USA Technologies September 2015 Investor Presentation...

34

USA Technologies Investor Presentation September 2015 NASDAQ: USAT

Transcript of USA Technologies September 2015 Investor Presentation...

USA Technologies

Investor Presentation

September 2015

NASDAQ: USAT

Safe Harbor Statement

2

All statements, other than statements of historical fact included in this presentation, are forward-looking statements. When used in this release, words such as "anticipate", "believe", "estimate", "expect", "intend", and similar expressions, as they relate to USA Technologies or its management, identify forward-looking statements. Such forward-looking statements are based on the beliefs of USA Technologies’ management, as well as assumptions made by and information currently available to USA Technologies’ management. Actual results could differ materially from those contemplated by the forward-looking statements as a result of certain factors, including but not limited to, business, financial market and economic conditions; the incurrence of any unanticipated or unusual non-operating expenses which would require diversion of cash resources; the ability of USA Technologies to predict or estimate its future quarterly or annual revenues and expenses given the developing and unpredictable market for its products; the ability of USA Technologies to retain key customers from whom a significant portion of its revenues are derived; the ability of a key customer to reduce or delay purchasing products from USA Technologies; whether suppliers would increase their prices, reduce output or change their terms of sale; whether, and the promptness with which, customers install new connections; whether, and the extent to which, new connections will generate new revenues for USA Technologies in future quarters; whether USA Technologies’ customers continue to utilize USA Technologies’ transaction processing and related services, as customer agreements are generally cancelable by the customer on thirty to sixty days' notice; the ability of USA Technologies to accurately estimate potential connections controlled by its existing customer base and predict future market conditions and customer behavior; whether customers will increase their purchases of USA Technologies’ products and services in the future; the extent to which USAT's 2015 Cashless Knowledge Base is predictive of average annual cash and cashless sales and top line cashless sales lift on a single vending machine; the ability of the Company’s 2015 Cashless Knowledge Base to predict future market conditions, customer and consumer behavior, and average ticket prices and cashless sales across all of USAT's customer locations; the accuracy and reliability of third party data relating to industry net operating profits and cost of goods sold; and the possibility that all of the expected benefits from adoption of cashless payment will not be realized by all vending operators, or will not be realized within the expected time period. Readers are cautioned not to place undue reliance on these forward-looking statements. Any forward-looking statement made in this presentation speaks only as of the date of this presentation. Unless required by law, USA Technologies does not undertake to release publicly any revisions to these forward-looking statements to reflect future events or circumstances or to reflect the occurrence of unanticipated events.

Non-GAAP Information: This presentation includes a discussion of non-GAAP net income (loss) and Adjusted EBITDA which are non-GAAP financial

measures that USA Technologies believes are useful for an understanding of the Company’s ongoing operations. These non-GAAP financial measures

are supplemental to, and not a substitute for, GAAP financial measures such as operating margin or net income or loss. Details of these items and

a reconciliation of these non-GAAP financial measures to GAAP financial measures can be found in the Appendix to this presentation, and at

www.USAT.com under the “Investor Relations” tab.

Investment Highlights

3

Market and technology leader of cashless payment services in self-serve retail

market

Large penetration opportunity in U.S. vending and adjacent vertical market

segments

Trajectory to reach 500 thousand connections in FY 2017 as connections generate

recurring revenue

Revenue growth accelerated at 26% 3 year CAGR

Anticipated free cash flow from operations on a go forward basis

Management team with deep relevant experience

Federal NOLs may shield over $100 million in net income

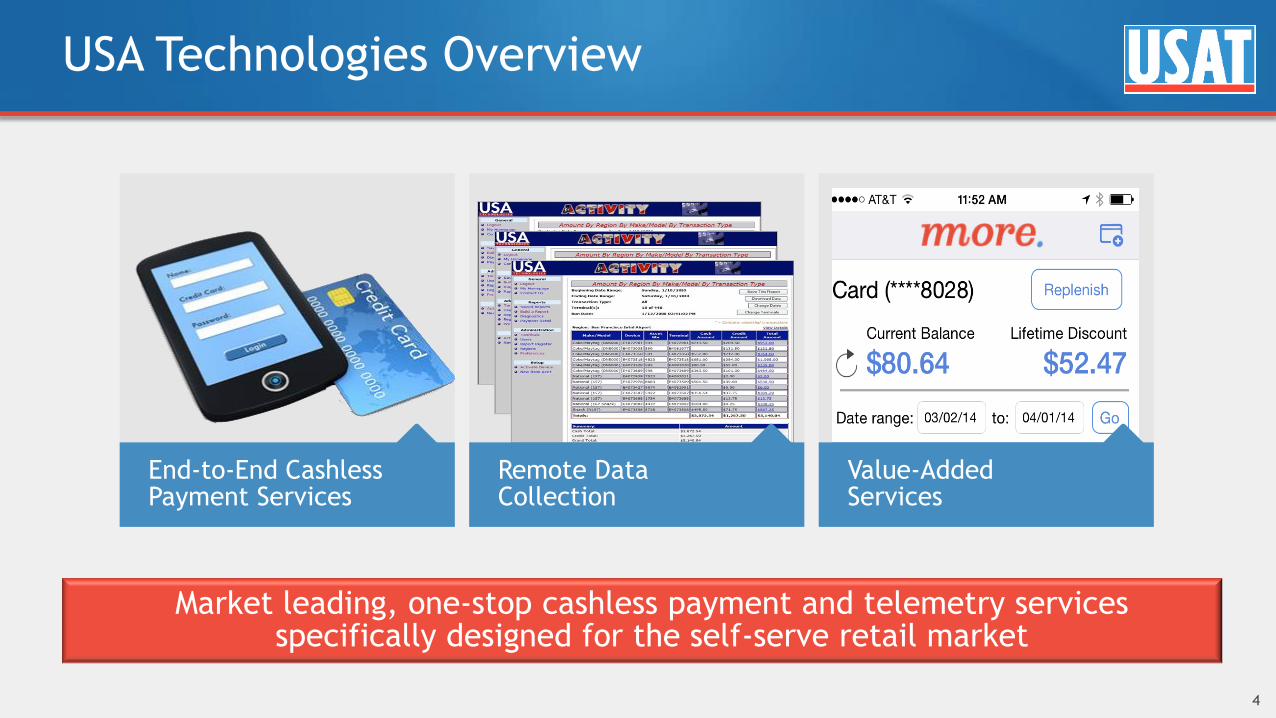

USA Technologies Overview

4

End-to-End Cashless Payment Services

Remote Data Collection

Value-Added Services

Market leading, one-stop cashless payment and telemetry services specifically designed for the self-serve retail market

