INFRASTRUCTURE FINANCING BY FINANCIAL INSTITUTIONS –AN APPRAISAL

Upload

dana-fisherCategory

view

220download

1

VA Financing and Appraisal Overview

Chapter 7

Today's FHA and VA 9/24/13

Chapter 7: VA Financing and Appraisal Overview

Introduction• VA loans were first offered in 1944 as a provision of the GI Bill

of Rights. The purpose of the lending program was to provide veterans with a mortgage loan guaranteed by the federal government with no down payment.

• VA-guaranteed loans are available through approved lenders for eligible veterans and are limited to properties that the veteran will occupy as the primary residence.

• Many of the property eligibility requirements mirror the requirements for FHA financing or the secondary mortgage market.

2

Today's FHA and VA 9/24/13

Chapter 7: VA Financing and Appraisal Overview

Key Terms

• Lender Appraisal Processing Program (LAPP) The purpose of this program is to speed up the time to loan closing by allowing VA-authorized lenders to receive appraisal reports directly from appraisers and process them without VA involvement.

• MPR (Minimum Property Requirements) For properties qualifying for VA loan guarantee.

• RLC (Regional Loan Center) For VA loan processing and other functions, such as adding an appraiser to the VA Fee Panel.

• TAS (The Appraisal System) A central data system used by the VA.

3

Chapter 7: VA Financing and Appraisal Overview

The VA Loan

• There is no maximum loan amount for a VA loan, but there is a maximum limit of guarantee to the lender.

• The veteran must meet income and credit qualifications.

• Usually, VA loans are subject to a funding fee; this amount may be financed.

Today's FHA and VA 9/24/13 4

The VA Loan (cont.)

• Usually concessions paid by the seller may not exceed 4%.

• Some services for a purchase transaction, such as a termite inspection, must be paid by the seller.

• Eligible properties must meet VA minimum property requirements.

Today's FHA and VA 9/24/13

Chapter 7: VA Financing and Appraisal Overview

5

Chapter 7: VA Financing and Appraisal Overview

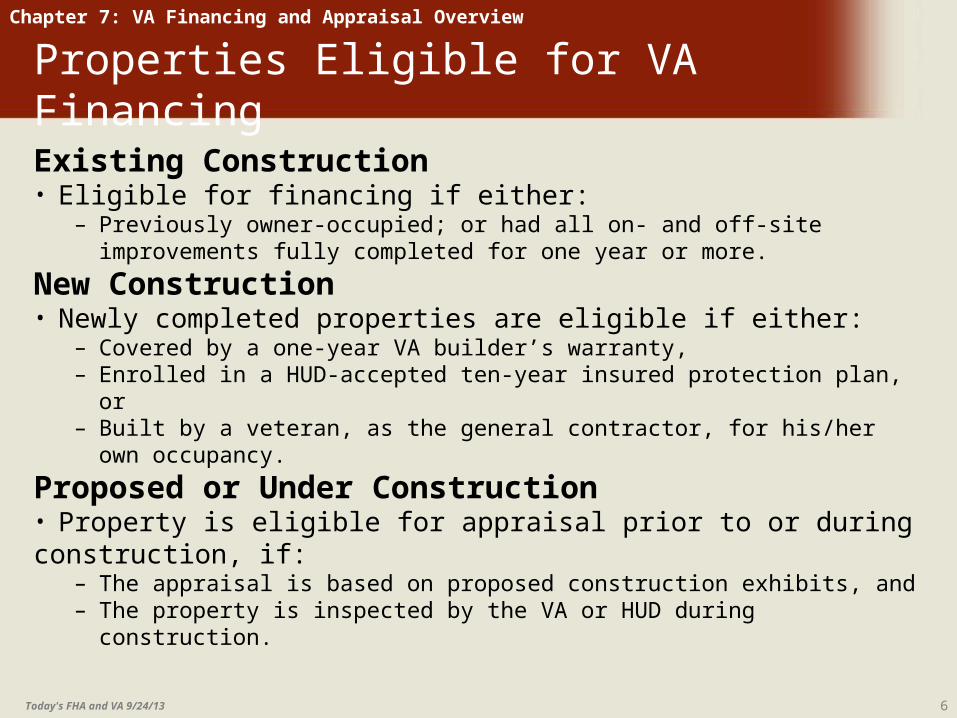

Properties Eligible for VA Financing

Existing Construction• Eligible for financing if either:

– Previously owner-occupied; or had all on- and off-site improvements fully completed for one year or more.

New Construction• Newly completed properties are eligible if either:

– Covered by a one-year VA builder’s warranty,– Enrolled in a HUD-accepted ten-year insured protection plan, or– Built by a veteran, as the general contractor, for his/her own

occupancy.

Proposed or Under Construction• Property is eligible for appraisal prior to or during construction, if:

– The appraisal is based on proposed construction exhibits, and– The property is inspected by the VA or HUD during construction.

Today's FHA and VA 9/24/13 6

Properties Eligible for VA Financing (cont.)

Manufactured Home Classified as Real Estate•For eligibility of a VA loan term of 30 years, a manufactured home must:

– Be classified and taxed as real property.– Be properly affixed to a permanent foundation.– Conform to VA MPRs, building codes, and zoning requirements.

Other Manufactured Homes•Modular homes are eligible if they are:

– Covered by a HUD structural engineering bulletin, or– Constructed to the standards of the state in which the factory is located

and receive that state’s approval certification, and– Delivered to the building site in sections, but are not attached to a

chassis supported by wheels.Property to be Altered/Improved/Repaired•Appraisal eligibility occurs:

– Prior to being altered, improved, or repaired, or – After being altered, improved, or repaired

Today's FHA and VA 9/24/13

Chapter 7: VA Financing and Appraisal Overview

7

Chapter 7: VA Financing and Appraisal Overview

Properties Ineligible for VA Financing

Properties not Likely to Meet MPRs•Property in a badly deteriorated condition is ineligible for appraisal unless there is likelihood that it can be repaired to meet VA minimum property requirements prior to loan closing.Location-Related Problem•Property is not eligible for appraisal if the improvements are located in:

– A special flood hazard area (SFHA) and:• Is proposed/under/new construction with elevation of the lowest floor

below the 100-year flood level, • Flood insurance is not available, or• Is in an area subject to regular flooding, whether or not it is in an SFHA.

