Using credit is a way of life. People use credit online and for everyday purposes. Some do it so...

22

Financial Literacy: Credit

-

Upload

kevin-logan -

Category

Documents

-

view

213 -

download

0

Transcript of Using credit is a way of life. People use credit online and for everyday purposes. Some do it so...

Financial Literacy: Credit

Using credit is a way of life.

People use credit online and for everyday purposes. Some do it so they don’t have to carry cash. Some use it to buy things that they cannot afford to pay cash for.

Most common forms of credit: Credit cards installment loans

What is credit?

We use credit to pay for : Cars Clothing Tuition Books Groceries Homes

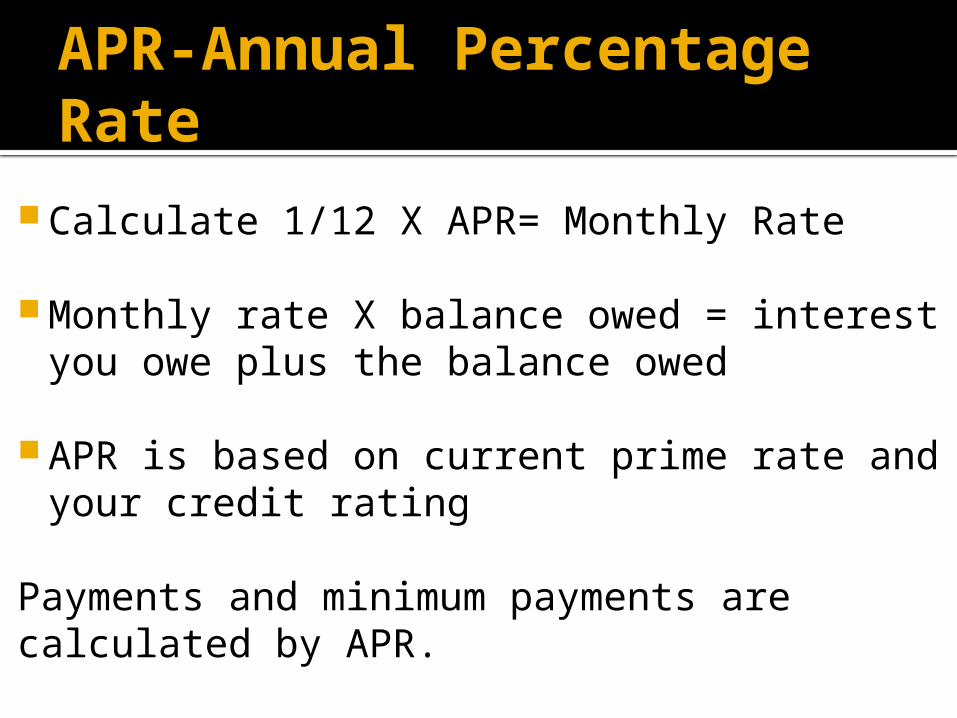

APR-Annual Percentage Rate

Calculate 1/12 X APR= Monthly Rate

Monthly rate X balance owed = interest you owe plus the balance owed

APR is based on current prime rate and your credit rating

Payments and minimum payments are calculated by APR.

Delinquency

Default –when you stop making payments

Banks and financial institutions have the right and ability to legally come after you for money owed.

Collection agencies must follow laws when contacting you but you must pay the amount that you owe

It is better to contact creditors if you foresee not being able to make your payments on time than to let a debt collector start contacting you. They will normally work out a payment plan for you to take care of debts.

Pros/Cons of credit

Pros Covers large costs or unforeseen expenses

Homes Cars

Flexibility Convenience

Cons Easy to get into debt

Higher costs due to interest $100 of groceries and only paying minimum could cost you double.