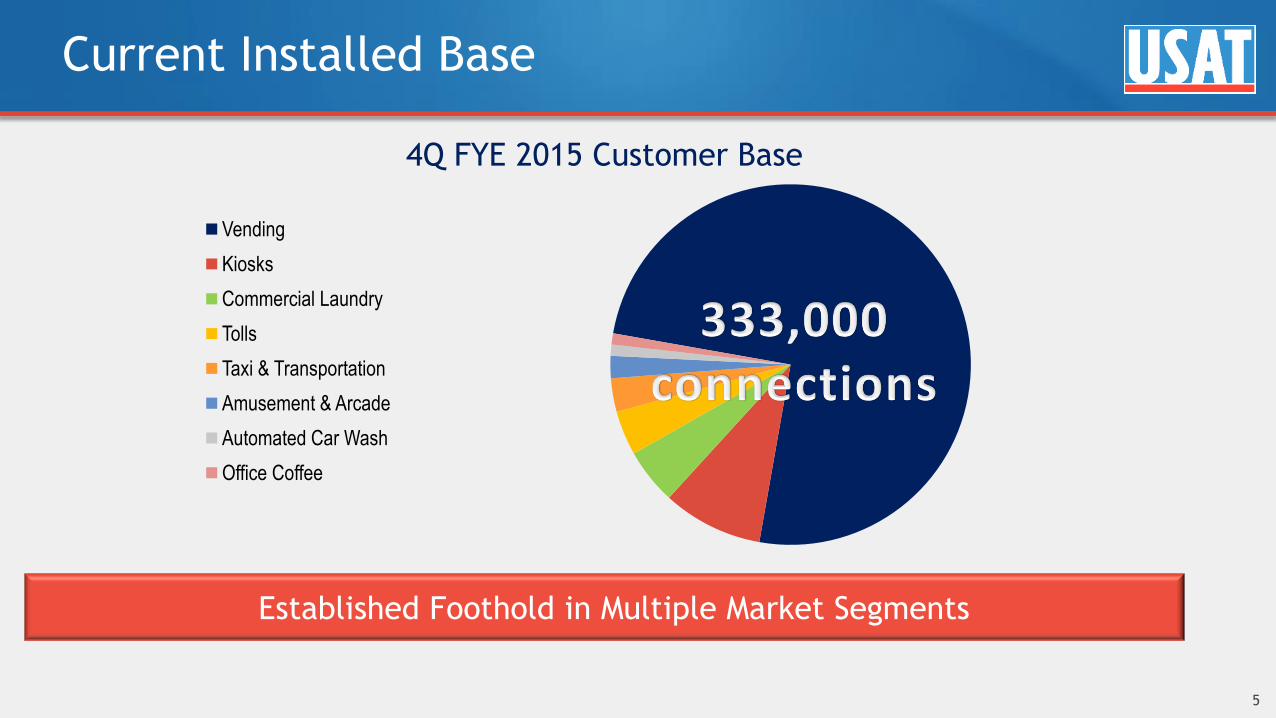

Current Installed Base

5

Vending

Kiosks

Commercial Laundry

Tolls

Taxi & Transportation

Amusement & Arcade

Automated Car Wash

Office Coffee

4Q FYE 2015 Customer Base

Established Foothold in Multiple Market Segments

Large Domestic Opportunity

6

Vending

Kiosks*

Commercial Laundry

Tolls

Taxi & Transportation

Amusement & Arcade

Automated Car Wash

Office Coffee

Self-Serve Retail Market

Sources: US Department of Transportation, 2008; IHL Kiosk Study, 2010 (2011 projections) First Research, March 2011, June 2010; Automatic Merchandisers State of the Coffee Industry 2009; Vending Times Census 2012; Smart Card Alliance 2006

Established Foothold in Multiple Market Segments

National Vending Trends

7

The 2015 USA Technologies’ KnowledgeBase shows vending consumers continue

to buy more, spend more and buy more often with credit and debit cards on

ePort-equipped machines.

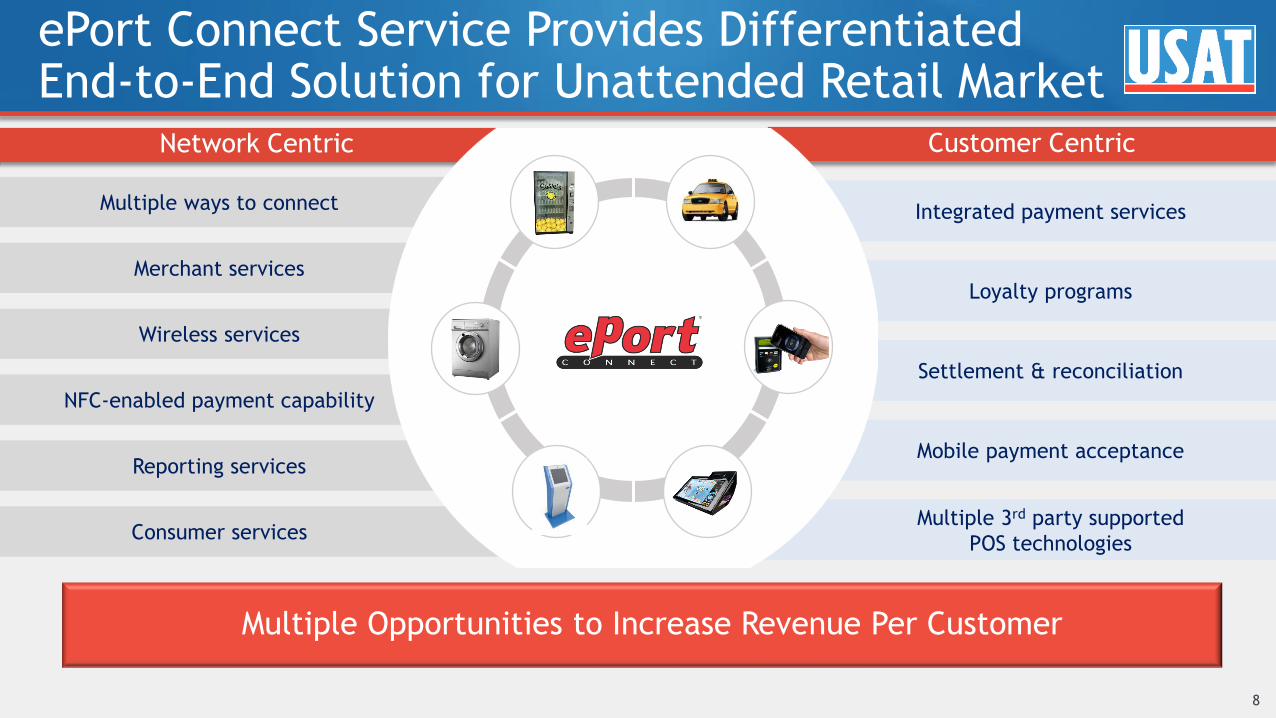

Network Centric

Multiple 3rd party supported

POS technologies

Mobile payment acceptance

Settlement & reconciliation

Loyalty programs

Integrated payment services

Consumer services

Reporting services

NFC-enabled payment capability

Wireless services

Merchant services

Multiple ways to connect

ePort Connect Service Provides Differentiated End-to-End Solution for Unattended Retail Market

8

Multiple Opportunities to Increase Revenue Per Customer

Customer Centric

Investment in Self Service

9

Significant companies partnering or working with USAT

Largest NFC-enabled Mobile Footprint

10

~300,000 NFC-enabled merchant locations,

90% of installed base

− All newly shipped ePort terminals are

NFC-enabled

Apple Pay introduction marks tectonic

shift, expected to drive demand and

adoption

− Accepted throughout USAT network

Google’s launch of Android Pay solidifies

broader market acceptance of the mobile

payments technology

Equipment

11

Sample USAT Customer Economics ePort Connect monthly service fee

– $7 - $10 per connection per month

– $12 - $15 per connection per month including terminal rental

Transaction processing fees

– 3 - 5.95% per transaction

Target gross profit margin

Target gross profit margin

Revenue Model

$6,426 $5,646 $5,896 $6,706

$14,444

$16,442

$23,371

$30,139

$35,638

$43,633

FY11 FY12 FY13 FY14 FY15 $0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000 Equipment Revenues

License & Trans. Fees

Revenue

~68% Recurring & Re-occuring Revenue

Business Model

($/000’s)

The Data: One Machine at a Time

12

Original pre cashless machine:

– Annual cash sales = $7,831 a year (average)

Machine sales with E-Port installation (after 12 months deployed):

– Total annual sales = $9,397 a year ($1,566 in new revenue)

– Cashless sales = $3,477 a year (37% of total sales)

– Incremental sales = $1,566 (20% Top line Sales Lift)*

– Incremental Net Operating Profit = $380

Notes:

* Top Line Sales Lift reported by USAT customers

Vending machine economics…

By using the new QuickStart program, vending machine operators

can make an additional $380 per year or over 240% increase in net

operating profit with no up front investment

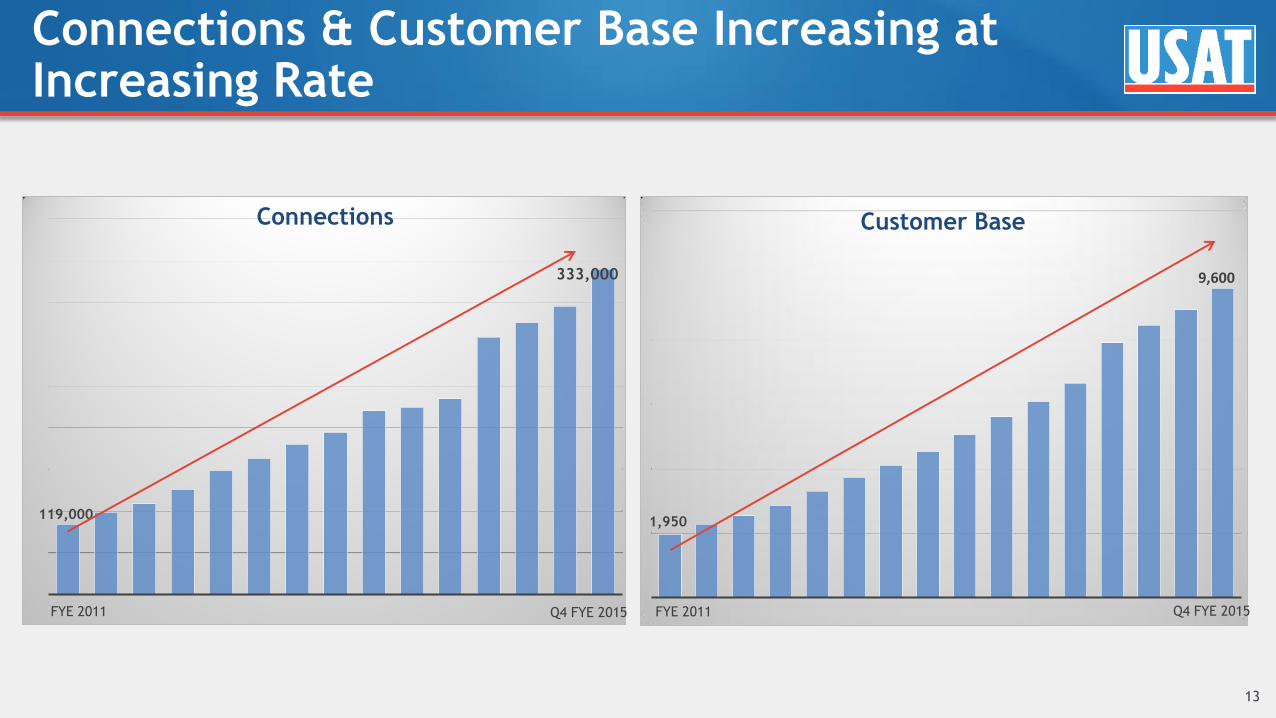

Connections & Customer Base Increasing at Increasing Rate

13

Wikianswers.com

1,950

9,600

FYE 2011

Customer Base

119,000

333,000

Connections

FYE 2011 Q4 FYE 2015 Q4 FYE 2015

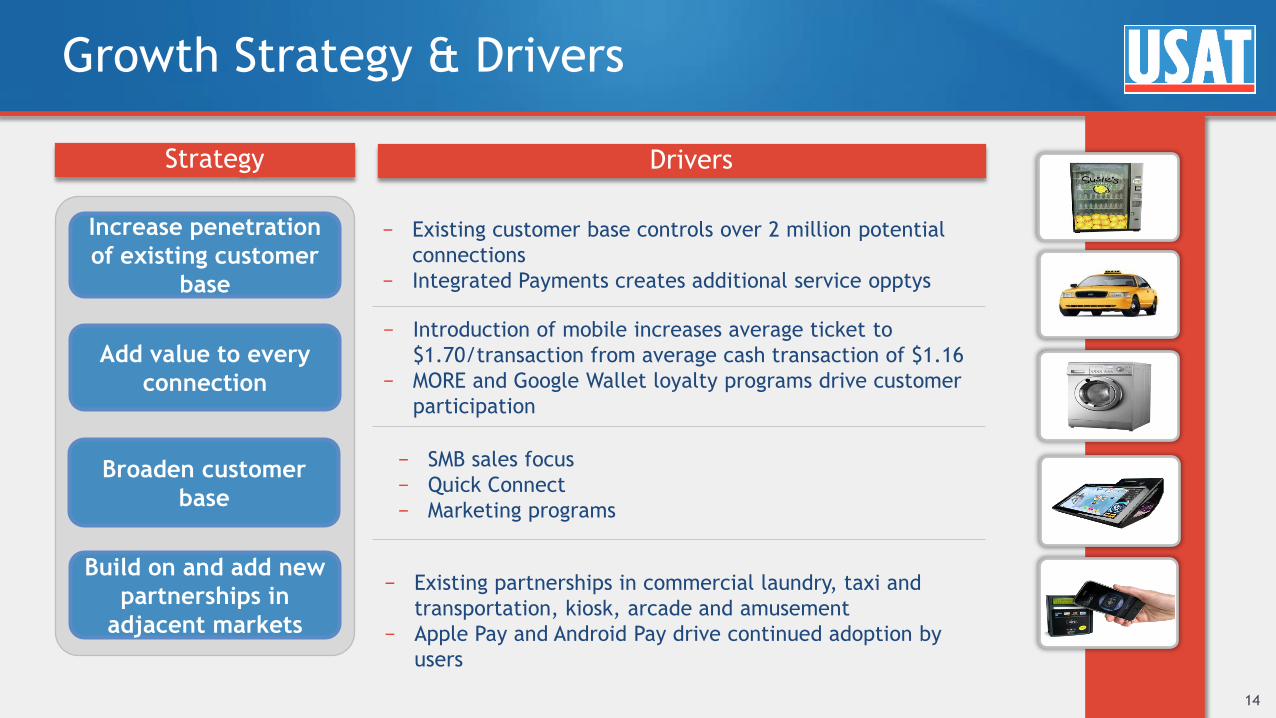

Growth Strategy & Drivers

14

− Existing customer base controls over 2 million potential

connections

− Integrated Payments creates additional service opptys

− SMB sales focus

− Quick Connect

− Marketing programs

− Existing partnerships in commercial laundry, taxi and

transportation, kiosk, arcade and amusement

− Apple Pay and Android Pay drive continued adoption by

users

− Introduction of mobile increases average ticket to

$1.70/transaction from average cash transaction of $1.16

− MORE and Google Wallet loyalty programs drive customer

participation

Increase penetration

of existing customer

base

Broaden customer

base

Build on and add new

partnerships in

adjacent markets

Add value to every

connection

Strategy Drivers

Competitive Advantage: Integrated Payment Services

15

Traditional Vending Cashless driving positive

returns

Mobile Payments ePort Mobile: delivery,

concessions and OCS

Dining Services Streamline payments for

dining halls, cafeterias

Online Payment Process cc in USALive; schedule

repeat transactions

Micro-Markets Process payments;

