User's Guide - Bank - Wolters Kluwer · Consumer Open-End Daily ... on your purchase of the ARTA...

241

Wolters Kluwer Financial Services ARTA ® Lending User's Guide - Bank

Transcript of User's Guide - Bank - Wolters Kluwer · Consumer Open-End Daily ... on your purchase of the ARTA...

Wolters Kluwer Financial Services

ARTA® Lending

User's Guide - Bank

This publication was written for ARTA Lending.

Publication Information / Version ARTA Lending User's Guide - Bank Last Edited: August 2016

Distributed Subject to Terms of a License or other Agreement

The contents of this publication, including its appendices, exhibits, and other attachments, as updated or revised, are highly confidential and proprietary to Wolters Kluwer Financial Services, Inc. or its subsidiaries or affiliates (“Wolters Kluwer Financial Services”). This publication is distributed pursuant to a Non-Disclosure Agreement, Evaluation Agreement, License Agreement and/or other similar agreement(s) with Wolters Kluwer Financial Services, Inc. or its subsidiary or affiliate. Unless otherwise specifically provided in such agreement(s), the reproduction of this publication is strictly prohibited. Use and distribution of this publication are also subject to the responsibilities and obligations of such agreement(s), which require confidential treatment of this publication and its contents.

Information in this guide is subject to change without notice and does not represent a commitment on the part of Wolters Kluwer Financial Services.

Do Not Reproduce or Transmit Unless otherwise specifically authorized in the agreement or license under which this publication has been provided, no part of this publication may be posted, played, transmitted, distributed, copied or reproduced in any form or by any means, electronic or mechanical, including photocopying, recording, or retaining on any information storage and retrieval system, without prior written permission from Wolters Kluwer Financial Services.

Requests for permission to reproduce content should be directed to Wolters Kluwer Financial Services, Inc., Corporate Legal Department, by telephone at 1-800-397-2341.

Not a Substitute for Legal Advice This publication is intended to provide accurate and authoritative information about the subject matter covered based upon information available at the time of publication. Examples given in this publication are for illustrative purposes only.

Development of this publication and the software (including forms, disclosures, reports, and other documents generated by the software) or other products that it describes was based on Wolters Kluwer Financial Services' understanding of various laws, regulations and commentaries. Wolters Kluwer Financial Services cannot and does not guarantee that its understanding is correct.

This publication is not intended, and should not be used, as a substitute for legal, accounting, or other professional advice. Wolters Kluwer Financial Services is not engaged in providing legal, accounting or other professional services. If legal or other professional assistance is required, you should seek the services of a competent professional. We encourage you to seek the advice of your own attorney concerning all legal issues involving the use of this publication and any products described in this publication. If your interpretations or your counsel’s interpretations are contrary to those expressed in this publication, you should of course, follow your/your counsel’s interpretations.

The following notice is required by law:

WOLTERS KLUWER FINANCIAL SERVICES’ PRODUCTS AND SERVICES ARE NOT A SUBSTITUTE FOR THE ADVICE OF AN ATTORNEY.

Warranty Disclaimer Except only for the warranties (if any) expressly set forth in the agreement(s) under which this publication is provided (i.e., your agreement or license for the described product), this publication is provided “as is”, and Wolters Kluwer Financial Services makes no warranty, express, implied, by description, by sample or otherwise, and in particular and without limitation, makes no implied warranties of merchantability or fitness for purpose. No modifications to this Warranty Disclaimer are authorized unless in writing and signed by the President or a Vice President of the Wolters Kluwer Financial Services entity licensing the product described in this publication.

Trademarks and Credits

ARTA is a registered trademark of Wolters Kluwer Financial Services, Incorporated.

All other trademarks are the property of their respective owners.

Copyright Information ©2016 Wolters Kluwer Financial Services, St. Cloud, Minnesota

This publication is the confidential information of Wolters Kluwer Financial Services. Distribution of this publication is subject to restrictions in the license or agreement under which this publication is provided to authorized Wolters Kluwer Financial Institution customers.

All rights reserved.

ii User's Guide - Bank ii

Table of Contents

Introducing ARTA Lending .............................................................................................. 1 What is ARTA Lending? ................................................................................................ 1 ARTA Lending Product Family ........................................................................................ 1

What’s in the modules? ............................................................................................ 2 What’s in the Components? ....................................................................................... 3

ARTA Lending Documentation Roadmap ........................................................................... 3 About This User’s Guide .............................................................................................. 4

Purpose ............................................................................................................... 4 Using This Guide .................................................................................................... 4 Understanding Conventions ....................................................................................... 5

Help! How to Get It .................................................................................................... 7 What’s This? Help ................................................................................................... 7

Getting Started ............................................................................................................ 9 Introduction ............................................................................................................. 9 Getting Acquainted with ARTA Lending ............................................................................ 9

To Start ARTA Lending ............................................................................................. 9 Logging into ARTA Lending ........................................................................................ 9

Navigating ............................................................................................................. 11 Using the Main Menu ............................................................................................. 11 Using the Transaction Menu ..................................................................................... 12 Using the Transaction Toolbar .................................................................................. 13

Entering Data ......................................................................................................... 14 Understanding Field Colors...................................................................................... 14 What about the Colors on the Navigator? .................................................................... 15 Special Characters ................................................................................................ 16 Date Formats ...................................................................................................... 16

Using ‘Save As’ in ARTA Lending .................................................................................. 17 Quitting the ARTA Lending Program .............................................................................. 18

Before Quitting .................................................................................................... 18 To Close and Quit ................................................................................................. 18

Starting Setup ........................................................................................................... 19 Introduction ........................................................................................................... 19 Tips for Setup ......................................................................................................... 19 General Setup ........................................................................................................ 20

Security Overview ................................................................................................ 20 Group Setup ........................................................................................................ 21 User Setup .......................................................................................................... 24

User's Guide - Bank iii

Lender Setup ...................................................................................................... 27 Lending Setup ........................................................................................................... 29

Introduction ........................................................................................................... 29 Policy Setup ........................................................................................................... 29

Tips for Creating a Policy Profile .............................................................................. 29 Setting Up a New Policy ......................................................................................... 29 Accrual Methods ................................................................................................... 31

Repayment Methods Setup ......................................................................................... 35 Initial Setup ........................................................................................................ 35

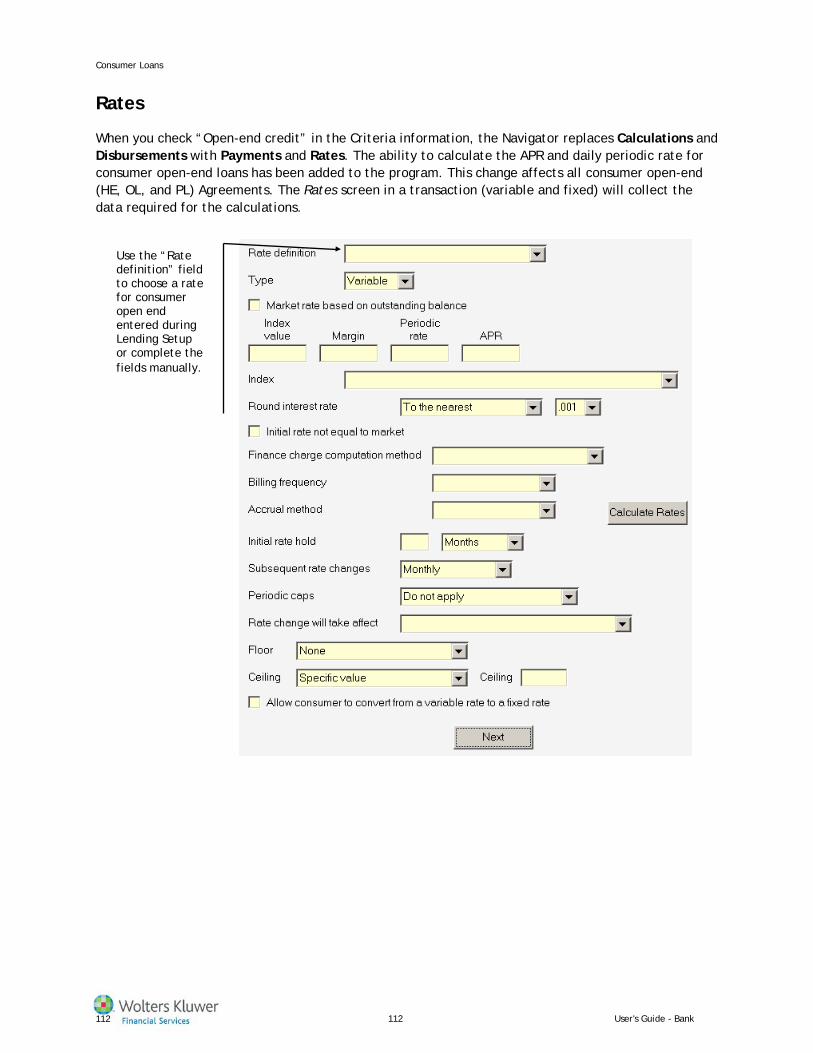

Rates Setup ........................................................................................................... 38 Initial Setup ........................................................................................................ 38 Consumer Open-End Daily Periodic Rate and APR Calculations .......................................... 40

Index History Setup .................................................................................................. 41 Creating a Custom Index ........................................................................................ 43 Deleting Indexes .................................................................................................. 44

Documents Setup ..................................................................................................... 44 Tips for Setting Up Your Documents ........................................................................... 45 Printing Blank Documents ....................................................................................... 45

Template and Report Setup .......................................................................................... 46 Templates ............................................................................................................. 46

