V I S I O N · V I S I O N To be the pre-eminent financial institutionin Pakistan and achieve...

26

V I S I O N To be the pre-eminent financial institution in Pakistan and achieve market recognition both in the quality and delivery of service as well as the range of product offering. M I S S I O N To be recognized in the market place by Institutionalizing a merit & performance culture, Creating a powerful & distinctive brand identity, Achieving top-tier financial performance, and Adopting & living out our core values.

Transcript of V I S I O N · V I S I O N To be the pre-eminent financial institutionin Pakistan and achieve...

V I

S I

O N To be the pre-eminent financial institution

in Pakistan and achieve market recognitionboth in the quality and delivery of serviceas well as the range of product offering.

M I

S S

I O

N To be recognized in the market place byInstitutionalizing a merit & performanceculture, Creating a powerful & distinctivebrand identity, Achieving top-tier financialperformance, and Adopting & living outour core values.

BULLETINECONOMICSeptember - October 2003

Contents

§ Editor’s Corner ii§ Abstract of the Bulletin 04§ Small and Medium Enterprises

Promoting their growth in Pakistan 05§ Pakistan’s Bond Market 12§ Cotton – Current Demand and Supply Position 16§ Pak Trade with Islamic Countries 19§ Market Analysis 21§ Banks’ Performance at a Glance 23§ Key Economic Indicators 24

NBP Performance at a Glance

BULLETINECONOMICSeptember - October 2003

ii

Dear readers,

There is a growing interest worldwide in improving the performance of the financial sector through morestringent regulation and supervision. The objectives of financial sector regulation are broadly speaking;to safeguard the stability of the financial system, to promote efficiency in the operation of financial marketsand to provide adequate protection to consumers of financial services.

Prudential regulation is a form of regulatory activity, with its main focus on the safety and soundness offinancial institutions. It generally seeks to ensure that financial institutions have adequate resources tosupport the volume and nature of business undertaken, provide some minimum level of assurance toconsumers about the financial soundness and integrity of financial institutions, ensures that financialinstitutions manage and monitor risks, keeps a close scrutiny of the quality and strategy of management,relies on professional experts among others.

The State Bank of Pakistan has established prudential regulations that act as the ground rules and guidelinesfor the financial industry. These mostly pertain to capital adequacy, quality of assets, management,classification and provisioning for loans, risk concentration, etc. Banks and development financial institutionsare expected to operate within this framework and conduct their business in a safe and sound manner,taking into account the risks associated with their activities. It is the State Bank’s intention to help developthe banks’ internal capacity.

While regulations, have been in force for more than a decade, periodic revisions are made to improve uponthe regulatory regime by the State Bank. Given the changes and new developments in the financial markets,the existing prudential regulations have been updated and have incorporated some of the best internationalpractices. Separate sets of prudential regulations have been issued for Corporate/Commercial Bank, SMEFinancing, Mircofinance Banks/Institutions, and Consumer Financing. Earlier banks were applying thesame single set of rules for all these sectors. The new Prudential Regulations would come into effect fromJanuary 1, 2004, giving banks time to prepare themselves for complying with the new set of rules.

The new Prudential Regulations for Corporate/Commercial Banking have four different sections, RiskManagement, Corporate Governance, Know Your Customer and Anti Money Laundering, and Operations.For SME Financing and Consumer Financing the separate set of regulations cover only the Risk Managementcategory, as for the remaining categories the Prudential Regulations for Corporate Banking would beapplicable.

The new set of prudential regulations for SMEs is expected to encourage banks and development financialinstitutions to develop new products to meet the financing requirements of SMEs, be more pro-activelyinvolved with the SMEs, than what they have been doing historically, or, in other words, let the SMEsbecome the focus for a significant portion of their lending portfolio.

Editor’s Corner

BULLETINECONOMICSeptember - October 2003

iii

This would assist the government’s Poverty Reduction Strategy, as SMEs have been identified as one ofthe four sectors to lead the revival of economic growth. A key economic determinant of poverty in Pakistanhas been the sluggish investment levels, particularly in the labour intensive sectors. If banks/DFIs enhancetheir lending to SMEs, it could go a long way in reviving economic activity, providing employmentopportunity, kick start the economy, particularly, industrial activity, and lead to better human development.

As there are no general or universal programmes to provide social safety nets for the poor, a number ofprogrammes are operating to respond to the needs of the poor. Microfinance is one such scheme, whichenables the poor to gain access to capital to finance investment in income generating activities. Consumerfinancing would allow individuals to meet their personal or household needs. It should help stimulatecapital investment and spur economic growth.

As such, State Bank of Pakistan while encouraging and promoting self-regulation, developing effectiverisk management capabilities in the banks/DFIs, improving corporate governance is at the same time lendingsupport to the government’s efforts at poverty alleviation.

4

BULLETINECONOMICSeptember - October 2003

Abstract of the BulletinSmall and Medium Enterprises – Promoting theirgrowth in Pakistan

§ Small and medium enterprises play a fundamentalrole in promoting economic and industrial production.They have linkages with larger enterprises andcontribute towards value addition and exports.

§ SMEs have strong links with growth, employmentand poverty reduction.

§ Recognizing the strength of SMEs, the governmentof Pakistan has established the SME Bank, and Smalland Medium Enterprise Development Authority withthe objective to launch an aggressive SMEdevelopment strategy.

§ Given the importance of SMEs in the economicdevelopment of Pakistan, and to encourage the flowof bank credit to this sector, a separate set ofPrudential Regulations specifically for SMEs havebeen issued by the State Bank of Pakistan.

§ These regulations should encourage banks/DFIs todevelop new financing techniques and innovativeproducts to meet the financial requirements of SMEs.

Pakistan’s Bond Market

§ Bonds are debt instruments, which can help raisefunds for long term investment projects and shortterm financial needs.

§ The bond market plays an active role in mobilizingand channeling savings into productive investmentthat promote economic growth and providesinfrastructure for the development of a soundfinancial system.

§ Pakistan’s bond market is at an early stage ofdevelopment. It currently covers debt and debt likesecurities issued by the government, statutorycorporations and corporate entities. The governmentissues dominate the bond market. The market sizeis much smaller compared to many developedcountries.

§ The issuing and trading of corporate debt securitiesin not a new phenomenon in Pakistan. During the

1960s and early 1970s, corporate debentures issuedby Pakistani companies were listed on the stockexchanges. This activity came to a stand still afterthe nationalization of financial institutions in 1972.

§ Since 1995, several measures have been taken bythe government to promote bond market in Pakistan.The economic environment for a healthy corporatebond market is much favourable now. Currently theTerm Finance Certificates and Pakistan InvestmentBonds provide an attractive opportunity for theinvestors.

Cotton – Current Demand and Supply Position

§ Current cotton crop has been affected by heavy rainsand pest attack.

§ As consumption requirement of mills has grown ataround 12 million bales, the gap is met throughimports.

§ Price of cotton has risen in the local cotton marketand this has had an affect on the textile sector, whichcontinues to dominate the industrial activity in thecountry, contributing the major share of exportearnings and as a major employer of industriallabour force.

Pak Trade with Islamic Countries

§ Pakistan enjoys cordial trade relations with Islamiccountries.

§ It imports petroleum and products from Saudi Arabia,Kuwait, UAE and Iran, and exports textile products,rice, leather, fruits and vegetables etc.

Market Analysis

§ The market underwent a major correction inSeptember and October 2003. Negative sentimentwas fuelled by expectations of a rise in interest ratesand new regulations governing bank investingactivities in equity markets.

§ Draft rules announced on margin financing did littleto help market sentiment. It will take some time forshattered confidence to be restored and the marketrecovery is expected to be gradual.

Small and Medium Enterprises – Promotingtheir growth in Pakistan

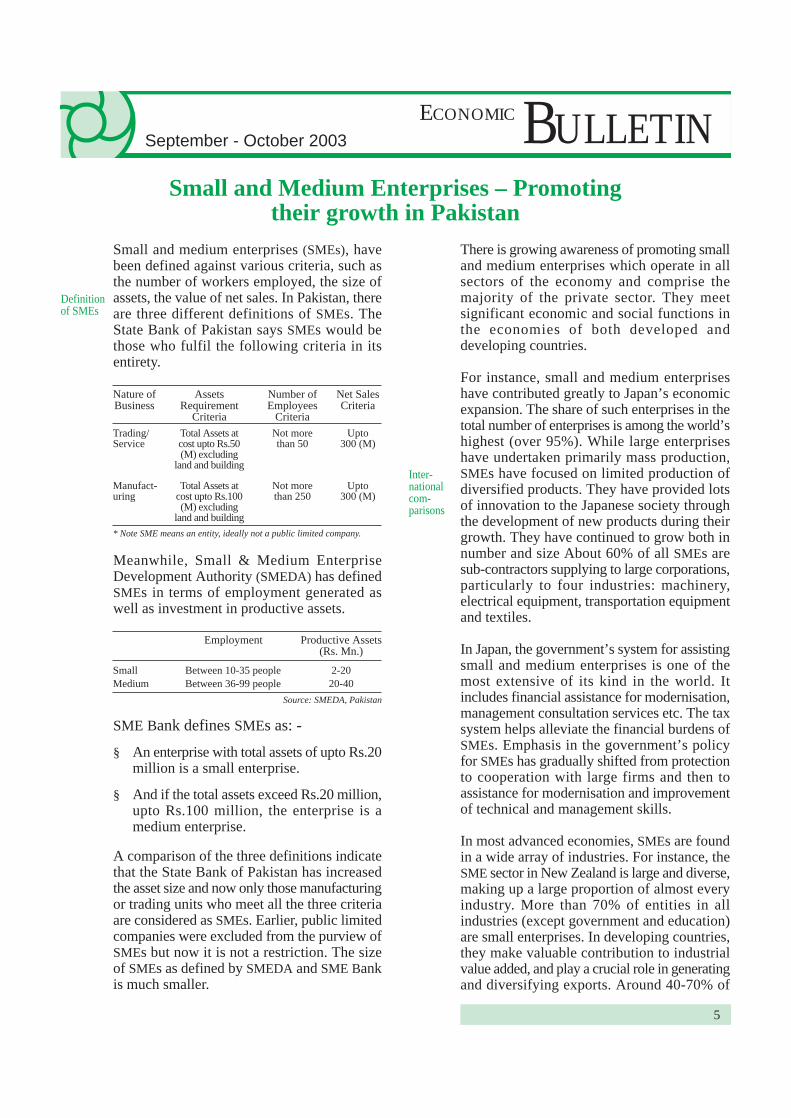

Small and medium enterprises (SMEs), havebeen defined against various criteria, such asthe number of workers employed, the size ofassets, the value of net sales. In Pakistan, thereare three different definitions of SMEs. TheState Bank of Pakistan says SMEs would bethose who fulfil the following criteria in itsentirety.

