USD/SGD: 1 - uobgroup.com · It was all about the OPEC overnight, and OPEC representatives...

12

FX Insights Thursday, 01 December 2016 1 | Page Quek Ser Leang [email protected] Lee Sue Ann [email protected] Global Economics & Markets Research Email: [email protected] URL: www.uob.com.sg/research Thursday, 01 December 2016 FX Insights Chart Of The Day – USD/SGD: 1.4345 Resumption of bullish trend only if daily closing above 1.4365. We shifted to a neutral stance yesterday (see Chart of the Day update) and were of the view that USD has entered a neutral consolidation phase. The strong overnight rally was clearly unexpected but we are not convinced that the current USD strength is the resumption of the recent bullish trend. Only a daily closing above 1.4365 would indicate that a move towards the year’s high at 1.4445 has started. That said, the shorter-term outlook is constructive and any pull-back is expected to encounter solid support near 1.4280 followed by the stronger level near 1.4230.

Transcript of USD/SGD: 1 - uobgroup.com · It was all about the OPEC overnight, and OPEC representatives...

FX Insights Thursday, 01 December 2016 1 | P a g e

Quek Ser Leang [email protected] Lee Sue Ann [email protected] Global Economics & Markets Research

Email: [email protected] URL: www.uob.com.sg/research

Thursday, 01 December 2016 FX Insights

Chart Of The Day – USD/SGD: 1.4345 Resumption of bullish trend only if daily closing above 1.4365.

We shifted to a neutral stance yesterday (see Chart of the Day update) and were of the view that USD has entered a neutral

consolidation phase. The strong overnight rally was clearly unexpected but we are not convinced that the current USD strength

is the resumption of the recent bullish trend. Only a daily closing above 1.4365 would indicate that a move towards the year’s

high at 1.4445 has started. That said, the shorter-term outlook is constructive and any pull-back is expected to encounter solid

support near 1.4280 followed by the stronger level near 1.4230.

FX Insights Thursday, 01 December 2016 2 | P a g e

OVERVIEW

It was all about the OPEC overnight, and OPEC representatives confounded the sceptics after reaching a landmark deal to

reduce oil output. The OPEC said that it would cut production by 1.2 million barrels a day from 33.6 million barrels and said it

expects producers from outside the group, including Russia, to join with additional cuts totaling 600,000 barrels a day. The

OPEC cuts were deeper than many had expected, amounting to about 1% of global production. The 14-member group hopes

the output cuts will help shrink a supply glut that has been fed in part by the US shale boom, and has depressed oil prices for

more than two years.

Crude benchmarks have rallied strongly on the news – both Brent and WTI are up over 8%. The inflationary impact of higher

crude prices combined with a solid US data flow overnight has combined to weaken the Treasury market, with 10-year yields up

around 9bps to 2.38%. US equities ended a mixed bag, perhaps partly reacting to President-elect Trump’s announcement of

former Goldman-Sachs banker Steven Mnuchin as his nominee for Treasury Secretary. The US dollar got a lift from the better-

than-expected ADP payrolls print – which came in at +216k for November, versus the revised +119k increase in October, well

above expectations for a +170k result.

Today, we receive the manufacturing ISM survey for November, October construction spending and November vehicle sales.

The weekly jobless claims and Bloomberg consumer comfort index will also be released. Fed’s Mester and Kaplan will speak.

Latest Flash Note: 30 Nov 16

A Robust 3Q 2016 GDP Growth Revised Higher To 3.2% http://bit.ly/2fTbche

FX Insights Thursday, 01 December 2016 3 | P a g e

* Shift in outlook.

* Percentage difference between the closing price and the last price 1-period ago. ** Percentage difference between the closing price and the last price on 31-Dec-15.

