Vantage GreenX Presentation to WESSA

20

Vantage GreenX Presentation to WESSA April 2014

-

Upload

wind-energy-update -

Category

Engineering

-

view

23 -

download

2

Transcript of Vantage GreenX Presentation to WESSA

Vantage GreenX Presentation to WESSA April 2014

2

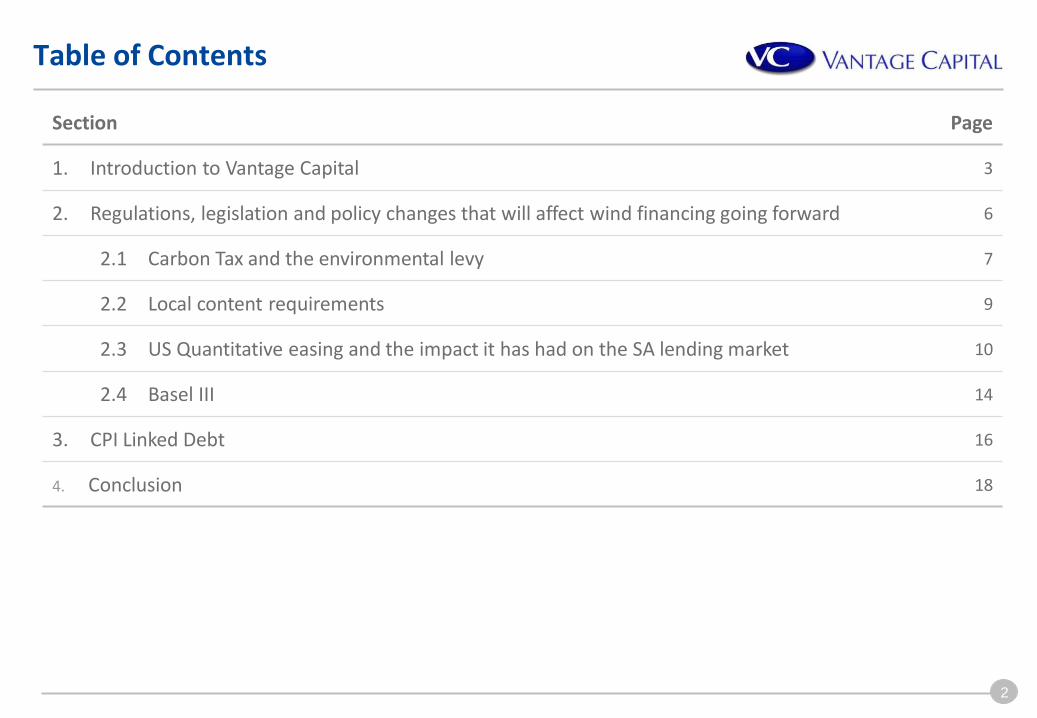

Section Page

1. Introduction to Vantage Capital 3

2. Regulations, legislation and policy changes that will affect wind financing going forward 6

2.1 Carbon Tax and the environmental levy 7

2.2 Local content requirements 9

2.3 US Quantitative easing and the impact it has had on the SA lending market 10

2.4 Basel III 14

3. CPI Linked Debt 16

4. Conclusion 18

Table of Contents

3

1. Introduction to Vantage Capital

4

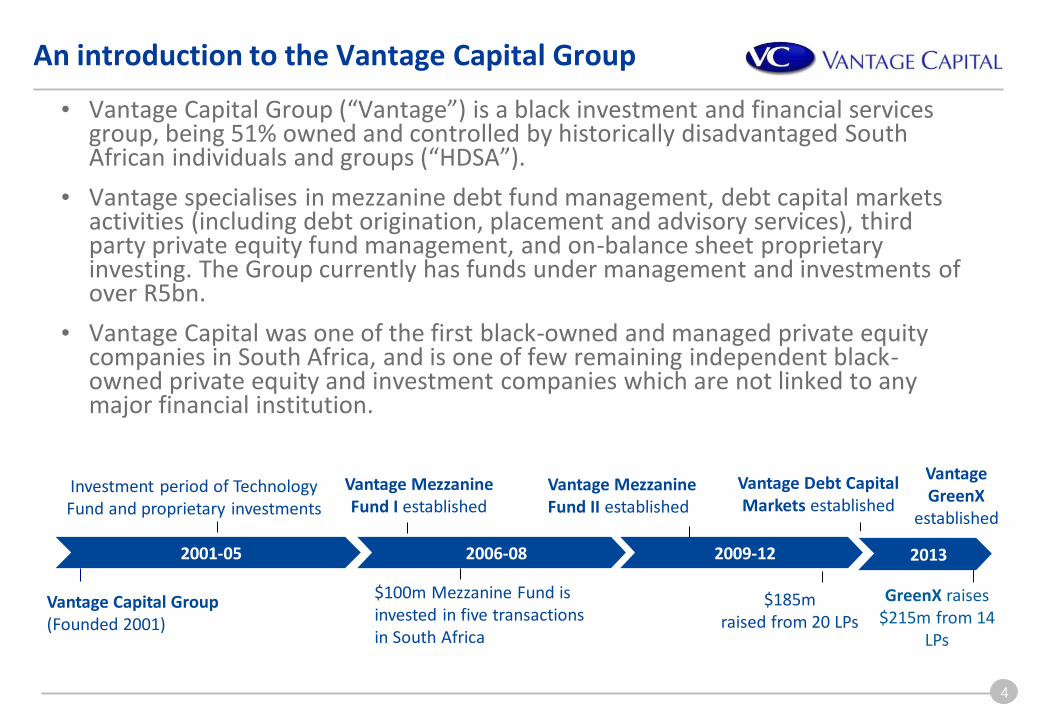

• Vantage Capital Group (“Vantage”) is a black investment and financial services group, being 51% owned and controlled by historically disadvantaged South African individuals and groups (“HDSA”).

• Vantage specialises in mezzanine debt fund management, debt capital markets activities (including debt origination, placement and advisory services), third party private equity fund management, and on-balance sheet proprietary investing. The Group currently has funds under management and investments of over R5bn.

• Vantage Capital was one of the first black-owned and managed private equity companies in South Africa, and is one of few remaining independent black-owned private equity and investment companies which are not linked to any major financial institution.

An introduction to the Vantage Capital Group

Vantage Capital Group (Founded 2001)

Investment period of Technology Fund and proprietary investments

2001-05 2006-08 2009-12

$100m Mezzanine Fund is invested in five transactions in South Africa

Vantage Mezzanine Fund II established

Vantage Mezzanine Fund I established

$185m raised from 20 LPs