– A coastal barrier resources system area.– An airport Noise Zone 3, if proposed or under construction.– A transmission line easement involving high-pressure gas, liquid

petroleum, or high-voltage electricity.– An area susceptible to geological or soil instability.

Today's FHA and VA 9/24/13 8

Properties Ineligible for VA Financing (cont.)

Condo not Approved•A condominium project must be acceptable to the VA before any unit in the project can be eligible for VA loan guaranty.Ownership not Fee Simple•Property involving a less than fee simple ownership (e.g., leaseholds, cooperatives, ground rental arrangements) is not eligible for appraisal without prior VA approval of the specific legal arrangement or project. Submissions to the VA Central Office must include:

– Details of the ownership arrangement, and– Copies of leases or other instruments creating the estate, and – Recommendations of the VA Office of Jurisdiction.

Today's FHA and VA 9/24/13

Chapter 7: VA Financing and Appraisal Overview

9

Chapter 7: VA Financing and Appraisal Overview

Minimum Property Requirements (MPRs)

Entity•The property must be a single, readily marketable real estate entity.Nonresidential Use•Any nonresidential use of the property must be subordinate to its residential use and character.•If any portion of a property is designed or used for nonresidential purposes, the use must not:

– Impair the residential character of the property, or – Exceed 25 percent of the total floor area.

Space Requirements•Each living unit must have the space necessary to assure suitable:

– Living– Sleeping– Cooking and dining accommodations– Sanitary facilities

Today's FHA and VA 9/24/13 10

Minimum Property Requirements (MPRs) (cont.)

Mechanical Systems•Mechanical systems must:

– Be safe to operate.– Be protected from destructive elements.– Have reasonable future utility, durability, and economy.– Have adequate capacity and quality.

Heating•Fee Appraisers must report any permanently installed, or to-be-installed, unvented fireplace or space heater that uses liquid or gaseous fuel.•Homes with wood-burning stoves as primary heating sources must have permanent conventional heating systems that maintain a temperature of at least 50 degrees Fahrenheit in plumbing areas.•Solar systems for domestic water heating or space heating must:

– Meet standards in the HUD Handbook 4930.2, Solar Heating – Domestic Hot Water Heating Systems, and – Be backed up 100 percent with a conventional thermal energy subsystem.

Today's FHA and VA 9/24/13

Chapter 7: VA Financing and Appraisal Overview

11

Minimum Property Requirements (MPRs) (cont.)

Water Supply and Sanitary Facilities•Each unit must have the following:

– Domestic hot water– Continuing supply of safe and potable water for drinking and household use– Sanitary facilities and a safe method of sewage disposal

Roof Covering•The roof covering must:

– Prevent entrance of moisture– Provide reasonable future utility, durability, and economy of maintenance

Crawl Space•The crawl space must:

– Have adequate access– Be clear of all debris– Be properly vented

•The floor joists must be above the highest level of the ground.•Dampness/ponding of water in the crawl space must be corrected.

Today's FHA and VA 9/24/13

Chapter 7: VA Financing and Appraisal Overview

12

Minimum Property Requirements (MPRs) (cont.)

Ventilation•Natural ventilation of structural spaces must be provided to reduce the effect of heat and moisture.

Electricity•Each unit must have electricity for lighting and for necessary equipment.

Hazards•The property must be free of hazards which may:

– Adversely affect the health and safety of the occupants.– Adversely affect the structural soundness of the dwelling or improvements. – Impair the customary use and enjoyment of the property by the occupants.

Drainage•The site must be graded so that it:

– Provides positive, rapid drainage away from the perimeter walls of the dwelling.

– Prevents ponding of water on the site.

Today's FHA and VA 9/24/13

Chapter 7: VA Financing and Appraisal Overview

13

Minimum Property Requirements (MPRs) (cont.)

Defective Conditions• Conditions that impair the safety, sanitation, or structural soundness of the dwelling will cause the property to be unacceptable until the defects or conditions have been fixed. • Such conditions include but are not limited to:

– Defective construction– Poor workmanship– Evidence of continuing settlement– Excessive dampness– Leakage– Decay– Termites

Wood-Destroying Insects/Fungus/Dry Rot• Appraisers must look for and report evidence of wood-destroying

insect infestation, fungus growth, and dry rot in addition to any VA requirements.

Today's FHA and VA 9/24/13

Chapter 7: VA Financing and Appraisal Overview

14

Minimum Property Requirements (MPRs) (cont.)

Lead-Based Paint•Constitutes an immediate hazard to be corrected, unless testing shows lead is not present in the paint above law-permitting levels.•Appraisers must:

– Assume that a defective paint condition on any interior or exterior surface of properties built prior to 1978 involves lead-based paint.

– Clearly identify the location of such conditions.– Recommend correction.– Any defective paint condition identified must receive adequate

treatment to prevent the ingestion of contaminated paint. Either:• The surface treatment must be washed, scraped, or wire brushed and

repainted, or• The paint must be removed or the surface covered with a suitable

material if the paint film integrity cannot be maintained.

Today's FHA and VA 9/24/13

Chapter 7: VA Financing and Appraisal Overview

15

Minimum Property Requirements (MPRs) (cont.)

Party Walls• A building constructed to a property line must be separated from the

adjoining building by a wall extending the full height of the building from the foundation to the roof ridge.

Gas and Petroleum Pipelines• No part of any residential structure may be located within a high-pressure

gas or liquid petroleum pipeline easement• Any detached improvements will not receive value for VA purposes.• If a proposed residential structure will be located outside the pipeline easement, but within an area that extends 220 yards on either side of the

centerline, the VA notice of value will be conditioned. A statement from an authorized official of the pipeline company must certify compliance for:

• High-Pressure Gas Pipelines• Liquid Petroleum Pipelines

Today's FHA and VA 9/24/13

Chapter 7: VA Financing and Appraisal Overview

16

Minimum Property Requirements (MPRs) (cont.)

High-Voltage Electric Transmission Lines•No part of any residential structure may be located within a high-voltage electric transmission line easement. •Any detached improvements, even partially in a transmission line easement, will not receive value for VA purposes.Access for Exterior Wall Maintenance•There must be space between buildings to permit maintenance of the exterior walls.