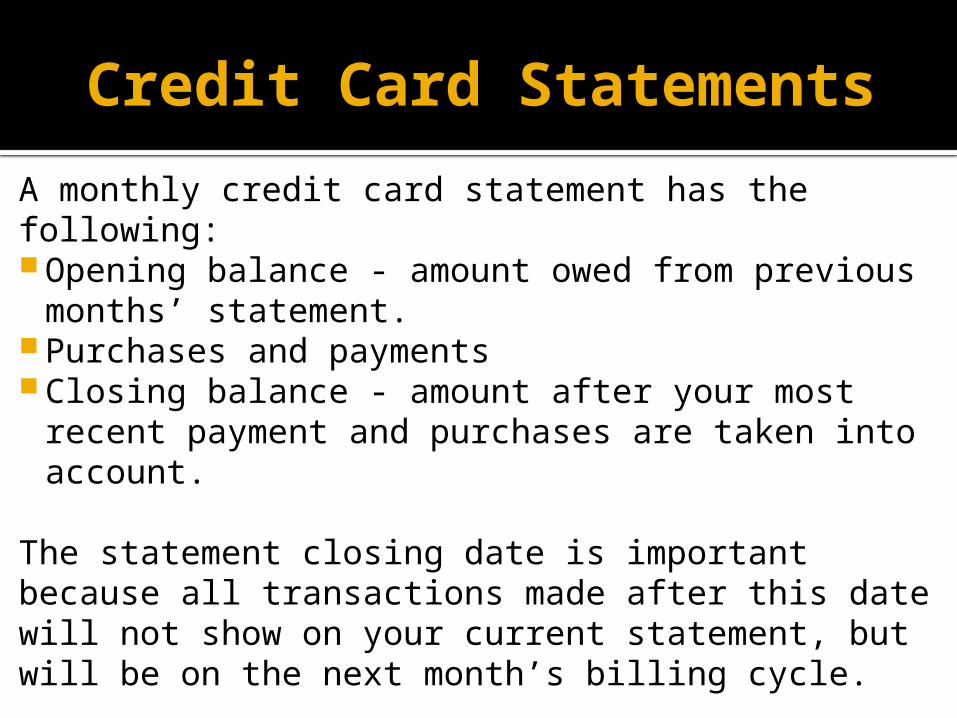

Credit Card Statements

A monthly credit card statement has the following: Opening balance - amount owed from previous

months’ statement. Purchases and payments Closing balance - amount after your most recent

payment and purchases are taken into account.

The statement closing date is important because all transactions made after this date will not show on your current statement, but will be on the next month’s billing cycle.

Charges and Purchases

Charges are all fees associated with your credit card, including the interest.

Purchases are transactions that you authorized to be put on your credit card account.

Credit limits and availability

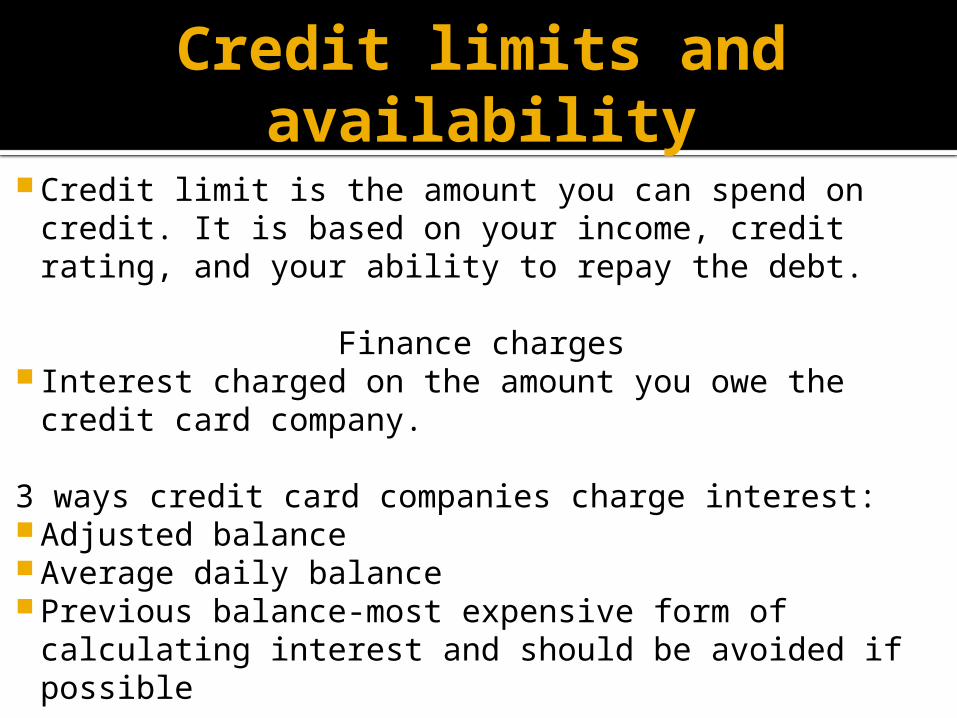

Credit limit is the amount you can spend on credit. It is based on your income, credit rating, and your ability to repay the debt.

Finance charges Interest charged on the amount you owe the credit

card company.

3 ways credit card companies charge interest: Adjusted balance Average daily balance Previous balance-most expensive form of calculating

interest and should be avoided if possible

Reconciling Your Account

Checking your account throughout the month, make it easier to reconcile your statement.

You can use a financial software program or simply match receipts to a paper statement.

It is important to match your receipts to your credit card statement to avoid fraudulent credit card activity.

The Cost of CreditBasic costs: Annual fees- Fees charged to carry the card. Half credit

card companies charge fees, they range from $50-$125

Finance charges – the amount of interest you are charged monthly. You are charged 1/12 of your APR on the balance you carry on your account each month. Companies make their money on interest; average is 17-21%.

APR = 12%/12 months = 1% monthly

Grace periods – Time between the billing statement and due date, usually 15 days. Costs nothing unless the credit card companies charges interest on purchases made during the grace period.

Other Fees

Late payment fees – Fees for payments due even 1 day late; fees average $29-$39. Paying your bills late will negatively impact your credit rating.

Over limit fees – fee charged for exceeding your credit limit; $29-$39 and is charged until you pay enough to reduce your balance below credit limit.

