Us Retail SGA Book of Metrics 021010

20

SGA Book of Metrics for Retail: 2009 Executive Summary First-of-its-kind insights into retail’s store operations, general and administrative functions Global Benchmarking Center February 2010

-

Upload

daengmaduppa -

Category

Documents

-

view

15 -

download

0

Transcript of Us Retail SGA Book of Metrics 021010

SGA Book of Metrics for Retail: 2009 Executive SummaryFirst-of-its-kind insights into retail’s store operations, general and administrative functions

Global Benchmarking CenterFebruary 2010

21“Low-cost performers” refers to companies in the first quartile of the five process categories. They are not necessarily “best in class” along other meaningful dimensions, such as quality, innovation, or customer/employee satisfaction. The benchmarks in this study suggest possible cost-reduction opportunities, which must be balanced against growth strategies.

Dear Colleague:

Managing through one of the deepest recessions of the past 30 years, retail executives are facing a market where reduced consumer spending has made cost-management initiatives more critical than ever. They are faced with many questions and challenges, such as:

• “Where will I get the most impact without negatively affecting our ability to serve the customer or the customer’s experience?”

• “Where can I reduce costs without endangering our ability to drive growth quickly when the economy improves?”

Measuring store operations and general and administrative costs (SGA) and comparing them against low-cost performers can help retail executives in their efforts to identify and close competitive cost gaps that exist in their business.

To develop a baseline of current, retail-specific data that can be used to quantify SGA improvement opportunities, Deloitte has conducted a benchmarking study of core SGA functions in the retail industry:

•Store operations•Merchandising•Supply chain management•Marketing•Information technology•Finance•Human resources•Support services

We believe that in conducting this study and by identifying the spend amounts of low-cost performers, we can provide retail executives relevant data and practical insights about their organizations’ competitive positioning.

We hope you find the results of our study helpful and instructive, and we invite you to contact us for further information about our research and how it may help your company.

Sincerely,

Stacy JaniakVice Chairman & U.S. Retail LeaderPartnerDeloitte LLP

John RooneyPrincipalNational Retail IndustryDeloitte Consulting LLP

Richard T. RothPrincipalNational Benchmarking LeaderDeloitte Consulting LLP

All study data and statistics referenced and presented in this report, as well as the representations made and opinions expressed, unless specifically described otherwise, pertain only to the participating organizations and their responses to the Deloitte Global Benchmarking Center study of retail process performance conducted in 2009.

As used in this document, “Deloitte” means Deloitte Consulting LLP, a subsidiary of Deloitte LLP. Please see www.deloitte.com/us/about for a detailed description of the legal structure of Deloitte LLP and its subsidiaries.

Overall findings ......................................................................................... 1

Key themes ................................................................................................ 3

Functional analysis .................................................................................... 5

Store operations ................................................................................. 5

Supply chain ....................................................................................... 6

Merchandising .................................................................................... 6

Information technology ...................................................................... 7

Finance ............................................................................................... 7

Looking forward ........................................................................................ 8

Study approach and methodology ............................................................. 9

Performance measures ............................................................................ 10

Representative participant list.................................................................. 13

About the Global Benchmarking Center .................................................. 14

Contents

Executive Summary SGA book of metrics for retail

1

As consumers spend less and save more, retailers face continued pressure to improve bottom-line perfor-mance — even after previous cost-cutting initiatives. We project that US consumer spending will rise in the next several years at a slower rate than the GDP due to tighter credit conditions, slowly recovering home equity, and slow recovering employment. Facing this, what should retail executives keep in mind as they take steps to reduce additional costs now?

The customer experience is often a critical competitive differentiator among retailers, making cost-reduction efforts tricky. For many, improvement benefits come not from reducing costs, but reallocating them more effec-tively. We believe that reducing or reallocating costs — while achieving sales growth and maintaining strong brand value — requires retailers to view cost improve-ment opportunities through a customer-experience lens: “How would this action impact my customers?” “How can we adjust our cost structure to achieve improvements and preserve customer loyalty?”

