Valuation for Natural Capital and Ecosystem Accounting ... · within the Knowledge Innovation...

57

Valuation for Natural Capital and Ecosystem Accounting Synthesis Paper

Transcript of Valuation for Natural Capital and Ecosystem Accounting ... · within the Knowledge Innovation...

Valuation for Natural

Capital and

Ecosystem Accounting

Synthesis Paper

Page 1 of 57

Valuation for Natural Capital and Ecosystem Accounting: Synthesis Paper Prepared for:

The European Commission as part of a contract on the provision of technical support for the

development of Natural Capital Accounting (Contract 07.0202/2017/767463/SERJENV.D.2), led by

UNEP-WCMC in collaboration with IEEP and UEA CSERGE. This report was prepared University of East Anglia, Centre for Social and Economic Research on the Global Environment (CSERGE) Published September 2017 Copyright European Union 2018. All rights reserved. Certain parts are licensed under conditions to the EU Citation

Badura T., Ferrini S., Agarwala M. and Turner K. (2017) Valuation for Natural Capital and Ecosystem

Accounting. Synthesis report for the European Commission. Centre for Social and Economic Research

on the Global Environment, University of East Anglia. Norwich 2017. Disclaimer: The information and views ser out in this report are those of the authors and do not necessarily reflect the official opinion of the Commission. The Commision does not guarantee the accurancy of the data included in this study. Neither the Commission not any person actting on the Commission’s behalf may be held responsible for the use which may be made of the information

contained therein.

The Centre for Social and Economic Research on the Global Environment (CSERGE), University of East Anglia (UK), is internationally renowned for working at the forefront of interdisciplinary research, on a range of environmental issues. CSERGE research covers a huge array of topics such as sustainable development, the relationship between humans and the environment, natural resource valuation and management, economic instruments, land use, water, energy, wetlands and coastal zone management, climate change,

ecosystem services and natural resource accounting.

Page 2 of 57

Table of Contents

0 INTRODUCTION 3

1 SUMMARY 4

2 BACKGROUND – NATIONAL AND WEALTH ACCOUNTING 11

2.1 Three approaches to natural capital accounting: 16

3 VALUATION IN/FOR NATURAL CAPITAL AND ECOSYSTEM ACCOUNTING

19

3.1 Exchange and welfare value concepts 21

3.1.1 Simulated exchange values 23

3.2 Valuing flows – ecosystem services 24

3.2.1 Valuing pollination 35

3.2.2 Valuing recreation services 39

3.3 Stock valuation – monetary asset accounts 42

4 KEY MESSAGES 45

5 BIBLIOGRAPHY 47

6 ANNEX 51

Page 3 of 57

0 Introduction

This report aims to fulfil two objectives identified with the clients (i.e. KIP INCA

partners and JRC in particular). These were to provide overviews1: 1) of the main issues

surrounding valuation methodologies in the context of ecosystem and natural capital

accounting; and 2) of the possible approaches for valuing crop pollination and recreation

within the Knowledge Innovation Project for an Integrated system for Natural Capital and

ecosystem services Accounting (KIP INCA). This report might be further expanded in the

future to provide an extended discussion of the valuation methodologies in context of the

KIP INCA future plans. The report provides a background for Technical Support actions in

Q3 and Q4 2017, aiming to support the valuation work being undertaken at the Joint

Research Centre.

Following an extended summary, this report starts with a brief background on national

and wealth accounting and sets out three possible generic approaches for future progress. It

also indicates how natural capital accounting can contribute to wider strategy and policy

analysis. It then discusses more specific issues related to valuation concepts such as exchange

and welfare values and their uses and limitations which are closely related to the

overarching purpose of the KIP INCA and its planned use of the derived information.

Further, this report discusses the valuation approaches for flows of ecosystem services as

well as how it might be possible to value assets (stocks) as part of the KIP INCA.

Complementary work has been undertaken for JRC covering specific ecosystem flows

valuation in more detail (Fact sheets feedback). This material is provided in the Annex.

We would like to keep this report as a living document that would be updated over the

duration of this project. This would allow for further reflection on both empirical results and

data availability, resulting from Technical support Action, and the incorporation of

comments and feedback from KIP INCA partners.

1 Please note that this report builds on an assumption of relative familiarity with the recent material and guidance documents

related to Natural Capital accounting. Namely, it is assumed that the reader is familiar with SEEA CF 2012, SEEA EEA 2012,

SEEA EEA Draft Technical recommendation (2017). Please refer to these documents for further background and information

related to the recent discussions on environmental and economic accounting as well as ecosystem accounting practices.

Page 4 of 57

1 Summary

National income accounting is a method of collecting, organising and reporting

desirable information on economic activity which can assist in the measurement of trends

and decision making. It does not fully measure human welfare/wellbeing, nor does it include

a comprehensive assessment of the impacts on the environment linked to the economic

activity. National accounts are human constructs, deliberately and strategically designed and

have always included a degree of pragmatism in their evolution. So what is included or

excluded from the national accounts is a matter of choice (Coyle 2014). The inclusion of

natural capital into this accounting context is, we would argue, also a choice and one in

which a degree of pragmatism is required.

A significant problem associated with the inclusion of natural capital and ecosystem

services into the national accounts is that market prices and so-called exchange values are

often missing. This has led to efforts to ‘impute’ values (proxy exchange values) which have

to be indirectly measured or estimated. Production function data if available are especially

useful in this context. There also needs to be a recognition that the prevailing institutional

governance arrangements (e.g. property rights regimes, existing laws and regulations,

cultural norms etc.) will condition the ‘imputed values’ that may be observed and calculated.

We also note the criticisms from some conservationists that assigning monetary values to

nature will end up in the complete ‘commodification’ of the environment. While such an

outcome would risk overemphasising the substitution possibilities between natural capital

and other forms of capital, as well as excluding the intrinsic value nature might possess, this

outcome is not inevitable. A pluralistic approach to valuing nature has much to recommend

it. With this line of reasoning it is possible to discern a number of value dimensions: the

value elicitation process, and the source of the value information i.e. individual community

societal/cultural group; the value motivation i.e. self-regarding or other-regarding; the

overall institutional context; and the value scale i.e. to society or to the individual. What is

required is a pragmatic view of environmental valuation which accepts that not all aspects of

nature can be meaningfully captured in money terms, but much can be treated in this way

and this could bolster conservation (Turner 2016). We outline in a succeeding section how

natural capital accounting incorporating monetary values can contribute to economic

development plans and strategies at the national and regional level, as well as down at the

project/programme level. This pragmatic approach is mirrored in the history of national

accounting in debates over whether parts of the informal economy can be estimated in value

terms and included in the accounts. It is also the case that a significant amount of

Government spending does not directly reflect exchange values, although some is based on

costs of production.

Page 5 of 57

As yet, natural capital lacks a widely agreed definition and a number of different

possible approaches could claim to provide (with varying degrees of complexity, uncertainty

and practicality) natural capital accounting processes. Most prominently these include:

Provide a limited extension to the measurement of economic activity via the main

national income/capital accounts, or within the framework of the UN System of

National Accounts (SNA)

Compile physical accounts (based on, for example, land use and habitat units2) as

satellite accounts, which highlight the contribution of the environment to the

economy and society

Compile physical and monetary natural capital satellite accounts, which are

compatible with but separate from national income/capital accounts

Fully integrate natural capital and ecosystem services accounts into national

accounts

Compile comprehensive social welfare wealth accounts (with economic welfare

values linked to wellbeing) in line with sustainable development principles (weak or

strong)

Compile corporate natural capital accounts (identifying firms’ dependencies and

impacts on natural capital in value terms).

Because each of these approaches have different objectives and answer somewhat different

questions, they require different data and, importantly, different values and valuation

methods. For simplicity, in the report we distinguish three broad approaches to natural

capital accounting each with the following objective:

1) Development of extended SNA type accounts to include more environmental

impacts, but which still follow SNA conventions and restrictions on how economic

activity is measured (APPROACH ONE). This approach would hence be strictly

based on exchange value concept.

