U.S. PUBLIC EQUITY MARKETS ARE STAGNATING · 2020-01-01 · attractiveness of U.S. public equity...

17

U.S. PUBLIC EQUITY MARKETS ARE STAGNATING APRIL 2017

Transcript of U.S. PUBLIC EQUITY MARKETS ARE STAGNATING · 2020-01-01 · attractiveness of U.S. public equity...

U.S. PUBLIC EQUITY MARKETS ARESTAGNATING

APRIL 2017

2

U.S. PUBLIC EQUITY MARKETS ARE STAGNATING

April 2017

3

Members

Gregory Baer President, The Clearing House Association

Kenneth Bentsen, Jr. President & Chief Executive Officer, Securities Industry and Financial Markets Association

Andrew Berry Managing Director, Head of Regulatory Strategy and Initiatives, Americas, UBS

Jeffrey Brown Senior Vice President & Acting General Counsel, Charles Schwab

Tim Buckley Chief Investment Officer, Vanguard

Roel C. Campos Partner, Locke Lord Bissell & Liddell LLP; Former Commissioner, Securities and Exchange Commission

Jason Carroll Managing Director, Hudson River Trading

Benjamin M. Friedman William Joseph Maier Professor of Political Economy, Harvard University

Kenneth A. Froot Andre R. Jakurski Professor of Business Administration, Harvard Business School

Travers Garvin Director, Public Affairs, Kohlberg Kravis Roberts & Company

Adam Gilbert Global Regulatory Leader, Financial Services Advisory Practice, PricewaterhouseCoopers, LLP

Robert R. Glauber Adjunct Lecturer, Harvard Kennedy School of Government; Visiting Professor, Harvard Law; Former Chairman/CEO, NASD

Kenneth C. Griffin President & Chief Executive Officer, Citadel LLC

R. Glenn Hubbard Dean & Russell L. Carson Professor of Finance and Economics, Columbia Business School; Co-Chair, Committee

Wei Jiang Arthur F. Burns Professor of Free and Competitive Enterprise & Vice Dean for Curriculum and Instruction Dean’s Office, Columbia Business School

Steven A. Kandarian Chairman, President & Chief Executive Officer, MetLife, Inc.

Andrew Kuritzkes Executive Vice President & Chief Risk Officer, State Street Corporation

Theo Lubke Chief Regulatory Reform Officer, Securities Division, Goldman Sachs

Barbara G. Novick Vice Chairman, BlackRock

4

Sandra E. O’Connor Managing Director, Chief Regulatory Affairs Officer, J.P. Morgan Chase

Robert C. Pozen Senior Lecturer, MIT Sloan School of Management

Nancy Prior President, Fixed Income Division, Fidelity

Peter Solmssen Executive Vice President & General Counsel; Legal, Compliance, Regulatory Affairs & Government Affairs, AIG

William Schlich Global Banking and Capital Markets Leader, Ernst & Young

Hal S. Scott Nomura Professor, Director of the Program on International Financial Systems, Harvard Law School; Director, CCMR

John Shrewsberry Chief Financial Officer, Wells Fargo

Nicholas Silitch Senior Vice President & Chief Risk Officer, Prudential Financial

Leslie N. Silverman Partner, Cleary Gottlieb Steen & Hamilton LLP; Committee Legal Advisor

Jeffrey M. Solomon Chief Executive Officer, Cowen and Company

Makoto Takashima President and CEO, Sumitomo Mitsui Banking Corporation

John L. Thornton Chairman, The Brookings Institution; Co-Chair, Committee

Joseph Ucuzoglu Chairman and Chief Executive Officer, Deloitte & Touche LLP

Betty Whelchel U.S. Head of Public Policy & Regulatory Affairs, BNP Paribas

Candi Wolff Executive Vice President and Head of Global Government Affairs, Citigroup

Bill Woodley Global Chief Operating Officer & Deputy Chief Executive Officer for North America, Deutsche Bank

Yuqiang Xiao General Manager of ICBC New York, Industrial and Commercial Bank of China, LTD

5

The Committee is an independent 501(c)(3) research organization, financed by contributions from individuals, foundations, and corporations. The Committee’s membership includes thirty-seven leaders drawn from the finance, business, law, accounting, and academic communities. The Committee Co-Chairs are R. Glenn Hubbard, Dean of Columbia Business School, and John L. Thornton, Chairman of the Brookings Institution. The Committee’s Director is Hal S. Scott, Nomura Professor and Director of the Program on International Financial Systems at Harvard Law School.

