V RISK CONSIDERATIONS FOR SBA LENDERS banking, construction, distribution & packaging, food and...

33

VALUATION AND R ISK C ONSIDERATIONS FOR SBA L ENDERS N OVEMBER 1, 2017 | 11:30 AM E ASTERN B RAD B RUMBAUGH , CFA, CBA B OB B RUMBAUGH , MCMEA, BCA, MBA

Transcript of V RISK CONSIDERATIONS FOR SBA LENDERS banking, construction, distribution & packaging, food and...

VALUATION AND RISK CONSIDERATIONS FOR SBA LENDERS

NOVEMBER 1, 2017 | 11:30 AM EASTERN

BRAD BRUMBAUGH, CFA, CBABOB BRUMBAUGH, MCMEA, BCA, MBA

VALUATION AND RISK CONSIDERATIONS FOR SBA LENDERS

BIOGRAPHIES

VA

LUA

TIO

NA

ND

RIS

KC

ON

SID

ER

AT

ION

SF

OR

SB

A L

EN

DE

RS

Page |3

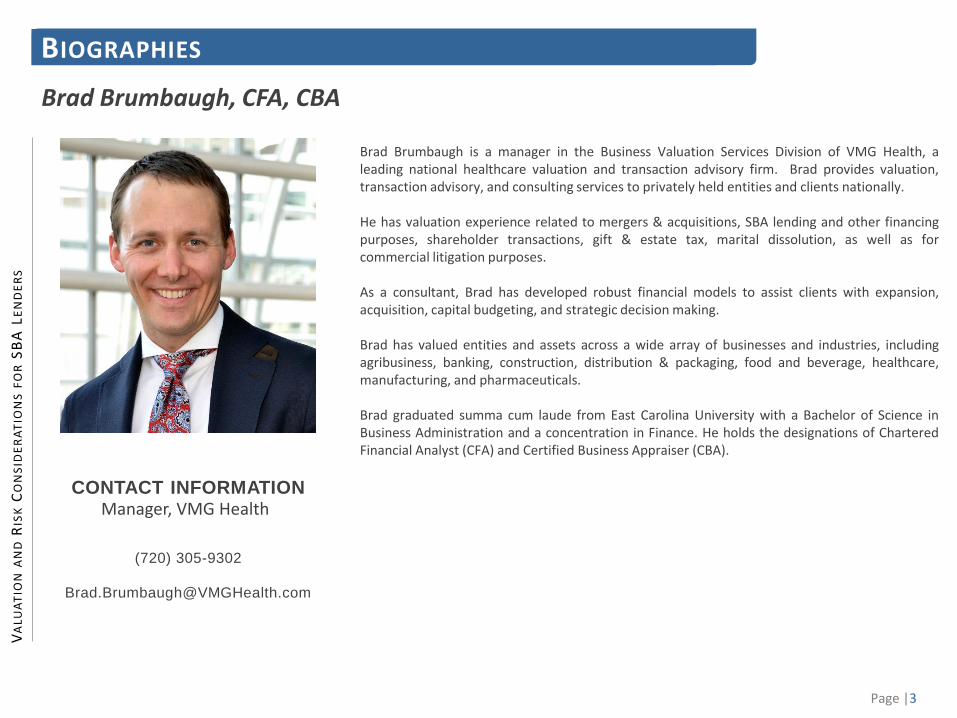

Brad Brumbaugh is a manager in the Business Valuation Services Division of VMG Health, aleading national healthcare valuation and transaction advisory firm. Brad provides valuation,transaction advisory, and consulting services to privately held entities and clients nationally.

He has valuation experience related to mergers & acquisitions, SBA lending and other financingpurposes, shareholder transactions, gift & estate tax, marital dissolution, as well as forcommercial litigation purposes.

As a consultant, Brad has developed robust financial models to assist clients with expansion,acquisition, capital budgeting, and strategic decision making.

Brad has valued entities and assets across a wide array of businesses and industries, includingagribusiness, banking, construction, distribution & packaging, food and beverage, healthcare,manufacturing, and pharmaceuticals.

Brad graduated summa cum laude from East Carolina University with a Bachelor of Science inBusiness Administration and a concentration in Finance. He holds the designations of CharteredFinancial Analyst (CFA) and Certified Business Appraiser (CBA).

Brad Brumbaugh, CFA, CBA

BIOGRAPHIES

CONTACT INFORMATION

(720) 305-9302

Manager, VMG Health

VA

LUA

TIO

NA

ND

RIS

KC

ON

SID

ER

AT

ION

SF

OR

SB

A L

EN

DE

RS

Page |4

Bob Brumbaugh is a Master Certified Machinery and Equipment Appraiser (MCMEA), one of only32 appraisers to have earned this designation. He is also a respected business broker andfinancial valuation consultant. Over the past several years, Bob has prepared Machinery /Equipment appraisals, Furniture Fixture & Equipment (FF&E) appraisals, and Inventory analysisreviews for most major national banks, regional lending institutions, SBA projects, and numerouscommunity banks.