Today's FHA and VA 9/24/13

Chapter 7: VA Financing and Appraisal Overview

17

Chapter 7: VA Financing and Appraisal Overview

MPR Variations and Exemptions

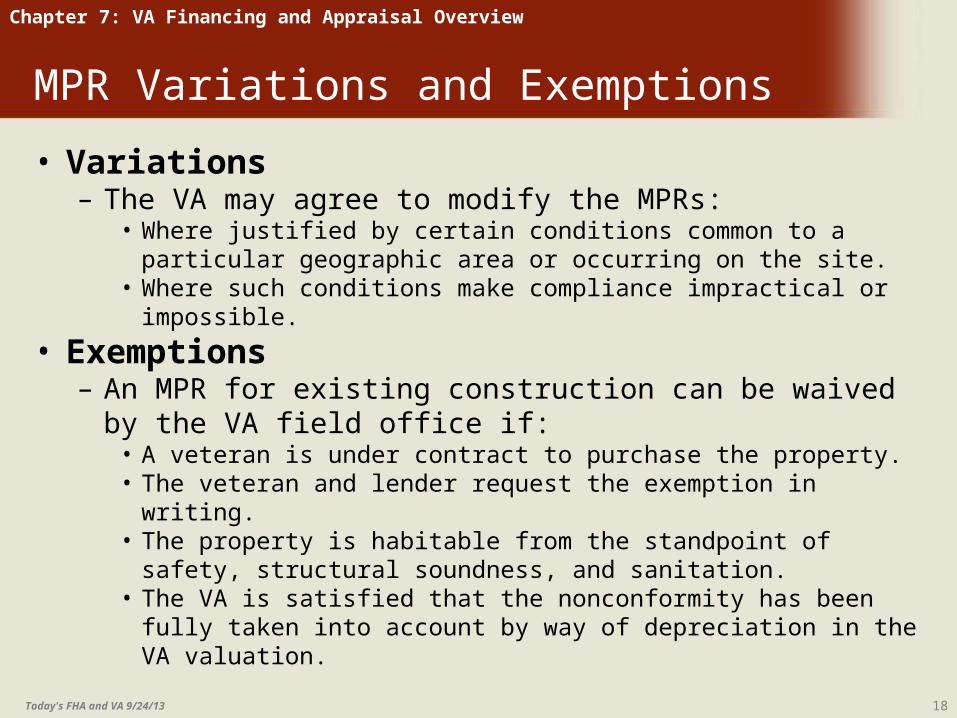

• Variations– The VA may agree to modify the MPRs:

• Where justified by certain conditions common to a particular geographic area or occurring on the site.

• Where such conditions make compliance impractical or impossible.

• Exemptions– An MPR for existing construction can be waived by the

VA field office if:• A veteran is under contract to purchase the property.• The veteran and lender request the exemption in writing. • The property is habitable from the standpoint of safety, structural

soundness, and sanitation.• The VA is satisfied that the nonconformity has been fully taken

into account by way of depreciation in the VA valuation.

Today's FHA and VA 9/24/13 18

Chapter 7: VA Financing and Appraisal Overview

Becoming a VA Appraiser

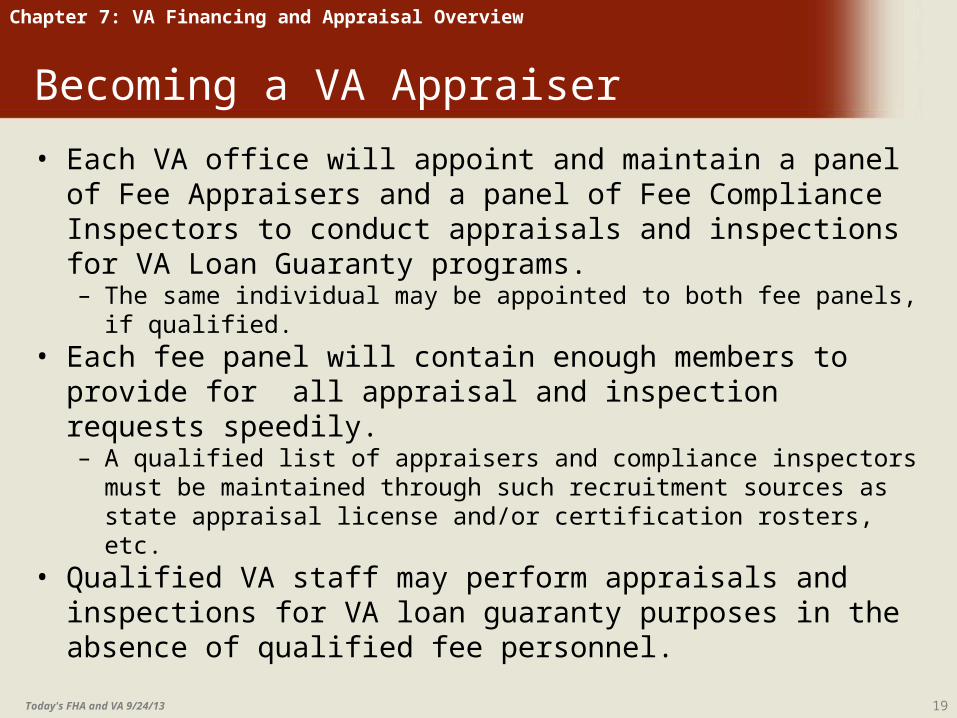

• Each VA office will appoint and maintain a panel of Fee Appraisers and a panel of Fee Compliance Inspectors to conduct appraisals and inspections for VA Loan Guaranty programs.– The same individual may be appointed to both fee panels, if

qualified.• Each fee panel will contain enough members to provide for

all appraisal and inspection requests speedily. – A qualified list of appraisers and compliance inspectors must be

maintained through such recruitment sources as state appraisal license and/or certification rosters, etc.

• Qualified VA staff may perform appraisals and inspections for VA loan guaranty purposes in the absence of qualified fee personnel.

Today's FHA and VA 9/24/13 19

Chapter 7: VA Financing and Appraisal Overview

Appraiser Pre-requisite Requirements

• State licensure or certification.• Five years’ experience in appraising residential properties.• Submit two letters from appraisers attesting to the applicant’s

qualifications.• There may be no conflict of interest between the applicant’s

employment and performance as a Fee Appraiser with the VA.• Employees of HUD, Fannie Mae, Freddie Mac, or the Postal Service are

ineligible.• Local and state government employees may be designated but care

must be taken so that there will not be a conflict of interest or the appearance of a conflict of interest.

