Usefulness of corpotate annual report: Empirical study

41

WELCOME

-

Upload

pip-freixas -

Category

Business

-

view

48 -

download

1

Transcript of Usefulness of corpotate annual report: Empirical study

WELCOME

A Study on

Usefulness of Corporate Annual

Reports in Bangladesh

Corporate Annual Reports

Corporate annual report provided to investors is the major source that provides information on the effectiveness of the accomplishments of managers in meeting their fiduciary duties and carrying out their stewardship functions.

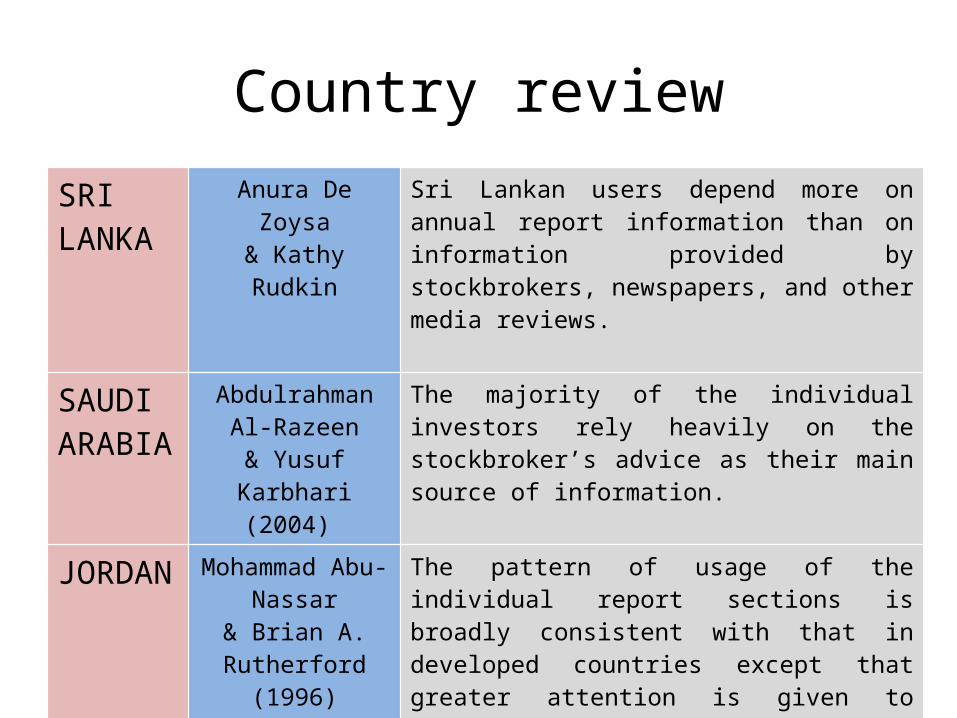

Country reviewSRI LANKA

Anura De Zoysa& Kathy Rudkin

Sri Lankan users depend more on annual report information than on information provided by stockbrokers, newspapers, and other media reviews.

SAUDI ARABIA

Abdulrahman Al-Razeen

& Yusuf Karbhari(2004)

The majority of the individual investors rely heavily on the stockbroker’s advice as their main source of information.

JORDAN Mohammad Abu-Nassar

& Brian A. Rutherford

(1996)

The pattern of usage of the individual report sections is broadly consistent with that in developed countries except that greater attention is given to auditors’ reports.

KUWAIT Kamal Naser, Rana Nuseibeh &Ahmed Al-Hussaini(2003)

The users mainly rely mainly on the information made directly available by the company

AUSTRALIA John K. Courtis(1982)

The users mainly depend on the stockbroker’s advice and ranked the importance of annual reports as 3rd.

QATAR Jalal M. Alattar &Khalid Al-Khater(2007)

The users consider annual reports to be very important and to be the main source of information for investment decision.

Survey Response

User Group Approached Responded Response Percentage (%)