Definitionof SMEs

5

BULLETINECONOMICSeptember - October 2003

Nature ofBusiness

AssetsRequirement

Criteria

Number ofEmployees

Criteria

Net SalesCriteria

Trading/Service

Total Assets atcost upto Rs.50(M) excluding

land and building

Not morethan 50

Upto300 (M)

Manufact-uring

Total Assets atcost upto Rs.100(M) excluding

land and building

Not morethan 250

Upto300 (M)

* Note SME means an entity, ideally not a public limited company.

Meanwhile, Small & Medium EnterpriseDevelopment Authority (SMEDA) has definedSMEs in terms of employment generated aswell as investment in productive assets.

Employment Productive Assets(Rs. Mn.)

SmallMedium

Source: SMEDA, Pakistan

Between 10-35 peopleBetween 36-99 people

2-2020-40

SME Bank defines SMEs as: -

§ An enterprise with total assets of upto Rs.20million is a small enterprise.

§ And if the total assets exceed Rs.20 million,upto Rs.100 million, the enterprise is amedium enterprise.

A comparison of the three definitions indicatethat the State Bank of Pakistan has increasedthe asset size and now only those manufacturingor trading units who meet all the three criteriaare considered as SMEs. Earlier, public limitedcompanies were excluded from the purview ofSMEs but now it is not a restriction. The sizeof SMEs as defined by SMEDA and SME Bankis much smaller.

There is growing awareness of promoting smalland medium enterprises which operate in allsectors of the economy and comprise themajority of the private sector. They meetsignificant economic and social functions inthe economies of both developed anddeveloping countries.

For instance, small and medium enterpriseshave contributed greatly to Japan’s economicexpansion. The share of such enterprises in thetotal number of enterprises is among the world’shighest (over 95%). While large enterpriseshave undertaken primarily mass production,SMEs have focused on limited production ofdiversified products. They have provided lotsof innovation to the Japanese society throughthe development of new products during theirgrowth. They have continued to grow both innumber and size About 60% of all SMEs aresub-contractors supplying to large corporations,particularly to four industries: machinery,electrical equipment, transportation equipmentand textiles.

In Japan, the government’s system for assistingsmall and medium enterprises is one of themost extensive of its kind in the world. Itincludes financial assistance for modernisation,management consultation services etc. The taxsystem helps alleviate the financial burdens ofSMEs. Emphasis in the government’s policyfor SMEs has gradually shifted from protectionto cooperation with large firms and then toassistance for modernisation and improvementof technical and management skills.

In most advanced economies, SMEs are foundin a wide array of industries. For instance, theSME sector in New Zealand is large and diverse,making up a large proportion of almost everyindustry. More than 70% of entities in allindustries (except government and education)are small enterprises. In developing countries,they make valuable contribution to industrialvalue added, and play a crucial role in generatingand diversifying exports. Around 40-70% of

Inter-nationalcom-parisons

BULLETINECONOMICSeptember - October 2003

6

the value added originates from only a fewindustries, usually food & beverages, jewellery& gems, leather & leather products, furniture,textiles, wood & products and handicrafts.

In Pakistan the SME sector can be the engineof growth, given the large number ofopportunities in the services sector, in theagriculture sector and in the industrial sector.They have however not been able to deriveoptimal benefits from time to time. This islargely because of the problems the SMEs facein Pakistan.

Pakistan National Human Development Report2003, UNDP has highlighted constraints to therapid growth of small scale enterprises in smalltowns of Pakistan. Following are the majorconstraints: -

· Inability of small units to get vendingcontracts for the manufacture of componentsfrom the LSM sector.

· Due to lack of expertise in productionmanagement, the frequent inability to achieve

Cons-traintsto growthof SMEs

quality control, and to meet tight deliveryschedules.

· Lack of specific skills like advanced millwork, metal fabrication, precision welding, all ofwhich are needed for producing quality productswith low tolerances and precise dimensional control.In other cases accounting and management skillsmay be inadequate.

· Difficulty faced by small units in gettinggood quality raw materials, which often canonly be ordered in bulk (for which the smallentrepreneurs do not have the workingcapital), and from distant large cities.

· Lack of specialized equipment.

· Absence of fabrication facilities such asforging, heat treatment and surface treatmentwhich are required for manufacture of highvalue added products, but are too expensivefor any one small unit to set up.

· Lack of capital for investment and absenceof credit facilities.

Excerpts from Governor SBP’s SpeechAddressed at the SMEDA-IBP Seminar

Box

In his key note address at the SMEDA-IBP seminar on “Issue ofSME Financing” held at Lahore on October 24, 2003, Dr. IshratHusain, Governor State Bank of Pakistan, has talked about themajor players who have to work together in a coordinated mannerto contribute to the success of the SMEs. We reproduce here someexcerpts from his speech: -

· First, the government and the regulatory agencies such as the StateBank of Pakistan should provide conducive enabling environment forSMEs to operate. This means that macro economic policies are sound,regulatory regime is supportive and legal system enforces contractsand property rights. In the past the SROs were being used to favourcertain individuals or tariffs were raised to protect selective groupsor banks loans were given to supporters of the ruling parties. In thepast four years, however, these practices have been done away andneither any SRO has been issued nor any preference in the tariff hasbeen given.

· The SBP reviewed its own role to determine whether or not it was creatingany hurdles in the way of lending to SMEs. We found out that the sameprudential regulations which applied to corporate borrowers were alsomade applicable to consumer, SME, Micro finance although the

requirements were different for each market segment. We therefore decidedto formulate a separate set of regulations for SMEs.

· The second player in this process is the Provincial and the localGovernments. They have to allocate and earmark land for setting upindustrial estates and deliver the infrastructure facilities in these estates.

· The third player is the Provincial Small Industries Corporations whichused to provide common technical service centres such as design,fabrication, foundry, repair workshops, marketing outlets and otherservices to the SMEs. As the performance of this type of public sectorcorporations has not been very satisfactory in the past it is time toconsider a public-private partnership in which the management andoperations of these facilities and centres are entrusted to the privatepartners.

· Fourth, organizations such as SMEDA have to play a critical role inthe business development support, advisory services and managerialtraining of SMEs. SMEDA can design simplified standardized bookkeeping, inventory management and ledger forms which can aid inthe preparation of financials.

· Fifth, there is a widespread network of technical and vocational traininginstitutes and polytechnics throughout the country. The provincialgovernments who own these institutes should examine the contentsand curriculum, pedagogical tools, evaluation and assessment procedure,

SMEsandemploy-mentgenera-tion

SMEs role in the generation of employment,creation of income for a significant number oflow income workers and for filling the domesticdemand for low cost goods and services issignificant. Unemployment and poverty areformidable challenges faced by a large segmentof the population of many developing countriesof Asia and the Pacific.

Rapid economic growth is a necessary conditionfor poverty reduction. Growth resulting in theincreased capacity of the domestic labour marketto absorb surplus labour is key to fightingpoverty. Growth creates jobs that use labour,the main asset of the poor. As growth proceeds,private sector employment becomes the majorsource of economic support for the majority ofworkers and their families. SMEs play a centralrole in the development of private sector activity,in both urban and rural areas.

SME could be those with larger plant size andusing modern technology often linked withlarge enterprises as sub-contractors andproducing modern consumer and manufacturingproducts. These are mostly present in the urbanareas. Then there is the traditional SME sector,consisting of artisans, workshops, craftindustries which are normally found in ruralareas. There is a third category of SMEs, theagro-based industries, most often found in semi-urban areas.

In Pakistan, approximately 220,000 SMEsoperate, which provide employment to over80% of the labour force, contribute around 50%

incentive structure for the faculty members and bring about thenecessary changes to align the supply of the graduates with theemerging needs of the SME sector.

· Sixth, the SME Bank alone cannot cater to the needs of the entiresector but it could develop a prototype of program lending, creditappraisal and delivery methodology, standardized documentation,monitoring mechanisms which can be replicated and followed byother commercial banks.

· Seventh, the commercial banks, leasing industry, modarabas themselveshave to develop dedicated groups for servicing the SMEs. They shouldestablish their presence and branches at the clusters and places suchas Daska, D. I. Khan, Wazirabad, Khairpur, Kotri, Gwadar whichhave large untapped potential. The banking industry has to invest inpeople, processes and systems to minimize their risks and enhancetheir returns on the SME segment.

· Eighth, the Institute of Bankers has to play a role. As this is a newfield of endeavour the banking staff have to be imparted training

in credit appraisal, documentation, approval, monitoring and recoveryand his can be done under the auspices of IBP.

· Ninth, the large firms have a major role to play in the promotion andgrowth of SMEs through sub-contracting arrangements. These largefirms can also leverage their standing with the financial institution byborrowing at fine margins in their own name and advancing this totheir sub-contractors and vendors. They can deduct the amountsadvanced from the payments due for the goods supplied or servicesrendered.