2) Development of a separate set of (physical/monetary) Satellite natural capital

accounts that can provide complementary information to SNA type accounts. They

would serve to highlight the different contributions of the environment to the macro

economy and hence allow for a degree of flexibility and fit-for-purpose design

(APPROACH TWO). This approach could use different value concepts including

exchange and economic welfare values.

3) Development of comprehensive social welfare Wealth accounts, these are data

intensive and require a full range of shadow values for monetary valuation purposes

in order to capture wellbeing (APPROACH THREE).

2 In the SEEA context the relevant spatial statistical units are Basic statistical units (BSUs), Ecosystem Assets (EA)

and Ecosystem Accounting Area (EEA). See SEEA EEA 2017 for further details.

Page 6 of 57

The choice made between these different approaches will determine the form and

extent of any new accounting system and appropriate economic valuation methods. But the

approaches are not mutually exclusive. For example, information could be transferred from

the second to the first or to the third as knowledge improves and/or changes in accounting

practices are agreed. Similarly, information from accounts based on one approach could be

used to complement accounts based on another approach for specific policy requirements.

The first of these approaches (APPROACH ONE) it has been argued, limits the type of

values that can be utilised to incorporate environmental impacts into a monetary account.

From this viewpoint only exchange values can be used, although some analysts have made

the case for a wider inclusion of externality effects (Vincent 2015).Taking the example of a

positive externality where an ecosystem provides a service that is an input used by a firm to

increase production, the input value could be interpreted as an implicit exchange value. The

input value would be measured in terms of the value of the additional output produced by

the firm, and Vincent (2015) has argued that this is the maximum amount a producer would

be willing to pay for the ecosystem service if a market actually existed. If this approach is to

be generalised a number of practical measurement problems would need to be overcome.

The second approach (APPROACH TWO) aims to bring together a separate set of satellite

(physical/monetary) accounts covering ecosystem services assets (stock) and services (flows).

The objective is to ‘mirror’ changes in economic activity (expressed in the SNA type

accounts) with a set of ‘environmental’ accounts which quantify and value the consequences

of economic activity as it impinges on the environment and society through various drivers

and pressures. An agreed baseline position and timeline is required, but a wider range of

plural values can be utilised e.g. exchange and economic welfare values plus others.

The third approach (APPROACH THREE) attempts to provide a comprehensive social

welfare based wealth account in monetary terms (economic welfare values). These accounts

would aim to reflect the fullest possible quantification of capital assets and economic and

social wellbeing impacts (including for example health and education) in order to achieve

sustainable development.

The three approaches to natural capital accounting can play a diverse number of roles in the

policy process. At a strategic level (e.g. promotion of the Circular Economy strategy),

quantifying the natural capital asset base and the benefits it provides to the economy and

society represents an important component of a national or regional economic development

strategy. Such an approach would seek to increase resource use efficiency, increase resource

supply security and promote eco-innovation, thereby raising the overall productivity of the

economy. A monitoring system for natural capital can identify gaps in knowledge and lead

to a risk register (Mace et al 2015) together with information on ‘critical natural capital’

limits. Prior identification of the pressures, drivers and threats/opportunities to natural

Page 7 of 57

capital can facilitate the move to sustainable development paths. It may also be possible to

investigate societal inequalities by augmenting income data (Gini coefficient) with natural

capital provision and access data. At the enabling/implementation level natural capital

accounting can help in the assessment of the effectiveness of prevailing policy instruments

and the practicability of policy objectives, or future policy options. The same accounting

information can also play a role in individual project/programme assessment (see for

example the Balance Sheet approach (UK NEA Follow On 2014; Turner 2016).

The natural capital accounting system generally conceptualises the ecosystem as the

asset (stock), rather than the constituent parts. The assets are described in terms of a

particular land cover class or ecosystem type and in terms of their extent and condition. Hein

et al (2016) provide additional concept ideas relating to ecosystem assets, they argue that

capacity, capability to supply services and the potential supply of services are necessary

measures for accounting. These notions are closely related to sustainability and critical

natural capital limits and thresholds thinking. The distinction between intermediate services

and final ecosystem service flows used by beneficiaries, also needs to be borne in mind

(Boyd and Banzhaf 2007; Fisher et al 2009). Physical accounts classify and record the extent,

condition of and annual service flow from ecosystem assets. Monetary accounts put

monetary values (point estimates) on final ecosystem services on an annual basis, or on the

capacity to produce future flows of final services. There is a further choice to be made on

monetary values: welfare and/or exchange values. The former reflect the willingness to pay

for goods and services, regardless of whether they are exchanged for cash, or how much cash

they would be exchanged for if they were exchanged. The latter are the value at which flows

and stocks are in fact, or could be, exchanged for cash. Market prices are the reference for

valuation in most official guidance (e.g. OECD 2009). The guidance continues to cover

contexts in which no market price is available and recommends that if costs are also not

available, then stocks and flows may be valued, as a last resort, at the discounted present

value of expected returns. We take a closer look at valuation methods for ecosystem services

in a later section, along with some pragmatic guiding principles.

But other problems and choices also loom large in this accounting context. It is

important to clearly distinguish between stock and flow concepts. The SEEA EEA3 defines

the ecosystem stock account in terms of the extent or volume of the asset and its condition or

quality, at the start and end of a year. The services account shows flows over a given period

of time, but with the complication that some cross-cutting service accounts will be necessary

3 SEEA EEA refers to the report published by United Nations, European Commission, Food and Agricultural Organization of

the United Nations, Organisation for Economic Co-operation and Development, The World Bank (2014b) System of

Environmental-Economic Accounting 2012 – Experimental Ecosystem Accounting. United Nations, New York

Page 8 of 57

in cases where some services are provided by a number of habitats. A particularly difficult

challenge is posed when there is uncertainty over the sustainability of a given stock under

use pressure or environmental change. The use of point estimates for ecosystem services

values when non-marginal stock changes occur and thresholds are crossed is problematic.

The development of ‘red flag’ (e.g. UK NEAFO 2014) warning measures in the physical

accounts needs urgent attention given the uncertainties over threshold effects. If a strong

sustainability position is accepted then restoration costs may play a role in any satellite

account.

Stock (asset) sustainability and lifetime questions are important and add a further level

of complication to the accounting task. Hein et al (2016) have put a new emphasis on

ecosystem capacity and capacity accounts. The capacity relates to the sustainable rate of

usage of a ‘bundle’ of ecosystem services and represents an important link to long term

viability of an asset. This link is not reflected in the currently proposed approach to asset

valuation relying on a net present value basis for an expected flow of ecosystem services. In a

satellite account, UK ONS (2017) has suggested a proxy approach in which a minimum

restoration/ replacement cost would be charged and summed over the asset lifetime

(undiscounted). The acceptance of a strong sustainability worldview (with its constant

capital rule) is critical to this sort of proxy method and does not fit easily into SNA practice.

There is some debate over whether restoration costs are or are not equivalent to asset

depreciation in national accounts. On an annual basis, the latter represents the cost of

replacing the asset in its depreciated state, but the sum over all annual depreciation charges

is equivalent to the cost of replacing the asset in its non-depreciated state.

The use of replacement cost values will also be conditioned by the institutional /policy

context. Taking water purification as an example, this is strictly an intermediate ecosystem

service which yields the final service, clean water which has an economic benefit value to

consumers. However, if a formal water quality standards regime is in place then a value

comparison between a wetland providing a natural purification service and a water

treatment facility is a valid procedure. The costs of the two alternatives could be compared in

order to derive a cost effective solution.

Asset lifetime considerations bring in the question of an appropriate discount rate.

