Us wireless market_q1_2015_update_may_2015_chetan_sharma_consulting

26

US Wireless Market Update Q1 2015 Chetan Sharma Consulting chetansharma.com Research. Technology. Strategy. Intellectual Property. Thought Leadership Summits.

-

Upload

chetan-sharma -

Category

Technology

-

view

6.003 -

download

0

Transcript of Us wireless market_q1_2015_update_may_2015_chetan_sharma_consulting

US Wireless Market Update Q1 2015

Chetan Sharma Consultingchetansharma.com

Research. Technology. Strategy. Intellectual Property. Thought Leadership Summits.

Page Title Goes HereChetan Sharma Consulting

© Chetan Sharma Consulting, 2015. All Rights Reserved

• Product & Tech Strategy– Consumer & Enterprise

• Roadmap• Product/Technology Strategy• Technical Due-Diligence• R&D• Business Plan Development• Revenue Models

• Market Research– Research and Forecasting– Competitive Analysis– Market Sizing

• Intellectual Property– Strategy, Audit, & Policy– Patents, Infringement analysis– Patent Mining and Valuation– Litigation

• Mobile Thought-leadership Summits– Mobile Future Forward– Mobile Breakfast Series

www.chetansharma.com

14 yr young Management Consulting firm exclusively focused on Mobile

Advisor to major operators, OEMs, brands, startups, VCs, and Fortune 500 firms around the world

Strategy for each of the top 6 global mobile data operators, top OEMs and Internet players

Have a unique 360o view of the ecosystem

Page Title Goes HereUS Mobile Market Update Q1 2015

© Chetan Sharma Consulting, 2015. All Rights Reserved

Summary

• The US mobile data services revenue grew 4% Q/Q and 15% Y/Y. The overall services revenue declined 1%. The device revenue for the operators grew by 41% allowed the overall service revenues to grow 5% Y/Y.

• We are forecasting that the mobile data service revenues will increase by 22% to $132 Billion in 2015. Verizon will become the first operator to generate more than $50B from data services in 2015.

• After acquiring lusacell and Nextel Mexico AT&T became the biggest North American operator with over 136 million subs.

• The average mobile data consumption (cellular) is approximately 2.5GB/mo. In the US, it took roughly 20 years to reach the 1GB/user/mo mark. However, the second GB mark has been reached in less than 4 quarters. An entire year’s worth of mobile data traffic in 2007 is now reached in less than 75 hours.

• From 2010 to 2013, the data pricing declined by only single digits YoY. However, in 2014, the data pricing has plummeted by 77%. In Q1 2015, the data pricing stayed pretty steady.

• The intense competition amongst the operators meant a 6% rise in OPEX QoQ and a 12% decline in CAPEX YoY. The income declined 4% while EBITDA grew modestly at 2%.

• Smartphone penetration increased to 76% and roughly 95% of the devices sold now are smartphones.

• 4th wave services continue to grow at a very past face around the globe. At least 37 companies generated a billion dollar or more from 4th wave services in 2014 – a 311% jump from 2012.