Investors 44 27 61

Stockbrokers 8 6 75

Total 52 33 63

Pre-Readership Consideration

Finance Course or Training on Stock Market

Education Level

Experience

Financial Courses

17%

83%

Stock Brokers

YesNo

48%52%

Shareholders

YesNo

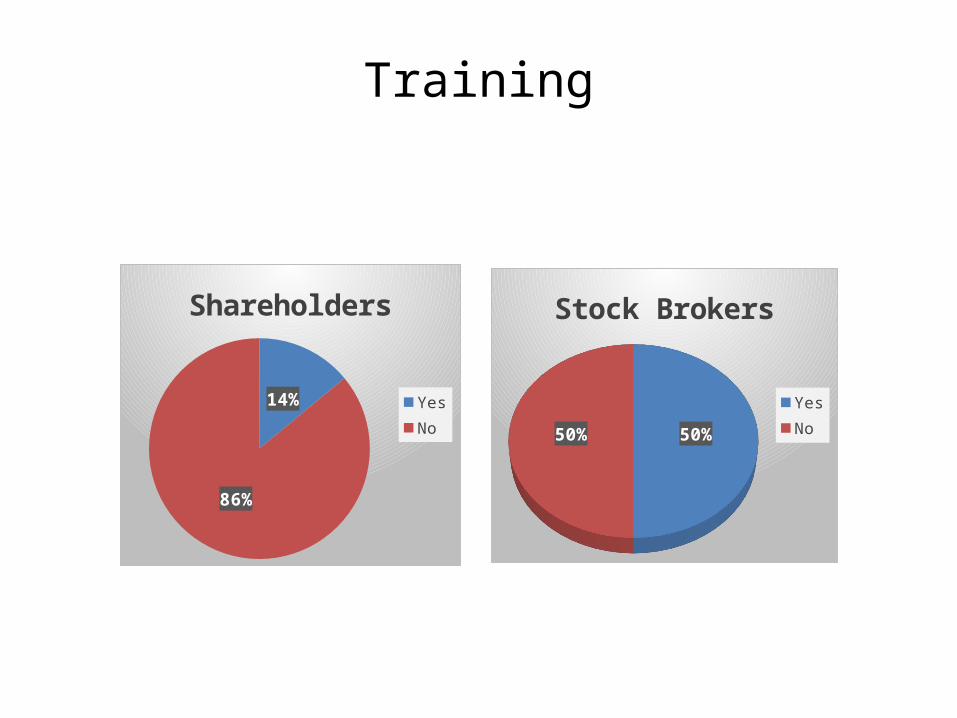

Training

50%50%

Stock Brokers

YesNo

14%

86%

Shareholders

YesNo

Education

33%

67%

Stock Brokers

Graduate/Postgraduate of BusinessGraduate/Postgraduate of Others

52%48%

Shareholders

Graduate/Postgraduate of BusinessGraduate/Postgraduate of Others

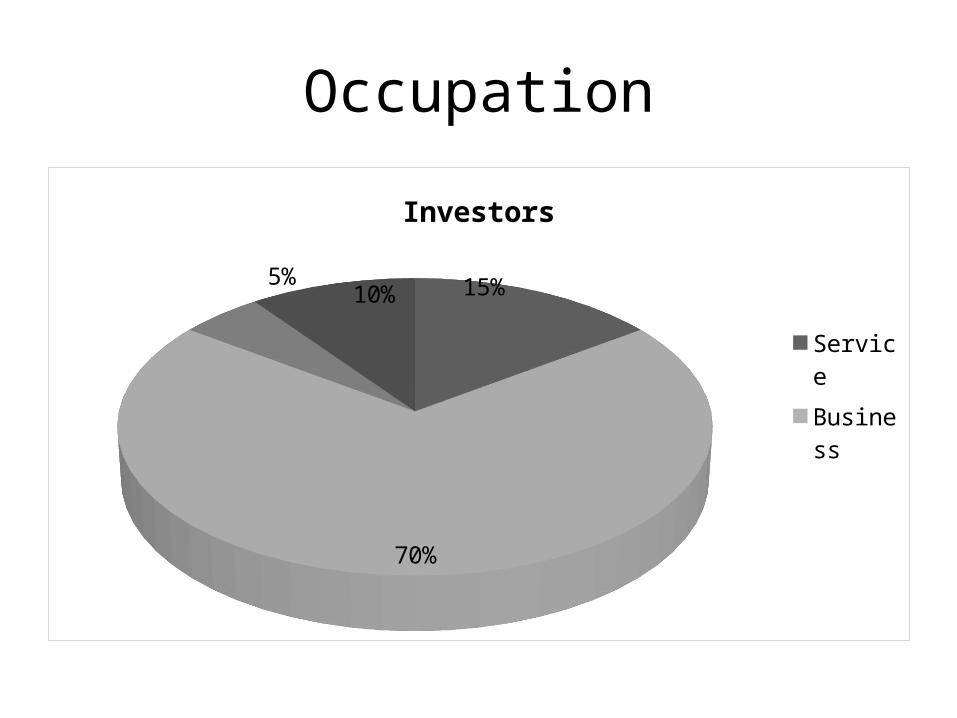

Occupation

15%

70%

5%10%

Investors

ServiceBusinessStudentOthers

Trading Experience

67%17%

16%

Stock Brokers

1-5 years6-10 years11-20 years48%

38%

14%

Shareholders

1-5 years6-10 years11-20 years

Reading between Numbers

Reading Annual Reports

40%

20%

20%

20%

Stock Brokers

AlwaysUsuallySometimesRarelyNever

11%

36%39%

14%

Shareholders

AlwaysUsuallySometimesRarelyNever

Importance of Sources of Information

Investors

Sources of information

Mean value

Standard Deviation

Mean difference

t - statistic Sig. (2-tailed)

Null Hypothesis

Broker_advice 3.14 1.457 .138 .510 .614 Accepted

FnF_advice2.93 1.280 -.069 -.290 .774

Accepted

Annual_report4.14 .915 1.138 6.696 .000

Accepted

Interim_report3.86 .915 .862 5.073 .000

Accepted

Communication_mgt3.17 1.311 .172 .708 .485

Accepted

Media_report3.21 1.424 .207 .783 .440

Accepted

Ho: µ ≥ 3 (Source of information is perceived as at least moderately important)H1: µ < 3 (Source of information is perceived as less than moderately important)

Sources of information

Mean value

Standard Deviation

Mean difference

t - statistic Sig. (2-tailed)

Null Hypothesis

Publication_DSE_BSEC3.24 1.455 .241 .893 .379

Accepted

Technical_analysis2.76 1.405 -.241 -.925 .363

Accepted

Info_internet2.83 1.391 -.172 -.668 .510

Accepted

Rumors1.90 1.319 -1.103 -4.506 .000

Rejected

Ho: µ ≥ 3 (Source of information is perceived as at least moderately important)H1: µ < 3 (Source of information is perceived as less than moderately important)

