Using Refundable Tax Credits to Help Low- income...

42

Using Refundable Tax Credits to Help Low- income Taxpayers by Jon Forman Alfred P. Murrah Professor of Law University of Oklahoma Norman, Oklahoma & ATAX Fellow, UNSW University of Melbourne Melbourne, Australia August 16, 2011

Transcript of Using Refundable Tax Credits to Help Low- income...

Using Refundable Tax Credits to Help Low-income Taxpayers

by Jon FormanAlfred P. Murrah Professor of Law

University of OklahomaNorman, Oklahoma

& ATAX Fellow, UNSW

University of MelbourneMelbourne, Australia

August 16, 2011

2

Figure 1. Share of Household Income

0

10

20

30

40

50

60

Poorest 20% Middle 20% Richest 20%

Per

cent

Free market After taxes & transfers

U.S.: Share of Household Income & Gini Index, 2005

Market income Disposable incomeQuintilesLowest 1.50 4.42Second 7.26 9.86Middle 14.00 15.33Fourth 23.41 23.11Highest 53.83 47.28Gini Index 0.493 0.418

3

Rising Inequality

4

10.6 9.8 10.211.3 11.9

13.2 13.8 14.8 14.816.2

14.5 14.717.0

19.1

22.724.6

26.1 25.5

0

5

10

15

20

25

30

1970 1975 1980 1985 1990 1995 2000 2005 2009

Rat

io

Year

Figure 3. Ratio of Average Household Income of the Top 5 and 20 Percent of Households to the Average Household Income of the Bottom 20 Percent of Households, 1970-2009

Top 20%/bottom 20%Top 5%/bottom 20%

Source: U.S. Census Bureau, table IE-3, http://www.census.gov/hhes/www/income/data/historical/inequality/index.html.

Inequality and Redistribution

CountryGini

Before Gini

After

Poverty Before

(50% of median

income)

Poverty After

(50% of median

income)

Tax %

GDP

Social Spending

%GDP Australia 0.46 0.3 28.6 12.4 30.6 17.1Canada 0.44 0.32 23.1 12.0 33.3 16.5

Mexico n/a 0.47 21.0 18.4 20.6 7.0Sweden 0.43 0.23 26.7 5.3 49.1 29.4United Kingdom 0.46 0.34 26.3 8.3 37.1 21.3United States 0.46 0.38 26.3 17.1 28.0 15.9OECD 0.45 0.31 26.4 10.6 35.9 20.5

5

6

U.S. Average Annual Earnings of Full-time Workers, 2008

Doctors (Family & GP) $161,490Lawyers 124,750Economists 90,830Nurses (RN) 65,130Police 52,810Auto mechanics 38,967Secretaries 29,990Garbage collectors 37,540Orderlies 24,620Waiters and waitresses 19,580

7

Distribution of Earnings, 2004

$15,600 $26,000 $36,000$50,000

$84,000

$0

$100,000

$200,000

$300,000

$400,000

0 10 20 30 40 50 60 70 80 90 100

Percentile

Ear

ning

s

8

9

Figure 8. The Size Distribution of Wealth, 2004: Percentage Share of Wealth Held by...

34.324.6

12.3 13.4

84.7

11.33.8 0.2

01020

3040506070

8090

100

Top 1% Next 4% Next 5% Next10%

Top20%

2nd20%

3rd 20% Bottom40%

Perc

ent

10

Figure 10. Share of Household Income

0

10

20

30

40

50

60

Poorest20%

Middle 20% Richest20%

Per

cent

Egalitarian Free market After taxes & transfers Just?

