UWA BUSINESS SCHOOL University of Western Australia ...

447

Case studies on Internationalisation of companies listed on the Stock Exchange of Singapore for the period from 1998 to 2007 Leong Horn Kee Bachelor of Technology (Production Engineering), University of Loughborough, UK Bachelor of Science (Economics), University of London, UK Bachelor of Arts (Chinese Language and Literature), Beijing Normal University, China Master of Business Administration, INSEAD, France Master of Business Research, University of Western Australia, Australia UWA BUSINESS SCHOOL University of Western Australia Supervised by: Winthrop Professor Ann Tarca This Thesis is presented for the degree of Doctor of Business Administration of the University of Western Australia 2013

Transcript of UWA BUSINESS SCHOOL University of Western Australia ...

Case studies on Internationalisation of companies listed on the Stock

Exchange of Singapore for the period from 1998 to 2007

Leong Horn Kee Bachelor of Technology (Production Engineering), University of Loughborough, UK

Bachelor of Science (Economics), University of London, UK Bachelor of Arts (Chinese Language and Literature), Beijing Normal University, China

Master of Business Administration, INSEAD, France Master of Business Research, University of Western Australia, Australia

UWA BUSINESS SCHOOL University of Western Australia

Supervised by: Winthrop Professor Ann Tarca

This Thesis is presented for the degree of Doctor of Business Administration of the

University of Western Australia

2013

i

ABSTRACT

This study examines the internationalisation of 14 companies listed on the main board

of the Stock Exchange of Singapore (SGX). Past research has been mixed regarding

whether internationalisation has improved the performance of multinational companies

(MNCs). Two established theories on internationalisation are the Eclectic Paradigm

and Uppsala Internationalisation Framework. To determine the best approach to

undertake this study, certain quantitative and qualitative research models for

internationalisation, including Yip’s model, were reviewed. This study adopts a

qualitative approach based on multiple case studies. For the theoretical research

framework, an Internationalisation Reference Model (Reference Model) is developed

using the McGrath Review Model, modified to be applicable for this study. The study

explores the Antecedents, Processes and Outcomes concerning the structures, business

strategies and performance of these SGX companies with regard to their

internationalisation programmes for the period from 1998 to 2007.

The study was conducted in three phases. The first phase was a pilot study that initially

tested the research design and data collection methods. This pilot study aided in the

design of the main study and enabled the formulation of relevant research questions.

The pilot study determined that 12 was the saturation level for the number of

companies to be included in the research. The second phase of the study was the

selection of SGX companies for case study. Companies in the manufacturing industry

were selected and 14 companies agreed to participate. The third phase was to conduct

one-to-one in-depth interviews with these companies’ senior executives such as

ii

Chairmen and Chief Executive Officers (CEOs). Data were collected from the

interviews and archival records such as the annual reports of the companies.

Analysis was undertaken using Nvivo9 software for the interview data, from which

numerous themes and sub-themes of internationalisation relevant to Singaporean

companies were derived. Then the co-axial technique was used to examine the

relationships between internationalisation and actual performance. The cross-company

and intra-industry comparisons were presented, and enlightening perspectives and

results were derived. Using the Reference Model, insights were gained into the

iterative framework of the Antecedents, Processes and Outcomes of these companies’

internationalisation programmes and strategies.

A main research finding is that Singaporean companies’ internationalisation

approaches conform to the established theories of the Eclectic Paradigm and Uppsala

Internationalisation Framework. The second main finding is that the companies in this

study have attained better performance in relation to their level of, and perceived

importance of, internationalisation. Like foreign MNCs, Singaporean companies have

used internationalisation as a main business strategy. Conventional internationalisation

concepts such as economy of scale, localisation of management, centralisation and

decentralisation of resources, and regional expansion; are employed by Singaporean

companies. An interesting finding is that Singaporean companies are driven by certain

themes unique to Singapore such as survival and the small size of the Singapore

market. Of special interest is the finding that most of the sample companies are self-

motivated to venture overseas for opportunities and they have made limited use of the

Singapore government’s promotional incentives and assistance to internationalise.

iii

The study provides a new Reference Model that can be used as a research tool when

studying the internationalisation strategies of companies. The Reference Model offers

another avenue for the conduct of future research on internationalisation. This study

adds to the research on internationalisation. The study gives a deeper understanding

and new perspectives on issues regarding the internationalisation of companies in small

but economically developed countries like Singapore. Although Singapore has a small

domestic market and limited resources, Singaporean companies have managed to

compete effectively in the international arena.

iv

v

CERTIFICATE OF AUTHORSHIP

I hereby declare that this study is my own work. To the best of my knowledge and belief,

it contains no material previously published or written by another person nor material

which to a substantial extent has been accepted for the award of any other degree or

diploma at The University of Western Australia (UWA) or any other educational

institution, except where due acknowledgement is made in the thesis.

I agree that this thesis be accessible for the purpose of study and research in accordance

with the normal conditions established by UWA for the care, loan and reproduction of

theses.

Leong Horn Kee

vi

vii

ACKNOWLEDGEMENTS

This research would not have been completed without the help, assistance and

encouragement of a large number of people. I wish to offer my most heartfelt thanks to

the following:

1. My thesis supervisor Professor Ann Tarca, who is an invaluable source of

guidance and encouragement. Her insight, advice and patience have been

critical for the development and completion of this thesis.

2. The interviewees, who gave their invaluable time and shared their thoughts

openly. Without exception, they were co-operative, helpful and responsive to

my request for interviews, and provided every form of assistance that I needed

for the interviews and research of their companies.

3. My two research assistants, Desmond Khoo and Andrew Ling, who provided

much help in collecting research materials, reports, statistics and documents.

4. My executive secretary, Amy Cheah, who arranged the interviews, typed the

corrections to the report and prepared the transcripts of the interviews. She

collected the companies’ annual reports, and performed the role of general

liaison and co-ordinator among the various parties involved in my research.

5. Elite Editing, for undertaking the professional editing of the thesis, and editorial

intervention was restricted to Standards D and E of the Australian Standards

for Editing Practice.

6. Finally, my personal thanks to my wife and four children for their constant

encouragement, which enabled me to persevere and complete this research.

viii

ix

CONTENTS

ABSTRACT ...................................................................................................................... i CERTIFICATE OF AUTHORSHIP ............................................................................ v

ACKNOWLEDGEMENTS .......................................................................................... vii CONTENTS .................................................................................................................... ix

LIST OF FIGURES ..................................................................................................... xiii LIST OF TABLES ........................................................................................................ xv

LIST OF ABBREVIATIONS .................................................................................... xvii LIST OF APPENDICES ............................................................................................. xix

DEDICATION .............................................................................................................. xxi CHAPTER 1. RESEARCH RATIONALE ................................................................... 1

1.1. Introduction ............................................................................................................ 1 1.2. Overview ................................................................................................................ 1 1.3. Topic ...................................................................................................................... 2 1.4. Potential significance ............................................................................................. 4 1.5. Structure ................................................................................................................. 5 1.6. Conclusion.............................................................................................................. 8

CHAPTER 2. LITERATURE REVIEW ...................................................................... 9 2.1. Introduction ............................................................................................................ 9 2.2. Defining multinationality, globalisation and internationalisation .......................... 9

2.2.1. Multinationality ............................................................................................. 10 2.2.2. Globalisation ................................................................................................. 11 2.2.3. Internationalisation ........................................................................................ 13

2.3. Theoretical foundation of early research .............................................................. 15 2.3.1. Transaction cost analysis theory ................................................................... 16 2.3.2. Foreign direct investments theory ................................................................. 18

2.4. Multinationality and performance ........................................................................ 23 2.4.1. World/USA studies ....................................................................................... 24 2.4.2. European and other country studies .............................................................. 25 2.4.3. Singaporean studies ....................................................................................... 26

2.4.4. Quantitative and qualitative studies .............................................................. 33 2.5. Various levels of internationalisation studies ...................................................... 34

2.5.1. Multiple-industries level studies ................................................................... 34 2.5.2. Industry-level studies .................................................................................... 34 2.5.3. Company-level studies .................................................................................. 35 2.5.4. Subsidiary-level studies ................................................................................ 35

2.6. Imperatives of internationalisation ....................................................................... 36

2.6.1. Eclectic Paradigm ......................................................................................... 36 2.6.2. Uppsala Internationalisation Framework ...................................................... 38

2.7. Factors of internationalisation .............................................................................. 39

2.7.1. Economy of scale .......................................................................................... 40 2.7.2. Geographical diversification ......................................................................... 41 2.7.3. Locational advantage .................................................................................... 41 2.7.4. Learning experience ...................................................................................... 42

2.7.5. Strategic advantage ....................................................................................... 43

x

2.7.6. Options advantage ......................................................................................... 43 2.7.7. Improved product quality .............................................................................. 44