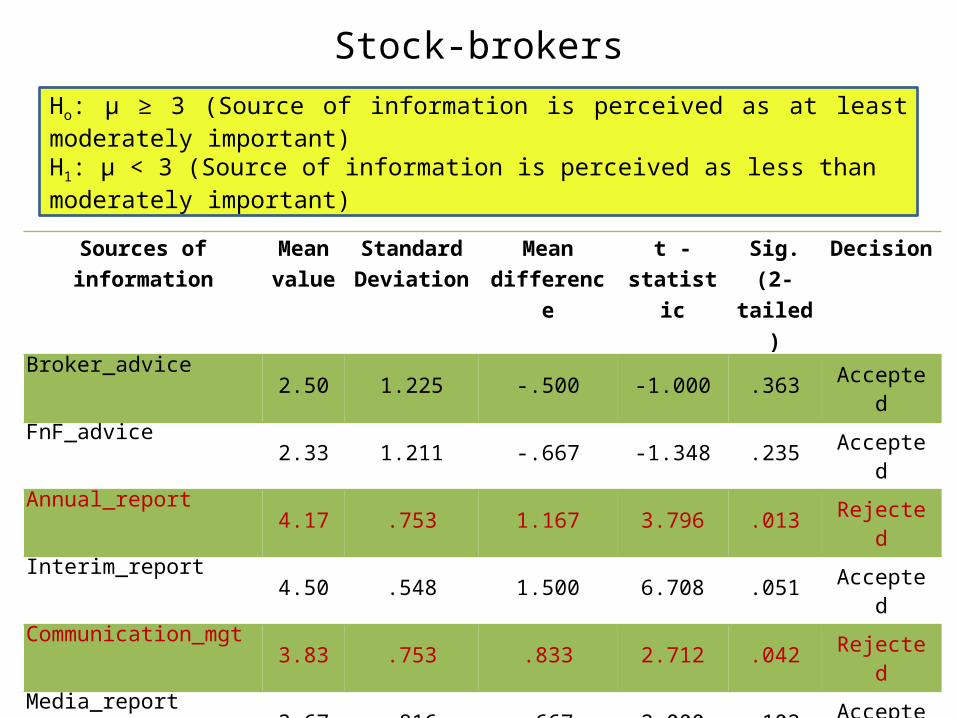

Stock-brokers

Sources of information Mean value

Standard Deviation

Mean difference

t - statistic Sig. (2-tailed)

Decision

Broker_advice 2.50 1.225 -.500 -1.000 .363 Accepted

FnF_advice 2.33 1.211 -.667 -1.348 .235 Accepted

Annual_report 4.17 .753 1.167 3.796 .013 Rejected

Interim_report 4.50 .548 1.500 6.708 .051 Accepted

Communication_mgt 3.83 .753 .833 2.712 .042 Rejected

Media_report 3.67 .816 .667 2.000 .102 Accepted

Publication_DSE_BSEC 3.83 .753 .833 2.712 .042 Rejected

Technical_analysis 3.83 .753 .833 2.712 .042 Rejected

Info_internet 2.00 1.549 -1.000 -1.581 .175 Accepted

Rumors 1.17 .408 -1.833 -11.000 .000 Rejected

Ho: µ ≥ 3 (Source of information is perceived as at least moderately important)H1: µ < 3 (Source of information is perceived as less than moderately important)