· Finally, the associations of SMEs should launch awareness programmesamong their members about the opportunities that are already available,assist them in linking up with the appropriate support institutions,listen to the genuine difficulties and problems faced by their membersand articulate them to the right quarters.

· The State Bank of Pakistan would very much like the SME financingto become a mainstream activity of the banks in Pakistan.

BULLETINECONOMICSeptember - October 2003

7

to GDP, and more than 50% towards exportearnings. They help the women in both theurban and rural areas to utilize their vocationalskills and contribute and support the largeindustrial establishments. With populationgrowing at 2.1% per annum and addition of 3.1million persons every year, the growing labourforce is a formidable challenge facing Pakistan.

The size of the labour force is around 43 million,where 70% reside in rural areas and 30% inurban areas. The government acknowledgesthe repercussions of growing unemploymentand has taken steps to create job opportunities.These include among others, the developmentof small and medium enterprises, as it wouldhelp in generating jobs on a large scale.

In countries with growing population theprobability of getting employment is low, whichis reflected in low human resource development.Most are poor because of their inability to geta job. The unemployment problem hascompounded in Pakistan because of theincreased frequency of negative growth yearsin some of the major crops. The slowdown ingrowth and increased instability of output inmajor crops has resulted in sharply increasedrural poverty. This alongwith slow growth oflarge scale manufacturing has made thingsworse.

In most success stories of economicdevelopment, the growth of SMEs has beencentral, particularly in providing employment

SMEsin China

SMEsandpovertyalleviation

SMEsandexportpromotion

for poor people. In the case of China, theTownship and Village Enterprise have playedthis role. In response to an initial set of reformsthat created a better investment climate in theearly 1980s, these enterprises sprung up quicklyand generated a large amount of employmentand income. Their success has contributed muchto China’s growth and poverty reduction.

SMEs in Bangladesh have contributedsignificantly to manufacturing growth andemployment creation. There are around 27,000medium sized enterprises and around 150,000small scale enterprises in the country. 80% ofmanufacturing establishments are SMEsaccounting for 80% of the labour force. Thegarments industry has contributed to SMEdevelopment through orders for accessories,packaging materials etc, while the footwearindustry increased sub-contracts to SMEs. InThailand SMEs account for 70% of employmentin the industrial sector, where the main industrieswhich are dominated by SMEs include metaland steel, plastic products, rubber and garments.

It is not only in developing countries likePakistan, where SMEs help in job creation, butan ILO report on “General conditions tostimulate job creation in small and mediumsized enterprises” (1995) show that small andmedium sized enterprises are major contributorsto private sector employment in the industrial-ised countries. SME employment in membercountries accounts for between 57% (US) and81% (Italy) of employment in industry andmarket services combined. The share of smallenterprises alone ranges from 44% (Canada)to 71% (Italy).

The focus on development of small scaleindustries, which have a low gestation period,are labour intensive and can generate a largeoutput per unit of investment compared to thelarge scale manufacturing sector would notonly accelerate economic growth in the mediumterm at relatively low levels of investment, butwould also increase employment and exportsfor given levels of GDP growth.

SME development is an effective tool toalleviate poverty. In our part of the world, thefundamental challenge is poverty reduction, asnearly two-thirds of the world’s poor live inAsia. In Pakistan, the incidence of poverty has

BULLETINECONOMICSeptember - October 2003

8

increased over the years and is currently ataround 32%, with a higher percentage in ruralthan urban areas.

The governments have over the years takeninitiatives at helping the poor. The Governmentof Pakistan’s Poverty Reduction Strategy aimsto provide an integrated focus on a diverse setof factors that impact poverty. Small andMedium Enterprises have been identified asone of the four sectors to lead the revival ofeconomic growth. The importance of the privatesector has been emphasised alongwith enhancedinvestment as core elements of the strategy forhigh growth and employment generation. Itaccords high priority to the development ofmicro, small and medium enterprises.Development of SMEs is a tool that has beenintroduced in many countries, particularly indeveloping, as one of the potential contributorsto poverty alleviation.

SMEs are highly labour intensive and provideemployment to the bulk of Pakistan’s non-agricultural labour force. SMEs in themanufacturing sector also account for asignificant share of manufactured exports.Promoting SME growth would thus lead to morejob opportunities, better income, and in raisingliving standards.

The rapid growth of small scale enterpriseswould not only accelerate economic growth inthe medium term at relatively low levels ofinvestment, but would also increase employmentand exports for given levels of GDP growth.Employment generation is critical for povertyreduction. The Poverty Reduction Strategy hasrecognized the centrality of employmentgeneration for poverty reduction. SMEs arehighly labour intensive and provide employmentto the bulk of Pakistan’s non-agricultureworkforce. SMEs in the manufacturing sectoralso account for a significant share ofmanufactured exports. Promoting SME growthwould help those 70% of the population wholive in rural areas, who are pushed into povertybecause of inadequate income.

In developing countries like Pakistan, SMEsare exporting a wide array of products. Specificsectors with large SME presence like carpetmanufacturing, cutlery, surgical instruments,gems and jewellery, fisheries, power looms areinvolved in the export of unfinished products.

Bangla-desh /ThailandSMEs

SMEDAestab-lished

The contribution of these exporting smallenterprises in the total export exchequer canbe increased by shifting from low value addedto higher value added or finished goods. SMEDAis driving industrial growth towards valueadded products, resulting in increased exportearnings.

International experience shows that SMEs haveplayed a significant role in the early phases ofan export oriented industrialisation strategy bysupplying low cost labour intensive productssuch as textiles and garments, leather goodsand other consumer products. As they havedeveloped, SMEs have produced lightengineering goods. In countries like China,Korea, Philippines, Thailand, the electronicssector is proving to be highly productive,especially for exports from the SME sector.

In the newly industrialised economies, theexport oriented development strategy made asignificant contribution and in that contextSMEs had a major role to play. In Malaysia,SME exports make up about 20% of totalexports, in Pakistan SME exports account forabout 80% of total exports of manufacturedproducts and in the Philippines, some 90% ofexporters fall into the category of SMEs andtheir contribution to export is estimated ataround 20%.

In the past, the Government of Pakistan had auniform policy for large and small enterprisesin industry and trade. As a consequence, thespecific needs of the SMEs could not be met.Given the potential of the SME sector, thegovernment has established the Small andMedium Enterprise Development Authority(SMEDA) and the SME Bank. The later bymerging Small Business Finance Corporationand Regional Development Finance Corporationwith a mandate to provide financial assistanceand business support services to SMEs.

SMEDA has been created with an SME focus,with a mandate to act as the provider andfacilitator of support services to SMEs,(financial, management, marketing etc); to bethe resource base for the SMEs; and to be thevoice of SMEs in Pakistan. In other words, itfunctions as the apex policy formulation bodyfor the SMEs. It has identified businessopportunities. As most of the SMEs are involvedin the production of export oriented items,SMEDA is encouraging growth of value added

BULLETINECONOMICSeptember - October 2003

9

products. It provides sector briefs, which helpin understanding the sector; the regulatoryprocedures assist in knowing the prevailinglaws of the country, pre-feasibility studies havebeen published on certain sectors, whichintroduces the subject matter and provide ageneral idea and information on the said area.As SMEs are highly labour intensive most ofwhom are unskilled and untrained, SMEDA isimparting training to them, primarily in threemajor areas: Management, Technical andAgricultural training and development.

In the provinces following organizations areinvolved in promotion of small and mediumindustries:

Punjab Small Industries CorporationSindh Small Industries CorporationNWFP Small Industries CorporationThe Directorate of Small Industries Balochistan

These have helped set up small industries inthe provinces, training centres of traditionalcrafts and providing job opportunities to a largenumber.

Despite their dominant numbers and importancein job creation, SMEs have faced difficulty inobtaining formal credit. Although there is anestablished market structure for financialservices, the access to them is not easy forSMEs. Most need some kind of collateral whichthe SMEs may not be able to provide. Some ofthe enterprises poorly document their businessactivities and are unable to provide the collateralneeded.

It was felt that a Bank must be established toexclusively cater to the needs of the SME sector,offering specialised financial products andservices to help stimulate SME development.The SME Bank was set up in December 2001,with the objective to support and promotedevelopment of SMEs, concentrate on valueaddition and export oriented SMEs, and enableSMEs to play a role in stimulating GDP growth,create job opportunities and reduce poverty.