Most environmental economists agree that for environmental long lived assets a discount

rate based on market rates is not appropriate. Markets are essentially driven by short term

considerations. So for ecosystem assets a capacity and accounting lifetime of 100years seems

reasonable, together with a declining discount rate such as that adopted in the UK, based on

the Ramsey formula (e.g. ONS 2017).

The distinction between stock and flow has also been recently highlighted in work in

the USA (Fenichel and Abbott 2014, Fenichel et al., 2016). This line of argument seeks to keep

Page 9 of 57

natural capital separate from ecosystem services by linking natural capital more formally to

national capital accounts, with ecosystem services classified as part of the national income

account. A complication with this stream of research is the necessity to accommodate the

“scarcity effect” of natural capital depletion and the effect on market prices. This problem

seems to have been overcome in some empirical cases on groundwater and fisheries

compiled by these analysts (see sections in the main report).

The environmental economics literature now contains a range of tried and tested

valuation methods and techniques for market and non-market goods and services which can

in principle be used to value ecosystem services flows. For accounting purposes a clear,

explicit and consistent application of valuation methods is important. For example, ONS

(2017) have suggested a number of principles as guidance in the valuation process which we

have reinterpreted as follows:

Use of a particular technique should be clearly explained and related to the

underlying biophysical assessment process

Valuation methods should be transparent, intuitive and replicable

Where possible calculated values should be compartmentalised into their ‘price’ and

‘quantity’ components

‘Benefits transfer’ potential for using available estimates should be explored with

caution.

Four broad categories of valuation methods are potentially available:

Market-based methods (using market price values)

Revealed preference methods (related to the behaviour of individuals and the

expenditure they incur)

Cost-based methods

Stated preference methods (related to the answers provided by individuals when

responding to survey questions about their willingness to pay for something).

A fuller discussion of these methods is provided in a later section of this report.

The diverse range of methods for valuing flows of ecosystem services (e.g. Freeman et

al 2013) that are available to some extent reflect the prevailing set of different policy

objectives and contexts. An important first step in the process of developing natural capital

accounts is to get clarity and agreement on the broad approaches to accounting and the

related policy objectives. For example, while more effort might be put into developing a full

set of SNA-compatible natural capital accounts, specific satellite ecosystem service accounts

might also be constructed to provide complementary information (e.g. pollination accounts).

The ultimate objective of development of natural capital accounts is facilitation of

better-informed decision making. The debate surrounding the use of valuation methods for

Page 10 of 57

the natural accounts is far from settled. Since both the potential use and possible

methodologies are not yet fully clarified, we would argue that an open approach in the

context of KIP INCA might be taken to valuation methodologies. Nevertheless, this

pragmatism should involve a clear identification of and clear specification of the agreed

goals for the use of accounts. The work within the KIP INCA context allows grounds for

testing some of the approaches as well as comparing results under different approaches. This

is an opportunity that should be fully, but carefully, exploited.

Page 11 of 57

2 Background – national and wealth accounting

Current macroeconomic decision making is largely guided by the information derived

from the System of National Accounts (SNA; EC et. al. 2009) and its flagship policy indicator,

the Gross Domestic Product (GDP). Despite its frequent and (unfortunately) common public

interpretation as a welfare index, GDP does not provide a comprehensive picture of welfare

changes (Dasgupta 2009). It is clearly a fundamental component of overall wellbeing and is

a necessary but not sufficient measure of welfare. GDP is a gross flow measure, building on

SNA’s objective to “compile measures of economic activity in accordance with strict

accounting conventions based on economic principles” (EC et. al. 2009, para 1.1). It accounts

for flows of economic activities for a specified accounting period, however it omits some

non-market goods and services. This has consequences for environmental protection policy.

Rather than GDP, a stock of wealth indicator is required to measure intertemporal

sustainable growth and development progress.

Recent decades have seen an increased realisation of the need to better understand and

manage the relationship between human society and the environment. Decreases in

environmental quality have led to calls for improvement in our measurement systems for

sustainable development. A spectrum of approaches can be envisaged for this task. On one

end of this spectrum are different variants of a limited extension of national accounting that

incorporate environmental and ecosystem assets into its measurement system4. The

environmental and ecosystem accounts could also be constructed as satellite accounts that

are not integrated within the SNA system. These could be biophysical only, or also

encompass monetary accounts. A future and ambitious goal might be to fully integrate

ecosystem services into SNA system. At the other end of the spectrum of approaches to

natural capital accounting is wealth accounting. On a conceptual basis, some of these

approaches differ in the focus of their measurement systems and hence their ultimate

usability potential for policy making. While national accounting is focused on the flows of

economic activity over an accounting period (usually a year), wealth accounting focuses on

the changes in the (as far as possible) comprehensive set of stocks of capital assets

underpinning economic growth. In other words, national income accounting focuses

predominantly on the (changes in) flow of economic activities, wealth accounting aims to

measure (changes in) stocks of assets that condition the flows. These different approaches

offer useful insights for policy making and present different, and to certain extent

4 Note that, due to focus of this report on the accounting for environmental and ecosystem goods and services, we omit in the

following discussion the social dimension of sustainable development. Nonetheless a substantial progress has been made in

understanding and data collection on indicators related to social capital.

Page 12 of 57

complementary, alternatives and context for assessment of economic growth and

development. We feel that it is important to keep in mind the different possibilities for the

KIP INCA.

As it is predominantly focused on market activity5, SNA is missing important

information that is relevant for the assessment of growth in its broadest sense. Indeed,

important omissions of SNA’s measurements have been discussed since its inception in the

1950’s. Some contributions to economic activity are not reflected in the national accounts. In

particular, as a systematic measurement tool of economic activity, that aims to measure

output in terms of goods and services exchanged in markets, national accounting omits

economically, socially and environmentally important non-market goods and services. From

an economic point of view, for example, the SNA disregards unpaid work that takes place at

home which might significantly skew the view of economic production and economic

growth (see e.g. Landefeld and McCulla 2000). Similarly, a number of ecosystem related

goods and services (e.g. soil formation, fish nursery grounds) that support economic activity

are invisible in the SNA in the sense that they are implicit, but not explicit in their

contribution to production (e.g. food production, fisheries). Other ecosystem related goods

and services are omitted from the SNA in different ways. Their role in supporting human

wellbeing is not explicitly recognized and while some can be included in the prices of other

goods and services (e.g. amenity value of landscapes increasing property prices or increased

tourism revenue in the area), in some cases their value is ignored altogether (e.g. the value

ascribed to an existence of endangered species or the carbon sequestration and storage value

of some vegetation covers). An underestimation of the role of the environment in economic

and other human activity contributes to inefficient management and potential environmental

degradation.

Recent efforts, especially the System of Environmental-Economic Accounting, Central

Framework and Experimental Ecosystem Accounting (SEEA CF6 and SEEA EEA) aim to

extend and integrate the national accounts for environmental and ecosystem assets.

Ecosystems are viewed as assets that contribute to SNA-measured economic activity, but

also as assets that generate economic and human activity outside of SNA’s current

measurement system. This extension might effectively allow a) understanding how much

economic activities are dependent and/or impact on environmental and ecosystems assets

and b) extending the measurement of national accounts to some ecosystem services that

5 We acknowledge that SNA includes the public services provides by Government (such as schooling, hospitals, defence and so

on). It breaks these down into collective and individual public goods. But valuation is on the basis of the cost of providing those

services. 6 SEEA CF refers to the report published by United Nations, European Commission, Food and Agricultural Organization of the

United Nations, International Monetary Fund, Organisation for Economic Co-operation and Development, The World Bank

(2014a) System of Environmental-Economic Accounting 2012 – Central Framework. United Nations, New York

Page 13 of 57

contribute to human wellbeing that were previously fully or partially missing in national

accounting (e.g. air and water purification provided by various vegetation types).