01-Dec-16 Summary of Views

FX Pairs Spot Outlook Since/ Rate

Target Trailing-Stop Support Resistance

USD/SGD 1.4345 Neutral 30 Nov 16

1.4245 - -

S1: 1.4280 S2: 1.4230

R1: 1.4365 R2: 1.4400

EUR/SGD 1.5185 Neutral 28 Nov 16

1.5130 - -

S1: 1.5135 S2: 1.5100

R1: 1.5220 R2: 1.5250

GBP/SGD 1.7945 Neutral 16 Nov 16

1.7605 - -

S1: 1.7880 S2: 1.7840

R1: 1.8050 R2: 1.8150

AUD/SGD 1.0595 Neutral 24 Nov 16

1.0560 - -

S1: 1.0540 S2: 1.0500

R1: 1.0630 R2: 1.0700

JPY/SGD 1.2515 Neutral 29 Nov 16

1.2670 - -

S1: 1.2470 S2: 1.2380

R1: 1.2580 R2: 1.2620

USD/MYR 4.4650 Bullish 10 Nov 16

4.2470 4.4770 4.4000

4.4200 4.4000

S1: 4.4400 S2: 4.4200

R1: 4.4700 R2: 4.4770

USD/THB 35.70 Neutral 29 Nov 16

35.55 - -

S1: 35.65 S2: 35.58

R1: 35.74 R2: 35.80

USD/CNH 6.9080 Neutral 29 Nov 16

6.9195 - -

S1: 6.9000 S2: 6.8900

R1: 6.9280 R2: 6.9400

CNH/SGD 0.2074 *Bullish 01 Dec 16

0.2074 0.2083 0.2062

S1: 0.2067 S2: 0.2062

R1: 0.2076 R2: 0.2083

EUR/USD 1.0585 Neutral 28 Nov 16

1.0650 - -

S1: 1.0550 S2: 1.0515

R1: 1.0670 R2: 1.0700

GBP/USD 1.24515 Neutral 16 Nov 16

1.2475 - -

S1: 1.2420 S2: 1.2300

R1: 1.2550 R2: 1.2600

AUD/USD 0.7390 Neutral 24 Nov 16

0.7380 - -

S1: 0.7355 S2: 0.7300

R1: 0.7440 R2: 0.7500

NZD/USD 0.7080 Neutral 29 Nov 16

0.7085 - -

S1: 0.7050 S2: 0.7000

R1: 0.7110 R2: 0.7150

USD/JPY 114.40 *Bullish 01 Dec 16

114.40 115.60 113.20

S1: 113.60 S2: 113.20

R1: 115.00 R2: 115.60

FX Pairs Ranges for 30-Nov-16 Performance*

Open High Low Close 1-day 1-week 1-month YTD**

USD/SGD 1.4246 1.4355 1.4229 1.4336 +0.61% +0.12% +3.05% +1.12%

EUR/SGD 1.5167 1.5204 1.5126 1.5172 +0.02% +0.41% -0.61% -1.44%

GBP/SGD 1.7792 1.7943 1.7698 1.7921 +0.74% +0.64% +5.27% -14.2%

AUD/SGD 1.0660 1.0673 1.0562 1.0580 -0.75% +0.13% 0% +2.59%

JPY/SGD 1.2675 1.2699 1.2510 1.2518 -1.23% -1.62% -5.62% +6.27%

USD/MYR 4.4600 4.4640 4.4600 4.4640 0% +0.54% +6.53% +4.05%

USD/THB 35.65 35.75 35.55 35.69 +0.08% 0% +1.91% -0.91%

USD/CNH 6.9140 6.9190 6.8939 6.9185 +0.06% -0.50% +2.08% +5.33%

EUR/USD 1.0646 1.0666 1.0551 1.0585 -0.58% +0.27% -3.58% -2.53%

GBP/USD 1.2491 1.2525 1.2419 1.2507 +0.09% +0.46% +2.18% -15.0%

AUD/USD 0.7483 0.7497 0.7374 0.7382 -1.34% -0.04% -2.97% +1.33%

NZD/USD 0.7130 0.7170 0.7071 0.7080 -0.60% +1.08% -0.96% +3.72%

USD/JPY 112.38 114.53 112.02 114.44 +1.85% +1.72% +9.18% -4.87%

FX Insights Thursday, 01 December 2016 4 | P a g e

USD/SGD: 1.4345

USD/SGD tracked higher along with major currencies weakening across the board overnight, along with stronger than

expected ADP report, to hit high of 1.4355 late in the session, finishing 0.6% higher on Wednesday at 1.4335. With the

stronger USD, SGD NEER index dropped back just marginally below the midpoint this morning after several sessions in the

upper half of the policy band. For now, the 0.0% to -0.5% range below the midpoint suggests USD/SGD at 1.4345 to 1.4416.