Founded in 2006, the Committee undertook its first major report at the request of the incoming U.S. Secretary of the Treasury, Henry M. Paulson. Over ten years later, the Committee’s research continues to provide policymakers with an empirical and non-partisan foundation for public policy.

6

U.S. PUBLIC EQUITY MARKETS ARE STAGNATING

The public capital markets play a vital role in the U.S. economy, as they are the principal vehicle through which companies raise the funding necessary for growth and the principal repository for individual and institutional investment. Ultimately, the global economic leadership of the United States depends on the strength of these markets.

Ten years ago, at the request of Secretary of the Treasury Henry Paulson, the Committee on Capital Markets Regulation released a report finding that foreign companies were no longer going public on U.S. exchanges at historical rates and foreign companies listed on U.S. exchanges were delisting at an increasing rate.1 The attractiveness of U.S. public equity markets to foreign companies was clearly weakening.

Today, the Committee is releasing a new report finding that over the past ten years the

attractiveness of U.S. public equity markets to private U.S. companies has deteriorated, whereas the public equity markets of foreign countries, particularly China, have become increasingly attractive to private foreign companies.

The Committee believes that today’s stagnant IPO markets are a serious drag on U.S.

economic growth. For example, one study estimates that the slowing U.S. IPO market has resulted in the loss of 22 million American jobs over the course of a decade.2 The weak IPO market also makes it more difficult for venture investors to realize a return on their investments and thereby discourages the formation and growth of new venture capital funded businesses. As an example of the importance of the venture capital industry for the broader U.S. economy, a recent study found that venture-backed companies generate revenue equal to 20% of U.S. GDP.3

The Committee believes that excessive regulation and litigation risk are contributing to

the declining attractiveness of U.S. public equity markets. As a first step towards reinvigorating U.S. public equity markets, the Committee

recommends that the SEC work with private U.S. companies to better understand why they are not going public and whether specific regulatory changes could incentivize them to do so. As a second step, the SEC should empower U.S. shareholders of public companies to adopt a mandatory system of individual arbitration to replace securities class actions that are costing public companies and investors billions of dollars each year.

The Committee’s report has four parts. Part I evaluates trends in U.S. public equity

markets. Part II evaluates trends in U.S. private markets. Part III evaluates why private U.S. companies are avoiding U.S. public equity markets, with a particular focus on securities class actions. Part IV compares trends in foreign public equity markets to trends in U.S. public equity markets.

1 Committee on Capital Markets Regulation, The Competitive Position of the U.S. Public Equity Market (Dec. 2007), http://www.capmktsreg.org. 2 David Weild and Edward Kim, Grant Thornton, A Wake-Up Call for America, 27 (Nov. 2009). 3 IPO Task Force, Rebuilding the IPO OnRamp, 5 (Oct. 20, 2011), https://www.sec.gov/info/smallbus/acsec/rebuilding_the_ipo_on-ramp.pdf.

