Vaish Associates - ICSI - The Institute of Company Secretaries of India · SEBI or an Investment...

39

Vaish Associates © Vaish Associates

-

Upload

truonghanh -

Category

Documents

-

view

217 -

download

0

Transcript of Vaish Associates - ICSI - The Institute of Company Secretaries of India · SEBI or an Investment...

Vaish Associates

© Vaish Associates

© Vaish Associates

© Vaish Associates

© Vaish Associates

© Vaish Associates

As per section 2 (m) of the As per section 2 (m) of the Regulations, Regulations, ““Joint VentureJoint Venture””means a foreign entity formed, means a foreign entity formed, registered or incorporated in registered or incorporated in

accordance with the accordance with the regulations of the host country regulations of the host country

in which the Indian party in which the Indian party makes a direct investment.makes a direct investment.

© Vaish Associates

In terms of Regulation 4 of the Notification, general permissionIn terms of Regulation 4 of the Notification, general permission has has been granted to persons residents in India for purchase / acquisbeen granted to persons residents in India for purchase / acquisition of ition of securities in the following manner :securities in the following manner :

(i)(i)out of the funds held in RFC account; out of the funds held in RFC account; (ii)(ii)as bonus shares on existing holding of foreign currency shares; as bonus shares on existing holding of foreign currency shares; andand(iii)(iii)when not permanently resident in India, out of their foreign when not permanently resident in India, out of their foreign currency resources outside India.currency resources outside India.

General permission is also available to sell the shares so purchGeneral permission is also available to sell the shares so purchased or ased or acquired.acquired.

© Vaish Associates

© Vaish Associates

© Vaish Associates

The ceiling of 400 per cent of net worth will not be applicable The ceiling of 400 per cent of net worth will not be applicable where the investment where the investment

is made out of balances held in Exchange Earnersis made out of balances held in Exchange Earners‘‘ Foreign Currency account of the Foreign Currency account of the

Indian party or out of funds raised through Indian party or out of funds raised through ADRs/GDRsADRs/GDRs..

The above ceiling of 400 percent includes contribution to the cThe above ceiling of 400 percent includes contribution to the capital of the overseas apital of the overseas

JV/WOS, loan granted to the JV/WOS and 100 percent of the guaranJV/WOS, loan granted to the JV/WOS and 100 percent of the guarantees (other than tees (other than

performance guarantees) and 50 per cent of the amount of performperformance guarantees) and 50 per cent of the amount of performance guarantees. ance guarantees.

Indian parties are prohibited from making investment in a foreigIndian parties are prohibited from making investment in a foreign entity engaged in n entity engaged in

real estate (meaning buying and selling of real estate or tradinreal estate (meaning buying and selling of real estate or trading in Transferable g in Transferable

Development Rights (Development Rights (TDRsTDRs) but does not include development of townships, ) but does not include development of townships,

construction of residential/commercial premises, roads or bridgeconstruction of residential/commercial premises, roads or bridges) or banking s) or banking

business, without the prior approval of the Reserve Bank.business, without the prior approval of the Reserve Bank.

© Vaish Associates

Valuation of the shares of the foreign company shall beValuation of the shares of the foreign company shall beIn case of partial / full acquisition of an existing foreign comIn case of partial / full acquisition of an existing foreign company, where pany, where the investment is more than USD 5 million, valuation of the sharthe investment is more than USD 5 million, valuation of the shares of the es of the company shall be made by a Category I Merchant Banker registeredcompany shall be made by a Category I Merchant Banker registered with with SEBI or an Investment Banker / Merchant Banker outside India regSEBI or an Investment Banker / Merchant Banker outside India registered istered with the appropriate regulatory authority in the host country; awith the appropriate regulatory authority in the host country; and, in all nd, in all other cases by a Chartered Accountant or a Certified Public Accoother cases by a Chartered Accountant or a Certified Public Accountant.untant.In cases of investment by way of swap of shares, irrespective ofIn cases of investment by way of swap of shares, irrespective of the the amount, valuation of the shares will have to be made by a Categoamount, valuation of the shares will have to be made by a Category I ry I Merchant Banker registered with SEBI or an Investment Banker outMerchant Banker registered with SEBI or an Investment Banker outside side India registered with the appropriate regulatory authority in thIndia registered with the appropriate regulatory authority in the host e host country. Approval of the Foreign Investment Promotion Board (FIcountry. Approval of the Foreign Investment Promotion Board (FIPB) will PB) will also be a prerequisite for investment by swap of shares.also be a prerequisite for investment by swap of shares.

