VAT from External Auditor’s Perspective€” VAT Logic Test (Recalculation) — ... PowerPoint...

24

© 2017 KPMG Lower Gulf Limited and KPMG LLP, operating in the UAE, member firms of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 1 VAT from External Auditor’s Perspective November 2017

Transcript of VAT from External Auditor’s Perspective€” VAT Logic Test (Recalculation) — ... PowerPoint...

© 2017 KPMG Lower Gulf Limited and KPMG LLP, operating in the UAE, member firms of the KPMG network of independent member firms affiliated with KPMG

International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 1

VAT from External Auditor’s PerspectiveNovember 2017

© 2017 KPMG Lower Gulf Limited and KPMG LLP, operating in the UAE, member firms of the KPMG network of independent member firms affiliated with KPMG

International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 2

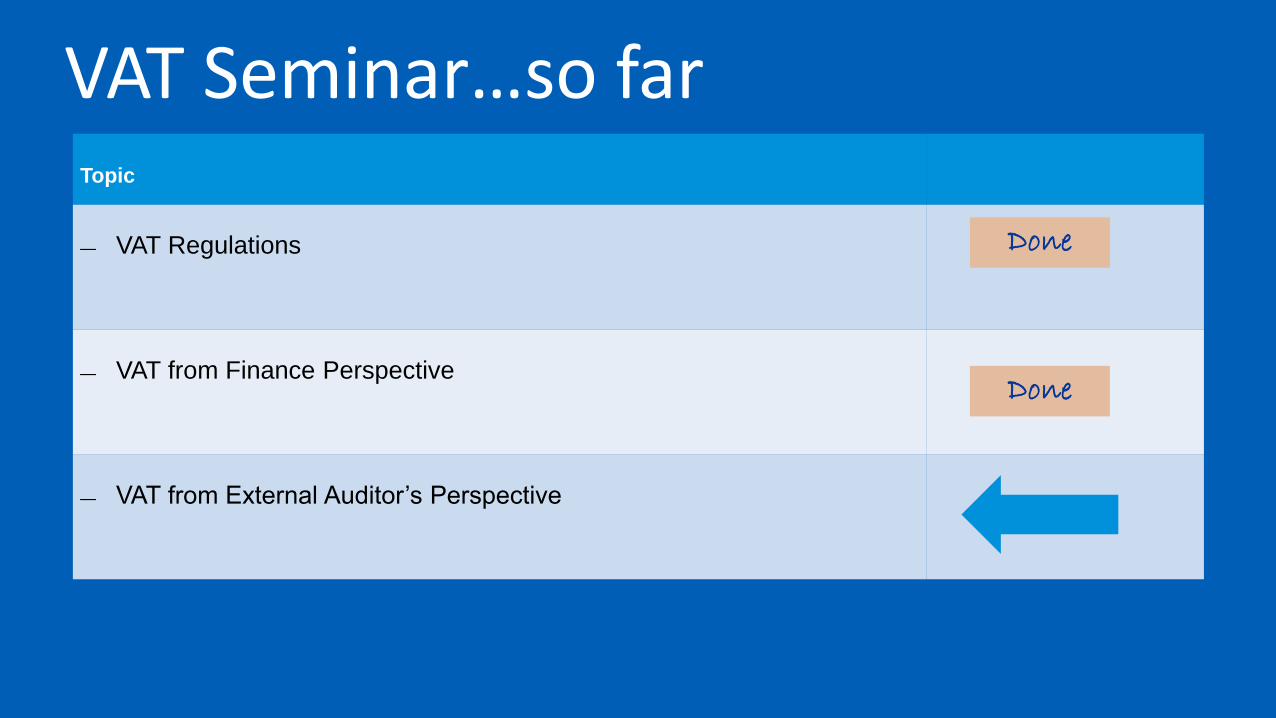

VAT Seminar…so farTopic

— VAT Regulations

— VAT from Finance Perspective

— VAT from External Auditor’s Perspective

Done

Done

© 2017 KPMG Lower Gulf Limited and KPMG LLP, operating in the UAE, member firms of the KPMG network of independent member firms affiliated with KPMG

International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 3

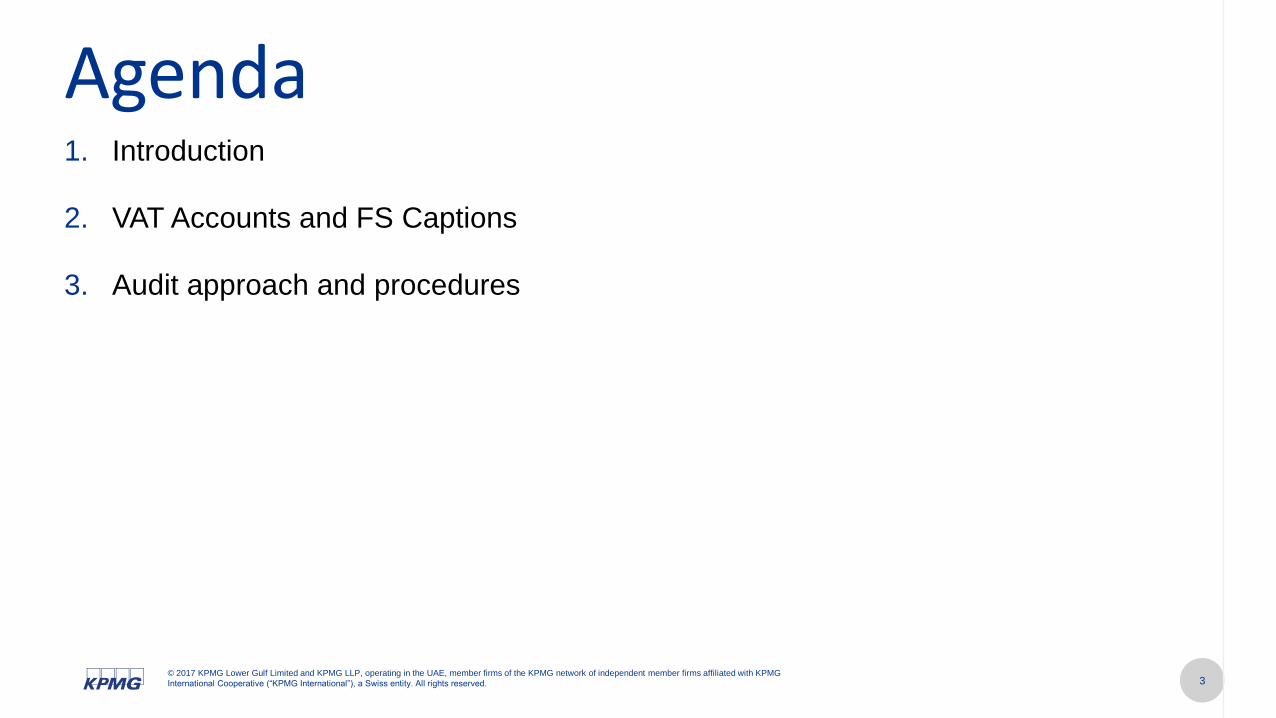

1. Introduction

2. VAT Accounts and FS Captions

3. Audit approach and procedures

Agenda

© 2017 KPMG Lower Gulf Limited and KPMG LLP, operating in the UAE, member firms of the KPMG network of independent member firms affiliated with KPMG

International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 4

4

Quiz - Audit

What does an auditor say when boarding a train?