7

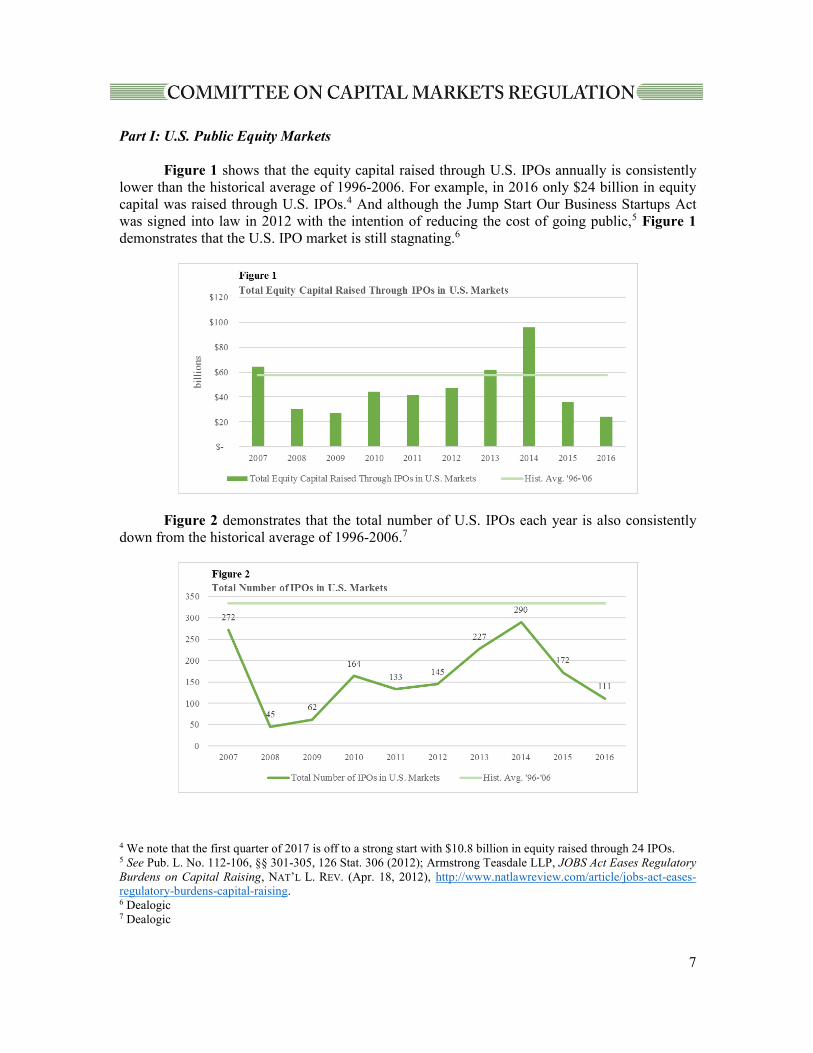

Part I: U.S. Public Equity Markets

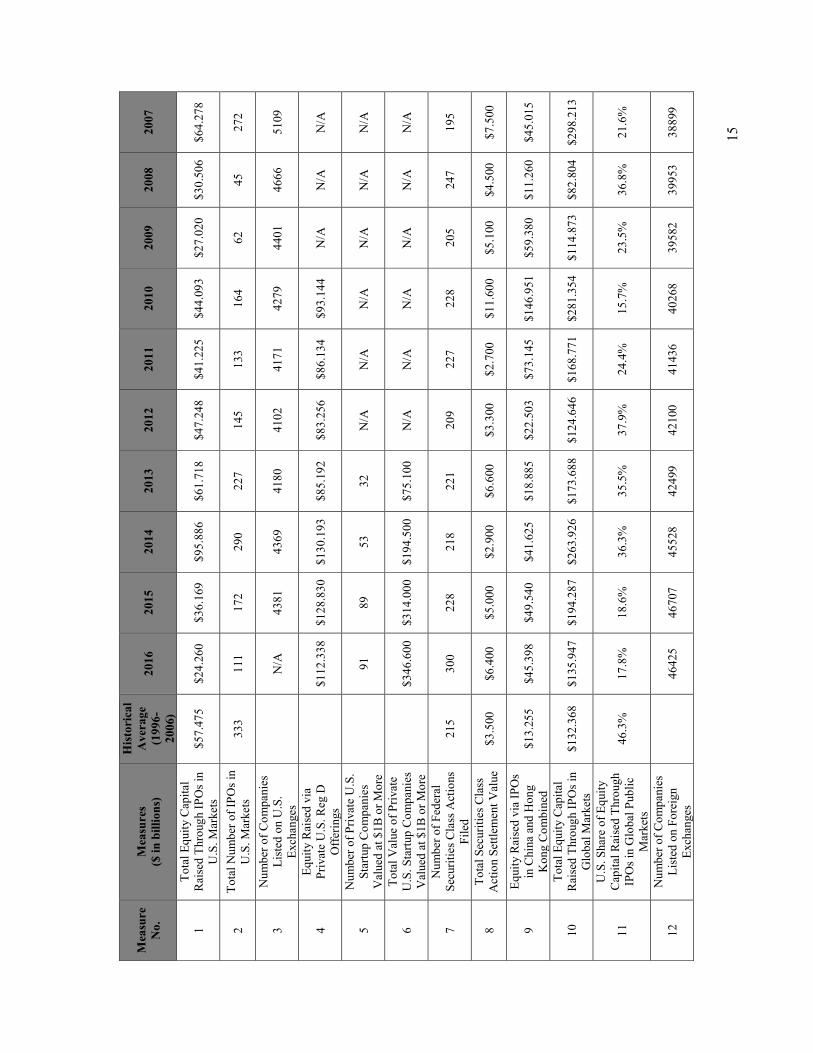

Figure 1 shows that the equity capital raised through U.S. IPOs annually is consistently lower than the historical average of 1996-2006. For example, in 2016 only $24 billion in equity capital was raised through U.S. IPOs.4 And although the Jump Start Our Business Startups Act was signed into law in 2012 with the intention of reducing the cost of going public,5 Figure 1 demonstrates that the U.S. IPO market is still stagnating.6

Figure 2 demonstrates that the total number of U.S. IPOs each year is also consistently down from the historical average of 1996-2006.7

4 We note that the first quarter of 2017 is off to a strong start with $10.8 billion in equity raised through 24 IPOs. 5 See Pub. L. No. 112-106, §§ 301-305, 126 Stat. 306 (2012); Armstrong Teasdale LLP, JOBS Act Eases Regulatory Burdens on Capital Raising, NAT’L L. REV. (Apr. 18, 2012), http://www.natlawreview.com/article/jobs-act-eases-regulatory-burdens-capital-raising. 6 Dealogic 7 Dealogic

8

Figure 3 shows that the number of public companies in the United States has been decreasing at a consistent pace in recent years and is now lower than it was in the 1980s.8 So not only are private companies not going public, but many public companies are also leaving U.S. public markets. This reduces U.S. investors’ ability to diversify their domestic equity portfolios.

Part II: U.S. Private Markets

On the other hand, the market for raising equity capital privately in the United States is strong. Figure 4 shows that more equity capital is raised by private Reg D offerings each year than is raised by U.S. IPOs.9 Furthermore, the market for raising equity capital privately is growing, whereas the U.S. IPO market is shrinking.