• By completing the application to become a VA fee appraiser (VA Form 26-6681) applicants are authorizing VA to obtain a credit report. (In item #19 of the VA Form 26-6681, preceding the list of Geographic Area(s) of Practice), enter “By signing below I agree that VA may obtain a copy of my credit report.”

Today's FHA and VA 9/24/13 20

Appraiser Pre-requisite Requirements (cont.)

• Field stations will perform a search through the Credit Alert Interactive Voice Response System to determine if the applicant has any outstanding delinquent debts to the Federal Government. – If the applicant owes the Federal Government a delinquent debt, there must

be evidence of payment in full of the debt, or evidence of an acceptable repayment plan.

• Written tests are not required. Field stations shall require a demonstration appraisal on a Freddie Mac Form 70 or Fannie Mae Form 1004 (Uniform Residential Appraisal Report). Prior to the demonstration appraisal, applicants will be furnished instructional or procedural material necessary to complete the appraisal.

• An individual may be designated to more than one fee roster geographic area provided he demonstrates the required experience or qualifications.

• A fee panel vacancy must exist in the area in which the applicant wishes to work.

Today's FHA and VA 9/24/13

Chapter 7: VA Financing and Appraisal Overview

21

Communication Requirements for the VA Appraiser

1. Fee Appraisers must have Internet/e-mail access. • VA Fee Appraisers must have Internet access that is compatible with the

VA’s Portal and Internet-based appraisal assignment and central data system, called TAS (“The Appraisal System”).

• Fee Appraisers must have access to an e-mail address.

• Lenders are using e-mail as the primary means of conveying the electronic Request for Determination of Reasonable Value form. E-Appraisal will notify the appraiser by e-mail when the appraisal assignment is made.

2. A fax machine, or access to a fax machine, is mandatory. Since e-mailing of the Request for Determination of Reasonable Value remains optional for lenders, some of them choose to fax the signed form to the assigned Fee Appraiser to save mailing time. Any Fee Appraiser found to be without a functioning fax number will be contacted by the VA and asked to remedy the problem. If the VA is unable to contact the appraiser, no further appraisal assignments will be made until fax communication has been restored.

Today's FHA and VA 9/24/13

Chapter 7: VA Financing and Appraisal Overview

22

Communication Requirements for the VA Appraiser (cont.)

3. A telephone answering machine, voice mail system, or someone to answer the telephone during working hours (8:00 a.m.–4:00 p.m.) Monday through Friday, is mandatory. If no one is available to answer the appraiser’s telephone or to check e-mail during unavailable periods, the appraiser is required to have a recorded telephone message and an e-mail response to inform callers of the date of expected return.

4. Fee Appraisers must respond to inquiries from VA staff, lenders, or real estate agents no later than the following business day. Failure to respond by the end of the next business day will result in immediate withholding of new assignments until the appraiser has responded.

5. Fee Appraisers must notify their VA Office of Jurisdiction at least seven business days in advance of being absent for vacation so that assignments will be stopped. It is the responsibility of the appraiser to e-mail the VA Fee-Personnel Vacation Request Form.

6. Immediate notification is required when the Fee Appraiser needs assignments to be stopped for illness or emergencies.

Today's FHA and VA 9/24/13

Chapter 7: VA Financing and Appraisal Overview

23

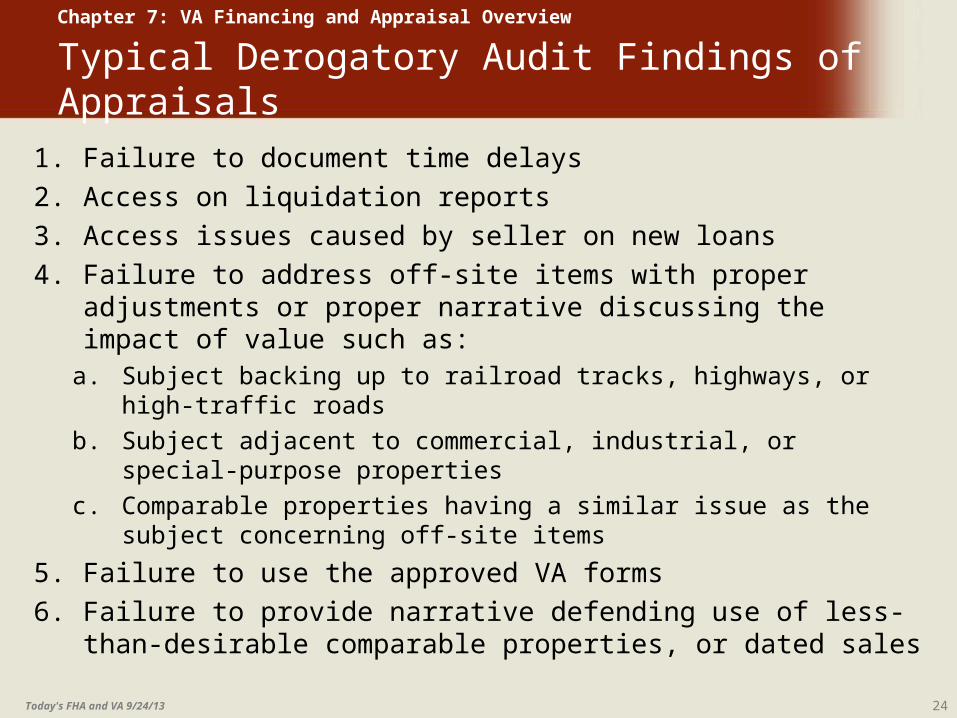

Typical Derogatory Audit Findings of Appraisals

1. Failure to document time delays

2. Access on liquidation reports

3. Access issues caused by seller on new loans

4. Failure to address off-site items with proper adjustments or proper narrative discussing the impact of value such as:

a. Subject backing up to railroad tracks, highways, or high-traffic roads

b. Subject adjacent to commercial, industrial, or special-purpose properties

c. Comparable properties having a similar issue as the subject concerning off-site items