Latest Flash Note: 29 Nov 16

Singapore SMEs: Emerging Signs Of Stress http://bit.ly/2gTwFrQ

24-HOUR VIEW: 1-3 WEEKS VIEW:

The strong rally in USD is unexpected and is accompanied

by strong momentum. However, any further up-move would

likely be at a slower pace in view of the overbought

conditions. From here, a move above last week’s 1.4365

peak would not be surprising but a sustained extension

beyond 1.4400 seems unlikely. Support is at 1.4315 ahead

of the stronger level near 1.4280.

Neutral: Resumption of bullish trend only if daily closing

above 1.4365.

[See Chart of the Day on page 1]

FX Insights Thursday, 01 December 2016 5 | P a g e

EUR/SGD: 1.5185

24-HOUR VIEW: 1-3 WEEKS VIEW:

In line with expectation, EUR extended its gain but the up-

move was checked by the strong 1.5220 resistance (high of

1.5204). Another attempt towards 1.5220 seems likely but we

expect this level to continue to act as a major resistance. On

the downside, only a move back below 1.5135 would indicate

that the short-term upward pressure has eased.

Neutral: Shift to bullish if daily closing above 1.5250.

Upward momentum is improving and EUR is pressing higher

towards the top end of the expected 1.5050/1.5220

consolidation range. While a move above 1.5220 is not ruled

out, there is another strong level at 1.5250 and only a clear

break above this level would indicate the start of a sustained

up-move. Overall, EUR is expected to be underpinned for

now with solid support at 1.5100.

GBP/SGD: 1.7945

24-HOUR VIEW: 1-3 WEEKS VIEW:

GBP is currently holding just below the major 1.7950

resistance and based on the strong momentum, a break

above this level would not be surprising and could lead to

further up-move towards 1.8000. Support is at 1.7880 ahead

of the stronger level near 1.7840.

Neutral: Shift to bullish if daily closing above 1.7950.

GBP is currently holding near the top end of the expected

sideway consolidation range of 1.7550/1.7950. Upward

momentum has improved considerably and a daily closing

above 1.7950 would indicate that a move towards 1.8050,

1.8150 has started. This appears to be a likely scenario

unless there is a move back below 1.7840 within these 1 to 2

days.

AUD/SGD: 1.0595

24-HOUR VIEW: 1-3 WEEKS VIEW:

The unexpected sharp drop appears to be running ahead of

itself and while a move below the overnight low of 1.0562 is

not ruled out, the next support at 1.0540 is likely strong

enough to hold any further decline. Resistance is at 1.0630

and the 1.0673 high seen yesterday is not expected to be

challenged.

Neutral: In a 1.0500/1.0700 range.

In recent updates, we noted that only a daily closing above

1.0700/10 would shift the current neutral outlook for AUD to

bullish. The sharp drop yesterday has put paid to the

scenario and AUD has likely moved back into a

1.0500/1.0700 consolidation range.

JPY/SGD: 1.2515

24-HOUR VIEW: 1-3 WEEKS VIEW:

The sudden acceleration lower in JPY that took out last

week’s 1.2565/70 low was clearly unexpected. Further

weakness seems likely but the pace of any decline is likely

to be slower. From here, as long as 1.2580 is not taken out,

we could see another leg lower to 1.2470 before a sustained

rebound can be expected.

Neutral: Shift to bearish only if daily closing below 1.2510.

The unexpected sharp decline in JPY yesterday is currently

holding around the major 1.2510 support (low seen on the

day of Brexit). A daily closing below this level would shift the

current neutral outlook to bearish targeting a move to 1.2380.

This appears to be a likely scenario unless JPY can move a

back above 1.2620 within these few days.

FX Insights Thursday, 01 December 2016 6 | P a g e

USD/MYR: 4.4650

MYR weakened further to 4.467/USD on Wednesday, and ended the month 6.5% lower for the biggest monthly drop since

August 2015 and fifth consecutive monthly decline. Malaysia’s foreign-exchange reserves continue to be supported by sustained

current-account surpluses and FDI inflows which were a buffer against financial-market volatility, whilst depreciation of the MYR

has not led to a material decline in Malaysia’s foreign exchange reserves, Malaysia’s Second Finance Minister Johari Abdul

Ghani said in a statement.