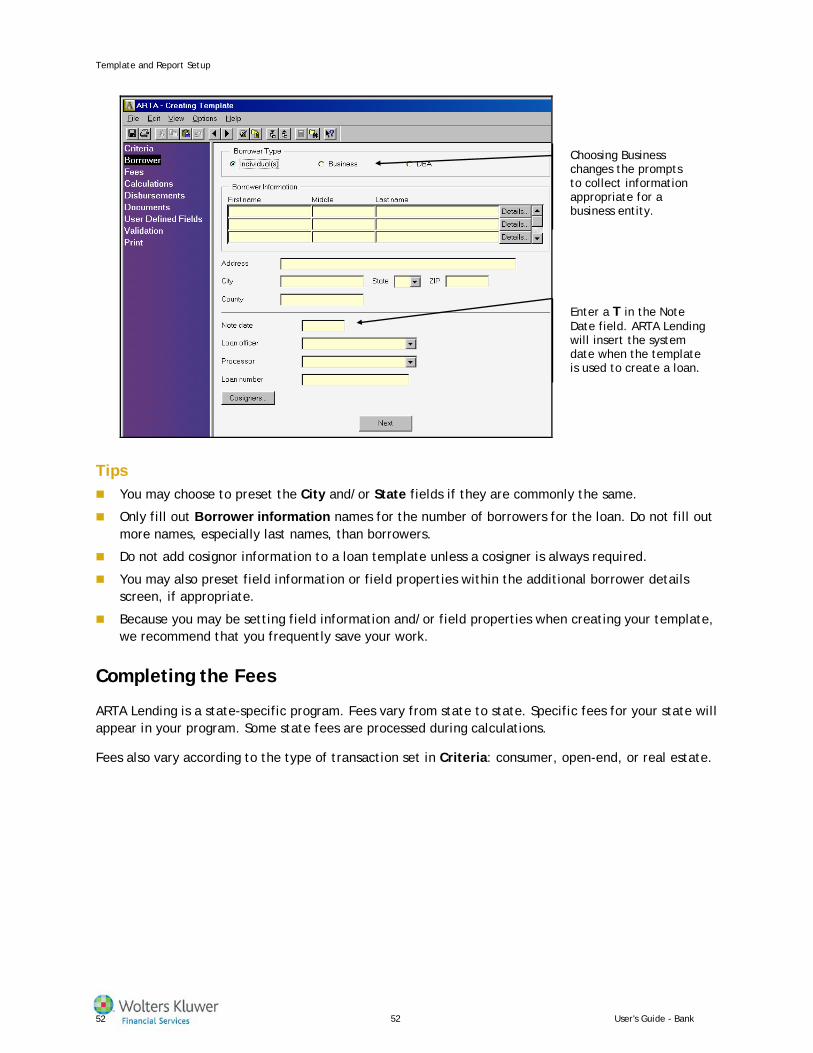

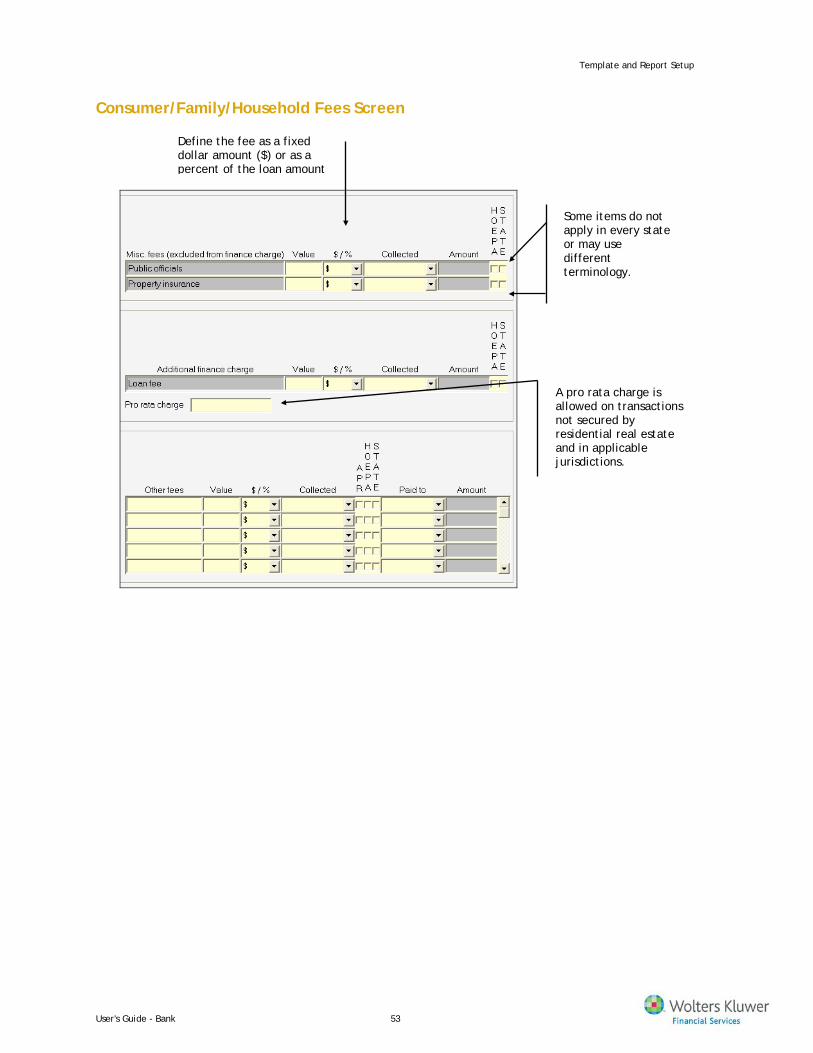

Considerations in Designing Templates ....................................................................... 46 Creating a New Template ....................................................................................... 47 Template Navigation ............................................................................................. 47 Printing Template Setup ......................................................................................... 50 Completing the Criteria Information .......................................................................... 50 Completing the Borrower Information ........................................................................ 51 Completing the Fees ............................................................................................. 52 Completing Documents .......................................................................................... 63 Template Setup Completion .................................................................................... 65 Template Maintenance .......................................................................................... 65

Reports ................................................................................................................. 65 Setting Up a New Report ........................................................................................ 66 Report Setup Criteria ............................................................................................ 66 Designing Reports ................................................................................................. 69

Insurance Setup ......................................................................................................... 70 Introduction ........................................................................................................... 70 Credit Life Insurance Setup ........................................................................................ 70

Credit Insurance Forms .......................................................................................... 70 Credit Insurance Setup Worksheets ............................................................................ 70 Adding New Credit Life Insurance ............................................................................. 71