Bob has delivered more than a thousand individual appraisal reports for a variety of projects. Hisexperience covers a wide range of industries including restaurants, food, packaging,manufacturing, medical, heavy equipment, farm, scientific laboratories, and more. One of Bob’sbest references is the FDIC for which he has appraised the assets of about 10% of all failed banksin the country over the past eight years. He has also assisted on numerous occasions withlitigation issues as an expert witness and has assisted with merger and acquisition facilitation byproviding appraisals and valuations for private industry.

Previously, Bob was active in the financial securities industry for more than twenty-seven years.As President and owner of a NASD/FINRA member broker/dealer, he originated several PrivatePlacement Regulation D, Section 504 and 506 security offerings, for funding of start-up anddevelopmental stage companies. Bob has also been an institutional equity trader.

During his business career, Bob has also been associated with the finance departments of TulaneUniversity, Wesleyan College, and an affiliate of the University of Phoenix as an adjunctprofessor. Additionally, he has sponsored and facilitated many CPA continuing education classeson capital formation topics. Bob has also served as a credit manager and controller of a majorcorporation.

Bob holds an MBA degree in Finance and Marketing from Western Michigan University and a BBAdegree in Management from Eastern Michigan University. He has also taken American Society ofAppraisers (ASA) Business Valuation courses, and is also a Business Certified Appraiser (BCA).

Bob Brumbaugh, MCMEA, BCA, MBA

BIOGRAPHIES

CONTACT INFORMATION

(919) 870-8258

Founder & CEO Brumbaugh Appraisals

VA

LUA

TIO

NA

ND

RIS

KC

ON

SID

ER

AT

ION

SF

OR

SB

A L

EN

DE

RS

Page |5

AGENDA

SBA Requirements

Business Appraisal Overview

I. Income ApproachII. Market ApproachIII. Cost Approach

I.

II.

Business Appraisal Overview – Report ElementsIII.

Questions & AnswersIV.

II.

III.

IV.

VALUATION AND RISK CONSIDERATIONS FOR SBA LENDERS

SBA REQUIREMENTS

VA

LUA

TIO

NA

ND

RIS

KC

ON

SID

ER

AT

ION

SF

OR

SB

A L

EN

DE

RS

Page |7

Property Types

SBA REQUIREMENTS

Special Purpose Properties:

Typically real estate intensive businesses (see next slide for examples)

Requires a Certified General Real Property Appraiser

Appraisal must allocate value to land, building, equipment and intangibleassets

Certified Equipment Appraiser may also be necessary

Non-Special Purpose Properties:

All other businesses not listed on the following slide

Requires Business Appraiser (ASA, CBA, ABV, CVA, or BCA)

1

2

The SBA classifies properties into two main categories:

VA

LUA

TIO

NA

ND

RIS

KC

ON

SID

ER

AT

ION

SF

OR

SB

A L

EN

DE

RS

Page |8

Examples of Special Purpose Properties (per SBA)

SBA REQUIREMENTS

If not listed, the valuation is a Non-Special purpose property and requires a

Business Appraiser

Amusement Parks Hotels, motels, and

other lodging facilities Marinas

Travel & Entertainment

Museums Railroads Theaters Wineries

Healthcare & Life Services

Funeral homes with crematoriumsHospitals, surgery centers, urgent care centers and other health or medical facilitiesNursing homes, including assisted living facilities

Bowling alleys Clubhouses Swimming pools

SportFacilities

Golf courses Sports arenas Tennis clubs

Car wash properties Gas stations Service centers

Auto Services

Farms Mines Oil wells

Natural Resources

Quarries Gravel pits

Other Cemeteries Cold storage facilities where more than 50% of total square footage is equipped for refrigerationDormitories Sanitary landfills