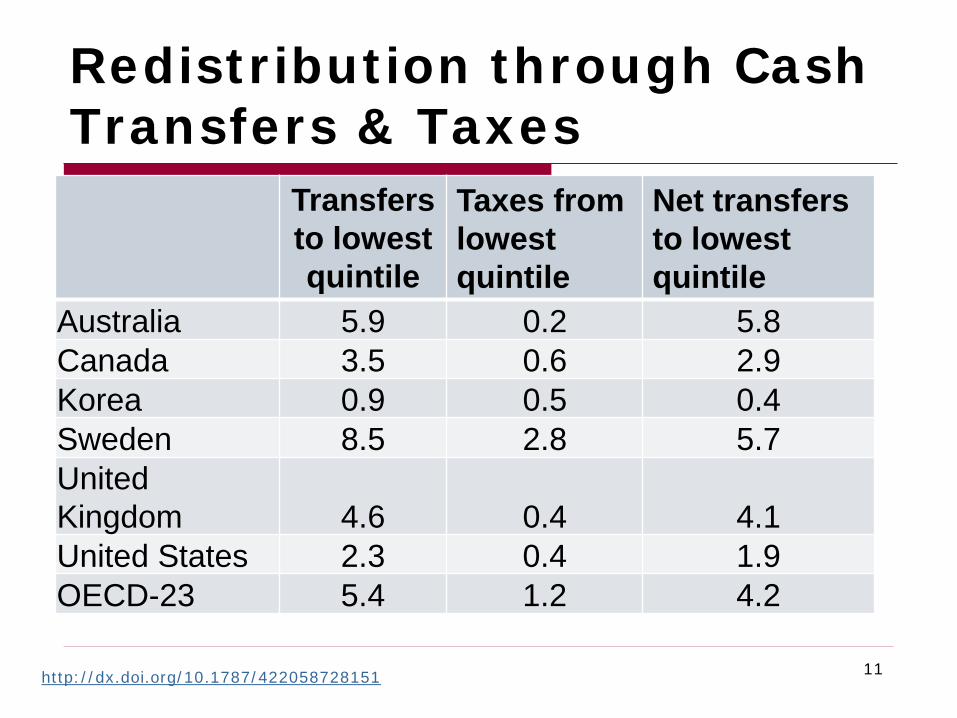

Redistribution through Cash Transfers & Taxes

Transfers to lowest quintile

Taxes from lowest quintile

Net transfers to lowest quintile

Australia 5.9 0.2 5.8Canada 3.5 0.6 2.9Korea 0.9 0.5 0.4Sweden 8.5 2.8 5.7United Kingdom 4.6 0.4 4.1United States 2.3 0.4 1.9OECD-23 5.4 1.2 4.2

11http://dx.doi.org/10.1787/422058728151

U.S. Standard Deductions, Personal Exemptions, and Simple Income Tax Thresholds, 2011

Unmarried individuals

Heads of household with one

child

Married couples filing joint returns

with two children

Standard deduction $5,800 $ 8,500 $11,600

Personal exemptions $3,700 $ 7,400 $14,800

Simple income tax threshold

$9,500 $15,900 $26,400

12Rev. Proc. 2011-12, 2011-2 IRB 297, http://www.irs.gov/pub/irs-irbs/irb11-02.pdf.

Tax Rate Schedules for Various Taxpayers, 2011

13

Tax rate Rate bracket

Unmarried individuals

Heads of household with one child

Married couples filing joint returns with two

children10 $0 to $8,500 $0 to $12,150 $0 to $17,00015 $8,500 to $34,500 $12,150 to $46,250 $17,000 to $69,00025 $34,500 to $83,600 $46,250 to $119,400 $69,000 to $139,35028 $83,600 to $174,400 $119,400 to $193,350 $139,350 to $212,30033 $174,400 to $379,150 $193,350 to $379,150 $212,300 to $379,15035 Over $379,150 Over $379,150 Over $379,150

Rev. Proc. 2011-12, 2011-2 IRB 297, http://www.irs.gov/pub/irs-irbs/irb11-02.pdf.

14Congressional Budget Office, Trends in Federal Tax Revenues and Rates (December 2, 2010), at 10, http://finance.senate.gov/imo/media/doc/120210DEtest.pdf.

15

Center on Budget and Policy Priorities, Top Ten Tax Charts (April 14, 2011), http://www.offthechartsblog.org/top-ten-tax-charts/.

1620 Facts About U.S. Inequality that Everyone Should Know, http://stanford.edu/group/scspi/cgi-bin/facts.php.

Productivity and Real Income

Rising Poverty

17U.S. Census Bureau, Income, Poverty, and Health Insurance Coverage in the United States: 2009, (Current Population Report No. P60-238, September 2010), http://www.census.gov.