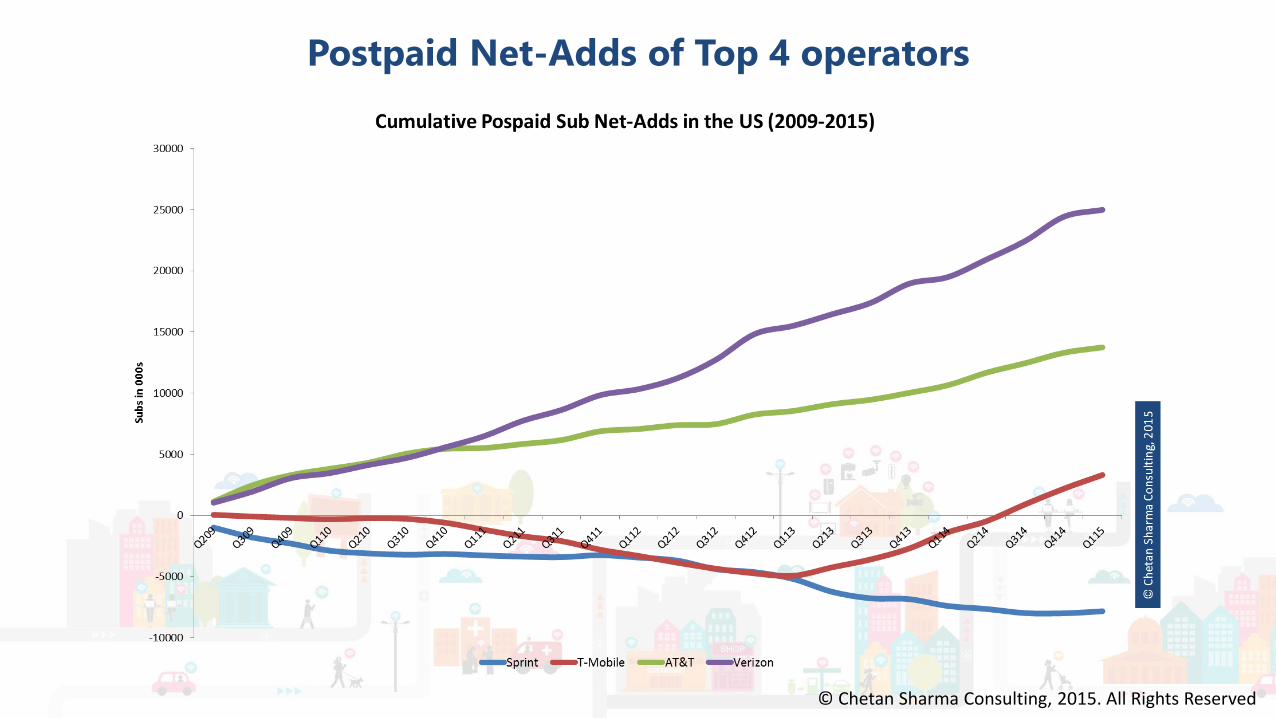

• The difference between Sprint and T-Mobile number of subs is just 300K subs now – the narrowest it has ever been. Like we suggested mid-last year, T-Mobile is likely to become the number three operator. This is more or less just a symbolic event with the transfer of bragging rights. Overall, churn was low for all operators in Q1 2015.

• T-Mobile accounted for over 40% of the overall net-adds for the year with AT&T and Sprint coming in second at 26%. Verizon slipped to a distant fourth with only 8%.

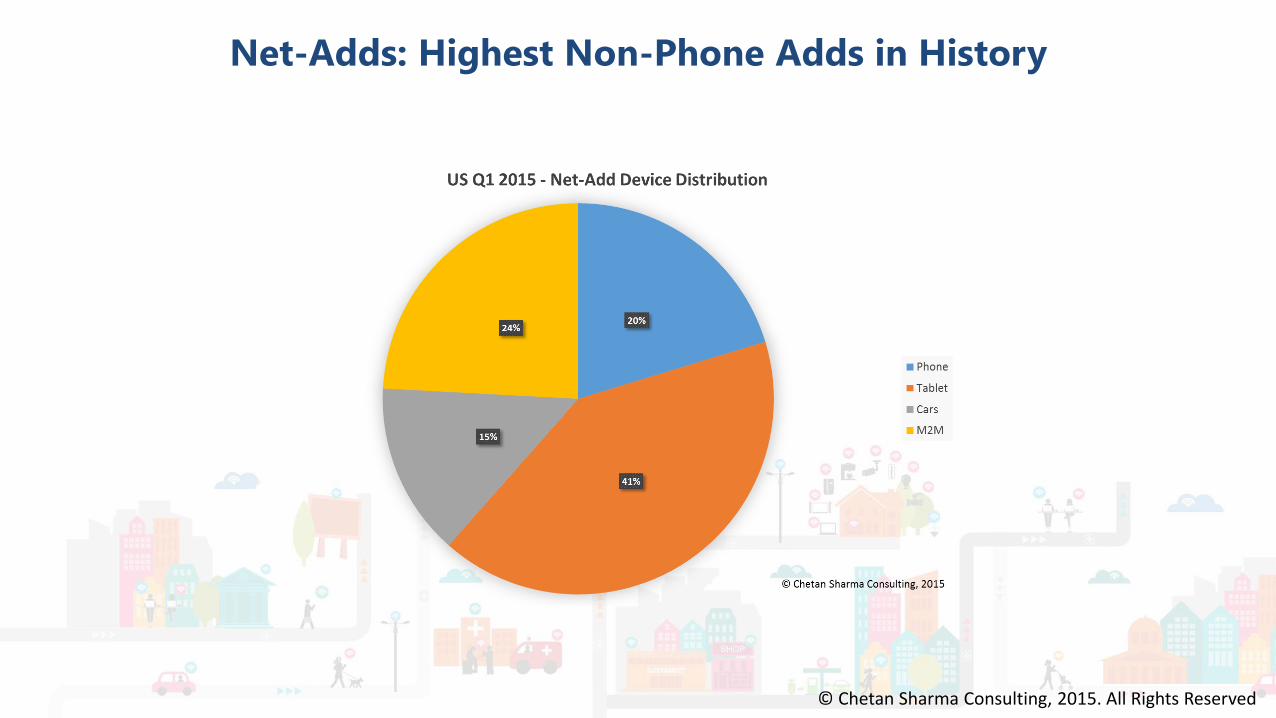

• Operator’s non-phone net-adds were 4 times that of the phone net-adds, highest it has ever been in the history of the industry.

