Value Chain Management - globaltaxevent.com · KPMG International provides no client services....

40

© 2016 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. Value Chain Management 2016 Latin America Tax Summit, Rio de Janeiro 29 February to 2 March Challenges and opportunities ahead

Transcript of Value Chain Management - globaltaxevent.com · KPMG International provides no client services....

© 2016 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

Value Chain Management

2016 Latin America Tax Summit, Rio de Janeiro29 February to 2 March

Challenges and opportunities ahead

© 2016 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

Value Chain ManagementSession

Panelists

Tim Seitz— KPMG in US Head of Global Value

Chain

Brant Miller— Flextronics VP Tax and Financial

Murilo Mello— KPMG in Brazil seconded partner

2

© 2016 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

Agenda — Overview

— Value management point of view

— Relevance now

— Traditional Supply Chain Models— Overview

— The new tax and regulatory reality: impacts on global value chain

— Case Study— Value chain planning

— Driving change and achieving results

— Closing remarks

3

© 2016 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

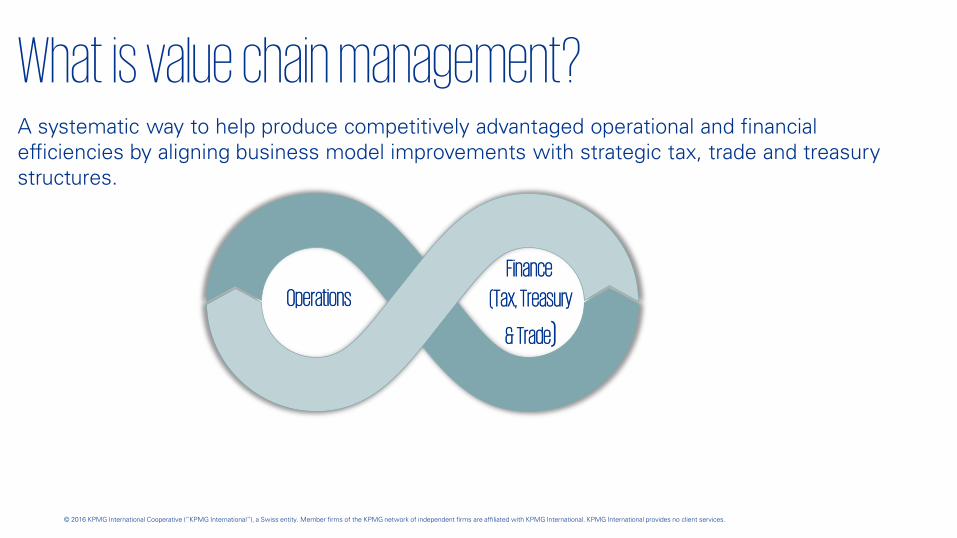

What is value chain management?A systematic way to help produce competitively advantaged operational and financial efficiencies by aligning business model improvements with strategic tax, trade and treasury structures.

Operations

Finance

(Tax, Treasury

& Trade)

© 2016 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

Relevant Trends: Harsh Fiscal Environment

© 2016 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

Relevant Trends: OECD BEPS action plan

Hybrid mismatch arrangements

Strengthen controlled foreign corporation (“CFC”) rules

Limit base erosion via interest deductions and other financial payments

Counter harmful tax practices taking into account transparency and substance

Prevent treaty abuse

Prevent artificial avoidance of taxable nexus/ permanent establishment status (“PE”)

Challenges of a digital economy

4

3

6

5

2

1Assure transfer pricing outcomes are in line with value creation –intangiblesAssure transfer pricing outcomes are in line with value creation – risks and capitalAssure transfer pricing outcomes are in line with value creation – high risk transactions

Establish methodologies to collect and analyze data on BEPS

Require disclosure of aggressive tax planning arrangements

Re-examine transfer pricing documentation

Make dispute resolution mechanisms more effective14

Multilateral Instruments15

12

11

13

7

8-9-

10

Coherence Substance TransparencySignificant VCM Impact

© 2016 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

Relevant Trends: Operating environment

Development of more complex & higher risk supply

chainsSlow global growth/

Harsh fiscal

environment

Regionalization

Faster product life cycles Innovation on the rise Big Data – fewer but bigger betsNew, disruptive OEMs

© 2016 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

Supply Chain Models

Traditional models and the new regulatory-tax reality

8

© 2016 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

The traditional model Principal – Limited risk manufacturing/distribution

— Principal– Regional responsibility– Tax effective location – Purchase raw materials and

sale finished goods.– IP ownership or royalty

— Limited Risk Manufacturers and Distributors– Control and bear limited risks– Rewarded with a sales based

return.

