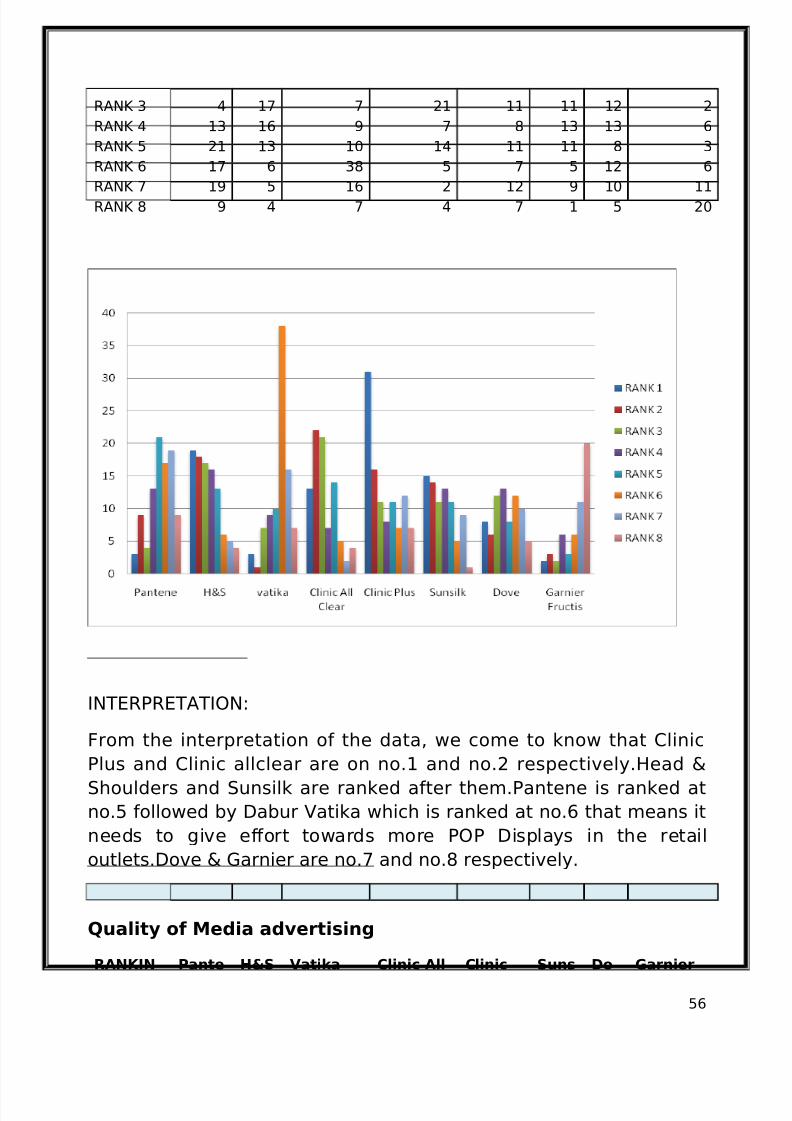

Plus and Clinic allclear are on no.1 and no.2 respectively.Head &Shoulders and Sunsilk are ranked after them.Pantene is ranked at

no.5 followed by Dabur Vatika which is ranked at no.6 that means it

needs to give effort towards more POP Displays in the retail

outlets.Dove & Garnier are no.7 and no.8 respectively.