© Vaish Associates

© Vaish Associates

The Indian party / entity may extend loan / guarantee only to anThe Indian party / entity may extend loan / guarantee only to an overseas overseas JV/ WOS in which it has equity participation.JV/ WOS in which it has equity participation.No guarantee should be 'open ended' i.e. the amount and period oNo guarantee should be 'open ended' i.e. the amount and period of the f the guarantee should be specified upfront.guarantee should be specified upfront.As in the case of corporate guarantees, all guarantees (includinAs in the case of corporate guarantees, all guarantees (including g performance guarantees) are required to be reported to the Reserperformance guarantees) are required to be reported to the Reserve Bank, ve Bank, in Form ODIin Form ODI--Part II.Part II.Specific approval of the Reserve Bank will be required for creatSpecific approval of the Reserve Bank will be required for creating ing charge on immovable property and pledge of shares of the Indian charge on immovable property and pledge of shares of the Indian parent/ parent/ group companies in favour of a nongroup companies in favour of a non-- resident entity.resident entity.In cases where invocation of the performance guarantees breach tIn cases where invocation of the performance guarantees breach the he ceiling for the financial exposure of 400 per cent of the net woceiling for the financial exposure of 400 per cent of the net worth of the rth of the Indian Party, the Indian Party shall seek the prior approval of Indian Party, the Indian Party shall seek the prior approval of the the Reserve Bank before remitting funds from India, on account of suReserve Bank before remitting funds from India, on account of such ch invocation.invocation.

Indian Parties are permitted to issue Indian Parties are permitted to issue corporate guarantees on behalf of their corporate guarantees on behalf of their first level step down operating JV /WOS first level step down operating JV /WOS set up by their JV / WOS operating as a set up by their JV / WOS operating as a Special Purpose Vehicle (SPV) under Special Purpose Vehicle (SPV) under the Automatic Route the Automatic Route –– Subject to the Subject to the extent limit for ODIextent limit for ODIFurther, the issuance of corporate Further, the issuance of corporate guarantee on behalf of second generation guarantee on behalf of second generation or subsequent level step down operating or subsequent level step down operating subsidiaries will be considered under the subsidiaries will be considered under the Approval Route (provided Indian Party Approval Route (provided Indian Party holds 51% or more stake in the overseas holds 51% or more stake in the overseas subsidiary)subsidiary)