5. Failure to use the approved VA forms

6. Failure to provide narrative defending use of less-than-desirable comparable properties, or dated sales

Today's FHA and VA 9/24/13

Chapter 7: VA Financing and Appraisal Overview

24

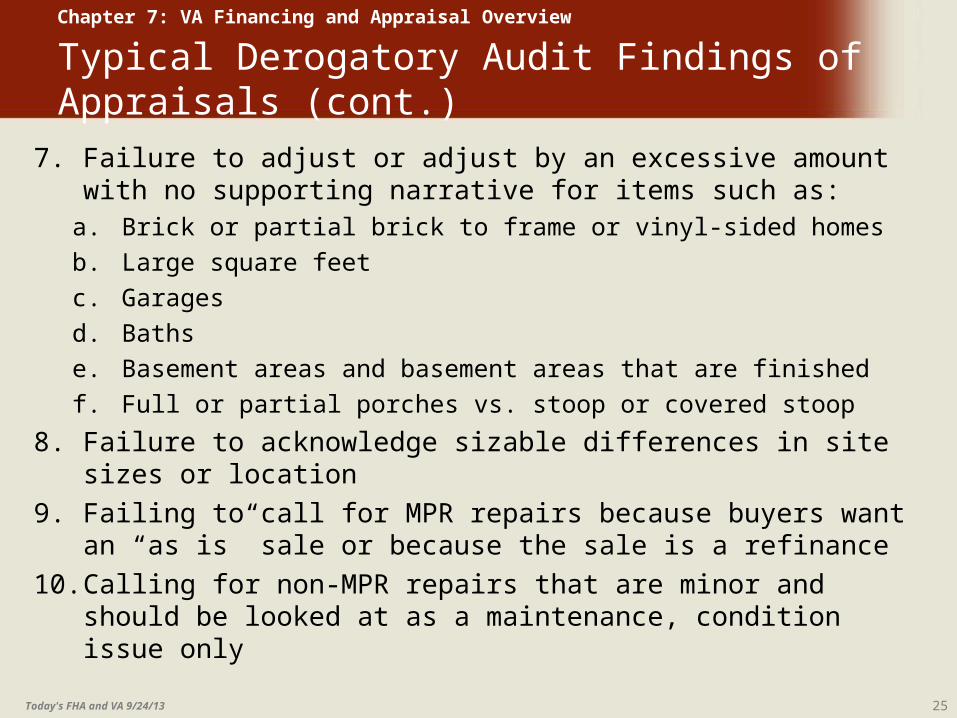

Typical Derogatory Audit Findings of Appraisals (cont.)

7. Failure to adjust or adjust by an excessive amount with no supporting narrative for items such as:

a. Brick or partial brick to frame or vinyl-sided homes

b. Large square feet

c. Garages

d. Baths

e. Basement areas and basement areas that are finished

f. Full or partial porches vs. stoop or covered stoop

8. Failure to acknowledge sizable differences in site sizes or location

9. Failing to call for MPR repairs because buyers want an “as is” sale or because the sale is a refinance

10. Calling for non-MPR repairs that are minor and should be looked at as a maintenance, condition issue only

Today's FHA and VA 9/24/13

Chapter 7: VA Financing and Appraisal Overview

25

Typical Derogatory Audit Findings of Appraisals (cont.)

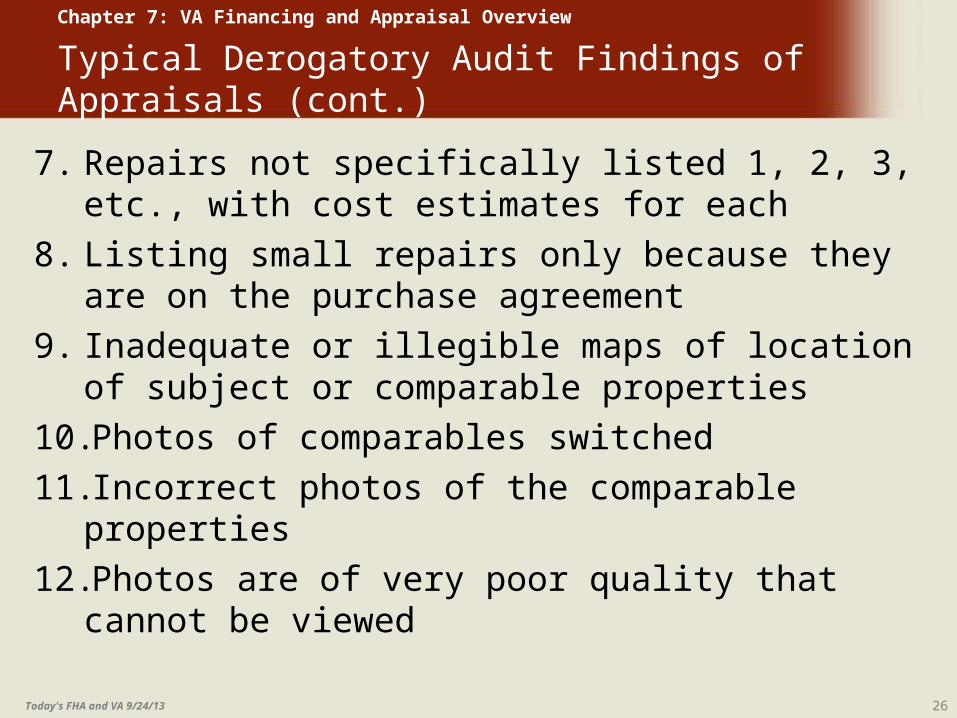

7. Repairs not specifically listed 1, 2, 3, etc., with cost estimates for each

8. Listing small repairs only because they are on the purchase agreement

9. Inadequate or illegible maps of location of subject or comparable properties

10.Photos of comparables switched

11.Incorrect photos of the comparable properties

12.Photos are of very poor quality that cannot be viewed

Today's FHA and VA 9/24/13

Chapter 7: VA Financing and Appraisal Overview

26

VA Appraisal RequirementsUSPAP

• Every VA appraisal must meet the Uniform Standards of Professional Appraisal Practice (USPAP) reporting options of an Appraisal Report or Restricted Appraisal Report. VA approval is required prior to performing a “restricted” appraisal.

• The USPAP Jurisdictional Exception Rule grants Federal agencies the ability to follow their own requirements when there is a conflict between USPAP and Federal agency requirements.