This study compares store operations and general and administrative functions (SGA1) against median and

Overall findings

Figure 1: Total SGA function cost as a percent of sales

35.9%

Information technologyFinanceHuman resourcesSupport services

Store operationsMerchandisingSupply chainMarketing

24.9%

Retailmedian

Retaillow-cost performer

Information technologyFinanceHuman resourcesSupport services

Store operationsMerchandisingSupply chainMarketing

Privatelabel

Non-privatelabel

Figure 2: Total SGA function cost as a percent of sales (median)

46.8%

38.4%

low-cost performers in the benchmark group. The results show gaps that point to significant potential for strategic cost reductions, not only for short-term relief during this economic downturn, but also for the long-term process efficiencies needed to jump start growth upon recovery.

The study also shows that retail low-cost performers have created distinctive characteristics over their median counterparts by:

Allotting more staff to shopper-facing areas •Transforming their advertising mix for an enhanced •return on investmentReverting to in-house supply chain options to •improve cost performanceReducing store operations cost by managing their •assortment to a smaller number of stock-keeping units (SKUs) — without negatively impacting salesInvesting strategically in IT •Reducing costs in traditional back-office areas to the •point where they can focus on improving new areas of spend, such as marketing, IT and supply chain

1 This study’s reference to “SGA” should not be confused with the traditional selling, general and administrative function. We’re defining SGA in a wider, expanded sense to also include store operations, merchan-dising and supply chain.

SGA book of metrics for retail 2

As expected, according to the study, the median allocate more than 70% of SGA to store operations — dwarfing other functional cost areas (Figure 1). This area continues to represent a key opportunity for all retailers in our study: Apparel, private label2, other/specialty and non-private label (Figure 2).

Our analysis included an examination of cost gaps between median and low-cost performers in the study — by function and by sector. We compared metrics such as cost and full-time equivalents (FTEs) against a defined set of retail peers to identify cost gaps. This analysis is significant; while a metric is a useful number on its own, a cost gap – measured in pure dollars – identifies opportunities for improvement. In other words, companies looking to move from the median to low-cost performer level will see what that means to them in actual cost savings.

Information technologyFinanceHuman resourcesSupport services

Store operationsMerchandisingSupply chainMarketing

Retailoverall

Apparel Other/Specialty

36.8%

Figure 3: Total SGA function cost gap from median to low-cost performer per $1 billionin sales by subsector ($US M)

109.9

62.3

108.7

Our study found that the apparel sector has a lower cost-improvement opportunity than the other/specialty retailers. Merchandising is the only retail-specific “front-office” function where apparel has a larger opportunity than the other/specialty retailers (Figure 3).

Overall, we’ve found that the gap between the median and low-cost performers is smaller in typical back-office functions (i.e., finance, human resources, support services) and higher in areas such as marketing, infor-mation technology and merchandising. This is likely because retailers, in our experience, have prioritized cost-reduction efforts on the back-office functions first, viewing the other functions as more strategic.

2 The private label peer group includes study participants with a high percentage of sales from private label products; the median, or midpoint value, of “private label sales as a percent of total sales” is 98% of the peer group.

Note: Retail overall includes apparel, other/specialty and other subscribers. See page 13 for details.

3

Key themes

Low-cost performers spend much more on visual merchandising and online advertising than traditional print and TV/radio advertising

Retail low-cost performers consistently place a higher percentage of their advertising spend on below-the-line (BTL) vehicles targeting customers more directly through loyalty programs, community via event sponsorships, in-store displays and messaging, or online. In contrast, the median spends more proportionately on above-the-line (ATL) vehicles, which include more traditional mass advertising through print, TV and radio (Figure 4). This validates the strong industry case for BTL being more cost-effective while delivering better results. We also note an increase in customer research spending for low-cost performers.