© Vaish Associates

© Vaish Associates

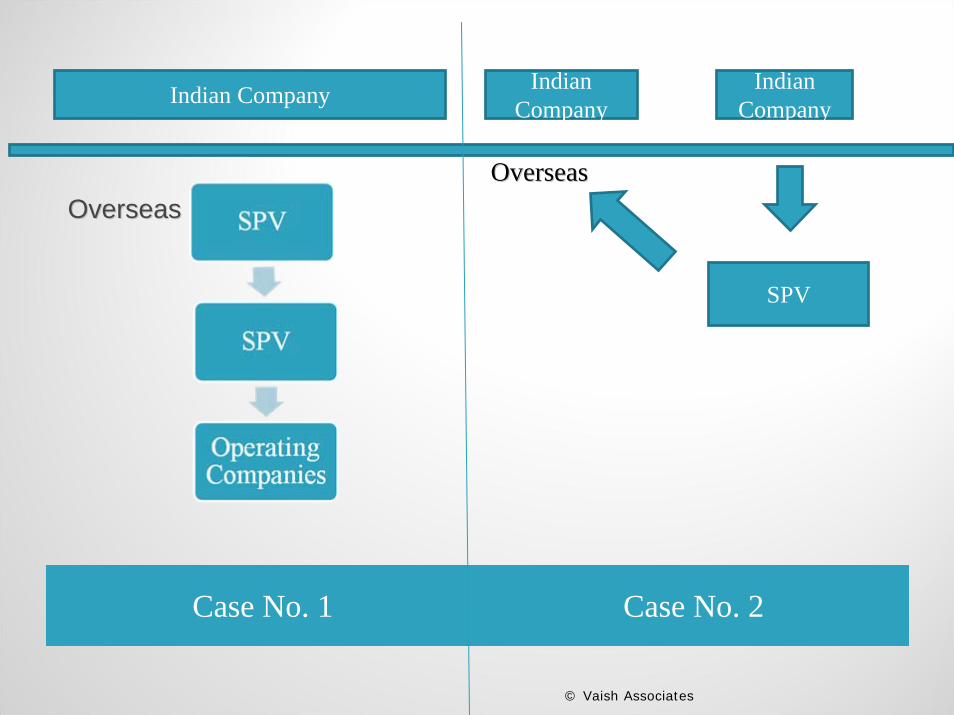

Case No. 1 Case No. 2

OverseasOverseasOverseasOverseas

© Vaish Associates

Indian Company Indian Company

Indian Company

SPV

Investments in unincorporated entities overseas in the oil sectoInvestments in unincorporated entities overseas in the oil sector (i.e. for r (i.e. for exploration and drilling for oil and natural gas, etc.) by exploration and drilling for oil and natural gas, etc.) by

(i)(i) NavaratnaNavaratna PSUsPSUs, ONGC , ONGC VideshVidesh Ltd.(OVLLtd.(OVL) and Oil India ) and Oil India Ltd.(OILLtd.(OIL) may be ) may be permitted by AD Category permitted by AD Category -- I banks, without any limit, I banks, without any limit,

(ii)(ii) by other Indian companies (up to 400 per cent of their net worthby other Indian companies (up to 400 per cent of their net worth duly supported duly supported by certified copy of the Board resolution approving such investmby certified copy of the Board resolution approving such investment).ent).Provided such investments are approved by the competent Provided such investments are approved by the competent authority.authority.

Capitalization of exports and other dues.Capitalization of exports and other dues.Indian party is permitted to Indian party is permitted to capitalisecapitalise the payments due from the foreign entity the payments due from the foreign entity towards exports, fees, royalties or any other dues from the foretowards exports, fees, royalties or any other dues from the foreign entity for ign entity for supply of technical knowsupply of technical know--how, consultancy, managerial and other services how, consultancy, managerial and other services within the ceilings applicable. within the ceilings applicable. CapitalisationCapitalisation of export proceeds remaining of export proceeds remaining unrealisedunrealised beyond the prescribed period of realization will require prior beyond the prescribed period of realization will require prior approval of the Reserve Bank.approval of the Reserve Bank.

© Vaish Associates

In terms of Regulation 7 an Indian party In terms of Regulation 7 an Indian party seeking to make investment in an entity seeking to make investment in an entity outside India, which is engaged in the outside India, which is engaged in the financial sector, should fulfill the following financial sector, should fulfill the following additional conditions:additional conditions:

(i)(i)be registered with the regulatory authority in be registered with the regulatory authority in India for conducting the financial sector India for conducting the financial sector activities;activities;

(ii)(ii)has earned net profit during the preceding three has earned net profit during the preceding three financial years from the financial services financial years from the financial services activities;activities;

(iii)(iii)has fulfilled the prudential norms relating to has fulfilled the prudential norms relating to capital adequacy; and capital adequacy; and

(iv)(iv)has obtained approval from the regulatory has obtained approval from the regulatory authorities concerned both in India and abroad authorities concerned both in India and abroad for venturing into such financial sector activity.for venturing into such financial sector activity.