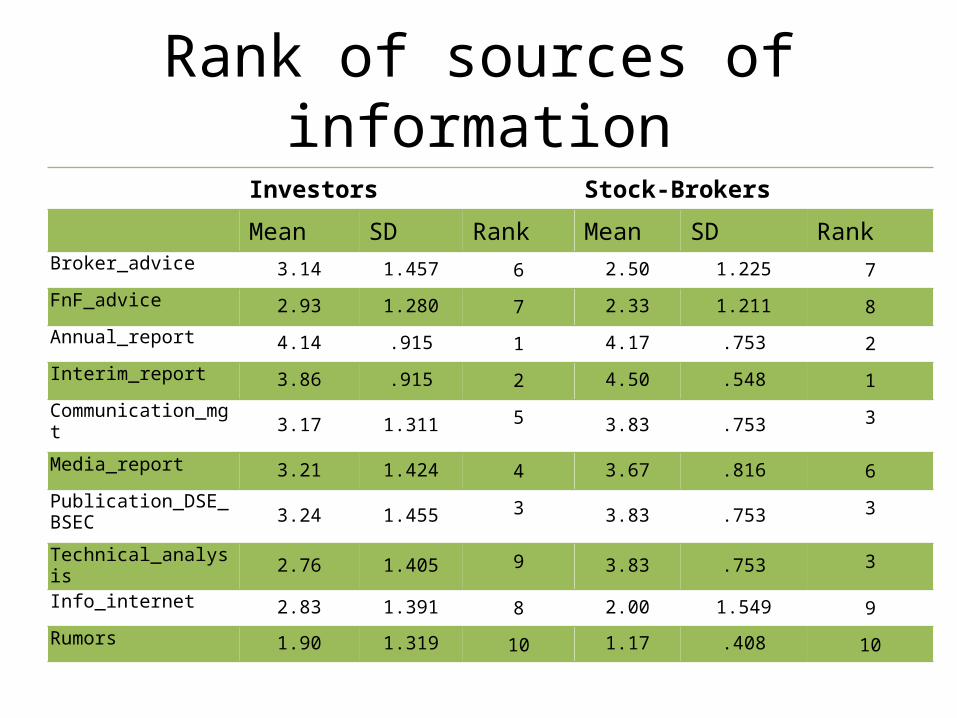

Rank of sources of information

Investors Stock-BrokersMean SD Rank Mean SD Rank

Broker_advice 3.14 1.457 6 2.50 1.225 7

FnF_advice 2.93 1.280 7 2.33 1.211 8

Annual_report 4.14 .915 1 4.17 .753 2

Interim_report 3.86 .915 2 4.50 .548 1

Communication_mgt3.17 1.311

53.83 .753

3

Media_report 3.21 1.424 4 3.67 .816 6

Publication_DSE_BSEC3.24 1.455

33.83 .753

3

Technical_analysis 2.76 1.405 9 3.83 .753 3

Info_internet 2.83 1.391 8 2.00 1.549 9

Rumors 1.90 1.319 10 1.17 .408 10

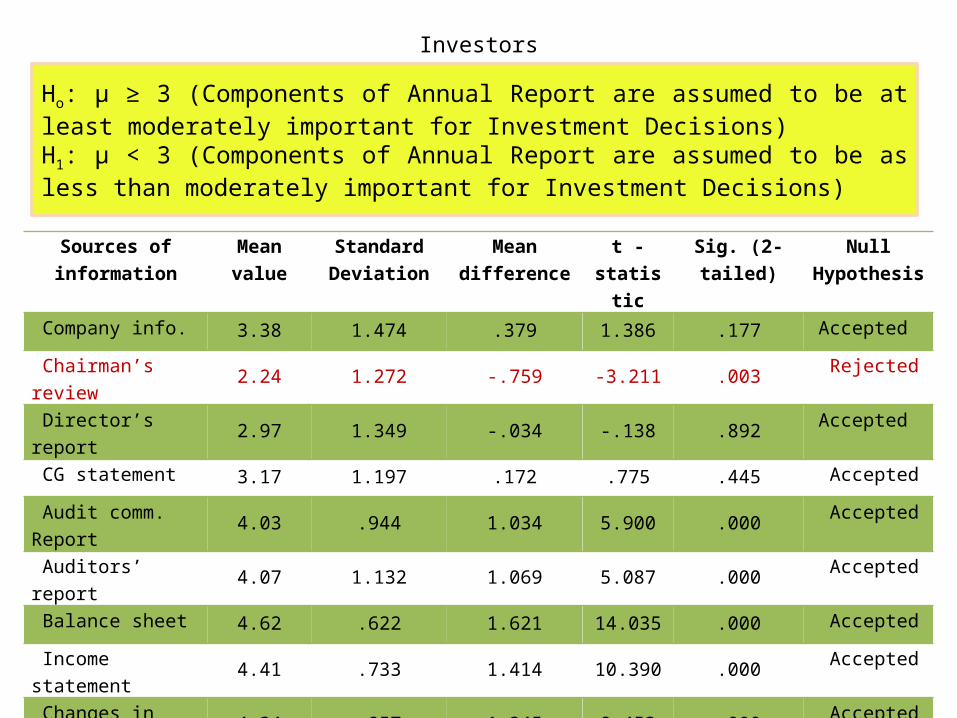

How important the annual report contents

are?

Investors

Sources of information

Mean value

Standard Deviation

Mean difference

t -statistic Sig. (2-tailed) Null Hypothesis

Company info. 3.38 1.474 .379 1.386 .177 Accepted

Chairman’s review 2.24 1.272 -.759 -3.211 .003 Rejected

Director’s report 2.97 1.349 -.034 -.138 .892 Accepted

CG statement 3.17 1.197 .172 .775 .445 Accepted

Audit comm. Report 4.03 .944 1.034 5.900 .000 Accepted

Auditors’ report 4.07 1.132 1.069 5.087 .000 Accepted

Balance sheet 4.62 .622 1.621 14.035 .000 Accepted

Income statement 4.41 .733 1.414 10.390 .000 Accepted

Changes in equity 4.34 .857 1.345 8.453 .000 Accepted

Cash flow state. 3.97 1.267 .966 4.103 .000 Accepted

Acc. Policy notes 3.59 1.119 .586 2.822 .009 Accepted

Ho: µ ≥ 3 (Components of Annual Report are assumed to be at least moderately important for Investment Decisions)H1: µ < 3 (Components of Annual Report are assumed to be as less than moderately important for Investment Decisions)

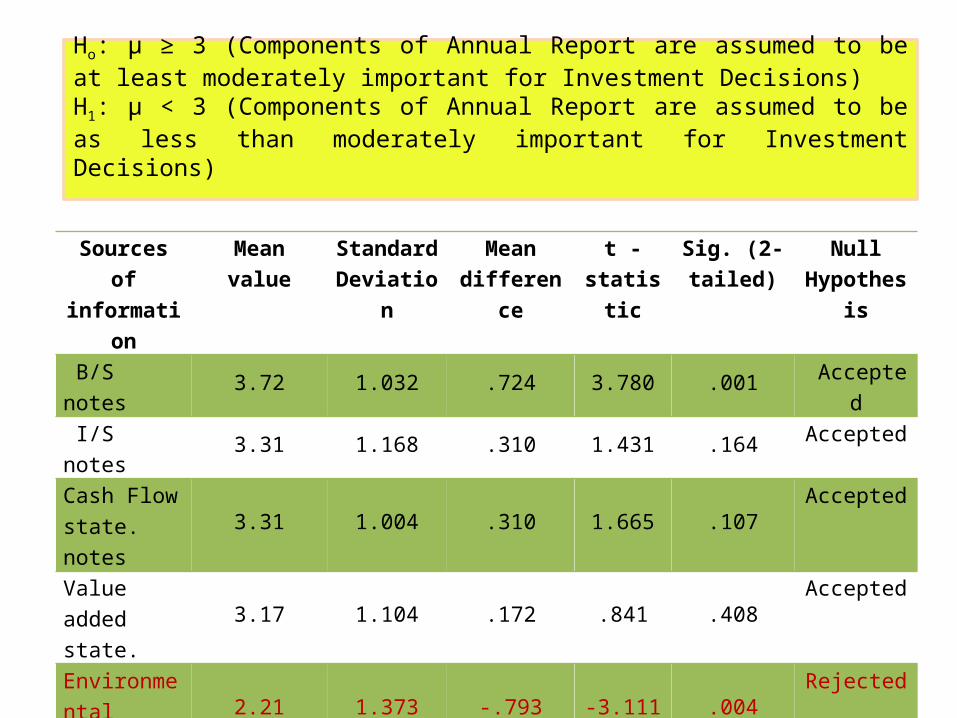

Sources of information

Mean value Standard Deviation

Mean difference

t -statistic

Sig. (2-tailed)