Extend loyalty program

Deepens Customer Entrenchment and Maximizes Revenue per Customer

Delivery of end-to-end solution enables consolidated reporting across multiple cashless point-of-

sale locations

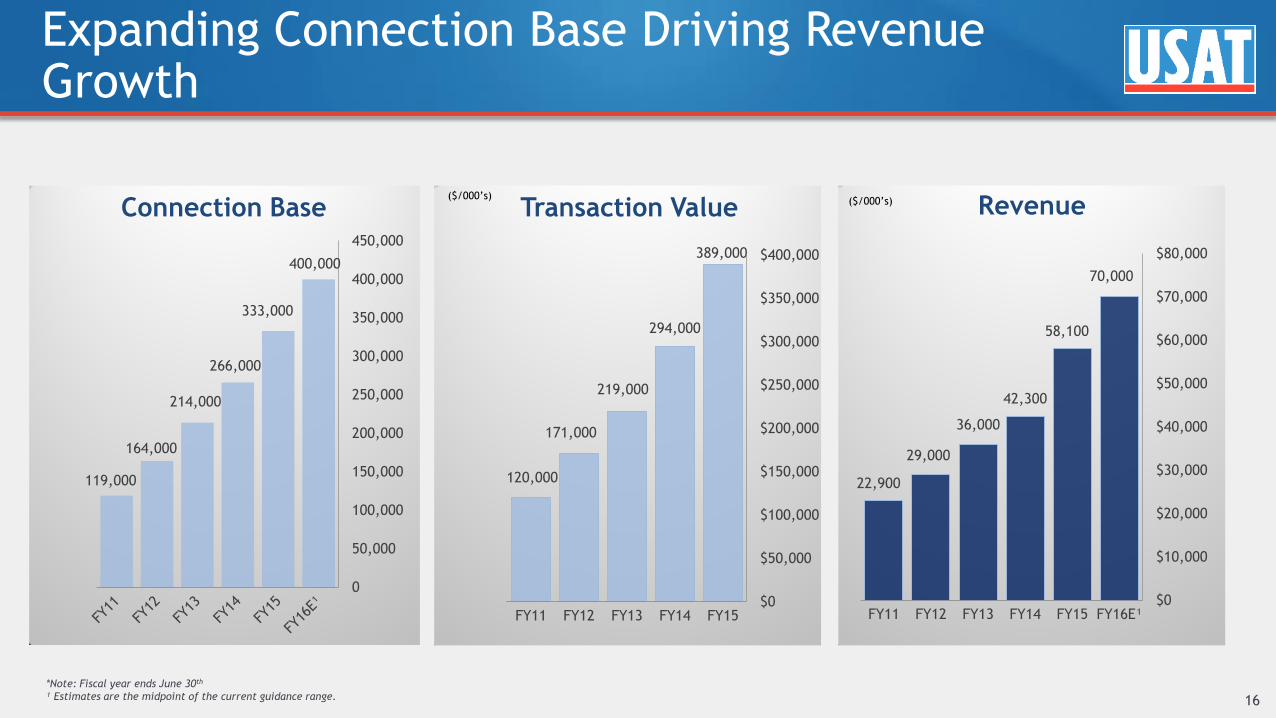

Expanding Connection Base Driving Revenue Growth

120,000

171,000

219,000

294,000

389,000

FY11 FY12 FY13 FY14 FY15 $0

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

$350,000

$400,000

22,900

29,000

36,000

42,300

58,100

70,000

FY11 FY12 FY13 FY14 FY15 FY16E¹ $0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

$70,000

$80,000

16

Revenue

119,000

164,000

214,000

266,000

333,000

400,000

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

Connection Base Transaction Value ($/000’s)

($/000’s)

*Note: Fiscal year ends June 30th

¹ Estimates are the midpoint of the current guidance range.

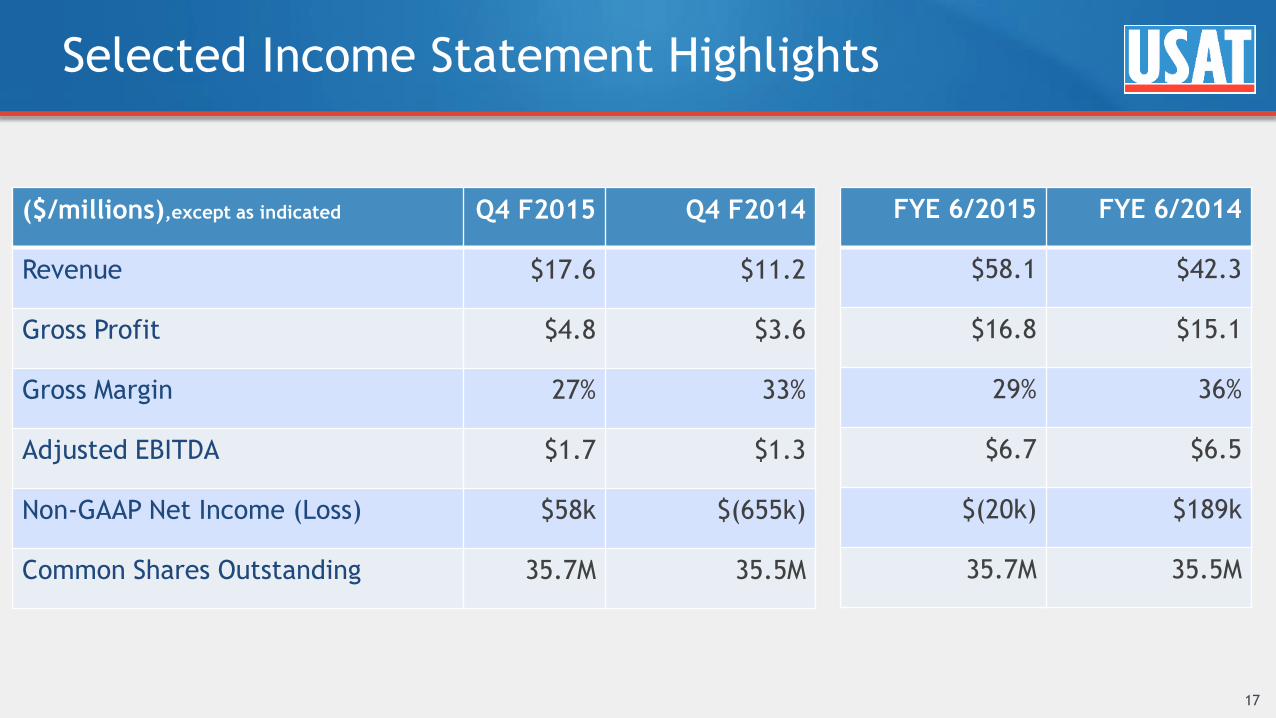

Selected Income Statement Highlights

17

($/millions),except as indicated Q4 F2015 Q4 F2014

Revenue $17.6 $11.2

Gross Profit $4.8 $3.6

Gross Margin 27% 33%

Adjusted EBITDA $1.7 $1.3

Non-GAAP Net Income (Loss) $58k $(655k)