© Vaish Associates

Additional Investments by a JV/ WOS Additional Investments by a JV/ WOS or its step down subsidiary will also have or its step down subsidiary will also have to comply with the above conditions.to comply with the above conditions.

Regulated entities in the financial sector Regulated entities in the financial sector making investments in any activity making investments in any activity overseas are required to comply with the overseas are required to comply with the above guidelines.above guidelines.

Unregulated entities in the financial Unregulated entities in the financial services sector in India may invest in non services sector in India may invest in non financial sector activities subject to financial sector activities subject to compliance with the provisions of compliance with the provisions of Regulation 6.Regulation 6.A company not complying with A company not complying with

Regulation 7 needs to seek express Regulation 7 needs to seek express approval of RBI for every remittance, approval of RBI for every remittance, loan or guarantee made to WOS/JV. loan or guarantee made to WOS/JV.

© Vaish Associates

The July, 2011 Circular has introduced The July, 2011 Circular has introduced three important provisions with respect to three important provisions with respect to NBFCsNBFCs registered with the RBI.registered with the RBI.

(i)(i)Investment in nonInvestment in non--financial service financial service sectors shall not be permitted.sectors shall not be permitted.(ii)(ii)Overseas investment should not Overseas investment should not involve multi layered, cross jurisdictional involve multi layered, cross jurisdictional structures and at most only a single structures and at most only a single intermediate holding entity shall be intermediate holding entity shall be permittedpermitted.(iii)(iii)In case of opening of subsidiary abroad, In case of opening of subsidiary abroad, the parent NBFC shall not be permitted to the parent NBFC shall not be permitted to extend implicit or explicit guarantee to or extend implicit or explicit guarantee to or on behalf of such subsidiaries; and on behalf of such subsidiaries; and ……..

© Vaish Associates

(iii) In case of subsidiary, it should not In case of subsidiary, it should not be a shell company be a shell company i.ei.e "a company that "a company that is incorporated, but has no is incorporated, but has no significant assets or operations." significant assets or operations." However companies undertaking However companies undertaking activities such as financial activities such as financial consultancy and advisory services consultancy and advisory services with no significant assets shall not with no significant assets shall not be considered as shell companies;be considered as shell companies;

(iv) The aggregate overseas investment (iv) The aggregate overseas investment should not exceed 100% of the should not exceed 100% of the NoFNoF. . The overseas investment in a single The overseas investment in a single entity, including its step down entity, including its step down subsidiaries, by way of equity or subsidiaries, by way of equity or fund based commitment shall not be fund based commitment shall not be more than 15% of the more than 15% of the NBFC'sNBFC's owned owned funds.funds.

© Vaish Associates

© Vaish Associates

Listed Indian companies are permitted to invest up to 50 per ceListed Indian companies are permitted to invest up to 50 per cent of their nt of their net worth in (i) shares and (ii) bonds / fixed income securitiesnet worth in (i) shares and (ii) bonds / fixed income securities ( rated not ( rated not below investment grade) issued by listed overseas companies.below investment grade) issued by listed overseas companies.

Mutual Funds are registered with SEBI are permitted to invest wiMutual Funds are registered with SEBI are permitted to invest within an thin an overall cap of USD 7 billion in overall cap of USD 7 billion in ADRsADRs/ / GDRsGDRs, equities of overseas , equities of overseas companies listed in recognized stock exchanges, money market companies listed in recognized stock exchanges, money market instruments etc.instruments etc.

A limited number of qualified Indian Mutual Funds, are permittedA limited number of qualified Indian Mutual Funds, are permitted to to invest cumulatively up to USD 1 billion in overseas Exchange Trainvest cumulatively up to USD 1 billion in overseas Exchange Traded ded Funds as may be permitted by SEBI.Funds as may be permitted by SEBI.

Domestic Venture Capital Funds registered with SEBI may invest iDomestic Venture Capital Funds registered with SEBI may invest in n equity and equity linked instruments of offequity and equity linked instruments of off--shore Venture Capital shore Venture Capital Undertakings, subject to an overall limit of USD 500 million.Undertakings, subject to an overall limit of USD 500 million.