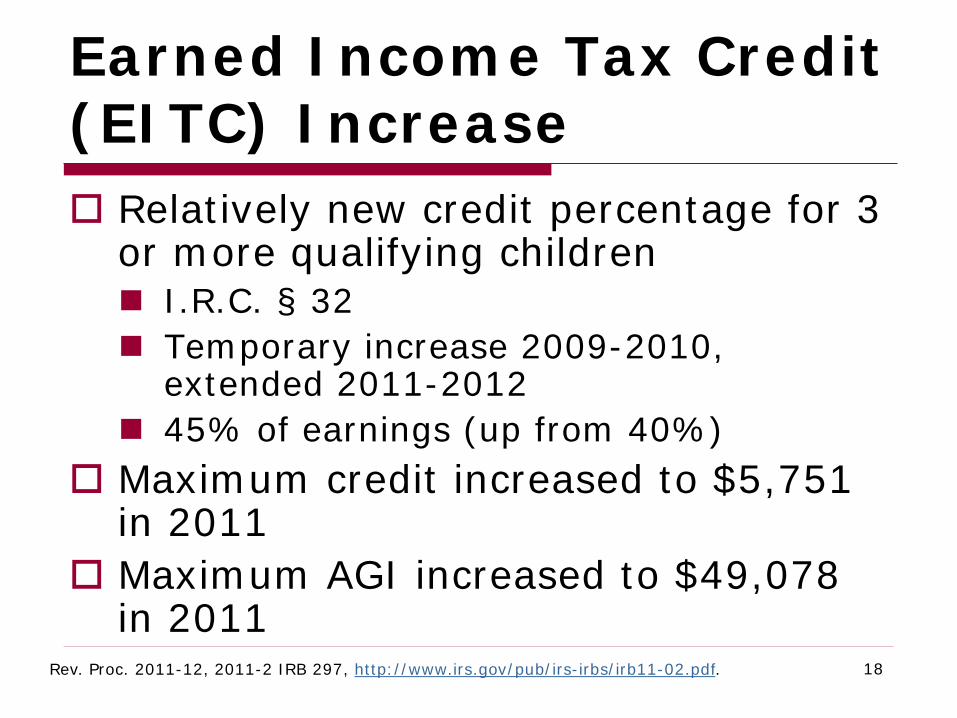

Earned Income Tax Credit (EITC) Increase Relatively new credit percentage for 3

or more qualifying children I.R.C. § 32 Temporary increase 2009-2010,

extended 2011-2012 45% of earnings (up from 40%)

Maximum credit increased to $5,751 in 2011

Maximum AGI increased to $49,078 in 2011

18Rev. Proc. 2011-12, 2011-2 IRB 297, http://www.irs.gov/pub/irs-irbs/irb11-02.pdf.

Child Tax Credit $1,000 per qualifying child I.R.C. § 24

Temporary expansion of eligibility for refundable credit (15% × earned income minus $3,000 threshold)

More lower income families qualify: 2008 – threshold amount was = $8,500 2009-2012 – threshold amount = $3,000