VA

LUA

TIO

NA

ND

RIS

KC

ON

SID

ER

AT

ION

SF

OR

SB

A L

EN

DE

RS

Page |9

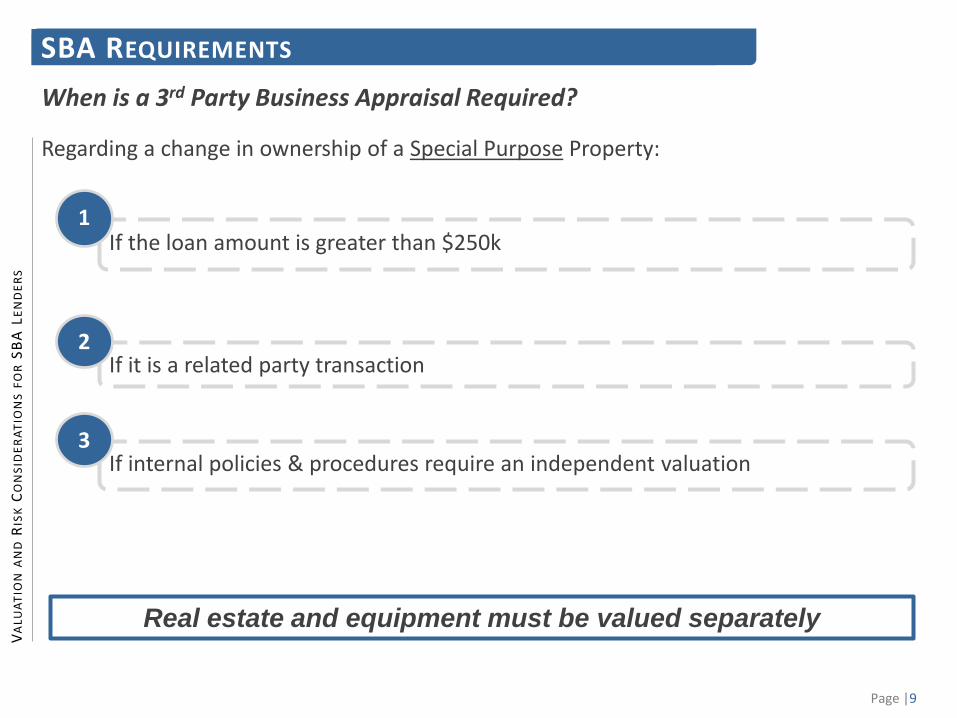

When is a 3rd Party Business Appraisal Required?

SBA REQUIREMENTS

Regarding a change in ownership of a Special Purpose Property:

If the loan amount is greater than $250k1

If it is a related party transaction2

If internal policies & procedures require an independent valuation3

Real estate and equipment must be valued separately

VA

LUA

TIO

NA

ND

RIS

KC

ON

SID

ER

AT

ION

SF

OR

SB

A L

EN

DE

RS

Page |10

When is a 3rd Party Business Appraisal Required?

SBA REQUIREMENTS

Regarding a change in ownership of a Non-Special Purpose Property:

If the amount being financed minus the appraised value of real estate and/or equipment is greater than $250k

1

If it is a related party transaction2

If internal policies & procedures require an independent valuation3

Real estate and equipment must be valued separately

VA

LUA

TIO

NA

ND

RIS

KC

ON

SID

ER

AT

ION

SF

OR

SB

A L

EN

DE

RS

Page |11

Recommendations:

Options When a 3rd Party Business Appraisal is NOT Required

SBA REQUIREMENTS

Limited scope / Calculation Engagement by a business

appraiser

1Internal valuation,

reviewed by business appraiser

2

More cost effective and reliable than internal valuation

VA

LUA

TIO

NA

ND

RIS

KC

ON

SID

ER

AT

ION

SF

OR

SB

A L

EN

DE

RS

Page |12

Accepted Business Appraisal Credentials

SBA REQUIREMENTS

Accredited Senior Appraiser (ASA)

Certified Business Appraiser (CBA)

Accredited in Business Valuation (ABV)

Certified Valuation Analyst (CVA)*

Business Certified Appraiser (BCA)

*Effective April 1, 2013, the National Association of Certified Valuators and Analysts' (NACVA) Accredited Valuation Analyst™ (AVA®)credential was merged into the Certified Valuation Analyst®(CVA®).

The SBA requires one of the following designations for Business Appraisal as a “Qualified Source”:

VALUATION AND RISK CONSIDERATIONS FOR SBA LENDERS

BUSINESS APPRAISAL OVERVIEW

VA

LUA

TIO

NA

ND

RIS

KC

ON

SID

ER

AT

ION

SF

OR

SB

A L

EN

DE

RS

Page |14

Business Appraisal Data Requirements

BUSINESS APPRAISAL OVERVIEW

Financials Minimum of 3 years’ Income Statements and Balance Sheets Interim Financials for the most recent reporting period Accounts Receivable Aging Schedule for the most recent reporting period Corporate Tax Returns for the last 3 years Financial Projections / Prospective Budget

23

Business Overview / Plan1

Operating/Partnership Agreement22

Fixed Asset List / Depreciation Schedule24

Employee Roster Including position, compensation level, and structure (i.e. salary, performance based, etc.)

25

Significant Contracts (e.g. non-compete, employment contracts, client contracts, etc.)26

Prior or concurrent Real Estate / Equipment Appraisals performed (if applicable)7

