Utdallas.edu /~ metin Page 1 Formulation Problems Outline u Whitt Window Company u Hotdogs and Buns...

20

utdalla s .ed u / ~ m e t i n P a g e 1 Formulation Problems Outline Whitt Window Company Hotdogs and Buns Portfolio Optimization No debt With debt Production Planning 1-period Forward: Setting Formulation Backward: Formulation Setting Production Planning Metalco Blends Alloys Fagersta Steelworks Backward: Incomplete Setting, Formulation Complete Setting

-

Upload

diane-paul -

Category

Documents

-

view

222 -

download

0

Transcript of Utdallas.edu /~ metin Page 1 Formulation Problems Outline u Whitt Window Company u Hotdogs and Buns...

utdallas.edu /~

metin

Page 1Formulation Problems

Outline Whitt Window Company Hotdogs and Buns Portfolio Optimization

No debt With debt

Production Planning 1-period Forward: Setting Formulation Backward: Formulation Setting

Production Planning Metalco Blends Alloys Fagersta Steelworks

Backward: Incomplete Setting, Formulation Complete Setting

utdallas.edu /~

metin

Page 2Whitt Window Company - Setting

utdallas.edu /~

metin

Page 3Whitt Window Company - Formulation

utdallas.edu /~

metin

Page 4Hotdogs and Buns - Setting

utdallas.edu /~

metin

Page 5Hotdogs and Buns - Formulation

utdallas.edu /~

metin

Page 6

Linear Programming formulations can be used to select a desirable bond portfolio.

ProMax has raised $8,000,000 to invest into four bonds. The average annual return, the worst-case annual return and the duration of each bond is below:

ProMax wants to maximize the expected return from its bond investments– The worst-case return of bond portfolio must be at least 9%. The average duration of a portfolio can be

computed as a weighted average, e.g., 3 million, 2.5 million and 2.5 million investments to bonds 1,2,3, yield average duration of

=2 years– To achieve diversification, at most 40% can be invested in a single bond.– The average duration of bond portfolio must be at least 2 years. The average duration of a portfolio can be

computed as a weighted average, e.g., 3 million, 2.5 million and 2.5 million investments to bonds 1,2,3, yield average duration of

=2 years Formulate a linear program to maximize the average annual return of a portfolio.

Average Return Worst-case Return Duration

Bond 1 14% 5% 2

Bond 2 9% 8% 1

Bond 3 12% 10% 3

Bond 4 15% 12% 3

Portfolio Optimization - Setting

utdallas.edu /~

metin

Page 7

Is there a missing constraint? How to make sure that the total money available for investing is 8,000,000?

1. Decision Variables: is the money invested in bond in million dollars

2. Objective function:

3. Constraints– The worst-case return of bond portfolio must be at least 9%.

– To achieve diversification, at most 40% can be invested in a single bond.

– The average duration of bond portfolio must be at least 2 years. The average duration of a portfolio can be computed as a weighted average, e.g., 3 million, 2.5 million and 2.5 million investments to bonds 1,2,3, yield average duration of

Portfolio Optimization - Formulation

utdallas.edu /~

metin

Page 8

Financial institutions use debt to increase their investment capital. ProMax has raised $8,000,000 from a private equity fund to invest into four bonds. The average annual return, the worst-case annual return and the duration of each bond is below:

ProMax wants to maximize the expected return from its bond investments– The worst-case return of bond portfolio must be at least 2%.– To achieve diversification, at most 35% can be invested in a single bond.– ProMax can borrow extra money to invest into bonds 1 & 2 and bonds 3 & 4

» High leverage: Bonds 1 & 2 have relatively high worst-case return. ProMax leverages its high worst-case return investments by a factor of 4. At least 20% (=1/(1+4)) of investments in high return investments must come from ProMax raised funds. The rest, at most 80%, can come from debt.

» Low leverage: Bonds 3 & 4 have relatively low worst-case return. ProMax leverages its low worst-case return investments by a factor of 1. At least 50% (=1/(1+1)) of investments in high return investments must come from ProMax raised funds. The rest, at most 50%, can come from debt.

» Borrowed money must be returned in a year with 1% interest

Formulate a linear program to maximize the average annual return of a portfolio over a year.

Average Return Worst-case Return Duration

Bond 1 7% 3% 1

Bond 2 5% 4% 1

Bond 3 10% 1% 1

Bond 4 12% -2% 1

Portfolio Optimization with Debt - Setting

utdallas.edu /~

metin

Page 9

1. Decision Variables: is the money invested in bond in million dollars is the money borrowed to invest in high worst-case return bonds is the money borrowed to invest in high worst-case return bonds

2. Objective function:

3. Constraints– The worst-case return of bond portfolio must be at least 2%.

– To achieve diversification, at most 35% can be invested in a single bond.