19

Poverty Levels & Net Federal Tax Thresholds, 2010

Unmarried individual

Single parent w/ 1

child

Married couple w/ 2 children

Married couple w/ 3 children

1. Poverty levels $10,830 $14,570 $22,050 $25,7902. Simple income tax threshold (before credits)

$9,350 $15,700 $26,000 $29,650

3. Income tax threshold after credits

$13,395 $32,380 $50,250 $60,567

4. Employee payroll tax threshold

$0 $0 $0 $0

5. Combined income & payroll tax threshold

$9,348 $25,717 $38,635 $43,788

20

Taxes at Poverty Level, 2010

21

Unmarried individual

Single parent w/

1 child

Married couple w/ 2 children

Married couple w/ 3 children

1. Poverty levels $10,830 $14,570 $22,050 $25,7902. Income tax at poverty level (after credits)

-$453 -$4,450 -$7,712 -$8,554

3. Employee Social Security & Medicare tax at poverty level

$829 $1,115 $1,687 $1,973

4. Combined income & payroll tax at poverty level

$376 -$3,335 -$6,025 -$6,581

5. Combined tax as a % of income at poverty level

3.5% -22.9% -27.3% -25.5%

22-$10,000

-$5,000

$0

$5,000

$10,000

$15,000

Tax

Liab

ility

Income

Net Federal Tax Liabilities for Selected Households, 2010

Unmarried Individual

Head of Household, 1 Child

Married Couple, 2 Children

Married Couple, 3 Children

23

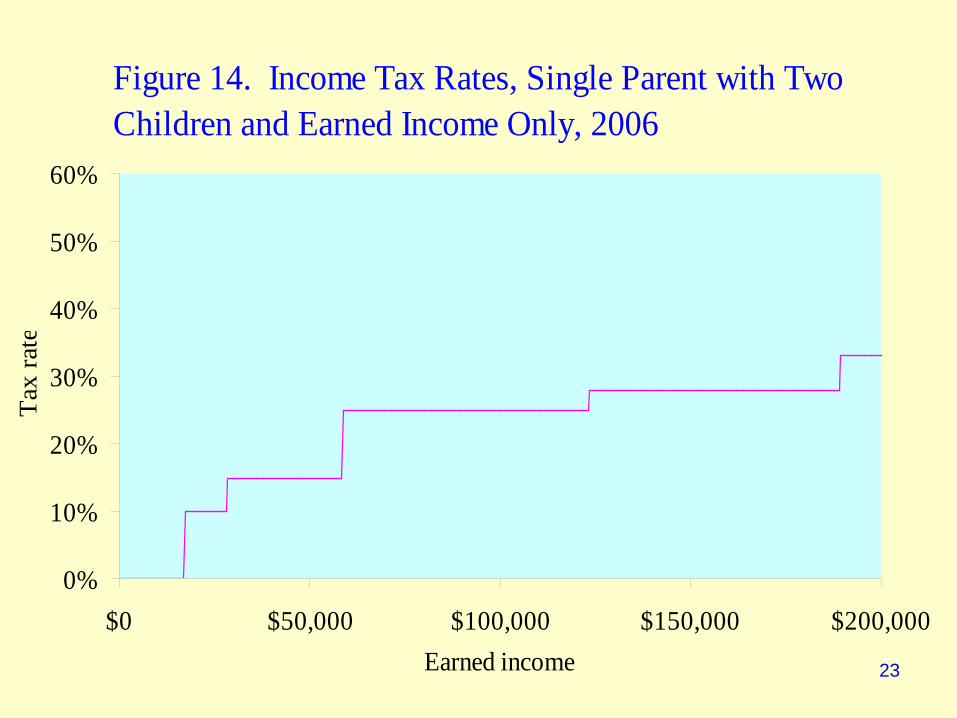

Figure 14. Income Tax Rates, Single Parent with Two Children and Earned Income Only, 2006