Null Hypothesis

B/S notes 3.72 1.032 .724 3.780 .001 Accepted

I/S notes 3.31 1.168 .310 1.431 .164 Accepted

Cash Flow state. notes 3.31 1.004 .310 1.665 .107 Accepted

Value added state. 3.17 1.104 .172 .841 .408 Accepted

Environmental reports 2.21 1.373 -.793 -3.111 .004 Rejected

Reviews 4.17 .928 1.172 6.800 .000 Accepted

Essay 2.72 1.131 -.276 -1.314 .200 Accepted

Ho: µ ≥ 3 (Components of Annual Report are assumed to be at least moderately important for Investment Decisions)H1: µ < 3 (Components of Annual Report are assumed to be as less than moderately important for Investment Decisions)

Components of Annual report

Mean value

Standard Deviation

Mean difference

t - statistic Sig. (2-tailed) Decision

Company info. 4.00 1.265 1.000 1.936 .111 Accepted

Chairman’s review 4.17 1.329 1.167 2.150 .084 Accepted

Director’s report 3.83 1.329 .833 1.536 .185 Accepted

CG statement 4.17 .983 1.167 2.907 .034 Rejected

Audit comm. Report4.33 .816 1.333 4.000 .010 Rejected

Auditors’ report 4.50 .548 1.500 6.708 .001 Rejected

Balance sheet 4.83 .408 1.833 11.000 .000 Accepted

Income statement 4.67 .516 1.667 7.906 .001 Rejected

Changes in equity 4.33 .816 1.333 4.000 .010 Rejected

Cash flow state. 4.17 .753 1.167 3.796 .013 Rejected

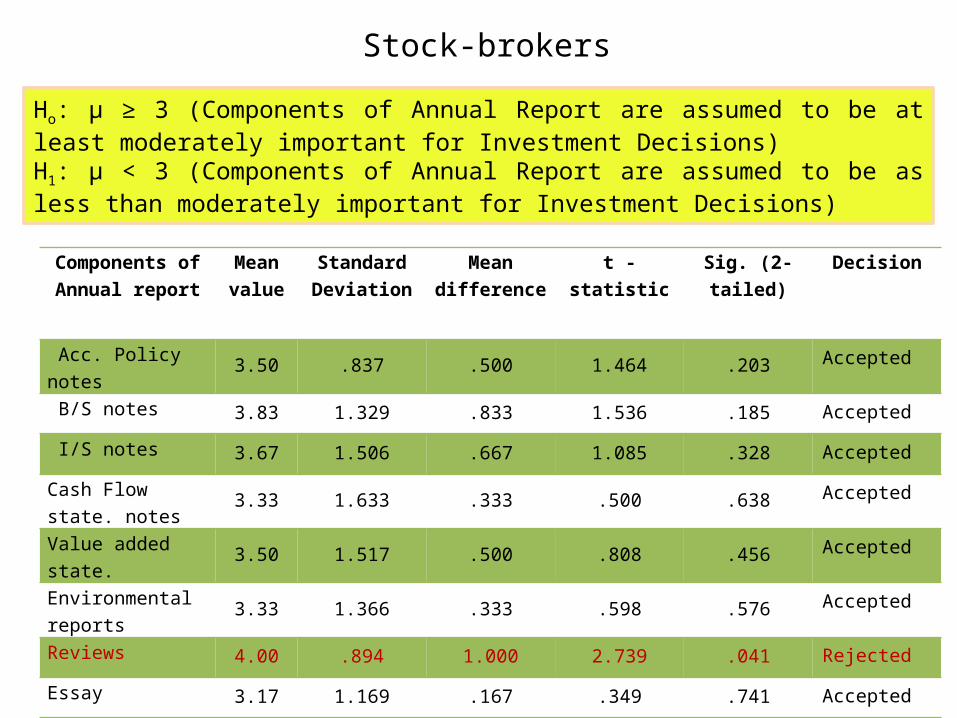

Stock-Brokers

Ho: µ ≥ 3 (Components of Annual Report are assumed to be at least moderately important for Investment Decisions)H1: µ < 3 (Components of Annual Report are assumed to be as less than moderately important for Investment Decisions)

Components of Annual report

Mean value

Standard Deviation

Mean difference

t - statistic Sig. (2-tailed) Decision

Acc. Policy notes 3.50 .837 .500 1.464 .203 Accepted

B/S notes 3.83 1.329 .833 1.536 .185 Accepted

I/S notes 3.67 1.506 .667 1.085 .328 Accepted

Cash Flow state. notes 3.33 1.633 .333 .500 .638

Accepted

Value added state. 3.50 1.517 .500 .808 .456 Accepted

Environmental reports 3.33 1.366 .333 .598 .576

Accepted

Reviews 4.00 .894 1.000 2.739 .041 Rejected

Essay 3.17 1.169 .167 .349 .741 Accepted

Stock-brokers

Ho: µ ≥ 3 (Components of Annual Report are assumed to be at least moderately important for Investment Decisions)H1: µ < 3 (Components of Annual Report are assumed to be as less than moderately important for Investment Decisions)