Common Shares Outstanding 35.7M 35.5M

FYE 6/2015 FYE 6/2014

$58.1 $42.3

$16.8 $15.1

29% 36%

$6.7 $6.5

$(20k) $189k

35.7M 35.5M

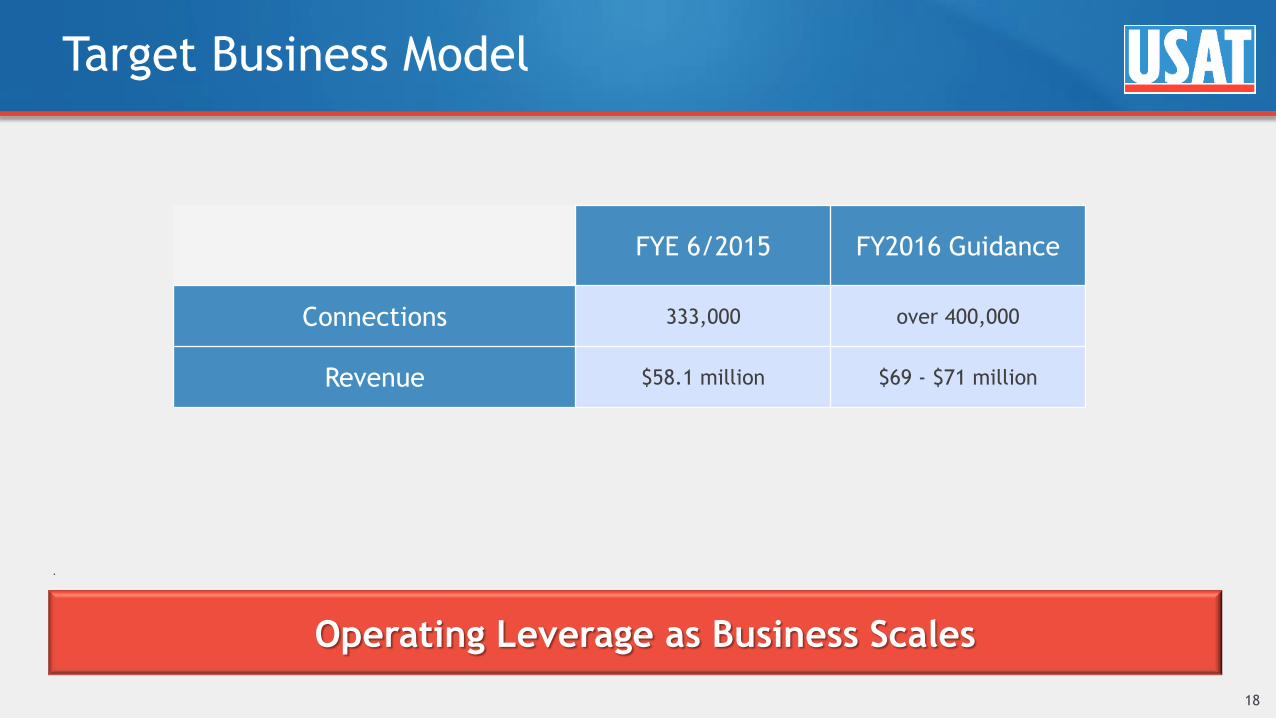

Target Business Model

18

FYE 6/2015 FY2016 Guidance

Connections 333,000 over 400,000

Revenue $58.1 million $69 - $71 million

.

Operating Leverage as Business Scales

Management Team

19

Stephen P. Herbert

Chairman and CEO

Chairman and CEO since 2011

President and COO from 1999

Operations, Sales and Marketing at PepsiCo including market

strategy for vending and retail channels of Pepsi Cola N.A.

David M. DeMedio

Chief Service Officer

Former Chief Financial Officer

Controller and Director of Network and Financial Services from

1999

Accounting Supervisor, Elko, Fischer, Cunnane and Assoc., LLC

Certified Public Accountant

J. Duncan Smith

CFO

Appointed CFO in August 2015

CFO of Bryn Mawr Bank Corp 2005-2015

Led 8 Acquisitions in 10 years at Bryn Mawr

Certified Public Accountant

George Harrum

SVP Operations

SVP Operations and Customer Service since 2001

Various Operations Positions, Danyl/Schlumberger from 1982

Michael K. Lawlor

SVP Sales & Business

Development

SVP Sales and Business Development since 2010

Sales and partner development programs from 1996

National and Regional sales manager positions, Pepsi Cola Co.

Maeve McKenna Duska

SVP Marketing

Senior Vice President Marketing since 2015

Vice President Marketing from 2009

Marketing for all products and services for flagship ePort

branded services from 2004

Marketing Manager, Higher Education, Aramark

Key Takeaways

Market and technology leader of cashless payment services in self-serve retail market

Large penetration opportunity in U.S. vending and adjacent vertical market segments

Trajectory to reach 500 thousand connections in FY 2017 as connections generate recurring revenue

Revenue growth expected to accelerate from 26% 3 year CAGR

Anticipated free cash flow from operations on a go forward basis

Management team with deep relevant experience

Federal NOLs may shield over $100 million in net income

20

Appendix A: Condensed Financial and Other Data

21

The Data: One Machine at a Time

22

Illustration of one

machine

September 16, 2015

Base Case - Cash Only Machine:

Annual Cash Sales (1) 7,831$

Annual Cash Only Net Operating Profit 157$ 2%

Add Cashless Option to Machine:

Annual Cash Sales 7,831$

Incremental Sales (2) 1,566 (20% top line sales increase)

Total Sales (3) 9,397$ 100%

Cashless Sales 3,477$ 37%

Cost to Deliver Incremental Sales (4) 877$

All in Cashless Costs (5) 309

Total Costs - Incremental 1,186$

Incremental Sales 1,566$

Incremental Costs 1,186

Incremental Net Operating Profit (6) 380$ 4%

Incremental Net Operating Profit 380$

Annual Cash Only Net Operating Profit 157

Total Net Operating Profit 537$

Increase in Net Operating Profit 380$ 242%

(1) Total average cashless and cash sales of $9,397 less assummed 20% cashless sales lift of $1,566

(2) Top Line Sales Lift representing sales lift budgeted for the upcoming year by a USAT customer

(3) Represents average annualized sales computed from the Company's 2015 Knowledge Base

(4) NAMA industry data for cost of goods sold + sales tax + commissions = 56%

(5)

(6) NAMA industry data for the vending industry has NOP at <2%

Cashless costs include transaction & monthly service fees.

5 Quarter Connections & Other Data

23

Three months ended Three months ended Three months ended Three months ended Three months ended

June 30, March 31, December 31, September 30, June 30,

2015 2015 2015 2015 2014

Connections:

Gross New Connections 34,000 24,000 14,000 13,000 25,000

% from Existing Customer Base 89% 82% 82% 84% 84%

Net New Connections 31,000 14,000 12,000 10,000 22,000

Total Connections 333,000 302,000 288,000 276,000 266,000

Customers:

New Customers Added 675 475 550 600 650

Total Customers 9,600 8,925 8,450 7,900 7,300

Volumes:

Total Number of Transactions (mill ions) 62.2 54.8 51.0 48.7 47.0

Transaction Volume ($millions) $112.8 $97.7 $89.3 $89.2 $82.9

Financing Structure of Connections:

JumpStart 3.8% 16.5% 14.4% 22.7% 56.4%

QuickStart & All Others 96.2% 83.5% 85.6% 77.30% 43.6%

Total 100.0% 100.0% 100.0% 100.0% 100.0%

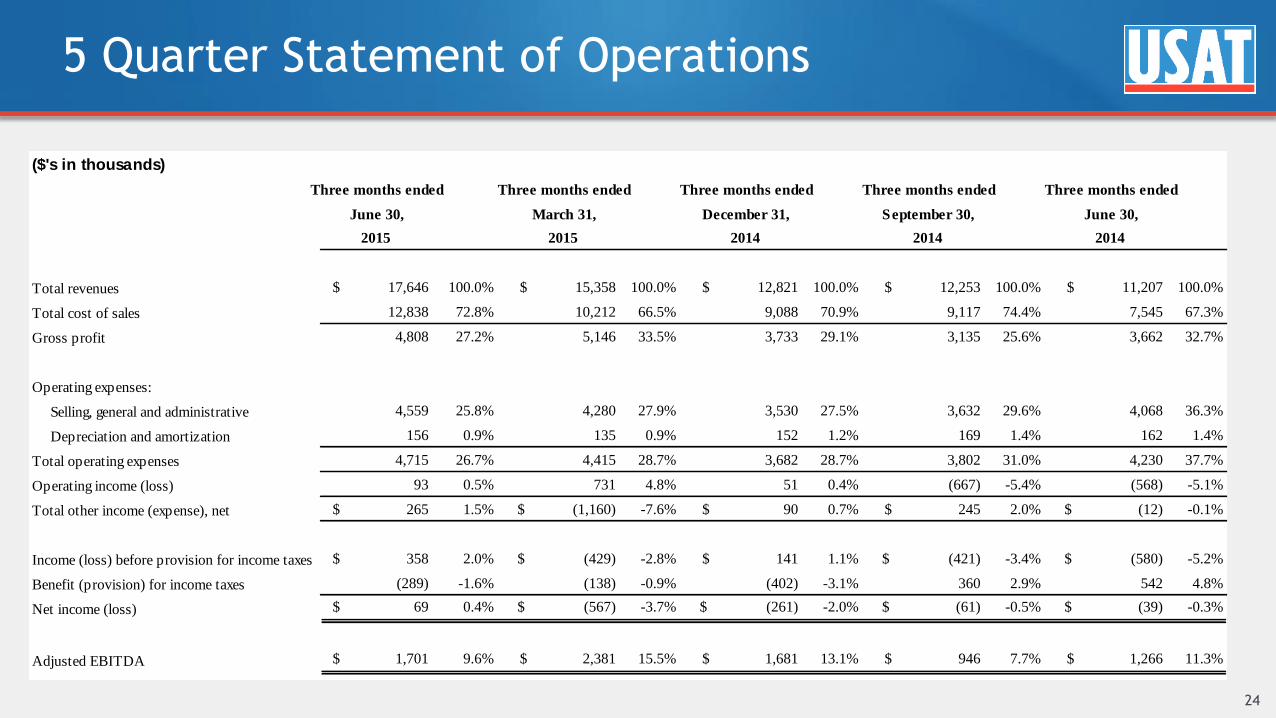

5 Quarter Statement of Operations

24

($'s in thousands)