Figure 5: Total SKUs per retailer

121,478

Retailmedian

79,104

Retaillow-cost performer

Low-cost performers benefit from targeted investments and simplified SKUs

When it comes to the operations-specific elements of merchandising, low-cost performers within a given sector — e.g., apparel — rely on targeted investments and a smaller assortment of SKUs for their advantage over the median. They manage 35% fewer SKUs (Figure 5), providing the necessary product variety customers demand without the complexity of overextended inventory. In addition, through further correlation analysis, we found that low-cost performers spend 84% more on store operations technology, which contributes to lower process costs.

Note: Total SKUs per retailer includes all SKUs, i.e., styles, colors, sizes, etc.

Print advertisingTV/Radio advertisingSponsorship advertising

Visual merchandisingOnline advertisingOther advertising

Figure 4: Advertising spend allocation

Retail median Retail low-cost performer

SGA book of metrics for retail 4

Retailoverall

Figure 7: Occupancy, depreciation, and maintenance as a percent of total SGA cost (median)

29.1%

39.0%

22.4%

35.5%

Apparel Non-privatelabel

Other/Specialty

20.8%

Privatelabel

Within functions, the top five costs represent 65% to 70% of total SGA cost for each of the subsectors

We probed costs within functions and, not surpris-ingly, found that store operations dominates the cost categories (Figure 6). In our experience, retailers have typically brought store real estate costs down by rene-gotiating leases, standardizing maintenance policies, and reducing usage costs by incorporating efficient energy and maintenance technologies. Also, we believe that increased productivity and innovation have helped low-cost performers decrease merchandising store activities and advertising spend.

Store size has a direct impact on cost per square foot

Occupancy costs generally represent 20-35% of overall SGA cost, and apparel and private label retailers tend to have higher occupancy spend. As expected, store size directly impacts cost per square foot, with larger stores driving lower per-square-foot costs (Figures 7-8).

Average square footage per store

Figure 8: Occupancy cost per square foot

$80

60

40

20

0800006000040000200000

Store operations: Occupancy, depreciation, maintenenceStore operations: Merchandise and sell goodsStore operations: Manage and plan store operationsStore operations: Miscellaneous other costMarketing: Advertising spend

Figure 6: Top five costs as a percent of total SGA (median)29.1%

15.5%

10.0%8.9%

5.7%

5

Functional analysis

Store operations:

Retailers focus staff on shopper-facing functions to ensure a brand-building customer experience that supports growth

Retailers focus staff on shopper-facing functions to ensure a brand building customer experience that supports growth

As expected, more than 84% of staff resides in store operations, with store labor costs as a percent of sales being relatively consistent between the median and low-cost performers. However, it’s interesting to note that low-cost performers can maintain their overall low-cost ranking while still spending 6% more on store operations staff per billion in sales than the median; through this, we can infer that the low-cost performers focus their spend in customer-facing areas and achieve cost reductions in non-customer-facing areas. While both

median and low-cost performers are employing process and technology innovations to help reduce staff require-ments in heavy transactional areas, such as finance and HR, low-cost performers are doing a better job of ensuring they have the necessary higher-level staff.

In addition, apparel low-cost performers have 68% lower process costs than the median in managing and planning store operations, representing about $30 million in opportunity per $1 billion in sales. Meanwhile, the difference is much lower within the other/specialty subsector, where low-cost performers spend 22% less than the median on process costs.

Figure 9: Manage and plan store operations process cost per $1 billion in sales ($US M)