iv User's Guide - Bank iv

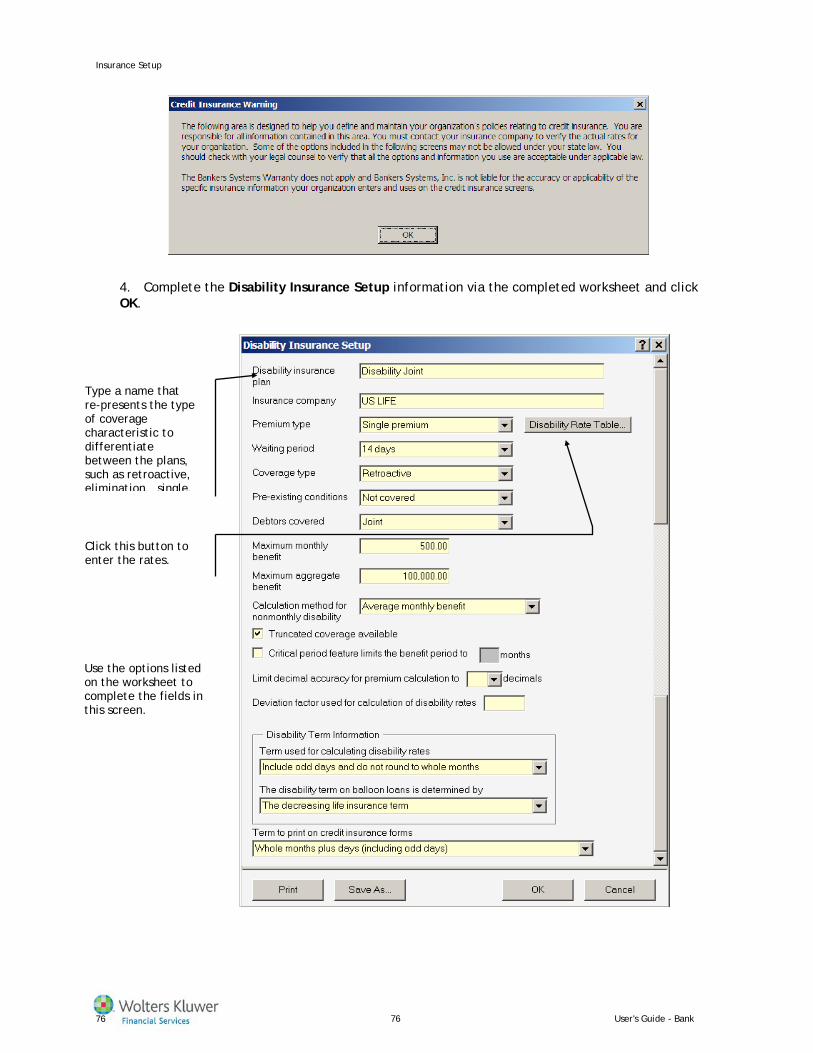

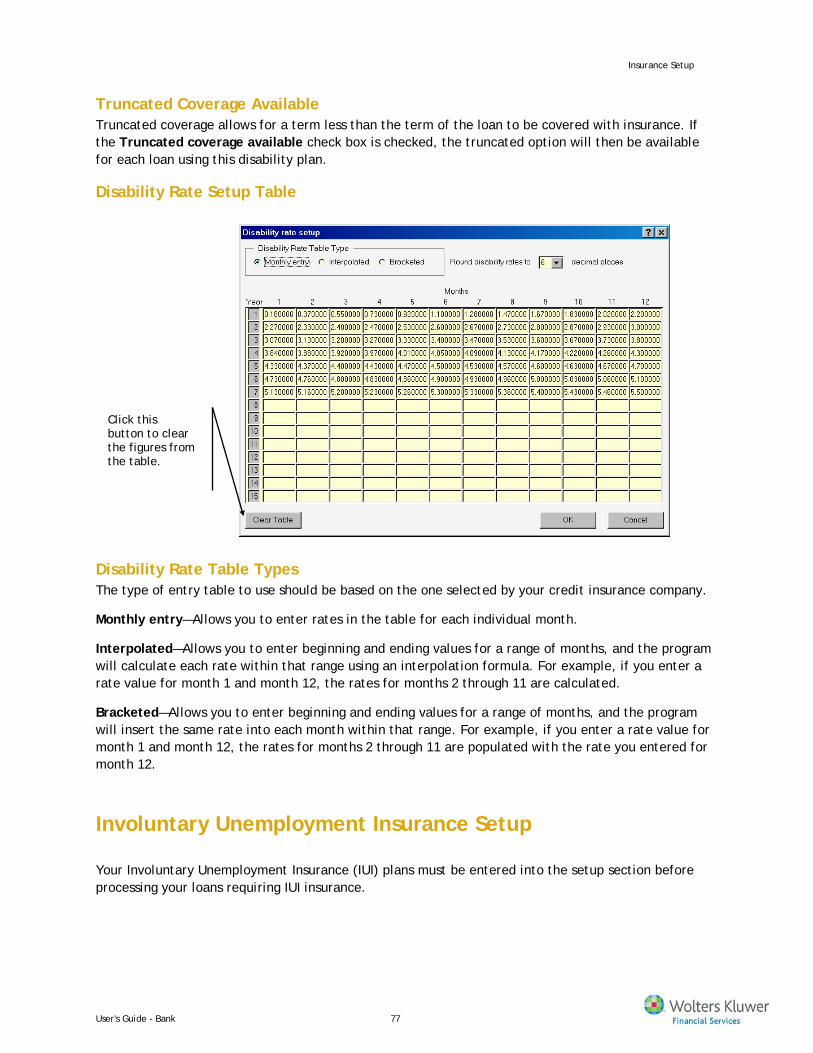

Disability Insurance Setup .......................................................................................... 75 Disability Insurance Forms ...................................................................................... 75 Adding a New Disability Insurance Plan ....................................................................... 75

Involuntary Unemployment Insurance Setup .................................................................... 77 IUI Forms ........................................................................................................... 78 Adding a New Involuntary Unemployment Insurance Plan ................................................. 78

Private Mortgage Insurance Setup ................................................................................ 80 Setting Up a PMI Plan ............................................................................................ 80 Transaction PMI ................................................................................................... 81

Data Exchange ........................................................................................................... 84 User-Defined Fields .................................................................................................. 84

Adding a New User-Defined Field .............................................................................. 84 Data Specifications .................................................................................................. 86

Creating a Data Specification ................................................................................... 87 Export Targets ........................................................................................................ 88

Setting Up the Export Target ................................................................................... 88 Exporting Data from a Transaction ............................................................................ 89

Import Sources ........................................................................................................ 90 Setting Up a New Import Source ............................................................................... 90

Import/Export Development Kit ................................................................................... 91 Consumer Loans ........................................................................................................ 92

Introduction ........................................................................................................... 92 Preparing for Consumer Open-End Loans ..................................................................... 92

Creating a New Consumer Loan ................................................................................... 93 Creating a New Loan ............................................................................................. 93 Transaction Navigator for Loans ............................................................................... 93

Criteria ................................................................................................................. 94 Borrower ............................................................................................................... 96 Fees..................................................................................................................... 99

Consumer Open-End Fees ...................................................................................... 101 Calculations .......................................................................................................... 101

Payment Frequencies ........................................................................................... 101 Basic Calculations ................................................................................................ 102 Preferred Rate Options ......................................................................................... 104 Credit Insurance Option ........................................................................................ 105 State-Specific Fee Processing.................................................................................. 106 Loan Calculations ................................................................................................ 107

Disbursements ....................................................................................................... 109 Payments .......................................................................................................... 110 Rates ............................................................................................................... 112

User's Guide - Bank v

Documents ........................................................................................................... 113 Documents List ................................................................................................... 113 Completing the Document Prompts .......................................................................... 115

Validation............................................................................................................. 115 Print ................................................................................................................... 116

Printing Your Loan Documents ................................................................................ 117 Commercial/Ag Loans .................................................................................................118

Introduction .......................................................................................................... 118 Templates ............................................................................................................ 118

Creating a New Loan ............................................................................................ 118 Criteria ................................................................................................................ 119 Borrower .............................................................................................................. 120 Fees.................................................................................................................... 122 Calculations .......................................................................................................... 123

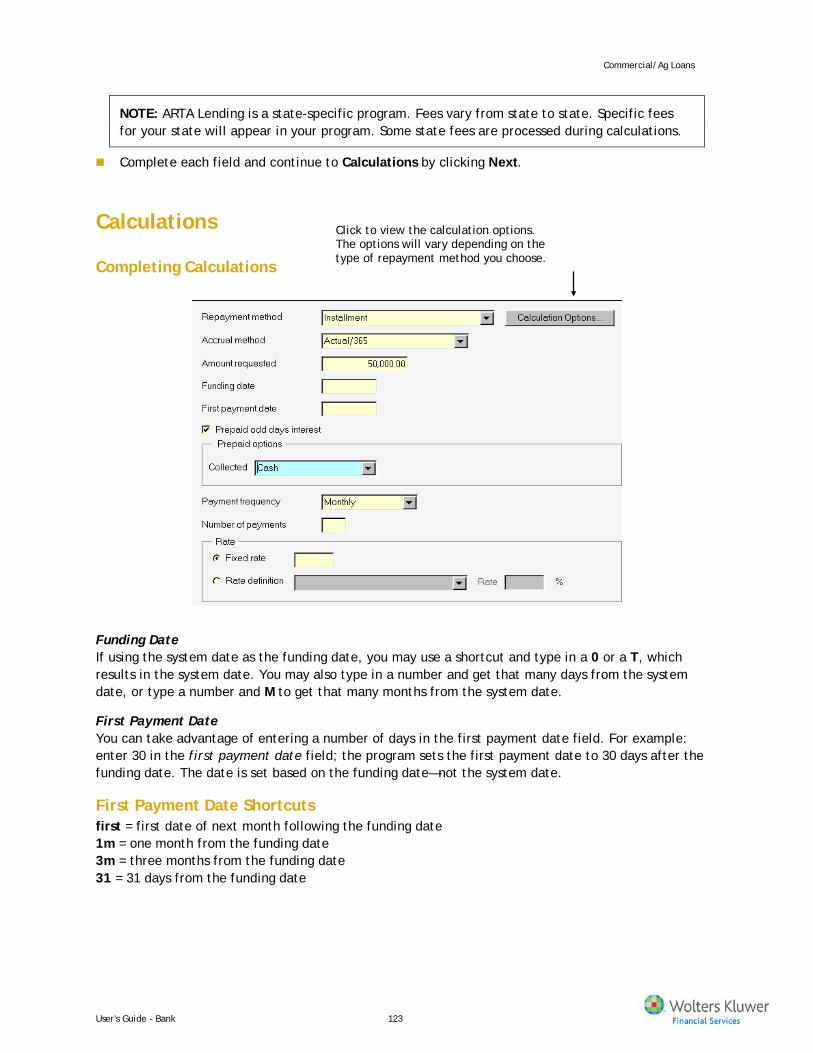

Repayment Methods ............................................................................................. 124 Calculation Options Button .................................................................................... 125 State-Specific Fee Processing.................................................................................. 125 Calculations Results ............................................................................................. 126

Disbursements ....................................................................................................... 127 Documents ........................................................................................................... 128 Validation............................................................................................................. 130 Print ................................................................................................................... 131

Residential Real Estate Loans .......................................................................................132 Introduction .......................................................................................................... 132

Flood Hazard Determination ................................................................................... 132 Templates ............................................................................................................ 132

Criteria ............................................................................................................ 133 Borrower ........................................................................................................... 134

Fees.................................................................................................................... 137 Calculations ....................................................................................................... 145 Disbursements .................................................................................................... 150 Documents ........................................................................................................ 151 Validation ......................................................................................................... 153 Print ................................................................................................................ 154

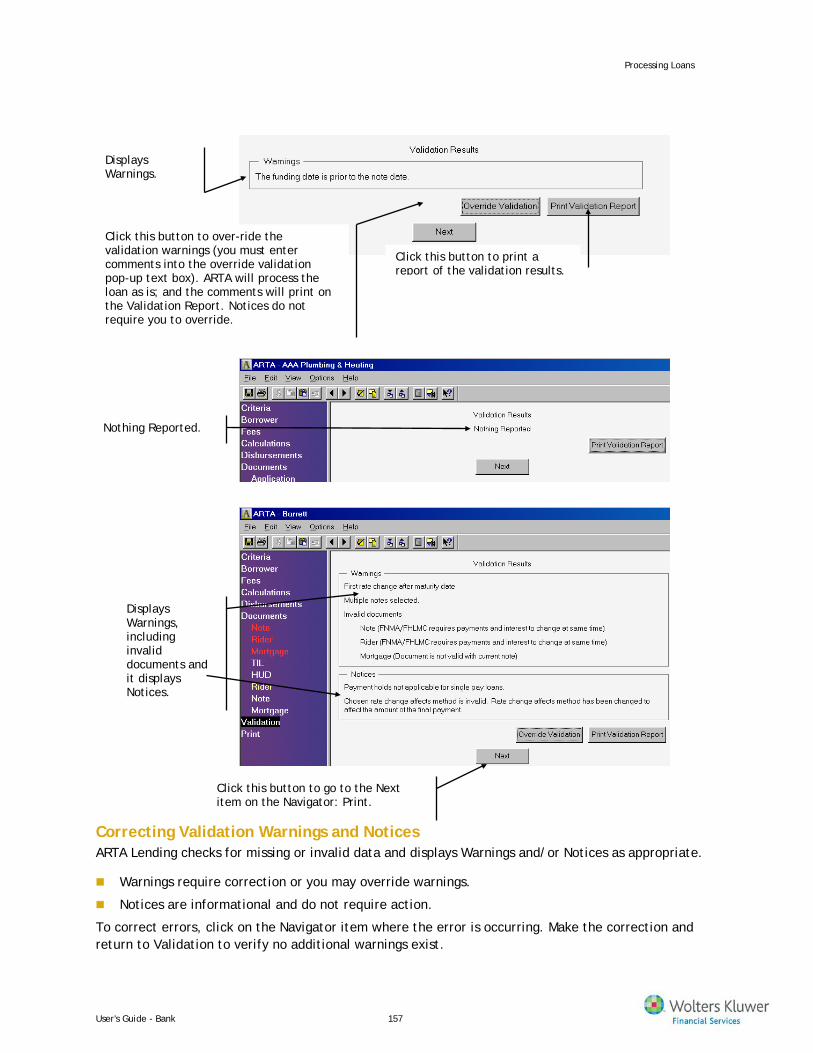

Processing Loans .......................................................................................................155 Introduction .......................................................................................................... 155 Recalling Loans ...................................................................................................... 155