SNA and SEEA measure flows and stocks related to economic and human activity by

collecting, organising and reporting associated information. The SEEA’s major addition to

SNA is the collection of physical data related to environment and ecosystems and the

organisation of it in a coherent manner following SNA conventions. Employing the exchange

value concept it aims to monitor the value of flows over the accounting year and change in

the value of assets. It relies on the market prices of goods and services exchanged in the

markets; or the ‘assumed’ transaction prices for goods and service that have no market.

The extension of SNA to ecosystem related goods and services represents a welcome

start in broadening our measurement of “what matters” for sustainable development

decision making. The systematisation of physical data on ecosystem assets is likely to

support numerous possible analyses and evidence gathering beyond national accounting. In

particular, it might support further development of and facilitate the broader use of wealth

accounting.

Wealth accounting aims to address the limited scope of national accounts and GDP by

focusing on the changes in capital stocks that are reflecting the changes in overall wealth.

SNA does not allow a charge for depreciation of natural assets to be included in income and

production accounts. GDP was always meant to be used strictly as a measure of economic

production (e.g. UNU-IHDP and UNEP 2012).The inability of main indicator commonly

used to guide policy - GDP - to measure natural capital depreciation is seen by some as its

major shortcoming (e.g. Dasgupta 2009). A policy of maximising the rate of economic growth

may result in a decrease in overall wealth or human wellbeing. SNA accounts for the

depreciation of reproducible capital7, however it does not account for the depreciation of

natural or human capital. As such SNA is not fully suited to assess changes in the overall

wealth of countries, or to signal possible suboptimal development trajectories.

Wealth accounting aims to augment the current target indicator for economic policy,

GDP, by a measure of wealth that can evaluate the changes in capital assets that all add

together to build a country’s wealth. From this perspective, an economy’s wealth is

composed of reproducible capital (infrastructure, buildings and machines), natural capital

(renewable and non-renewable natural resources) and human capital (education and

health)8. The economic indicators should reflect a measure of this wealth that accounts for

the depreciations of all capital assets. In contrast to national accounting, wealth accounting

7 We acknowledge that the reliability of reproducible capital depreciation in SNA can be questioned.

8 Note that wealth accounting might tend to stress intangible wealth such as social and institutional capital, technology, etc.

Page 14 of 57

estimates the shadow prices of capital assets – which in this context translate as the

contribution of a marginal unit of the asset to human wellbeing (see section below for further

discussion on welfare or shadow prices).

Two main initiatives represent the current approaches to wealth accounting: the

comprehensive wealth approach of the World Bank9 (World Bank 2006, 2011) and The

Inclusive Wealth Report10 (UNU-IHDP and UNEP 2012). These two approaches provide

initial insights into the extended use of wealth accounting which can encompass the

construction of natural capital accounts.

Needless to say national and welfare accounting aim to provide measurement

approaches guided by different objectives (see also box below). While the former is focused

on measuring flows (economic activities), the latter aims to measure stock (wealth).

Measuring wealth is more difficult, but of significant importance and interest to decision

making - after all it is the stock of natural capital that underpins the flows of benefits from it.

SEEA EEA can be seen as a significant step from the SNA system towards comprehensive

wealth accounting. The latter, however, remains a complex and ambitious long term goal.

The Inclusive Wealth Index (IWI) for example requires a large amount of shadow price data

and in principle should include health and education among other things. Due to

computational difficulties health was not included in the index, despite its obvious

importance in wellbeing UNU-IHDEP-UNEP (2014). For a critique of the IWI and

suggestions for substitute information (e.g. sustainability limits linked to critical natural

capital assessments) see Roman and Thiry (2016).

9 In its approach, the World Bank accounts for exhaustible resources, renewable resources and agricultural land. The wealth

measure also includes intangible capital (raw labour, human capital, social capital and the quality of institutions). 10 This approach accounted for reproducible capital, human capital, knowledge, natural capital, population, institutions and

time.

Page 15 of 57

Box 1: Weak vs. strong sustainability

Related to the debate on which measurement system should underpin public decision

making is the long standing debate between supporters of weak and strong sustainability.

Assuming sustainability (i.e. non declining overall stock of different forms of capital), the

critical issue that the opponents in this debate is the degree to which natural capital is

substitutable for other forms of capital. The proponents of strong sustainability see some

components of natural capital (‘critical natural capital’) as non- substitutable and as such it

should be conserved and protected so that its overall stock is not decreasing over time.

Weak sustainability accepts depletion of natural capital, as far as this decrease is offset by

innovation and technical progress which increases efficiency of usage and/or the role of

other forms of capital. This paradigm is historically more broadly reflected in our society –

e.g. in land use change, such as transforming stocks of forests to agricultural production or

through use of fossil fuels to produce man made capital.

The two standpoints could be seen at the opposite sides of a spectrum of political and

philosophical positions stakeholders might take to the management of the environment.

What each person, company, country or organisation adopts as her/his/its worldview, is

likely to define the choice of measurement system to account for sustainable growth.

Further the positions held from this spectrum might be different for different aspects of

natural capital. For example, for some aspects of natural capital society/individuals can

hold a strong sustainability perspective (e.g. species and ecosystem protection under the

Habitat and Birds directive), but weak sustainability perspective for other aspects of

natural capital (e.g. converting some components of natural capital to infrastructure allows

increase in social capital in terms of mobility and economic growth). Indeed, it seems

important to consider carefully which components of natural capital society deem to be

substitutable and which not.

The standpoint on the weak vs strong sustainability would be reflected in the measurement

system one adopts. From the three approaches specified in section 2.1, Approach 3 (Wealth

Accounting) can, if feasible, provide a measurement framework that would allow

measurement of progress in strong sustainability terms. Approach 1 and 2 can provide

measurement frameworks for weak sustainability position, although Approach 2

information could also be used to impose ‘critical natural capital’ conservation rules and

regulations in line with strong sustainability.

Page 16 of 57

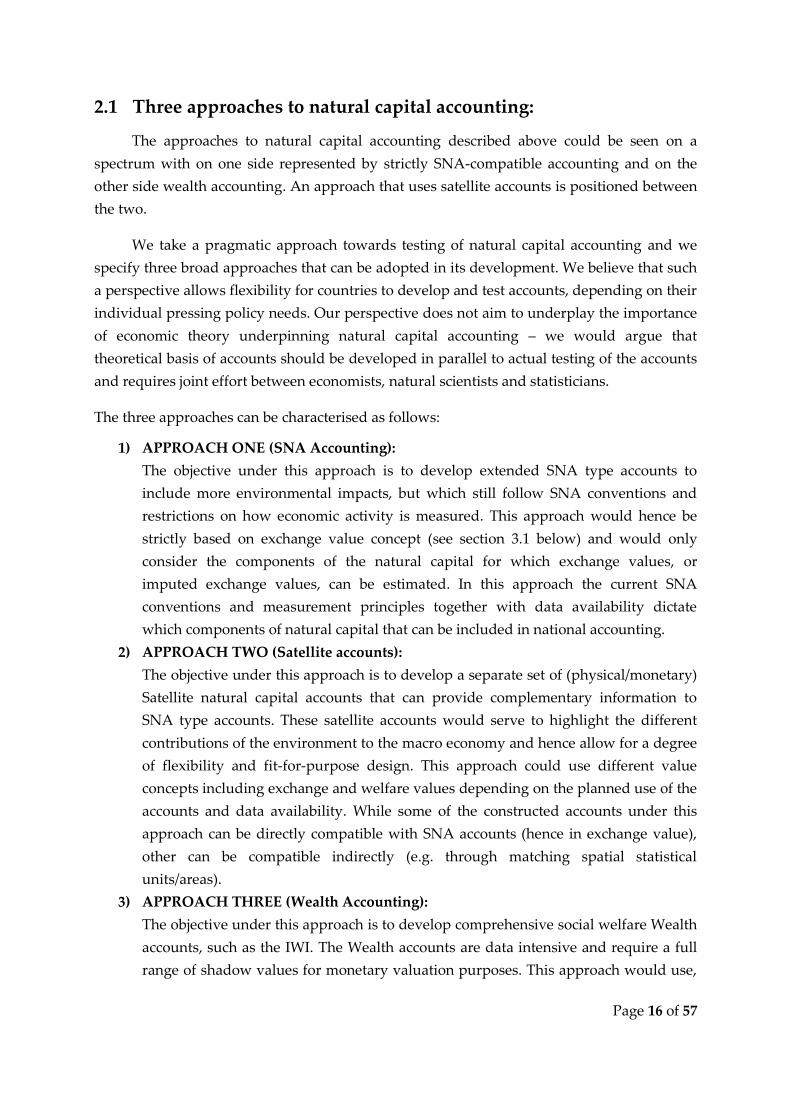

2.1 Three approaches to natural capital accounting:

The approaches to natural capital accounting described above could be seen on a

spectrum with on one side represented by strictly SNA-compatible accounting and on the

other side wealth accounting. An approach that uses satellite accounts is positioned between

the two.