Necessary for all valuation methods

VA

LUA

TIO

NA

ND

RIS

KC

ON

SID

ER

AT

ION

SF

OR

SB

A L

EN

DE

RS

Page |15

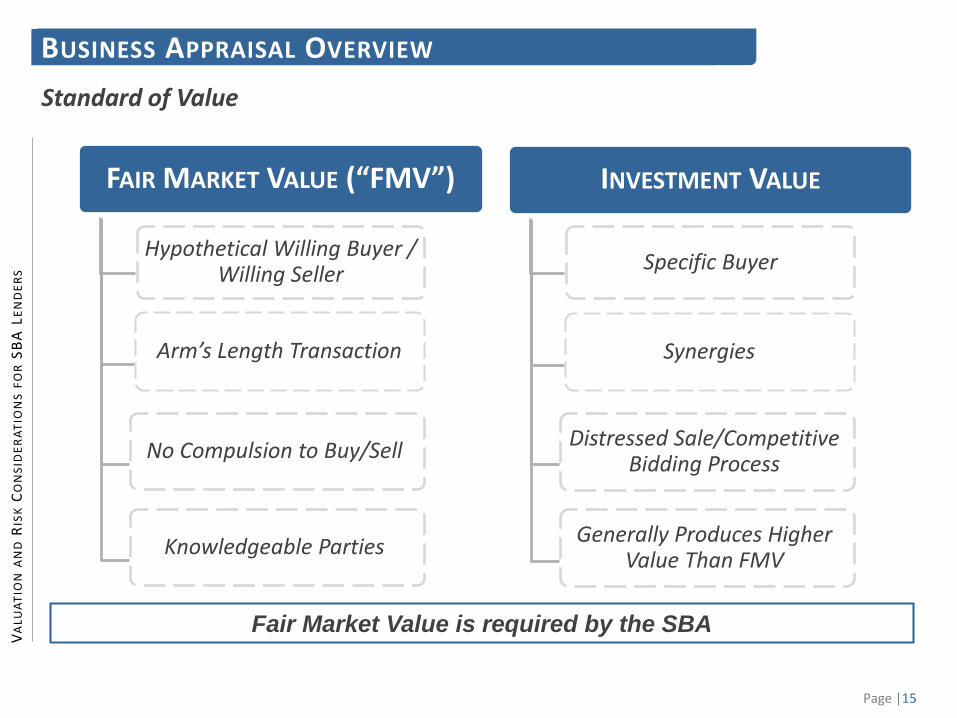

Standard of Value

BUSINESS APPRAISAL OVERVIEW

Fair Market Value is required by the SBA

Hypothetical Willing Buyer / Willing Seller

Arm’s Length Transaction

No Compulsion to Buy/Sell

Knowledgeable Parties

FAIR MARKET VALUE (“FMV”)

Specific Buyer

Synergies

Distressed Sale/Competitive Bidding Process

Generally Produces Higher Value Than FMV

INVESTMENT VALUE

VA

LUA

TIO

NA

ND

RIS

KC

ON

SID

ER

AT

ION

SF

OR

SB

A L

EN

DE

RS

Page |16

Fair Market Value vs. Investment Value

BUSINESS APPRAISAL OVERVIEW

Prudent buyers don’t pay for opportunities they bring to the table

Ability to drive revenue from other investments Negotiation power not realizable by most potential buyers

Revenues

Common deviations from FMV in projections representing Investment Value:

Expenses Ability to negotiate with suppliers based on related investments/unique relationships

Ability to eliminate certain job functions and expenses due to centralized functions Rent expense above/below market rates or excluded due to related party

ownership

Assumed ability to use excessive leverage over the long-termCapital Structure

VA

LUA

TIO

NA

ND

RIS

KC

ON

SID

ER

AT

ION

SF

OR

SB

A L

EN

DE

RS

Page |17

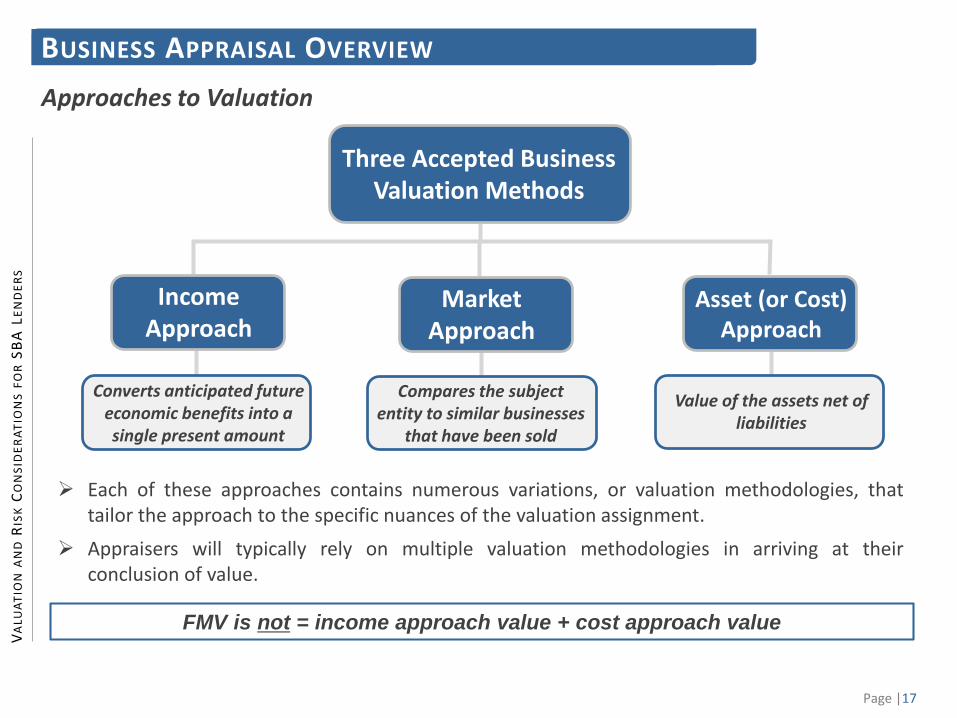

Approaches to Valuation

BUSINESS APPRAISAL OVERVIEW

Three Accepted Business Valuation Methods

Income Approach

Asset (or Cost) Approach

Compares the subject entity to similar businesses

that have been sold

MarketApproach

Converts anticipated future economic benefits into a single present amount

Value of the assets net of liabilities

Each of these approaches contains numerous variations, or valuation methodologies, thattailor the approach to the specific nuances of the valuation assignment.

Appraisers will typically rely on multiple valuation methodologies in arriving at theirconclusion of value.