Mind the GAAP…

© 2017 KPMG Lower Gulf Limited and KPMG LLP, operating in the UAE, member firms of the KPMG network of independent member firms affiliated with KPMG

International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 5

5

Quiz - Audit

How many auditors does it take to change a light

bulb?

How many did it take last year?

© 2017 KPMG Lower Gulf Limited and KPMG LLP, operating in the UAE, member firms of the KPMG network of independent member firms affiliated with KPMG

International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 6

6

Quiz - Audit

What does an auditor's wife ask her husband when

she can't get to sleep?

"Tell me about your day, dear."

VAT accounts and FS Captions

© 2017 KPMG Lower Gulf Limited and KPMG LLP, operating in the UAE, member firms of the KPMG network of independent member firms affiliated with KPMG

International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 8

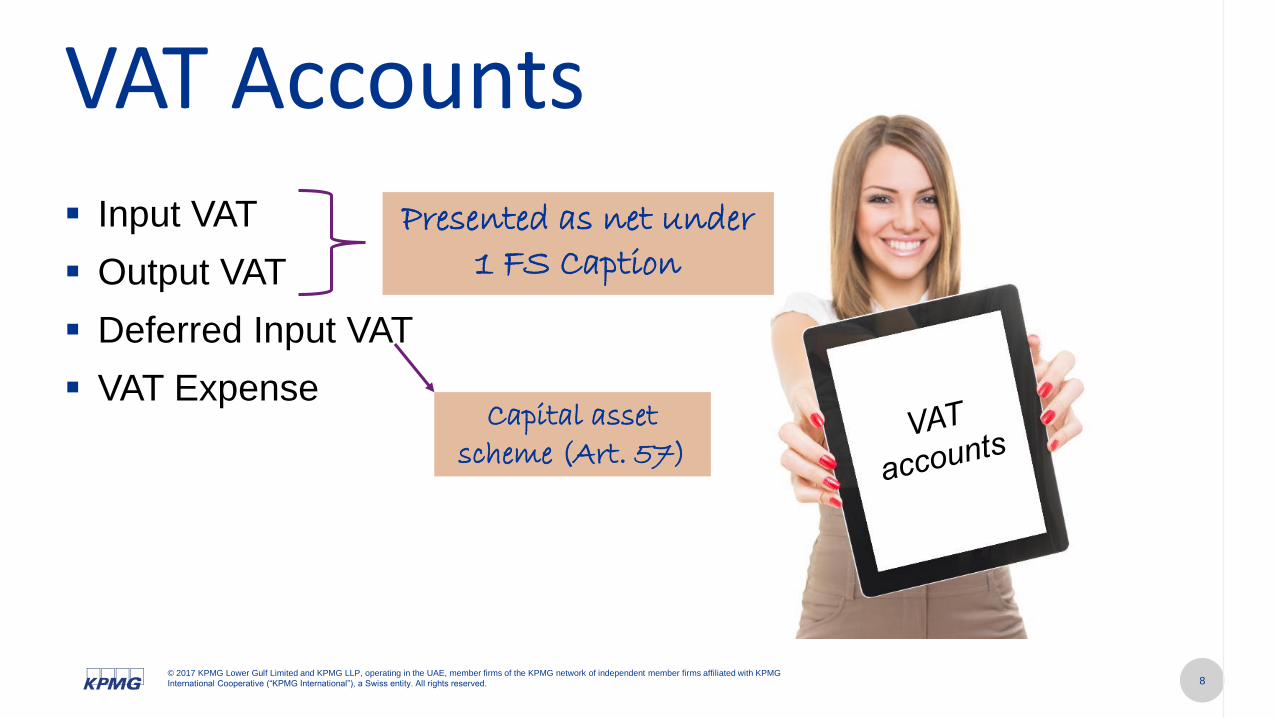

VAT Accounts▪ Input VAT

▪ Output VAT

▪ Deferred Input VAT

▪ VAT Expense

Presented as net under 1 FS Caption

Capital asset scheme (Art. 57)

© 2017 KPMG Lower Gulf Limited and KPMG LLP, operating in the UAE, member firms of the KPMG network of independent member firms affiliated with KPMG