1-3 WEEKS VIEW:

Bullish: Aim for the 2015 high of 4.4770.

USD continues to trade in a narrow range and barring a move below 4.4200, this pair is expected to grind higher towards the

4.4770 high seen in 2015. A clear break above 4.4770 would shift the focus towards the round number psychological level of

4.5000.

USD/THB: 35.70

Thai manufacturing output is projected to climb 1% in 2017 from 0.5% expansion this year, Office of Industrial

Economics said on Wednesday, boosted by a recovering economy, government infrastructure investment, while manufacturing

output in last 2 months of 2016 is expected to be positive, growing 2.5% y/y per month. In separate news, the cabinet gave the

nod on Tuesday to the reinstatement of tourism stimulus measures including a 15,000-baht tax break on domestic tour

packages and hotel accommodation for individual taxpayers.

1-3 WEEKS VIEW:

Neutral: Shift to bullish if daily closing above 35.74.

The strong gains in USD over the past couple of days were unexpected. As noted yesterday, a clear break above last week’s

35.74 high would indicate a resumption of the recent bullish trend (targeting a move to 35.90 and beyond). The prospect for

such a move does not appear to be very high at this stage but upward pressure is expected to grow as long as 35.58 is not

taken out.

USD/CNH: 6.9080

Onshore RMB closed 0,06% firmer at 6.8870/USD in Asia on Wednesday, and offshore CNH rose 0.2% to 6.9001/USD,

helped by recent official comments and a stall in the USD advance. However, both units still ended the month weaker on the

back of the Trump dollar rally, while CFETS RMB index was 0.7% higher for the month in Nov, its second consecutive

monthly gain. In further signs of further tightening of cross border capital flows and dampen depreciation expectations, China

will not approve requests to bring RMB overseas for the purpose of converting into foreign currencies without valid business

reasons, and foreign currencies should be bought in the onshore market, according to a Bloomberg report on Wednesday.

The reports said that PBoC notices cross-border RMB outflows have accelerated of late and RMB withdrawals have been

increasing significantly, replacing FX in capital outflows, and that China will further standardize corporates’ RMB-denominated

outbound direct investment, strengthen inspection on whether deals are real, and develop system for companies to report big

cross-border fund movement for ODI in advance.

1-3 WEEKS VIEW:

Neutral: In a broad 6.8900/6.9400 range.

USD dropped to a low of 6.8939 yesterday, holding comfortably above the low end of our expected sideways trading range of

6.8900/6.9500. The subsequent strong rebound from the low reinforces our current neutral view and we continue to expect

USD to trade sideways for now even though 6.8900/6.9400 should be able to contain the price action.

CNH/SGD: 0.2074

1-3 WEEKS VIEW:

Shift from neutral to bullish: Target a move to 0.2083

The unexpected rally in CNH yesterday took out the strong 0.2067 resistance and is currently holding just below the 0.2076

high seen earlier this month. Based on the impulsive momentum, further up-move seems likely in the days ahead and a break

of 0.2076 could lead to a rapid rise to 0.2083. In other words, the outlook for this pair has shifted to bullish. Support is at the

previous 0.2067 resistance but only a move below 0.2062 would indicate that our bullish expectation is wrong.