FMV is not = income approach value + cost approach value

VA

LUA

TIO

NA

ND

RIS

KC

ON

SID

ER

AT

ION

SF

OR

SB

A L

EN

DE

RS

Page |18

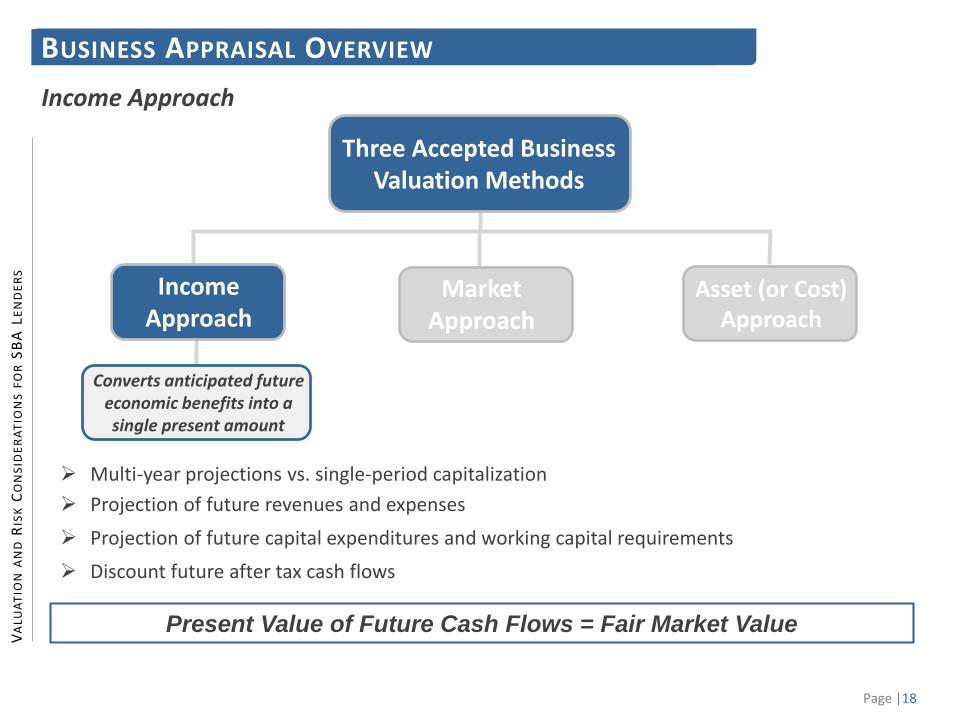

Income Approach

BUSINESS APPRAISAL OVERVIEW

Three Accepted Business Valuation Methods

Income Approach

Asset (or Cost) Approach

MarketApproach

Converts anticipated future economic benefits into a single present amount

Multi-year projections vs. single-period capitalization

Projection of future revenues and expenses

Projection of future capital expenditures and working capital requirements

Discount future after tax cash flows

Present Value of Future Cash Flows = Fair Market Value

VA

LUA

TIO

NA

ND

RIS

KC

ON

SID

ER

AT

ION

SF

OR

SB

A L

EN

DE

RS

Page |19

Red Flags for Review - Normalization Adjustments

BUSINESS APPRAISAL OVERVIEW – INCOME APPROACH

Were the following adjustments made to the revenues and/or expenses (where applicable)?

Revenue and expense adjustments are necessary for both Income and Market

Approach Methods

Occupancy adjustment

2

3

Non-recurring revenues and expenses One time revenue sources (e.g. government incentive programs) One time expenses (e.g. consulting / legal fees

1

Non-operating revenues and expenses Investment/rental income Personal auto expense Travel