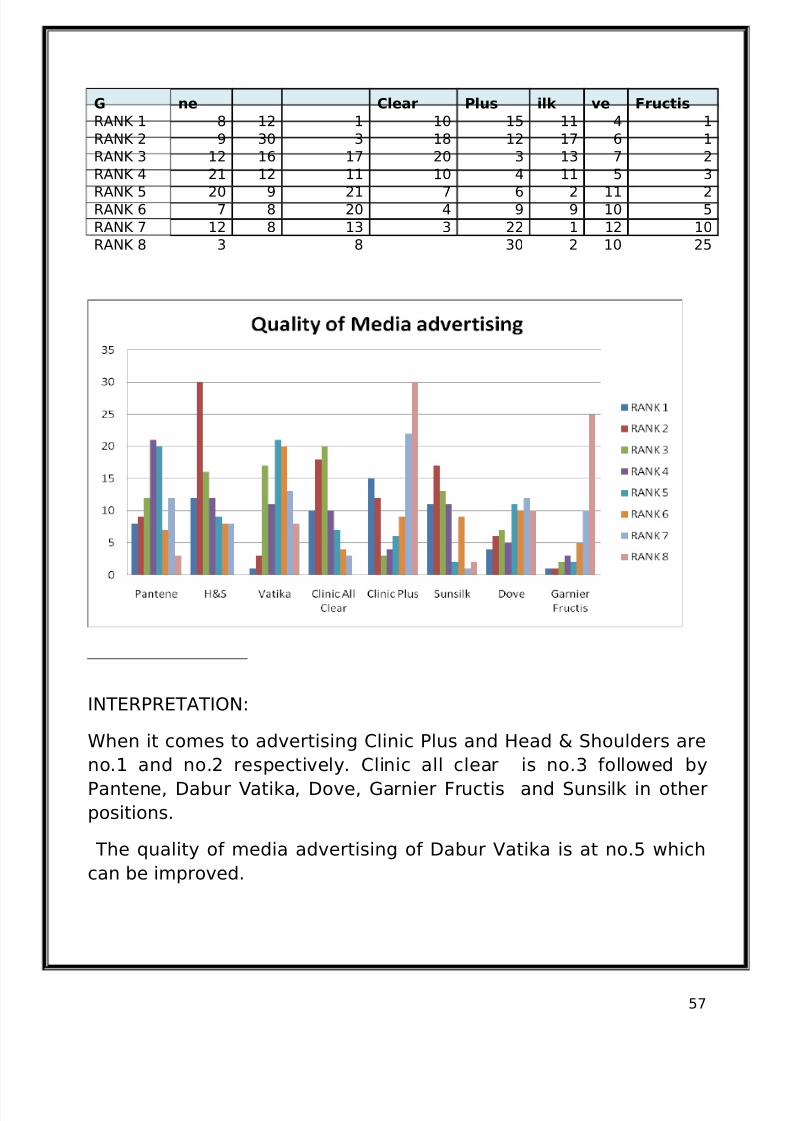

Quality of Media advertising

RANKIN Pante H&S Vatika Clinic All Clinic Suns Do Garnier

56

7/27/2019 Vatika Shampoo Project

http://slidepdf.com/reader/full/vatika-shampoo-project 57/64

G ne Clear Plus ilk ve Fructis

RANK 1 8 12 1 10 15 11 4 1

RANK 2 9 30 3 18 12 17 6 1

RANK 3 12 16 17 20 3 13 7 2

RANK 4 21 12 11 10 4 11 5 3

RANK 5 20 9 21 7 6 2 11 2RANK 6 7 8 20 4 9 9 10 5

RANK 7 12 8 13 3 22 1 12 10

RANK 8 3 8 30 2 10 25

INTERPRETATION:

When it comes to advertising Clinic Plus and Head & Shoulders are

no.1 and no.2 respectively. Clinic all clear is no.3 followed byPantene, Dabur Vatika, Dove, Garnier Fructis and Sunsilk in other

positions.

The quality of media advertising of Dabur Vatika is at no.5 which

can be improved.