International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 9

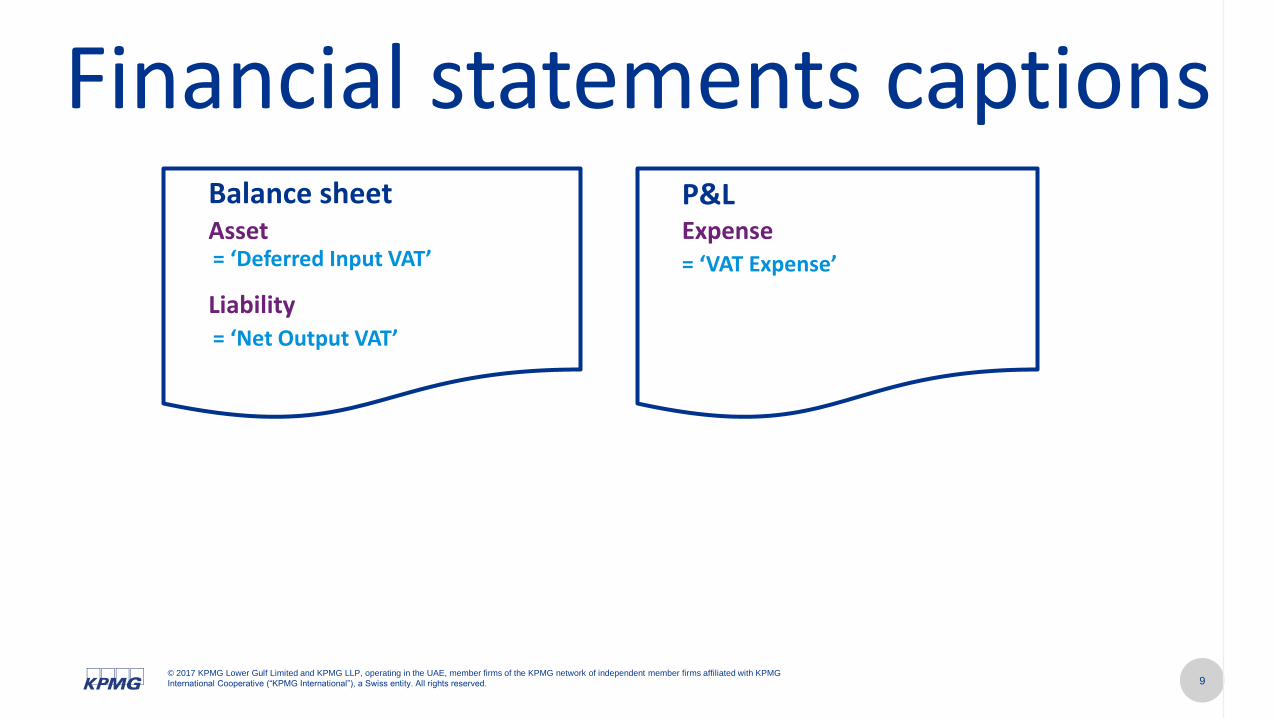

Financial statements captionsBalance sheet P&LAsset

Liability

= ‘Deferred Input VAT’

= ‘Net Output VAT’

Expense= ‘VAT Expense’

Audit Approach and Procedures

© 2017 KPMG Lower Gulf Limited and KPMG LLP, operating in the UAE, member firms of the KPMG network of independent member firms affiliated with KPMG

International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 11

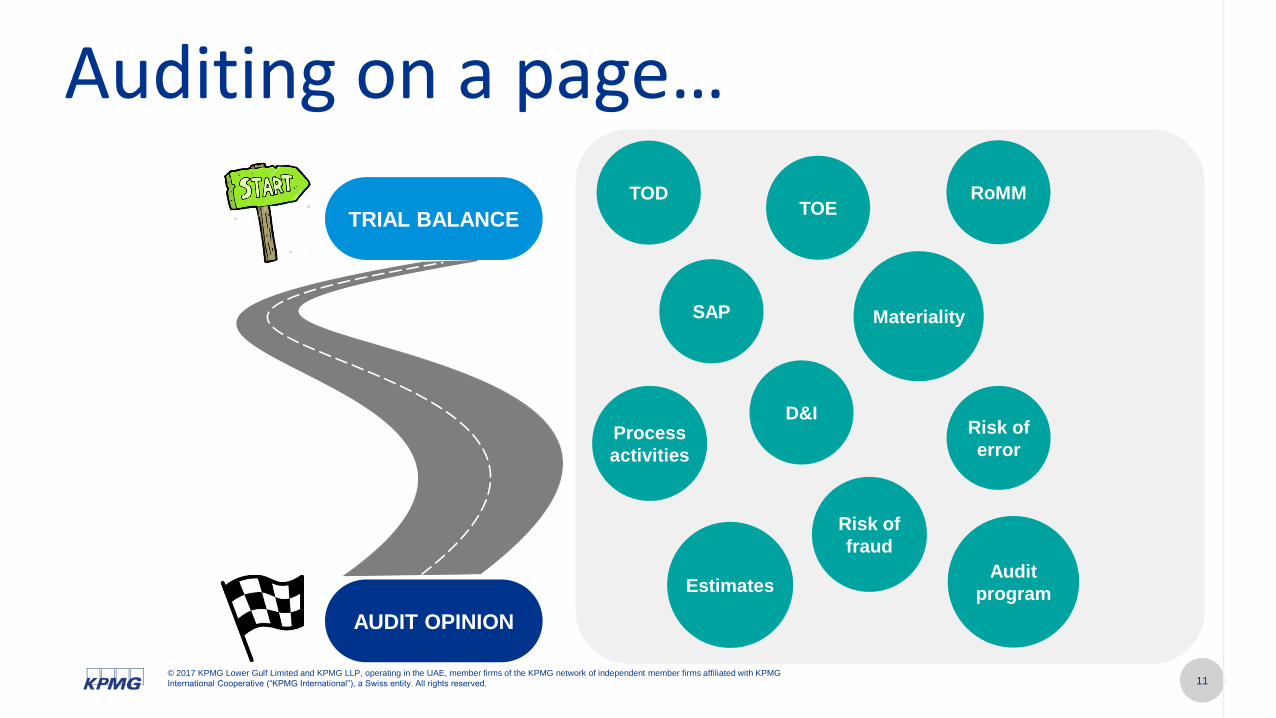

Auditing on a page…

TRIAL BALANCE

AUDIT OPINION

TODTOE

RoMM

MaterialitySAP

D&IRisk of

errorProcess

activities

Risk of

fraud

Audit

programEstimates

© 2017 KPMG Lower Gulf Limited and KPMG LLP, operating in the UAE, member firms of the KPMG network of independent member firms affiliated with KPMG