8 World Bank 9 Dealogic and FormDs.com. Does not include equity raised by pooled investment funds or REITs.

9

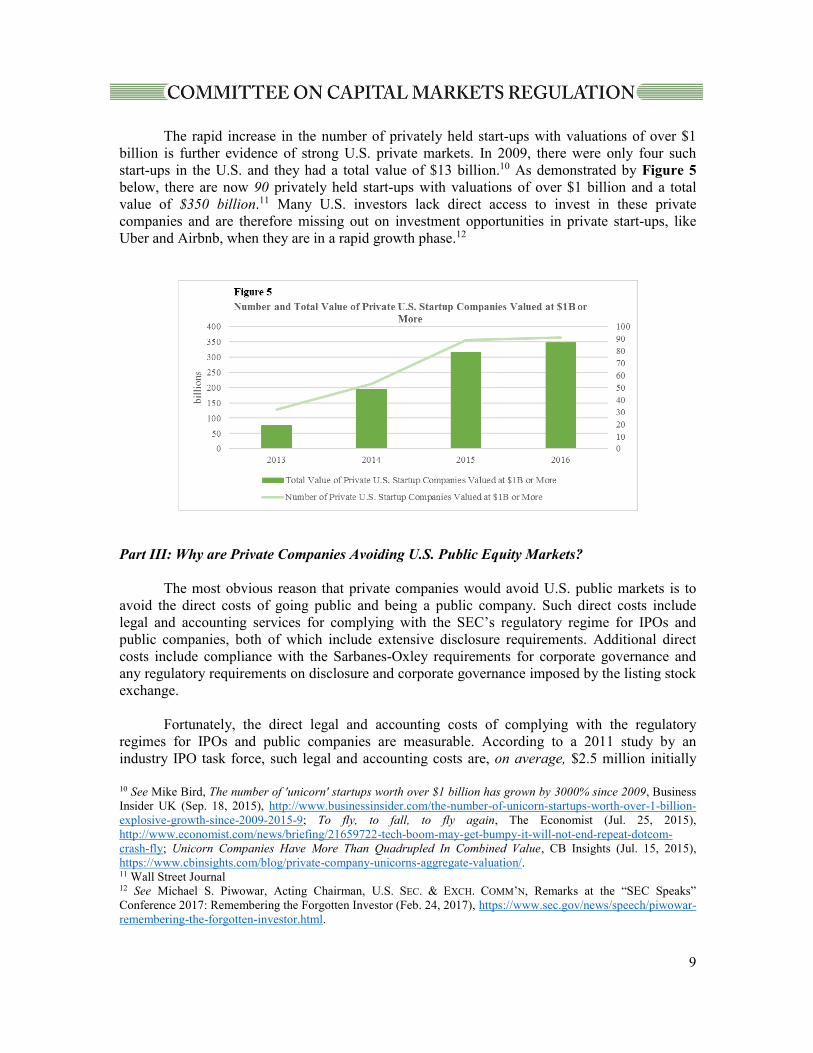

The rapid increase in the number of privately held start-ups with valuations of over $1 billion is further evidence of strong U.S. private markets. In 2009, there were only four such start-ups in the U.S. and they had a total value of $13 billion.10 As demonstrated by Figure 5 below, there are now 90 privately held start-ups with valuations of over $1 billion and a total value of $350 billion.11 Many U.S. investors lack direct access to invest in these private companies and are therefore missing out on investment opportunities in private start-ups, like Uber and Airbnb, when they are in a rapid growth phase.12

Part III: Why are Private Companies Avoiding U.S. Public Equity Markets?

The most obvious reason that private companies would avoid U.S. public markets is to avoid the direct costs of going public and being a public company. Such direct costs include legal and accounting services for complying with the SEC’s regulatory regime for IPOs and public companies, both of which include extensive disclosure requirements. Additional direct costs include compliance with the Sarbanes-Oxley requirements for corporate governance and any regulatory requirements on disclosure and corporate governance imposed by the listing stock exchange.

Fortunately, the direct legal and accounting costs of complying with the regulatory

regimes for IPOs and public companies are measurable. According to a 2011 study by an industry IPO task force, such legal and accounting costs are, on average, $2.5 million initially 10 See Mike Bird, The number of 'unicorn' startups worth over $1 billion has grown by 3000% since 2009, Business Insider UK (Sep. 18, 2015), http://www.businessinsider.com/the-number-of-unicorn-startups-worth-over-1-billion-explosive-growth-since-2009-2015-9; To fly, to fall, to fly again, The Economist (Jul. 25, 2015), http://www.economist.com/news/briefing/21659722-tech-boom-may-get-bumpy-it-will-not-end-repeat-dotcom-crash-fly; Unicorn Companies Have More Than Quadrupled In Combined Value, CB Insights (Jul. 15, 2015), https://www.cbinsights.com/blog/private-company-unicorns-aggregate-valuation/. 11 Wall Street Journal 12 See Michael S. Piwowar, Acting Chairman, U.S. SEC. & EXCH. COMM’N, Remarks at the “SEC Speaks” Conference 2017: Remembering the Forgotten Investor (Feb. 24, 2017), https://www.sec.gov/news/speech/piwowar-remembering-the-forgotten-investor.html.