• In addition, every VA appraisal must be:– Performed within VA timeliness requirements.– Uploaded into E-Appraisal by the appraiser as a Portable Document

Format (PDF) file.

Today's FHA and VA 9/24/13

Chapter 7: VA Financing and Appraisal Overview

27

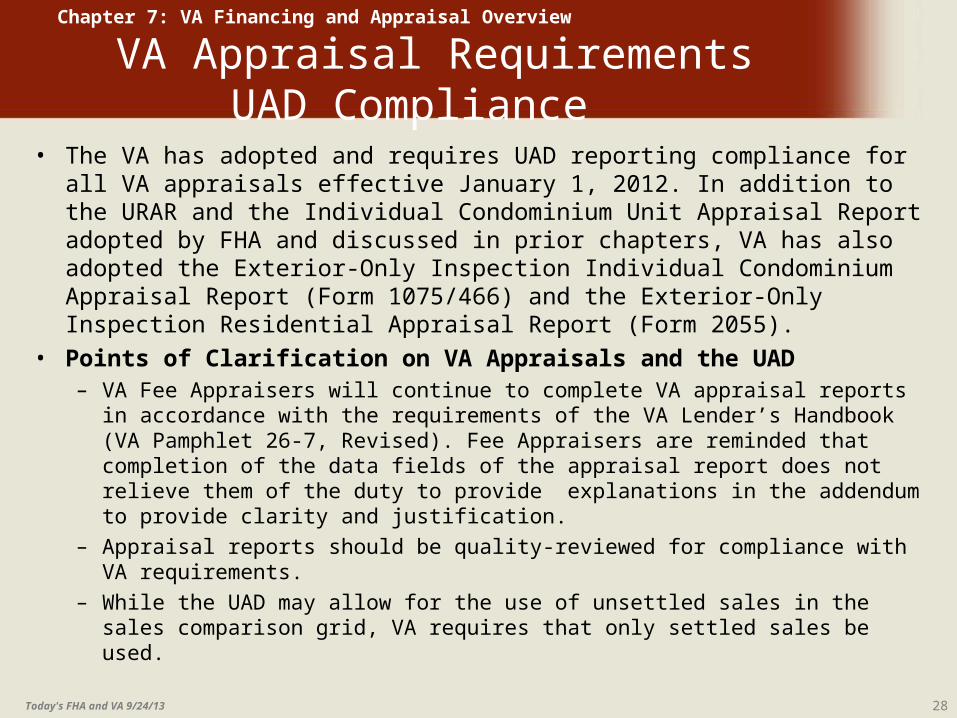

VA Appraisal RequirementsUAD Compliance

• The VA has adopted and requires UAD reporting compliance for all VA appraisals effective January 1, 2012. In addition to the URAR and the Individual Condominium Unit Appraisal Report adopted by FHA and discussed in prior chapters, VA has also adopted the Exterior-Only Inspection Individual Condominium Appraisal Report (Form 1075/466) and the Exterior-Only Inspection Residential Appraisal Report (Form 2055).

• Points of Clarification on VA Appraisals and the UAD– VA Fee Appraisers will continue to complete VA appraisal reports in

accordance with the requirements of the VA Lender’s Handbook (VA Pamphlet 26-7, Revised). Fee Appraisers are reminded that completion of the data fields of the appraisal report does not relieve them of the duty to provide explanations in the addendum to provide clarity and justification.

– Appraisal reports should be quality-reviewed for compliance with VA requirements.

– While the UAD may allow for the use of unsettled sales in the sales comparison grid, VA requires that only settled sales be used.

Today's FHA and VA 9/24/13

Chapter 7: VA Financing and Appraisal Overview

28

VA Appraisal Requirements (cont.)UAD Compliance

• Points of Clarification on VA Appraisals and the UAD– UAD requires appraisers to give specific information about prior remodeling– 15 years; the VA expects Fee Appraisers to recognize and describe

remodeling and to make appropriate adjustments. Fee Appraisers should report UAD information concerning the remodeling if it is available in the “normal course of business” within VA timeliness statutes for completion of the appraisal.

• Changes to VA Policies and Procedures in Relation to Adoption of the UAD– The requirement that only “Department of Veterans Affairs” be entered in the

Lender/Client field of the appraisal form is rescinded. The lender’s name will be entered with “Department of Veterans Affairs,” as the client of the field.

– The requirement that “Intended User: Any VA Approved Lender” be entered in the Address field for the lender is rescinded. The address of the lender will now be entered in this field.

– The requirement that “Any Qualified Veteran” be entered in the Borrower field is rescinded. The Veteran purchaser’s name will be the borrower in this field.

Today's FHA and VA 9/24/13

Chapter 7: VA Financing and Appraisal Overview

29

1004MC Market Conditions Addendum

• Effective March 27, 2009, all VA appraisals must include the Fannie Mae Market Conditions Addendum, Form 1004MC. For appraisals performed on or after August 1, 2009, appraisers may charge a fee of $50 for completing the form.

Today's FHA and VA 9/24/13

Chapter 7: VA Financing and Appraisal Overview

30

Approaches to ValueSales Comparison Approach

• The VA relies exclusively on the sales comparison approach to value, except in circumstances involving inadequate comparable sales or extremely unique properties. VA value estimates should never exceed the indicated value of the sales comparison approach.

• Key points to keep in mind:– The appraiser must select the three best closed comparable sales available

and properly adjust the sale price of each for market recognized differences between it and the subject property.

– The appraiser must explain reliance on sales that are not comparable to the subject.

– Sales listings, contract offers, and unsettled sales must not be used as comparables.

– Comparable sales should preferably exhibit a narrow price range. Appraisers must explain a wide range in the sale prices of comparables before or after adjustment.

Today's FHA and VA 9/24/13

Chapter 7: VA Financing and Appraisal Overview

31

Approaches to Value (cont.)Sales Comparison Approach

– A single data source is adequate if it provides quality sales data verified by closed transactions. Sales data provided by a party to the financing of the subject property must be verified.

– Comparable sales should be recent, typically within six to twelve months. Sales over six months old may be considered outdated. The appraiser must explain the use of sales over twelve months old.

– Comparable sales should be located as close to the subject as practical, with the proximity to the subject described. To locate properties in cities, blocks should be used; in rural areas, miles.