2.7.8. Enhanced customer preference ..................................................................... 45 2.8. Singapore government assistance programmes ................................................... 45 2.9. Research focus ..................................................................................................... 49 2.10. Conclusion ......................................................................................................... 51

CHAPTER 3. RESEARCH DESIGN AND METHODOLOGY .............................. 53 3.1. Introduction .......................................................................................................... 53 3.2. The choice of a qualitative multiple case studies methodology ........................... 54

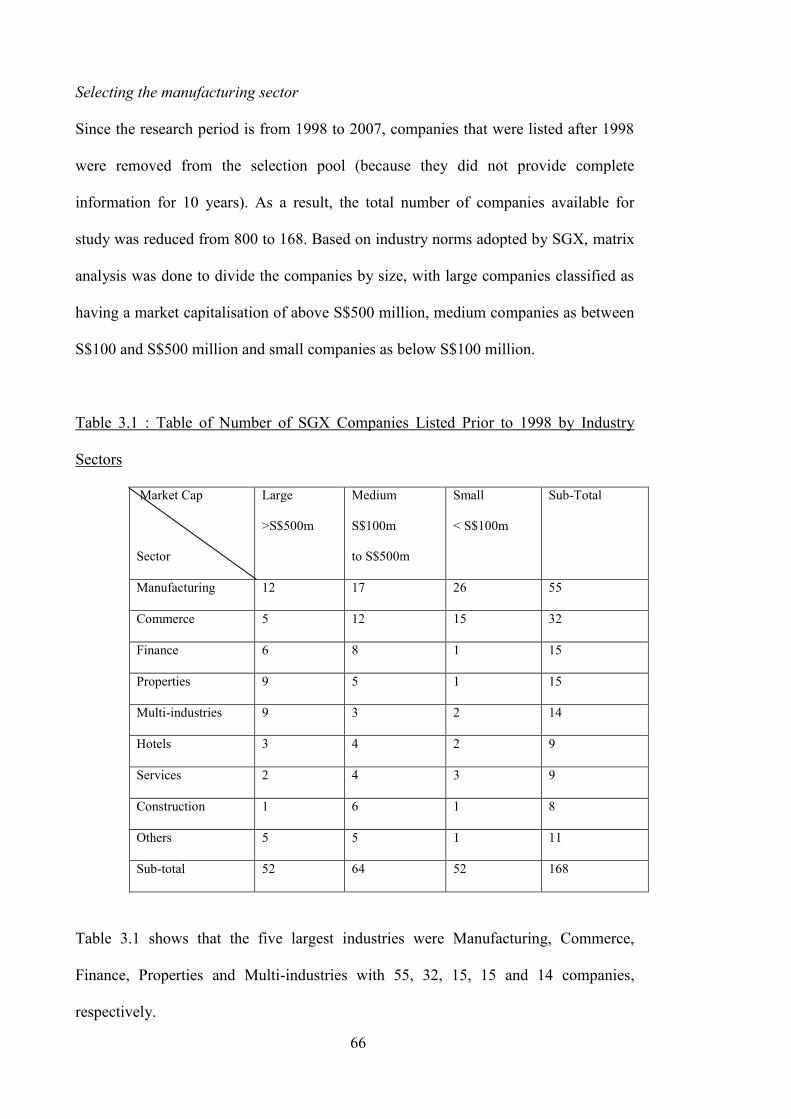

3.2.1. Choice of qualitative approach ..................................................................... 54 3.2.2. Rationale for a multiple case study approach ............................................... 56 3.2.3. Level of studies – company-level and industry-level ................................... 58 3.2.4. Research period 1998 to 2007 ....................................................................... 58 3.2.5. Saturation on number of cases ...................................................................... 60

3.3. Developing a three-stage research approach ........................................................ 61 3.3.1. Phase 1: Pilot study of SGX companies ....................................................... 61

3.3.2. Phase 2: Selection of sector and companies for case study .......................... 63 3.3.3. Phase 3: Multiple case study of selected SGX companies ........................... 69 3.3.4. Interactive data analysis ................................................................................ 75

3.4. Ethical considerations .......................................................................................... 78 3.5. Models of internationalisation ............................................................................. 79

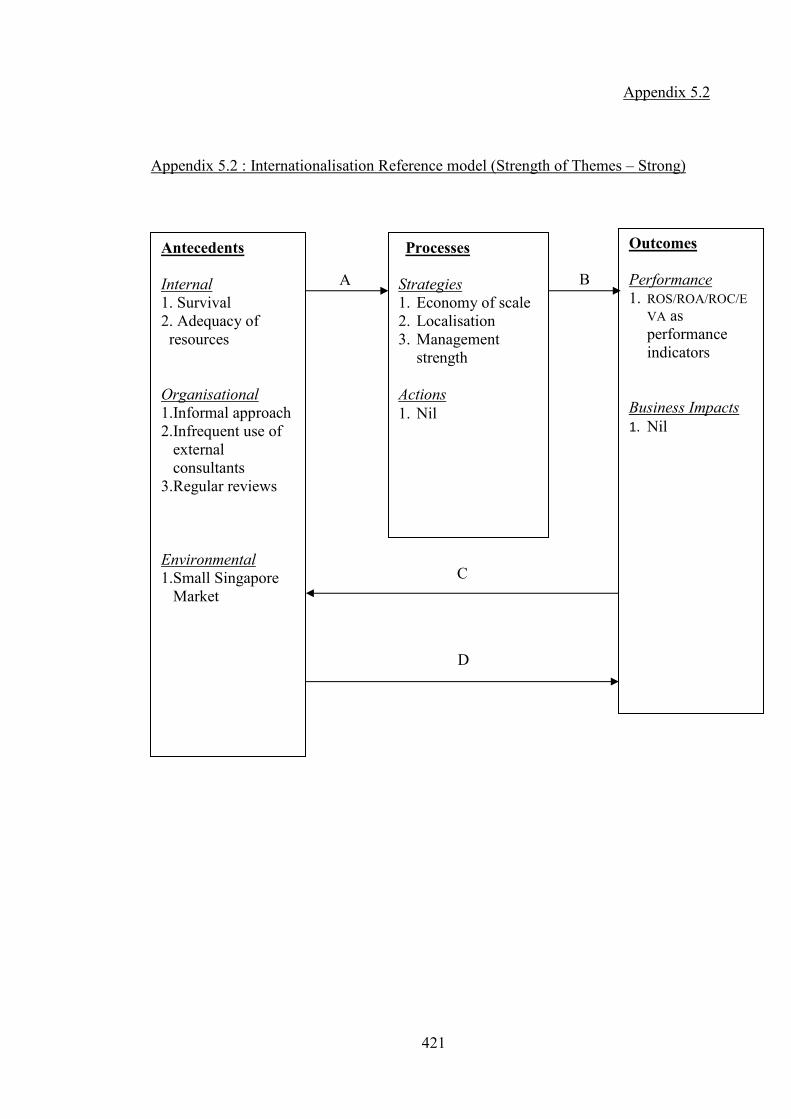

3.5.1. Models in prior literature .............................................................................. 79 3.5.2. Developing an alternative model .................................................................. 84 3.5.3. Model of Internationalisation adopted for this study .................................... 86

3.6. Factors included in the Reference Model ............................................................ 88 3.6.1. Block 1: Antecedents of internationalisation ................................................ 88 3.6.2. Block 2: Processes of internationalisation .................................................... 90 3.6.3. Block 3: Outcomes of internationalisation.................................................... 91

3.7. Internationalisation measures ............................................................................... 92

3.7.1. Measures on the level of internationalisation ............................................... 93 3.8. Key research questions ......................................................................................... 94

3.8.1. Questions relating to antecedents .................................................................. 94 3.8.2. Questions relating to processes ..................................................................... 95 3.8.3. Questions relating to outcomes ..................................................................... 96

