VALUE CREATION THROUGH FINANCIAL REPORTING: THE CONSTRUCTION INDUSTRY PERSPECTIVE Being a paper...

18

VALUE CREATION THROUGH FINANCIAL REPORTING: THE CONSTRUCTION INDUSTRY PERSPECTIVE Being a paper presented By MR. WOLFGANG KOLLERMANN, CNA Financial Director Julius Berger Nigeria Plc at the 20 th ANNUAL conference of certified national accountants Date: 26 October, 2015 Venue: International Conference Centre Theme: value creation and relevance of the professional accountant

-

Upload

gerard-newton -

Category

Documents

-

view

213 -

download

0

Transcript of VALUE CREATION THROUGH FINANCIAL REPORTING: THE CONSTRUCTION INDUSTRY PERSPECTIVE Being a paper...

VALUE CREATION THROUGH FINANCIAL REPORTING:

THE CONSTRUCTION INDUSTRY PERSPECTIVE

Being a paper presented By

MR. WOLFGANG KOLLERMANN, CNAFinancial Director

Julius Berger Nigeria Plcat the

20th ANNUAL conference of certified national accountants

Date: 26 October, 2015 Venue: International Conference Centre

Theme: value creation and relevance of the professional accountant

Mr. Wolfgang Kollermann is the Financial Director of Julius Berger Nigeria Plc and the Chairman of Julius Berger Medical Services Limited. He is also a Director in Abumet Nigeria Limited and PrimeTech Design & Engineering Nigeria Limited. He holds a higher diploma in Business administration and accounting. He has been in Nigeria since 1998 rising through the ranks to the zenith of his career when he was appointed the Financial Director of Julius Berger Nigeria Plc in 2010. Mr. Kollermann is happily married with two children.

He is a member of the Association of National Accountants of Nigeria (ANAN) and has been a registered professional with the Financial Reporting Council of Nigeria (FRCN) since 2012.

THE PRESENTER

Value Creation through Financial Reporting: The Construction Industry Perspective.

INTRODUCTION

OVERVIEW OF VALUE CREATION AND FINANCIAL

REPORTING

THE CONSTRUCTION INDUSTRY OVERVIEW

CONSOLIDATED FINANCIAL STATEMENTS

VALUE CREATION – TAXATION IN A GROUP STRUCTURE

CONCLUSION

Value Creation through Financial Reporting: The Construction Industry Perspective.

TA

BLE O

F C

ON

TEN

T

The purpose of any business is to create value for its investors, customers, employees, as well as, its environment. In achieving this objective, business executives employ the use of Financial Reporting to communicate to its stakeholders. However, the current reporting practices generally focus on previous costs and proceeds and have limited impact on indicators of future prosperity. Given the uncertainty that exists with non-physical assets, investors require greater detail about companies if they are to reach informed decisions.

Therefore, the growing recognition that the range of issues and opportunities affecting long term business value is much broader than can be reflected in a set of current year financial measures.

Value Creation through Financial Reporting: The Construction Industry Perspective.

INTR

OD

UC

TIO

N

Accounting goes beyond figures and the substance of any transaction should prevail upon its legal form.Financial Reporting needs to reflect this fact if they are to support investors’ capital allocation decisions effectively. Effective Financial Reporting provides a basis to address this by refocusing reporting around an organisation’s business model and operational priorities. The aim is to reflect the critical opportunities and challenges that affect the business; the same issues that management are dealing with on a daily basis within the organisation.

Value Creation through Financial Reporting: The Construction Industry Perspective.

INTR

OD

UC

TIO

N

Value Creation

The concept of value creation entails the performance of actions that increase the worth of a business. Many business operators now focus on value creation both in the context of creating better value for customers purchasing its products and services, as well as for shareholders in the business who want to see their stake appreciate in value.

Financial Reporting

Financial report is basically formal record of the financial activities of a business, person, or an entity which is presented in a structured manner for better understanding. Hitherto, the value added statement generally displays the additional value being created by any organization to its various stakeholders.

Value Creation through Financial Reporting: The Construction Industry Perspective.

OV

ER

VIE

W O

F V

ALU

E C

REATIO

N

AN

D F

INA

NC

IAL R

EP

OR

TIN

G

Effective Financial Reporting will provide a more complete picture of value, how it is shaped by current and future events, and explain what management is doing to create and preserve it. Ultimately, this is about business making its case for capital in a more effective way; bridging the gap between management’s value creation story and investors’ assessment of business value and stewardship. Effective Financial Reporting with a view on value creation should bring together material information about an organisation’s strategy, governance, performance and prospects in a way that reflects the true and fair view of any business and its going concern status.

It should provide a clear and concise representation of how an organisation demonstrates stewardship and how it creates and sustains value today and in the future.

Value Creation through Financial Reporting: The Construction Industry Perspective.

OV

ER

VIE

W O

F V

ALU

E C

REATIO

N

AN

D F

INA

NC

IAL R

EP

OR

TIN

G

Effective Financial Reporting combines financial and non-financial information with a forward looking perspective that is designed to help readers understand all the components of business value and how they may be affected by future opportunities and exposures. Taken together, these characteristics mean that it can provide a clearer perspective over business performance and value.