• M2M+Connected car is a billion dollar revenue stream for AT&T. M2M+Telematics will become a billion dollar stream for Verizon by 2016.

• In our 4th wave series of papers, we had postulated for years that the 4th wave revenues will become bigger than any of the previous curves. This finally happened in 2014 in the US market with the revenues from the 4th wave applications and services built on top of the IP access layer surpassed both voice and data revenues.

Page Title Goes HereUS Mobile Market Update Q1 2015

© Chetan Sharma Consulting, 2015. All Rights Reserved

Apple Watch – New Interaction Models

Apple is never the first one to introduce a new consumer gadget but it is generally the first to make it work for the market so allies and enemies are all eager for Apple to come in and create awareness. For me, the exciting part wasn’t the watch itself though it clearly the best smartwatch available in the market but the new interaction models it introduced. The reincarnation of Morse code in the language of vibrations and heartbeats. The splitting of screen on two different computers on the body is quite fascinating and has design implications for the developers. It will take time for us (as consumers and developers) to understand and absorb the advantages of such a model. The transmission of signals from the body is enormously powerful in creating the preventive care culture around the globe. The story on wearables is just starting out.

Q1 2015 – 4th wave in action

For a casual observer of the industry, Verizon’s acquisition might have come as a surprise but for the students of the 4th wave, it was normal course of action. In my talks, I often say that for service providers to compete with the OTTs, they have to become OTTs themselves. One could argue if AOL was the right company for this strategy but large operators are opening up their checkbooks to do cross-domain acquisitions. AOL brings a new billion dollar revenue stream however it doesn’t solve the basic fragmentation problem that operators have. They can’t effectively compete with Google and/or Facebook without covering the entire market. Without domination (in market share) or collaboration, the opportunity will remain small and might even vanish in due time.

As we mentioned earlier this year, globally, 37 companies generated (not valuation) a billion dollar or more in revenue from 4th wave services in 2014 – a 311% jump from 2012.

Unicorns at incumbents

Tech press and the startup world is infatuated with unicorns. The billion dollar is a magical marker that inspires the ecosystem to be in the elite club but what about when a new unicorn stream is created at an incumbent? It rarely makes waves. At a 100+ year old incumbent, even less so. AT&T has been lighting up connected cars faster than any other mobile operator in the world right now. While 3.5M connected cars might not instill excitement, one must consider the replacement cycles of automobiles which is several times that of a smartphone. Our estimates suggest that the connected car segment will become a billion dollar business for AT&T by 2016. The M2M+Connected Car revenue stream is already a billion dollar business for AT&T. Verizon is also slowly getting there. Their M2M+Telematics revenue stream should reach an annualized revenue stream of over a billion dollars by 2016. Some operators in Europe are also making inroads into the new connected devices revenue streams. Similarly, the likes of Microsoft and Google have created new billion dollar revenue streams in mobile. As a separate entity, these will be decacorns but don’t get appreciated when residing with the parent company.

Page Title Goes HereUS Mobile Market Update Q1 2015

© Chetan Sharma Consulting, 2015. All Rights Reserved

Is Android in trouble?

• Much of the current situation has been predictable for some time. While Samsung has ridden the smartphone wave masterfully, it hasn’t been able to build a platform moat, something that helps fundamentally differentiate its products in the sea of Android devices around the planet. They are not in a Blackberry or Nokia panic situation yet as some in the media have surmised. But, they need to figure a way out of the middle band. Unlike Nokia or Blackberry who were blinded by their success and ignorance, Samsung has shown it is a more nimble competitor. Samsung’s R&D and marketing is also second to none. Its diversified portfolio also helps in cushioning the drop in the phone segment. Historically, OEMs with such sharp revenue declines haven’t been able to arrest the decline. Can Samsung do it? Samsung is launching Galaxy 6 at MWC this weekend.

• Given that Samsung controls most of Android ecosystem profits, the Android ecosystem suffered a 44% decline in profits. The woes of OEMs such as Sony, Motorola, and others also contributed to the decline. We can expect some of the Android OEMs leaving the device business altogether.