4.44%

1.43%

2.22%

1.74%

4.8

Low-Cost PerformerMedian

Apparel Other/Specialty

SGA book of metrics for retail 6

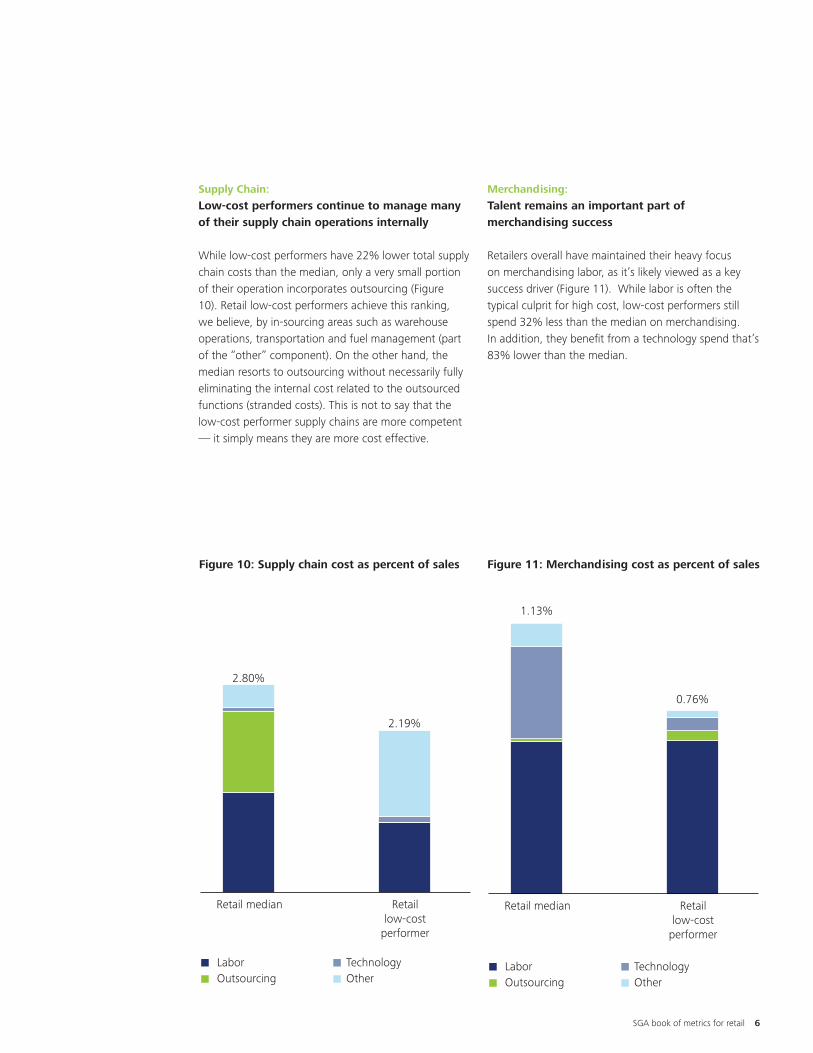

Supply Chain:

Low-cost performers continue to manage many of their supply chain operations internally

While low-cost performers have 22% lower total supply chain costs than the median, only a very small portion of their operation incorporates outsourcing (Figure 10). Retail low-cost performers achieve this ranking, we believe, by in-sourcing areas such as warehouse operations, transportation and fuel management (part of the “other” component). On the other hand, the median resorts to outsourcing without necessarily fully eliminating the internal cost related to the outsourced functions (stranded costs). This is not to say that the low-cost performer supply chains are more competent — it simply means they are more cost effective.

Figure 10: Supply chain cost as percent of sales

TechnologyOther

LaborOutsourcing

Retail median Retaillow-cost

performer

2.80%

2.19%

Merchandising:

Talent remains an important part of merchandising success

Retailers overall have maintained their heavy focus on merchandising labor, as it’s likely viewed as a key success driver (Figure 11). While labor is often the typical culprit for high cost, low-cost performers still spend 32% less than the median on merchandising. In addition, they benefit from a technology spend that’s 83% lower than the median.

Figure 11: Merchandising cost as percent of sales

TechnologyOther

LaborOutsourcing

Retail median Retaillow-cost

performer

1.13%

0.80%

Figure 10: Supply chain cost as percent of sales

TechnologyOther

LaborOutsourcing

Retail median Retaillow-cost

performer

2.80%

2.19%

Figure 11: Merchandising cost as percent of sales

TechnologyOther

LaborOutsourcing

Retail median Retaillow-cost

performer

1.13%

0.76%

7

Information technology:

Surprisingly, outsourcing is not driving lower IT costs

While low-cost performers have a 36% lower IT cost per end-user relative to the median, it’s not because they outsource much more, as is often thought (Figure 12). Low-cost performers in our study achieve their cost savings through a lower labor and technology spend than the median.