Consequently, effective Financial Reporting on value creation focusses on key drivers of value in the business. As business owners, there are some things we usually want more of as we grow our businesses - more clients, more revenue, more profit. But, how can we break things down to understand more clearly what drives these outcomes so that we can take concrete steps to improve them? The answer is VALUE CREATION!

Value Creation through Financial Reporting: The Construction Industry Perspective.

OV

ER

VIE

W O

F V

ALU

E C

REATIO

N

AN

D F

INA

NC

IAL R

EP

OR

TIN

G

The Nigerian & International financial regulations and guidelines are primarily designed to meet the reporting requirements of the public sector, oil and gas industry and financial institutions

However, the construction industry as part of the real sector is one of the key sectors for the Nigerian economy that comprises a wide range of products and services varying in terms of the economic value they generate and reflecting differences in the use of particular factors of productions.

Due to the increasing project risk and complexity together with the growth of long-term contracts and opportunities in post construction services which creates numerous challenges and opportunities, it is essential to create value by delivering a powerful combination of technology and comprehensive pre-integrated business solutions from initial contract identification to maintaining proper records during construction processes and finally, contract close-out.

Value Creation through Financial Reporting: The Construction Industry Perspective.

TH

E C

ON

STR

UC

TIO

N I

ND

US

TR

Y

OV

ER

VIE

W

With focus on effective financial reporting, the construction industry requires an industry tailored reporting standards that is different from other industries as a result of its unique characteristics. These include, amongst others, the largely long-term nature of contract implementation.In light of the above, and the peculiarity of the industry, the application of the accounting standard on construction contract (IAS 11) was adopted. The emphasis on this standard is the method of accounting for a project, be it short or long term. The standard, therefore, recommends the application of an accounting method called the “percentage of completion method” for recognising construction revenue based on approved certification by clients and invoices with executed works not yet certified. However, in order to successfully apply this standard to effectively create value, there are important aspect of the business which must be given significant attention.

Value Creation through Financial Reporting: The Construction Industry Perspective.

TH

E C

ON

STR

UC

TIO

N I

ND

US

TR

Y

OV

ER

VIE

W

TH

E C

ON

STR

UC

TIO

N I

ND

US

TR

Y

OV

ER

VIE

W

It is important to understand some key trends and dynamics in the industry such as pricing, completion speed, service delivery etc. to be able to provide solutions to sophisticated building challenges. There is a need for synergy between the various components in the construction process. Therefore, accounting is also part of the construction process since it provides vital information on the various revenue and cost elements portraying the true position of the company’s worth at any particular point in time; thus creating VALUE.

Value Creation through Financial Reporting: The Construction Industry Perspective.

In order to achieve high efficiency, construction companies are often structured in groups having to prepare consolidated financial statements for ease of reporting and administrative efficiency. There are several factors that influence, shape and drive the outcome of any construction activity. These are referred to as “key drivers” and are integral to value creation within the industry. These key drivers which are peculiar in the industry translate into effective management of construction process. This requires adequate planning & budgeting, cost control measures, appropriate contract structuring & monitoring, project execution and debt recovery. These are usually categorized into short and long term issues.Key drivers specifically associated with the industry include management depth & concession, competitive advantage and earnings

Value Creation through Financial Reporting: The Construction Industry Perspective.

TH

E C

ON

STR

UC

TIO

N I

ND

US

TR

Y

OV

ER

VIE

W

Management depth and succession: this entails the confidence of employees to the organization and adequate plans put by management to ensure that the going concern nature of the company is not threatened by both internal or external factors. Arrangements are usually put in place for effective transfer of knowledge and succession. Effective internal control mechanisms must be put in place and checks should be done periodically to ensure that the controls are operating effectively. Accounting also plays an important role in providing information which is used as a basis for executive management decisions.

Competitive advantage: this is an advantage over competitors gained by offering consumers greater value, either by means of lower prices or by providing greater benefits and service that justifies higher price. Skilled employees are the keys to success of any organization. Without managing and identifying the right skill for every assigned role, the overall value to be created by the system will be minimized. Specialization and cross-training at key levels of management will provide the desired technical know-how such that the company can thrive on its goodwill to gain more advantages over its competitors thereby creating strong working capital position and creditworthiness.

Earnings: typically refer to AFTER-TAX net income. Ultimately, a business's earnings are the main determinant of its share price, because earnings and the circumstances relating to them can indicate whether the business will be profitable and successful in the long run. The effectiveness of value creation depends on the successes of project management which results in favorable margins which in turn translate into growth thereby creating value to the stakeholders. But, how could value be generated through TAXATION to boost current and future earnings?

Value Creation through Financial Reporting: The Construction Industry Perspective.