Cash advance fees – transaction fees of $6-$10 per transaction plus higher APR on cash advances.

Did you know?

The average consumer owes $15,100 in credit card debt with a rate of 17-21%.

What influences your rate? Credit History

Do you make payments as required? Do you make your payments on time? Do you go over your credit limits?▪ Credit rating is assigned to each consumer, the higher the

rating the better and the lower your interest rate will be.

Prime Rate

Minimize costs of credit/help you build credit

Keep Credit Limits Low.

Charge only what you can afford to pay off each month and paying off balance each month.

Do not exceed your credit limit.

Make your payments on time.

Protecting Yourself If you have an error on your statement, you

must notify your credit card company in writing within 60 days.

The credit card has 30 days to respond and up to 60 days to investigate the charges.

If you lose your credit card or it is stolen, immediately contact your credit card company so that the card can be canceled

The most you will be responsible for is $50 of any fraudulent charges.

Protecting Yourself

If you are no longer using a credit card. You should request in writing that the account be closed.

3 basic safety tips:1. Keep your PIN # in a safe location.2. Do not give your credit card to merchants that you are not familiar with.3. Shred all receipts after reconciling your statement.

Common/Don’t

Common debts: Student loans & Credit Cards

Common ways to get into Debt: Job loss Illness

Don’t:: Make purchases on credit you can’t

afford Live beyond your means

Consequences

Repossession Credit score drops Legal action-lawsuits and

garnishments Physical-due to stress Relationships- money problems are

leading causes to divorce

Get out of debt

Contact creditors and discuss ways to lower your debt-payment plans and lower rates.

Loan consolidation Bankruptcy

Loss of assets Harm to credit Not all debts are taken care of

Types of Loans Secured loans (collateral)

Automobiles Unsecured loans (signature) Lump sum (90-180 day loan) Installment loan Line of credit (revolving-similar to credit

card)

Components of a loan: Principle – amount borrowed Interest rate – fixed or adjustable Term – length of loan

The Loan Process

Lenders look at: Time at residence - stability Time on job Income Credit report- Other debts

When applying for a loan: Purpose of the loan Amount to borrow Why you want the loan How you will repay How much you can afford

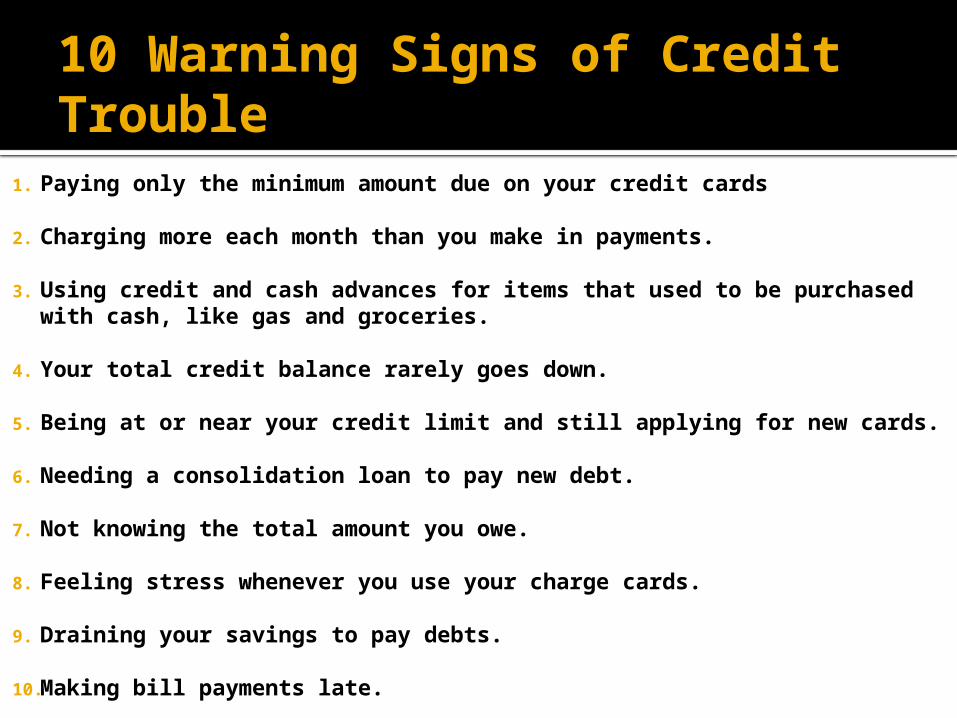

10 Warning Signs of Credit Trouble

1. Paying only the minimum amount due on your credit cards

2. Charging more each month than you make in payments.

3. Using credit and cash advances for items that used to be purchased with cash, like gas and groceries.

4. Your total credit balance rarely goes down.

5. Being at or near your credit limit and still applying for new cards.

6. Needing a consolidation loan to pay new debt.

7. Not knowing the total amount you owe.

8. Feeling stress whenever you use your charge cards.

9. Draining your savings to pay debts.

10. Making bill payments late.