Prior approval of the Reserve Prior approval of the Reserve Bank would be required in all other Bank would be required in all other cases of direct investment abroad.cases of direct investment abroad.

For this purpose, application For this purpose, application together with necessary documents together with necessary documents should be submitted in Form ODI should be submitted in Form ODI through their through their AuthorisedAuthorised Dealer Dealer Category Category –– I banks. I banks.

RBI should take into account the RBI should take into account the prima facie viability of the JV/ WOS prima facie viability of the JV/ WOS abroad, contribution to external abroad, contribution to external trade and other benefits, financial trade and other benefits, financial position and business track records position and business track records of the Indian party and its expertise of the Indian party and its expertise etc. etc.

© Vaish Associates

PProprietorship concerns and roprietorship concerns and unregistered partnership firms are unregistered partnership firms are allowed to set up JVs / WOS outside allowed to set up JVs / WOS outside India with the prior approval of the India with the prior approval of the Reserve Bank subject to satisfying Reserve Bank subject to satisfying certain eligibility criteria mentioned in certain eligibility criteria mentioned in the Regulations.the Regulations.Registered Trusts and Societies Registered Trusts and Societies

engaged in manufacturing / educational engaged in manufacturing / educational / hospital sector are allowed to make / hospital sector are allowed to make investment in the same investment in the same sector(ssector(s) in a ) in a JV/WOS outside India, with the prior JV/WOS outside India, with the prior approval of the Reserve Bank, after approval of the Reserve Bank, after satisfying the eligibility criteria satisfying the eligibility criteria mentioned in the Regulations.mentioned in the Regulations.

© Vaish Associates

A JV / WOS set up by the Indian A JV / WOS set up by the Indian party as per the Regulations may party as per the Regulations may diversify its activities / set up step diversify its activities / set up step down subsidiary / alter the down subsidiary / alter the shareholding pattern in the overseas shareholding pattern in the overseas entity (subject to compliance with entity (subject to compliance with regulation 7 of the Regulations in regulation 7 of the Regulations in the case of financial sector the case of financial sector companies).companies).

Indian Party should report details Indian Party should report details of such decision with the RBI of such decision with the RBI through AD Category 1 Bankthrough AD Category 1 Bank within within 30 days of the approval of those 30 days of the approval of those decisions by the competent authority decisions by the competent authority of the JV / WOS concerned of the JV / WOS concerned

© Vaish Associates

© Vaish Associates

To provide more operational flexibility Indian promoters who havTo provide more operational flexibility Indian promoters who have set up WOS e set up WOS abroad or have at least 51 per cent stake in an overseas JV, mayabroad or have at least 51 per cent stake in an overseas JV, may write off capital or write off capital or such other receivables even while such JV /WOS continues to funcsuch other receivables even while such JV /WOS continues to function as under:tion as under:

(i)(i) Listed Indian companies are permitted to write off capital and oListed Indian companies are permitted to write off capital and other receivables up ther receivables up to 25 per cent of the equity investment in the JV /WOS under theto 25 per cent of the equity investment in the JV /WOS under the Automatic Route; Automatic Route; andand

(ii)(ii) Unlisted companies are permitted to write off capital and other Unlisted companies are permitted to write off capital and other receivables up to 25 receivables up to 25 per cent of the equity investment in the JV /WOS under the Approper cent of the equity investment in the JV /WOS under the Approval Route.val Route.The write off/ restructuring has to be reported to the RBI throuThe write off/ restructuring has to be reported to the RBI through ADgh AD--Category 1 Category 1 Bank within 30 days of such write off/ restructuring. Write off/Bank within 30 days of such write off/ restructuring. Write off/ restructuring shall restructuring shall also be subject to submission of the following:also be subject to submission of the following:

(i)(i) A certified copy of the balance sheet showing the loss in the ovA certified copy of the balance sheet showing the loss in the overseas WOS/JV set erseas WOS/JV set up by the Indian Party; andup by the Indian Party; and

(ii)(ii) Projections for the next five years indicating benefit accruing Projections for the next five years indicating benefit accruing to the Indian to the Indian company consequent to such write off / restructuring.company consequent to such write off / restructuring.