Operator M&A

• In his classic book, “Competition in Telecommunications,” Nobel Laureate Jean Tirole wrote, “With digital technology, telecommunications, cable TV, broadcasting, and computers have become a single industry, which will be a critical element of our economies’ backbone. With the impending opening of competition, industrial restructuring is progressing at a fast pace.” The book was written almost 15 years ago. As I have written before, the computing and communications industries are merging into one and that collision is generating ripple effects some of which we are starting to understand (more on the Connected Intelligence Era trends here)

• One of the implications of the 4th wave evolution is that there will be fewer mobile operators in the world. As we have argued in the papers, many of the smaller players just won’t be able to keep up and compete. AT&T acquired Mexican operator Iusacell (it also made the bid for Nextel Mexico) which made AT&T a clear leader in North America with almost 131 Million subscriptions. As we mentioned in our 4th wave series of papers, the number of operators will continue to shrink with fewer global operators who will seek to combine wireless and wireline assets to strengthen their moat. It is quite likely that US Cellular will be acquired in 2015.

Net-Neutrality Debates

• After a blockbuster spectrum auction, FCC is looking to put its stamp on the future of the Internet by proposing net-neutrality rules later this week. President Obama decisively tilted FCC’s position on the subject. However, this is not a done deal yet. The legal and political apparatus is likely to react quite strongly to the ruling and we are in for a tough fight on this one. Other governments and regulators are also keenly watching the debate and the final ruling. Dish ended up acquiring a bulk of the spectrum wares. Is this a precursor of their wireless moves or was this just old-fashioned asset hoarding?

4th Wave Revenues

• For the first time, US operators revealed some of their 4th wave (digital) services metrics publicly. Verizon reported $585 million in 2014 up 45% from a year ago. At the current run-rate, this will be a billion dollar business by 2016. AT&T reported 2.8M connected car connections and 140K home security connections. The connected car segment is clearly on its way to becoming a billion+ dollar business for AT&T. Connected cars accounted for 62% of the connected devices for AT&T

• Globally, 37 companies generated a billion dollar or more from 4th wave services in 2014 – a 311% jump from 2012.

Page Title Goes HereUS Mobile Market Update Q1 2015

© Chetan Sharma Consulting, 2015. All Rights Reserved

Google Fi – Google Fiber for Wireless

When Google-Fi was announced, there was plenty of media frenzy around Google going after the operators. Folks who wrote such articles don’t understand the business of either Google or the operators. Google is a brilliant strategist which does some projects to push its strategy in the ecosystem. The goal is generally not a new revenue stream but twisting the value-chain enough to serve its purpose long-term.

However, there are couple of direct and subtle signals that Google did send to the markets. First, there are some technical tricks that Google was able to pull off to make WiFi/Cellular handoffs to work. Second, and perhaps more important is that the control point moved from the network to the device which at scale can be the biggest disruption the mobile industry has ever seen. It is not easy to pull off given the interdependency of OEMs to the operators. But sometime in the future, it is not hard to envision that for every session, the device (and associated cloud infrastructure) initiates the auction amongst the available networks and picks one based on performance, pricing, revenue share, and other parameters. That day is not here yet but service providers should start planning for this scenario.

WiFi-first network has good potential and we will see many of them pop up around the globe but getting scale is the biggest question mark in such endeavors (beyond some technical issues of seamless interop).

One should also remember that while WiFi usage in the US is 3x that of cellular usage, the use of WiFi hasn’t really slowed down the cellular data growth one bit. They both are growing at approximately 100% Y/Y.

Post-PC – Apple has no peer

There are has been a lot of debate around the PC and Post-PC worlds. Apple has benefited from the transition to the Post-PC universe like no other company. Its Post-PC revenue in Q1 was four times the Post-PC revenue of Google, Microsoft, Facebook, and Amazon combined. Largely due to the iPhone, Apple has been able to carve out a dominant space on the current wave of computing.

Service provider M&A

When Comcast initially announced the merger with Time Warner, it looked like a slam dunk but it was swiftly rebuffed by the regulators. This sets up an interesting 18 months for the US market. Unless there is a change in power (democrats to republicans), the big mergers in the same domain are off the table. So, how do existing behemoths grow? They start to look overseas (e.g. AT&T acquiring Mexican operators), look sideways (e.g. AT&T acquiring DirectTV) or look upwards (e.g. Verizon acquiring AOL). There are still a number of questions posed to the likes Comcast, Time Warner, Dish, T-Mobile and Sprint. Will this finally force Comcast to be a more active mobile player by acquiring one of the two smaller operators? Will the regulators allow such a move? Is Sprint back in the equation? How anxious is Deutsche Telecom to offload its US assets? How will Dish use its spectrum assets? We might see all these questions answered in the next 18 months or not.