Recalling a Loan .................................................................................................. 155 Searching for a Loan ............................................................................................ 156

Validation............................................................................................................. 156

vi User's Guide - Bank vi

Overriding Validation............................................................................................ 158 Print ................................................................................................................... 159 Using the Print Preview ............................................................................................ 159 Printing ............................................................................................................... 160 Denying a Loan Request............................................................................................ 162

ARM Early Disclosure..................................................................................................165 Introduction .......................................................................................................... 165

Key Features ...................................................................................................... 165 ARM Programs Supported ....................................................................................... 166

Creating an ARM Program.......................................................................................... 166 Product ............................................................................................................ 167 FNMA/FHLMC Documents ....................................................................................... 169 Non-FNMA/FHLMC Forms and Wolters Kluwer Financial Services’ Documents ........................ 173 Non-FNMA/FHLMC Forms and Non- Wolters Kluwer Financial Services Documents .................. 173 Negative Amortization .......................................................................................... 173 Payment ........................................................................................................... 174 Rate ................................................................................................................ 176 Validation ......................................................................................................... 177 Print ................................................................................................................ 179

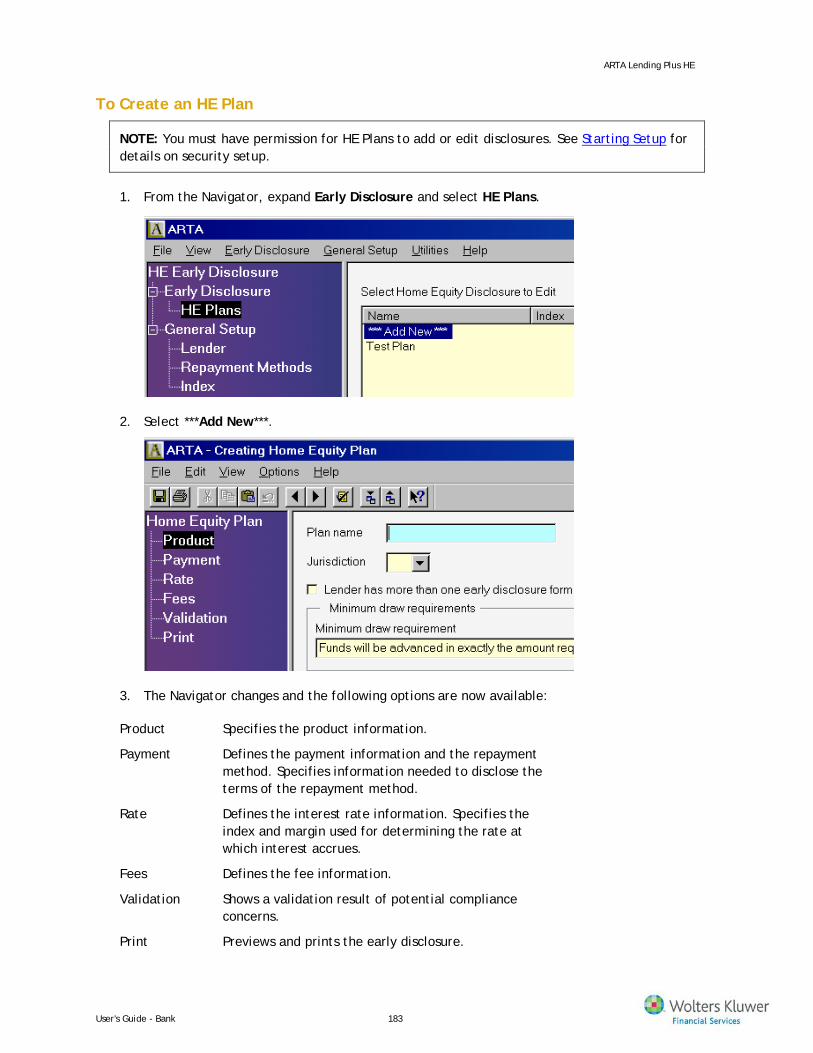

ARTA Lending Plus HE ................................................................................................181 Introduction .......................................................................................................... 181

Key Features ...................................................................................................... 181 Before Processing Your HE Plans ................................................................................. 182 Creating a Home Equity Plan ..................................................................................... 182

Product ............................................................................................................ 184 Payment ........................................................................................................... 184 Rate ................................................................................................................ 188 Fees ................................................................................................................ 191 Validation ......................................................................................................... 192 Print ................................................................................................................ 193

Using the Utilities .....................................................................................................195 Introduction .......................................................................................................... 195 Backup and Restore ................................................................................................. 195

Backup Guidelines ............................................................................................... 195 Backing Up Your Data Files ..................................................................................... 196 Restoring Your Data Files ....................................................................................... 197

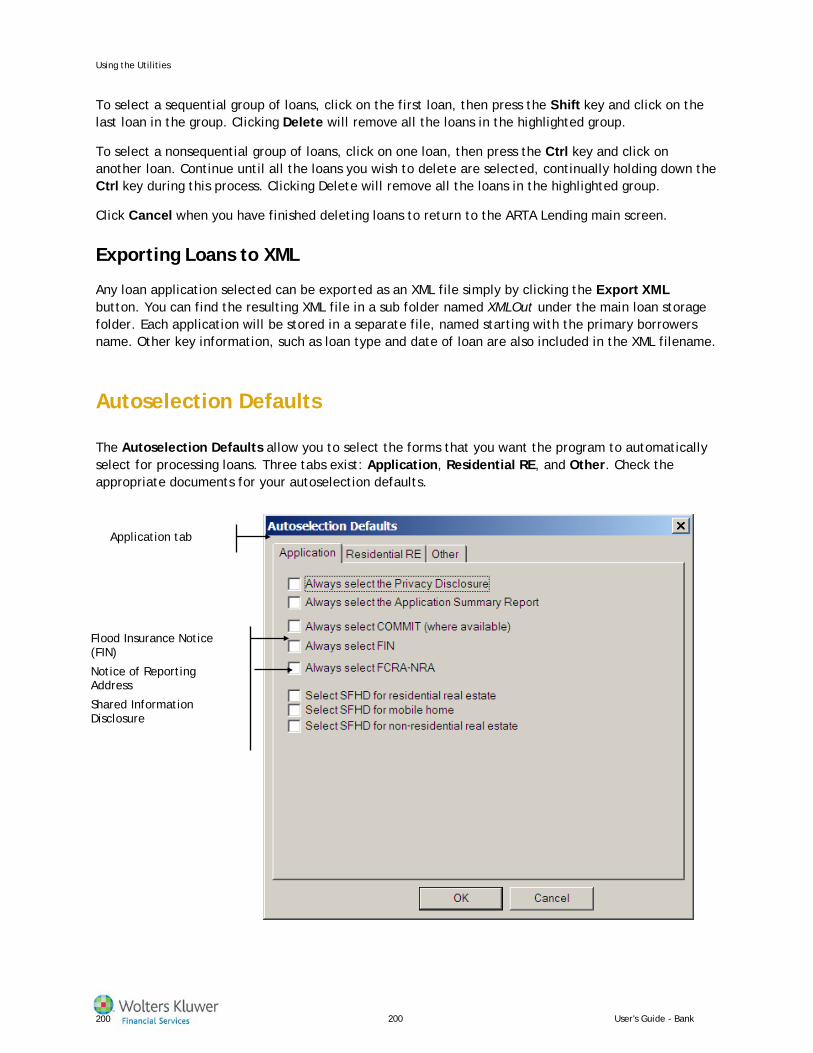

File Operations ...................................................................................................... 198 Searching for and Deleting Transaction Files ............................................................... 199 Exporting Loans to XML ......................................................................................... 200

Autoselection Defaults ............................................................................................. 200

User's Guide - Bank vii

Font Settings ......................................................................................................... 202 Client Directories ................................................................................................... 202

Changing Client Directories .................................................................................... 202 Customer Number ................................................................................................... 204 TRID Effective Date ................................................................................................. 204

Appendix A: Glossary .................................................................................................206 How to Contact Wolters Kluwer Financial Services Support .................................................231

Technical Support ................................................................................................... 231 Toll-Free SupportLine: 1-800-274-2711, ext. 1124021 ................................................... 231

viii User's Guide - Bank viii

Introducing ARTA Lending

What is ARTA Lending?

Congratulations on your purchase of the ARTA Lending Documentation System from Wolters Kluwer Financial Services.

ARTA Lending specializes in generating loan documents for routine and high-volume lending. It provides the practical features in a framework that’s sized to fit the business needs of financial institutions like yours.

The following topics are discussed in this chapter:

ARTA Lending Product Family

Documentation Roadmap

About This User’s Guide

Understanding Conventions

Help! How to Get It

End-to-End Solution The ARTA Lending product family is a collection of modules and components that work together and share common data and general services. This allows access to information in one central location. ARTA Lending offers various modules and components to provide an automated solution for the complete lending process from start to finish. Your lending processes move easily from application and credit checking to loan origination and loan closing.

ARTA Lending Product Family

The product family consists of the modules listed below. When installed, the modules become part of ARTA Lending—not as a separate program on your desktop.

ARTA Lending Configurations

ARTA Lending

ARTA Lending plus Home Equity

ARTA Lending for Credit Unions

ARTA ARM Early Disclosure

ARTA Home Equity Early Disclosure

ARTA ARM/HE Early Disclosure

User's Guide - Bank 1

Introducing ARTA Lending

Application Module Configurations

ARTA Lending and Application Module

ARTA Lending plus Home Equity and Application Module

ARTA Lending for Credit Unions and Application Module

Credit Bureau Access Module Configurations

ARTA Lending and Credit Bureau Access Module

ARTA Lending plus Home Equity and Credit Bureau Access Module

ARTA Lending for Credit Unions and Credit Bureau Access Module

ARTA Lending and Application/Credit Bureau Access Modules

ARTA Lending plus Home Equity and Application/Credit Bureau Access Modules

ARTA Lending for Credit Unions and Application /Credit Bureau Access Modules

Module Configurations

Application Module

Application/Credit Bureau Modules

ARM/HE plus Application Module

ARM/HE plus Application/Credit Bureau Modules

(For Credit Unions) Application Module

(For Credit Unions) Application/Credit Bureau Modules

(For Credit Unions) ARM/HE plus Application Module

(For Credit Unions) ARM/HE plus Application/Credit Bureau Modules

What’s in the modules?