Three months ended Three months ended Three months ended Three months ended Three months ended

June 30, March 31, December 31, September 30, June 30,

2015 2015 2014 2014 2014

Total revenues $ 17,646 100.0% $ 15,358 100.0% $ 12,821 100.0% $ 12,253 100.0% $ 11,207 100.0%

Total cost of sales 12,838 72.8% 10,212 66.5% 9,088 70.9% 9,117 74.4% 7,545 67.3%

Gross profit 4,808 27.2% 5,146 33.5% 3,733 29.1% 3,135 25.6% 3,662 32.7%

Operating expenses:

Selling, general and administrative 4,559 25.8% 4,280 27.9% 3,530 27.5% 3,632 29.6% 4,068 36.3%

Depreciation and amortization 156 0.9% 135 0.9% 152 1.2% 169 1.4% 162 1.4%

Total operating expenses 4,715 26.7% 4,415 28.7% 3,682 28.7% 3,802 31.0% 4,230 37.7%

Operating income (loss) 93 0.5% 731 4.8% 51 0.4% (667) -5.4% (568) -5.1%

Total other income (expense), net $ 265 1.5% $ (1,160) -7.6% $ 90 0.7% $ 245 2.0% $ (12) -0.1%

Income (loss) before provision for income taxes $ 358 2.0% $ (429) -2.8% $ 141 1.1% $ (421) -3.4% $ (580) -5.2%

Benefit (provision) for income taxes (289) -1.6% (138) -0.9% (402) -3.1% 360 2.9% 542 4.8%

Net income (loss) $ 69 0.4% $ (567) -3.7% $ (261) -2.0% $ (61) -0.5% $ (39) -0.3%

Adjusted EBITDA $ 1,701 9.6% $ 2,381 15.5% $ 1,681 13.1% $ 946 7.7% $ 1,266 11.3%

5 Quarter Revenues, Cost of Sales and Gross Profit

25

($'s in thousands)

Adjusted

Three months ended Three months ended Three months ended Three months ended Three months ended

June 30, March 31, December 31, September 30, June 30,

2015 2015 2014 2014 2014

Revenues:

License and transaction fees 11,938 67.7% 11,060 72.0% 10,479 81.7% 10,156 82.9% 9,460 84.4%

Equipment Sales 5,708 32.3% 4,298 28.0% 2,341 18.3% 2,096 17.1% 1,747 15.6%

Total revenue 17,646 100.0% 15,358 100.0% 12,821 100.0% 12,253 100.0% 11,207 100.0%

Cost of sales:

License and transaction fees 7,863 65.9% 7,157 64.7% 7,158 68.3% 7,251 71.4% 6,327 66.9%

Equipment Sales 4,975 87.2% 3,054 71.1% 1,930 82.4% 1,866 89.0% 1,218 69.7%

Total cost of sales 12,838 72.8% 10,212 66.5% 9,088 70.9% 9,117 74.4% 7,545 67.3%

Gross Profit:

License and transaction fees 4,075 34.1% 3,903 35.3% 3,322 31.7% 2,905 28.6% 3,133 33.1%

Equipment Sales 733 12.8% 1,244 28.9% 412 17.6% 230 11.0% 529 30.3%

Total Gross Profit 4,808$ 27.2% 5,146$ 33.5% 3,733$ 29.1% 3,135$ 25.6% 3,662$ 32.7%

5 Quarter Balance Sheet and Cash Flow Highlights

26

($'s in thousands)

At or for the quarter ended: June 30, March 31, December 31, September 30, June 30,

2015 2015 2014 2014 2014

Cash 11,374$ 8,475$ 6,734$ 10,916$ 9,072$

Finance Receivables - Current 941$ 750$ 363$ 279$ 120$

Finance Receivables - Non-Current 3,698 3,505 1,643 949 353

Total Finance Receivables 4,639$ 4,255$ 2,006$ 1,228$ 473$

Jump Start Rental Equipment 11,993$ 12,566$ 15,300$ 16,593$ 19,824$

Deprecation Expense on Rental Equipment 1,205$ 1,279$ 1,272$ 1,285$ 1,376$

Net cash provided by (used in) operating activities 2,681$ 65$ (3,039)$ (1,405)$ 2,267$

Cash Used for Purchase of Property for Rental Program - - - (1,642) (3,672)