Page Title Goes HereUS Mobile Market Update Q1 2015

© Chetan Sharma Consulting, 2015. All Rights Reserved

Net-Neutrality and Zero-Rating Debates

In the tech world few things ignite the discussion with religious fervor as the net-neutrality debates. From Washington DC to New Delhi, from Brussels to Santiago, net-neutrality and zero-rating have inflamed passions. Most of the times those fighting on either sides have no clue about the issues at hand and what are they fighting for. Ask a protester on the street about the intricacies of net-neutrality and you will get blank looks or confused answers. Both issues boil down to “transparency” and “control” – who gets to decide what and what are they going to disclose. The answer to many of these debates is fairly simple – ensure there is enough competition and put the (granular) “control” and the “responsibility” in the hands of the customer for e.g. they should decide which apps should make it into the “Zero Rating” club for them. The problem goes away at least in principle.

The Upcoming 5G wars?

I started my career when 1G was all the rage. My first 4G project was back in 2002. By some measures, we are already behind on the 5G discussions. In general, it takes 7-10 years before the standards are finalized and then the network technology lasts for approximately 20 years before a market moves onto the next generation of technology. US led in the growth of 1G (AMPS, TACS) followed by Europe on 2G (GSM, CDMA). Japan took the leadership role with 3G (WCDMA, EVDO) and US wrestled it back on 4G (LTE). Japan and EU are determined to lead on 5G and have been making very public statements and R&D investments about their ambitions on 5G. Japan of course has a very clear goal of having 5G by Tokyo Olympics in 2020. Am sure some operator(s) somewhere will jump the gun and start calling LTE-A+ as 5G around 2017-18 or sooner. You can expect a lot of activities both in public and private on 5G as companies and governments try to figure out a way to claim the 5G leadership mantle.

We have summarized our thoughts on 5G in this paper – 5G: The history of the future. I have been giving a number of talks on 5G in North America and Europe and many of these will be made public in due course.

What to expect in the coming months?

2014 was a tremendous year for the mobile as it becomes omnipresence in every industry. We saw some massive moves, astounding acquisitions, and interesting strategic endeavors. 2015 promises to be an exciting year for the industry as well.

As usual, we will be keeping a very close eye on the micro- and macro-trends and reporting on the market on a regular basis in various private and public settings.

The next 10 years will generate almost 1000 Trillion dollars in global GDP, which is 60% more than the last 10 years. What will be significant is how the “Connected Intelligence” built using networks, sensors, and software is going to transform every industry, every nation. We will covering the future of the mobile industry in-depth at our Mobile Future Forward summit this fall on Sept 29th.

Against this backdrop, the analysis of the Q1 2015 US wireless data market is:

Page Title Goes HereUS Mobile Market Update Q1 2015

© Chetan Sharma Consulting, 2015. All Rights Reserved

Service Revenues

• The US mobile data services revenues in Q1 2015 increased 3% and reached $30B.

• After crossing the $100B in data revenues last year, the US market is set for explosive growth and is likely to cross $130B in data revenues in 2015.

• Verizon and AT&T dominated the quarter accounting for 70% of the mobile data services revenue and had 68% of the subscription base.

• Verizon and AT&T are at #2 & #3 global mobile data revenue ranking respectively in Q1 2015. Sprint and T-Mobile also maintained their rankings in the top 10 global mobile data operators.

ARPU

• The Overall ARPU fell by 2.71%.

• Data contribution to the overall revenues is now at 62%.

• The postpaid ARPU continues to decline for all operators with all but Verizon suffering double digit YoY losses.

Subscribers

• The US market had 4.6M net-adds. Probably for the first time, Verizon finished last in terms of net-adds for the quarter. T-Mobile led with 1.8M net-adds mostly postpaid.

• T-Mobile added almost as many postpaid subs as rest of the three operators combined.