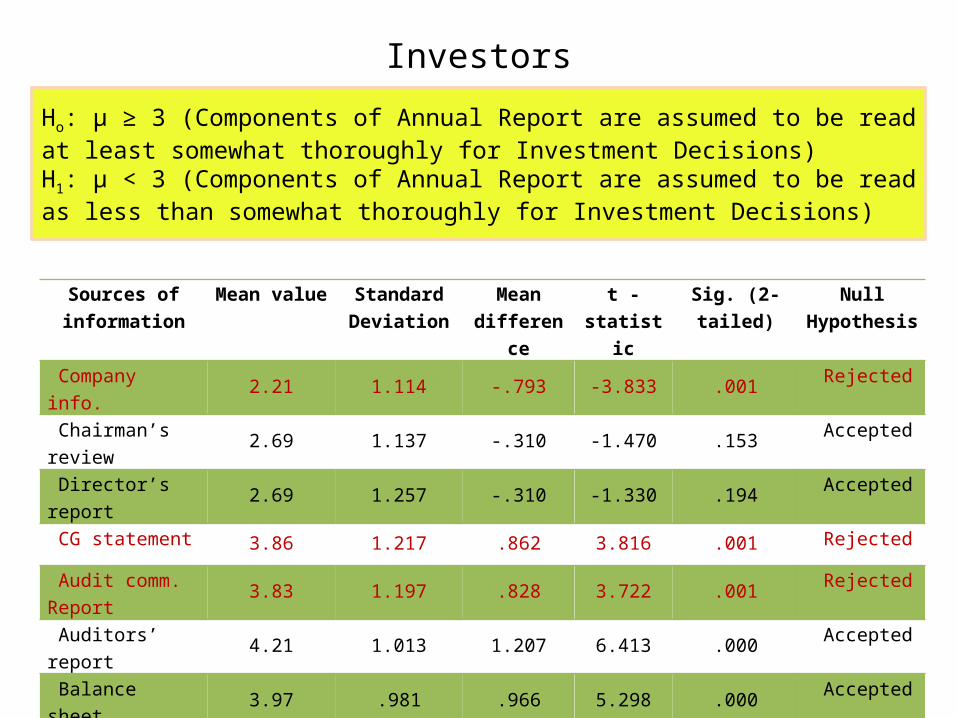

Thoroughness

Investors

Sources of information

Mean value Standard Deviation

Mean difference

t -statistic Sig. (2-tailed) Null Hypothesis

Company info.2.21 1.114 -.793 -3.833 .001

Rejected

Chairman’s review2.69 1.137 -.310 -1.470 .153

Accepted

Director’s report2.69 1.257 -.310 -1.330 .194

Accepted

CG statement3.86 1.217 .862 3.816 .001

Rejected

Audit comm. Report 3.83 1.197 .828 3.722 .001

Rejected

Auditors’ report4.21 1.013 1.207 6.413 .000

Accepted

Balance sheet3.97 .981 .966 5.298 .000

Accepted

Income statement3.79 1.114 .793 3.833 .001

Rejected

Ho: µ ≥ 3 (Components of Annual Report are assumed to be read at least somewhat thoroughly for Investment Decisions)H1: µ < 3 (Components of Annual Report are assumed to be read as less than somewhat thoroughly for Investment Decisions)

Sources of information

Mean value Standard Deviation

Mean difference

t -statisti

c

Sig. (2-tailed) Decision

Changes in equity 3.52 1.153 .517 2.415 .023 Accepted

Cash flow state. 3.34 1.111 .345 1.672 .106 Accepted

Acc. Policy notes 3.59 1.119 .586 2.822 .009 Accepted

B/S notes 3.14 1.246 .138 .596 .556 Accepted

I/S notes 2.9310 1.03272 -.06897 -.360 .722 Accepted

Cash Flow state. notes 2.9310 1.25160 -.06897 -.297 .769 Accepted

Value added state. 2.0345 1.20957 -.96552 -4.299 .000 Accepted

Environmental reports 3.6897 1.31213 .68966 2.830 .009 Rejected

Reviews 2.5172 1.27113 -.48276 -2.045 .050 Rejected

Essay 2.84. 1.23970. -.160 -.1291 .030 Rejected

Ho: µ ≥ 3 (Components of Annual Report are assumed to be read at least somewhat thoroughly for Investment Decisions)H1: µ < 3 (Components of Annual Report are assumed to be read as less than somewhat thoroughly for Investment Decisions)