0%

10%

20%

30%

40%

50%

60%

$0 $50,000 $100,000 $150,000 $200,000Earned income

Tax

rate

24

Figure 15. Social Security Tax Rates on Earned Income, 2006

0%

10%

20%

30%

40%

50%

60%

$0 $50,000 $100,000 $150,000 $200,000Earned income

Tax

rate

25

Figure 17. Actual Tax Rate on Single Parents with Earned Income Only, 2006

-40%

-20%

0%

20%

40%

60%

$0 $50,000 $100,000 $150,000 $200,000

Earned income

Eff

ectiv

e ta

x ra

te

Effective tax rate Linear trend line

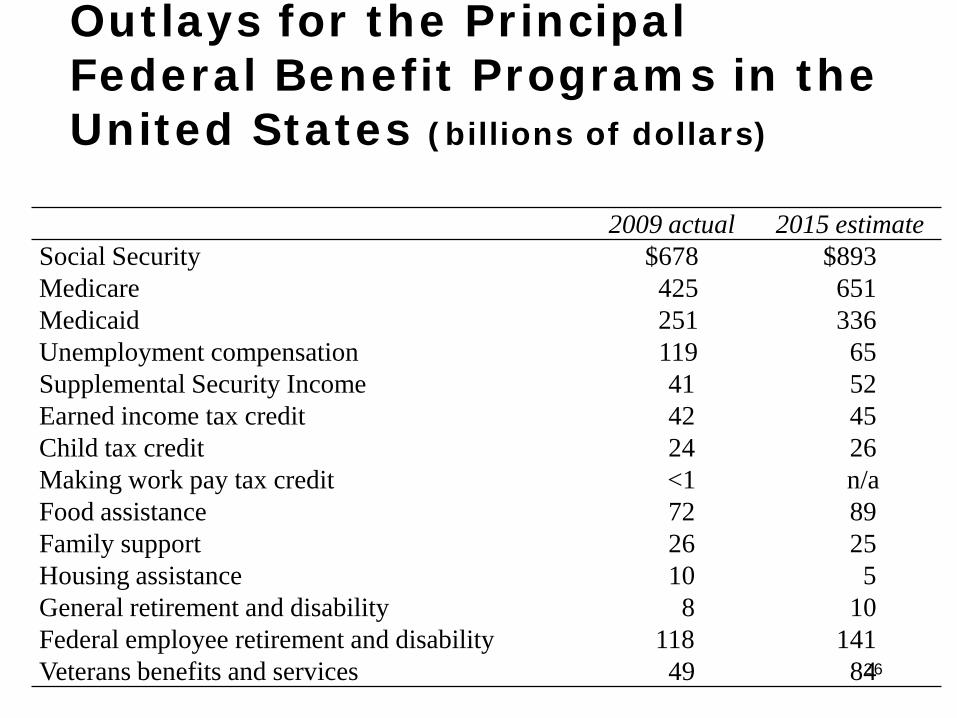

Outlays for the Principal Federal Benefit Programs in the United States (billions of dollars)

26

2009 actual 2015 estimateSocial Security $678 $893Medicare 425 651Medicaid 251 336Unemployment compensation 119 65Supplemental Security Income 41 52Earned income tax credit 42 45Child tax credit 24 26Making work pay tax credit <1 n/aFood assistance 72 89Family support 26 25Housing assistance 10 5General retirement and disability 8 10Federal employee retirement and disability 118 141Veterans benefits and services 49 84

27

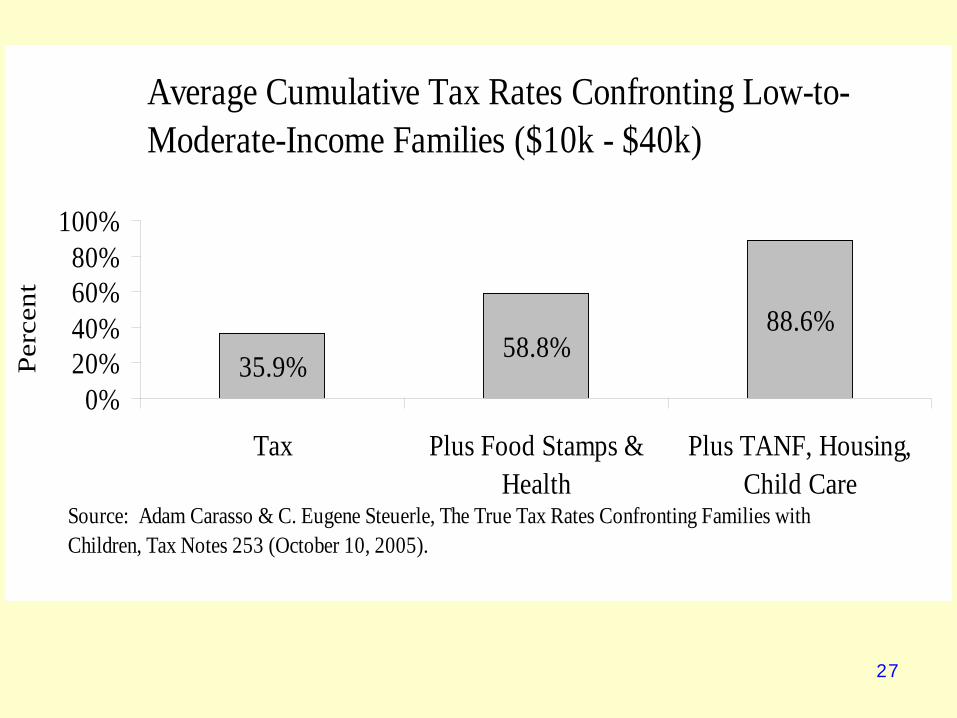

Average Cumulative Tax Rates Confronting Low-to-Moderate-Income Families ($10k - $40k)

35.9%58.8%

88.6%

0%20%40%60%80%

100%

Tax Plus Food Stamps &Health

Plus TANF, Housing,Child Care

Perc

ent

Source: Adam Carasso & C. Eugene Steuerle, The True Tax Rates Confronting Families with Children, Tax Notes 253 (October 10, 2005).