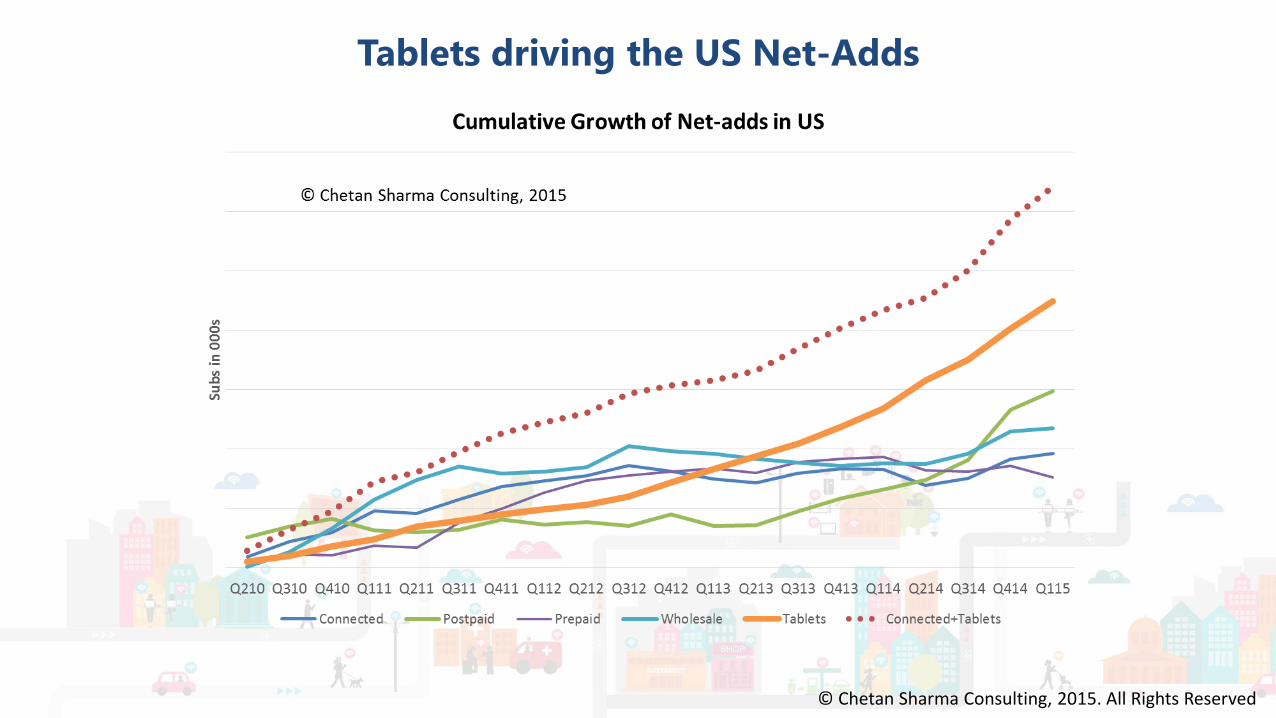

• Connected devices (excluding tablets) had the best net-add performance followed by tablets.

• T-Mobile led in the phone category while remaining three operators added more than 1M non-phone customers.

Shared Data Plans

• Shared data plans launched by Verizon and AT&T have been quite successful. The attachment rates have increased tremendously over the course of 2013-14 with more consumers opting for cellular tablets and connected devices. 70% of postpaid accounts at AT&T are now on shared plans.

• Some more granular data plans for tablets have also spurred interest as the cellular broadband is becoming available on demand vs. expensive on premise Wi-Fi solutions.

• 50% of AT&T’s postpaid accounts are on 10GB+ plans.

Page Title Goes HereUS Mobile Market Update Q1 2015

© Chetan Sharma Consulting, 2015. All Rights Reserved

4th Wave Progress

• The number of players making $250M/quarter on mobile continues to increase rapidly and these aren’t your traditional wireless players. For example, Mobile is now contributing 70% (up from 30% in Q1 2013) to Facebook’s quarterly revenues. Latest addition to the club is Twitter which is now doing 89% in mobile (of the total advertising revenue) up from 60% in 2013. Even traditional players like Hertz, Sears, and Starbucks are generating meaningful revenues from mobile. There are now dozens of such players and the list is just growing. (for more discussion on the topic please see: “Mobile 4th Wave: Evolution of the Next Trillion Dollars”)

• The cloud and security segments have also gained significant traction with incumbents as well as startups launching new initiatives and technologies.

• Verizon reported $150 million revenue from M2M and Telematics. At the current run-rate, this will be a billion dollar business by 2016.

• AT&T reported 684K net-adds on the connected car platform. We estimate that connected car will become a billion dollar revenue stream for AT&T in 2015. Connected cars accounted for 62% of the connected devices for AT&T.

Connected Devices

• Connected devices (non-phones) accounted for almost 52% of the net-adds in Q4 2014. This means that while there is a healthy smartphone sales pipeline, it is for the existing subs and as such net-adds for the phone business is tapering off and we can expect that new net-adds will continue to be dominated by the connected devices segment.

• For AT&T, Connected cars started to form a significant base of the connected devices segment with 68% of the new connections in the segment coming from cars.