International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 12

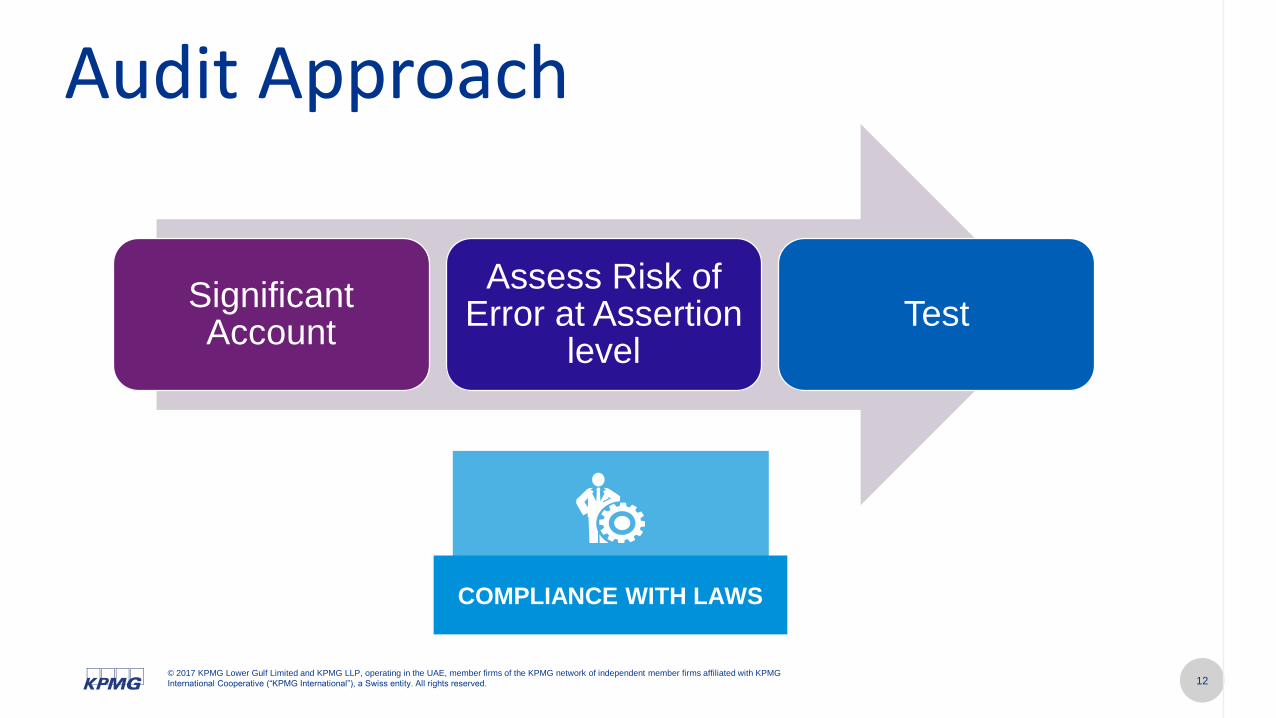

Audit Approach

COMPLIANCE WITH LAWS

Significant Account

Assess Risk of Error at Assertion

level Test

© 2017 KPMG Lower Gulf Limited and KPMG LLP, operating in the UAE, member firms of the KPMG network of independent member firms affiliated with KPMG

International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 13

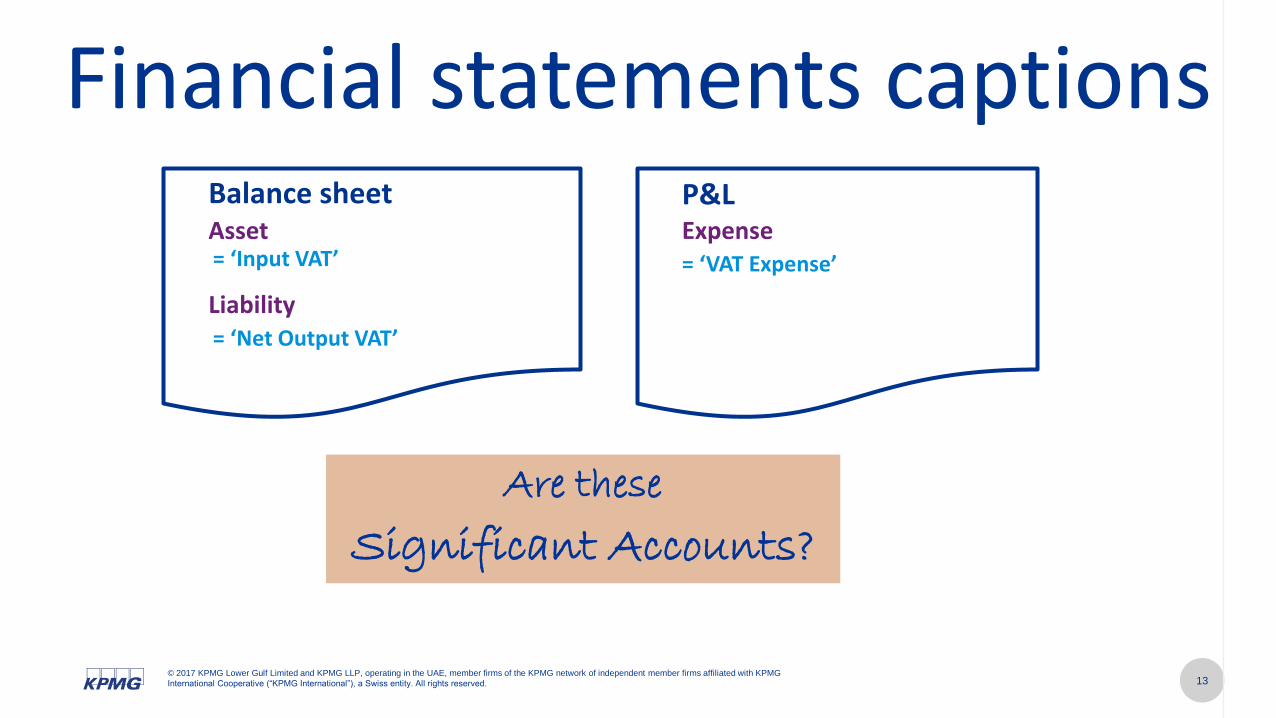

Financial statements captionsBalance sheet P&LAsset

Liability

= ‘Input VAT’

= ‘Net Output VAT’

Are these

Significant Accounts?

Expense= ‘VAT Expense’

© 2017 KPMG Lower Gulf Limited and KPMG LLP, operating in the UAE, member firms of the KPMG network of independent member firms affiliated with KPMG