2

Seasonality (i.e. use of annualized YTD vs. trailing twelve) 24

Owners Compensation 25

Corporate Federal and State Income taxes26

Charitable donations Expenses related to other businesses Interest payments

VA

LUA

TIO

NA

ND

RIS

KC

ON

SID

ER

AT

ION

SF

OR

SB

A L

EN

DE

RS

Page |20

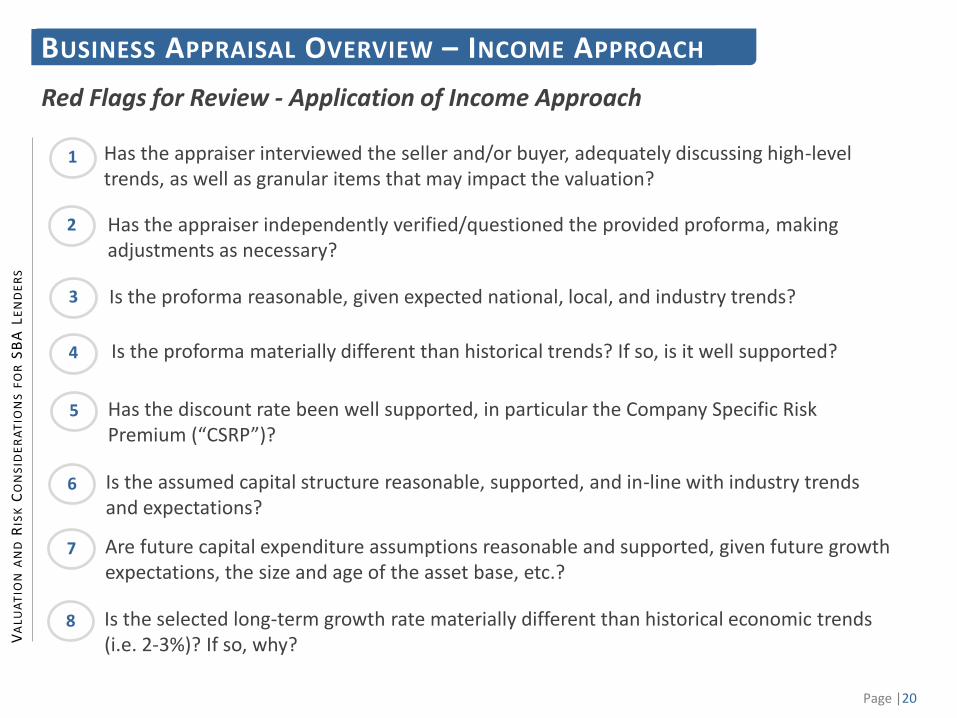

Red Flags for Review - Application of Income Approach

BUSINESS APPRAISAL OVERVIEW – INCOME APPROACH

Is the proforma reasonable, given expected national, local, and industry trends?

2

3

Has the appraiser interviewed the seller and/or buyer, adequately discussing high-level trends, as well as granular items that may impact the valuation?

1

2

Is the proforma materially different than historical trends? If so, is it well supported?

2

4

Has the discount rate been well supported, in particular the Company Specific Risk Premium (“CSRP”)?2

5

Is the assumed capital structure reasonable, supported, and in-line with industry trends and expectations?

6

Has the appraiser independently verified/questioned the provided proforma, making adjustments as necessary?

Are future capital expenditure assumptions reasonable and supported, given future growth expectations, the size and age of the asset base, etc.?

7

Is the selected long-term growth rate materially different than historical economic trends (i.e. 2-3%)? If so, why?

8

VA

LUA

TIO

NA

ND

RIS

KC

ON

SID

ER

AT

ION

SF

OR

SB

A L

EN

DE

RS

Page |21

Red Flags for Review - Company Specific Risk Factors (“CSRP”)

BUSINESS APPRAISAL OVERVIEW – INCOME APPROACH

Company Specific Risk Premium must be well supported

Local Demographic Trends Local Competitive Environment Location and Condition of Facility

Licensure Requirements Industry Trends Government / Regulatory Risk Pending / Threatened Litigation

Concentration Risk Functional or Technical

Obsolescence Ability to Attract/Retain Key Staff Duration and Relevance of

Contracts

Quality and Accuracy of Financial Data

Historical Financial Performance Liquidity Leverage / Borrowing Capacity

Perceived Risk in Projections

Geographic Risk

Financial Risk

Forecast Risk

Operational Risk

Industry/Regulatory

Risk

CSRP

VA

LUA

TIO

NA

ND

RIS

KC

ON

SID

ER

AT

ION

SF

OR

SB

A L

EN

DE

RS

Page |22

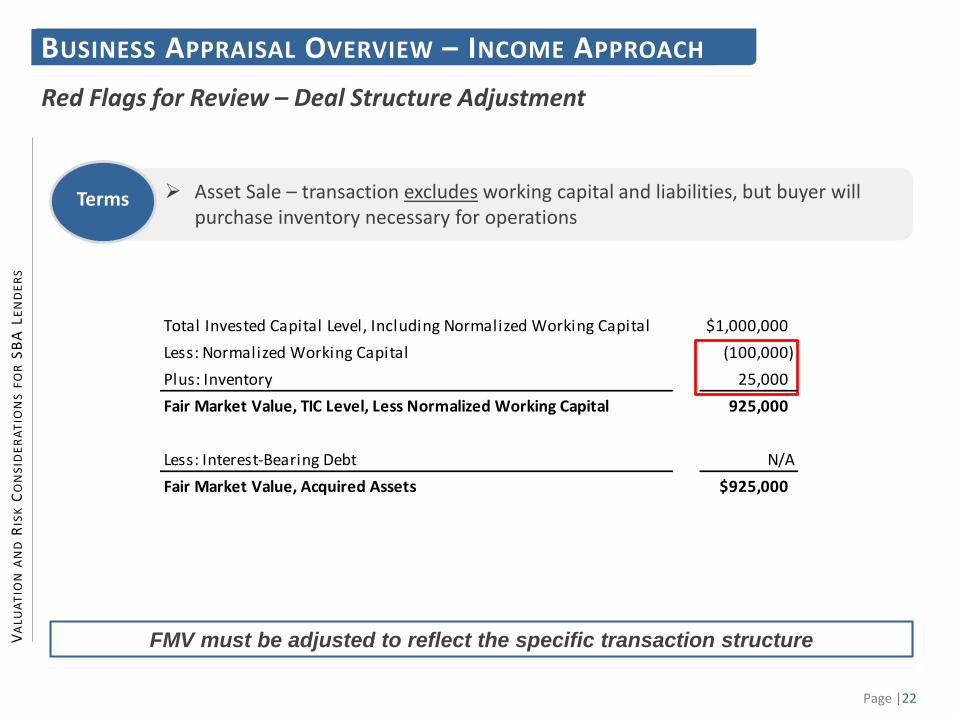

Red Flags for Review – Deal Structure Adjustment

Asset Sale – transaction excludes working capital and liabilities, but buyer will purchase inventory necessary for operations