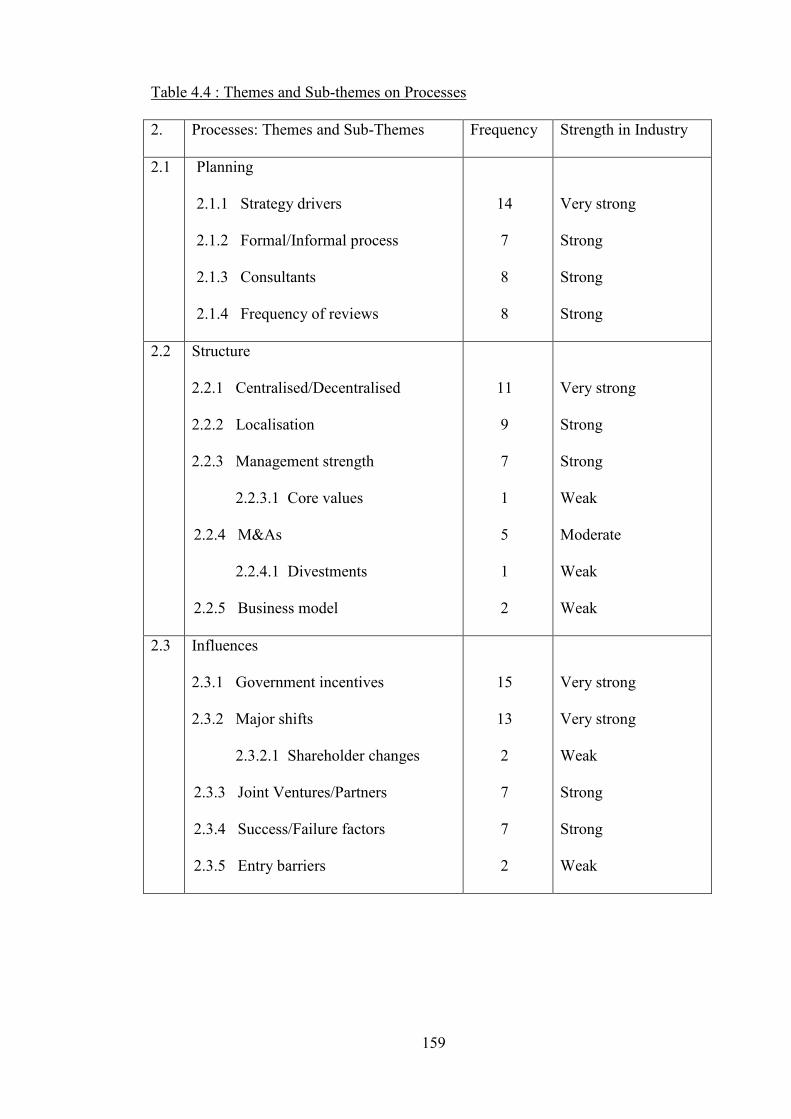

3.9. Data analysis procedures ...................................................................................... 98 3.9.1. Analysis of interview data using NVIVO ..................................................... 99

3.9.2. Data analysis using axial coding and Cruciform charts .............................. 103 3.10. Conclusion ....................................................................................................... 105

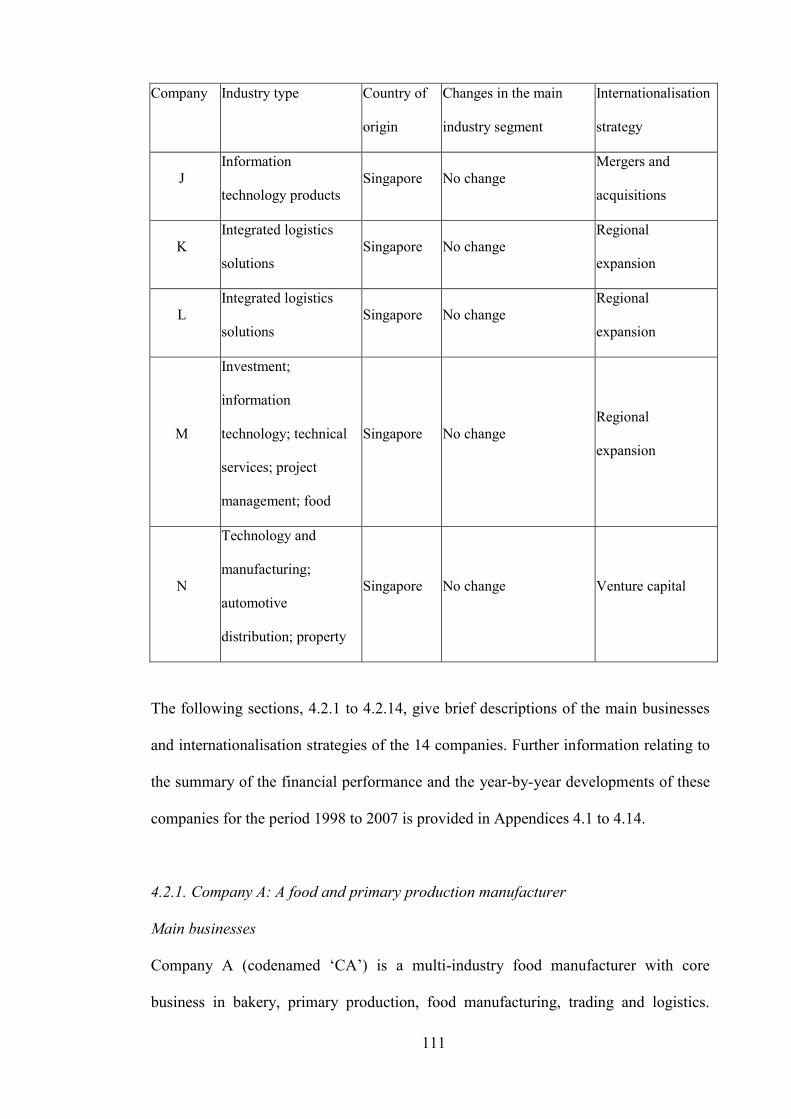

CHAPTER 4. ANALYSIS OF THE 14 SELECTED SGX COMPANIES ............ 107 4.1. Introduction ........................................................................................................ 107 4.2. Businesses and internationalisation strategies of participating SGX

companies ............................................................................................................. 108 4.2.1. Company A: A food and primary production manufacturer ....................... 111

4.2.2. Company B: A global food, beverage and frozen products manufacturer .. 113 4.2.3. Company C: A major alcoholic beverages producer .................................. 117

4.2.4. Company D: A major offshore marine company ........................................ 120 4.2.5. Company E: A manufacturer of motorcycles and motor electronics .......... 124 4.2.6. Company F: An Asian-based construction machinery producer and

distributor ..................................................................................................... 126 4.2.7. Company G: A motor parts and motor related producer ............................ 129 4.2.8. Company H: An IT and property related company..................................... 132

xi

4.2.9. Company I: A producer of construction materials ...................................... 135 4.2.10. Company J: A regional IT products producer and distributer .................. 137

4.2.11. Company K: A global logistics provider .................................................. 140 4.2.12. Company L: A global warehousing and logistic company ....................... 143 4.2.13. Company M: A global manufacturing services company ......................... 146 4.2.14. Company N: An IT products, property and car distribution

conglomerate ................................................................................................ 149 4.3. Analysis of research materials and interview data ............................................. 151 4.4. Theories based on the Eclectic Paradigm and the Uppsala Internationalisation

Framework ............................................................................................................ 152 4.4.1. Companies that adopted Eclectic Paradigm theory ..................................... 154 4.4.2. Companies that adopted Uppsala Internationalisation Framework theory . 155

4.5. Analysis of interview data using Nvivo method ................................................ 156 4.5.1. Antecedents for the internationalisation of SGX companies ...................... 161 4.5.2. Processes for the internationalisation of SGX companies .......................... 192 4.5.3. Outcomes of the internationalisation of SGX companies ........................... 226

4.5.4. Comparison of themes by ‘Strength in industry’ ........................................ 242 4.5.5. Comparison of the themes by size of SGX companies ............................... 247

4.6. Data analysis using Cruciform charts ................................................................ 248 4.7. Answers to key research questions .................................................................... 254

4.7.1. Questions relating to antecedents ................................................................ 255 4.7.2. Questions relating to processes ................................................................... 256 4.7.3. Questions relating to outcomes ................................................................... 257

4.8. Conclusion.......................................................................................................... 260

CHAPTER 5. CONCLUSION ................................................................................... 263 5.1. Introduction ........................................................................................................ 263 5.2. Theoretical findings and contribution ................................................................ 265

5.2.1. Theoretical findings .................................................................................... 265 5.2.2. Value of theoretical findings ....................................................................... 269

5.2.3. Theoretical contribution .............................................................................. 269 5.3. Empirical findings and contribution................................................................... 271

5.3.1. Empirical findings ....................................................................................... 271 5.3.2. Empirical contribution ................................................................................ 276

5.4. Implications for practitioners ............................................................................. 277

5.5. Limitations and areas for future research ........................................................... 279 5.5.1. Limitations .................................................................................................. 279

5.5.2. Areas for future research ............................................................................. 283 5.6. Conclusion.......................................................................................................... 285

BIBLIOGRAPHY ....................................................................................................... 287

LIST OF APPENDICES ............................................................................................ 303

xii

xiii

LIST OF FIGURES

Figure 3.1 : Interactive Data Analysis (Miles and Huberman 1994) ..................... 76

Figure 3.2 : Osegowitsch’s (2003) Model of Internationalisation and

Performance ........................................................................................ 80

Figure 3.3 : Yip’s Globalisation Drivers Model .................................................... 82

Figure 3.4 : McGrath General Model ..................................................................... 85

Figure 3.5 : Internationalisation Reference Model ................................................ 87

Figure 3.6 : Sample Cruciform Chart of Revenue Growth Versus Level of

Internationalisation ............................................................................ 104