57

7/27/2019 Vatika Shampoo Project

http://slidepdf.com/reader/full/vatika-shampoo-project 58/64

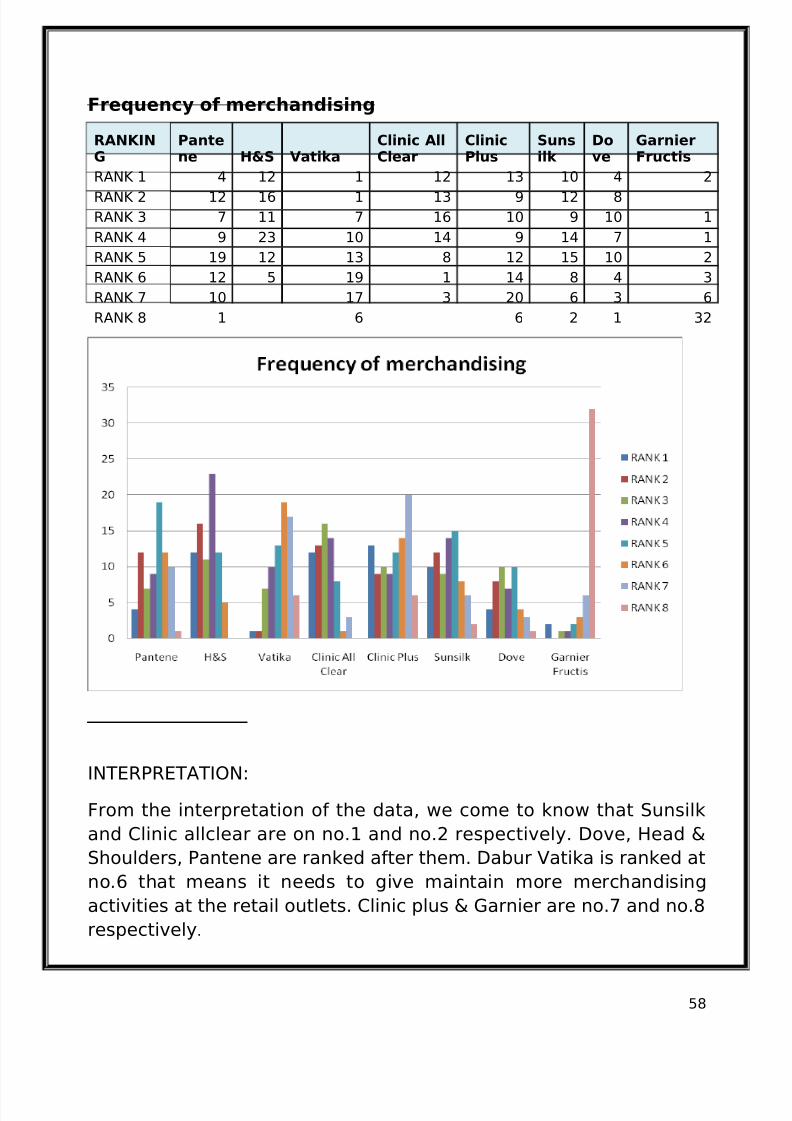

Frequency of merchandising

RANKING

Pantene H&S Vatika

Clinic AllClear

ClinicPlus

Sunsilk

Dove

GarnierFructis

RANK 1 4 12 1 12 13 10 4 2

RANK 2 12 16 1 13 9 12 8

RANK 3 7 11 7 16 10 9 10 1

RANK 4 9 23 10 14 9 14 7 1

RANK 5 19 12 13 8 12 15 10 2

RANK 6 12 5 19 1 14 8 4 3

RANK 7 10 17 3 20 6 3 6

RANK 8 1 6 6 2 1 32

INTERPRETATION:

From the interpretation of the data, we come to know that Sunsilk

and Clinic allclear are on no.1 and no.2 respectively. Dove, Head &

Shoulders, Pantene are ranked after them. Dabur Vatika is ranked at

no.6 that means it needs to give maintain more merchandising

activities at the retail outlets. Clinic plus & Garnier are no.7 and no.8

respectively.