– The appraiser must adequately explain any reliance on sales located further from the subject than similar comparable sales readily available in the subject neighborhood, or outside of the subject’s market area. In some rural areas, comparable sales may be 5, 10, or 20 miles away from the subject property and still within the subject’s immediate market area.

Today's FHA and VA 9/24/13

Chapter 7: VA Financing and Appraisal Overview

32

Approaches to Value (cont.)Sales Comparison Approach

– To be in a condition acceptable to the VA, properties must meet the VA’s Minimum Property Requirements (MPR). Since MPR repairs identified in the appraisal report must be completed as a report condition, value adjustments to the comparables are to be made as if the repairs are accomplished.

– Generally, good comparables require minimal adjustment for individual feature differences and a minimal total net adjustment. The appraiser must explain large adjustments.

– Adjustments based on some factor other than market reaction, such as builder costs for materials, etc., are not generally acceptable.

Today's FHA and VA 9/24/13

Chapter 7: VA Financing and Appraisal Overview

33

Approaches to Value Income Approach

• Development of an income approach for a single family property is not required. If the appraisal involves an income-producing property (more than one living unit), the appraiser will use the Small Residential Income Property Appraisal Report, Freddie Mac Form 72 or Fannie Mae Form 1025, which requires value estimates developed through both the income approach and the sales comparison approach in the final reconciliation.

• For VA purposes, a veteran may purchase a dwelling of up to four living units, so long as he occupies one of the units. In valuing such properties, consideration must be given to the income-producing potential of the remaining unit(s), whether or not the veteran actually plans to rent them out.

Today's FHA and VA 9/24/13

Chapter 7: VA Financing and Appraisal Overview

34

Approaches to ValueCost Approach

• The appraiser is not required to provide the cost approach to value on any VA appraisal (proposed, new, or existing construction). Since the residential real estate market does not base transaction decisions on a property’s reproduction or replacement cost, the cost approach to value may be used only to support the sales comparison approach in the final reconciliation. – This may be warranted in rare situations where the comparable

sales alone do not provide an adequate indication of value.

• For Example – The cost approach may be useful in supporting the sales

comparison approach in an appraisal of a new manufactured home in a rural area that has only recent sales of stick- built homes and much older manufactured homes.

Today's FHA and VA 9/24/13

Chapter 7: VA Financing and Appraisal Overview

35

Use of Assistants

• VA Fee Appraisers must comply with the VA’s policy concerning assistants. An appraiser who has relied on significant professional assistance in the appraisal must name the individual and the specific tasks performed in the reconciliation section of the report.

• The Fee Appraiser assigned by the VA must personally:1. View the interior and exterior of the subject property and the exterior of

each comparable.

2. Select and analyze the comparables.

3. Make the final value estimate.

4. Sign the appraisal report as the appraiser.

• The VA Fee Appraiser may not delegate any of these four important functions to an assistant, even though that person may be licensed or certified. The individual who signs the URAR as the appraiser must be the VA fee panel member who was assigned on the rotational basis by the VA.

Today's FHA and VA 9/24/13

Chapter 7: VA Financing and Appraisal Overview

36

VA Appraisal Fees and Payment IssuesFee Schedule

• Maximum fees for VA appraisals and inspections are established by each VA Regional Loan Center for its area of jurisdiction. Current VA appraisal fees are listed with each VA Regional Loan Center. Regional Loan Centers (RCL) include VA loan processing and other functions, such as adding an appraiser to the VA Fee Panel.

Today's FHA and VA 9/24/13

Chapter 7: VA Financing and Appraisal Overview

37

Desk and Field Reviews of Appraisal Reports

• Every appraisal report will be desk reviewed by a Lender Appraisal Processing Program (LAPP) Staff Appraiser Reviewer (SAR), by a VA Staff Appraiser, or both, to verify that the:– Report was submitted in a timely manner.– Fee Appraiser’s conclusions of value are consistent, sound,

supportable, and logical.– Report was prepared in accordance with acceptable appraisal

techniques and standards (USPAP), as well as specific VA instructions.

• The Lender Appraisal Processing Program (LAPP) is a program that speeds up the time to loan closing by allowing VA-authorized lenders to receive appraisal reports directly from appraisers and process them without VA involvement.

Today's FHA and VA 9/24/13

Chapter 7: VA Financing and Appraisal Overview

38

Quality Control and Standards

• All appraisal reports are reviewed for both work quality and timeliness. Non-acceptable quality or timeliness findings in any appraisal will be classified as negative work quality or timeliness findings. All negative work quality findings are further categorized according to their significance into substantive or non-substantive findings.

• A substantive negative work quality finding will be assessed where the VA has determined that the Fee Appraiser made a serious error of fact or methodology that materially impacted the appraised value or condition of the property. Examples include, but are not limited to:– Fraudulent reporting (misrepresentation of a material fact)– Appraising the wrong property– Failing to require necessary MPR repairs that may result in damage to the

veteran– Repeating or not correcting non-substantive errors after VA notification – Continued disregard for VA instructions or requirements after they have been

called to the appraiser’s attention– Serious USPAP violations

Today's FHA and VA 9/24/13

Chapter 7: VA Financing and Appraisal Overview

39

Quality Control and Standards (cont.)

• A non-substantive finding is generally one in which the VA has determined that the Fee Appraiser made a relatively minor error of fact or methodology that did not impact the final value or the reported condition of the property. Examples include, but are not limited to:– Failing to provide required information on the URAR

– Misreporting of distances between subject and comparables

– Inconsistency within the URAR

– Failing to adequately describe reasoning in support of adjustments*

– Using time adjustments not supported or documented by pending sales or listings*

– Making insupportable or “wrong-way” adjustments

– Minor USPAP violations

• Documented negative timeliness or quality findings can form the basis for administrative action by the VA. An appraiser who exhibits chronically deficient customer service will also be subject to administrative action.

Today's FHA and VA 9/24/13

Chapter 7: VA Financing and Appraisal Overview

40

Chapter 7: VA Financing and Appraisal Overview

Summary

1. VA loans were first offered in 1944 as a provision of the GI Bill of Rights. The purpose of the lending program was to provide veterans with a mortgage loan guaranteed by the federal government with no down payment required.

2. Several property types qualify for VA financing; however, the veteran must occupy at least part of any property that is either mixed in use or of more than one unit.