FX Insights Thursday, 01 December 2016 7 | P a g e

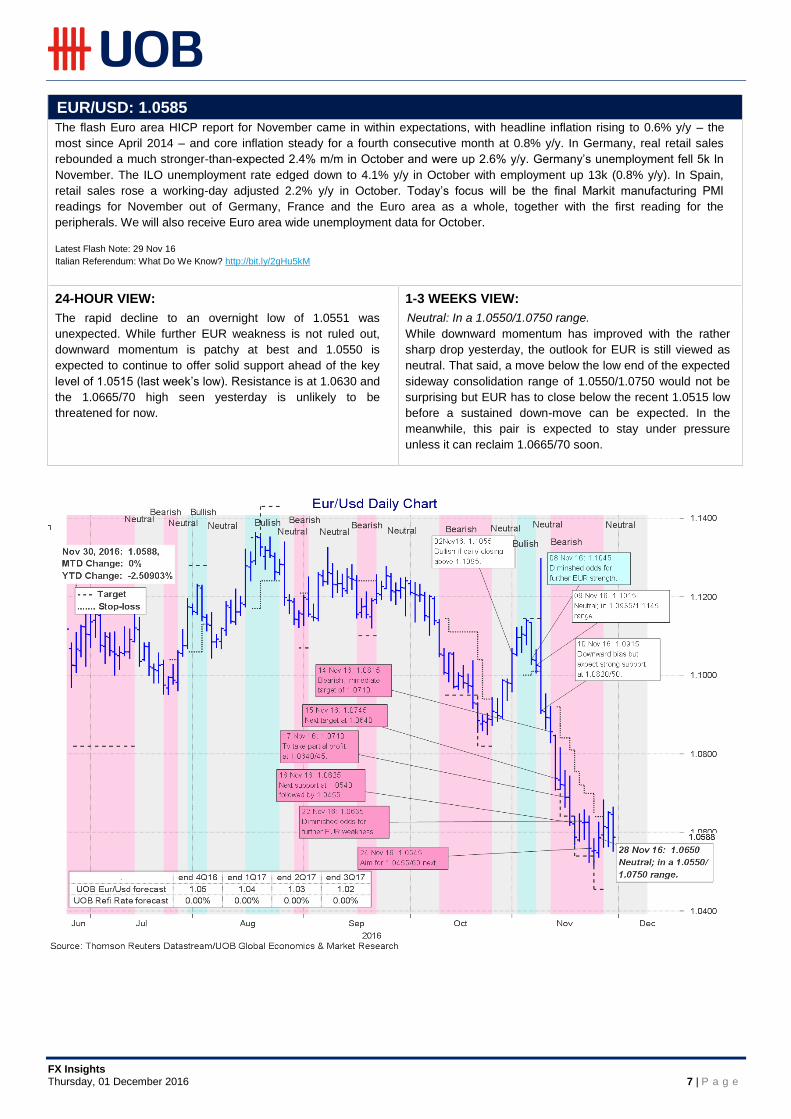

EUR/USD: 1.0585 The flash Euro area HICP report for November came in within expectations, with headline inflation rising to 0.6% y/y – the

most since April 2014 – and core inflation steady for a fourth consecutive month at 0.8% y/y. In Germany, real retail sales

rebounded a much stronger-than-expected 2.4% m/m in October and were up 2.6% y/y. Germany’s unemployment fell 5k In

November. The ILO unemployment rate edged down to 4.1% y/y in October with employment up 13k (0.8% y/y). In Spain,

retail sales rose a working-day adjusted 2.2% y/y in October. Today’s focus will be the final Markit manufacturing PMI

readings for November out of Germany, France and the Euro area as a whole, together with the first reading for the

peripherals. We will also receive Euro area wide unemployment data for October.

Latest Flash Note: 29 Nov 16

Italian Referendum: What Do We Know? http://bit.ly/2gHu5kM

24-HOUR VIEW: 1-3 WEEKS VIEW:

The rapid decline to an overnight low of 1.0551 was

unexpected. While further EUR weakness is not ruled out,

downward momentum is patchy at best and 1.0550 is

expected to continue to offer solid support ahead of the key

level of 1.0515 (last week’s low). Resistance is at 1.0630 and

the 1.0665/70 high seen yesterday is unlikely to be

threatened for now.

Neutral: In a 1.0550/1.0750 range.

While downward momentum has improved with the rather

sharp drop yesterday, the outlook for EUR is still viewed as

neutral. That said, a move below the low end of the expected

sideway consolidation range of 1.0550/1.0750 would not be

surprising but EUR has to close below the recent 1.0515 low

before a sustained down-move can be expected. In the

meanwhile, this pair is expected to stay under pressure

unless it can reclaim 1.0665/70 soon.