International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 14

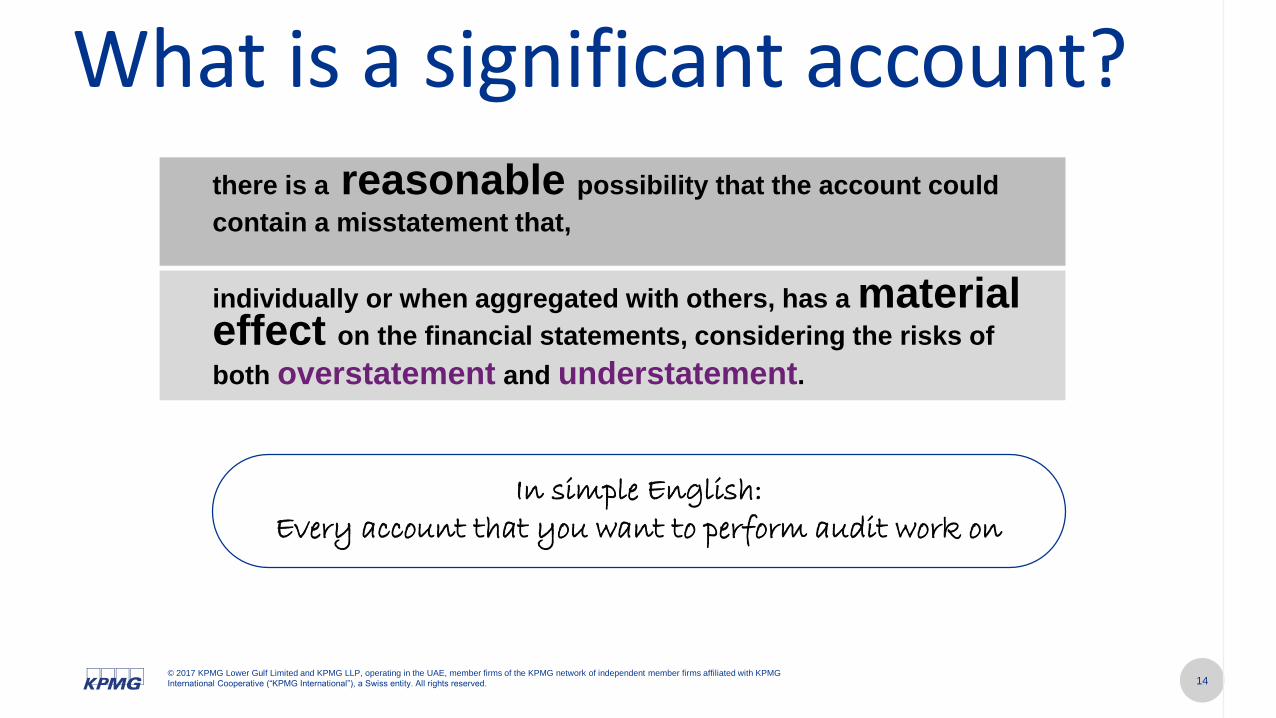

What is a significant account?

In simple English: Every account that you want to perform audit work on

there is a reasonable possibility that the account could

contain a misstatement that,

individually or when aggregated with others, has a material effect on the financial statements, considering the risks of

both overstatement and understatement.

© 2017 KPMG Lower Gulf Limited and KPMG LLP, operating in the UAE, member firms of the KPMG network of independent member firms affiliated with KPMG

International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 15

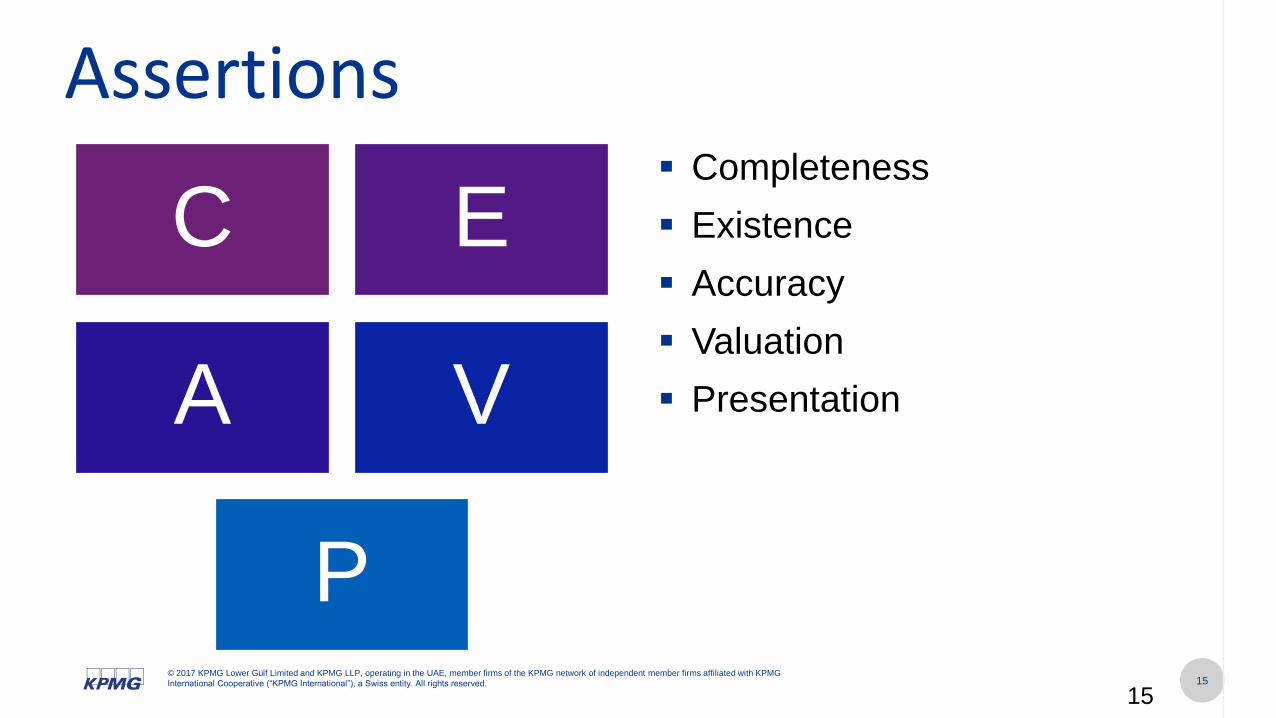

C E

A V

P

▪ Completeness

▪ Existence

▪ Accuracy

▪ Valuation

▪ Presentation

15

Assertions

© 2017 KPMG Lower Gulf Limited and KPMG LLP, operating in the UAE, member firms of the KPMG network of independent member firms affiliated with KPMG