Legal title flow

Internal service/ distribution fees

Provision of services

Manufacturing

services

Sale of

product

Royalty

3rd Party

Customers

Limited Risk

Manufacturer

s

IP

Owners

3rd Party

Suppliers

Limited Risk

Distributors

Regional Principal Company

Decision making / IP control

© 2016 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

— Procurement Principal: buys and resell goods and services, negotiates contracts and assumes commercial risks.

— Manufacturers likely to have lower purchase prices as reward for compliance with new arrangements and depending on efficiencies achieved.

— Procurement Principal can expand activities (manufacturing, logistics, inventory management).

Buy/Sell Goods

and services

Procurement

Principal

3rd Party

Customers

3rd Party

Suppliers

Plant Organisations

Semi processed

Plant Organisations

Finished goods

Regional Procurement

Support Services

Organisation

Local sales

Organisations

The traditional model Buy – sell procurement model

© 2016 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

Case Studies

11

© 2016 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

ICMS and ICMS STOperational efficiency

Case Study: Key points to be addressed

Quality

ETR management

PIS and COFINS

Income tax

Customs DutiesIPI

Treasury / Incentives

Business Model

Alignment

1 Competitive price

2

3

4

5

Margin improvement

6 Resilience

Major components & Source

Manufacturing, Assembly and Test

Design

Define the product

Channel Management

Operational considerations

Financial considerations

Risk management7

© 2016 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

Case Study #1Brazilian consumer company

13

© 2016 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

Case Study — A Brazilian company (“BR Ltda”), engaged on the

consumer market industry, has operations in Brazil for more than 35-years and revenues around US$ 400 million.

— For the domestic manufacturing process, BR Ltda imports or procure locally parts. BR Ltda does not utilize third parties or other types of contract manufacturing.

— The company has customers in all Brazilian states, as described in the next slide.

14

© 2016 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

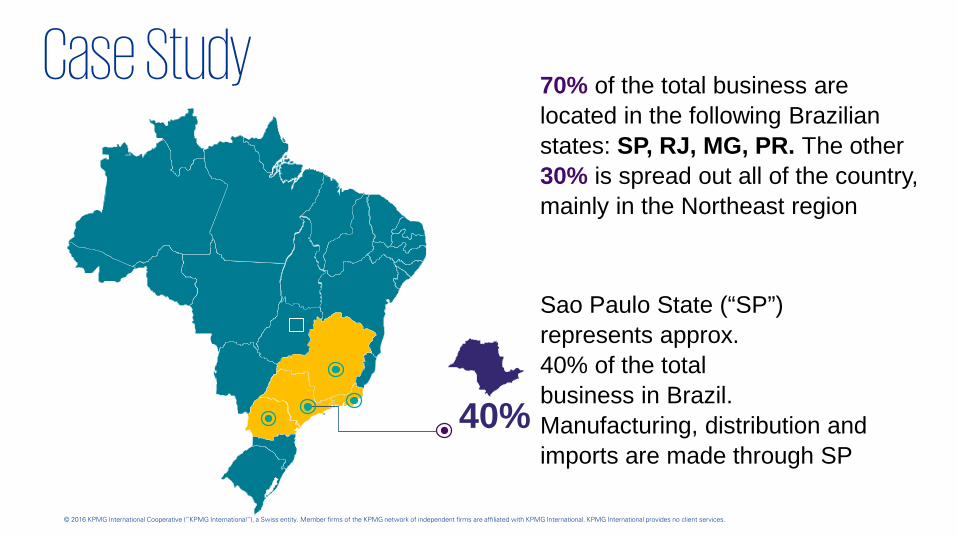

Facts and Assumptions Preliminary

70% of the total business are located in the following Brazilian states: SP, RJ, MG, PR. The other 30% is spread out all of the country, mainly in the Northeast region

40%

Sao Paulo State (“SP”) represents approx. 40% of the total business in Brazil. Manufacturing, distribution and imports are made through SP

Case Study

© 2016 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

Facts and Assumptions Preliminary Case Study

40% of imports are from the US and 60% from China

© 2016 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

Case Study — The shareholders of BR Ltda are considering to sell 30%-

40% of the company. The aim of this strategy is to raise funds for an international expansion

— An US Multinational Company, with operations in the same industry and with the intention to enter into the Brazilian market, has signed a MOU with the BR Ltda’s shareholders

— The US Multinational Company has “footprint” worldwide, with facilities in different countries and regions, including China

17

© 2016 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

Case Study — Before closing the deal and decide the viability of the

potential investment, the shareholders of the US Multinational Company want to understand the existing supply chain structure in Brazil

— Moreover, the US Multinational Company intends to “test” its international model of supply chain, utilized worldwide. Also the US Multinational Company expects to explore all viable planning supply chain alternatives, “risk free” or not