Vantage Debt Capital Markets established

2013

Vantage GreenX

established

GreenX raises $215m from 14

LPs

5

GreenX has positioned itself to complement the commercial banking sector.

• It intends to become a preferred distribution channel for banks who would like to sell-down long-term debt into the secondary debt market for sustainable energy projects funded in South Africa.

• It will do this by providing a debt instrument that non-banking financial institutions find attractive, given that it is offering exposure to an asset class that may not ordinarily have been considered.

• This exposure forms part of a carefully selected portfolio that will ensure investors are buying into a balanced spread of risks.

Beyond the inaugural fund, GreenX will also explore additional power and infrastructure opportunities.

• In addition to the REIPPPP(renewable energy IPP procurement program) programme, other countries on the continent are also investing in significant infrastructure programmes of which sustainable energy will constitute a large proportion.

• The Advisor will explore opportunities for investment in such opportunities by providing investors exposure to ex-SA projects and providing additional financing avenues for African projects.

The origins of the Vantage GreenX Debt Fund

6

2. REGULATIONS, LEGISLATION AND POLICY CHANGES THAT WILL AFFECT WIND FINANCING GOING FORWARD

7

• The promulgation of the Carbon Tax (which has now been deferred until 2016) and the environmental levy will have the effect of increasing the cost of new generation that is not environmentally friendly

• From a Renewable Energy Perspective this is good news as it will effectively make new fossil fuel base-load generation more expensive than before

• The attractiveness and ability of renewable energy technologies to compete on an unsubsidised basis becomes all the more compelling.