The Bank has also enhanced credit in exportoriented SME areas such as Sialkot, Daska,Gujranwala, Gujrat, Faisalabad and Multan. Ithas also introduced specialised financialproducts and programme lending schemes underthe name of Hunarmand Pakistan, that cater toa variety of credit needs of the SMEs. By theend of 2002, the Bank had introduced lending

SMEfinancing

SMEBankestabli-shed

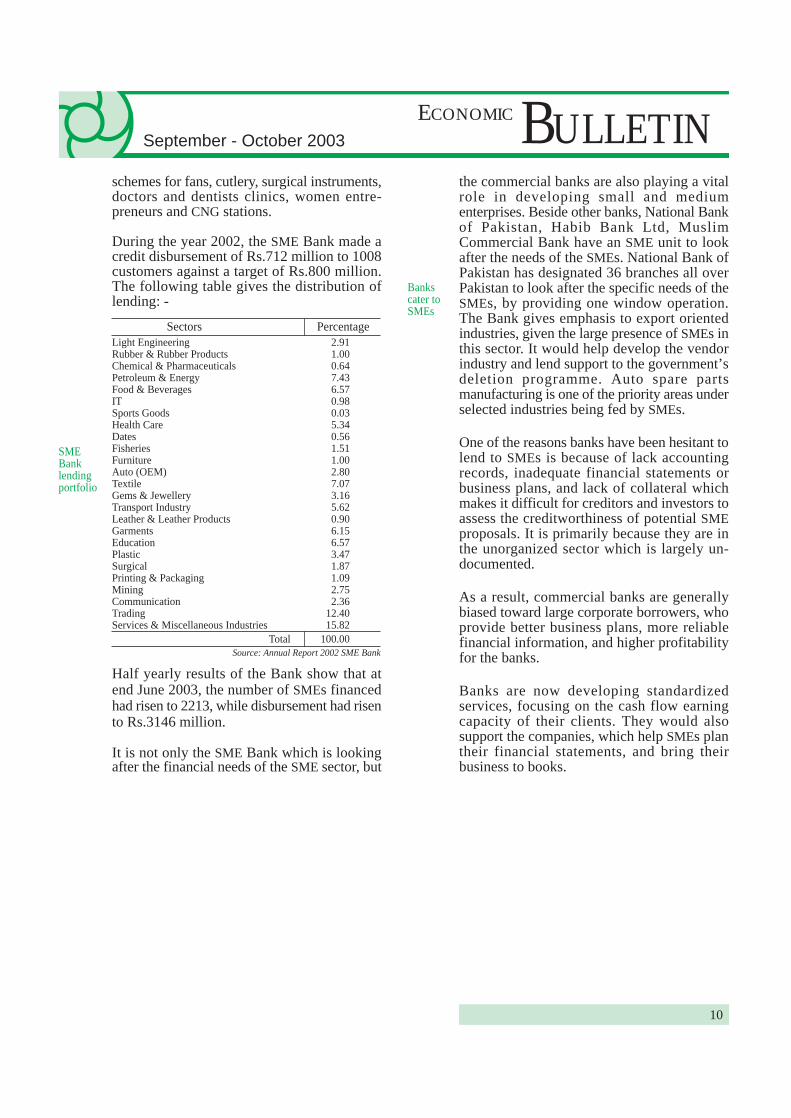

Sectors PercentageLight Engineering 2.91Rubber & Rubber Products 1.00Chemical & Pharmaceuticals 0.64Petroleum & Energy 7.43Food & Beverages 6.57IT 0.98Sports Goods 0.03Health Care 5.34Dates 0.56Fisheries 1.51Furniture 1.00Auto (OEM) 2.80Textile 7.07Gems & Jewellery 3.16Transport Industry 5.62Leather & Leather Products 0.90Garments 6.15Education 6.57Plastic 3.47Surgical 1.87Printing & Packaging 1.09Mining 2.75Communication 2.36Trading 12.40Services & Miscellaneous Industries 15.82 Total 100.00

Source: Annual Report 2002 SME Bank

BULLETINECONOMICSeptember - October 2003

10

schemes for fans, cutlery, surgical instruments,doctors and dentists clinics, women entre-preneurs and CNG stations.

During the year 2002, the SME Bank made acredit disbursement of Rs.712 million to 1008customers against a target of Rs.800 million.The following table gives the distribution oflending: -

Half yearly results of the Bank show that atend June 2003, the number of SMEs financedhad risen to 2213, while disbursement had risento Rs.3146 million.

It is not only the SME Bank which is lookingafter the financial needs of the SME sector, but

the commercial banks are also playing a vitalrole in developing small and mediumenterprises. Beside other banks, National Bankof Pakistan, Habib Bank Ltd, MuslimCommercial Bank have an SME unit to lookafter the needs of the SMEs. National Bank ofPakistan has designated 36 branches all overPakistan to look after the specific needs of theSMEs, by providing one window operation.The Bank gives emphasis to export orientedindustries, given the large presence of SMEs inthis sector. It would help develop the vendorindustry and lend support to the government’sdeletion programme. Auto spare partsmanufacturing is one of the priority areas underselected industries being fed by SMEs.

One of the reasons banks have been hesitant tolend to SMEs is because of lack accountingrecords, inadequate financial statements orbusiness plans, and lack of collateral whichmakes it difficult for creditors and investors toassess the creditworthiness of potential SMEproposals. It is primarily because they are inthe unorganized sector which is largely un-documented.

As a result, commercial banks are generallybiased toward large corporate borrowers, whoprovide better business plans, more reliablefinancial information, and higher profitabilityfor the banks.

Banks are now developing standardizedservices, focusing on the cash flow earningcapacity of their clients. They would alsosupport the companies, which help SMEs plantheir financial statements, and bring theirbusiness to books.

SMEBanklendingportfolio

Bankscater toSMEs

11

BULLETINECONOMICSeptember - October 2003

Box

Given the important role of Small and Medium Enterprises in theeconomic development of Pakistan, a separate set of PrudentialRegulations specifically for SME sector has been issued by theState Bank of Pakistan. The objective is to encourage banks/DFIsto develop new financing techniques and innovative products soto meet the financial requirements of SMEs.

Highlights of the Regulations

REGULATION R-1SOURCE AND CAPACITY OF REPAYMENTAND CASH FLOW BACKED LENDINGBanks/DFIs shall specifically identify the sources of repayment and assessthe repayment capacity of the borrower on the basis of assets conversioncycle and expected future cash flows. In order to add value, the banks/DFIsare encouraged to assess conditions prevailing in the particular sector/industrythey are lending to and its future prospects.

2. The rationale and parameters used to project the future cash flows shallbe documented and annexed with the cash flow analysis undertaken by thebank/DFI.

REGULATION R-2PERSONAL GUARANTEESAll facilities extended to SMEs shall be backed by the personal guaranteesof the owners of the SMEs. In case of limited companies, guarantees of alldirectors other than nominee directors shall be obtained.

REGULATION R-3LIMIT ON CLEAN FACILITIESIn order to encourage cash flow based lending, banks/DFIs are allowed totake clean exposure, i.e., facilities secured solely against personal guarantees,on a SME upto Rs.3 million provided that funded exposure should notexceed Rs.2 million.

REGULATION R-4SECURITIESSubject to the relaxation in Regulation R-3, for facilities upto Rs.3 million,all facilities over and above this limit shall be appropriately secured as persatisfaction of the banks/DFIs.

REGULATION R-5MARGIN REQUIREMENTSThe banks/DFIs shall adhere to the margin requirements as prescribed bythe State Bank of Pakistan from time to time.

REGULATION R-6PER PARTY EXPOSURE LIMITThe maximum exposure of a bank/DFI on a single SME shall not exceedRs.75 million. The total facilities (including leased assets) availed by asingle SME from the financial institutions should not exceed Rs.150 millionprovided that the facilities excluding leased assets shall not exceed Rs.100million.

REGULATION R-7AGGREGATE EXPOSURE OF A BANK/DFI ON SME SECTORThe aggregate exposure of a bank/DFI on SME sector shall not exceed thelimits as specified below: -

REGULATION R-8MINIMUM CONDITIONS FOR TAKING EXPOSURE

While considering proposals for any exposure (including renewal,enhancement and rescheduling/restructuring) exceeding such limit as maybe prescribed by State Bank of Pakistan from time to time (presently atRs.500,000/-), banks/DFIs should give due weightage to the credit reportrelating to the borrower and his group obtained from a Credit InformationBureau (CIB) of State Bank of Pakistan.

2. Banks/DFIs are encouraged to refer the prospective SME borrower toSME Associations for obtaining information about its character and creditworthiness.

3. Banks/DFIs shall, as a matter of rule, obtain a copy of financial statementsduly audited by a practicing Chartered Accountant, relating to the businessof every borrower who is a limited company or where the exposure of abank/DFI exceeds Rs.10 million, for analysis and record.

4. Banks/DFIs shall not approve and/or provide any exposure (includingrenewal, enhancement and rescheduling/restructuring) until and unless theLoan Application Form (LAF) prescribed by the banks/DFIs is accompaniedby a ‘Borrower’s Basic Fact Sheet’ under the seal and signature of theborrower as per approved format of the State Bank of Pakistan.

REGULATION R-9PROPER UTILIZATION OF LOAN

The banks/DFIs should ensure that the loans have been properly utilizedby the SMEs and for the same purposes for which they wereacquired/obtained.

REGULATION R-10RESTRICTION ON FACILITIES TO RELATED PARTIES

The bank/DFI shall not take any exposure on a SME in which any of itsdirector, major shareholder holding 5% or more of the share capital of thebank/DFI, its Chief Executive or an employee or any family member ofthese persons is interested.

REGULATION R-11LOANS/ADVANCES

Banks/DFIs shall observe the prudential guidelines given specific to thematter of classification of their SME asset portfolio and provisioning there-against.

The rescheduling/restructuring of non-performing loans shall not changethe status of classification of a loan/advance etc. unless the terms andconditions of rescheduling/restructuring are fully met for a period of at leastone year (excluding grace period, if any) from the date of suchrescheduling/restructuring and at least 10% of the outstanding amount isrecovered in cash.

For more details see www.sbp.org.pk

PERCENTAGE OF CLASSIFIED SMEs ADVANCES MAXIMUM LIMITTO TOTAL PORTFOLIO OF SMEs ADVANCES

a. Below 5% No limitb. Below 10% 3 times of the equityc. Below 15% 2 times of the equityd. Upto and above 15% Upto the equity

Prudential Regulations for SMEs Financing

12

BULLETINECONOMICSeptember - October 2003

Pakistan’s Bond MarketBonds are debt instruments, which can providefunds for the financing of long-term investmentprojects and also short term financial needs.As a long-term fund raising instrument, bondshelp promote the matching of long-term fundsand investment. Borrowing through bonds helpsdiversify funding sources primarily frombanks/international lending institutions to banks,insurance companies, pension funds andinvestment funds. Given the depth of the marketand the sizes that can be transacted, bonds canraise large funds without much slippage.