Free Cash Flow 2,681$ 65$ (3,039)$ (3,047)$ (1,404)$

Appendix B: Supplemental Financials and Non-GAAP

Tables

27

5 Quarter Statement of Operations

28

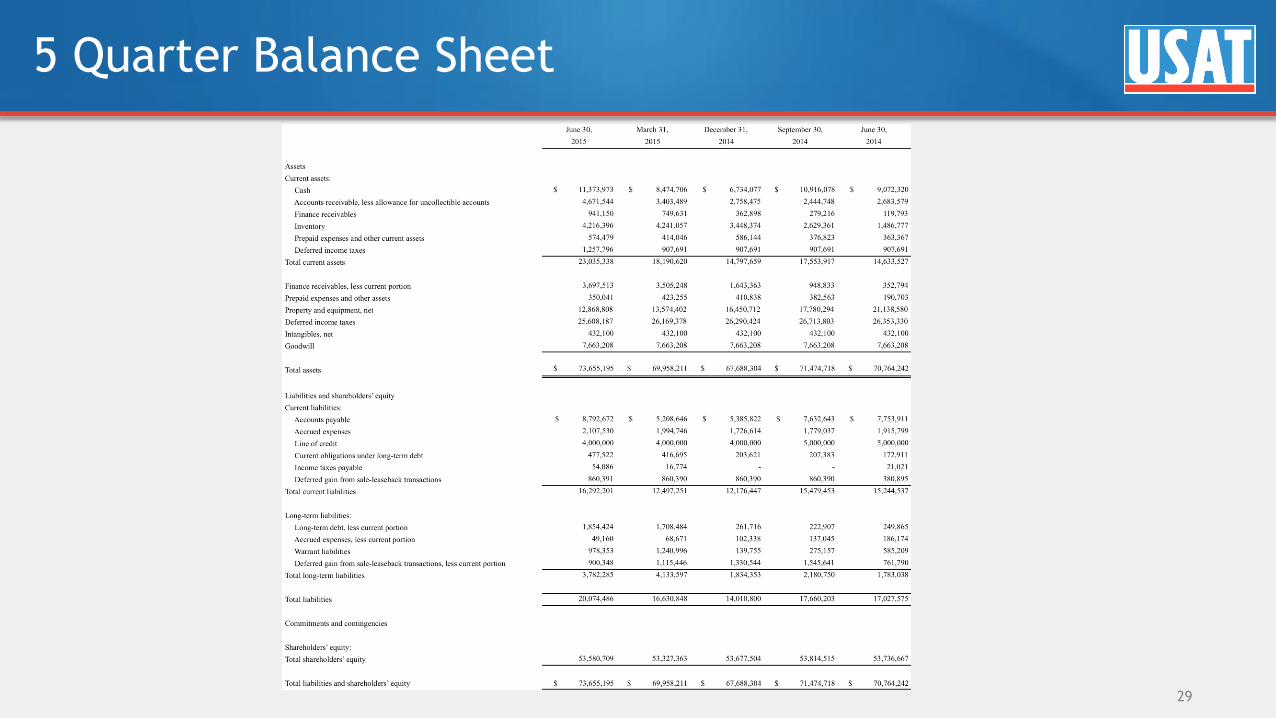

5 Quarter Balance Sheet

29

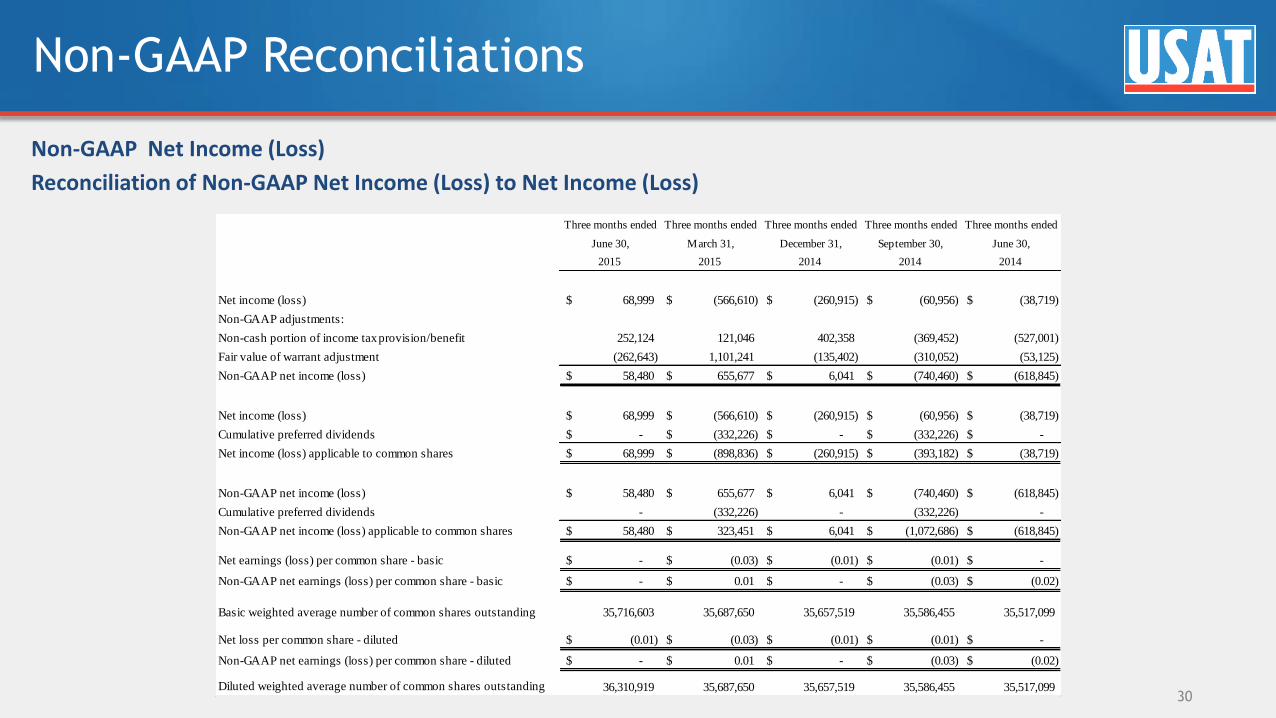

Non-GAAP Reconciliations

Non-GAAP Net Income (Loss)

Reconciliation of Non-GAAP Net Income (Loss) to Net Income (Loss)

30

Three months ended Three months ended Three months ended Three months ended Three months ended

June 30, March 31, December 31, September 30, June 30,

2015 2015 2014 2014 2014

Net income (loss) 68,999$ (566,610)$ (260,915)$ (60,956)$ (38,719)$

Non-GAAP adjustments:

Non-cash portion of income tax provision/benefit 252,124 121,046 402,358 (369,452) (527,001)

Fair value of warrant adjustment (262,643) 1,101,241 (135,402) (310,052) (53,125)

Non-GAAP net income (loss) 58,480$ 655,677$ 6,041$ (740,460)$ (618,845)$

Net income (loss) 68,999$ (566,610)$ (260,915)$ (60,956)$ (38,719)$

Cumulative preferred dividends -$ (332,226)$ -$ (332,226)$ -$

Net income (loss) applicable to common shares 68,999$ (898,836)$ (260,915)$ (393,182)$ (38,719)$

Non-GAAP net income (loss) 58,480$ 655,677$ 6,041$ (740,460)$ (618,845)$

Cumulative preferred dividends - (332,226) - (332,226) -

Non-GAAP net income (loss) applicable to common shares 58,480$ 323,451$ 6,041$ (1,072,686)$ (618,845)$

Net earnings (loss) per common share - basic -$ (0.03)$ (0.01)$ (0.01)$ -$

Non-GAAP net earnings (loss) per common share - basic -$ 0.01$ -$ (0.03)$ (0.02)$

Basic weighted average number of common shares outstanding 35,716,603 35,687,650 35,657,519 35,586,455 35,517,099

Net loss per common share - diluted (0.01)$ (0.03)$ (0.01)$ (0.01)$ -$

Non-GAAP net earnings (loss) per common share - diluted -$ 0.01$ -$ (0.03)$ (0.02)$

Diluted weighted average number of common shares outstanding 36,310,919 35,687,650 35,657,519 35,586,455 35,517,099

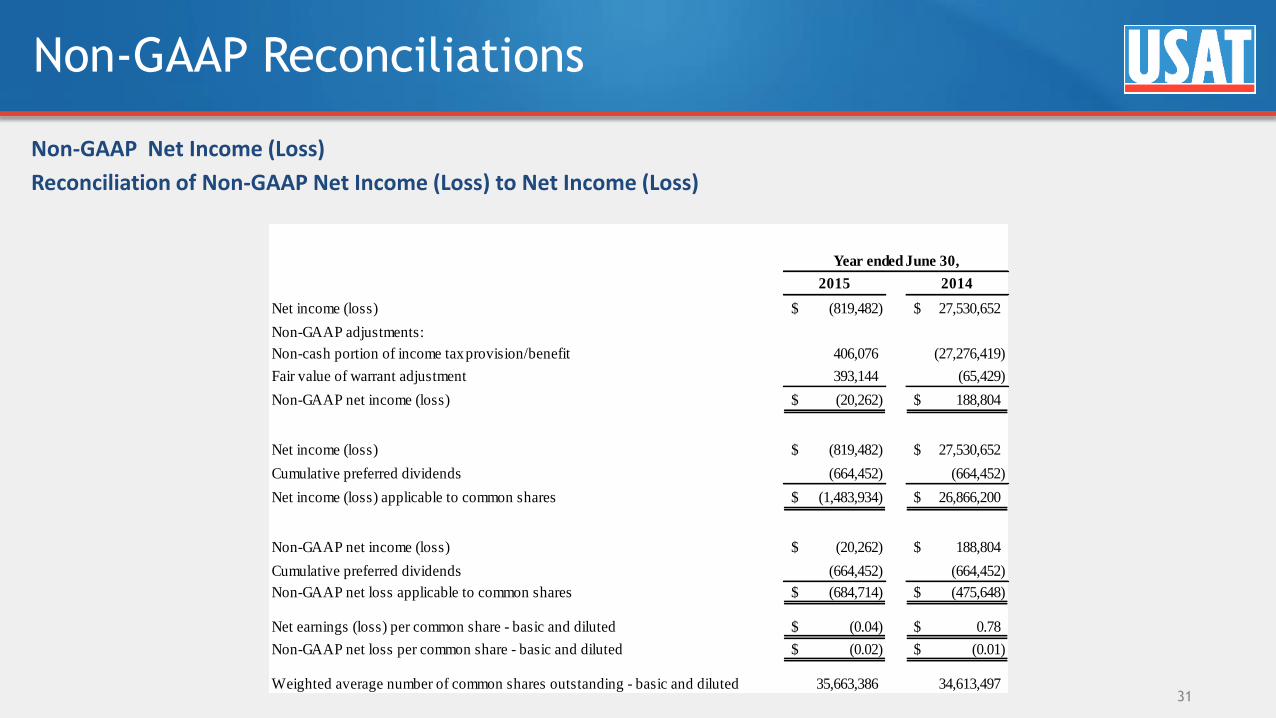

Non-GAAP Reconciliations

Non-GAAP Net Income (Loss)