© Vaish Associates

An Indian Party who has made An Indian Party who has made an investment abroad is under the an investment abroad is under the obligation to do the following obligation to do the following things:things:(i)(i)receive share certificate or any receive share certificate or any other document as an evidence of other document as an evidence of investment;investment;(ii)(ii)repatriate to India the dues repatriate to India the dues receivable from foreign entity;receivable from foreign entity;(iii)(iii)submit the documents / Annual submit the documents / Annual Performance Report to the Performance Report to the Reserve Bank.Reserve Bank.

© Vaish Associates

© Vaish Associates

An Indian Party without prior approval of the Reserve Bank may An Indian Party without prior approval of the Reserve Bank may transfer by way of sale to transfer by way of sale to another Indian Party or to a person resident outside India, any another Indian Party or to a person resident outside India, any share or security held by it in a share or security held by it in a JV or WOS outside India subject to the following conditions:JV or WOS outside India subject to the following conditions:the sale does not result in any write off of the investment madethe sale does not result in any write off of the investment made. . the sale is effected through a stock exchange where the shares othe sale is effected through a stock exchange where the shares of the overseas JV/ WOS are f the overseas JV/ WOS are

listed;listed;if the shares are not listed on the stock exchange and the shareif the shares are not listed on the stock exchange and the shares are disinvested by a private s are disinvested by a private

arrangement, the share price is not less than the value certifiearrangement, the share price is not less than the value certified by a Chartered Accountant / d by a Chartered Accountant / Certified Public Accountant as the fair value of the shares baseCertified Public Accountant as the fair value of the shares based on the latest audited financial d on the latest audited financial statements of the JV / WOS;statements of the JV / WOS;the Indian party does not have any outstanding dues by way of dithe Indian party does not have any outstanding dues by way of dividend, technical knowvidend, technical know--how how

fees, royalty, consultancy, commission or other entitlements andfees, royalty, consultancy, commission or other entitlements and / or export proceeds from the / or export proceeds from the JV or WOS; JV or WOS; the overseas concern has been in operation for at least one fullthe overseas concern has been in operation for at least one full year and the Annual year and the Annual

Performance Report together with the audited accounts for that yPerformance Report together with the audited accounts for that year has been submitted to the ear has been submitted to the Reserve Bank;Reserve Bank;the Indian party is not under investigation by CBI / the Indian party is not under investigation by CBI / DoEDoE/ SEBI / IRDA or any other / SEBI / IRDA or any other

regulatory authority in India.regulatory authority in India.

Indian Parties may disinvest in any of the Indian Parties may disinvest in any of the following cases without permission of following cases without permission of RBI:RBI:

(i)(i) Incase the JV/ WOS is listed in an Incase the JV/ WOS is listed in an overseas stock exchangeoverseas stock exchange

(ii)(ii) in cases where the Indian Party is in cases where the Indian Party is listed on a stock exchange in India and listed on a stock exchange in India and has a net worth of not less than Rs.100 has a net worth of not less than Rs.100 crorecrore..

(iii)(iii) if Indian Party is unlisted, and the if Indian Party is unlisted, and the investment in the overseas venture does investment in the overseas venture does not exceed USD 10 million.not exceed USD 10 million.