We take a pragmatic approach towards testing of natural capital accounting and we

specify three broad approaches that can be adopted in its development. We believe that such

a perspective allows flexibility for countries to develop and test accounts, depending on their

individual pressing policy needs. Our perspective does not aim to underplay the importance

of economic theory underpinning natural capital accounting – we would argue that

theoretical basis of accounts should be developed in parallel to actual testing of the accounts

and requires joint effort between economists, natural scientists and statisticians.

The three approaches can be characterised as follows:

1) APPROACH ONE (SNA Accounting):

The objective under this approach is to develop extended SNA type accounts to

include more environmental impacts, but which still follow SNA conventions and

restrictions on how economic activity is measured. This approach would hence be

strictly based on exchange value concept (see section 3.1 below) and would only

consider the components of the natural capital for which exchange values, or

imputed exchange values, can be estimated. In this approach the current SNA

conventions and measurement principles together with data availability dictate

which components of natural capital that can be included in national accounting.

2) APPROACH TWO (Satellite accounts):

The objective under this approach is to develop a separate set of (physical/monetary)

Satellite natural capital accounts that can provide complementary information to

SNA type accounts. These satellite accounts would serve to highlight the different

contributions of the environment to the macro economy and hence allow for a degree

of flexibility and fit-for-purpose design. This approach could use different value

concepts including exchange and welfare values depending on the planned use of the

accounts and data availability. While some of the constructed accounts under this

approach can be directly compatible with SNA accounts (hence in exchange value),

other can be compatible indirectly (e.g. through matching spatial statistical

units/areas).

3) APPROACH THREE (Wealth Accounting):

The objective under this approach is to develop comprehensive social welfare Wealth

accounts, such as the IWI. The Wealth accounts are data intensive and require a full

range of shadow values for monetary valuation purposes. This approach would use,

Page 17 of 57

when possible, shadow prices and otherwise exchange and welfare values when

appropriate. From a strong sustainability policy point of view this is the most

desirable type of account but in practice it is proving difficult to meaningfully reflect

a comprehensive range of external costs and benefits with links to wellbeing.

The activities surrounding SEEA EEA and SEEA CF indicate that the future goal is an

integrated account (Approach one) - i.e. fully compatible SNA type accounts with an

extended production boundary.11 Other initiatives related to wealth accounting would be

further enabled by Approach two.

The three approaches are not mutually exclusive and it is foreseeable that efforts

within each approach could support each other. For example, the development of SEEA EEA

and SEEA CF might be useful for all three approaches. We would argue that each approach

has its advantages and disadvantages. Approach one would be compatible with a

historically used and significantly developed and tested accounting systems and practices.

At the same time this approach risks ignoring components of natural capital for which

exchange values cannot be derived; and/or might disregard some dimensions of natural

capital values that might be important (e.g. non-use values, broader welfare values of

ecosystems). Approach two’s main advantage is its flexibility and fit-for-purpose orientation

that allows use of different data and, in particular, range of existing valuation studies for

deriving monetary values for natural capital accounts. Its disadvantage is that as the set of

accounts becomes more comprehensive it becomes more difficult to derive indexes of

change, or to rank order indicators. The third approach is in principle the most suitable

measurement system for an assessment of the development process – in social, economic and

environmental terms. However it is also the most difficult approach in terms of meaningful

data/information – it requires difficult estimations of shadow prices and as comprehensive a

data set as possible on all three dimensions of progress.

A particularly divisive issue across the three approaches is the use of non-market

valuation. Vincent (2015) has made the case for incorporating non-market valuation directly

into the main national accounts. He uses environmental externality and public goods

concepts to argue that there is a transaction (in money terms) between economic agents

involved in the activities generating external effects. Therefore there is a basis for arguing for

the incorporation of non-market values into national accounts. It seems to us that in practice

this line of reasoning is similar to the use of production function data to generate values; and

11 Note that SEEA EEA (2017) explicitly recognise (see 2.10) that it might be possible or desirable to construct

accounts that, for example, adopt different valuation concepts to suit particular policy needs – in line with what

we describe as approach two.

Page 18 of 57

satellite accounts, it could be argued, allow more flexibility and range of coverage in terms of

environmental impacts and values.

We believe that thinking about the development of natural capital accounting in terms

of what the final objectives of the accounts will be might be helpful in facilitating more

experimentation and allow progress in natural capital accounting. Keeping the three

approaches listed in this section in mind, the next sections will discuss the valuation

methodologies and issues relevant to the KIP INCA.

Page 19 of 57

3 Valuation in/for Natural capital and Ecosystem

Accounting

Building on the discussion above, it is important to note that accounting relies on two

key concepts of stocks and flows, where stocks are measured at a specific point of time and

flows are measured over selected time period. Following the SEEA EEA conceptual

framework (see Figure below) the concept of stock translates to spatially delineated

ecosystem assets that produce flows of ecosystem services. Ecosystem accounting aims to

measure both flows of ecosystem services over an accounting period (usually an accounting

year) as well as to monitor changes in stocks of ecosystem assets.

Figure 1 General Ecosystem Accounting framework [Source: SEEA EEA]

Ecosystem services contribute to two types of benefits. Many ecosystem services are

already present in national accounts (e.g. crops, timber, some aspects of tourism/recreation)

and these are in SEEA EEA terms called SNA benefits. The inclusion of ecosystem services

contributing to the production of SNA benefits leads to increases in intermediate

consumption, but does not have any effect on the overall level of income/GDP. Ecosystem

services contribution to production of benefits that are not accounted for in SNA - Non-SNA

benefits – lead to an expansion in the measures of output and hence changes

(increases/decreases) in GDP.

The SEEA EEA envisions the following five ecosystem accounts:

Ecosystem extent account – physical terms

Page 20 of 57

Ecosystem condition account – physical terms

Ecosystem services supply and use account – physical terms

Ecosystem services supply and use account – monetary terms

Ecosystem monetary asset account – monetary terms

The five accounts could be considered as satellite accounts of the SNA, however they

do not depend on the SNA accounts for their compilation (SEEA EEA 2017). Recent

discussion have also raised a possibility to compile ecosystem capacity accounts (Hein et al.

2016, SEE EEA 2017).

Assuming available biophysical data from physical accounts, valuation techniques can

be employed to provide monetary ecosystem service accounts and monetary ecosystem asset

accounts. The valuation step is essential if an integration with the SNA is required.

However, the valuation of nature-related goods and services is one of the most contested

topics and is conditioned by the adoption of different weak or strong sustainability

worldviews (see Box above). The debate exposes profound differences and as such is far

from settled, including the choice of adequate valuation concept and methods (e.g. SEEA

EEA, Obst et al. 2015, SEEA EEA 201712). See the discussion of the appropriate valuation

concepts further below.

Single ecosystem service flows from ecosystem assets are valued using the most

appropriate techniques in light of available data. Note here that it is crucial to identify the

benefits/beneficiaries, since without the demand there are no benefits and hence no

ecosystem services. As such, actual service usages need to be identified to value the flows of

services over the accounting period. This also holds true for expected future use of

ecosystem services to estimate asset values where identification of patterns of use is of

crucial importance.