International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 16

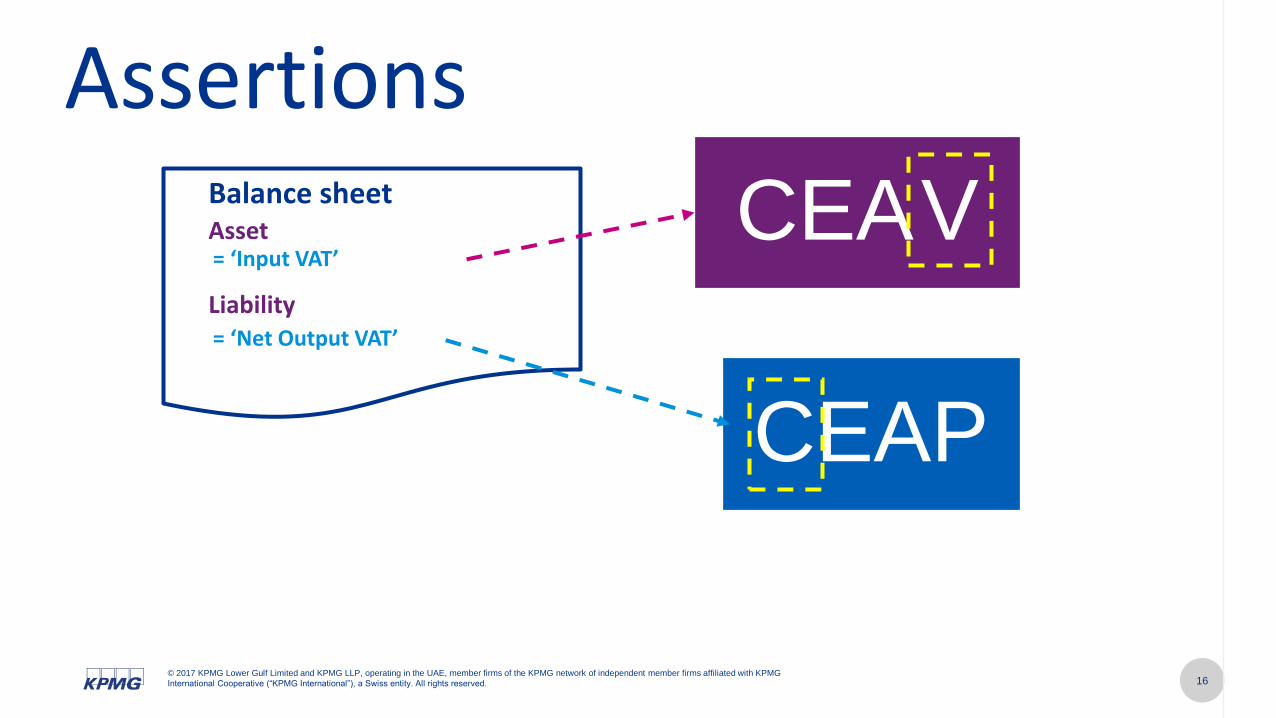

AssertionsBalance sheetAsset

Liability

= ‘Input VAT’

= ‘Net Output VAT’

CEAV

CEAP

© 2017 KPMG Lower Gulf Limited and KPMG LLP, operating in the UAE, member firms of the KPMG network of independent member firms affiliated with KPMG

International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 17

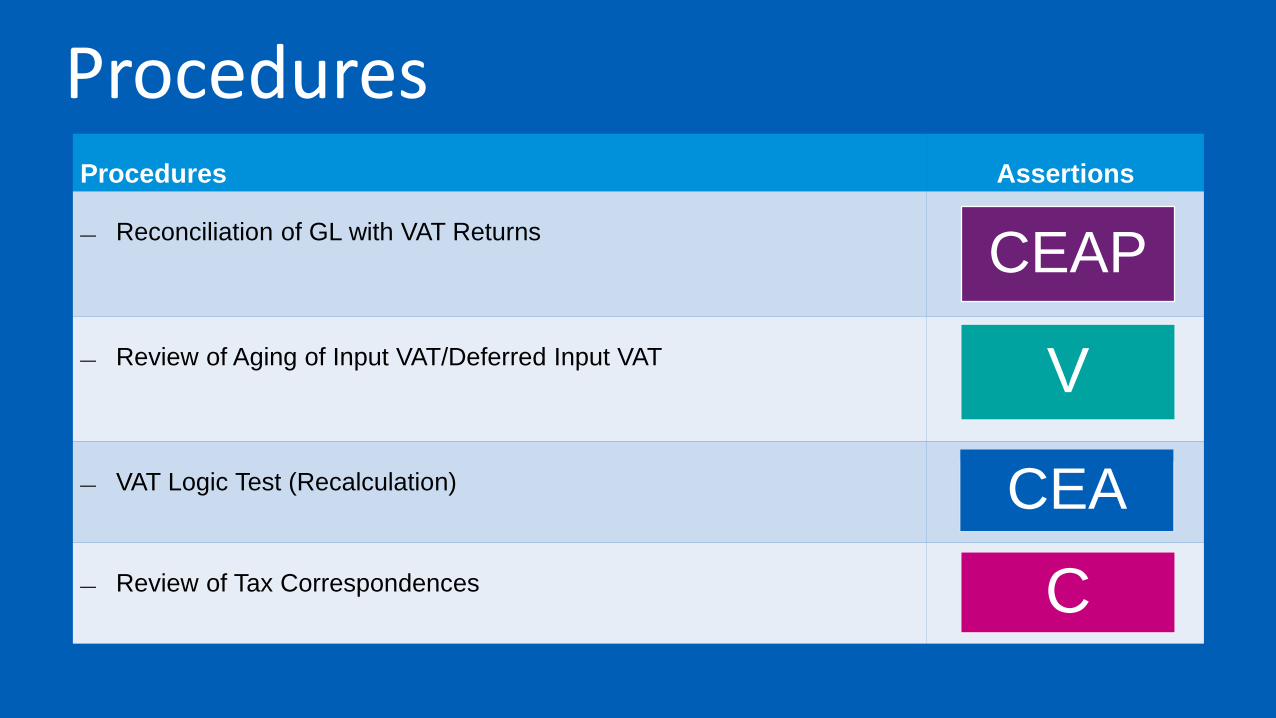

ProceduresProcedures Assertions

— Reconciliation of GL with VAT Returns

— Review of Aging of Input VAT/Deferred Input VAT

— VAT Logic Test (Recalculation)

— Review of Tax Correspondences

CEAP

V

CEA

C

© 2017 KPMG Lower Gulf Limited and KPMG LLP, operating in the UAE, member firms of the KPMG network of independent member firms affiliated with KPMG