Terms

FMV must be adjusted to reflect the specific transaction structure

BUSINESS APPRAISAL OVERVIEW – INCOME APPROACH

Total Invested Capital Level, Including Normalized Working Capital $1,000,000

Less: Normalized Working Capital (100,000)

Plus: Inventory 25,000

Fair Market Value, TIC Level, Less Normalized Working Capital 925,000

Less: Interest-Bearing Debt N/A

Fair Market Value, Acquired Assets $925,000

VA

LUA

TIO

NA

ND

RIS

KC

ON

SID

ER

AT

ION

SF

OR

SB

A L

EN

DE

RS

Page |23

Market Approach

BUSINESS APPRAISAL OVERVIEW

Three Accepted Business Valuation Methods

Income Approach

Asset (or Cost) Approach

Compares the subject entity to similar businesses

that have been sold

MarketApproach

Guideline Public Company and Merger & Acquisition Method

Estimates value by examining the value of similar businesses in a free and open market

Can be used as a reasonableness check for discounted cash flow value indication

Large transaction multiples are not relevant to small, local transactions

VA

LUA

TIO

NA

ND

RIS

KC

ON

SID

ER

AT

ION

SF

OR

SB

A L

EN

DE

RS

Page |24

Red Flags for Review - Application of Market Approach

BUSINESS APPRAISAL OVERVIEW – MARKET APPROACH

Do the market multiples align with those generated from the Income Approach? If not, is the deviation well supported?

2

3

Has the appropriate multiple been applied to the right metric and has that metric (i.e. net revenue, EBITDA, etc.) be adjusted to exclude non-recurring revenues and/or expenses?

1

Is the appraiser using known and reliable transaction databases (i.e. Pratt Stats, Bizcomps, IBA Database, etc.)?

2

4

Are the subject transactions from pure play comparables (i.e. is a transaction from a similar business, but has multiple different service lines)?

5

2 Are the observed transactions/multiples from firms of a similar size, industry, and region?

Is a blend of metrics being used to generate the value (i.e. revenue and SDE multiple)? If not, is the use of a single metric well supported?

6

Is the concluded value consistent with the specific deal terms (i.e. are the multiples based on stock or asset sales, and have they been adjusted accordingly)?

7

VA

LUA

TIO

NA

ND

RIS

KC

ON

SID

ER

AT

ION

SF

OR

SB

A L

EN

DE

RS

Page |25

Date Target Description MVIC Price Revenue SDE EBITDA P/Rev P/SDE P/EBITDA

12/29/16 Machine Shop $1,550,000 $2,207,000 $551,000 $372,000 0.70 2.81 4.17

02/01/16 Manufacturer of Metal Parts $19,500,000 $29,350,000 $5,025,000 $4,600,000 0.66 3.88 4.24

04/18/16 Machine Shop $745,000 $2,874,740 $62,929 ($8,025) 0.26 11.84 N/A

10/31/15 Aerospace Machine Shop $3,450,000 $1,883,792 $407,712 $207,712 1.83 8.46 16.61

11/09/94 Manufactures Fiberglass Products $300,000 $487,007 $13,184 $51,717 0.62 22.75 5.80

10/20/04 Manufacturer of Sport and Recognition Plaques $7,140,000 $619,592 $0 $62,426 11.52 N/A 114.38

12/31/12 Precision Machining Manufacturing & Distribution $825,000 $1,225,551 $127,959 $2,631 0.67 6.45 313.57

Red Flags for Review – Selecting Comparable Transactions

BUSINESS APPRAISAL OVERVIEW – MARKET APPROACH

Subject Entity:

Machining and Metal Fabrication Shop $1.5 MM annual revenue; $200k SDE; $100k EBITDA

Transaction Search in Pratts Stats Database:

Industry codes related to machining / metal fabrication 200+ transactions Dates ranging from 1994 to present Revenue ranging from $34k to $845 MM SDE ranging from ($900k) to $5 MM EBITDA ranging from ($6.9 MM) to $56 MM

Transactions must be scrubbed for comparability to the subject entity

VA

LUA

TIO

NA

ND

RIS

KC

ON

SID

ER

AT

ION

SF

OR

SB

A L

EN

DE

RS

Page |26

Cost Approach

BUSINESS APPRAISAL OVERVIEW

Three Accepted Business Valuation Methods

Income Approach

Asset (or Cost) Approach

MarketApproach

Value of the assets net of liabilities

Estimates the cost to recreate the business

Measures value by identifying and individually valuing the business’s tangible and intangibleassets and liabilities

Considered to provide a “floor” or lowest minimum value related to a business

Separate Real Estate and Fixed asset appraisals are generally required

VA

LUA

TIO

NA

ND

RIS

KC

ON

SID

ER

AT

ION

SF

OR

SB

A L

EN

DE

RS

Page |27

Red Flags for Review - Application of Cost Approach

BUSINESS APPRAISAL OVERVIEW – COST APPROACH

Are only operating assets considered (i.e. real estate owned by a related party, but not held within the subject entity should not be included)?