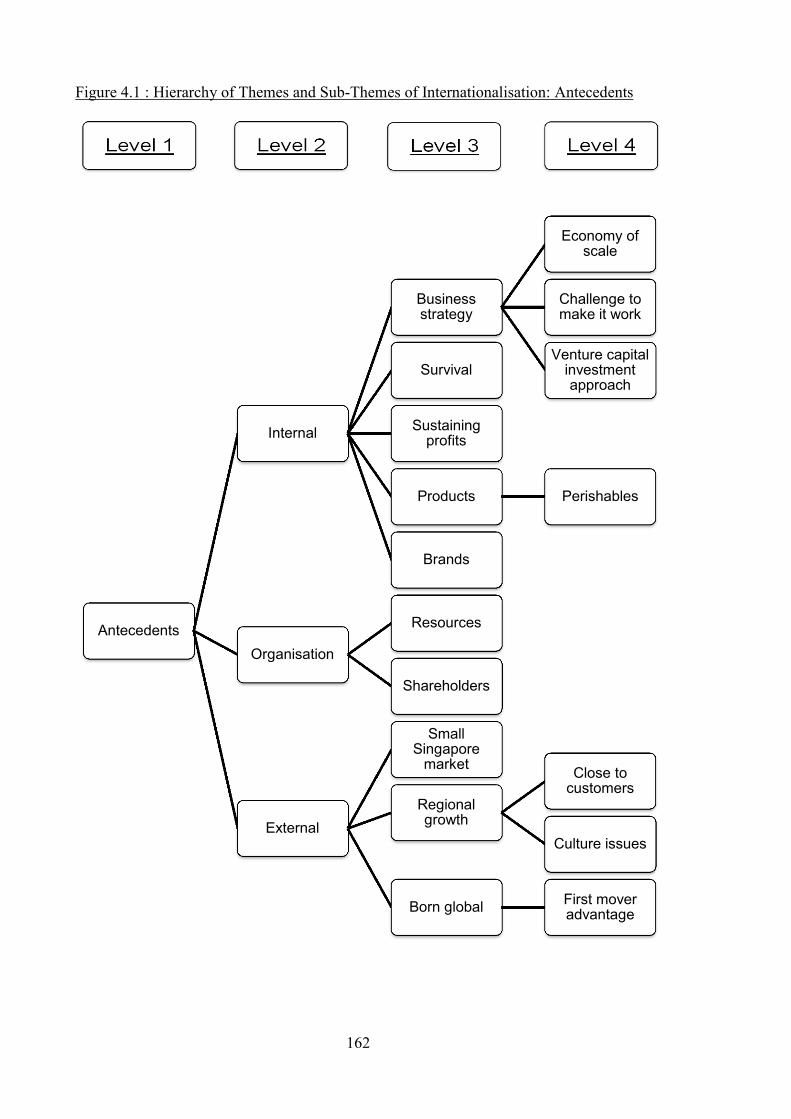

Figure 4.1 : Hierarchy of Themes and Sub-Themes of Internationalisation:

Antecedents ....................................................................................... 162

Figure 4.2 : Hierarchy of Themes and Sub-themes of Internationalisation:

Processes ........................................................................................... 193

Figure 4.3 : Hierarchy of Themes and Sub-themes of Internationalisation:

Outcomes ........................................................................................... 227

Figure 4.4 : Revenue Growth v. Level of Internationalisation Achieved ............ 249

Figure 4.5 : Profit Growth v. Level of Internationalisation Achieved ................. 250

Figure 4.6 : Revenue Growth v. Importance of Internationalisation ................... 252

Figure 4.7 : Profit Growth v. Importance of Internationalisation ........................ 253

xiv

xv

LIST OF TABLES

Table 2.1 : Studies of Internationalisation and Performance ................................. 30

Table 3.1 : Table of Number of SGX Companies Listed Prior to 1998 by

Industry Sectors ................................................................................... 66

Table 3.2 : Nvivo Analysis—Sample Table ........................................................ 102

Table 4.1 : Summary Table of the 14 Participating SGX Companies ................. 110

Table 4.2 : Adoption of Internationalisation Theories ......................................... 154

Table 4.3 : Themes and Sub-themes on Antecedents .......................................... 158

Table 4.4 : Themes and Sub-themes on Processes ............................................... 159

Table 4.5 : Themes and Sub-themes on Outcomes .............................................. 160

Table 4.6 : List of Themes and Sub-themes by Order of Strength in Industry .... 243

Table 4.7 : Comparison of Consistent and Unique Themes................................. 247

xvi

xvii

LIST OF ABBREVIATIONS

ASEAN Association of Southeast Asian Nations

CEO Chief Executive Officer

CFO Chief Financial Officer

CIS Commonwealth of Independent States

COE Certificate of Entitlement

DOI degree of internationalisation

DTD Double Tax Deduction

EVA Economic Value-Added

GEM Growth Enterprise Market

GLC government-linked companies

HR human resource

ICSB International Council for Small Business

IES International Enterprise Singapore

KPI key performance indicator

M&A merger and acquisition

MD Managing Director

MNC multinational company

NVOCC Non-Vessel Operating Common Carrier

PATMI profit after tax and minority interest

PFI Participating Financial Institution

PRC People’s Republic of China

R&D research and development

ROA return on assets

ROE return on equity

xviii

ROI return on investments

ROS return on sales

SBU strategic business unit

SGX Stock Exchange of Singapore

SEM structural equation modelling

SME small- and medium-sized enterprise

TCA transaction cost analysis

UK United Kingdom

xix

LIST OF APPENDICES

Appendix Page

Appendix 2.1 : Definitions of Globalisation ........................................................ 305

Appendix 2.2 : Details of International Enterprise Singapore incentives ............ 307

Appendix 3.1 : Pilot Study ................................................................................... 309

Appendix 3.2 : Letter of Invitation ...................................................................... 333

Appendix 3.3 : List of Participating Companies* and Executives*..................... 334

Appendix 3.4 : Consent Form .............................................................................. 335

Appendix 3.5 : Interview Guide ........................................................................... 336

Appendix 3.6 : Summary table of interview responses........................................ 338

Appendix 4.1 : Summary of developments and financials of Company A .......... 359

Appendix 4.2 : Summary of developments and financials of Company B .......... 363

Appendix 4.3 : Summary of developments and financials of Company C .......... 367

Appendix 4.4 : Summary of developments and financials of Company D .......... 371

Appendix 4.5 : Summary of developments and financials of Company E .......... 375

Appendix 4.6 : Summary of developments and financials of Company F .......... 379

Appendix 4.7 : Summary of developments and financials of Company G .......... 383

Appendix 4.8 : Summary of developments and financials of Company H .......... 387

Appendix 4.9 : Summary of developments and financials of Company I ........... 391

Appendix 4.10 : Summary of developments and financials of Company J ......... 395

Appendix 4.11 : Summary of developments and financials of Company K ........ 398

Appendix 4.12 : Summary of developments and financials of Company L ........ 402

Appendix 4.13 : Summary of developments and financials of Company M ....... 406

Appendix 4.14 : Summary of developments and financials of Company N ........ 409

Appendix 4.15 : Nodes / Sub-Nodes and Sources from Nvivo9 analysis ............ 413

Appendix 4.16 : Table of 10-year Revenue and profit average annual growth

rate of return and survey results ........................................................ 419

Appendix 5.1 : Internationalisation Reference model (Strength of Themes –

Very Strong) ...................................................................................... 420

Appendix 5.2 : Internationalisation Reference model (Strength of Themes –

Strong) ............................................................................................... 421

Appendix 5.3 : Internationalisation reference model (Strength of Themes –

Medium) ............................................................................................ 422

xx

Appendix 5.4 : Internationalisation reference model (Strength of Themes –

Weak) ................................................................................................ 423

xxi

DEDICATION

Dedicated to my wife Lee Eng, and my four children, Celine, Alvin, Bessie and

Delphine.

xxii

1

CHAPTER 1. RESEARCH RATIONALE

1.1. Introduction

This chapter explains the motivation for my study. It gives an overview of the scope of

the thesis and explains the research topic and its significance. This is followed by a

description of the structure of the research.

1.2. Overview

Over the past several decades, there has been a large increase in the number of

companies that have expanded beyond their national boundaries to locate parts of their

operations in other countries. Many reasons are given for internationalisation, such as

to be closer to customers or to take advantage of lower production costs or other

strategic and operational factors. Some companies have also sought to establish closer

and longer-term business relationships with their overseas partners (Wheatley, 1991,

Williams et al., 1998).

To leverage on their competitive advantages and ensure business survival in the fast

changing global economic environment, corporations have been shifting away from

depending on their domestic markets to develop a more globalised reach. This allows

them to diversify factor input sources and markets and to derive production capabilities

in different locations, technological knowhow and competitive strengths. As a result,

whether through organic growth or acquisitions, we have observed a major

international consolidation of companies, which has created truly multinational

companies (MNCs).