3. To qualify to become a VA Fee Appraiser, the appraiser must be licensed or certified by the appraiser’s state and have at least five years of residential appraisal experience.

4. No examination is required to become a VA Fee Appraiser; however, the applicant must have three reference letters, two of which must be from other appraisers.

Today's FHA and VA 9/24/13 41

Chapter 7: VA Financing and Appraisal Overview

Summary (cont.)5. The VA has specific appraisal development and reporting

requirements that may require invoking the Jurisdictional Exception Rule of USPAP.

6. The exclusive method of determining value in VA appraisal assignments is the sales comparison approach, except in unique circumstances. The appraiser is not required to develop or report the cost approach to value in any VA appraisal unless the method is useful for supporting the results of the sales comparison approach.

7. The Fee Appraiser assigned by the VA must personally view the interior and exterior of the subject property and the exterior of each comparable; select and analyze the comparables; make the final value estimate; and sign the appraisal report as the appraiser. Assistants are not permitted to perform these functions.

Today's FHA and VA 9/24/13 42

Chapter 7: VA Financing and Appraisal Overview

Summary (cont.)8. All appraisal reports are reviewed for both work quality and

timeliness. Non-acceptable quality or timeliness findings in any appraisal will be classified as negative work quality findings or negative timeliness findings. All negative work quality findings are further categorized according to their significance into substantive or non-substantive findings.

9. Maximum fees for VA appraisals and inspections are established by each VA Regional Loan Center for its area of jurisdiction.

Today's FHA and VA 9/24/13 43

Chapter 7 Quiz

1. In most cases, a VA loan requiresa. a funding fee; this amount may be financed.

b. a funding fee; this amount may not be financed.

c. mortgage insurance; this amount may be financed.

d. mortgage insurance; this amount may not be financed.

Chapter 7: VA Financing and Appraisal Overview

Today's FHA and VA 9/24/13 44

Chapter 7 Quiz

2. Existing construction is eligible for VA financing if a. on-site and off-site improvements are 50%

complete with a projected completion date in the next twelve months.

b. on-site and off-site improvements have been fully complete for six months.

c. on-site and off-site improvements have been fully complete for twelve months.

d. Only new construction is eligible for VA financing.

Chapter 7: VA Financing and Appraisal Overview

Today's FHA and VA 9/24/13 45

Chapter 7 Quiz

3. In selecting comparables for a condominium If a property requires improvements located in an area subject to regular flooding, but is not in a special flood hazard area, it is

a. eligible for appraisal.

b. eligible for appraisal as long as the problem has been adequately addressed in the engineering design.

c. eligible for appraisal, pending investigation of potential flood damage.

d. not eligible for appraisal.

Chapter 7: VA Financing and Appraisal Overview

Today's FHA and VA 9/24/13 46

Chapter 7 Quiz

4. An MPR for existing construction can be waived by the VA field office if:a. the property is approved from the standpoint of

safety and structural soundness, requiring only sanitary improvements for habitability.

b. the veteran and lender request the purchase verbally.

c. the veteran is under contract to purchase the property.

d. the veteran requests the exemption in writing.

Chapter 7: VA Financing and Appraisal Overview

Today's FHA and VA 9/24/13 47

Chapter 7 Quiz

5. ________________ employees may be designated as VA appraisers. a. Fannie Mae/Freddie Mac

b. HUD

c. Postal Service

d. State

Chapter 7: VA Financing and Appraisal Overview

Today's FHA and VA 9/24/13 48

Chapter 7 Quiz

6. To become a licensed VA appraiser, pre-requisite requirements for applicants include a. the applicant’s written acknowledgement of

assistance received while completing the demonstration report.

b. a demonstration appraisal that has not been appraised by members of the current panel.

c. evidence of a repayment plan and a promissory note for Federal delinquent debt balances.

d. a written exam.

Chapter 7: VA Financing and Appraisal Overview

Today's FHA and VA 9/24/13 49

Chapter 7 Quiz

7. Communication requirements for the VA appraiser includea. immediate notification for illness or emergencies when

assignments must be postponed.

b. immediate (same day) response to all inquiries (phone/fax/e-mail) from VA staff, lenders, or real estate agents, and all program participants.

c. a month’s advance notice in advance of being absent for vacations so that assignments can be rescheduled or moved to another appraiser.

d. someone available to answer the phone or an answering machine to record messages seven days a week.

Chapter 7: VA Financing and Appraisal Overview

Today's FHA and VA 9/24/13 50

Chapter 7 Quiz

8. The purpose of a VA loan is to offer mortgage loans guaranteed by the federal government witha. no down payment to all veterans, regardless of

circumstance.

b. no down payment to eligible veterans.

c. a small down payment to current U.S. military and their families.

d. a small down payment to eligible veterans.

Chapter 7: VA Financing and Appraisal Overview

Today's FHA and VA 9/24/13 51

Chapter 7 Quiz

9. When using the Sales Comparison Approach for a VA appraisal, a. multiple data sources are required.

b. multiple data sources are required with verification.

c. a single data source is sufficient with verification from closed transactions.

d. a single data source is sufficient without verification from closed transactions.

Chapter 7: VA Financing and Appraisal Overview

Today's FHA and VA 9/24/13 52

Chapter 7 Quiz

10. A VA appraiser is appraising a property located in a rural area with the closest comparable sales property located 15.9 miles away from the subject property. The Sales Comparison Approach states that the a. appraiser must attempt to find comparable property

sales in other areas.

b. appraiser must submit an extended comparison approval form.

c. appraiser will be unable to complete and must omit the property sales comparison section.

d. property is still applicable to be used for comparable sales.

Chapter 7: VA Financing and Appraisal Overview

Today's FHA and VA 9/24/13 53

Chapter 7 Quiz

11. A VA Fee Appraiser assistant may a. assist in drafting the appraisal report.

b. make the final value estimate.

c. select and analyze the comparables.

d. view the exterior of each comparable.

Chapter 7: VA Financing and Appraisal Overview

Today's FHA and VA 9/24/13 54

Chapter 7 Quiz

12. An example of a substantive negative work quality finding includesa. failing to provide required information on the

URAR.

b. failing to require necessary MPR repairs.

c. minor USPAP violations.

d. misreporting of distances between subject and comparables.

Chapter 7: VA Financing and Appraisal Overview

Today's FHA and VA 9/24/13 55