2

4

Have the assets been individually appraised at fair market value by a certified specialist (i.e. equipment appraiser)?

1

3

Have amounts on the balance sheet been adjusted to exclude assets and liabilities to continue to be held by the seller (i.e. working capital, long-term debt)? 2

2

Have identifiable and transferrable intangible assets been separately appraised and accounted for?

VA

LUA

TIO

NA

ND

RIS

KC

ON

SID

ER

AT

ION

SF

OR

SB

A L

EN

DE

RS

Page |28

12/31/XX Adjustments FMV Comments

ASSETSCash and Equivalents 25,000 (25,000) 0 Per deal terms, excluded

Accounts Receivable 50,000 (50,000) 0 Per deal terms, excluded

Inventories 100,000 (20,000) 80,000 Per Inventory Analysis

Current Assets 175,000 80,000

Furniture and Fixtures 300,000 (225,000) 75,000 Per Equipment Appraisal

Personal Auto 30,000 (30,000) 0 Excluded, personal asset

Gross Fixed Assets 330,000 75,000

less: Accumulated Depreciation (150,000) 150,000 0 Accounted for above

Net Fixed Assets 180,000 75,000

Total Assets 355,000 155,000

LIABILITIESAccounts Payable 15,000 (15,000) 0 Per deal terms, excluded

Current Portion of Long-term Debt 50,000 (50,000) 0 Per deal terms, excluded

Current Liabilities 65,000 0

Long-term Debt 200,000 (200,000) 0 Per deal terms, excluded

Long-term Liabilities 200,000 0

Total Liabilities 265,000 0

Equity 90,000 155,000 = Assets minus Liabilities

Indicated FMV of Acquired Assets 155,000

Red Flags for Review – Deal Structure Adjustments

BUSINESS APPRAISAL OVERVIEW – COST APPROACH

Net Book Value does not = Fair Market Value

Exclude cash, AR, current liabilities & LT debt1

Asset Sale – transaction excludesworking capital and liabilities, but buyer will purchase inventory necessary for operations.

Terms

Exclude non-operating assets (e.g. personal auto)2

Adjust all transferrable assets to FMV based on appraisals performed by specialists

3

VALUATION AND RISK CONSIDERATIONS FOR SBA LENDERS

BUSINESS APPRAISAL OVERVIEW – REPORT ELEMENTS

VA

LUA

TIO

NA

ND

RIS

KC

ON

SID

ER

AT

ION

SF

OR

SB

A L

EN

DE

RS

Page |30

Red Flags for Review – Report Elements

BUSINESS APPRAISAL OVERVIEW – REPORT ELEMENTS

National and Local Economic Overview “Why” and “how” the national/local economic and industry trends impact the subject entity

3

All report sections must explain the “why”, not just the “what”1

Sometimes, less is more2

Historical Financials Have material variances in historical financials been explained, discussed, and accounted for? If adjustments have been made to the financials, are they well supported and documented?

2

4

2

50+ pages does not necessarily = high quality

Management Interview / Projections Has the appraiser interviewed the seller and/or buyer, adequately discussing high-level trends, as

well as granular items that may impact the valuation? Has the appraiser independently verified/questioned the provided proforma, making adjustments

as necessary?

5

VA

LUA

TIO

NA

ND

RIS

KC

ON

SID

ER

AT

ION

SF

OR

SB

A L

EN

DE

RS

Page |31

Red Flags for Review – Report Elements (Continued)

BUSINESS APPRAISAL OVERVIEW – REPORT ELEMENTS

Market Approach Is there adequate discussion regarding the selection process of comparable transactions multiples,

and is it consistent with the overall fact pattern (i.e., economic/industry trends, company specific risk, etc.)

7

Income Approach Is the proforma reasonable, given expected national, local, and industry trends? Is the proforma materially different than historical trends? If so, is it well supported? Has the discount rate been well supported, in particular the Company Specific Risk Premium (“CSRP”)? Is the assumed capital structure reasonable, supported, and in-line with industry trends and expectations? Are future capital expenditure assumptions reasonable and supported, given future growth expectations, the size

and age of the asset base, etc.? Is the selected long-term growth rate materially different than historical economic trends (e.g. 2-3%)? If so, why?

6

2

50+ pages does not necessarily = high quality

Valuation Reconciliation Is there adequate support for the weighting among valuation approaches/methods used? Is there a material deviation among relied upon approaches, and has this been discussed?

8

VALUATION AND RISK CONSIDERATIONS FOR SBA LENDERS

QUESTIONS & ANSWERS

VA

LUA

TIO

NA

ND

RIS

KC

ON

SID

ER

AT

ION

SF

OR

SB

A L

EN

DE

RS

Page |33

Brad Brumbaugh, CFA, CBAManager, VMG Health200 Columbine Street, Suite 350Denver, CO 80206Direct (720) [email protected]

CONTACT INFORMATION

Bob Brumbaugh, MCMEA, BCA, MBAFounder & CEO, Brumbaugh Appraisals8601 Six Forks Road, Suite 400Raleigh, NC 27615Direct (919) [email protected]