• The following chart illustrates the possible tariff levels.

2.1. The impact of clean legislation in SA

8

Tariff Comparison BD1-3 vs Eskom & Medupi/Kusile

9

Technology BD 1 Submission BD 2 Submission BD 3 Submission

Thresholds Current Target Current Target Current Target

Onshore Wind 25% 45% 25% 60% 40% 65%

Solar PV 35% 50% 35% 60% 45% 65%

CSP without storage 35% 50% 35% 60% 45% 65%

CSP with storage 25% 45% 25% 60% 40% 65%

Biomass 25% 45% 25% 60% 40% 65%

Biogas 25% 45% 25% 60% 40% 65%

Landfill Gas 25% 45% 25% 60% 40% 65%

Small Hydro 25% 45% 25% 60% 40% 65%

2.2. Briefing Note 8 – Summary

Local content requirements

the local content

requirements get

more onerous as the

IPP Procurement

Process progresses

from BD1 to BD3

Key points

10

Prior to 22 May 2013, US Traders were heavily invested in Emerging Market bonds in their search for yield uplift.

• When Ben Bernanke announced that there would be a tapering of quantitative easing (which is where the Central Bank buys financial assets from commercial banks to increase the monetary base and lower the yield on those assets) it resulted in a large sell-off of local bonds in South Africa by these foreign investors

• This had the effect of:

• Decreasing local SA bond prices (which had the effect of increasing the yields to the buyers),

• Assuming bond yields represent sovereign risk and swap rates represent bank risk, the increase in bond yields had the effect of forcing swap rates up, and

• The subsequent repatriation of all the ZAR proceeds had the effect of devaluing the ZAR

At the time of preparing this presentation (April 2014), it is the view of many of the commercial bank Treasuries that the sell off is now largely complete and there is likely to be a stabilisation in the ZAR at somewhere between 10.50 and 11.50 to the US Dollar

2.3. The Bernanke Effect

11

The impact of US Quantitative Easing

12

• In order to stabilise the currency, earlier this year the South African Reserve Bank announced that it would consider increasing the SARB base or Repo rate which until now has been at a historic low of 5%