2

Multinationality started in developed countries such as the United States (US), United

Kingdom (UK), Japan and Germany. In recent years, even companies in small

countries such as Singapore have ventured overseas, seeking the benefits to be derived

from internationalisation. International business relationships are increasingly looked

upon as a strategic option equivalent to other business strategies like knowhow,

products and technologies (Friedman, 2005, Webster, 1992, Zain and Ng, 2006).

The primary focus of my thesis is to explore the global integration and

internationalisation strategies, processes and outcomes of Singaporean companies

during the period from 1998 to 2007. This is particularly pertinent because Singapore

has a very small and limited domestic market, and the Singapore government has been

promoting the internationalisation of local companies for the past three decades.

1.3. Topic

My study examines the influence of internationalisation on the performance of

companies listed on the Stock Exchange of Singapore (SGX) for the 10-year period

from 1998 to 2007. Singapore is evaluated by Foreign Policy, a US-based magazine,

and AT Kearny as one of the countries with the highest level of internationalisation

based on the International Cities Index (Foreign Policy, 2006). Internationalisation is a

strategic variable that affects the competitiveness of a country. Numerous aspects of

internationalisation have been explored in the past in the industrialised countries. As

Singapore is a newly developed economy, it is interesting to explore how

internationalisation has influenced Singapore-incorporated companies. There are

currently over 800 companies listed on the SGX. They constitute a sizeable base of

companies with publicly available market, business and company data to support the

research.

3

Numerous studies have investigated the motivations for corporations to become

international and the resulting influence of internationalisation on these companies.

Companies need or choose to become international for a variety of reasons such as

growth, survival, competitiveness, economies of scale, proximity to markets and

performance enhancement (Hutzschenreuter and Guenther, 2008, Kogut, 1989, Kogut,

1999).

Internationalisation has been generally defined as ‘a strategy undertaken by a

corporation to expand overseas to take advantage of various factors such as costs and

proximity to markets in the overseas markets’ (Fallah and Lechler, 2008).

Internationalisation refers to the overall extent of a company’s international

engagement. It can be represented by the amount of foreign-based assets as compared

to its total assets; the percentage of foreign-based sales as compared to total sales; or

the percentage of its operations located in foreign countries compared to total

operations. Most corporations started from large domestic home markets like the US,

UK, Europe and Japan. One of the main objectives of internationalisation is to improve

profitability (Norbarck and Persson, 2008). Only a limited number of studies have been

done on Southeast Asian and Singaporean companies (Siew Meng and Chin Tiong,

1993, Birkinshaw, 1995).

Publicly listed companies were selected for study because some details on the

companies’ history, business scope, plans, financial data, factories and operations

locally and overseas are available publicly in their annual reports.

4

This research is interesting and worthwhile, as it will enable managers to have a better

understanding of the imperatives and motivations that drive Singaporean companies to

become international. It also extends the literature by providing a comparison with

previous studies on this subject done by other researchers in Singapore and overseas.

The differences in experiences, strategies and performance results will enable the

formulation of a set of internationalisation strategies that could be more relevant for

Singapore-based companies.

1.4. Potential significance

From the onset, internationalisation has caused geographical boundaries to fade as new

business paradigms emerge. The traditional method of doing business within national

borders, dependent solely on huge domestic markets (for example, the US is a large

market in itself), has changed with the emergence of the global village (Friedman,

2005). To prepare companies to exit their national borders, it is important for them to

understand the effects, relationships and implications of the internationalisation

phenomenon, and to equip themselves with the knowledge and competencies to

overcome likely changes and challenges.

In Singapore’s context, internationalisation is a policy issue that has great significance.

As early as in 1992, Mr Lee Kuan Yew (Singapore’s former Prime Minister) urged

Singaporean companies to venture overseas. He termed it quaintly as ‘to spread a

second wing, that is an external wing’. Since then, the Singapore government has been

actively promoting the internationalisation of Singaporean companies through

government initiatives and policies aimed at encouraging and incentivising companies

to expand overseas. In particular, Singapore’s government-linked companies (GLCs)

have been encouraged to expand more actively overseas. This study examines the

5

measures undertaken by the Singapore government to promote internationalisation,

whether these initiatives had been effective, and the policy implications that can be

concluded from the analysis of the evidence and results.

This thesis therefore examines both the efforts directed by the Singapore government

as well as the private sector’s initiatives towards internationalisation as a business

strategy. The shared experience of becoming international will enable Singaporean

companies to better structure their organisations to tackle the world market and to

adopt the right strategies and action plans to compete well in the international arena.

The research will add to current knowledge on internationalisation and enable further

research in an area that is becoming increasingly relevant in today’s highly connected,

technology-driven and internationally competitive world market.

1.5. Structure

The study is structured into five main chapters. Following Chapter 1, which gives an

overview of the research rationale, Chapter 2 presents the literature review of relevant

research, from the seminal work by Vernon (1971) to the numerous studies looking at

the relationship between performance of large MNCs and their level of

internationalisation. The chapter describes the theoretical foundations of the research

on internationalisation. Noteworthy is the revelation that quantitative methods of

research have led to different results about the impact on the performance of

corporations. This subsequently led to more studies being conducted using qualitative

methods to derive deeper insights on internationalisation theories and strategies. The

two recognised theories on internationalisation are the Eclectic Paradigm and the

Uppsala Internationalisation Framework (Johanson and Vahlne, 2009). The chapter

ends by stating the perceived research gaps and intended research emphasis.

6

Chapter 3 describes the rationale for the selection of the qualitative case study

approach. The research is conducted in three phases:

1. A pilot study is undertaken to test the primary research parameters such as the

saturation level on the potential number of companies to be interviewed, the

relevant questions and issues to be posed, and the appropriateness of the

companies and interviewees to be selected.

2. An analysis of all SGX companies is conducted by examining the

internationalisation factors and performance measures based on data from

publicly available databases of SGX companies. This exercise enabled the

selection and invitation of an appropriate group of target companies for

participation in the case study research.

3. An in-depth qualitative study is conducted by using the case study approach to

examine in detail the purposes, processes and outcomes of the

internationalisation of selected SGX companies, by conducting one-to-one in-

depth interviews with the key senior executives of the participating companies.

Phase 1 (Pilot study) is meant to be a brief study, and Phase 2 is to examine the

publicly available data on the internationalisation of SGX companies and provide the

basis for the selection of an appropriate cluster of companies for the main part of the

research. Phase 3 is to conduct an in-depth study into selected companies. The main

results and findings are derived from the research materials gathered in Phase 2 and

from the in-depth case study interviews in Phase 3.

In the latter part of Chapter 3, certain previous quantitative and qualitative research

methodologies are examined, and a Reference Model is developed that is deemed

7

suitable for use in this study. The Reference Model displays the internationalisation

process in three blocks: Antecedents, Processes and Outcomes.

Following the Reference Model, key research questions are formulated. The first key

research question is ‘Does internationalisation result in better performance for

Singaporean companies?’ The two key research questions that follow are ‘What are the

main motivations for a Singaporean company to go international?’ and ‘What are the

outcomes of the internationalisation process?’ Another relevant and interesting

question is ‘As the Singapore government actively promotes internationalisation, do

government initiatives have any impact on the push of Singaporean companies to

internationalise?’

Chapter 3 concludes with a description of the data gathering techniques and procedures

using Nvivo9 software and co-axial analysis.

Chapter 4 provides the summary information on the selected SGX companies and

gives an analysis of the survey results using Nvivo9 software. The analysis provides

the answers to the various key research questions, and describes the themes and sub-

themes emerging from the interviews. Further analysis is conducted using co-axial

analysis, comparing the rated level and importance of internationalisation against the

actual performance of the companies.

Chapter 5 provides a summary of the main findings and their implications, and the

contributions of the thesis to the current body of research on internationalisation.

8

1.6. Conclusion

This chapter explains the research rationale and structure of the study. The research is a

worthwhile project because it adds to the knowledge and understanding of

internationalisation for companies in a small economy like Singapore. The next chapter

explores the literature in depth, considering both pioneering and current research on the

topic of internationalisation.

9

CHAPTER 2. LITERATURE REVIEW

2.1. Introduction

This chapter provides an overview of prior research undertaken in the area of

internationalisation. The chapter begins by explaining the meaning of

internationalisation, multinational corporations and globalisation. It then outlines the

key theoretical concepts and provides a review of the early quantitative studies that

compared the relationship between multinationality and internationalisation. The

review covers the research on internationalisation at the company, subsidiary, industry

and multiple-industries levels, and discusses the benefits of internationalisation in

many country settings. This chapter also discusses the research on the

internationalisation of Singaporean companies and the Singapore government’s

assistance for companies’ internationalisation objectives. The chapter concludes by

identifying the research gaps in the literature that led to the choice of research

emphasis for this thesis.