Reconciliation of Non-GAAP Net Income (Loss) to Net Income (Loss)

31

2015 2014

Net income (loss) (819,482)$ 27,530,652$

Non-GAAP adjustments:

Non-cash portion of income tax provision/benefit 406,076 (27,276,419)

Fair value of warrant adjustment 393,144 (65,429)

Non-GAAP net income (loss) (20,262)$ 188,804$

Net income (loss) (819,482)$ 27,530,652$

Cumulative preferred dividends (664,452) (664,452)

Net income (loss) applicable to common shares (1,483,934)$ 26,866,200$

Non-GAAP net income (loss) (20,262)$ 188,804$

Cumulative preferred dividends (664,452) (664,452)

Non-GAAP net loss applicable to common shares (684,714)$ (475,648)$

Net earnings (loss) per common share - basic and diluted (0.04)$ 0.78$

Non-GAAP net loss per common share - basic and diluted (0.02)$ (0.01)$

Weighted average number of common shares outstanding - basic and diluted 35,663,386 34,613,497

Year ended June 30,

Non-GAAP Reconciliations

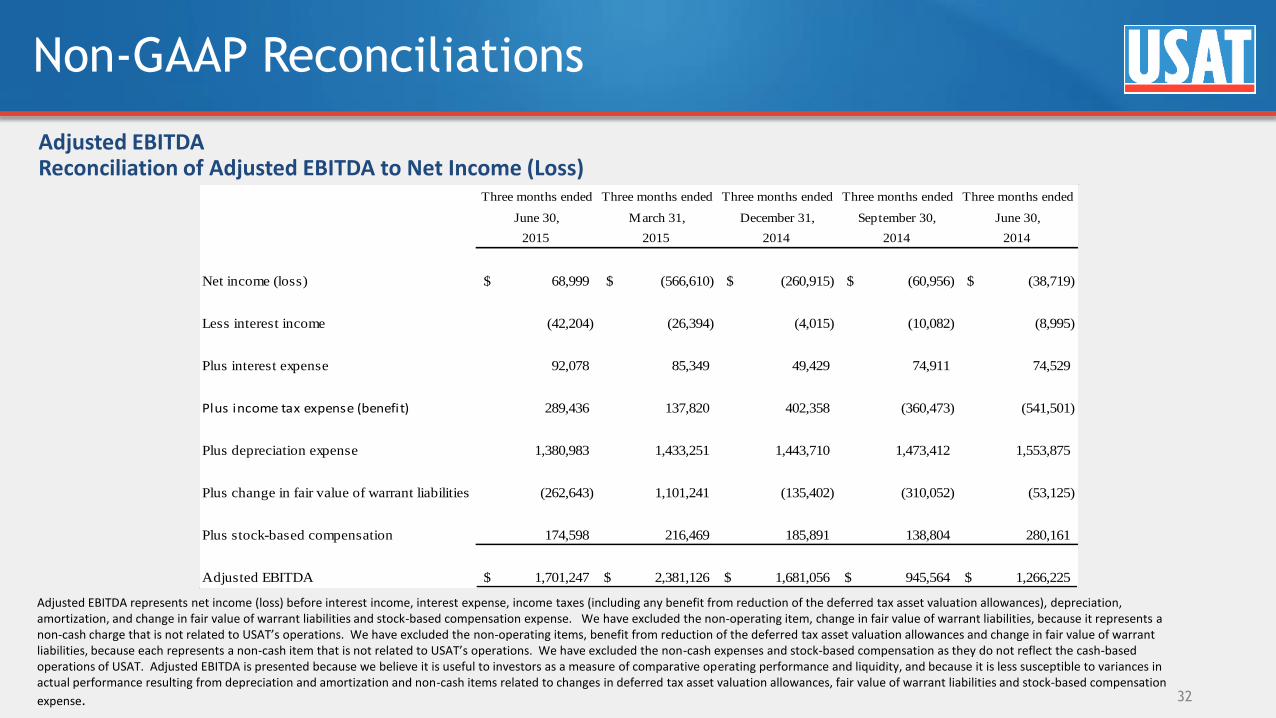

Adjusted EBITDA Reconciliation of Adjusted EBITDA to Net Income (Loss)

Adjusted EBITDA represents net income (loss) before interest income, interest expense, income taxes (including any benefit from reduction of the deferred tax asset valuation allowances), depreciation, amortization, and change in fair value of warrant liabilities and stock-based compensation expense. We have excluded the non-operating item, change in fair value of warrant liabilities, because it represents a non-cash charge that is not related to USAT’s operations. We have excluded the non-operating items, benefit from reduction of the deferred tax asset valuation allowances and change in fair value of warrant liabilities, because each represents a non-cash item that is not related to USAT’s operations. We have excluded the non-cash expenses and stock-based compensation as they do not reflect the cash-based operations of USAT. Adjusted EBITDA is presented because we believe it is useful to investors as a measure of comparative operating performance and liquidity, and because it is less susceptible to variances in actual performance resulting from depreciation and amortization and non-cash items related to changes in deferred tax asset valuation allowances, fair value of warrant liabilities and stock-based compensation

expense. 32

Three months ended Three months ended Three months ended Three months ended Three months ended

June 30, March 31, December 31, September 30, June 30,

2015 2015 2014 2014 2014

Net income (loss) 68,999$ (566,610)$ (260,915)$ (60,956)$ (38,719)$

Less interest income (42,204) (26,394) (4,015) (10,082) (8,995)

Plus interest expense 92,078 85,349 49,429 74,911 74,529

Plus income tax expense (benefit) 289,436 137,820 402,358 (360,473) (541,501)

Plus depreciation expense 1,380,983 1,433,251 1,443,710 1,473,412 1,553,875

Plus change in fair value of warrant liabilities (262,643) 1,101,241 (135,402) (310,052) (53,125)

Plus stock-based compensation 174,598 216,469 185,891 138,804 280,161

Adjusted EBITDA 1,701,247$ 2,381,126$ 1,681,056$ 945,564$ 1,266,225$

Non-GAAP Reconciliations

Adjusted EBITDA Reconciliation of Adjusted EBITDA to Net Income (Loss)

Adjusted EBITDA represents net income (loss) before interest income, interest expense, income taxes (including any benefit from reduction of the deferred tax asset valuation allowances), depreciation, amortization, and change in fair value of warrant liabilities and stock-based compensation expense. We have excluded the non-operating item, change in fair value of warrant liabilities, because it represents a non-cash charge that is not related to USAT’s operations. We have excluded the non-operating items, benefit from reduction of the deferred tax asset valuation allowances and change in fair value of warrant liabilities, because each represents a non-cash item that is not related to USAT’s operations. We have excluded the non-cash expenses and stock-based compensation as they do not reflect the cash-based operations of USAT. Adjusted EBITDA is presented because we believe it is useful to investors as a measure of comparative operating performance and liquidity, and because it is less susceptible to variances in actual performance resulting from depreciation and amortization and non-cash items related to changes in deferred tax asset valuation allowances, fair value of warrant liabilities and stock-based compensation

expense. 33

2015 2014

Net income (loss) (819,482)$ 27,530,652$

Less interest income (82,695) (30,337)

Plus interest expense 301,767 256,844

Plus income tax expense (benefit) 469,141 (27,255,398)

Plus depreciation expense 5,731,356 5,463,985

Plus amortization expense - 21,953

Plus change in fair value of warrant liabilities 393,144 (65,429)

Plus stock-based compensation 715,762 529,041

Adjusted EBITDA 6,708,993$ 6,451,311$

Year ended June 30,

Steve Herbert Chairman and CEO

Duncan Smith CFO

www.usatech.com

NASDAQ: USAT

800.633.0340

34