Graph of the South African interest rate SARB - long-term graph

Source – www.global-rates.com

The SARB Repo Rate from 2000-2014

13

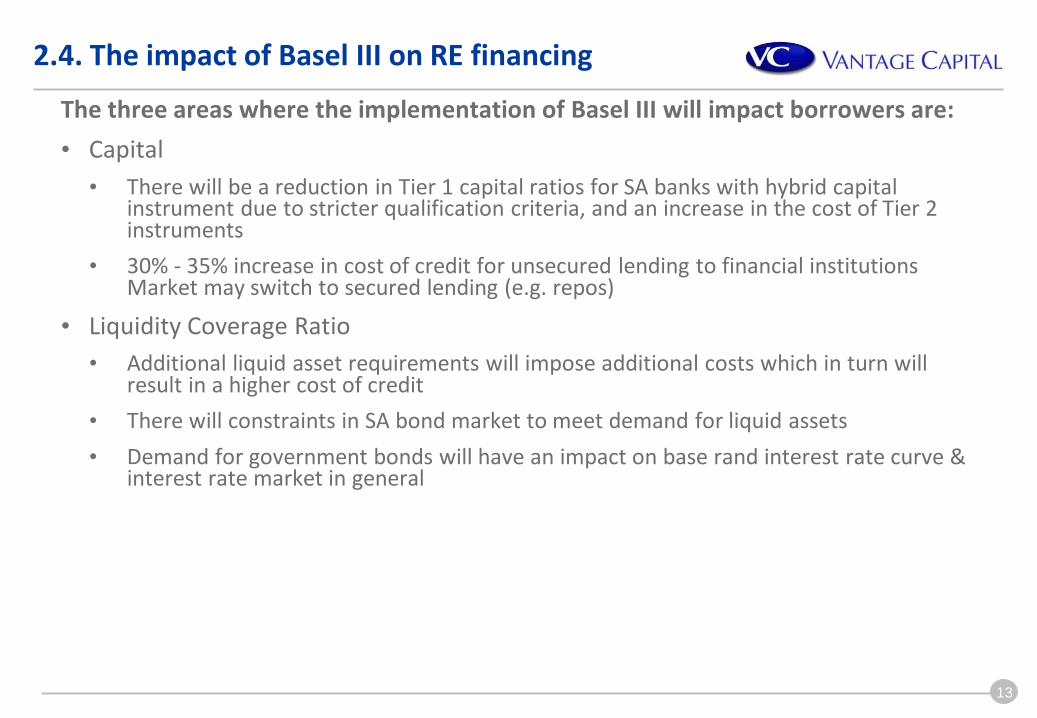

The three areas where the implementation of Basel III will impact borrowers are:

• Capital

• There will be a reduction in Tier 1 capital ratios for SA banks with hybrid capital instrument due to stricter qualification criteria, and an increase in the cost of Tier 2 instruments

• 30% - 35% increase in cost of credit for unsecured lending to financial institutions Market may switch to secured lending (e.g. repos)

• Liquidity Coverage Ratio

• Additional liquid asset requirements will impose additional costs which in turn will result in a higher cost of credit

• There will constraints in SA bond market to meet demand for liquid assets

• Demand for government bonds will have an impact on base rand interest rate curve & interest rate market in general

2.4. The impact of Basel III on RE financing

14

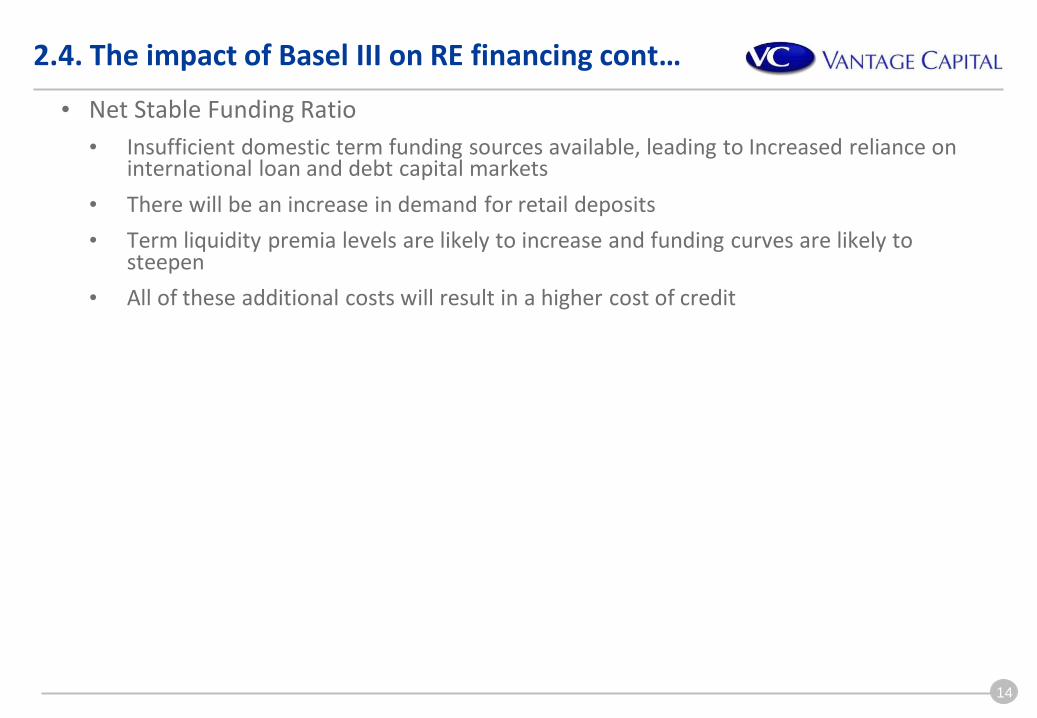

• Net Stable Funding Ratio

• Insufficient domestic term funding sources available, leading to Increased reliance on international loan and debt capital markets