Handsets

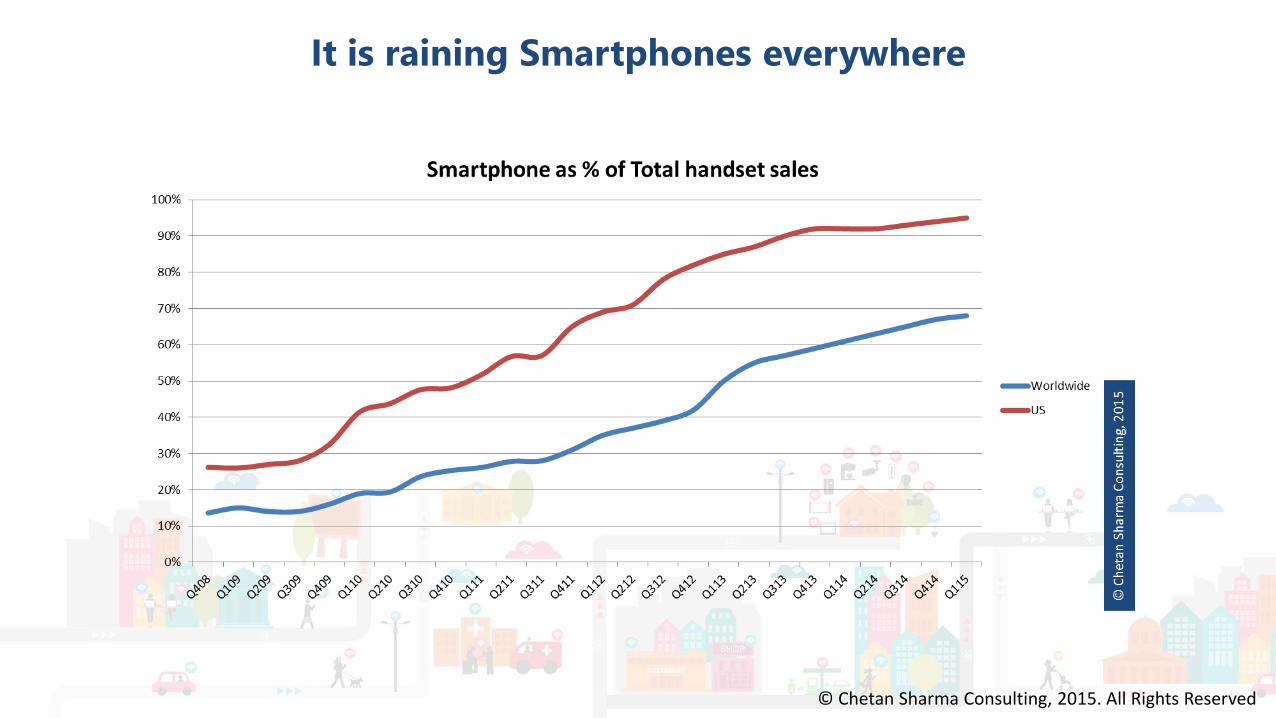

• Smartphones continued to be sold at a brisk pace accounting almost 95% of the devices sold in Q1 2015. The feature phone category is practically becoming extinct in the US market.

• The smartphone penetration in the US is now at 76%.

• Verizon continues to sell more LTE smartphones as its LTE sub tally rose to 71M making it the #2 LTE operator behind China Mobile which has more than twice LTE subs. Other three operators are also deep into their LTE deployments. Verizon reported that 86% of its total data traffic is on the LTE network now, clearly the fastest technology transitions we have seen in the US wireless industry.

Your feedback is always welcome.

Chetan Sharma

We will be keeping a close eye on the trends in the wireless data sector in our blog, twitter feeds, future research reports, articles, and our annual thought-leadership summit –Mobile Future Forward. The next US Wireless Data Market update will be released in Aug 2015.

Disclaimer: Some of the companies mentioned in this update are our clients.

Page Title Goes HereUS Mobile Data Services Revenue

© Chetan Sharma Consulting, 2015. All Rights Reserved

Page Title Goes HereSummary of the US Mobile Market Revenue Streams

© Chetan Sharma Consulting, 2015. All Rights Reserved

4th wave revenuessurpassed access revenues

YoY Growth

21%

Page Title Goes HereMarket will consolidate into 3 players

© Chetan Sharma Consulting, 2015. All Rights Reserved

Page Title Goes HereRevenue will be made from existing customers, new customer

revenue approaching ZERO

© Chetan Sharma Consulting, 2015. All Rights Reserved

Page Title Goes HereUS Mobile Market: Data Dominant

© Chetan Sharma Consulting, 2015. All Rights Reserved

Page Title Goes HereUS Market: Carrier Marketshare (2015)