FX Insights Thursday, 01 December 2016 8 | P a g e

GBP/USD: 1.2515

GBP/USD has climbed back above the 1.25-level, before easing earlier on Wednesday. The BoE’s published its latest

Financial Stability Report and the results of its latest round of stress tests on Wednesday. According to the report, the BoE

stated that financial stability had been maintained through a challenging period of uncertainty surrounding the domestic and

global economic outlook. The overall vulnerabilities have increased since the July report, primarily due to the EU referendum

outcome. The bank, however, also commented that substantial moves in market prices had not been amplified by the UK

financial system. It added that the overall outlook for financial stability remains challenging. Meanwhile, in the latest stress

tests for the UK banking sector, Royal Bank of Scotland failed the test with failure to meet Tier 1 capital target under adverse

conditions and will need to raise fresh capital. There were also shortcomings in Barclays and Standard Chartered, although

the banks have already taken action and they did not fail the tests. Today, the UK will print the Markit manufacturing PMI for

November.

24-HOUR VIEW: 1-3 WEEKS VIEW:

GBP traded in a choppy manner yesterday; whipsawing

between 1.2419 and 1.2525. While upward momentum is not

strong, the immediate bias is tilted to the upside but at this

stage, a clear break above 1.2550 seems unlikely. Support is

at 1.2460 ahead of the 1.2420.

Neutral: Back in a 1.2300/1.2600 range. [No change in view, see update from yesterday below]

We have held a neutral view on GBP for close to 2 weeks

now. The price action has been choppy but the range for the

past two weeks is well within our expected consolidation

range of 1.2300/1.2600. While shorter-term indicators are

mildly supportive, only a clear break above 1.2600 would

indicate that GBP has moved into a bullish phase. In the

meanwhile, expect further choppy trading between 1.2300

and 1.2600.

FX Insights Thursday, 01 December 2016 9 | P a g e

AUD/USD: 0.7390

AUD/USD was hit by the fall in non-oil commodities, with the pair seen falling below 0.7400. Earlier this morning, Australia’s AiG

performance of manufacturing index increased to 54.2 in November from previous 50.9. Focus now turns to retail sales data for

October early Friday morning. Australian Treasurer Morrison is focusing on the country's oil and gas sector before a final tax

review ahead of the mid-year budget to be presented on 19 December. He said that the country has witnessed a drastic fall in

revenue from both petroleum as well as crude oil taxes, owing to slump in output, besides, fall in global energy prices.

24-HOUR VIEW: 1-3 WEEKS VIEW:

The unexpected break of the major 0.7430 support sent AUD

reeling to a low of 0.7374. The decline appears incomplete

and further weakness towards 0.7355/60 seems likely. Only

a move back above 0.7440 would indicate that the immediate

downward pressure has eased.

Neutral: Back in a 0.7300/0.7500 range.

While the failure to move clearly above 0.7510 was not

unexpected, the sharp drop from the 0.7497 high yesterday

came as a surprise. The bias has shifted to the downside

but any further down-move is expected to encounter solid

support near 0.7300/10 (close to last month’s low). Looking

further ahead, only a clear break below this level would

indicate that AUD has entered a fresh bearish phase. In the

meanwhile, we expect this pair to trade in a 0.7300/0.7500

range.

FX Insights Thursday, 01 December 2016 10 | P a g e

NZD/USD: 0.7080

In data released earlier this morning, New Zealand's merchandise terms of trade fell 1.8% in the third quarter from the second,

as export prices fell more than import prices. According to Statistics New Zealand, the country's terms of trade have now fallen

in four of the last five quarters. Separately, house prices are still rising in most parts of New Zealand, but a trend of slowing

growth is continuing in Auckland, Hamilton and Christchurch, according to QV. This has led to a slower rate of growth

nationally. The latest monthly QV house price index shows nationwide residential property values as of November had

increased 12.4% in the past year, which is the slowest rate annualized growth rate since May 2016.

24-HOUR VIEW: 1-3 WEEKS VIEW:

While the major 0.7190 resistance capped as expected, the

sharp drop from the high of 0.7170 was surprising. The

down-move appears to be running ahead of itself but another

leg lower to test 0.7050 support seems likely. Resistance is

at 0.7110 followed by 0.7140. The 0.7170 is not expected to

come into the picture for today.

Neutral: Back in a 0.7000/0.7150 range.

While NZD rallied strongly yesterday and touched a high of

0.7170, it surrendered most of its gains by end of the day. As

noted, only a daily closing above 0.7150 would shift the

outlook for NZD to bullish and this has clearly not happened.