The identification of the actual use of services might differ across service types. For

example, most provisioning services’ usage will be reflected in increased extraction or output

quantities (e.g. food produced, timber harvested). In contrast, the usage (and value) of many

regulating and cultural services generally increase with the number of people in the relevant

area (e.g. flood protection, air and water purification or recreation).

The asset valuation in SEEA is expressed through the Net Present Value of Expected

Ecosystem Service flows from an ecosystem asset, assuming current consumption patterns.

However other theoretically possible approaches for asset valuation have also recently

12 SEEA EEA 2017 refers to the draft consultation report “SEEA Experimental Ecosystem Accounting: Technical

Recommendations” released on 6th March 2017 and developed by UNEP / UNSD / CBD project on Advancing Natural Capital

Accounting funded by NORAD.

Page 21 of 57

materialised (see later section). At this current stage, the focus of the KIP INCA is on

ecosystem service (flow) valuation.

3.1 Exchange and welfare value concepts

One of the contested topics in the context of valuation methods for natural capital

accounting has been the adequacy and relevance of the exchange value and welfare value

concepts. It has been argued that for SEEA EEA the chosen value concept can only be

exchange value, in order to allow integration of the values of stocks and flows related to the

man-made capital with the values of natural capital (e.g. SEEA, Obst et al 2015).

National accountants focus on exchange values or as Obst et al (2015) put it “the value

at which goods, services and assets are exchanged regardless of the prevailing market

conditions”. In the case of ecosystem services, for which markets often don’t exist, exchange

values essentially represent an assumed transaction between an ecosystem asset and

economic units, or “the monetary value of the ecosystems to economic production and

consumption” (SSE EEA 2017 6.59). In the figure below, the exchange value concept is

represented by producer surplus (area B) and cost of production (area C). This is equal to P*

times Q*, market price of a good/service and its consumed quantity. Using the exchange

value concept is convenient for national accounting as it allows consistent recording of

(assumed) transactions in national accounting, since the values for supply and use are the

same. At the same time, for most of the marketed goods the data is readily available. For

ecosystem services, most of which are not traded in the market, these values need to be

imputed (however, note that value imputation is already used for health, education or

intermediate financial services in the SNA).

In contrast, the welfare value concept and welfare analysis is related to the changes in

consumer surplus (area A), relative either to market or shadow price. The consumer surplus

area represents the difference between consumers’ full willingness to pay and the price they

actually pay which is typically smaller. For many policy analyses and decisions, it is the

welfare value concept that is of relevance. The welfare value concept underpins EU Cost

Benefit analyses guidelines (e.g. Sartori et al. 2014) and the majority of the studies analysing

the values of ecosystem services are based on the shadow or welfare value concept.

Page 22 of 57

Figure 2: Supply and Demand for ecosystem related goods and services

We argue that some degree of pragmatism is reasonable when choices are made on

valuation methods and estimates. It is our opinion that while the exchange value concept is

relevant for national accounting purposes, it should not be the only consideration for the EU

natural capital accounts. The choice of valuation approach and methods is dictated by the

aim of natural capital assessment (see SEEA EEA 2017). So if the sole purpose of constructing

natural capital accounts in the EU is to integrate the ecosystem values with SNA, it might be

necessary to only use the exchange value concept (e.g. Obst et al. 2015). But other accounting

practice options might be considered, especially if the ‘new’ accounts are satellites to the

main national accounts and the primary aim is to highlight the contribution of the

environment (ecosystems) to economic progress. Similarly, some accounts might serve a

specific policy goal and hence need a broader concept of value (e.g. assessment of the

contribution of national parks to societal welfare).

As a practical example UK ONS (2017) suggests that in situations where the exchange

values cannot be imputed it might be feasible to use welfare values, assumed as exchange

values (i.e. retaining use and supply values). This would provide an overestimation of the

exchange value and would need to be clearly noted in the accounts construction. Further, in

cases where the difference between the two value concepts might be significant, it could be

useful to attempt to report both value types, however how this could practically be achieved

would need to be clarified (ibid). We would argue that rather than assuming welfare values

as exchange values it would be perhaps more useful and transparent to produce satellite

accounts which, by definition, can be more flexible in terms of what values can be

incorporated. The goal of the satellite accounts would in this context be to emphasise the

contribution of environmental assets and services to economic development/progress, as

well as to give some signals on sustainability.

Page 23 of 57

The information organised and collected in the physical and monetary accounts could

also be used for purposes other than national accounting, such as policy evaluation,

management decisions or advocacy purposes. For example, Costs Benefit Analyses that

underpin a number of key EU policies and programmes (e.g. investment projects within

cohesion policy 2014-2020) use welfare value for assessments. Further, it might be of interest

to policy makers to develop wealth accounting in order to assess its progress in

sustainability. In this case, exchange values are augmented by shadow prices of natural

capital assets13.

What distinguishes actual exchange value is that it does not assume any institutional

arrangement by accepting the institutional arrangement in which the transaction took place.

As Atkinson and Obst (2016) note this is not a neutral position, since accounting does not

make any judgement about what the institutional arrangement should be. As such, using

both exchange and welfare values in satellite accounts derived under different institutional

arrangement can help to measure progress towards (desired) policy targets.

Ecosystem services are in many cases associated with non-use values. People may

value the continued existence of species and ecosystems for themselves, for others or for

future generations (i.e. existence, altruistic and bequest values, respectively). This component

of value might in some cases be significant. It is not yet clear how to capture non-use value

within an accounting system, as these values are generally captured through methods based

on the welfare value concept and stated preference valuation methods reliant on surveys14.

Given that the current stage in the EU natural capital accounting process is

experimental, we believe different approaches are still open for debate and should be

explored in a pragmatic process. However, it is also expected that the policy utility focused

work stream in this project (prepared by IEEP) is likely to shed more light on the policy

demands for the KIP INCA outputs which might help to select appropriate value concepts

and valuation methods.

3.1.1 Simulated exchange values

An emerging method of simulated exchange values potentially provides an

opportunity for using stated preference methods to derive exchange values. Caparrós et al

(2003) proposed the method and Caparrós et al (2015) further describe this method and

13 In a perfect competitive market, we acknowledge that exchange and shadow value for accounting purposes will be the same

as the marginal value that will be P*. However, we argue that markets or quasi-markets for ESs are far from “perfect”. 14 More fundamentally, the issue about the incorporation non-use values might be about the physical accounting units to use for

multiplying the potential estimated price.

Page 24 of 57

apply it to free access recreation services in Spain. The method estimates demand for a

service, using non-market valuation methods, and models the whole market - the demand

against the supply of a service under different market structures. In their application,

Caparrós et al (2015) derive the demand function from a stated preference survey and for the

supply curve of the service they survey public servants for an understanding of the cost

associated with the provision of free access recreation. The exchange value/price can then be

found at the intersection between the demand and supply curves.

A lack of research is available related to this approach to make it truly operational.

Further work is required to explore to what extend the method provides an option to use

existing evidence from stated preference literature to derive values compatible with the

exchange value concept and national accounts. Further, it is important to consider the efforts

related to understanding the supply of the services as well as the assumptions used in

implementing this method (e.g. assumptions related to the shape of the demand function).

From our view, as of yet, this approach either requires a number of bold assumptions or very

detailed dataset and/or effort in survey on the demand and supply for the service.

3.2 Valuing flows – ecosystem services

Valuing flows in the context of extending or/and integrating natural capital into SNA,

implies valuing final ecosystem services. While the biophysical definition of ESs often refers

to provision, regulating, cultural (e.g. CICES15) and supporting (MA 2005) services this

classification needs to be further adapted for economic assessment (e.g. Fisher and Turner

2008). There are flows of ecosystem service between ecosystem assets (i.e. intermediate or

supporting ecosystem services), but for the construction of monetary ecosystem services

accounts, only final ecosystem services should be accounted for and valued, otherwise

double counting might occur (Fisher et al. 2009).