This finding supports the belief that outsourcing rarely provides cost savings unless additional factors are taken into consideration: Sound management of the effort, clear and effective communication, effective processes, high-quality deliverables and explicit service-level agreements.

Finance:

Process innovation gives low-cost performers an edge over the median

Low-cost performers spend 27% less than the median on finance, with labor and technology being the largest sources of the cost gap (Figure 13).

In our experience, highly effective retailers have done a good job of developing the finance process innovations that help lower costs and increase productivity. They make use of efficient technologies and shared services to reduce transaction costs and labor requirements.

Figure 12: IT total cost per end-user ($US)

TechnologyOther

LaborOutsourcing

Retail median Retaillow-cost

performer

$2,567

$1,652

Figure 12: IT total cost per end-user ($US)

TechnologyOther

LaborOutsourcing

Retail median Retaillow-cost

performer

2,567

1,652

Figure 13: Finance cost as a percent of sales

TechnologyOther

LaborOutsourcing

Retail median Retaillow-cost

performer

0.57%

0.78%

SGA book of metrics for retail 8

Looking forward

More than ever, retail executives need timely, relevant, industry-specific data to make effective business decisions, to assess priorities and to develop a plan for improvement in the areas that matter most. Through benchmarking, executives can:

Identify and quantify potential improvement opportunities, •Set reasonable, attainable performance goals and analyze trends from one year to the next, •Establish targets that make sense and evaluate the accuracy of forecasts, and •Perform competitive analysis that leads to fast, meaningful improvement.•

By comparing their organizations’ performance against measures like those found in our study, retail executives can get help in making fast, effective decisions based on relevant, objective information — not anecdotal experi-ence or estimates. The answer isn’t always to be lowest cost in every area; rather, the goal should be to find the position that makes the most sense for the organization’s overall business strategy. Hence, cost-reduction initiatives should not necessarily be aimed at reaching the low-cost performer level across all functions. Organizations should determine what percentage is achievable and what tactics could potentially reduce the opportunity gap.

Of course, some reduction initiatives are tactical and immediate; others are strategic and long-term. Cost reduc-tions should reflect a balance of short-, mid- and long-term objectives so executives can effectively lead their companies forward during challenging business cycles.

9

Approach and methodology

Taxonomy

This report is the result of a Deloitte Global Benchmarking Center study of store operations, general and admin-istrative process performance. We gathered fiscal-year 2008 data across 40 process categories in eight functions. By following a strict taxonomy, the researchers generated apples-to-apples comparisons necessary for meaningful performance measures:

StoreOperations

MerchandisingSupply Chain Management

Marketing

Manage store-level •inventory

Merchandise and sell •goods

Manage and plan store •operations

Manage customer •services

Manage and plan store •real estate

Merchandise buying, •vendor management, and category performance

Plan, allocate and replenish •merchandise

Develop and manage •pricing strategies

Manage store presentation •(planogramming and layout)

Develop and source private •label

Warehousing •management

Merchandise distribution•

Transportation •management

Manage supply chain •performance

Advertising•

Promotions and events•

Develop visual •merchandising

Manage customer •research

Information Technology

FinanceHuman

ResourcesSupport Services

Application development •and management

Controls and risk •management

Infrastructure technology •management

Planning, strategy and •services

Transaction processing•

General accounting/•financial reporting

Controls•

Tax and treasury•

Performance management•

Transaction processing•

Rewards administration•

Talent management•

Strategy and program •design

Aviation•

Communications services•

Environmental health and •safety

Executive office•

Legal•

Mergers and acquisitions•

Non-merchandise •procurement

Strategic planning•

Travel management•

SGA book of metrics for retail 10

Key definitions and methodology

Data normalized by:Sales • for store operations, merchandising, supply chain, marketing, finance, support servicesEnd-users• for information technologyEmployees• for human resources