The bond market is the foundation of capitalmarket and plays an important role in mobilizingand channeling savings into productiveinvestment that promotes economic growth andprovides basic infrastructure for thedevelopment of a financial system. Bond marketdevelopment is beneficial, atleast, in twoaspects: Firstly, it helps to resolve liquidityproblem of banks in the country and secondlyit helps to increase the inflow of foreign capital.It can also add to corporate transparency andmarket discipline.

The consequences of operating a financialsystem with a banking system and equity marketbut without a bond market are profound andfar reaching. The absence of a bond marketmay render an economy less efficient andsignificantly more vulnerable to financial crisis.The underdevelopment of bond market limitsrisk-pooling and risk sharing opportunities forboth households and firms.

To develop a bond market, three essentialcomponents are needed:

§ A deep and liquid government bond market toserve as benchmark yield curve against whichcorporate paper can be priced.

§ An adequate infra-structure, both legal andoperational, to support trade and transfer ofinstrument and funds.

§ Collaboration of the intermediaries, the end usersand the private sector.

A government bond market, if operatingsatisfactorily, can significantly increase investors

confidence in the overall bond market and inthe whole capital market. A well developedgovernment bond market can help governmentto finance expenditure and conduct monetarypolicy efficiently.

Bond market allows a more efficient allocationof savings. Banks prefer to lend fairly shortterm loans because their funding sources arevery short and at the sametime they are subjectto regulation by the country’s central bank.Bond markets with their long-term institutionalinvestors on the other hand, help unleash majorforces of savings that can be channeled intoimportant investments for economic develop-ment. With their lower cost of capital andlong term nature they help spur industrialdevelopment.

According to an Asian Development Bankstudy, bond markets in general and corporatebond markets in particular, have developedrapidly in countries with stable and predictablemacro-economic environment. However, incountries having relatively unstable macro-economic environment, the corporate bondmarket has to rely heavily on governmentsupport.

Various studies conducted on the efficacy ofgenerating funds through bond floatationgenerally highlights the benefits of thegovernment bond markets and maintains thatbonds can provide an alternative non-inflationary source of financing, fostering ahealthy capital market and improve thefunctioning of the financial system. Activebond markets can have indirect benefits throughbetter monetary management, enhancedtransparency and a widening of investmentopportunities.

In developing countries, the role of the bondmarket has been very small, relative to that ofthe banking system or equity market. Althoughthere is considerable potential for developingdomestic bond market in Asian emergingcountries with high saving rates, little attentionhas been paid.

Fundraisinginstrument

Bondmarketpromoteseconomicgrowth

Threeessentialcompo-nents

Bondmarkethelpsdevelop-ment

Non inflat-ionarysource offinancing

Role ofbondmarket

BULLETINECONOMICSeptember - October 2003

13

One of the causes of the Asian financial crisiswas the poorly developed bond markets in theregion. Investors could not diversify theirinvestment for lack of opportunities. The lackof sophisticated Asian bond market resulted insubstantial official savings being investedoutside the region.

Domestic savings in Asia, which stand at morethan 30% of GDP, are the best funds for issuingbonds. There is also tremendous interest in highquality fixed income securities in Asia. Thereis a need for Asian central banks to invest theirforeign currency reserves in bonds. The Asianfinancial institutions have a strong demand forquality bonds with good yields. However, theAsian bond market still lacks quality issuersand investors’ confidence.

The equity market in Pakistan has grown interms of size accompanied with institutionaldevelopment, but fixed income securities markethas only partly developed. At present, littleattention is being paid to mopping up of fundsfrom the fixed income market whereas, theentire corporate sector relies on securing fundseither from the banks in the shape of loans orfrom the stock exchange by floating shares.

Consequently bond market development in thecountry has lagged as elsewhere in Asia. Itcurrently covers debt and debt like securitiesissued by the government, statutory corporationsand corporate entities. The market for bondsof statutory corporations and corporate entitiesthough, in early stage of development, has greatpotential for growth. However governmentissues dominate the bond market, with corporatebond market accounting for only 0.6% of GDP.

In Pakistan the bond market size can beexamined from the perspective of outstandingdebt and trends in the issue of governmentsecurities. Based on outstanding governmentdebt position, the market size appears to haveincreased from Rs.800 billion as of June 30,1995 to around Rs.1852 billion as of June 30, 2003, an increase of 132%. However, it looksdeceptively large as various forms ofgovernment debt take up nearly 40% of GDP.The actual bond market size is much smallercompared to many developed countries.

Several measures have been taken by thegovernment to promote bond market in Pakistan.

Pakistan’smarket

Marketsize

Promotingbondmarket inPakistan

Sales /auctionsof debtinstru-ments

Demandfor qualitybonds

Earlydevelop-ment stage

Debtinstru-ments

The government started borrowing throughauctions in the open market from 1991 to raisefunds on market related rate of return. In aneffort to develop bond market it introduced sixmonth treasury bills, a zero coupon debtinstrument, also known as Market TreasuryBills (MTBs), and a medium and long termFIBs, of 3-years, 5-years and 10-years maturitieswith coupon rates fixed at 13%, 14% and 15%respectively in March 1991. In July 1996. ShortTerm Federal Bonds (STFBs) were launchedreplacing 6-month MTBs, but in June 98, 6-month MTBs again replaced STFBs, and at thesametime MTBs of 3 months and 12 monthmaturity were also introduced.

The sale of FIBs was suspended in July’98, dueto very thin participation of investors afterbanks, the largest bidder of FIBs, stoppedbidding. However, sale and purchase ofoutstanding FIBs in the secondary marketcontinued despite suspension of auctions.Trading in STFBs remain in vogue till theirmaturities, while trading in TBs of all maturitieshas picked up in the secondary market. Afterthe lapse of 30 months since the suspension ofFIBs auction, the government, in December2000 introduced Pakistan Investment Bonds(PIBs), a new long term debt instrument aimedat expanding the horizon of investment forpensions and benevolent funds.

The bonds are of 3-years, 5-years and 10-years maturities available at fixed coupon rates,which were as high as 12.5%, 13.0% and 14.0%respectively at the time of launching. The rateshave fallen considerably in the past three years.Currently the rates are 6%, 7% and 8%.The launching of PIBs has helped boost thedevelopment of corporate bond market in thecountry.

The government debt instruments now compriseof Treasury Bills (TBs), which are purchasedby financial institutions, both banks and nonbanks, through auction conducted by the StateBank of Pakistan. The issuance of STFBs wasphased out in 1998-99, and replaced by MTBs.Federal Investment Bonds (FIBs) are mediumand long term debt instrument sold at par witha fixed yield. PIBs, are mainly long term debtinstrument. Both medium and long term FIBsand PIBs are permanent debt while floatingdebt comprises of TBs, which are short term.

Growthof MTBsand PIBs

14

BULLETINECONOMICSeptember - October 2003

1995 1996 1997 1998 1999 2000 2001 2002 2003A-Permanent Debt (Rs. Bn) 294 295 281 277 257 260 281 368 428 of which: (%) Federal Investment Bonds 56.5 55.3 54.8 52.0 52.9 51.2 40.2 22.0 10.5 Pakistan Investment Bond - - - - - - 16.4 41.8 53.5 Prize Bonds 15.3 17.3 21.7 25.6 31.5 31.2 32.7 28.0 30.4

B-Floating Debt (Rs.Bn) 294 361 434 474 562 647 738 558 516 of which: (%) Market Treasury Bills - - - - 25.3 13.9 14.1 37.3 78.1 6 Months Treasury Bills 59.9 67.9 - 7.2 - - - - - Adhoc Treasury Bills 20.7 16.9 14.1 13.1 16.0 13.9 16.9 22.0 - Short Term Federal Bonds - - 21.4 22.2 - - - - -

C-Unfunded Debt (Rs.Bn) 211 253 322 425 574 672 712 792 908 of which: (%) Defence Savings Certificates 40.3 41.5 42.5 39.7 37.2 38.0 38.2 37.1 34.1 Special Savings Certificates 34.1 39.8 39.4 34.8 31.9 25.0 24.9 27.0 32.4Total Debt 799 909 1037 1176 1392 1579 1731 1718 1852

(End-June)Outstanding Domestic Debt

Source: SBP Annual Reports

Since 1995, the share of permanent and floatingdebts in total domestic debt have declined.Within the permanent debt, the share of FIBshas fallen from 56.5% in FY95 to 10.5% inFY03, while that of PIBs increased from 16%to 53.5% in the last 3 years. Within floatingdebt, the share of MTBs has increased signifi-cantly.

The issuing and trading of corporate debtsecurities is not a new phenomenon in Pakistan.During the 1960s and early 1970s, before thenationalization of financial institutions in 1972,corporate debentures issued by Pakistanicompanies were not only listed on stockexchanges but there was also a secondary marketfor these instruments. However afternationalization, this activity came to a standstill. Pakistan’s first corporate debt was afive-year bond issued in 1988 by WAPDA, astatutory corporation. But the market experiencewith these bonds proved unsatisfactory due tolimited investors’ interest and illiquid secondarymarket.

In 1984, the government, in an effort to boostthe development of corporate bond market, hadalso introduced Term Finance Certificates(TFCs), a market related debt instrument whichthe corporate sector can borrow directly fromthe general public through the stock exchanges.In Pakistan, the corporate bond and TFCs areused interchangeably.

Corporatedebt

Corporatebondmarketdevelop-ment

Launchingof TFCs

Till early 1990s, TFCs were issued by majorstate owned organizations only. The privatesector Pakistani companies did not issue anyTFCs during this period. It was in February1995, that the first public TFC issued byPackages, the country’s largest papermanufacturer in private sector, was listed onthe stock exchanges followed by three otherswith a yield of between 17.8% and 19%.