Nevertheless, recent discussions have highlighted the need to account for the

intermediate ecosystem services (functions) in order to understand interdependencies

between ecosystem assets and to answer particular policy questions (e.g. SEEA EEA 2017

1.71, 1.72; 5.40 - 5.43). Indeed valuing intermediate ecosystem services can provide valuable

information for cost effectiveness and other management decisions (e.g. restoration of

ecosystems, conservation interventions etc.), but it is essential that the intermediate and final

services are clearly distinguished. Only final ecosystem services can be the focus of the

ecosystem use and supply accounts in the SNA/SEEA EEA or double counting can occur.

15 The Common International Classification of Ecosystem Services (CICES) – see https://cices.eu/

Page 25 of 57

Satellite accounts can be used to highlight the contribution of intermediate ecosystem

services that are valuable for the functioning of natural capital which produces the final

ecosystem services outcomes which are already accounted for in the SNA (e.g. pollination

for agricultural production). There may also be cost-effectiveness decision making contexts

in which it is valid to compare an ecosystem service alternative with a man-made capital

facility i.e. comparing natural wetland water purification with the construction of a treatment

plant, given an institutional context in which water quality legal standards are in force.

At the EU level, valuing chosen ecosystem services will depend on the data available

and the goal of the particular account(s). As discussed above, different valuation concepts

might be relevant in light of the goal the account should serve.

The valuation methods that can be used in the context of SEEA EEA (i.e. based on

exchange value concept) are classified in:

Market-based or cost-based methods

Unit resource rent

Production function, cost function and profit function methods

Replacement cost

Damage costs or defensive expenditure

Averting behaviour

Payment for Ecosystem Services (PES) schemes

Revealed Preference methods

Hedonic pricing

Marginal values from travel cost demand functions (simulated exchange)

Whether the intention of accounting is to complement/extent SNA with satellite

information, or to move to wealth accounting other valuation methods can be considered,

such as:

Stated Preference methods

Contingent Valuation

Choice experiment

Extensive literature is available on the theory and application of methods in context of

valuing preferences for ecosystem related goods and services and we recommend these for

Page 26 of 57

further detail16. In the following sub section we will focus on the specifics of valuation

methods for natural capital accounting.

Many of the methods listed above require extensive data and statistical expertise (e.g.

hedonic pricing), existing markets (e.g. PES); or detailed biophysical/scientific understanding

(e.g. Production function) to make the method practically applicable. Use of existing

valuation results, particularly for the KIP INCA project, might be needed.

In the case of market-based price values, usage should be conditioned by the

prevailing institutional arrangements (e.g. degree of competition in the market), and should

not include non-ecosystem inputs (reproducible man-made capital).

Resource rent approaches (which is estimated as the difference between the benefit

price and the unit costs of labour, produced assets and intermediate inputs) are most suited

to so-called provisioning ecosystem services but again much depends on the prevailing

market structures (e.g. subsidies might obscure the “true” exchange value). Another

potential approach would be to try to discern a production function and the contribution to

it made by an ecosystem service (typically provisioning and some regulating services).

Physical science and data gaps, and the existence of non-market values can complicate any

production function estimation. Given a pragmatic strategy, a possible alternative proxy

approach could be replacement costs or damage costs methods. The complications with this

proxy approach include the correct identification of the beneficiaries, and their actual

incurred costs. In other cases, avertive behaviour purchasing (or defensive costs) may

provide useful value estimates.

Hedonic pricing methods (which generally look at the variation in housing prices to

assess the value of local environmental attributes) are linked to market-based transactions

but require large data sets with spatial variation. Further it is sometimes difficult to

disentangle the ‘bundle’ of ecosystem services that may be represented by for example

residential property prices.

Travel cost methods (which use travel expenditures to a site/good, in terms of financial

and time costs, to assess good/site’s value) have been greatly refined over the years due to

the increased use and capability of Geographical Information Systems (GIS). However the

values they yield include welfare value (time) and other components which are already

included in national accounts. An alternative proxy approach could be to rely instead on raw

16 See e.g. Badura et al (2016) (available for download) for a short overview, Bateman et al (2011) for theory and

policy context for ecosystem service assessments and Freeman et al (2014) for a thorough theoretical and practical

discussion of valuation methods.

Page 27 of 57

travel cost (mean or median) data from surveys perhaps differentiated by day trip and

longer stay visits. In cases where there is an entry price to the facility/area this is a

willingness to pay measure. In satellite accounts travel cost measures could provide useful

supplementary information highlighting the contribution of the ecosystem service

(recreation) to among other things human wellbeing.

Stated preference methods (contingent valuation or choice experiments) based on

participant surveys (where individuals provide answers about choices related to

environmental change or their willingness to pay for any such changes), are the best option

for non-use values related to feasible transactions. However, care needs to be taken since

these methods are often based on the welfare value concept, although they can be designed

to capture only market based values. They may also have a role to play as a cross checking

device.

Recent discussions and literature (Freeman et al 2013, SEEA EEA 2017, Atkinson and

Obst 2016) have highlighted the possible usefulness of looking at the economic channels

through which ecosystem services affect human wellbeing. This categorisation recognises

three broad ecosystem service types:

ES#1, intermediate services which input in the production system along with

other producing factors

ES#2, final/intermediate ecosystem services which provide benefits to

households as complementary (or substitute) of marketed goods and services

ES#3, final ecosystem services which directly contribute to household

wellbeing.

This distinction can be useful for classifying methods for ecosystem service valuation

in a manner that is relevant to national accounting thinking, due to its explicit consideration

of users of the services. .Building on the discussion in section 2 of the report, we indicate the

links between service users and the three broad approaches to natural capital accounting:

1) Approach 1: development of SNA compatible natural capital accounts that will fully

follow SNA conventions and restrictions on what the accounts measure and how.

2) Approach 2: development of Satellite natural capital accounts that can provide

complementary information to SNA accounts and hence allow certain flexibility and

fit-for-purpose design, including use of different value concepts.

3) Approach 3: development of comprehensive Wealth accounts. Requiring an

extensive range of shadow pricing and wellbeing information.

Under Approach 1: ES1 services such as waste disposal and water quality, have values

that are implicitly encompassed within economic production and as such are already

included in SNA accounts. But valuation via exchange prices and production functions

Page 28 of 57

could add to information on the service’s contribution to final services. ES2 benefits fall into

two sub categories, in the first households purchase a good which has an ecosystem service

level condition associated with it e.g. local air quality or amenity. This group is already

included in SNA accounts via for example the property market. The second sub category

households choose a level of ecosystem service through their purchase of a complementary

market good, for e.g. recreation valued by travel costs and these will add to conventional

GDP. Finally ES3 services, non-use services, are excluded from SNA accounts because

exchange values are not available, only stated preference methods can be used in this

context.

Under Approach 2: all three ES1, ES2 and ES3 services could be quantified and valued

directly, or their supply contribution to final services assessed. Under Approach 3: some

variant of an inclusive wealth index would seek to encompass all the service categories and

other wellbeing components such as health and education.

Table 1 provides different perspectives on the methods that can be used for natural

capital accounting in light of the three strategic (1, 2 and 3) approaches to natural capital

accounting. It provides examples of methods that can be potentially used for valuing

individual ecosystem service flows within the context of KIP INCA. Please note that further

detail on this is to be explored in light of testing of the approaches over the course of KIP

INCA actions, and that the entries in the table are subject to further assessment. Table 2

provides examples of valuation methods that can be used to assess ESs considered by JRC.