© Chetan Sharma Consulting, 2015. All Rights Reserved

Page Title Goes HereNet-Adds: Highest Non-Phone Adds in History

© Chetan Sharma Consulting, 2015. All Rights Reserved

Page Title Goes HerePost-PC Platform World – Apple Dominates

© Chetan Sharma Consulting, 2015. All Rights Reserved

Page Title Goes HerePostpaid ARPU is in free fall

© Chetan Sharma Consulting, 2015. All Rights Reserved

Page Title Goes HerePostpaid Net-Adds of Top 4 operators

© Chetan Sharma Consulting, 2015. All Rights Reserved

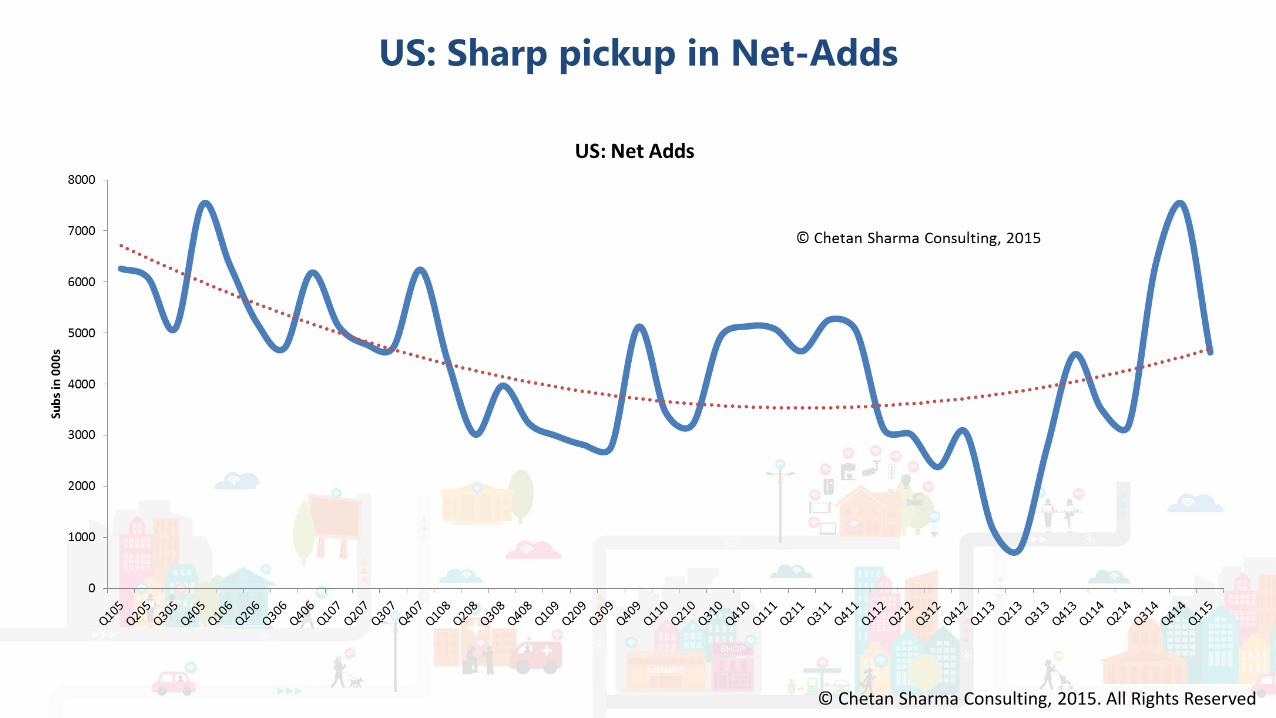

Page Title Goes HereUS: Sharp pickup in Net-Adds

© Chetan Sharma Consulting, 2015. All Rights Reserved

Page Title Goes HereTablets driving the US Net-Adds

© Chetan Sharma Consulting, 2015. All Rights Reserved

Page Title Goes HereIt is raining Smartphones everywhere

© Chetan Sharma Consulting, 2015. All Rights Reserved

Page Title Goes HereChinese OEMs dominate the unit sales, Apple the revenue

© Chetan Sharma Consulting, 2015. All Rights Reserved

Page Title Goes Here5G: The history of the future

© Chetan Sharma Consulting, 2015. All Rights Reserved

Page Title Goes HereMobile Future Forward – Sept 29th 2015get inspired to fuel your mind and strategy

© Chetan Sharma Consulting, 2015. All Rights Reserved

Mobile Future Forward is the most intellectual conference – CEO and founder, Connected Watch Company

It is a terrific event. Mobile Future Forward is causing everyone to think about what’s the next big thing – CEO, Global Mobile Operator

America’s greatest gathering of the wireless minds – CEO, Future Forecasting Service

Page Title Goes HereWe look forward to hearing from you

© Chetan Sharma Consulting, 2015. All Rights Reserved

Chetan Sharma

TW: @chetansharma

http://www.chetansharma.com

Mobile Future Forward

TW: @mfutureforward

http://www.mobilefutureforward.com

Research. Technology. Strategy. Intellectual Property. Thought Leadership Summits.