10

and $1.5 million per year thereafter.13 Of course, these costs vary widely based on the size of the company.

While these direct costs may be excessive and unnecessary in certain respects, the

Committee believes that the indirect costs of being a public company are likely of greater concern to private companies considering a public offering. These indirect costs can be divided into two categories.

The first category of indirect costs that public companies face is reduced control over

their corporate disclosures and corporate governance,14 as compared to private companies. Specifically, mandatory corporate disclosures can make it more difficult to retain competitive advantages and can have a negative impact on a company’s ability to allocate capital efficiently.

For example, quarterly disclosure requirements can produce a volatile share price for

young public companies with unpredictable earnings. And a volatile share price complicates future capital raising and stock-based compensation, both of which are critically important to young and growing companies. Therefore, the existing one-size-fits-all disclosure regime for all public companies may result in short-term performance expectations that do not suit certain young and growing companies. As a result, these companies are better off avoiding public markets until their businesses have matured.

The Committee recommends that the SEC work with young and growing private

companies to better understand whether reduced control over corporate disclosures and corporate governance are encouraging them to avoid public markets and whether these issues can be addressed through changes in regulation.

The second category of indirect costs that public companies face is increased litigation

risk as compared to private companies, specifically the risk of securities class actions due to deficient corporate disclosures. This is true for two reasons. First, public offerings are subject to liability under Section 11 and Section 12(a)(2) of the Securities Act for false or misleading statements made in offering materials, whereas private offerings are not.15 Second, private companies are generally not subject to ongoing disclosure obligations, whereas public companies are subject to on-going disclosure obligations and bear litigation risk from any material misstatements in these disclosures or in their press releases more generally.16

Indeed, the mere filing of a securities class action suit has a material negative impact on a

public company’s market capitalization.17 For example, a recent study suggests that the filing of a class action lawsuit is associated with a nearly 12% drop in the defendant firm’s stock price.18

13 IPO Task Force, Rebuilding the IPO OnRamp, 10 (Oct. 20, 2011), https://www.sec.gov/info/smallbus/acsec/rebuilding_the_ipo_on-ramp.pdf. 14 It is noteworthy that public companies can provide founders and executives with voting control over corporate decisions by issuing nonvoting stock as part of a dual class share structure for an IPO. Indeed, Alphabet, Facebook, Alibaba and Snap all adopted a dual class share structure when they went public. 15 See 15 U.S.C. § 77k; 15 U.S.C. § 77l(a)(2); Gustafson v. Alloyd, 513 U.S. 561 (1995). 16 See 15 U.S.C. § 78m(a); 15 U.S.C. § 78o(d); 17 C.F.R. § 240.10b-5. 17 See e.g., Mark Klock, Do Class Action Filings Affect Stock Prices? The Stock Market Reaction to Securities Class Actions Post PSLRA, 15 J. Bus. & Sec. L. 109 (2016).