The ARTA Lending modules are programs that work well together and have a similar interface.

Take a quick look at the ARTA Lending modules:

2 User's Guide - Bank 2

Introducing ARTA Lending

Application Module prints a credit application and related documents. You collect and incorporatethis information only once—up front. Once a loan decision is made, information can be passedalong for appropriate loan documentation.

Credit Bureau Access Module allows quick access to credit report and credit score information.Wolters Kluwer Financial Services has teamed up with Kroll Factual Data Corporation® as our creditreport provider. Credit report information is imported directly into ARTA Lending, making your loanorigination process more efficient.

ARTA Lending Plus HE supports open-end home equity lending. When installed, early disclosures,agreements, and other closing documents for consumer open-end home equity lending become partof ARTA Lending—not as a separate program on your desktop.

What’s in the Components?

ARTA Lending functionality is enhanced by the following components:

OneSumX Customer Due Diligence is a suite of integrated and component-based services includinga risk assessment module and an identity verification component with offerings to include OFACand FINCen lists, international data source, data retention, fraud databases, and more. All thesecombine to provide a risk-based approach to meeting the ID verification and record retentionrequirements of Section 326 of the USA PATRIOT Act.

Flood Determination Services allows you to order a flood determination for a real estate ormobile home transaction with a simple click of the Flood Determination Services icon in ARTALending. Via the Internet, Flood Determination Services collects the data needed to populate theStandard Flood Hazard Determination (SFHD) and Flood Insurance Notice (FIN).

Wiz Basic Home Mortgage Disclosure Act integration enables you to collect Home MortgageDisclosure Act (HMDA) reporting data for a single application or loan transaction, obtain geo-codeand rate spread information for a transaction, and edit check the Loan Application Register (LAR)data for a single transaction. In addition, batch functions on groups of transactions are alsosupported to collect or update the HMDA data.

Wiz Sentinel Home Ownership and Equity Protection Act provides a means for you to collect theappropriate information then determine the federal HOEPA status of a transaction and the HigherPriced Mortgage status when applicable. You may also, then, select appropriate federal disclosuredocuments for the transaction. Where state or local high-cost lending laws apply, ARTA Lendingalso provides a means to collect state/local data for a single application or loan transaction andobtain state/local determination for a transaction.

NOTE: State-specific high-cost lending documents are not supported by ARTA Lending. Only the determination is provided. You should consult with your legal counsel to determine the appropriate documents to provide based on the determination.

ARTA Lending Documentation Roadmap

Documentation for the ARTA Lending Documentation System includes:

User's Guide - Bank 3

Introducing ARTA Lending

The User’s Guide – Provides supporting information for using the ARTA Lending Documentation System.

The Release Notes – Contain:

― Late-breaking information about a new release

― Brief descriptions of the new features in the program

― Information on revisions to the program

― Technical notes

― The Release Notes are included with every software release. You can find them on the product CD in the Readme folder or on the Software Support web site at: http://support.wolterskluwerfs.com.

The Installation Instructions – Contain step-by-step instructions for installing ARTA Lending. To ensure a successful installation, follow the instructions carefully. The Installation Instructions are included with every software release in the Readme folder on the product CD and on the Software Support web site at: http://support.wolterskluwerfs.com.

Credit Insurance Setup Worksheets – These tools, included in your initial package, for credit life insurance and disability insurance allow you to get information from your insurance company. The requested information is needed to properly enter information in the Credit Life and Disability setup sections, which are used in calculating and disclosing credit insurance premiums.

ARTA Lending Sample Forms Book and ARTA Training Course Workbook – These are available through our training classes.

Module Guides – These can be found on the product CD or on our web site, one guide per module:

― Guide to ARTA Lending Application Module

― Guide to Credit Bureau Access Module

― Guide to Flood Certification Component

― Guide to HMDA Component

About This User’s Guide

Purpose

The purpose of the User’s Guide is to familiarize you with the power and flexibility of ARTA Lending. The User’s Guide is mostly a reference tool, though instructions on core tasks are provided.

NOTE: Wolters Kluwer Financial Services believes the information described in this guide is accurate and reliable. Much care has been taken in its preparation. However, Wolters Kluwer Financial Services accepts no responsibility, financial or otherwise, for any consequences arising out of the use of this guide. The information contained in this guide is subject to changes and revisions may be issued from time to time.

Using This Guide

This guide is intended for anyone involved in processing loans using ARTA Lending.

4 User's Guide - Bank 4

Introducing ARTA Lending

To use ARTA Lending and this guide effectively, you should be familiar with the Windows operating environment. You should know or learn Windows fundamentals before you begin working with ARTA Lending.

Due to the nature of the ARTA product family and the ability to purchase only those modules that you require, some buttons, views, or options may not be available to you that are presented in this guide. Generally, the options to which you should have access will be obvious in your program.

Organization of the User’s Guide The User’s Guide is organized to flow in a manner similar to how you might use ARTA Lending with loans.

Chapters 1 and 2 include conventions for using ARTA Lending, how to navigate, and use Help.

Chapters 3, 4, 5, and 6 discuss setup, including loan templates, security, policy, insurance, and other information required for lending.

Chapter 7 deals with importing and exporting of data, including the creation of user-defined fields.

Chapters 8, 9, and 10 deal with creating standard loans, including consumer, commercial, and real estate.

Chapter 11 deals with loan processing.

Chapters 12 and 13 deal with ARM and HE loans.

Chapter 14 discusses maintenance routines such as data backup.

Understanding Conventions

Certain conventions are used throughout the user guides. Familiarize yourself with these conventions before you begin working with ARTA Lending and using the guides.

Screen and Data Illustrations Certain data used in the documentation is fictitious, expressly and solely prepared for the purpose of concept or visual illustration associated with the appearance, maintenance, use, and operation of ARTA Lending. Any and all similarities to an actual financial institution or credit union data, or any other circumstances are purely coincidental.

Documentation Conventions

Action Description

Bold Bold typeface is used sporadically for emphasis throughout the text and consistently on words, specific file names, commands, and certain buttons that you must select.

Italics Italics are used for specialized terms and titles of other documentation and for emphasis in certain examples. Note that Flood Determination Services is always

User's Guide - Bank 5

Introducing ARTA Lending

partially italicized.

ALL CAPS Directory names, file names, and acronyms. However, when you type directory names and file names, you can use lowercase letters.

Mouse Conventions Use a single mouse click with ARTA Lending. The left mouse button is the primary mouse button, unless you have configured it otherwise.

Mouse Action Description

Point Position the pointer so it rests on the desired item on the screen.

Click Point to an item, press the left mouse button, and then immediately release the button without moving the mouse.

Double-click Point to an item, then quickly press and release the left mouse button two times.

Right-click Point to an item, press the right mouse button, and then immediately release the button without moving the mouse.

Keyboard Conventions The keys on your keyboard may be labeled differently than those described in this guide.

Keys Comments

Shortcut keys Use shortcut keys in combination or in sequence. For example, SHIFT+F3 means hold the SHIFT key while pressing the F3 key.

TAB, SHIFT+TAB,UP ARROW, DOWN ARROW, RIGHT ARROW, LEFT ARROW, HOME, END, PAGE UP, PAGE DOWN

Use these keys to navigate in the program.

Numeric keypad keys If your keyboard has a numeric keypad, press the Num Lock key to type numbers using the keypad.

6 User's Guide - Bank 6

Introducing ARTA Lending

File Extensions ARTA Lending uses some specialized file extensions for data and other uses.

File Extension Definition

!lk locked file

.ap application file

.bak backup file

.cb credit bureau file

.dat data file

.db setup file

.dbm template file

.ini initialization file that stores system-specific information about ARTA Lending

.ln loan file

Help! How to Get It

Regardless of your technical ability or experience with industry-related references, you may need help from time to time. With that in mind, we have developed several ways to make things easier for you.

Online Help or more specifically, What’s This? Help

User’s Guide, Module Guides, and the current Release Notes

Phone – Wolters Kluwer Financial Services Technical Support: 1-800-274-2711ARTA Lending Support, ext. 1124021

Web – http://support.wolterskluwerfs.com

NOTE: See the Technical Support page for detailed contact information

What’s This? Help

Context-sensitive Help, also known as What’s This? Help, contains a brief description of a specific field or item in a screen.

What’s This? Help button

User's Guide - Bank 7

Introducing ARTA Lending

To view What’s This? Help, click the ? button on a toolbar or the [?] button in the upper-right corner of some windows. Then, click the item you want information about. Another method is to click the mouse pointer on the item and press F1 on the keyboard. Shift+F1 also brings up the Help cursor.

TIP: To exit from What’s This? Help without making a selection, click the mouse button again or press Esc.

8 User's Guide - Bank 8

Getting Started

Getting Started

Introduction

The purpose of this chapter is to acquaint you with navigation in ARTA Lending and use of the toolbar and dialog boxes.

The following topics are discussed in this chapter:

Getting Acquainted with ARTA Lending

Navigating

Entering Data

Using ‘Save As’ in ARTA Lending

Quitting the ARTA Lending Program

Getting Acquainted with ARTA Lending

To Start ARTA Lending

Double-click the ARTA Lending icon on your desktop, or select the program through the Windows Start menu.

Logging into ARTA Lending

The first thing you will see is a request to logon to ARTA Lending. You must have a valid user ID and password to gain entry to ARTA Lending.

User's Guide - Bank 9

Getting Started

NOTE: When you open ARTA Lending for the very first time, the default User ID is Supervisor and the Password is password.

NOTE: If you cannot logon or do not see the Navigator items you need to complete tasks, contact your security administrator. Security setup for Groups and Users is discussed in detail in Starting Setup.