– Investment in bonds must be less than or equal to money available to invest

– Leverage constraints

and

Portfolio Optimization with Debt - Formulation

utdallas.edu /~

metin

Page 10Production Planning 1-period - Setting

Input and 1 hr: A

2As and 2 hrs: B

1B and 3 hrs: C Sell C at $100

Sell B at $60

Sell A at $15

A company produces products A, B, C Products A, B, C are sold at prices $15, $60 and $100 in unlimited numbers Products require the following

– A: Input material and 1 labor hour– B: 2 product As and 2 labor hours– C: 1 product B and 3 labor hours

A total of 60 labor hours are available Formulate a linear program to maximize profit

utdallas.edu /~

metin

Page 11

Let ix be the number of units produced corresponding to A, B, C;

Objective function: Max 15( BA xx 2 )+60( CB xx )+100 Cx

Constraints: CBA xxx 32 60

BA xx 2 0

CB xx 0

0ix , CBAi ,,

Production Planning 1-period - Formulation

utdallas.edu /~

metin

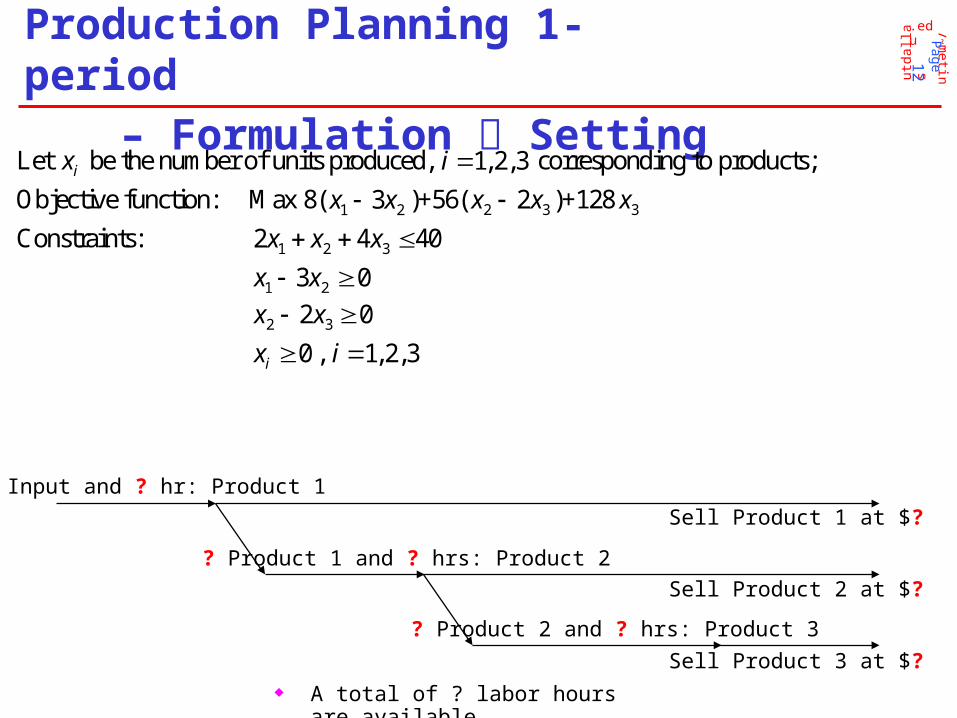

Page 12

Let ix be the number of units produced, 3,2,1i corresponding to products;

Objective function: Max 8( 21 3xx )+56( 32 2xx )+128 3x

Constraints: 321 42 xxx 40

21 3xx 0

32 2xx 0

0ix , 3,2,1i

Production Planning 1-period

– Formulation Setting

Input and ? hr: Product 1

? Product 1 and ? hrs: Product 2

? Product 2 and ? hrs: Product 3

Sell Product 3 at $?

Sell Product 2 at $?

Sell Product 1 at $?

A total of ? labor hours are available

utdallas.edu /~

metin

Page 13Production Planning - Setting

utdallas.edu /~

metin

Page 14

Let ix be the number of products produced in Month i , 4,3,2,1i ;

Let iy be the number of ending inventory produced in Month i , 4,3,2,1i ;

Objective function: Min 4321 7485 xxxx +2( 321 yyy )-6 4y

Constraints: 00 y

iiii dxyy 1 , 4,3,2,1i

0ix , 0iy , 4,3,2,1i

501 d , 652 d , 1003 d , 704 d

Production Planning - Formulation

utdallas.edu /~

metin

Page 15Metalco Blends Alloys - Setting

utdallas.edu /~

metin

Page 16Metalco Blends Alloys - Formulation

utdallas.edu /~

metin

Page 17Fagersta SteelworksIncomplete Setting, Formulation Complete Setting

A friend of yours is given a formulation problem and a diagram. The problem is as follows:

Your friend provides the formulation on the next page but loses the diagram. Using the information on the next page re-generate the diagram.

utdallas.edu /~

metin

Page 18Fagersta SteelworksFormulation

utdallas.edu /~

metin

Page 19Fagersta SteelworksComplete Setting: Diagram

M1

M2

S1

S2

P

Capacity

Capacity

Demand

utdallas.edu /~

metin

Page 20Summary

Whitt Window Company Hotdogs and Buns Portfolio Optimization

No debt With debt

Production Planning 1-period Forward: Setting Formulation Backward: Formulation Setting

Production Planning Metalco Blends Alloys Fagersta Steelworks

Backward: Incomplete Setting, Formulation Complete Setting