• There will be an increase in demand for retail deposits

• Term liquidity premia levels are likely to increase and funding curves are likely to steepen

• All of these additional costs will result in a higher cost of credit

2.4. The impact of Basel III on RE financing cont…

15

Up until now the pricing of CPI linked debt has been almost the same as that of traditional JIBAR debt as the CPI and JIBAR base lending rate have been very similar and the margins over CPI/JIBAR are also comparable

• The following factors are however making CPI linked debt more attractive:

• The upward movements in the base lending rate have not been matched by similar increases in CPI, making CPI linked debt a lot cheaper

• CPI linked debt provides a natural hedge against inflationary changes

• Equity returns are front ended as the debt has a balloon or back-ended repayment profile

• The front-ending of equity returns will result in sponsors being able to bid lower tariff’s for the same equity return

3. CPI Linked Debt

16

CPI movements year on year

17

4. VANTAGE GREENX CREDENTIALS 3. CONCLUSION

18

• The impact of regulation, legislation and policy changes will have both positive and negative impacts on the wind industry in South Africa

• The impending policy changes (most notably carbon taxes and the environmental levy) will further entrench the economic sustainability of wind projects as these changes will highlight how much lower wind tariff’s are relative to other competing technologies, including thermal alternatives.

• On the negative side, there are a couple of changes to policy and legislation that are going to make it more difficult to finance wind projects going forward. These include:

• Basel III which will make long term lending costly and difficult to hedge

• Monetary policy changes which will result in upward pressure on interest rates

• Local policy requirements will put pressure on EPC contractors and the procurement strategies of bidders participating in the process’

• CPI linked debt and access to funding from non-traditional lending sources, is likely to become a focus for developers who are in search of cheaper funding options.

Conclusion

19

Contact Details:

RIDHAA AHMED Associate Mobile: +27 84 354 3113 Tel: +27 21 418 1130 Email: [email protected] www.vantagecapital.,com

Johannesburg • Cape Town

ALASTAIR CAMPBELL Managing Director - Vantage GreenX Mobile: +27 83 563 1920 Tel: +27 11 530 9139 Email: [email protected] www.vantagecapital.com

Johannesburg • Cape Town

20

Disclaimer

This presentation is provided for information purposes only on the express understanding that the information contained herein will be regarded as strictly confidential. It is not to be delivered nor shall its contents be disclosed to anyone other than the entity to which it is being provided and its employees and shall not be reproduced or used, in whole or in part, for any purpose other than for the consideration of the financing or transaction described herein, without the prior written consent of a member of the Vantage GreenX Fund Manager.

The information contained in this presentation does not purport to be complete and is subject to change. This is a commercial communication. This presentation may relate to derivative products and you should not deal in such products unless you understand the nature and extent of your exposure to risk. The presentation does not include a personal recommendation and does not constitute an offer, or the solicitation of an offer for the sale or purchase of any financial product, service, investment or security. The investments and strategies discussed here may not be suitable for all investors; if you have any doubts you should consult your investment advisor.

The investments discussed may fluctuate in price or value Whilst every care has been taken in preparing this presentation, no member of the Vantage GreenX Fund Manager gives any representation, warranty or undertaking and accepts no responsibility or liability as to the accuracy, or completeness, of the information in this presentation Past performance is not indicative of future results. For the avoidance of doubt, our duties and responsibilities shall not include tax advisory, legal, regulatory accounting or other specialist or technical advice or services.

You are to rely on your own independent appraisal of and investigations into all matters and things contemplated by this presentation. By accepting this presentation, you agree to be bound by the foregoing limitations. Kindly note that this presentation does not represent an offer of funding since any facility to be granted in terms of this presentation would be subject to the Vantage Capital group (incorporating the Vantage GreenX Fund Manager) obtaining the requisite internal and external approvals.

Copyright 2014 – the Vantage Capital Group. All rights reserved.