TH

E C

ON

STR

UC

TIO

N I

ND

US

TR

Y

OV

ER

VIE

W

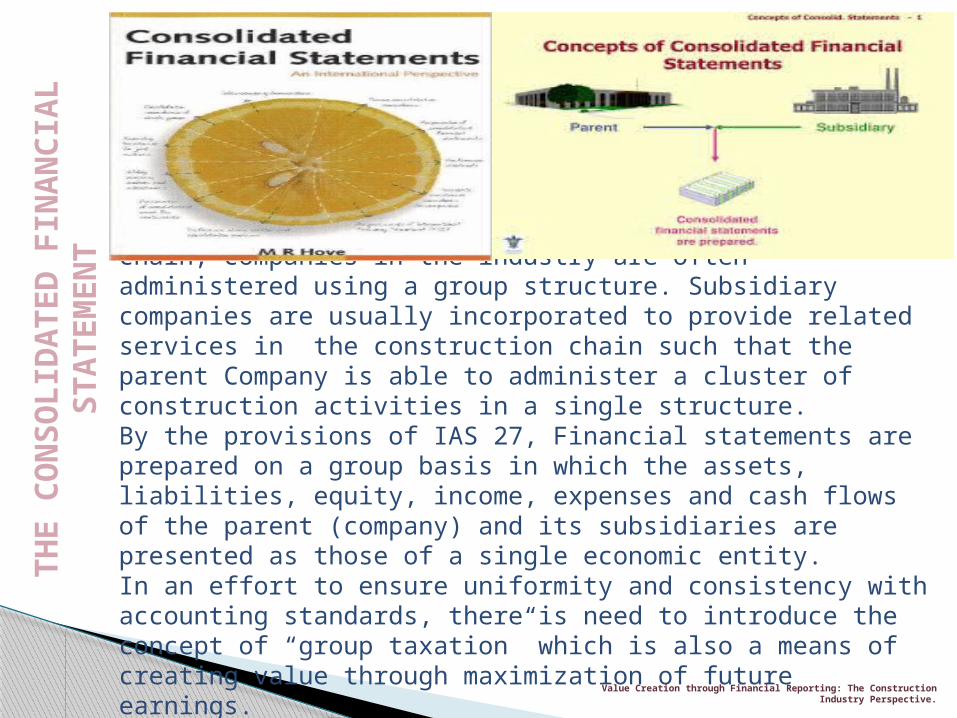

Due to the interwoven activities in the construction chain, companies in the industry are often administered using a group structure. Subsidiary companies are usually incorporated to provide related services in the construction chain such that the parent Company is able to administer a cluster of construction activities in a single structure. By the provisions of IAS 27, Financial statements are prepared on a group basis in which the assets, liabilities, equity, income, expenses and cash flows of the parent (company) and its subsidiaries are presented as those of a single economic entity.In an effort to ensure uniformity and consistency with accounting standards, there is need to introduce the concept of “group taxation” which is also a means of creating value through maximization of future earnings.

TH

E C

ON

SO

LID

ATED

FIN

AN

CIA

L

STATEM

EN

T

Value Creation through Financial Reporting: The Construction Industry Perspective.

As a special example, I would like to draw your attention to the idea of value generation through the introduction of effective group taxation.In the modern day organizational structure which is group driven, taxation when properly managed will be attractive to taxpayers because it gives them flexibility to organize their business activities, and engage in internal restructurings and asset transfers without having to worry about triggering a net tax. It will also eliminate the duplication of information and reduce the cost of administering taxation in accordance to the tax principle of economy. An efficient tax system is one key driver in value creation which allows resources to be allocated to their most productive uses without distorting corporate decision making. Efficiency is achieved when taxation supports the economic reality of a corporate group organization.

Value Creation through Financial Reporting: The Construction Industry Perspective.

TH

E V

ALU

E C

REATIO

N –

TA

XATIO

N I

N A

GR

OU

P

STR

UC

TU

RE

Furthermore, it will eliminate intragroup tax transactions such as VAT, withholding tax etc. while providing a formidable framework where gaps between accounting and tax treatments will be bridged. Group taxation, if implemented could potentially reduce compliance costs for taxpayers and administration cost incurred by the Government by making the tax rules more transparent and easily applicable. Finally, it is worthy to note that if group tax is implemented, a conducive atmosphere will be simultaneously created in addition to boosting the zeal of companies to create additional subsidiaries and/or diversify their investment to obtain higher economies of scale. Invariably, this will attract direct investments thereby creating opportunities for employment generation.

Value Creation through Financial Reporting: The Construction Industry Perspective.

TH

E V

ALU

E C

REATIO

N –

TA

XATIO

N I

N A

GR

OU

P

STR

UC

TU

RE

Conclusively, we have come to understand the following; Value creation takes place within a context. Accounting goes beyond figures Financial information is relevant for value creation. Value is created from the connectivity between a wide

range of factors.  Value creation manifests itself in outcomes and outputs.

Innovation is one of the key drivers to value creation

which is evolving. Measures of value creation are evolving. Accounting is an integral part of value creation in the

construction process

Value Creation through Financial Reporting: The Construction Industry Perspective.

CO

NC

LU

SIO

N

THANK YOU FOR LISTENING

Value Creation through Financial Reporting: The Construction Industry Perspective.

CO

NC

LU

SIO

N