The progress was slow in the presence ofgovernment guaranteed bonds with high couponrates and also because of high interest ratespaid on national savings schemes. However,the market for TFCs picked up after the declinein short-term interest rates and falling long termyields. In 1999 alone, four new TFCs wereissued. With further decline in interest ratesand cut in national savings schemes rates since2000, the market for TFCs has picked upconsiderably. About 62 new TFC issues havebeen launched since 1995 including 28 issuesthat were launched in 2001 and 2002.

In FY03, 21 issues have been launched, ofwhich, eight issues were by manufacturingconcerns, 7 by leasing companies and remainingby banks or services companies. However, theoutstanding stock of listed corporate bonds stillremains low at 2% of GDP. TFCs offer a returnthat competes with gains and risks oninvestments in deposit schemes of financialinstitutions and the national saving schemes.

Currently TFCs and PIBs provide an attractiveopportunity for the investors. The economic

BULLETINECONOMICSeptember - October 2003

15

Opportu-nity forinvestors

GrowingCorporateinterest

Need fora viablebondmarket

Source: SBP Annual Report 2002-03

FY91 13.9 6.2 14.8 34.9FY92 10.6 3.0 313 44.9FY93 12.6 5.1 35.8 53.5FY94 10.7 4.0 11.9 26.6FY95 8.8 2.3 18.9 30.0FY96 3.9 4.2 7.9 16.0FY97 1.1 0.1 3.5 4.7FY98 1.3 0.2 2.2 3.7

Total 62.9 25.1 126.3 214.3

YearAmount accepted

3 year 5 year 10 year Total

Auction of Federal Investment Bonds(Rs.Bn)

FY01 8.5 4.7 12.5 12.5FY02 46.1 24.8 9.8 10.4FY03 26.1 9.7 5.5 8.0

FY01 6.7 5.3 13.0 13.0FY02 47.3 24.7 10.6 10.9FY03 45.6 14.4 6.5 9.1

FY01 43.6 36.1 14.0 14.0FY02 144.9 58.2 11.6 12.0FY03 139.8 50.8 6.8 10.0

3 year

5 year

10 year

Amount Amount Average Averageoffered accepted yield coupon

(%) (%)Instrument Year

(Rs.Mn)

Source: SBP Annual Report 2002-03

Auction of Pakistan Investment Bonds

The corporate bond market has evolved rapidlyafter the picking up of TFCs market in the lasttwo years. Most of the TFCs have been launchedby the textiles and chemicals manufacturers.Some major companies, particularly the leasingcompanies are expected to utilize TFCs fundingin future resulting in further growth of TFCmarket. Since the corporate interest in issuingTFCs has increased, many companies in theprivate sector have started or decided to issueprivately placed TFCs.Some commercial banks are also planning toparticipate actively in the floatation and issuanceof TFCs. Infact few banks have already issuedTFCs to improve upon their capital adequacyratio. The trend will be further strengthened asthe environment is being made conducive forthe development of the corporate bond market.The decision to ban institutional investment inApril 2000 has given a boost to corporateinterest in issuing TFCs.

Pakistan needs a viable bond market in orderto mobilize private savings efficiently for longterm investments. The entry of big banks intothe advisory and arranging business couldfurther contribute in the promotion of TFCsprimary market. Policies are being designedto promote bond market as an alternativesource for long term project financing sincecommercial banks are shy of under taking risksof long term financing while DFIs suffer fromlack of funds.

The State Bank of Pakistan has also advisedcommercial banks to float long term bonds tomobilize funds for housing loans. Innovativeproducts have been developed by some banksfor house financing. This includes floatationof bonds by banks to mobilise funds andundertake mortgage financing.

environment for a healthy corporate bondmarket is much favourable as the marketcharacteristics have significantly changed infavour of the development of bond market. Inthe absence of Development Finance Institutionsactivity following the closure of Bankers Equityand merger of National Development FinanceCorporation with the National Bank of Pakistan,the importance of bond market in raising longterm funds for corporate sector can not beignored.

16

BULLETINECONOMICSeptember - October 2003

Cotton – Current Demand and Supply PositionPakistan has emerged as one of the major textileproducts supplier in the world market. Despitethe government’s efforts to diversify exportsand enlarge its industrial base, textiles continueto dominate the industrial activity in the country.Given its share in GDP, export earnings andvalue added in manufacturing, makes it thesingle largest determinant of growth of themanufacturing sector. It currently accounts for46% of total manufacturing activity, over 65%of export earnings, nearly 9% of GDP,employing 38% of industrial workers, andcontributing Rs. one billion in direct taxes. Itsshare in world yarn trade is around 30% andabout 8% in cotton cloth trade.

The textile sector depends on the agriculturesector for the supply of raw material. Pakistanis one of the four largest cotton growers in theworld, the others being, United States, Chinaand India. In addition to providing raw materialto the local textile industry, lint cotton is alsoa major export item. As a main cash crop, itcontributes substantially to the national income. Presently it accounts for nearly 12% of valueadded in agriculture, about 30% in value addedof major crops and 3% of GDP.

Cotton production in the 1990s averaged 9.8million bales. It touched historic highs of 12.8million bales in 1991-92, above the 11.2 millionbales of 1999-00. In the last 3 years (2000-2003), production has averaged 10.3 million

1994-95 8.7 27.81995-96 10.6 31.61996-97 9.4 29.11997-98 9.2 20.61998-99 8.8 25.21999-00 11.24 28.92000-01 10.73 30.22001-02 10.61 30.32002-03 10.21 27.62003-04 10.0E NA

Production % share in value added of(Mn bales) major agriculture crops

E = estimates Source: Economic Survey 2002-03

As capacity utilization of the mill sector hasrisen in recent years, the cotton requirement ofdomestic textile industry has simultaneouslygrown. Over the last four years there has beenan investment of $3 billion in the industry forbalancing, modernization and replacement. ThisBMR and capacity expansion in the textileindustry is reflected in rising imports of textilemachinery. Large scale balancing andmodernisation of industry apart from additionof new spindleage has considerably raised theconsumption of cotton.

bales. Though area under cotton has increasedsignificantly, per hectare yield of cotton at 570kgs is still the lowest. Efforts are needed toimprove per hectare yield and boost productionto meet the growing demand.

Raw Cotton

1993-94 320 8182 14 136 5886 6 80 1483 1310 315

1994-95 334 8307 14 130 5991 5 73 1559 1370 322

1995-96 349 8493 13 142 6356 5 79 1662 1495 327

1996-97 357 8137 10 143 6465 5 87 1670 1521 333

1997-98 353 8274 10 150 6556 4 80 1751 1533 340

1998-99 348 8298 10 166 6594 5 66 1840 1540 385

1999-00 351 8383 10 150 6750 4 66 1962 1670 437

2000-01 353 8507 10 146 7105 4 65 2070 1721 490

2001-02 354 8967 10 142 7078 5 65 2155 1809 568

2002-03 363 9216 10 147 7623 5 72 2371 1935 577

Production of Yarn/Cloth

YearNo. of

reportingfactories

Capacity installedSpindles000’Nos

Looms000’Nos

Rotors000’Nos

Raw Cottonconsumption000’Tonnes

Yarnproduction000’Tonnes

CottonCloth

ProductionMn.Sq.Mts.

Capacity workedSpindles000’Nos

Looms000’Nos

Rotors000’Nos

Source: Federal Bureau of Statistics

Textilescontribu-tion to theeconomy

Rise inproduction

Expansionin capacityutilization

BULLETINECONOMICSeptember - October 2003

17

The mill consumption of cotton has gone upfrom 9.4 million bales in FY00 to an estimated11 million bales in FY03, increasing at abouthalf a million bales per year in the last fouryears. Consumption requirements of mills forthe current season are being placed at 12 millionbales and at around 15 million bales after 2005.The growing imbalance between demand andsupply of cotton has necessitated imports, whichhave gone up from 0.5 million bales in FY00to 1.1 million bales in FY03. Failing to meetthe growing gap between demand and supplyhas turned the country from a surplus cottonproducer to a cotton importing country.

As for the current season, the governmenthad initially proposed a production target of10.55 million bales, to be sown at over 2.86million hectares. The current crop was promisingas output was expected to reach 11 million balesfrom a sown area of 3.09 million hectares,up 9.1% from last year and 6.6% against thetarget.

However, heavy downpour in August damagedcotton sown in Punjab and Sindh, and pestattacks in September damaged some 20-25%crop in both the provinces, adversely affectingexpectations of higher production. Sindh hasreported 4% decline in cotton output. Whileanticipating lower crop due to sizeablepest attack, the Federal Committee onAgriculture has revised down the productiontarget by 5.2%, fixing the new target at 10million bales.

Based on phutti arrivals, the Pakistan CottonGinners Association is anticipating a crop of9.5 million bales on ex-gin basis. Total arrivalsas of November 1, are reported to be higher by24% over the same period last year. However,trade circles are apprehensive that due to heavypest infestation, the pace of arrivals in thecoming weeks would slowdown. These circlesexpress doubts about the government’s revisedtarget and are anticipating a final crop of between8.5-9 million bales, further widening thedemand/supply gap. Even a crop of 10 millionbales, as anticipated by the government, willfall short of requirements, necessitating importsof 2 million bales this season. In the last twomonths, mills are reported to have

Cottonconsump-tiongrows

Importsnecessary

Pricesof cottonrise

booked imports of 0.7 million bales of cotton.In October alone about 0.3 million bales werebooked.

In the local cotton market, the price of cottonhas risen by more than 50% in recent weeks.This rise is not only because of a significantincrease in the world cotton prices on accountof supply shortages, but also because of fear oflower domestic crop and large scale holdingof stocks by growers and ginners, anticipatinga further rise. In the New York Cotton futuresmarket, cotton prices reached 5 year peak at80.59 and 82.72 cents per lb for December andMarch settlements respectively. In line withinternational trend, growers and ginners sawdomestic lint prices rising in the local marketto a record Rs.3600 per maund.