2.2. Defining multinationality, globalisation and internationalisation

One of the early pioneers of the globalisation literature was Fayerweather (1969), who

described globalisation as a ‘unification idea’ in which an MNC presents a completely

unified stance in all countries in which it does business, with standardised products

based on concentrated production. Another well-recognised early article on global

strategy was by Levitt (1983), who discussed the concept of the global village and

suggested that the use of a global strategy was inevitable, and that all companies would

one day be producing globally standardised products for unified markets. Cvar (1986)

further expressed the view that a global company is one organised in such a way as to

take maximum advantage of efficiencies through the reduction of costs wherever

10

possible. Thereafter, there was a strong groundswell by MNCs to standardise their

products and procedures across the globe.

In the past, globalisation and global strategy were viewed together as a generic

international strategy adopted by multinational companies as an alternative to ‘multi-

domestic’ or ‘multi-local’ strategies, by locating their operations or plants in different

countries. This status of a company is generally termed as ‘multinationality’. It was

further expounded that multinationals, which put local responsiveness first, would

choose a multi-local strategy, while companies that decided to pursue lower costs

would choose an internationalisation strategy. This uni-dimensional view looked upon

the choice to adopt a global strategy as a conscious decision to base the company’s

international competitive strategy on the main objective of lowering costs through

concentration of production and a drive towards standardisation of production and

marketing policies.

2.2.1. Multinationality

‘Multinationality’ was defined in a 1973 United Nations article on ‘Multinational

Corporations in World Development’ as the status of a corporation or enterprise that is

involved in activities in more than one nation. It stated that there are certain qualifying

criteria to be used in respect of the type of activities or the importance of the foreign

component in the total activity. These activities may be related to sales, assets,

production, employment or profits generated by the foreign branches and affiliates. A

foreign branch is defined as that part of the corporation that operates abroad. An

affiliate is the part of the corporation under effective control of the parent company and

may be either a subsidiary (with the parent holding a majority of shares or a lesser

portion), or an associate (in which the investor holds 20 per cent or less of shares).

11

Deriving from this definition, any corporation with one or more foreign branches or

affiliates engaged in any of the activities mentioned will qualify as ‘multinational’.

2.2.2. Globalisation

There have been many discussions of the definitions of globalisation in numerous

research papers and reports (Beyer, 1994, Cairncross, 1997, Dicken, 1998, Dunning,

1993a, Giddens, 1990, Jameson and Miyoshi, 1998, Robertson, 1992, Walters, 2002).

These have covered a wide range of perspectives and definitions of globalisation from

a variety of academic, linguistic, economic and religious fields and have demonstrated

a considerable variance in concepts and approaches (see Appendix 2.1: Definitions of

Globalisation). However, three common factors are evident: (1): the integration of a

previously insular national or regional phenomenon (for example, culture, interest rates,

technology, ideas, consumption patterns, diseases or standards) into some sort of

worldwide, or near worldwide structure; (2) the process by which this integration

occurs; and (3) identification of a set of integrating mechanisms (for example, disease

paths, exchange rates, trade, foreign direct investment, books, movies, travel or internet)

that facilitate the integration by transmitting influence (for example, disease pathogens,

inflationary pressure, fashions or behaviours) from one location to another.

Building on these points, the following general description of globalisation is offered

by a practitioner article (Clark and Knowles, 2003). Globalisation is the process by

which economic, political, cultural, social and other relevant systems of nations are

integrating into world systems. It has the following two elements:

(a) A world system, which is a planet-wide complex of channels capable of

transmitting stimuli simultaneously to many locations at wide geographic distances;

and

12

(b) A degree of globalisation, which is the extent to which the economic, political,

cultural, social and other relevant systems of nations are actually integrated into world

systems. This degree varies considerably.

This description has the virtue of being general, in that it does not limit globalisation to

any particular metric, observable phenomenon, model, theory or disciplinary

perspective; yet, it captures the basic idea that all fields are grappling with and

attempting to model into their own academic context. The description also recognises

globalisation as a dynamic process that affects different phenomena to varying degrees,

occurring in economic, cultural or social domains. The description also provides a

framework for capturing the rate at which the process is advancing in particular

contexts. Emerging and existing world systems include inflation, interest rates,

business cycles, fashion, pop music, technical and professional standards, consumption

behaviours, diseases and media.

In recent years, with the rise of the green movement and concerns about environment

protection, the process of globalisation has been blamed as the cause of the spread of

diseases, the breakdown of cultures and changes in geo-political power across nations.

Numerous sociologists, scientists, anthropologists and environmentalists have

examined the topic and sought to identify the impact of globalisation in their respective

fields (Friedman, 1999). Giddens (1999) opined that the widespread usage and

coverage of the term globalisation has led to referring to it as a ‘runaway force’, which

leads to the convergent view that globalisation has been overly faulted for all cross-

border ills in cultural, social, political and economic arenas.

13

Globalisation has been generally employed as a broad-based term for the process

whereby global forces or developments interact and give rise to the social advent called

‘globalisation’, a phenomenon involving different organisations, nations or entities.

2.2.3. Internationalisation

Internationalisation has been generally interpreted in a variety of ways, with the most

common concept being the optimisation of various resources by MNCs to be located in

different countries (Ghoshal, 1987, Ghoshal and Bartlett, 1988a). According to Kobrin

(1991), an internationalised company contains subunits that can be incomplete

economic entities, and their value is, as part of the entire organisation, derived from

their relationships with others, to produce maximum returns for the group. Therefore,

increasing and strengthening integration should result in increased intra-unit exchanges

of people, raw materials, resources, technologies, components and finished products.

However, these views alone do not define what internationalisation actually is. Among

other things, internationalisation can be a negative connotation. It has been described

as the advent of a force that has led, on the premise of worldwide economic

advancement and integration, to global environmental degradation and economic

exploitation.

Bartlett and Ghoshal (1989) proposed an organisational form they termed the

transnational, and re-iterated the conventional view that in the internationalised

organisation, the cost and quality advantages of global efficiency are expected to

provide optimal value that customers will eschew differences in preferences and accept

standard products. The current conventional wisdom tends to continue to equate

internationalisation with lowering of costs and standardisation, with Hill and Jones’s

(2000) widely used text on strategic management being one such example. Birkinshaw

14

(1995) provided additional support where he stated that economy of scale was the most

significant driver of international integration in his study of US manufacturing

companies.

It is therefore understandably difficult to define a term that in recent years has come to

mean many different things. For the purposes of this study, it is necessary to

concentrate on the application of the term ‘internationalisation’ with regard to how it

has affected Singapore-based international business corporations, and in particular, to

focus on what is understood by the term ‘internationalisation strategy’. This approach

does not seek to ignore the wider social and technological impacts of

internationalisation. However, it aims to focus primarily on business and management

literature in which business strategies have been placed at the core of this

internationalisation research. This is in accordance with Bartlett and Ghoshal (1989),

who have ventured to term multinational corporations as the ‘dominant vehicle’ of

internationalisation.

In summary, this study defines internationalisation as:

A strategy undertaken by a corporation to expand overseas to take

advantage of various factors such as costs of production, drawing upon

domestic resources, manpower and regulatory advantages, sharing of

technologies and knowhow across borders, and proximity to markets in

the overseas markets.

For the purpose of this thesis, the term ‘internationalisation’ is used as a business-

related concept that refers to the process of MNCs expanding and shifting their

operations overseas. Therefore, throughout this thesis, the term internationalisation is

15

use for the study of MNCs. In summary, globalisation is used to describe a social

phenomenon, whereas internationalisation describes a business process.

In terms of the relationship between multinationality and internationalisation, in this

thesis, internationalisation describes the process through which MNCs expanded out of

their domestic markets and established branches or affiliates overseas.

2.3. Theoretical foundation of early research

The study of the internationalisation of companies has traditionally focused on

manufacturing MNCs, although later studies have extended the scope to services and

other sectors. Early studies tended to compare the level of internationalisation against

performance, and explored issues relating to the motivations for, and benefits of,

internationalisation. Typically, the main proposition underpinning the research was that

more internationalisation should lead to better performance. Later studies became more

interdisciplinary in nature and encompassed areas such as strategic management,

international business concepts, international finance and economics. Other research

has also ventured into the various cultural and cross-cultural aspects of

internationalisation (Gaines and Liu, 2000, Hewapathirana, 2009, Pei-Wen, 2004).

Vernon’s pioneering seminal work investigated the association between

internationalisation and performance (Vernon, 1971, Vernon, 1981). He made a

comparison of the Return on Assets (ROA) of domestic companies and MNCs, and

found the latter to have superior performance.