Driver analysis:Examined select drivers in highest cost categories to •identify what factors impact them the most

Peer groups:Retail overall (all participants of study)•Apparel subsector•Other/Specialty subsector (retailers offering a specific •product type, such as toys or sporting goods)Private label peer group (participants with a high •percentage of sales from private label products; the median, or midpoint value, of “private label sales as a percent of total sales” is 98% for this peer group)Non-private label peer group•

Low-cost performers: Participating companies in the first quartile of the eight functions*

Median: Midpoint value of participants

Total SGA cost at the companies in the study: Labor: Fully loaded labor cost (compensation and •benefits) of employees, contractors and temporariesOutsourcing: Services provided by third-party vendors•Technology: Hardware, software, license fees, and •the related supportOther: Facilities, supplies, travel, training •

Process cost: Cost of labor plus outsourcing at the companies in the study

*Low-cost performers are not necessarily “best in class” along other meaningful dimensions, such as quality, innovation, or customer/employee satisfaction. The benchmarks in this study suggest possible cost-reduction opportunities, which must be balanced against growth strategies.

All study data and statistics referenced and presented in this report, as well as the representations made and opinions expressed, unless specifically described otherwise, pertain only to the participating organizations and their responses to the Deloitte Global Benchmarking Center study of retail process performance conducted in 2009.

3-year revenue CAGR

Total sales

Other/SpecialtyApparel

Gross margin

Employees

Stores

Min 1st Quartile Median 3rd Quartile Max

Retail banners

Average squarefootage per store

$59M $46.8B$2.6B$1.3B $7.0B

14 6,351689352 1,196

1 2021 4

-8.4% 26.2%2.1%-0.1% 11.0%

511 324,00019,5526,925 43,328

34%23% 27% 44% 67%

3,126 129,00011,8224,531 38,779

Profile of participants

11

Performance measures

The following is a list of sample metrics available to participants:

Demographics

Total sales

Three-year revenue CAGR

Employees

End-users

Domestic sales as % of total sales

Gross margin %

Number of retail banners

Number of stores

Average square footage per store

Baseline

Total SGA cost distribution by cost component

Total SGA cost distribution by function

Total SGA staff distribution by function

Executive summary

Total SGA cost as a percent of sales by function

Total SGA cost gap to low-cost performer by function

Eight largest cost gaps across all cost categories

Cost as a percent of total SGA cost

Total process cost as a percent of sales

Staff per $1B in sales by function

Store operations

Store operations cost as a % of sales (labor, outsourcing, technology, other)

Store operations cost allocation (labor, outsourcing, technology, other)

Store management cost allocation

Process category cost as % of sales

Store operations process category cost allocation

Total store operations FTEs per $1B revenue

Store operations fully loaded labor rate

Store operations total cost per store operations staff

Store operations total cost per store

Occupancy cost per store

Store operations process cost per store

Sales per sq ft selling space

Store operations cost per sq ft selling space

Sales per labor hour (SPLH)

Store associate turnover %

Inventory shrink %

Total shopper returns as % of total sales

Loss prevention process cost as a percent of sales

Merchandising

Merchandising cost as a % of sales (labor, outsourcing, technology, other)

Merchandising cost allocation (labor, outsourcing, technology, other)

Process category cost as % of sales

Merchandising process category cost allocation

Total merchandising FTEs per $1B revenue

Merchandising fully loaded labor rate

Sales per buyer

Average number of SKUs managed per buyer

Number active vendors

Number of purchase orders generated

% goods sourced domestically

Private label sales as % of total sales

% direct sales (online, catalog, phone) as % of total sales

% sales promoted

% sales on markdown

Supply chain

Supply chain cost as a % of sales (labor, outsourcing, technology, other)