Speculators in the local market could createserious supply problems for the domestic textileindustry by raising lint prices. Some weakspinners have already closed down theiroperations and it is expected that cotton demandby textile industry may fall. However, thegovernment does not expect any abnormal pricehike despite a shortfall in cotton output thisseason. In the international market, there wassome drop in cotton prices in mid Novemberbut this was considered a temporaryphenomenon, and lint prices could move upagain. In the domestic market, prices havefalledn in the past few weeks but they continueto remain high.

Pest infestation of the local cotton crop andreportedly large purchases of cotton by bigtextile mills has resulted in escalation in cottonprices with adverse affects for the industry andthose associated with the sector. The farmerssuffer because of low yields, and rising cost ofinputs because of increased use of pesticides.It is largely the smaller or average growers withlittle resources who would be affected the most.With the closure of a large number ofpowerlooms in Faisalabad district, thousandsof daily wagers have been rendered jobless.This is a great setback as it would see theirincomes dwindle. Loss of economicopportunities would push them further intopoverty.

The increase in poverty two years back wasbecause of the severe drought which lowered

Currentcropaffectedbyrains/pest

Adverseaffects ontextilesector

BULLETINECONOMICSeptember - October 2003

18

agricultural growth and affected the lives of68% of the people who live in rural areas anddepend directly or indirectly on the agriculturalsector for their livelihood. The current situationthough not so severe would however, affect thelives of thousands associated with cotton andtextiles.

Pest infestation in the country and the resultingdamage of the local crop, and rising cotton pricein the international market due to heavypurchases by the Chinese after poor weatherdestroyed their cotton crop, has exacerbatedthe situation. Cotton yarn prices have also risenin the local market. As raw cotton prices haverise by 50% to Rs.3,400 per maund, the millershave not only to pay higher price for cottonpurchase but are also paying more to the banksin terms of cotton finance margin and assales tax.

There were reports from Faisalabad, the textilehub of the country, that nearly 25,000powerlooms faced with increase in cotton andpolyester yarn prices have closed down. As theprices of cotton and polyester yarn had risen,

many yarn exporters were finding it difficult tohonour their commitment as per the alreadysettled rates.

Majority of exporters who purchase cotton yarnon a day to day basis are the worst hit becauseof the unprecedented increase in the price ofcotton yarn. Rates of all yarn brands and countshave gone up by Rs.10-Rs.15 per bundle inrecent days.

The All Pakistan Cotton PowerloomsAssociation seeks a reduction in the price ofcotton and yarn, a ban on the export of cottonyarn and encouragement of value addition. Withpolyester staple fibre industry having undergonecapacity expansion and prospects thatsubstitution by textile manufacturer from cottonto relatively cheaper synthetic fibre, could occur,the All Pakistan Cloth Exporters Associationhas sought reduction in import duty so thatdiversion towards polyester blend is facilitatedand the value added textile sector, comprisingof fabrics, bedlinen, knitted garments, textilemade-ups does not receive any setback.

19

BULLETINECONOMICSeptember - October 2003

Pak Trade with Islamic Countries

1998-99 (Rs.Mn)

Exports Imports Balance Exports Imports Balance Exports Imports Balance Exports Imports Balance1999-00 2001-01 2001-02

Afghanistan 48.2 37.0 11.2 115.2 40.8 74.4 140.4 29.5 110.9 169.3 22.9 146.4

Bahrain 34.8 78.4 (-)43.6 43.0 114.6 (-)71.6 43.8 80.0 (-)36.2 43.1 59.6 (-)16.5

Bangladesh 119.4 32.3 87.1 120.4 29.5 90.9 133.4 33.5 100.0 101.1 27.7 73.4

Egypt 35.3 30.5 4.8 35.4 36.9 (-)1.5 40.9 29.9 11.0 38.7 33.2 5.5

Iran 11.3 77.8 (-)66.5 11.5 130.2 (-)118.7 23.9 374.4 (-)350.5 29.2 158.2 (-)129.0

Iraq 9.6 - - 2.3 - - 16.3 0.2 16.1 30.3 0.2 30.1

Indonesia 125.3 213.8 (-)88.5 52.9 175.6 (-)122.7 136.4 161.7 (-)25.3 76.8 243.2 (-)166.4

Jordan 4.7 21.5 (-)16.8 6.1 53.7 (-)47.6 15.9 30.6 (-)14.7 28.4 27.7 0.7

Kuwait 36.8 558.3 (-)521.5 40.6 1236.8 (-)1196.2 45.8 964.6 (-)918.8 58.4 731.9 (-)673.5

Malaysia 33.4 634.5 (-)601.1 45.7 439.3 (-)393.6 50.9 428.1 (-)377.2 51.8 456.3 (-)404.5

Saudi Arabia 184.7 643.0 (-)458.3 214.8 923.0 (-)708.2 273.0 1259.2 (-)986.2 330.4 1200.7 (-)870.3

Sultanat-e-Oman 48.3 38.0 (-)10.3 53.0 31.0 22.0 43.7 26.3 17.4 47.3 6.9 40.4

Turkey 35.1 131.9 (-)96.8 61.0 106.6 (-)45.6 100.5 47.6 52.9 98.3 34.8 63.5

UAE 422.8 634.6 (-)211.8 493.0 907.6 (-)414.6 626.1 1328.1 (-)702.0 727.3 1354.6 (-)627.3Source: Annual Report 2002-03

State Bank of Pakistan

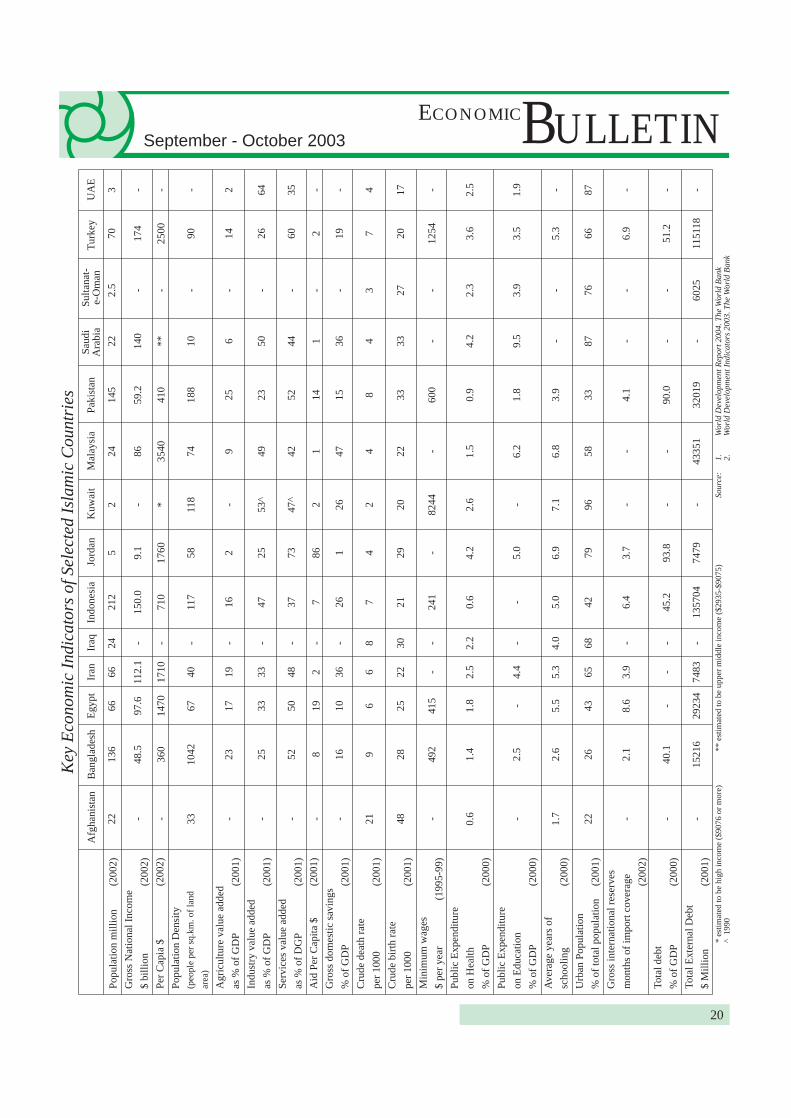

Pakistan enjoys cordial trade relations withmembers of OIC. There is ample goodwill forexpansion of trade and establishment of jointventures in various industrial sectors. Fromcountries like Kuwait, UAE and Saudi Arabia,Pakistan imports large quantities of oil andexports both traditional and non-traditionalitems. Similarly Iran is a major supplier of oilto Pakistan. Large quantities of palm oil areimported from Malaysia. Pakistan traditionallyexports textile products, rice, surgicalinstruments, fruits and vegetables to thesecountries. There is regular exchange of visits

by the trade delegations, members of theChamber of Commerce and holding of seminars.Efforts are made to explore new avenues forexpansion of trade and investment, cooperationin technical education, health and other fields.

Besides trade, these countries are a home toa large number of Pakistani expatriates whosend back huge remittances. A large numberof professionally qualified personnel areemployed in the field of health, medicine andengineering.