(iv)(iv) if Indian Party is listed, with net worth if Indian Party is listed, with net worth of less than Rs.100 of less than Rs.100 crorecrore but investment but investment in an overseas JV/WOS does not exceed in an overseas JV/WOS does not exceed USD 10 millionUSD 10 million

© Vaish Associates

An Indian party may pledge the An Indian party may pledge the shares of JV / WOS to an AD shares of JV / WOS to an AD Category Category –– I bank or a public I bank or a public financial institution in India for financial institution in India for availing of any credit facility for availing of any credit facility for itself or for the JV / WOS abroad in itself or for the JV / WOS abroad in terms of Regulation 18 of the terms of Regulation 18 of the Notification. Indian party may also Notification. Indian party may also transfer by way of pledge, the shares transfer by way of pledge, the shares held in overseas JV/WOS, to an held in overseas JV/WOS, to an overseas lender, provided the lender overseas lender, provided the lender is regulated and supervised as a bank is regulated and supervised as a bank and the total financial commitments and the total financial commitments of the Indian party remain within the of the Indian party remain within the limit stipulated by the Reserve Bank limit stipulated by the Reserve Bank for overseas investments, from time for overseas investments, from time to time.to time.

© Vaish Associates

Prior permission in Form ODI Prior permission in Form ODI –– to to accept shares of company outside accept shares of company outside India in lieu of fees due to it for India in lieu of fees due to it for professional services (subject to professional services (subject to conditions mentioned in the conditions mentioned in the Regulations)Regulations)

RBI to consider:RBI to consider:(i) Credentials/Net Worth/nature of (i) Credentials/Net Worth/nature of profession;profession;(ii) (ii) ForexForex earnings/ balances in earnings/ balances in EEFC/RFC accounts;EEFC/RFC accounts;(iii) Financial and business track (iii) Financial and business track record;record;(iv) Potential for (iv) Potential for forexforex inflow to the inflow to the country.country.

© Vaish Associates

Under the Under the LiberalisedLiberalised Remittance Remittance Scheme, all resident individuals, Scheme, all resident individuals, including minors, are allowed to freely including minors, are allowed to freely remit up to USD 200,000 per remit up to USD 200,000 per financialfinancialyear (April year (April –– March) for any permissible March) for any permissible current or capital account transaction or current or capital account transaction or a combination of both.a combination of both.Under the scheme resident individuals Under the scheme resident individuals can acquire and hold immovable can acquire and hold immovable property or shares or debt instruments or property or shares or debt instruments or any other assets outside India, without any other assets outside India, without prior approval of the Reserve Bank. prior approval of the Reserve Bank. Individuals can also open, maintain and Individuals can also open, maintain and hold foreign currency accounts with hold foreign currency accounts with banks outside India for carrying out banks outside India for carrying out transactions permitted under the transactions permitted under the Scheme. Scheme.

However there are certain prohibitions However there are certain prohibitions such as;such as;(i)(i)purchase of FCCBS.purchase of FCCBS.(ii)(ii)trading in trading in forexforex board.board.(iii)(iii)setting up a company abroadsetting up a company abroad(iv)(iv)directly or indirectly to Bhutan, directly or indirectly to Bhutan, Pakistan , Nepal and Mauritius.Pakistan , Nepal and Mauritius.(v)(v)directly or indirectly to countries directly or indirectly to countries identified by FATF as identified by FATF as ““non conon co--operative operative countries and territoriescountries and territories””, from time to , from time to time.time.(vi)(vi)margins or margin calls to overseas margins or margin calls to overseas exchanges.exchanges.(vii)(vii)those individuals and entities those individuals and entities identified as posing significant risk of identified as posing significant risk of committing acts of terrorismcommitting acts of terrorism

© Vaish Associates

General permission has been General permission has been granted to a person resident in India granted to a person resident in India who is an individual who is an individual ––

to acquire foreign securities as a to acquire foreign securities as a gift from any person resident outside gift from any person resident outside India;India;

to acquire shares under cashless to acquire shares under cashless Employees Stock Option Employees Stock Option Programme (ESOP) issued by a Programme (ESOP) issued by a company outside India, provided it company outside India, provided it does not involve any remittance does not involve any remittance from India;from India;

to acquire shares by way of to acquire shares by way of inheritance from a person whether inheritance from a person whether resident in or outside India;resident in or outside India;

© Vaish Associates

to purchase equity shares offered to purchase equity shares offered by a foreign company under its by a foreign company under its ESOP Schemes (subject to certain ESOP Schemes (subject to certain conditions more particularly conditions more particularly mentioned in the Regulations)mentioned in the Regulations)Foreign companies are permitted Foreign companies are permitted to repurchase the shares issued to to repurchase the shares issued to residents in India under any residents in India under any ESOP Scheme (subject to certain ESOP Scheme (subject to certain conditions more particularly conditions more particularly mentioned in the Regulations)mentioned in the Regulations)In all other cases not covered, In all other cases not covered, approval of the Reserve Bank is approval of the Reserve Bank is required for acquisition of foreign required for acquisition of foreign security.security.