Canada 2010 Canada Child Tax Benefit (CCTB) C$112.33 for each child under age 18

National Child Benefit Supp. (NCBS) Up to C$174.00 per month

Child Disability Benefit (CDB) Up to C$205.83 per month

Universal Child Care Benefit (UCCB) C$1,200 per year for children under 6

28

Canada, cont. Working Income Tax Benefit (WITB) refundable tax credit of 25% of earned

income in excess of C$3,000 maximum of C$925 for individuals

(C$1,680 for single parents and couples) Refundable Goods and Services Tax

Credit C$250 for taxpayer, spouse or partner C$131 for each child

29

United Kingdom 2010 Child Benefit £20.30/week oldest child; £13.40 others

Child Tax Credit £545 per year/family+ £2,300/child

Working Tax Credit £1,920 per year per worker + 80% × child care, up to £140/week for

1 child; £240/week for 2+ children

30

Australia 2010 Family Tax Benefit Part A: up to A$4,905.60 child under 13;

A$6,161.20 child 13-15; etc. Part B: extra help for low-income single

parents & families with one main income Baby Bonus $5,294, paid in 13 fortnightly

installments Child Care Tax Rebate 50 percent of out-of-pocket child care 31

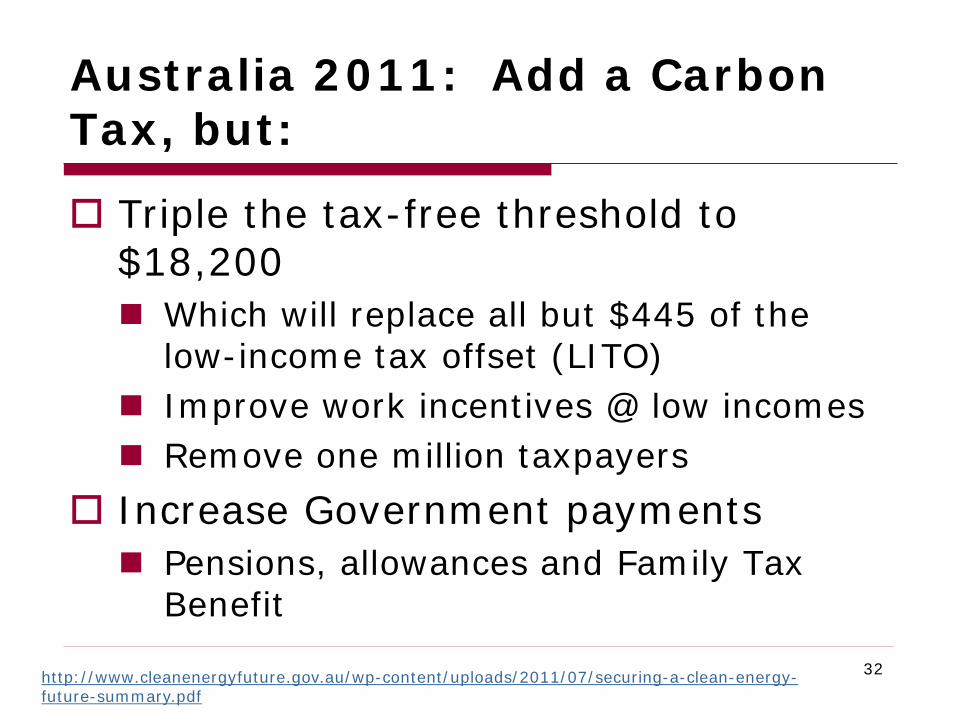

Australia 2011: Add a Carbon Tax, but:

Triple the tax-free threshold to $18,200 Which will replace all but $445 of the

low-income tax offset (LITO) Improve work incentives @ low incomes Remove one million taxpayers

Increase Government payments Pensions, allowances and Family Tax

Benefit32http://www.cleanenergyfuture.gov.au/wp-content/uploads/2011/07/securing-a-clean-energy-