International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 18

18

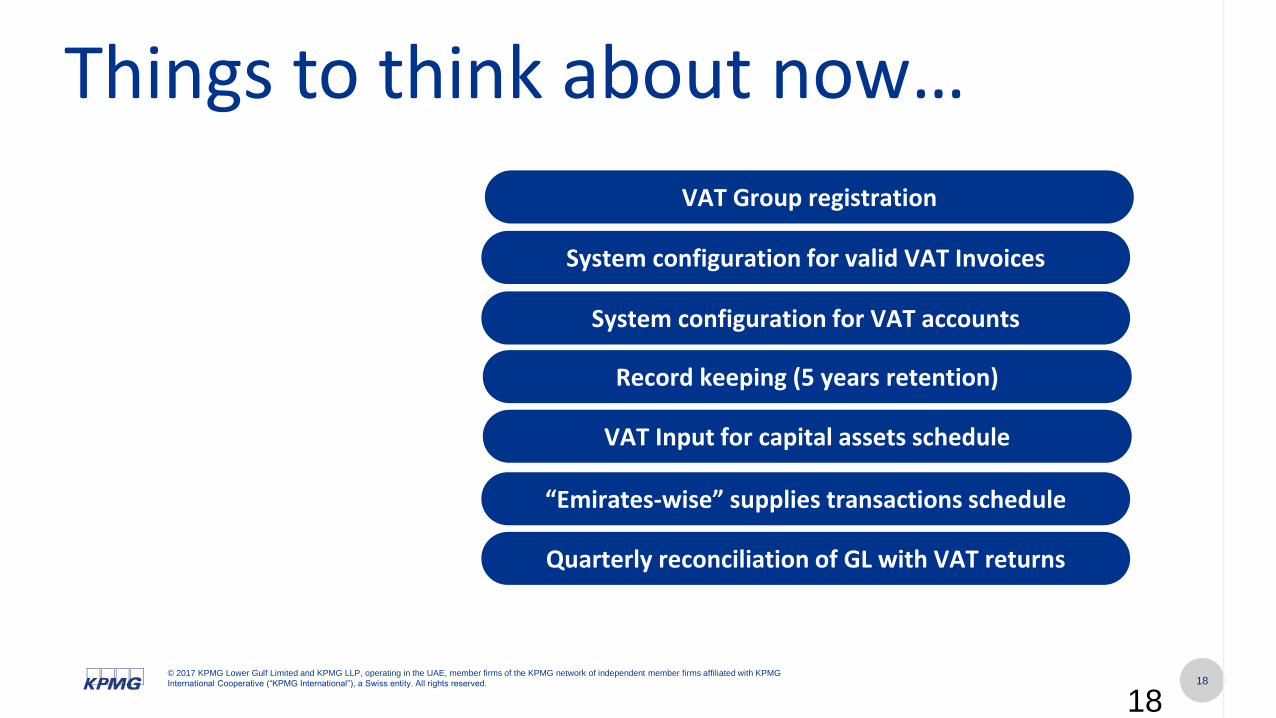

Things to think about now…

System configuration for valid VAT Invoices

System configuration for VAT accounts

“Emirates-wise” supplies transactions schedule

VAT Group registration

Quarterly reconciliation of GL with VAT returns

Record keeping (5 years retention)

VAT Input for capital assets schedule

© 2017 KPMG Lower Gulf Limited and KPMG LLP, operating in the UAE, member firms of the KPMG network of independent member firms affiliated with KPMG

International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 19

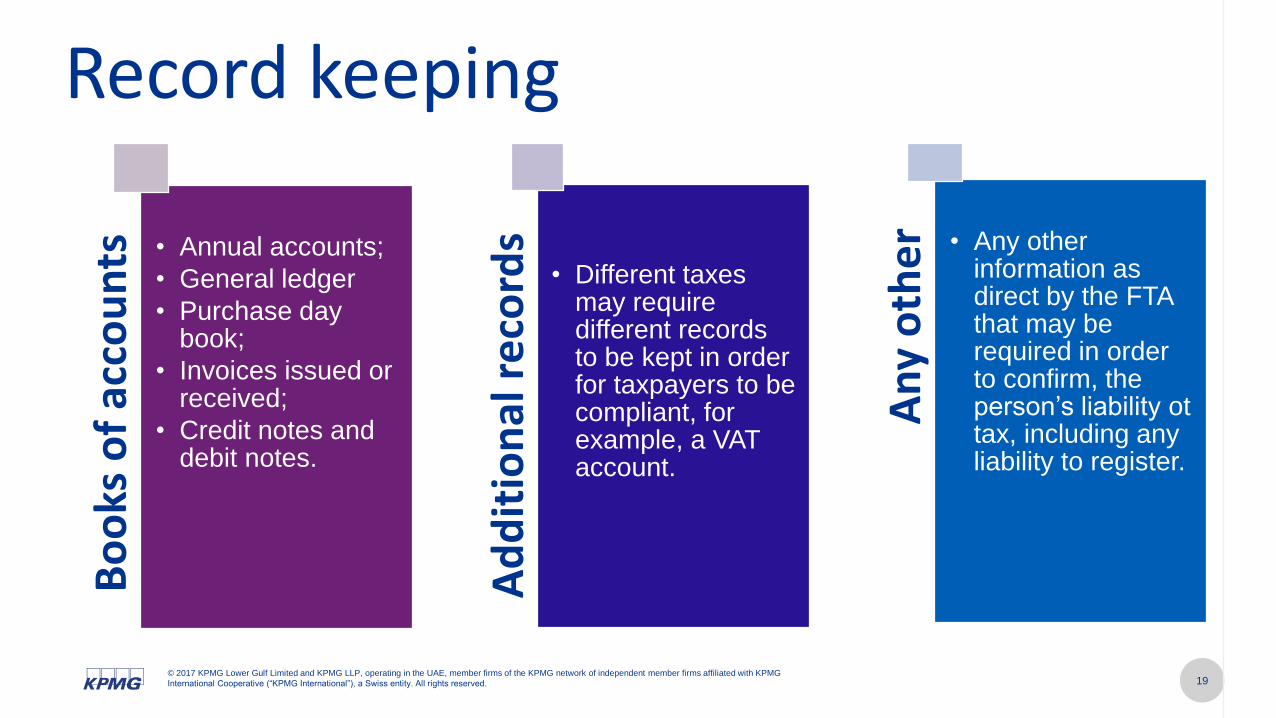

Record keepingB

oo

ks o

f ac

cou

nts • Annual accounts;

• General ledger

• Purchase day book;

• Invoices issued or received;

• Credit notes and debit notes.

Ad

dit

ion

al r

eco

rds

• Different taxes may require different records to be kept in order for taxpayers to be compliant, for example, a VAT account.

An

y o

the

r in

form

atio

n• Any other information as direct by the FTA that may be required in order to confirm, the person’s liability ottax, including any liability to register.