10 User's Guide - Bank 10

Getting Started

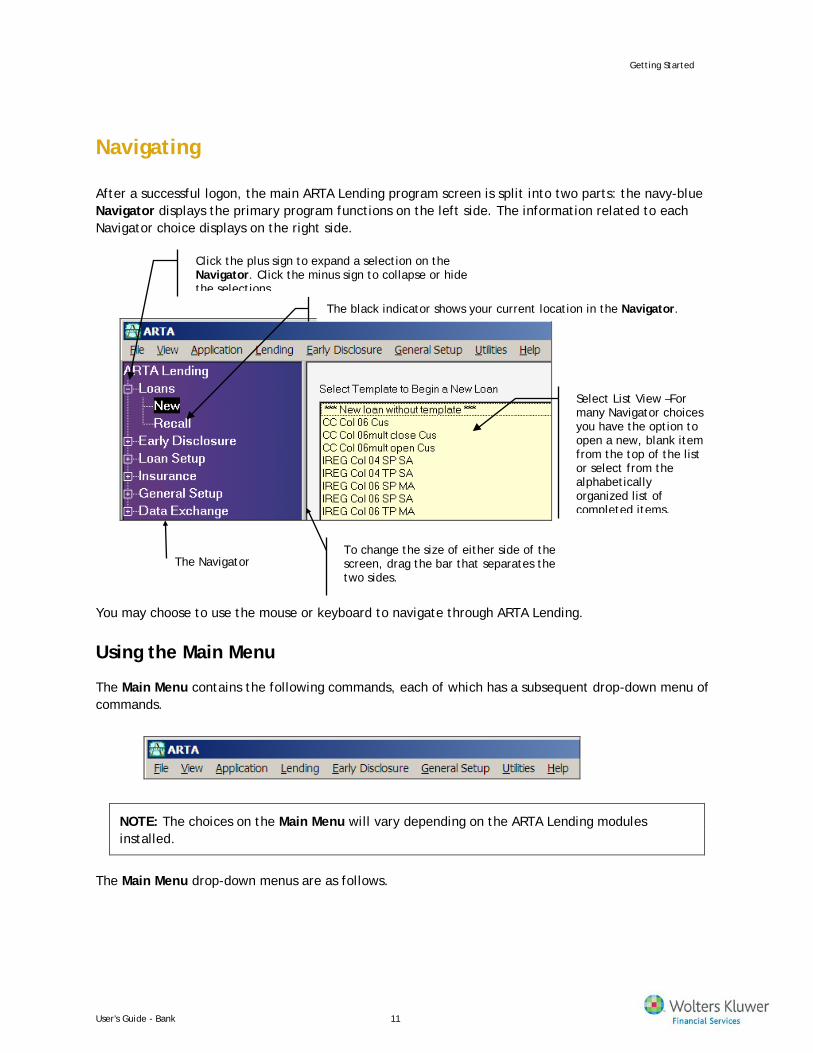

Navigating

After a successful logon, the main ARTA Lending program screen is split into two parts: the navy-blue Navigator displays the primary program functions on the left side. The information related to each Navigator choice displays on the right side.

You may choose to use the mouse or keyboard to navigate through ARTA Lending.

Using the Main Menu

The Main Menu contains the following commands, each of which has a subsequent drop-down menu of commands.

NOTE: The choices on the Main Menu will vary depending on the ARTA Lending modules installed.

The Main Menu drop-down menus are as follows.

To change the size of either side of the screen, drag the bar that separates the two sides.

The Navigator

Select List View –For many Navigator choices you have the option to open a new, blank item from the top of the list or select from the alphabetically organized list of completed items.

The black indicator shows your current location in the Navigator.

Click the plus sign to expand a selection on the Navigator. Click the minus sign to collapse or hide the selections.

User's Guide - Bank 11

Getting Started

Main Menu Name Drop-Down Menu Commands

File Client Printer Setup Exit

View Status Bar Refresh

Application New Recall Application Worklist Loan Decision Worklist

Lending New Recall Loans Worklist Setup Insurance

Early Disclosure ARM Programs HE Plans

General Setup Lender Group User Data Exchange

Utilities Backup and Restore File Operations Autoselection Defaults Font Settings

HMDA Reporting Client Directories Customer Number

Help What’s This? Shift+F1 About ARTA…

TIP: To open a menu from the keyboard, press Alt and type the underlined character of the menu. For example, press Alt, then G to display the General Setup menu, then press L for Lender.

Using the Transaction Menu

Whenever you are working in a loan or other transaction, the Transaction menu contains the following commands, each of which has a subsequent drop-down menu of commands.

12 User's Guide - Bank 12

Getting Started

The Transaction menu drop-down menus are described below.

Menu Name Drop-Down Menu Commands

File Save Ctrl+S Save As… Preview and Print… Ctrl+P Import Export Close Exit

Edit Undo Ctrl+Z Cut Ctrl+X Copy Ctrl+C Paste Ctrl+V

View Toolbar Status bar Parties Calculations Summary Amortization

Options Add Documents Validation

Help What’s This? Shift+F1 About ARTA…

Using the Transaction Toolbar

Whenever you are working in a loan or other transaction, the Transaction Toolbar is displayed below the Transaction menu. The Transaction Toolbar displays button icons that correspond to menu commands.

User's Guide - Bank 13

Getting Started

Toolbar Button Descriptions

Save

Preview and Print

Cut

Copy

Paste

Undo

Previous (Ctrl+PgUp)

Next (Ctrl+PgDwn)

Validation

Add Documents

Import data

Export data

Calculate Payments

Parties

HMDA

Flood Determination Services

Red Flag/ OneSumX Customer Due Diligence

HOEPA

What’s This? Help

Toolbar Tips The Parties button gives you quick access to all the parties to the loan information.

Click the Save button to quickly save your loans.

Clicking the Print and Preview button displays the Print option on the Navigator; you must select the Print All Selected Documents to print to the printer.

Clicking the Undo button will reverse changes made within a field before you leave that field.

TIP: If you forget what a toolbar icon represents, place the mouse pointer on the button for a few seconds—but do not click. This displays a pop-up screen with the name of the toolbar button’s command on it. The pop-up screen is called a “tool tip.”

Entering Data

Understanding Field Colors

As you enter information into data fields, you may notice that different colors display from field to field. ARTA Lending continually monitors data entry to ensure that the right type and value of data is entered into a field. Field colors are used by ARTA Lending to help ensure proper data entry and to help troubleshoot and correct data entry errors.

14 User's Guide - Bank 14

Getting Started

Field Color Reference

Field Colors Description

Blue

Designates your current field location.

Green

Indicates a required field; therefore, you must enter data into the field. If left blank, it will result in a validation warning.

Yellow

Indicates the normal data entry field. You can enter data, or leave the field blank if not applicable for your institution or for the given transaction.

Purple

Indicates a field is protected, but the value can be changed while processing a loan. If changed, it will result in a validation notice.

Gray

Indicates a protected field. The field is visible during loan processing, but you cannot enter, change, or erase data appearing in the field.

Red

Signals potential data entry errors. If left unchanged, it will result in a validation notice.

Dark Red

Indicates a change has been made to a protected (purple) field. It will result in a validation warning if not changed back to the preset value.

White on Black During template creation, this indicates a field has been set to invisible. You will not see these fields when processing a loan using the template.

NOTE: Some of the field colors listed above will only show when field attributes are set in a template. See Template and Report Setup for information on setting field attributes in a template.

What about the Colors on the Navigator?

Text in the left-hand transaction Navigator will sometimes change from white to a different color when displaying documents selected during a loan operation.

User's Guide - Bank 15

Getting Started

Navigator Color Description

Red Signals potential data entry errors. If left unchanged, it will result in a validation notice.

Yellow Indicates an autoselected document is no longer needed when changes were made after the autoselection took place.

Special Characters

Do not use special characters when typing into text boxes. Some of the special characters have special meaning to the program and cause errors when printing documents.

Special characters to avoid using include the following:

! @ # $ % ^ & *

( ) / | + = < >

Date Formats

ARTA Lending provides flexible date entry, allowing you to type a full date using four-year digits such as, 7/1/2005 for July 1, 2005, as well as a number of “shortcut” techniques for entering dates. A common shortcut technique is abbreviating the year to only two digits such as 7/1/05 or 7/05. Date fields in the program attempt to interpret information entered so dashes or date separators are not needed since the program automatically formats the date. When deciding whether a date should be forward-dated or backdated, the program assumes that a loan is entered on the same day that it is closed.

NOTE: Double-check the final date displayed if you used a shortcut to enter it.

Date Shortcuts Entering 3m will calculate a date 3 months into the future.

Entering the letter “t” will default to today’s date.

Entering the word “first” will default to the first of the next month.

If you type one, two, or three digits in a date field, the program interprets this as the number of days from today’s date. The program calculates the date you want as the system date (today’s date) plus the number of days (typed) into the future. For example, entering ‘30’ will display the date 30 days into the future.

16 User's Guide - Bank 16

Getting Started

When placing four to seven digits in a date field, the program will attempt to interpret the date. It is important to note that what the program interpreted may not match what you meant. To be sure that the correct date is entered, type a full 8-digit date (for example, 11/01/2005).

IMPORTANT: One exception to the above shortcuts is the “first payment date”' field found on the Calculations screen. The above rules still apply, but instead of calculating from today’s date, the field calculates from the date entered in the “funding date” field on the same screen. You are responsible for verifying that a date you enter is correct if you use a date shortcut and enter fewer than 8 digits.

Date Interpretations ARTA Lending further tries to assist you by determining a date, in some cases, from rules about various date fields. An example of this is the Related Documents section on the Line of Credit document. Document prompts request the date of the security agreement, mortgage, and guaranty. Because these documents would typically have been executed on the same day or before the current transaction, the program assumes that these dates will equal or precede the note date of the current transaction.

Another factor in date interpretation is the system date. The system date has a year beginning with the 20xx century indicator. If you type fewer than 8 digits to describe a “related document” date, the program assumes, since it is a prior date that a 19xx century is required. So, if today's date is 11/1/05 and you type 010105 as the date for a related document, the system interprets the shortcut date as 01/01/1905. In these situations, you must type full 8-digit date to get the date to print with the 20xx century indicator.