Supply chain cost allocation (labor, outsourcing, technology, other)

Process category cost as % of sales

Supply chain process category cost allocation

Total supply chain FTEs per $1B revenue

Supply chain fully loaded labor rate

Inventory turns

Cartons picked per labor hour (pick function only)

% merchandise returns to warehouse

Vendor compliance offset $ as % of total revenue

Transportation cost per inbound carton

Transportation cost per outbound carton

Import order cycle time days

Import shipments routed via airfreight as % of total shipments

SGA book of metrics for retail 12

Marketing

Marketing cost as a % of sales (labor, outsourcing, technology, other)

Marketing cost allocation (labor, outsourcing, technology, other)

Process category cost as % of sales

Marketing process category cost allocation

Total marketing FTEs per $1B revenue

Marketing fully loaded labor rate

Advertising spend allocation

Customer loyalty spend as % of total sales

Information technology

Information technology cost as a % of sales (labor, outsourcing, technology, other)

Total IT FTE per $1B revenue

Total IT cost as a % of sales (net)

Total IT cost per end-user (labor, outsourcing, technology, other)

Total IT cost allocation (labor, outsourcing, tech-nology, other)

IT process category cost per end-user

IT process cost (labor, outsourcing) cost allocation

IT FTEs per 1000 end-user

IT fully loaded labor rate

Finance

Finance cost as a % of sales (labor, outsourcing, technology, other)

Finance cost allocation (labor, outsourcing, technology, other)

Finance process category cost as % of sales

Finance process category cost allocation

Total finance FTEs per $1B revenue

Total finance FTEs per company sales

Finance fully loaded labor rate

Cycle time - Number of business days from cut-off of first sub-ledger to GAAP general ledger close

# days payable outstanding (DPO)

Human resources

HR cost as a % of sales (labor, outsourcing, technology, other)

Total HR FTE per $1B revenue

Total HR cost per employee

HR cost allocation (labor, outsourcing, technology, other)

HR process category cost per employee

HR process category cost allocation

HR FTEs per 1000 employees

HR function fully loaded labor rate

Support services

Support services cost as a % of sales (labor, outsourcing, technology, other)

Support services cost allocation (labor, outsourcing, technology, other)

Support services process category cost as a % of sales

Support services process category cost allocation

Total support services FTE per $1B revenue

Support services function fully loaded labor rate

13

Representative participant list

Abercrombie & Fitch Co.•Academy Sports & Outdoors, Ltd.•Advance Auto Parts, Inc.•Aeropostale, Inc.•AnnTaylor Stores Corporation•Army and Air Force Exchange Service•Beall’s, Inc.•Best Buy Co., Inc.•Burlington Coat Factory Warehouse Corp•Canadian Tire Corporation, Limited•Carrefour SA•C.I. Hermeco Corporation•Coldwater Creek, Inc.•Cost Plus, Inc.•Decathlon SA •Dick’s Sporting Goods, Inc.•The Dress Barn, Inc.•The Finish Line, Inc.•Food Lion, LLC•Foot Locker, Inc.•The Gap, Inc.•Groupe ADEO (France)•Guess?, Inc.•The Gymboree Corporation•Harris Teeter, Inc.•

Additional participant categorization

Private label, 41%

Non-privatelabel, 35%

hhgregg, Inc.•Jos. A. Bank Clothiers, Inc.•Kibe•Kmart Corporation (Sears)•Limited Brands, Inc.•The Liquor Control Board of Ontario•Maurices Inc.•The Men’s Wearhouse, Inc.•Navy Exchange Service Command•Nordstrom, Inc.•Office Depot, Inc.•Pacific Sunwear of California, Inc.•Payless ShoeSource•PETCO Animal Supplies, Inc.•Sears Holdings Corporation•