The subsequent studies by Vernon and others investigating the influence of

internationalisation on corporations tended to adopt comparative approaches. For

16

example (Grant et al., 1988) examined the relative performance of corporations that

had remained domestic against those that had become international. The early research

was mainly conducted on European and US companies. Later research expanded the

coverage to Japan and other countries, as these countries started to produce several

large international companies. Recent research has tended to focus on MNCs and to

adopt control approaches. Researchers have used operational multinationality as a

continuous variable for comparison against performance. The theoretical foundation

underpinning the examination of the internationalisation of companies and their

performance rests on two key concepts. The first is the transaction cost analysis theory

(TCA), which states that a company’s decision either to undertake a transaction

themselves in their internal structure between related entities or to let the market

perform the transaction is based on transaction cost differentials (Coase, 1937,

Williamson, 1976). According to this theory, the cost benefit advantages of

internationalisation have to be greater than the additional direct costs brought by the

complexities and uncertainties caused by internationalisation.

2.3.1. Transaction cost analysis theory

Williamson (1975, 1985) explained that TCA is based on the premise that a company

will internalise those activities that it is able to conduct at a lower cost, and rely on

external providers for activities in which such providers have an advantage. TCA is

developed on a micro-analytic framework with strong links to observed behaviour.

Companies are assumed to be subject to bounded rationality. In addition, at least some

companies are assumed to be opportunistic if given the chance. Similarly, imperfect or

asymmetric market information will give some companies the opportunity to exploit

advantages (especially financial) in their dealings with other companies.

17

Transaction costs (such as the costs governing a production system) tend to be low in

highly competitive markets, and therefore provide minimal or no cost advantage or

incentive to substitute internal organisation for market exchange. In comparison, when

confronted with an imperfect market or market intelligence, companies are expected to

internalise transactions to reduce costs of exchange. The objective of forward

integration of operations is to minimise the sum of transaction costs (John and Weitz,

1988, Williamson, 1985). The higher the cost of contracting externally, the greater will

be the incentive to internalise transactions.

Forward integration means that a company may decide to invest into businesses that

relate to its main products, such as into other similar and related products or services,

or those that are downstream businesses to the main production output of the company.

Backward integration is the business direction where the company invests into sub-

components, supplies and support services that lead to the production of its main

products.

However, unlike production costs, transaction costs are very difficult to measure and

estimate precisely, because they represent the potential outcomes of alternative

decisions. John and Weitz (1988) said that studying transaction cost issues often cannot

measure such costs directly, instead only testing whether organisational relations align

with the attributes of transactions as predicted by the transaction cost rationale.

Studies of TCA in terms of asset specificity and internal uncertainty have been

conducted by numerous researchers (Anderson, 1985, John and Weitz, 1988, Anderson

and Coughlan, 1987). Asset specificity refers to the extent to which specialised internal

18

investments are required to support a transaction, whereas uncertainty refers to the

ability to predict the relevant contingencies, both internal and external to the company.

2.3.2. Foreign direct investments theory

The second research approach employed in the early period is the theory of foreign

direct investments, which is focused on how MNCs conduct business internationally.

Hymer (1976) initiated the concept of market imperfections and considered that the

TCA of internationalisation concept propounded by Coase (1937) can be extended to a

theory of foreign direct investments (Hymer, 1976, Hymer, 1960). This theory posits

that companies can exploit differential advantages in labour, land, resources, tax, local

knowledge and other factors through foreign direct investments into foreign markets.

Companies undertake cross-border geographical diversification because they can

exploit unique advantages of proprietary knowledge, technological advantages,

managerial skills, availability of resources, supply of raw materials and other

intangible assets, which enable them to make extraordinary performance gains.

Aharoni (1966) presented a discourse on the definition and process of foreign direct

investments. He suggested that the foreign investment decision process was not a

single identifiable act, and viewed it as a complex succession of acts involving a

dynamic social and interactive process of mutual influences among various executives

of a company, constrained by the company’s business strategy, resources and the

management or manpower capacity, goals and needs of its members, throughout which

choices emerge (Aharoni, 1966).

The foreign investment decision process is undertaken by a group of executives in a

company, who typically have different backgrounds, knowledge, experience and

19

orientations. It is a long process and involves different organisational levels. Decisions

are made under uncertainty because of the lack of information and the limited capacity

of the management team.

According to Aharoni (1966), the decision process starts because of an outside factor

that causes a decision-maker to look overseas. The strength of this force determines the

investigation process, throughout which management accumulates psychological

commitments toward other organisations and entities. The more committed they

become, the higher the probability of a decision to invest. Thus, if the force that caused

the manager to look abroad is strong enough, the decision to invest abroad is gradually

formed, and the investigation process may concentrate on minimising the size of the

investment and the risks involved. The process changes with the accumulation of

experience and the result of organisational modifications such as the creation of an

international division.

Aharoni (1966) considers that a foreign investment decision process includes several

elements. First, any choice made by a company depends on its internal systems. These

systems comprise management’s relations with other individuals and entities both

within and outside the company, including customers, suppliers, banks, competitors

and government agencies in host and home countries. Second, the process evolves over

a certain (and potentially extended) period of time. Third, decisions are made under

uncertainty, which means that the management’s perception of uncertainty is a major

element in the process. This perception changes as a result of experience and

knowledge, and management’s level of interest can vary over time, reflecting how

comfortable they are with the uncertainty surrounding the decision. Fourth, companies

20

have goals and objectives. Finally, there are many constraints on the freedom of action

of the management.

The decision-making process is spread over a long period (Aharoni, 1966). Implicit

and explicit negotiations, both inside the company and with outsiders, may cause the

process to become extended. During that period, there can be many changes; it is often

found that certain factors were not taken into account, were taken over by events or

proved to be unpredictable. These changes invariably require more modifications,

more approvals and sometimes a new round of negotiations has to be started.

When a series of investment decisions are examined, another important factor emerges

which is the accumulation of experience by executives in various echelons regarding

foreign investments creates profound changes in the company itself. Gradually,

companies evolve into multinational corporations, after successfully establishing or

acquiring operations and business opportunities abroad (Aharoni, 1966).

Organisations learn, and with learning the perception of uncertainty in foreign

operations changes; that is, investments previously perceived as risky become

acceptable. When the process is put in a historical perspective, it may be observed that

the company commenced to look overseas after it received significant export orders

over a period of time. Alternatively, a foreign agent might have developed an overseas

market, with the management paying little or no attention to this foreign development.

With the growth of export business, sometimes even without any deliberate action

from headquarters (HQ), an export department may have been created. This, in turn,

forms a group of people in the company who feel obligated, driven by their vested

21

interest, to expand the company’s international operations. The very existence of an

international division gives a momentum to international operations, which are

subsequently expanded. The assignment of a group of executives to an international

division creates several institutional and individual commitments. The cost of

investigation in an international division is generally lower, as knowledge has been

accumulated from previous investigations. Further, because of their role and

experience, the international executives perceive the risk of foreign operations to be

lower; they have more knowledge about remote control operations. With time, foreign

investments become a substantial part of total operations. The level of the international

division in the company’s hierarchy becomes much higher and the involvement of top

management increases. When evaluating the expansion of existing foreign operations

is considered, the investigation becomes much more favourable.

The location pattern also evolves and, very often, the first subsidiary selected for

foreign operations may change. The foreign subsidiary may have accumulated

considerable experience in foreign operations in its domestic location and in other

countries. This phenomenon can be attributed to the idea of experience first, where

companies may prefer to ‘get their feet wet in safer water’ (Aharoni, 1966). Thus,

because of path dependence, the history of the company is an important variable.

Aharoni studied US companies. A similar incremental process of learning and

experience, and the choice of familiar countries first, were found by Johanson and

Vahlne (1977) in their observations of Swedish companies. They concluded that

companies were inhibited by lack of knowledge about markets. Therefore, companies

proceeded in small steps, adjusting their actions as they gained knowledge through

experience. Thus, internationalisation is an evolutionary, continuous process from

22

export to joint venture representation, to sales subsidiary, to resource development

subsidiary. Further, based on experience and knowledge acquisition, companies

entered new markets with successively greater psychic distance. These explanations

were considered at the company level, rather than at the individual level. As stated by

the authors that in their model, they considered knowledge to be vested in the decision-

making system. They did not deal explicitly with the individual decision maker

(Johanson and Vahlne, 1977).

In subsequent works, Johanson and Vahlne (1990, 2009) expanded the notion of

knowledge development to include knowledge gained through relationships with other

bodies in the foreign market. They viewed markets as networks of relationships among

companies. They argued that the localisation process in relevant networks was

necessary for successful internationalisation. Relationships offered potential for

building trust and commitments, which, in turn, shaped a company’s market

knowledge.

Following the theoretical concepts described above (which take the approach that

companies customarily focus on domestic beginnings and then grow incrementally

towards internationalisation, thus becoming a MNC), researchers started to

conceptualise a new breed of companies called ‘born-global companies’ (Zhou et al.,

2007). Zhou (2007) defined born-global companies as young, small entrepreneurial

companies that, from the onset, are organised and structured such that a substantial

amount of their total revenues were drawn from multiple countries. Zhou argued that

this new global phenomenon was due to experienced entrepreneurs having established

international connections and networks, which enabled them to form companies or

joint ventures with international visions, worldwide acceptable innovative products and

23

a focus on international sales from their inception. Therefore, these born-global

companies could leapfrog the domestic growth route and launch into the international

arena from the outset (Oviatt and McDougall, 2005a, Oviatt and McDougall, 2005b).