58

7/27/2019 Vatika Shampoo Project

http://slidepdf.com/reader/full/vatika-shampoo-project 59/64

Quality of merchandising

RANKING

Pantene H&S Vatika

Clinic AllClear

ClinicPlus

Sunsilk

Dove

GarnierFructis

RANK 1 2 10 1 15 18 15 4 2

RANK 2 10 15 1 11 4 13 8

RANK 3 11 8 4 14 8 10 10 1

RANK 4 8 7 7 6 6 11 7 1

RANK 5 12 10 12 4 7 9 2

RANK 6 12 5 20 2 13 8 6 4

RANK 7 10 6 18 3 15 8 11 9

RANK 8 1 8 15 6 2 1 25

INTERPRETATION:

From the interpretation of the data, we come to know that Clinic

Plus and H&S are on no.1 and no.2 respectively.Clinic all clear ,

sunsilk, Pantene are ranked after them. Dabur Vatika is ranked at

no.7 that means it needs to provide high quality merchandising at

59

7/27/2019 Vatika Shampoo Project

http://slidepdf.com/reader/full/vatika-shampoo-project 60/64

par with its other competitors at the retail outlets.Garnier is at no.8

respectively.

FINDINGs• During the survey it was found that the availability of Dabur

Vatika shampoo (in lari) was less as compared to other

competitor brands.

• The visibility of Dabur Vatika shampoo (in lari) was also not

good in most of the retail outlets.

• All the variants Dabur Vatika Shampoo (sachets) are not

properly merchandised.

• The retailers not satisfied with the credit system. They want

more credit days for the payment.

• We found that in some of the retail outlet which are located in

the interior don’t get the adequate and frequent supply of the

Dabur product.

• The profit margin on Dabur Vatika shampoo (sachets) is less as

compared to other competitor brands.

• The frequency of consumer sales promotion and retailer sales

promotions is not upto the mark.

60

7/27/2019 Vatika Shampoo Project

http://slidepdf.com/reader/full/vatika-shampoo-project 61/64

• The retailers are not satisfied with the damage settlement of

Dabur Vatika shampoo done by the stockiest.

• The retailers responded negatively when it came to marketing

and promotional activities of Dabur Vatika shampoo withrespect to other competitor brands.

• In some of the store we found that retailers are complaining

about the behavior of the sales person as they are saying thatthey will supply the Dabur products only when if the purchase

more than 5000 at a time.

• There are 10 outlets are covered indirectly through

wholrsalers.

• There are 10 outlets using self managed transportation to get

their required products from the nearer market.

RECOMMENDATIONS

• The availability and visibility of a product should be

emphasized.

• Better distribution channel should be maintained.

• Company should introduce sales promotion schemes like free

weight, contest, free gifts trials, offers etc and consider more

below the line promotion for Bhubaneswar.

• A proper feedback mechanism should be established so that

feedback from consumer & retailers should be taken and

implemented.

61

7/27/2019 Vatika Shampoo Project

http://slidepdf.com/reader/full/vatika-shampoo-project 62/64

• There should be incentives for merchandisers for every display

they enroll.

• Selection of skilled and trained salesman affects the sales.

• Right on time concept is very important in the FMCG Industry

because in the absence of it retailers purchase other companyproducts.

• Frequency of advertisement should be increased to make the

consumer familiar to products.

• Promote Vatika anti-dandruff variants- so that it will compete

with the Head & shoulder and Cilinic all Clear.

• Consumers have strong perception and belief about the

Ayurvedic nature of the Dabur, so that company should comewith the Ayurvedic concept Shampoo to harness that segmentof the consumer.

CONCLUSION

In the era of the tough competition in FMCG market. The major sales and distribution make

the product available and visible in the marketing effective coverage play a vital role for

sustain or make the product growing.

62

7/27/2019 Vatika Shampoo Project

http://slidepdf.com/reader/full/vatika-shampoo-project 63/64

So, in my project as Dabur is already having a very good distribution network in the market.

It should focus on new strategies product like Vatika . Vatika goal can be achieved

efficiently and effectively distribution system.

BIBLIOGRAPHY

Websites

• www.google.com

• www.dabur.com

63

7/27/2019 Vatika Shampoo Project

http://slidepdf.com/reader/full/vatika-shampoo-project 64/64

• www.business-standard.com

• www.wikipedia.com

• www.marketresearch.com

• www.timesofindia.com

Books referred to;