Using ‘Save As’ in ARTA Lending

When creating or editing information in many parts of ARTA Lending, a Save As button appears at the bottom of the screen. This functionality allows you to reuse information. For example, in Lender Setup, you can use the Save As button to save lender information under the name of a different branch. When you open the branch information, you only need to change information specific to the branch rather than re-enter everything.

To use Save As: 1. Open any previously saved information.

2. Edit as necessary to create a different profile.

3. Click Save As.

User's Guide - Bank 17

Getting Started

4. Enter a new name and click Save.

5. Click OK on the screen to finish.

Quitting the ARTA Lending Program

Before Quitting

Before you quit ARTA Lending, make sure all loans, templates, and setup files are saved and closed.

Save Your Files You can save loans at any time.

To save files, click the Save button on the toolbar.

Another way to save your files is to press the Ctrl+S shortcut.

IMPORTANT: Remember to save your work often!

To Close and Quit

Always exit ARTA Lending by clicking the close button [X] in the upper-right corner or by choosing the Exit option from the File menu.

IMPORTANT: Do not turn off or restart your computer while the program is running. Exiting the program in an irregular way can cause data corruption.

Type the name for the new item, in this case a lender, and click Save.

18 User's Guide - Bank 18

Starting Setup

Starting Setup

Introduction

Before processing transactions, you need to set up ARTA Lending for use at your institution. This chapter will step you through the following:

Tips for Setup

Lender Setup

Security Overview

Group Setup

User Setup

Adding information into the various setup sections will allow you to customize ARTA Lending to your daily uses, allowing your loan officers and customers to only work with information needed to complete transactions at your institution. Note that basic setup information applies to all modules and components in ARTA Lending.

Tips for Setup

Setup and Customization The setup areas are designed for setting, customizing, and maintaining your lending information for processing transactions with the appropriate loan documentation. This is where you define the default settings for your financial institution. In the setup areas, you enter data once and reuse it during application and loan transactions.

Some important notes before you begin setup:

ARTA Lending performs best if you enter as much information as you can in the setup areas. This will help increase the productivity of your ARTA Lending users.

Your ability to achieve your goals is based on your own needs and how well you can define them and then transfer them into the design of ARTA Lending.

It is your responsibility to verify that the setup information is accurate and correctly entered into the program and to review the setup after program updates.

Setup can be approached as a repeated process. If you make errors during setup, you can always go back and make changes.

Setup allows you to define default settings for your institution, which will eliminate repetitive data entry.

As you move through the setup screens, press the Tab key to move to the next field or Shift+Tab to move back a field. You may find this easier.

User's Guide - Bank 19

Starting Setup

NOTE: The purpose of the following setup information is to instruct you on the use of ARTA Lending and not to advise you on the guidelines, policies, procedures, or requirements of your institution. Do not alter your policies based on this information.

General Setup

In General Setup you can set up lender information and establish the security for your institution in ARTA Lending by setting up users and groups and assigning users to groups.

IMPORTANT: The setup items can be entered in any order you choose. However, at least one lender and one policy must be defined for ARTA Lending to select and print documents.

Entry into the setup sections of ARTA Lending is based on the user permissions established in Groups and Users. A user must have the proper permissions to access setup and change or enter information. Without proper permissions, setup choices do not appear on the Navigator menu.

NOTE: Carefully read the following sections in this chapter for more information on establishing permissions and security in ARTA Lending: Security Overview, Group Setup, and User Setup.

Security Overview

Each user who will do work on ARTA Lending must be assigned a user ID and password. This is specified in each user’s profile, accessed from the General Setup, User section of the Main Navigator.

In addition to a user ID and password, users need permission to work in various areas of the program. Permissions to use various modules, nodes, and menus in ARTA Lending are controlled by Groups. Even with a user ID and password for logon rights, a user will not be able to do work on ARTA Lending until they have been assigned to a group.

TIPS: A security administrator must create at least one group before a user can log on. These groups define the access rights of individual users that are assigned to the groups. The security administrator can create as many groups as needed to meet the security needs of their institution.

After groups are created, the security administrator updates each user profile to assign the user to a group, thus establishing the user’s permissions to the program, and to add a unique user ID and initial password for the user.

Once groups and users are set up, users will be able to log on and access those functions and areas to which they are authorized.

ARTA Lending will dynamically display only those functional areas to which a user has permissions. This means a loan processor might only see the Loans tasks if that is the only permission to the program.

20 User's Guide - Bank 20

Starting Setup

Someone who only uses the Application module would not see other Navigator commands. This can help make staff training easier.

Use of a Super-user ID A super-user ID is provided so that when ARTA Lending is installed, the security administrator can log on to the program to create one or more Security Groups, and to assign a User ID and initial password to each user.

IMPORTANT: Immediately after installing ARTA Lending, the security administrator can log on to ARTA Lending using the super-user ID, to setup security: The super-user ID is “supervisor” and the password is “password”.

We recommend using the super-user ID for initial security administration purposes only. The super-user ID does not have a profile; therefore it cannot be assigned to a group and will not have permission to some ARTA Lending functions.

After logging on with the super-user ID, we recommended that the security administrator, create a “security administration” group. This allows you to:

Specify a security administration group with all program permissions.

Administer security and user access without providing the initial super-user ID and password to other users.

After this group is created, and the security administrator or other users are assigned to this group, you should change the initial password for the super-user ID. This will help limit access to the program using the super-user ID.

Group Setup

Before any users can log on to ARTA Lending, security groups must be created by the security administrator.

To create security groups:

1. On the Main Navigator, select General Setup, Group.

Group Setup from the Main Navigator

User's Guide - Bank 21

Starting Setup

You can also access Group Setup by selecting Group from the General Setup menu, as shown below.

The Select Group to Edit screen appears.

22 User's Guide - Bank 22

Starting Setup

2. Click Add New to create a new group. The Group Setup screen appears.

NOTE: Permissions on the Group Setup screen may vary slightly depending on which ARTA Lending modules or components are installed.

3. Type a unique name for your security group in the Group name text box. The group name must be at least one character. Letters, numbers, spaces and other keyboard characters can be used.

4. Select the appropriate check boxes and corresponding options to give this group access to the program functions you want. Clear the check box to remove a permission.

5. When you have finished setting permissions, click OK to save your changes and return to the Select Group to Edit screen.

User's Guide - Bank 23

Starting Setup

Deleting a Security Group You cannot delete a group that has users assigned to it. To successfully delete a group, first reassign or remove all assigned users. Also, in order to delete a group, you must have permission to User Setup and Group Setup.

To delete a security group:

1. From the Select Group to Edit screen, right-click the group you want to delete.

2. Click the Delete command from the shortcut menu that appears.

3. In the confirmation message that appears, click Yes to verify you want to delete the selected group.

Group Setup Report The Group Setup Report shows the permissions given to the group, and lists the names and user IDs of users assigned to the group. You can view and print out a report of the group you are currently working with by clicking the Print Group Setup button at the bottom of the Group Setup screen. The Report Preview screen is displayed.

User Setup

After one or more Groups are defined, the security administrator can add users to each group as appropriate. If you created your user profiles before creating groups, you will need to assign each user to a group before a user can access any features in ARTA Lending.

TIP: When creating the user IDs and passwords, we recommend that the security administrator set all user passwords to an initial generic password. Each user should be instructed to change their password upon their first logon.

24 User's Guide - Bank 24

Starting Setup

To create or edit Users:

1. On the Main Navigator, select General Setup, User.

User Setup from the Main Navigator

User's Guide - Bank 25

Starting Setup

2. Click Add New to create a new user, or click a user name to edit an existing user’s information. The User Setup screen appears.

3. Enter the appropriate information in the fields and click OK to save your changes.

NOTE: You must at least fill in the Full Name, User ID, Group and Password for each user.

Observe the following rules for User ID:

The ID must be between 1 and 35 alpha or numeric characters.

Spaces are allowed.

No special characters are allowed.

Observe the following rules for passwords:

The password must be between 8 and 35 alpha or numeric characters.

No special characters are allowed.

Spaces are allowed.

Asterisks appear for each keyed character.

26 User's Guide - Bank 26

Starting Setup

Passwords are case-sensitive.

NOTE: If a user forgets the password, the administrator will need to reset it in User Setup.

Lender Setup

Lender information is needed to print in the “lender” section of the documents and must be set up to autoselect and print your loan documentation. It also gives you more options for printing your reports.

NOTE: You will need to belong to a group with permissions to Lenders to add or edit the contents.

To setup a lender:

1. Expand General Setup, select Lender.

2. Click ***Add New*** to start a new Lender or, if other Lender profiles exist, select one of themto edit.

3. Complete the Lender Setup information and click OK.

Remember that the green field color indicates required information and the field must have an entry.

Enter the hyphen for the tax identification number (TIN), which differs from the social security number. Example: 12-1234567

User's Guide - Bank 27

Starting Setup

If you check this box to use an alternate address, more text fields appear for alternate address entry.

Credit high and low ranges that you enter here are passed to party Details in transactions. However, the setup ranges will be overwritten if you pull a credit report using Credit Bureau.

28 User's Guide - Bank 28

Lending Setup

Lending Setup

Introduction

Setting common defaults for use during transactions is beneficial. The use of standard default material speeds and reduces the number of decisions required during the loan application process. This chapter addresses the addition of default information to the following setup areas:

Policy Setup

Repayment Methods Setup

Rates Setup

Index History Setup

Documents Setup

Policy Setup

The policy profile designates which state’s document set to use for the transaction along with other optional policy issues, such as default values for late charges and available accrual methods. This information must be completed for proper document autoselection and printing.

NOTE: You must have permission for Lending Setup, Policy to add or edit policies.

Tips for Creating a Policy Profile

Some items to note before creating policies:

You must have one policy profile set up to effectively use ARTA Lending.

Try to name your policy profile with a meaningful name; for example, Consumer Non-Real Estate. This will help you easily recognize the different policies created.

You can set up as many different policies as you need for the different kinds of loans you process.

Once created, you can select a policy profile whenever you create a loan or template.

Information from a selected policy profile will only default into the loan documents once. Edits made to the policy after beginning a loan will not refresh the prompts.

Setting Up a New Policy

1. Expand Lending Setup from the Navigator and select Policy.

2. Click ***Add New***.

3. Complete the Policy Setup information and click OK.

User's Guide - Bank 29

Lending Setup

After you make your state selection, the Accrual Methods button is displayed.