The early research was mainly quantitative, examining the relationship between

internationalisation and performance based on comparative studies of MNCs. The

control approach was adopted to enable researchers to study the impact of different

levels of internationalisation on a company’s performance. However, as evidence was

mixed about the influence of internationalisation on performance, the later research

tended to become qualitative, and the earlier comparative and control approaches were

sidelined. As an alternative, case study approaches were used in an attempt to gain a

better and more in-depth understanding of internationalisation as a business strategy.

The next section of this literature review examines the research on the control approach;

that is, those studies that investigate the extent to which different degrees or levels of

internationalisation have affected companies’ performance. These studies are listed in

Table 2.1 and discussed below.

2.4. Multinationality and performance

There has been considerable research on the relationship between multinationality and

performance. As explained above, the term ‘multinationality’ is generally used to

describe the extent of a company’s foreign-based investments in overseas markets, and

the degree of internationalisation (DOI) usually refers to the geographical

diversification of the company. In the area of international finance, a significant

amount of research has examined the relationship between multinationality and

market-based measures of performance such as market capitalisation or stock market

24

returns (Errunza and Senbet, 1981, Errunza and Senbet, 1984, Doukas et al., 1999,

Morck and Yeung, 1991, Morck and Yeung, 1992). The studies are discussed below,

grouped by country or region.

2.4.1. World/USA studies

Studies based on an international sample or on US companies provide mixed evidence

about the relationship of internationality and performance. In a large cross-country

study, Buckley, Dunning and Pearce (1977) examined 387 of the world’s largest

industrial companies and compared their foreign subsidiary sales ratios to their

performance measures, ROA and sales growth for the period 1962 to 1972. The survey

contains both US and non-US companies. They concluded that there was a positive

relationship between degree of internationalisation and return on assets for the full

sample. However, when the sub-samples of US and non-US companies were tested

separately, there was no correlation found between internationalisation and return on

assets. They also found a positive relationship between internationalisation and sales

growth for the 1967 to 1972 period, but inconsistent outcomes on the direct

relationship between internationalisation and performance for the full 1962 to 1972

period.

Studies of US companies have reported no relationship of internationality and growth

or even a negative relationship. Severn and Laurence (1974) examined 62 US

manufacturing MNCs and compared their foreign asset ratios to the performance

measure of ROA. They concluded that there was no significant relationship between

profitability and internationalisation. Siddhartan and Lall (Siddharthan and Lall, 1982)

examined the 74 largest US manufacturing MNCs, compared their foreign sales ratio to

sales growth and concluded that there was a negative relationship between

25

internationalisation and growth. Chang and Thomas (1989) investigated 64 US

manufacturing companies, compared their growth in foreign sales ratio with their

growth in ROA and found a negative relationship between growth in internationality

and profitability.

2.4.2. European and other country studies

Studies in other countries have also reported mixed results. Kumar (1984) studied 672

UK manufacturing MNCs, comparing their foreign sales ratio to ROA, return on sales

(ROS) and sales growth. The study concluded that there was no significant relationship

between internationalisation and profitability or sales growth.

Grant (1987) studied 304 UK manufacturing companies by comparing the level of

sales to ROA and return on equity (ROE). He found a positive relationship between

multinationality and profitability. Geringer, Beamish and da Costa (1989), who

compared foreign sales ratio and ROA, also found a positive relationship.

Lu and Beamish (2001) studied 95 listed Japanese companies and compared the

number of foreign direct investments and number of host countries with the

performance measures, ROA and ROS. The authors concluded that there was a u-

shaped relationship between internationalisation and profitability, which meant that the

correlation was valid for the smallest and largest companies, but not for the mid-range

companies. The results were interpreted as follows: smaller companies can be more

focused and start from smaller bases, and thus can enjoy relatively significant benefits

from internationalisation. The largest companies can also derive benefit from

internationalisation owing to their resources and scale.

26

2.4.3. Singaporean studies

The preceding section demonstrates that there is already a very large body of research

examining the relationships between internationalisation and measures of corporations’

performance. However, a literature search indicated that not many studies have been

conducted on this subject for Singapore-based companies.

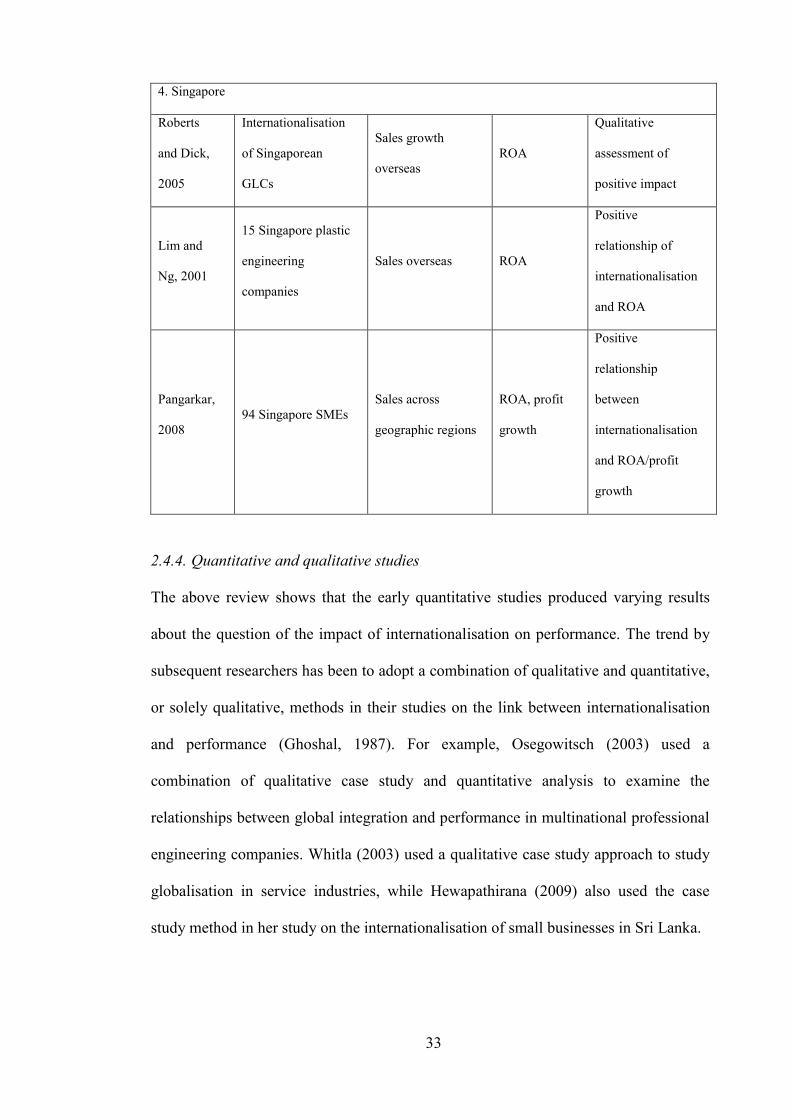

The first general pool of studies in Singapore focused on the competitiveness of

Singapore as a country (Blomqvist, 2002, Robert and Dick, 2005). They described how

Singapore’s economic policies have assisted companies to sustain international

competitiveness in the new internationalised world economy.

Zutshi and Gibbons (2004) commented that western management theories of

internationalisation do not fully explain the evolution of Asian MNCs, and they held

Singapore as a model of internationalised economic expansion. The authors studied the

internationalisation process and strategies of two GLCs.

Singaporean corporations have been strongly encouraged by the Singapore government

to regionalise their operations. Using Singapore’s public enterprise sector as a case

study, Roberts and Dick (2005) described the internationalisation strategies of

Singaporean GLCs. The authors concluded that effective systems of corporate controls

are necessary for the development of the international capabilities of Singapore GLCs.

Another study examined the success of Singaporean companies making investment

inroads into China as a form of international strategy. Kumar, Siddique and Wong

(2005) examined the internationalisation of ethnic Chinese business companies from

Singapore and delved into their strategies, processes and international competitive

advantages. Lim and Ng (2001) made a specific industry-level study on the factors

27

influencing the internationalisation decisions of small- and medium-sized enterprises

(SMEs) in Singapore, with particular reference to the plastic engineering industry.

Pangarkar (2008) examined the relationship between the internationalisation and

performance of SMEs in Singapore. He studied the relationship between the DOI and

performance of 94 SMEs in Singapore, using a DOI measure based on the dispersion

of sales across geographic regions. He found that DOI had a positive impact on the

performance (ROA and profit growth) of these companies. The analysis was conducted