Components of Annual report

Mean value

Standard Deviation

Mean difference

t - statistic Sig. (2-tailed) Null Hypothesis

Company info. 3.83 1.169 .833 1.746 .141 Accepted

Chairman’s review 3.00 1.265 .000 .000 1.000 Accepted

Director’s report 3.67 .816 .667 2.000 .102 Accepted

CG statement 3.50 .837 .500 1.464 .203 Accepted

Audit comm. Report4.33 .816 1.333 4.000 .010

Rejected

Auditors’ report 4.33 1.033 1.333 3.162 .025 Rejected

Balance sheet 4.67 .516 1.667 7.906 .001 Rejected

Income statement 4.50 .548 1.500 6.708 .001 Rejected

Changes in equity 4.33 .816 1.333 4.000 .010 Rejected

Cash flow state. 4.33 .816 1.333 4.000 .010 Rejected

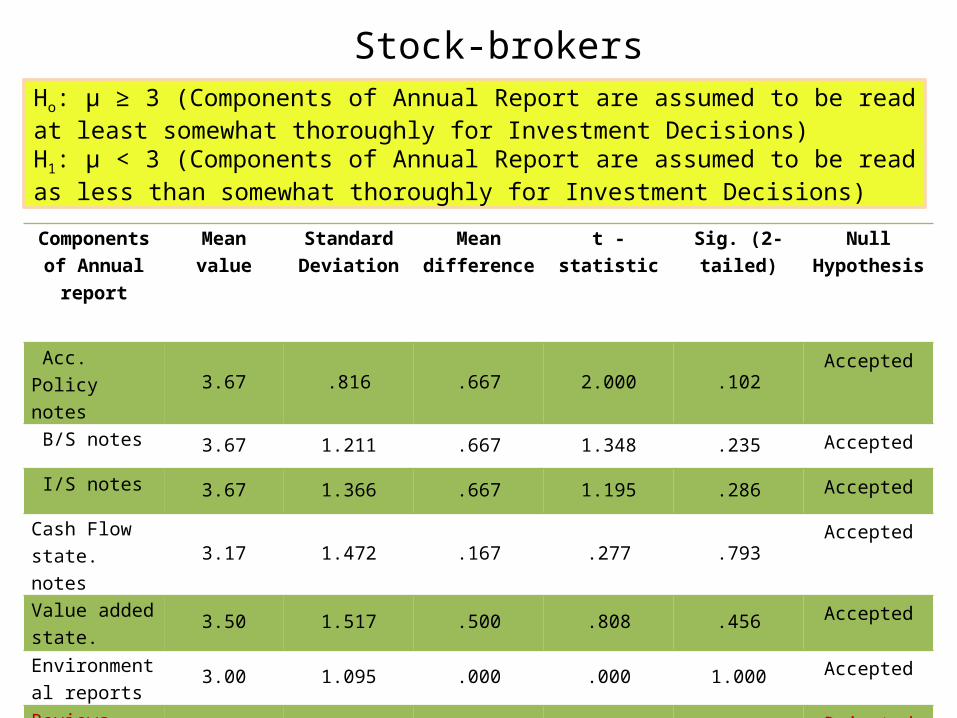

Stock-brokersHo: µ ≥ 3 (Components of Annual Report are assumed to be read at least somewhat thoroughly for Investment Decisions)H1: µ < 3 (Components of Annual Report are assumed to be read as less than somewhat thoroughly for Investment Decisions)

Components of Annual report

Mean value Standard Deviation

Mean difference

t - statistic Sig. (2-tailed) Null Hypothesis

Acc. Policy notes 3.67 .816 .667 2.000 .102 Accepted

B/S notes3.67 1.211 .667 1.348 .235 Accepted

I/S notes3.67 1.366 .667 1.195 .286 Accepted

Cash Flow state. notes 3.17 1.472 .167 .277 .793

Accepted

Value added state. 3.50 1.517 .500 .808 .456

Accepted

Environmental reports 3.00 1.095 .000 .000 1.000

Accepted

Reviews4.17 .983 1.167 2.907 .034 Rejected

Essay3.33 1.366 .333 .598 .576 Accepted

Stock-brokersHo: µ ≥ 3 (Components of Annual Report are assumed to be read at least somewhat thoroughly for Investment Decisions)H1: µ < 3 (Components of Annual Report are assumed to be read as less than somewhat thoroughly for Investment Decisions)

Importance

Thoroughness

Investors

Correlation T-statistic Sig. (2 tailed) Null Hypothesis Company info. .779 2.451 .021 Rejected

Chairman’s review .694 .197 .846 Accepted Director’s report .714 1.548 .133 Accepted CG statement .630 2.461 .020 Rejected Audit comm. Report .719 1.095 .283 Accepted

Auditors’ report .773 1.653 .109 Accepted Balance sheet .469 2.457 .020 Rejected Income statement .666 3.279 .003 Rejected Changes in equity .676 3.591 .001 Rejected

Ho : µ1=µ2 (Degree of thoroughness and degree of importance of components of annual report are equal. )H1: µ1≠µ2 (Degree of thoroughness and degree of importance of components of annual report are not the equal.)

Correlation T-statistic Sig. (2 tailed) Null Hypothesis

Cash flow state. .648 2.365 .025 Rejected Acc. Policy notes .550 1.229 .229 Accepted B/S notes .702 .891 .380 Accepted I/S notes .706 1.000 .326 AcceptedCash Flow state. notes

.848 3.638 .001 Rejected

Value added state. .629 1.270 .214 Accepted

Environmental reports

.598 .796 .433 Accepted

Reviews .720 2.853 .008 RejectedEssay .600 1.030 .312 Accepted

Ho : µ1=µ2 (Degree of thoroughness and degree of importance of components of annual report are equal. )H1: µ1≠µ2 (Degree of thoroughness and degree of importance of components of annual report are not the equal.)

Correlation T-statistic Sig. (2 tailed) Null Hypothesis Company info. .947 1.000 .363 Accepted Chairman’s review .250 1.581 .175 Accepted Director’s report .600 -.415 .695 Accepted CG statement .608 1.000 .363 Accepted Audit comm. Report .700 .000 1.000 Accepted Auditors’ report .707 .542 .611 Accepted Balance sheet .632 1.000 .363 Accepted Income statement .707 1.000 .363 Accepted Changes in equity 1.000 Std error of the difference was

zeroRejected

Ho : µ1=µ2 (Degree of thoroughness and degree of importance of components of annual report are equal. )H1: µ1≠µ2 (Degree of thoroughness and degree of importance of components of annual report are not the equal.)