18

© 2016 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

Case Study — Furthermore, both US and BR companies are flexible

regarding the location and charges in connection of the intangibles (“IP”), provided there is no adverse tax impacts and risks on this IP movement

— Finally, the companies are aware of the current tax-regulatory scenario worldwide, triggered by BEPS, as well the regulatory compliance environment in the region (e.g. Central Bank regulations). Nevertheless they would like to explore alternatives to manage efficiently its supply chain operation

19

© 2016 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

Potential tax credit accumulation situation

Credit

18%

Debt

4%

Accumulated credits

10%~14%

Challenge: ICMS credit

accumulation on the resale

of imported goods

Case StudyIssue: potential ICMS credit accumulation on inter state sales

Import

Brazilian Subsidiary

(SP)

Interstate

ResaleB2B

(other States)

Foreign Parent

CompanyICMS 18%

ICMS 4%

© 2016 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

Import

Brazilian Subsidiary

(SP) Resale

B2B

(Other States)

Potential tax credit

accumulation eliminated

Foreign Parent Company

Special tax regimes: ICMS on

import may be suspended which

eliminates the ICMS credit

accumulation.

Alternative # 1ICMS management

ICMS ~ 6% ICMS 4%

Important aspects

The company must present a tax model study on ICMS credit position

The application must comply with other rules, e.g. clearance certificate and may attract tax inspection

Case StudyPotential alternative: Special ICMS regime on imports

© 2016 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

ICMS-STPIS/

COFINS

IPI

Mark up -

applicable to all taxes

Challenge: reduction on the high

tax burden on the resale of

imported goods

Alternative # 2Tax efficient mark-up model

Import Brazilian Subsidiary Resale B2B Foreign Parent

Company

Case StudyIssue: direct imports and resale of final products capturing final mark up

© 2016 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

Lower mark up

ICMS-ST PIS/COFINS IPI

Alternative # 2 Tax efficient mark-up model

Tax benefits reached ICMS-ST

elimination (Trading company) and tax optimization on

mark up.

BrazilianSubsidiary

(SP)

B2BForeignParent

CompanyTrading - OEM

(SP)Import Resale

Branch(AnotherState)

Trading - OEM(Branch) Resale

B2B(Otherstates)

Mark up not “captured” by ICMS ST

NO ICMS-ST PIS/COFINS IPI

Case StudyPotential alternative: utilization of trading company or local contract manufacturing

© 2016 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

Alternative # 1ICMS management

Important aspects

Trading Company as IOR is deemed as ICMS ST taxpayer

The utilization of a local manufacturing company could represent operational and tax savings from an operational, tax and logistic perspective

The utilization of tax incentives for the local manufacturing or assembling could also “boost” the incentives

Case StudyPotential alternative: utilization of trading company or local contract manufacturing

© 2016 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

Case Study #2Market growth and value chain planning

25

© 2016 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

Case Study — Multinational company (“MNC A”) operating in

Brazil in the consumer industry has been forecasting a market growth of 12% on different segments

—In case MNC A keeps the current logistic network and according to the sales growth plan, approx. US$ 37 million logistics costs in 2025 growth are estimated. This cost will represent approx. 13% of the net sales.

26

© 2016 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

Case Study — MNC A has the following supply chain structure:

— One distribution center in São Paulo, which distributes products to all other States in Brazil

— The importer of record is the legal entity located in the State of São Paulo

— Due to limitation on the transfer of intangible rights, MNC A cannot utilize a third party manufacturer. It will need to explore alternatives in connection with the distribution channels and tax incentives.

27

© 2016 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

Alternative # 4Distribution center

Sale DC(SP)

B2B(SP)

LocalManufacturer

(SP) ICMS-ST No ICMS-ST

DC(Other state)

ResaleB2B

(Other States) ICMS-ST

ICMS –ST isNOT paid by manufacturer

Important aspects

Breakdown of supply chain structure into different regions (SP=>SP and remaining states through another location)

Achievement: ICMS reimbursement is no

longer needed

Case StudyPotential alternative: Distribution Center with state tax incentives

© 2016 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

Alternative # 1ICMS management

Important aspects

The analysis of logistics costs as well as tax incentives on different regions could enable cost reductions.

For distribution activities, for example, RJ, MG and PE States could offer tax incentives.

Important: due to current judicial, legislative and economic scenario in the country, a risk assessment on the utilization of the tax incentives should be made.

Different DCs set up in different states could also improve logistic / transit times, depending on the region.

Important: setting up new DCs could involve important changes on operation.

IT systems, new logistics controls and close down of previous structure (e.g. warehouse) could trigger costs, which should be leverage due to the potential savings to be obtained.

Case StudyPotential alternative: DC + Tax Incentives

© 2016 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

Alternative # 1ICMS managementCase Study

Potential alternative: DC + Tax Incentives Current Operational Model

(“as is”)

Imports through SP and DC in SP distributes national and imported products to Brazil.