Sears Canada, Inc. -Sears Domestic, Inc. -Lands’ End, Inc. -

Sephora USA, Inc.•Shoe Carnival, Inc.•The Sports Authority, Inc.•Toys “R” Us Holdings, Inc•The Wet Seal, Inc.•Williams-Sonoma, Inc.•The Yankee Candle Company, Inc. •

Participants by industry subsector

Apparel, 41%

Other/Specialty,35%

Other subsectors,24%

SGA book of metrics for retail 14

About the Global Benchmarking Center

Deloitte’s Global Benchmarking Center (GBC) was established to provide executives with industry-relevant metrics and insight. The GBC delivers this information through annual benchmark studies in areas such as sales, general and administrative (SG&A), finance and accounting, supply chain, information technology, human resources, and operations. The GBC has conducted studies in more than 600 global organizations since 2005. These studies are uniquely designed to provide industry-specific insight relevant to multiple functions.

Financial Services•Banking -Securities -Insurance -

Life Sciences and Health Care•Health Care Provider -Life Sciences -Health Plan -

Public Sector•Federal -State -Local -

Technology, Media and Telco•Media -Telecommunications -High Technology -

Consumer and Industrial Products•Aerospace and Defense -Automotive -Process & Industrial Products -Consumer Products -

Retail•Apparel -Other/Specialty -Private Label -Tourism, Hospitality and -Leisure

Energy and Resources•Oil and Gas -Mining -Power and Utilities -Water and Waste -Management

Industry

Store Operations•

Merchandising•

Supply Chain•

Marketing•

Information Technology•

Finance•

Human Resources•

Support Services•

Retail Functions

15

AuthorsRichard T. RothPrincipalNational Benchmarking Practice LeaderDeloitte Consulting LLPAtlanta, GA+1 404 942 [email protected]

Rod SidesPrincipal Retail Operations Excellence LeaderDeloitte Consulting LLPCharlotte, NC+1 704 887 [email protected]

ContributorsMark E. DanielGlobal Benchmarking CenterDeloitte Consulting LLPAtlanta, GA+1 404 631 [email protected]

Jean-Michel FallySenior ManagerDeloitte Consulting LLPIrving, TX+1 469 417 [email protected]

Andrew SimpsonGlobal Benchmarking CenterDeloitte Consulting LLPMcLean, VA+1 703 251 [email protected]

Participation in this study is open to all retailers. For information, visit www.deloitte.com/us/SGA4Retail, or contact:

Global Benchmarking CenterDeloitte Consulting LLP+1 866 897 [email protected]

To learn more about our Retail practice, visit us online at www.deloitte.com/us/Retail. Here you can access our complimentary Dbriefs webcast series, Deloitte Insights podcast program, innovative and practical industry research, and a lot more about the issues facing retailers from some of the industry’s most experienced minds.

Stacy JaniakVice Chairman & U.S. Retail LeaderDeloitte LLPTel: +1 312 486 [email protected]

John SchefflerPartner & U.S. Assurance Leader, RetailDeloitte & Touche LLPTel: +1 415 783 [email protected]

John RooneyPrincipal & U.S. Consulting Leader, RetailDeloitte Consulting LLPTel: +1 215 446 [email protected]

Lawrence HutterPartner, Deloitte UK & Global Consumer Business &Transportation Industry LeaderDeloitte Touche TohmatsuTel: +44 20 7303 [email protected]

Nancy WertheimPartner & U.S. Tax Leader, RetailDeloitte Tax LLPTel: +1 617 437 [email protected]

Sandra ViolaDirector of MarketingDeloitte Services LPTel: +1 212 436 [email protected]

For information about Deloitte LLP’s Retail services, contact:

This publication contains general information only and is based on the experiences and research of Deloitte practitioners. Deloitte is not, by means of this publication, rendering business, financial, investment, or other professional advice or services. This publication is not a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional advisor. Deloitte, its affiliates, and related entities shall not be responsible for any loss sustained by any person who relies on this publication.

Copyright © 2010 Deloitte Development LLC. All rights reserved.Member of Deloitte Touche Tohmatsu