These items may not apply in every state.

Enter standard vesting language.

Check this box to select the Fed box option.

Check this box to define custom fields.

30 User's Guide - Bank 30

Lending Setup

Custom Fields on Documents ARTA Lending provides two custom fields that you can define for use on documents. The heading text you type displays as a prompt on the screen. Each field allows you to enter loan-specific data. Both the heading and the text entered will appear on the upper right-hand corner of some documents such as the UN and NDas notes.

Accrual Methods

After you make your state selection for your Policy profile, the Accrual Methods button displays.

Accrual Method Setup All accrual methods listed on this screen may not be applicable in your state. All methods are selected by default. Clear the check mark from those accrual methods that you do not want to have available at loan transaction time.

Click this button to select the accrual methods for this Policy profile.

User's Guide - Bank 31

Lending Setup

Accrual Method Descriptions Actual/365—The actual/365 accrual method is used to calculate simple interest loans. The word actual refers to the actual days in each period that are counted in charging interest. With this method, daily interest is calculated based on 365 days per year. The resulting daily factor is multiplied by the actual number of days in the period over which interest is being calculated.

Actual/360—The actual/360 accrual method is used to calculate simple interest loans. The word actual refers to the actual days in each period that are counted in charging interest. With this method, daily interest is calculated based on 360 days per year. The resulting daily factor is multiplied by the actual number of days in the period over which interest is being calculated.

You may clear the options not used by your institution.

Click a check box to clear the check mark.

32 User's Guide - Bank 32

Lending Setup

Actual/Actual—The actual/actual accrual method is used to calculate simple interest loans. The word actual refers to the actual days in each period that are counted in charging interest. With this method, daily interest is calculated based on the actual number of days in the year (365 days for nonleap years and 366 days for leap years). The resulting daily factor is multiplied by the actual number of days in the period over which interest is being calculated.

Periodic—The periodic accrual method is used to calculate simple interest loans. The daily interest factor is calculated based on equal-length periods.

Precomputed Add-OnThe interest of the loan is calculated at the beginning of the transaction and added to the principal. When add-on interest is used to calculate a loan, an add-on rate is used instead of a simple interest rate.

The APR is higher than the rate stated in the loan agreement because the add-on accrual method does not take into consideration the reduction of principal as installment payments are made.

Precomputed DiscountThe interest of the loan is calculated at the beginning of the transaction and deducted in advance from the face value of the loan. The borrower receives the face value less the interest.

Precomputed SimpleThe simple rate is considered an equivalent rate of interest (ERI). The payment is calculated such that the ERI is not exceeded.

Split Rate Add-OnThis method of accruing split rate interest assigns an add-on interest rate to two or three different tiers.

If the tiers are based on the loan amount, the interest rate for each tier is applied to that portion of the loan balance, which falls within that tier.

If the tiers are based on a number of months, the interest rate is determined by a formula which weights the interest rate for each tier according to the number of months in the loan term which are contained in that tier. The tiers can be based either on the loan amount or on a number of months.

Split Rate Simple—This method of accruing split rate interest assigns a simple interest rate to two or three different loan amount tiers. The interest rate for each tier is applied to that portion of the loan balance that falls within that tier.

Split Rate Setup The Split Rate Setup button appears in Policy setup under the Calculation Options area.

NOTE: Split Rate Setup is not available in every state.

User's Guide - Bank 33

Lending Setup

Define Split Rates by Dollar Amount If split rate simple is the only available split rate accrual method for the “Applicable law state/document set” selected, the Split Rate Setup screen allows you to define tiers by dollar amount.

Define Split Rates by Dollar Amount or by Months If split rate add-on is the only available split rate accrual method for the “Applicable law state/document set” selected, the Split Rate Setup screen allows you to define tiers by dollar amount or by months.

If split rate add-on and split rate simple are both available accrual methods for the “Applicable law state/document set” selected, the Split Rate Setup screen allows you to define tiers by dollar amount or by months. If you define the tiers by months and calculate a loan using the split rate simple accrual method, you will receive the following error message: Split rate definition based on monthly tiers is not currently supported.

The Split Rate Setup button is available with the Split Rate Add On and/or the Split Rate Simple accrual method.

Define your split rate tiers by the dollar amount of the loan.

♦ Type the dollar amount that defines the upper end of the first split rate tier.

♦ Type the interest rate for the first split rate tier. Repeat for the second split rate tier.

♦ Type the interest rate for the third split rate tier.

34 User's Guide - Bank 34

Lending Setup

Repayment Methods Setup

This section allows you to define the repayment method options available for consumer open-end loans during the draw period and repayment period.

Setting up repayment methods allows you to choose which of all defined methods will be used in the transaction. The methods specified in the transaction will print on the loan documents.

NOTE: You must have permissions to Lending Setup, Repayment Methods to edit the contents. For more information see Consumer Loans: Payment Frequencies.

Initial Setup

1. Expand Lending Setup from the Navigator and select Repayment Methods. Note the two repayment period tabs.

2. Select one or more repayment methods from the Draw period repayment methods tab. Draw period repayment methods describe the payments during the draw period and are required for all consumer open-end loans.

Choose this option if your split rate tiers are defined by the term of the loan.

Type the number of months in the first and second split rate tier.

User's Guide - Bank 35

Lending Setup

Select one or more repayment methods from the Repay period repayment methods tab. Repay period repayment methods are only used when the draw period expires before the maturity date.

Check all of the Draw Period repayments applicable to your plans.

Selections are saved as you select each option.

You may select as many repayment methods as you want in this setup section.

When you process an open-end loan, you will be able to select up to three repayment methods for the given transaction. At least one method for the draw and repayment periods must be chosen in order to process a loan.

36 User's Guide - Bank 36

Lending Setup

3. When you are finished, you may return to the Main Navigator. The program saves your selections.

Check all Repay Period repayments that are applicable to your plans.

As you check your selections, the program saves your data.

You may select as many repayment methods as you want in this setup section.

When you process an open-end loan, you will be able to select up to three repayment methods for the given transaction. At least one method for the draw and repayment periods must be chosen in order to process a loan.

User's Guide - Bank 37

Lending Setup

Rates Setup

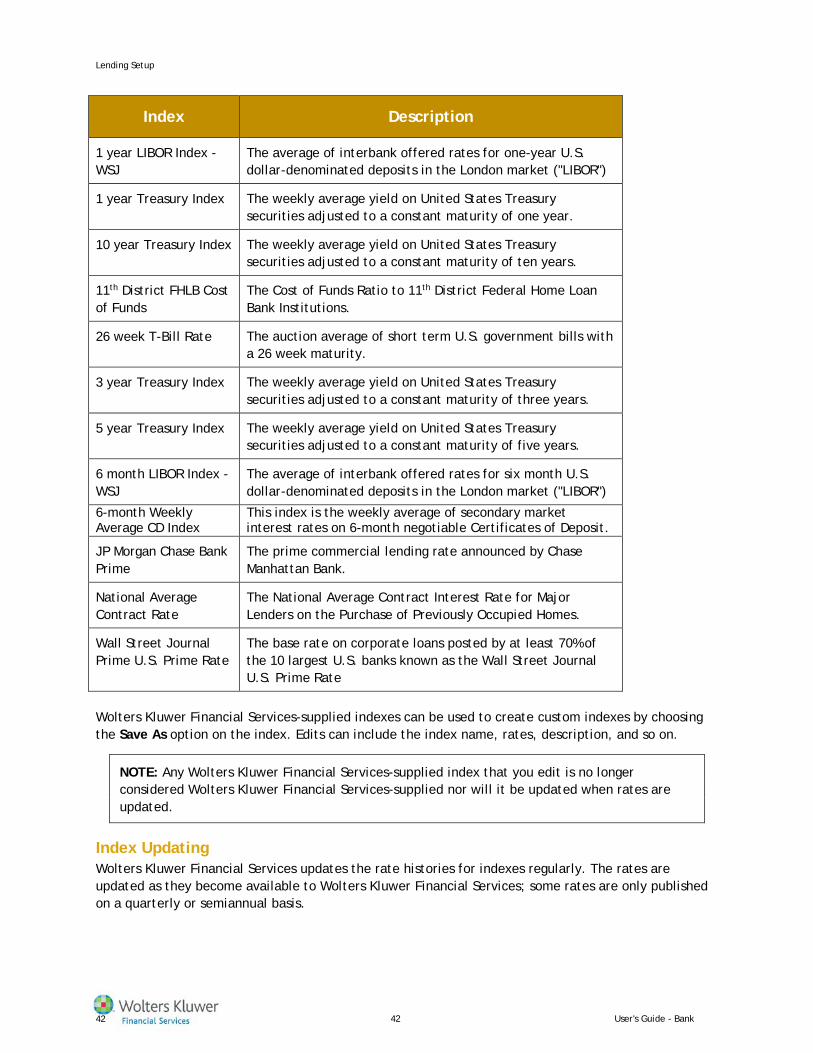

The Rates setup area allows you to define your fixed or variable interest rate index. This helps ensure proper calculations at transaction time.

NOTE: You must have permission to Rates to add or edit the contents.

Initial Setup

1. Expand Lending Setup from the Navigator and select Rates.

2. Click ***Add New***. Type a descriptive name for this new interest rate plan. The rate plan name is used to identify the plan.

3. Complete the Rate Setup information and click OK.

Choose this option if this rate plan is to be used for your consumer open-end loans.

If you have no floor and/or no ceiling, you may choose Specific value and leave the rate field blank.

The four options available for Rate change affects are discussed below.

38 User's Guide - Bank 38

Lending Setup

Rate Change Affects The four options for Rate change affects are:

Payment

Final payment

Payment amount and final payment

Term of loan

NOTE: These four options also link to the repayment method selected for a transaction (that is, installment, balloon, and so on). You will always see all four options for Rate change affects for all loan types. If an unsupported option is selected, however, it will be flagged at the validation step.

The following table lists the applicable Rate change affects options for the repayment method selected:

Rate change affects

Repayment Method

Payment amount

Final Payment

Payment amount & final payment

Term of loan

Installment X X X

Balloon X X

Amortized Balloon

X X X

Single Payment

X

Interest Only X

Principal Reduction

X

Demand Interest Only

X