future-summary.pdf

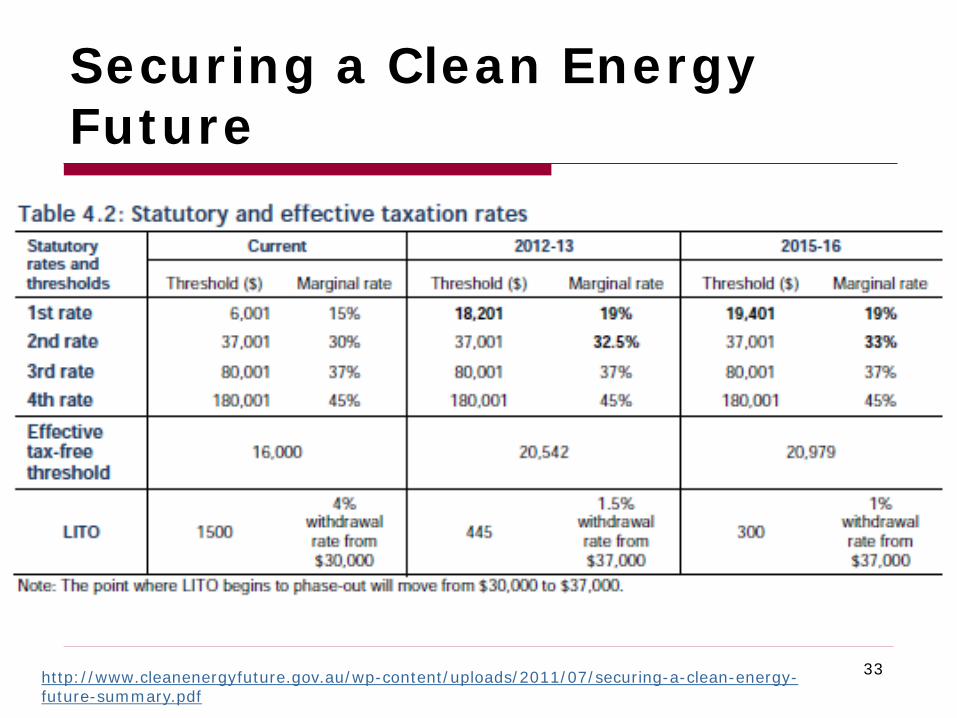

Securing a Clean Energy Future

33http://www.cleanenergyfuture.gov.au/wp-content/uploads/2011/07/securing-a-clean-energy-future-summary.pdf

34http://www.futuretax.gov.au/content/TaxForum/discussion_paper/tax_forum_next_steps_for_Australia_20110729.pdf

35

36

37

Figure 12. How a 30 Percent Payroll Tax Can Reduce Work Effort

$0

$5,000

$10,000

$15,000

$20,000

$25,000

05001,0001,5002,0002,500

Hours of work

Inco

me

afte

r ta

x

Income $10/hour

Income after tax

Utility curve 1

Utility curve 2

After: 1,750 hours, $12,500/year

Before: 2,000 hours, $20,000/year

38

Figure 21. How a Simple 50 Percent Earnings Subsidy Can Increase Work Effort

$0

$2,500

$5,000

$7,500

$10,000

$12,500

$15,000

$17,500

$20,000

05001,0001,5002,0002,500

Hours of work

Post

-tra

nsfe

r In

com

e

Income $5/hour

Income after transfer

Utility curve 1

Utility curve 2

After: 1,750 hours, $13,125/year

Before: 1,500 hours,$7,500/year

39

How an Integrated Tax & Transfer System Would Affect a Single Parent with 2 Children($2,000 Personal Tax Credits, $2,000 per Worker Credits, and 20 & 35% Tax Rates)

40

Pre-transfer earnings

Plus personal tax

credits

Plus worker credit

Less tax imposed

After-tax income

0 $6,000 0 0 $6,000$10,000 $6,000 $2,000 $2,000 $16,000$20,000 $6,000 $2,000 $4,000 $24,000$50,000 $6,000 $2,000 $10,000 $48,000

$100,000 $6,000 $2,000 $27,500 $80,500$200,000 $6,000 $2,000 $62,500 $145,500

41

How an Integrated Tax and Transfer System Would Affect a Single Parent with Two Children ($2,000 Universal Grants, $2,000 per Worker Credits, and 20 and 35 Percent Tax Rates)

$0

$25,000

$50,000

$75,000

$100,000

$0 $25,000 $50,000 $75,000 $100,000

Pre-transfer earnings

Post

-tax,

pos

t-tra

nsfe

r in

com

e

Pre-transfer earnings

Post-tax, post transferincome

About the Author Jonathan Barry Forman (“Jon”) is the Alfred P.

Murrah Professor of Law at the University of Oklahoma College of Law and the author of Making America Work(Washington, DC: Urban Institute Press, 2006).

Jon was the Professor in Residence at the Internal Revenue Service Office of Chief Counsel, Washington, DC, for the 2009-2010 academic year.

Jon can be reached at [email protected], +1-405-325-4779, www.law.ou.edu/faculty/forman.shtml.

42