BULLETINECONOMICSeptember - October 2003

20

Key

Eco

nom

ic In

dica

tors

of S

elec

ted

Isla

mic

Cou

ntri

es

* es

timat

ed to

be

high

inco

me

($90

76 o

r mor

e)**

est

imat

ed to

be

uppe

r mid

dle

inco

me

($29

35-$

9075

)^

199

0

Afg

hani

stan

Ban

glad

esh

Egyp

tIr

anIr

aqIn

done

sia

Jord

anK

uwai

tM

alay

sia

Paki

stan

Saud

iA

rabi

aSu

ltana

t-e-

Om

anTu

rkey

UA

E

Popu

latio

n m

illio

n (2

002)

Gro

ss N

atio

nal I

ncom

e$

billi

on

(200

2)Pe

r Cap

ia $

(200

2)Po

pula

tion

Den

sity

(peo

ple

per s

q.km

. of l

and

area

)

Agr

icul

ture

val

ue a

dded

as %

of G

DP

(200

1)In

dust

ry v

alue

add

edas

% o

f GD

P(2

001)

Serv

ices

val

ue a

dded

as %

of D

GP

(200

1)A

id P

er C

apita

$(2

001)

Gro

ss d

omes

tic s

avin

gs%

of G

DP

(200

1)C

rude

dea

th ra

tepe

r 100

0(2

001)

Cru

de b

irth

rate

per 1

000

(200

1)M

inim

um w

ages

$ pe

r yea

r(1

995-

99)

Publ

ic E

xpen

ditu

reon

Hea

lth%

of G

DP

(200

0)Pu

blic

Exp

endi

ture

on E

duca

tion

% o

f GD

P(2

000)

Ave

rage

yea

rs o

fsc

hool

ing

(200

0)U

rban

Pop

ulat

ion

% o

f tot

al p

opul

atio

n(2

001)

Gro

ss in

tern

atio

nal r

eser

ves

mon

ths

of im

port

cove

rage (2

002)

Tota

l deb

t%

of G

DP

(200

0)To

tal E

xter

nal D

ebt

$ M

illio

n(2

001)

22 - - 33 - - - - - 21 48 - 0.6 - 1.7 22 - - -

136

48.5

360

1042 23 25 52 8 16 9 28 492

1.4

2.5

2.6 26 2.1

40.1

1521

6

66 97.6

1470 67 17 33 50 19 10 6 25 415

1.8 - 5.5 43 8.6 -

2923

4

66 112.

1

1710 40 19 33 48 2 36 6 22 - 2.5

4.4

5.3 65 3.9 -

7483

24 - - - - - - - - 8 30 - 2.2 - 4.0 68 - - -

212

150.

0

710

117

16 47 37 7 26 7 21 241

0.6 - 5.0 42 6.4

45.2

1357

04

5 9.1

1760 58 2 25 73 86 1 4 29 - 4.2

5.0

6.9 79 3.7

93.8

7479

2 - * 118 - 53^

47^ 2 26 2 20 82

44 2.6 - 7.1 96 - - -

24 86 3540 74 9 49 42 1 47 4 22 - 1.5

6.2

6.8 58 - -

4335

1

145

59.2

410

188

25 23 52 14 15 8 33 600

0.9

1.8

3.9 33 4.1

90.0

3201

9

22 140

** 10 6 50 44 1 36 4 33 - 4.2

9.5 - 87 - - -

2.5 - - - - - - - - 3 27 - 2.3

3.9 - 76 - -

6025

70 174

2500 90 14 26 60 2 19 7 20 1254 3.6

3.5

5.3 66 6.9

51.2

1151

18

3 - - - 2 64 35 - - 4 17 - 2.5

1.9 - 87 - - -

Sour

ce:

1.W

orld

Dev

elop

men

t Rep

ort 2

004.

The

Wor

ld B

ank

2.W

orld

Dev

elop

men

t Ind

icat

ors

2003

. The

Wor

ld B

ank

21

BULLETINECONOMICSeptember - October 2003

Market AnalysisMarket Outlook

The market underwent a major correction in Septemberand October 2003. The KSE-100 lost 680 points overthe two month period (823 points or 18% from the alltime high of 4604 on September 12,’03 to the Octoberlow of 3781). By mid-November, the market appearedto have settled around the 3800 Index level but averagedaily trading volumes shrank considerably from 453min September, to 215m in October and only 126m in thefirst two weeks of November.

KSE-100

The market had become over leveraged and a correctionwas due, but a number of factors combined to make thecorrection larger and longer than had been anticipated.The State Bank of Pakistan (SBP) announcement of aRs50b Jumbo bond PIB offering between October andDecember ’03 meant some of the excess liquidity wouldbe removed from the market and led to expectations ofa possible rise in interest rates. A lack of progress onthe privatization of PSO also kept the market suppressed.Also preventing a recovery, or prolonging the slump,were the following factors:§ SBP imposed ceiling on bank investment in shares§ Introduction of draft margin financing rules§ Restriction of “badla” stocks

Ceiling on bank investment in equity marketsThe SBP’s new Prudential Regulations place a ceilingon bank participation in the equity markets at 20% ofbank equity (35% of equity for Islamic Banks and non-deposit taking DFIs). Exempt from this ceiling are bankshareholdings in strategic investments, associatedcompanies, NIT units and OGDCL shares bought throughsubscription. Banks are important institutional investors

in the equity market and this restriction on theirinvestments will lead to some supply pressure, pluslower activity from banks in the long run. Banks haveone year to comply with the limits.

Draft margin financing rulesInvestors sentiment was adversely affected by the SBP’sintroduction of draft rules for margin financing, whichis widely expected to eventually replace the existingbadla / COT system of financing.

According to the SBP’s draft regulations, banks will beable to extend margin financing to brokers that areregistered as limited companies and are credit rated byan approved credit rating agency. A minimum marginof 30% of the current value of approved shares must bekept by the banks at all times. Margin financing willonly be available against a list of approved shares.There is a general expectation that eventually, the newmargin financing rules will replace the badla system.

On the positive side, margin financing by banks willremove the conflict of interest that exists in the badlasystem in which brokers and investors in the market arealso badla financiers. The badla system could be usedas a tool for market manipulation which it is hopedmargin financing by banks will prevent. Bank marginfinancing could also lead to more stable financing costs,and avoid the daily turnover cost that exists in the badlasystem. However, from an operational point of viewbank margin financing will be more difficult for brokeragehouses to manage and so may raise transaction costs.

The fact that the minimum margin limit is proposed at30% instead of 20% in badla finance means that themarket will be less leveraged. Traders will of coursenot like this restriction, and this would lower tradingvolumes, but it will also help engender greater stabilityin the market. The proposed margin financing systemis in use markets around the world and its implementationin Pakistan is in our view inevitable.

Restricted set of badla stocksThe KSE announced in October that it will reduced thenumber of scrips eligible as margin for badla transactionsto 30. This will become effective on December 15,2003, and has dampened trader enthusiasm somewhat,

BULLETINECONOMICSeptember - October 2003

22

as the decision means less flexibility for speculators. Inour view the market will adjust to the new rule fairlyquickly.

Interest rates rising?There is a general perception that interest rates havebottomed out and will increase slightly from now. Thisis needless to say a threat for the equity markets. TheState Bank, in its 2003 Annual Report has also indicatedthat the surge in liquidity is bound to lead to inflationarypressures, and the focus may now shift to controllinginflation through interest rates and sterilization of excessfunds. So far however the SBP has been very firm incontrolling interest rates through its t-bill and PIB auctioncut off yields and has not allowed a significant rise ininterest rates.

OGDCL adds depth to the marketThe offer for sale of 5% of OGDCL shares (includingthe green shoe option) worth Rs6.9b is big news for themarket. This is the largest IPO in the history of the KSE,and the company will be a pivotal stock, in league withPTCL. The OGDCL IPO is good for the market as it willserve to both deepen and add breadth to what is reallya very small market.

Despite falling remittances, there is still tremendousexcess liquidity as evidenced from the OGDCL oversubscription. An eventual improvement is thereforeexpected in market sentiment and share prices. Sellingfrom banks and the time taken for the market to adjustto new interest rate expectations and badla rules coulddelay that recovery for the short term, but the snowballingnegative sentiment seems to have come under check byearly November.

(Contributed by Taurus Securities Ltd, a subsidiaryof National Bank of Pakistan)

Market OutlookOverall economic fundamentals remain good and thereis a great deal of institutional interest in the market.

BULLETINECONOMICSeptember - October 2003

23

Banks’ Performance at a GlanceNine Months Ended September 30, 2003

Net Interest Income

NBPMCB

Askari Commercial

Bank Al-Falah

Union Bank

PICIC Commercial

Standard CharteredCitib

ank

ABN Amro Bank

Habib Bank A. G. Zurich

(Rs.M

n)

Sep 02 Sep 0310000

900080007000600050004000300020001000

0

Assets400000

300000

200000

100000

0

NBPMCB

Askari Commercial

Bank Al-Falah

Union Bank

PICIC Commercial

Standard Chartered

Citibank

ABN Amro Bank

Habib Bank A. G. Zurich

(Rs.M

n)

Investment200000

180000

160000

140000

120000

100000

80000

60000

40000

20000

0

NBPMCB

Askari Commercial

Bank Al-Falah

Union Bank

PICIC Commercial

Standard CharteredCitib

ank

ABN Amro Bank

Habib Bank A. G. Zurich

(Rs.M

n)

Deposits

NBPMCB

Askari Commercial

Bank Al-Falah

Union Bank

PICIC Commercial

Standard Chartered

Citibank

ABN Amro Bank

Habib Bank A. G. Zurich

(Rs.M

n)

500000

400000

300000

200000

100000

0

Advances

NBPMCB

Askari Commercial

Bank Al-Falah

Union Bank

PICIC Commercial

Standard Chartered

Citibank

ABN Amro Bank

Habib Bank A. G. Zurich

(Rs.M

n)

120000

90000

60000

30000

0

Non fund based Income

NBPMCB

Askari Commercial

Bank Al-Falah

Union Bank

PICIC Commercial

Standard Chartered

Citibank

ABN Amro Bank

Habib Bank A. G. Zurich

(Rs.M

n)

Sep 02 Sep 036000

5000

4000

3000

2000

1000

0

Admin Expenses

NBPMCB

Askari Commerc

ial

Bank Al-Fala

h

Union Bank