Next steps

© 2017 KPMG Lower Gulf Limited and KPMG LLP, operating in the UAE, member firms of the KPMG network of independent member firms affiliated with KPMG

International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 21

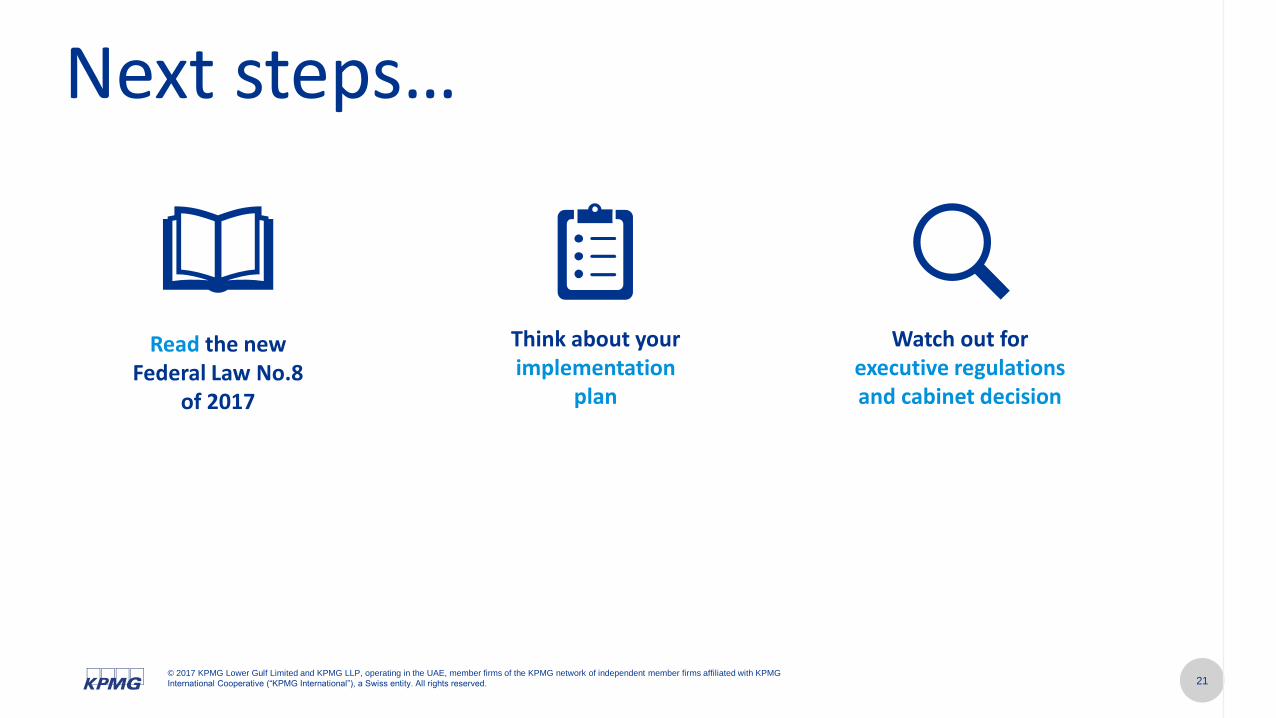

Next steps…

Read the new Federal Law No.8

of 2017

Think about your implementation

plan

Watch out for executive regulations and cabinet decision

© 2017 KPMG Lower Gulf Limited and KPMG LLP, operating in the UAE, member firms of the KPMG network of independent member firms affiliated with KPMG

International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 22

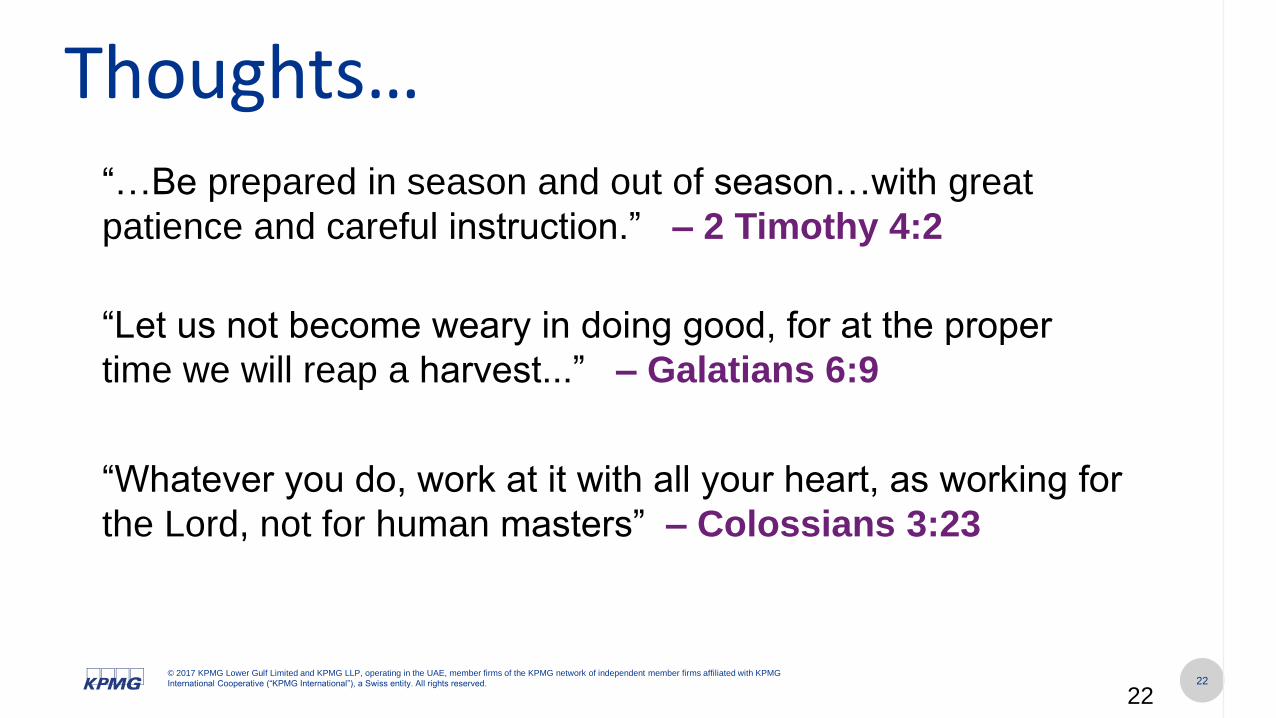

“…Be prepared in season and out of season…with great

patience and careful instruction.” – 2 Timothy 4:2

22

Thoughts…

“Let us not become weary in doing good, for at the proper

time we will reap a harvest...” – Galatians 6:9

“Whatever you do, work at it with all your heart, as working for

the Lord, not for human masters” – Colossians 3:23

What questions do you have?

Thank you

© 2017 KPMG International Cooperative (“KPMG International”), a Swiss entity.

Member firms of the KPMG network of independent firms are affiliated with

KPMG International. KPMG International provides no client services. No member

firm has any authority to obligate or bind KPMG International or any other

member firm vis-à-vis third parties, nor does KPMG International have any such

authority to obligate or bind any member firm. All rights reserved.