© Vaish Associates

The shares acquired by The shares acquired by persons resident in India in persons resident in India in accordance with the provisions accordance with the provisions of the Act or Rules or of the Act or Rules or Regulations made Regulations made thereunderthereunderare allowed to be pledged for are allowed to be pledged for obtaining credit facilities in obtaining credit facilities in India from an AD Category India from an AD Category –– I I bank / Public Financial bank / Public Financial Institution.Institution.

© Vaish Associates

A person resident in India, being A person resident in India, being an Indian Company or Body an Indian Company or Body Corporate created by an act of Corporate created by an act of Parliament , Parliament , --May issue FCCBS not exceeding May issue FCCBS not exceeding USD 500 million to person USD 500 million to person resident outside India (subject to resident outside India (subject to Regulation)Regulation)May issue May issue FCCBsFCCBs beyond USD beyond USD 500 million with specific 500 million with specific approval from the RBI.approval from the RBI.May issue Foreign Currency May issue Foreign Currency Exchangeable Bonds to a person Exchangeable Bonds to a person resident outside India in resident outside India in accordance with the Regulations.accordance with the Regulations.

The company/ body corporate The company/ body corporate issuing issuing FCCBsFCCBs shall within 30 shall within 30 days from the date of issue, days from the date of issue, furnish a report to the RBI giving furnish a report to the RBI giving the details and documents as the details and documents as under:under:Total amounts for which Total amounts for which FCCBsFCCBshave been issuedhave been issuedNames of the investors resident Names of the investors resident outside India and no. of outside India and no. of FCCBsFCCBsissued to each of themissued to each of themThe amount repatriated to India The amount repatriated to India through normal banking channels through normal banking channels and/ or amount received by debit and/ or amount received by debit to NRE/ FCNR accounts in Indiato NRE/ FCNR accounts in India

© Vaish Associates

PenaltiesPenaltiesUnder the Act, if any person Under the Act, if any person

contravenes any rule, regulations, contravenes any rule, regulations, notification, direction or order notification, direction or order issued in exercise of the powers issued in exercise of the powers under this Act, he shall be liable under this Act, he shall be liable to a penalty of to a penalty of uptoupto thrice the sum thrice the sum involved, or involved, or uptoupto two two lakhlakh rupees rupees where the amount is not where the amount is not quantifiable, and where such quantifiable, and where such contravention is continuing a contravention is continuing a further penalty which may extend further penalty which may extend to five thousand rupees per day.to five thousand rupees per day.

Power to compound contraventionPower to compound contravention.Any contravention maybe Any contravention maybe

compounded on application made compounded on application made by the person committing such by the person committing such contravention, within 180 days contravention, within 180 days from date of receipt of such from date of receipt of such application. application.

Where a contravention has been Where a contravention has been compounded under subcompounded under sub--section section (1), no proceeding or further (1), no proceeding or further proceeding, as the case maybe, proceeding, as the case maybe, shall be initiated or continued, as shall be initiated or continued, as the case may be, against the the case may be, against the person committing such person committing such contravention under that section, contravention under that section, in respect of the contravention so in respect of the contravention so compounded.compounded.© Vaish Associates

© Vaish Associates

Can individuals receive shares of a foreign company in Can individuals receive shares of a foreign company in exchange of shares held by them in Indian Companies?exchange of shares held by them in Indian Companies?

Can an Indian Party make investments in overseas Can an Indian Party make investments in overseas L.L.P.?L.L.P.?

© Vaish Associates

THANK YOUTHANK YOU