Stock-brokers

Correlation T-statistic Sig. (2 tailed) Null Hypothesis

Cash flow state. .868 -1.000 .363 Accepted Acc. Policy notes .878 1.000 .363 Accepted B/S notes .953 1.000 .363 Accepted I/S notes .907 .000 1.000 AcceptedCash Flow state. notes

.888 .542 .611 Accepted

Value added state.

1.000 Std error of the difference was zero

Rejected

Environmental reports

.802 1.000 .363 Accepted

Reviews .910 -1.000 .363 AcceptedEssay .960 -1.000 .363 Accepted

Ho : µ1=µ2 (Degree of thoroughness and degree of importance of components of annual report are equal. )H1: µ1≠µ2 (Degree of thoroughness and degree of importance of components of annual report are not the equal.)

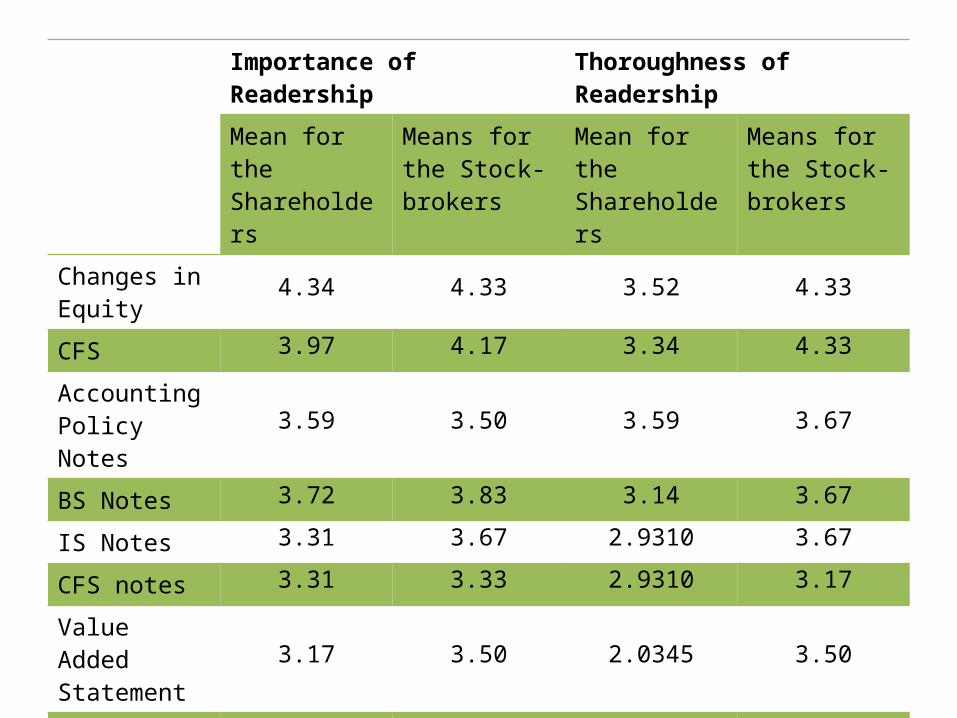

Readership Comparison

Importance of Readership Thoroughness of Readership

Mean for the Shareholders

Means for the Stock-brokers

Mean for the Shareholders

Means for the Stock-brokers

Company info 3.38 4.00 2.21 3.83

Chairman’s Review 2.24 4.17 2.69 3.00

Director’s Report 2.97 3.83 2.69 3.67

CG Statement 3.17 4.17 3.86 3.50

Audit Committee Report

4.03 4.33 3.83 4.33

Auditor’s Report 4.07 4.50 4.21 4.33

BS 4.62 4.83 3.97 4.67

IS 4.41 4.67 3.79 4.50

Importance of Readership Thoroughness of ReadershipMean for the Shareholders

Means for the Stock-brokers

Mean for the Shareholders

Means for the Stock-brokers

Changes in Equity 4.34 4.33 3.52 4.33

CFS 3.97 4.17 3.34 4.33Accounting Policy Notes 3.59 3.50 3.59 3.67

BS Notes 3.72 3.83 3.14 3.67IS Notes 3.31 3.67 2.9310 3.67CFS notes 3.31 3.33 2.9310 3.17Value Added Statement 3.17 3.50 2.0345 3.50

Environmental Report 2.21 3.33 3.6897 3.00

Reviews 4.17 4.00 2.5172 4.17Essays and Pictorial 2.72 3.17 2.84 3.33

Findings

While collecting data, we found the stock-brokers to be more cordial and cooperating than the investors.

Company information though not perceived to be much important by the investors but is somewhat read thoroughly.

Environmental report is neither perceived as important nor read thoroughly. Inferences can be drawn that they are not much concerned about the company's environmental disclosure. Either they don’t have faith in the company reporting or they simply don’t care about the environmental reporting.

Neither the investor nor the brokers considered audit committee report as important.

Findings

• Brokers did not regard Auditors Report as important. Likewise they don’t read them thoroughly .

• Rumors were found to be the least important source of information for both the investors and the brokers.

• Interim reports were found to be perceived more important than annual reports as an important source of information by the brokers .

• Corporate governance was not taken importantly by either parties.

Recommendations

• Organizations should provide more transparent and understandable

financial information through annual report which ultimately lead to

take rational and sound investment decision.

• Awareness should be created among general investors through various

training programs and seminars.

• Efficient efforts should be taken to make the annual report more

reliable to the shareholders.

• Purpose of maximizing shareholders value should be clearly

highlighted in the annual report.