Table 1: Valuation methods for different ESs accounting strategies

Category Explanation

from economic

perspective

Examples of

ecosystem

services

Link to national

accounting perspective

Valuation

methods for

integration

SNA

Valuation methods

for supplementation

of SNA with satellite

accounts

Valuation methods

for wealth accounting

ES#1 ESs as input to

economic

production

Nutrient cycling,

water regulation,

water

purification, crop

pollination

Value of ecosystem

service is implicit in the

value of economic

production as

measured in standard

national accounts (e.g.

in conventional GDP).

Market/cost-based

methods (e.g.

production function,

avoided costs)

No extra methods

required

ES#2 ESs as joint

inputs to final

consumption

Amenity value,

purified air,

recreational

activities, flood

protection

Some values of

ecosystem service are

already reflected in

household

consumption as

measured in standard

national accounts (e.g.

in conventional GDP)

others provided

extended benefits (non-

SNA benefits).

Market/cost-

based methods

(e.g. production

function)

Revealed Preference

methods or

market/cost-based

methods (e.g. hedonic

pricing in property

markets, travel cost,

damage costs)

Stated Preference

methods such as

contingent valuation,

(discrete) choice

experiment

ES#3 ESs as direct

input to

households

wellbeing

Carbon storage Value of ecosystem

service is not associated

with any purchase of a

market good

Simulated

Exchange

values

Simulated Exchange

values or stated

preference methods

Stated Preference

methods such as

contingent valuation,

(discrete) choice

experiment [Source: Adapted from Freeman et al. 2013 and Atkinson Obsts 2016]

Page 30 of 57

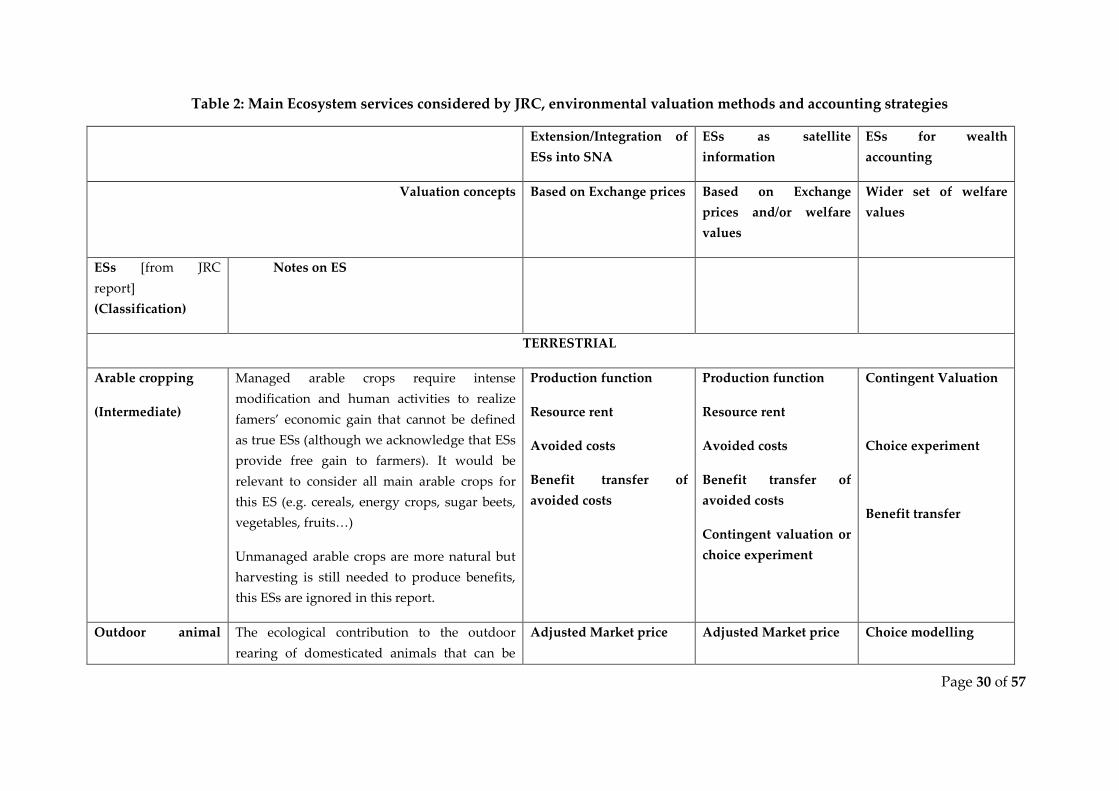

Table 2: Main Ecosystem services considered by JRC, environmental valuation methods and accounting strategies

Extension/Integration of

ESs into SNA

ESs as satellite

information

ESs for wealth

accounting

Valuation concepts Based on Exchange prices Based on Exchange

prices and/or welfare

values

Wider set of welfare

values

ESs [from JRC

report]

(Classification)

Notes on ES

TERRESTRIAL

Arable cropping

(Intermediate)

Managed arable crops require intense

modification and human activities to realize

famers’ economic gain that cannot be defined

as true ESs (although we acknowledge that ESs

provide free gain to farmers). It would be

relevant to consider all main arable crops for

this ES (e.g. cereals, energy crops, sugar beets,

vegetables, fruits…)

Unmanaged arable crops are more natural but

harvesting is still needed to produce benefits,

this ESs are ignored in this report.

Production function

Resource rent

Avoided costs

Benefit transfer of

avoided costs

Production function

Resource rent

Avoided costs

Benefit transfer of

avoided costs

Contingent valuation or

choice experiment

Contingent Valuation

Choice experiment

Benefit transfer

Outdoor animal The ecological contribution to the outdoor

rearing of domesticated animals that can be

Adjusted Market price Adjusted Market price Choice modelling

Page 31 of 57

husbandry

(Intermediate)

used for the production of food. The outdoor

rearing of animal provides higher organoleptic

properties of food and better quality of life to

animals.

Replacement costs

Resource rent

Replacement costs

Resource rent

Contingent valuation or

choice experiment

Benefit transfer

Timber

(Final)

The ecological contribution to the growth of

tree for timber production.

Adjusted Market price

Resource rent

Crop pollination

(Intermediate)

Movement of floral gametes for reproduction

of plants thanks to wild bees and pollinators.

Production function

Replacement costs

Adjusted Market price

Production function

Replacement costs

Adjusted Market price

Contingent valuation or

choice experiment

Contingent valuation

Choice experiment

Benefit transfer

Erosion control

(Final)

Retention of soil within an ecosystem Avoided costs

Replacement costs

Benefit transfer of

avoided costs

Avoided costs

Replacement costs

Contingent valuation or

choice experiment

Hedonic price

Contingent valuation

Choice experiment

Benefit transfer

Outdoor recreation

(Final)

The natural amenities which provide recreation

opportunities for human beings.

Resource rent

Production function

Resource rent

Production function

Contingent valuation or

Contingent valuation

Choice experiment

Page 32 of 57

choice experiment

Travel cost or hedonic

price

Travel cost

Benefit transfer

MARINE

Marine fish

(Final)

Wild fish species that can be harvested and

used as food. Harvesting is still needed to

produce benefits out of this ESs.

Adjusted Market price

Residual Resource rent

Adjusted Market price

Residual Resource rent

Contingent valuation or

Choice experiment

Travel cost

Benefit transfer

Choice modelling

Contingent valuation

Travel cost

Benefit transfer

FRESHWATER

Water purification

(Intermediate/Final)

Removal or breakdown of excess nutrients of

compounds in water

Replacement costs

Resource rent

Payment for ecosystem

services

Contingent valuation

Choice modelling

Fiscal instruments

Payment for ecosystem

services

Benefit transfer

Contingent valuation

Choice experiment

Benefit transfer

Page 33 of 57

Water provisioning

(Intermediate)

The provision of water flow for human uses

can produce several benefits (e.g. bottle water)

Adjusted Market price

Resource rent

Payment for ecosystem

services

Replacement cost

Adjusted Market price

Resource rent

Payment for ecosystem

services

Replacement cost

Contingent valuation or

choice experiment

Contingent valuation

Choice experiment

Benefit transfer

Flood control

(Intermediate)