.

SP

DC in RJ distributes national and imported products to Brazil.

Imports carried out through Rio de Janeiro.

Value Prop #1One DC (RJ)

Value Prop #2Two DCs (MG and PE)

DC in MG distributes national and imported products (South region). DC in PE distributes (North and Northeast).

MGRJ

PE

© 2016 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

Alternative # 1ICMS managementCase Study

Potential alternative: DC + Tax Incentives

• ICMS deferral on import of goods.• 1.5% ICMS presumed tax credit. • 1.5% ICMS presumed tax credit .

• ICMS deferral on import of goods. • Average presumed tax credit of 1.1%.

• ICMS deferral on import of goods.• Maximum presumed tax credit of 47.5% calculated upon the ICMS due (tax

basis x applicable tax rate).

• Tax risk assessment recommended !

Exampleof Tax IncentivesState

RJ

MG

PE

!

© 2016 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

Case Study #3Local Manufacturing

32

© 2016 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

Case Study — Multinational Company B (“MNC B”) had a quick-off meeting

regarding its “Green Project” for operations in Brazil.

— The key aspect for the proposed investment is to analyze the most favorable location for its the Brazilian manufacturing plant, combining operational and tax efficiency.

— The following aspects should be accomplished on this project: (i) analysis and comparison of domestic tax incentives with the Manaus Free Trade Zone (“MFTZ”) incentives and (ii) impacts in terms of costs, service level and risks.

33

© 2016 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

Potential tax reductions

Alternative # 3 Manaus Free Trade Zone (MFTZ)

MFTZ Tax incentives

ICMS:

Tax credit

(12%)

PIS-COFINS:

Reduced (3.65%)

IPI:

Exempt

MFTZ Tax incentives

ICMS:

suspended

PIS-COFINS:

suspended

IPI:

suspended

II: reduced

(88%)

BrazilianSubsidiary

Foreign ParentCompany MFTZ

Import Sale

Important aspects

Logistics costs and compliance with Manaus Free Trade Zone – MFTZ benefits are extremely important element in the model

Case StudyPotential alternative: Local Assembling

© 2016 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

ManausFree Trade Zone (MFTZ)■ MFTZ requirement:

Basic Productive Process (“PPB”).

Other requirements should be met

■ Corporate income tax

75% reduction of IRPJ for the period of 10 years (currently limited to year 2073). Not applicable to Social contribution on net income (CSLL).

■ Import duties

Reduction of up to 88% of the import tax.

■ Excise taxes (IPI)

Exemption of IPI for products consumed and/or manufactured within MFTZ.

■ Sales tax (ICMS)

Deferred ICMS tax on import of raw materials used in a manufacturing process of intermediate products;

© 2016 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.36

Mexican maquiladora

Maquiladora

Provides at least 30% of new

machinery and equipment

LATAM clients

Commercial Relationship –

Sale of products

Maquila ServiceCo

Sale of products in Mexican

market

Maquila Activities:- Plant- Grow- Harvest- Pack- Export

Offshore

ABC ForeignCo

Exportation of finished products

Owner of seeds, location in

favorable tax jurisdiction

Local distribution of

finished products

© 2016 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

Raw materials/components can be owned by ABC’s foreign entity or head office

Manufacture commercial relationship with ABC’s foreign entity or head office.

Subject to transformation process (including plant, grow, harvest and pack).

Maquila contract under IMMEX regime

Mexican Maquila can be subject to “Agricultural tax regime” – 90% of its total revenue must come from agricultural activities.

Creation of a Maquila ServiceCo for sale of finished products within the Mexican market (local sales).

Domestic and permanent imported raw material/components should be exported.

37

Mexican maquiladora

© 2016 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

Machinery and equipment:

Property of ABC’s foreign entity (Head office) – must represent at least 30% of the total machinery and equipment used in the maquila operation (new machinery in Mexico). Property of a third party foreign resident – must be provided with a commercial relationship of manufacturing with the head office.

Leased.

Property of the maquila entity.

Mexican maquiladora can access to a specific tax benefits for IT purposes (Agriculture tax regime up to approx MXN $10 million pesos).

38

Mexican maquiladora

© 2016 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

Transfer pricing provisions should be complied with by the Mexican maquiladora, a minimum taxable profit is required, maquiladoras are not expected to generate tax losses. Analysis between safe harbor method and economical study.

Combined activities can be carried out by the maquiladora entity (maquila / non maquila), tax losses carry forward:

Analysis to apply non maquila tax losses to maquila profits.

39

Mexican maquiladora

© 2016 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavor to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation.

The KPMG name and logo are registered trademarks or trademarks of KPMG International.

40