To put it another way, the outlook for NZD remains neutral

for now and we are back into a 0.7000/0.7150 sideways

trading range.

FX Insights Thursday, 01 December 2016 11 | P a g e

USD/JPY: 114.40

The big mover on oil as the risk on trade comes back in favour of the USD/JPY has pushed the pair above 114.00 for the first

time since February. Meanwhile, capital spending in Japan was down 1.3% on quarter in 3Q16.That missed expectations for a

fall of 0.4% following the 3.1% gain in the three months prior. Excluding software, capex was down 1.4% versus expectations

for a decline of 0.06% after the 3.1% jump in 2Q. Separately, the Nikkei Japan manufacturing PMI slowed marginally to 51.3 in

November from October's 51.4, showing expansion for the third month in a row.

24-HOUR VIEW: 1-3 WEEKS VIEW:

The massive rally is clearly overbought but in view of the

impulsive momentum, it is premature to expect a sustained

pull-back. USD could gravitate towards 115.00 but this is

rather strong level and may not be easy to crack. Support is

at 114.00 followed by 113.60.

Shift from neutral to bullish: Over-extended but room for

further gains to 115.60.

The sudden surge in USD yesterday that took out the recent

high of 113.89 was unexpected. The very strong daily closing

suggests that the current movement is the start of a fresh

bullish phase. From a shorter-term perspective, the up-move

is severely over-extended but there appears to be room for

further gains towards 115.60 (61.8% retracement of the 1-

year decline from 125.85, June 2015 to 99.08, June 2016). In

order to maintain the current overbought momentum, any

pull-back should not move back below 113.20.

Disclaimer: This analysis is based on information available to the public. Although the information contained herein is believed to be reliable, UOB

Group makes no representation as to the accuracy or completeness. Also, opinions and predictions contained herein reflect our opinion as of date

of the analysis and are subject to change without notice. UOB Group may have positions in, and may effect transactions in, currencies and financial

products mentioned herein. Prior to entering into any proposed transaction, without reliance upon UOB Group or its affiliates, the reader should

determine, the economic risks and merits, as well as the legal, tax and accounting characterizations and consequences, of the transaction and that

the reader is able to assume these risks. This document and its contents are proprietary information and products of UOB Group and may not be

reproduced or otherwise.

Singapore Company Reg No. 193500026Z

Last updated on 17 Nov 16

*Meetings associated with a Summary of Economic Projections and a press conference. #Meetings associated with release of Inflation Report.

^Meetings associated with release of Monetary Policy Statement. %

Meetings associated with release of Outlook Report.

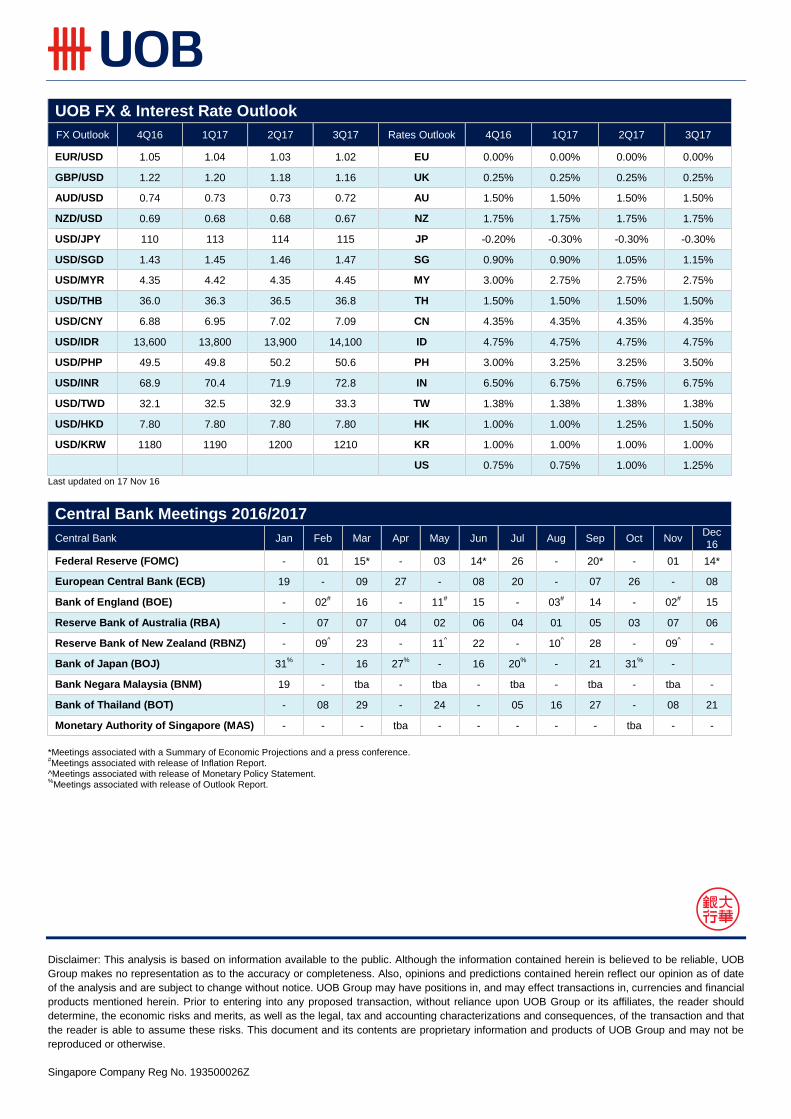

UOB FX & Interest Rate Outlook

FX Outlook 4Q16 1Q17 2Q17 3Q17 Rates Outlook 4Q16 1Q17 2Q17 3Q17

EUR/USD 1.05 1.04 1.03 1.02 EU 0.00% 0.00% 0.00% 0.00%

GBP/USD 1.22 1.20 1.18 1.16 UK 0.25% 0.25% 0.25% 0.25%

AUD/USD 0.74 0.73 0.73 0.72 AU 1.50% 1.50% 1.50% 1.50%

NZD/USD 0.69 0.68 0.68 0.67 NZ 1.75% 1.75% 1.75% 1.75%

USD/JPY 110 113 114 115 JP -0.20% -0.30% -0.30% -0.30%

USD/SGD 1.43 1.45 1.46 1.47 SG 0.90% 0.90% 1.05% 1.15%

USD/MYR 4.35 4.42 4.35 4.45 MY 3.00% 2.75% 2.75% 2.75%

USD/THB 36.0 36.3 36.5 36.8 TH 1.50% 1.50% 1.50% 1.50%

USD/CNY 6.88 6.95 7.02 7.09 CN 4.35% 4.35% 4.35% 4.35%

USD/IDR 13,600 13,800 13,900 14,100 ID 4.75% 4.75% 4.75% 4.75%

USD/PHP 49.5 49.8 50.2 50.6 PH 3.00% 3.25% 3.25% 3.50%

USD/INR 68.9 70.4 71.9 72.8 IN 6.50% 6.75% 6.75% 6.75%

USD/TWD 32.1 32.5 32.9 33.3 TW 1.38% 1.38% 1.38% 1.38%

USD/HKD 7.80 7.80 7.80 7.80 HK 1.00% 1.00% 1.25% 1.50%

USD/KRW 1180 1190 1200 1210 KR 1.00% 1.00% 1.00% 1.00%

US 0.75% 0.75% 1.00% 1.25%

Central Bank Meetings 2016/2017

Central Bank Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec 16

Federal Reserve (FOMC) - 01 15* - 03 14* 26 - 20* - 01 14*

European Central Bank (ECB) 19 - 09 27 - 08 20 - 07 26 - 08

Bank of England (BOE) - 02# 16 - 11

# 15 - 03

# 14 - 02

# 15

Reserve Bank of Australia (RBA) - 07 07 04 02 06 04 01 05 03 07 06

Reserve Bank of New Zealand (RBNZ) - 09^ 23 - 11

^ 22 - 10

^ 28 - 09

^ -

Bank of Japan (BOJ) 31% - 16 27

% - 16 20

% - 21 31

% -

Bank Negara Malaysia (BNM) 19 - tba - tba - tba - tba - tba -

Bank of Thailand (BOT) - 08 29 - 24 - 05 16 27 - 08 21

Monetary Authority of Singapore (MAS) - - - tba - - - - - tba - -