11

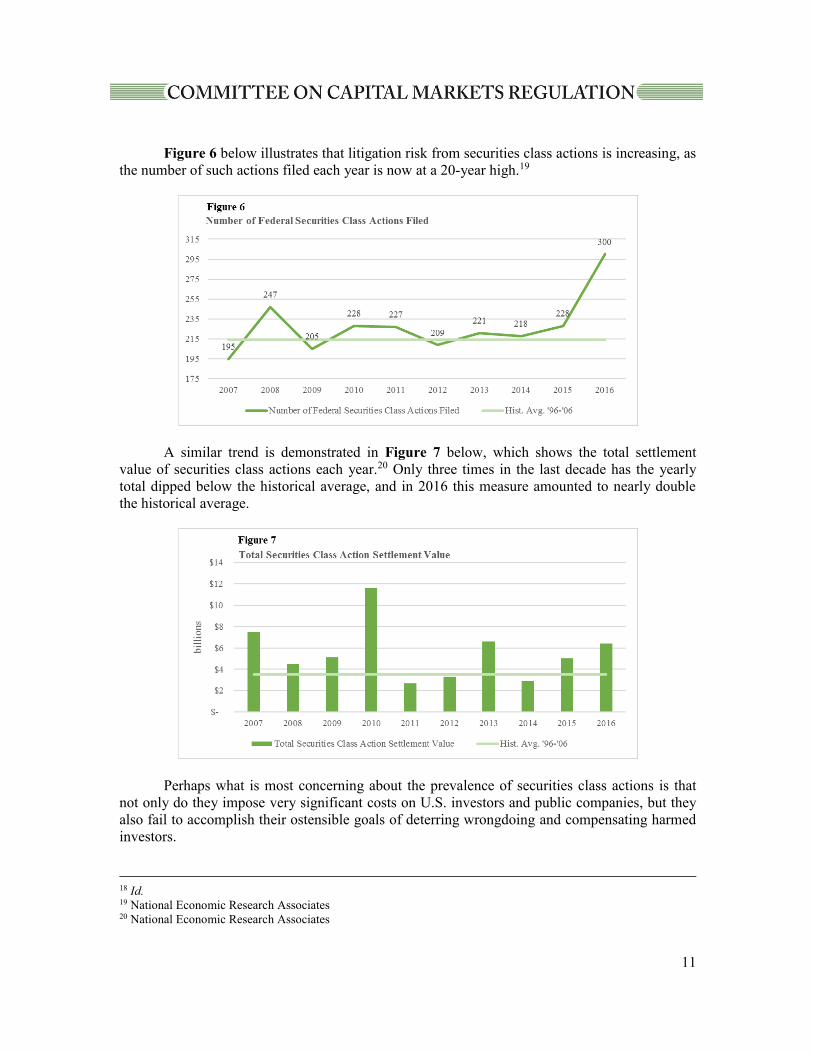

Figure 6 below illustrates that litigation risk from securities class actions is increasing, as

the number of such actions filed each year is now at a 20-year high.19

A similar trend is demonstrated in Figure 7 below, which shows the total settlement value of securities class actions each year.20 Only three times in the last decade has the yearly total dipped below the historical average, and in 2016 this measure amounted to nearly double the historical average.

Perhaps what is most concerning about the prevalence of securities class actions is that not only do they impose very significant costs on U.S. investors and public companies, but they also fail to accomplish their ostensible goals of deterring wrongdoing and compensating harmed investors.

18 Id. 19 National Economic Research Associates 20 National Economic Research Associates

12

Securities class action lawsuits are often settled for a very small fraction of the damages claimed, and a third or more of that settlement amount will usually be paid out to the plaintiffs’ attorneys.21 Typically, a significant portion of the funds recovered in securities class actions is not even distributed to members of the class.22 Furthermore, these suits do little to deter bad behavior, as individual directors and officers rarely pay for any part of the plaintiffs’ recovery.23 Instead, as former SEC Commissioner Paul Atkins explains, “the costs of defending and settling these suits are borne by the company’s shareholders, leading to an absurd situation in which money is merely shifted from one group of innocent investors to another, with plaintiff and defense attorneys siphoning off billions of dollars in the process.”24

Fortunately, the SEC is well positioned to immediately address this problem by

empowering shareholders to adopt a mandatory system of individual arbitration to replace securities class action litigation. Indeed, shareholders have demonstrated a preference for arbitrating these claims by proposing such provisions in the past.25 However, the SEC has arguably overstepped its statutory authority by blocking these past attempts.26 We urge the agency to step aside and permit such shareholder decisions in the future. Part IV: Global Trends in Public Equity Markets

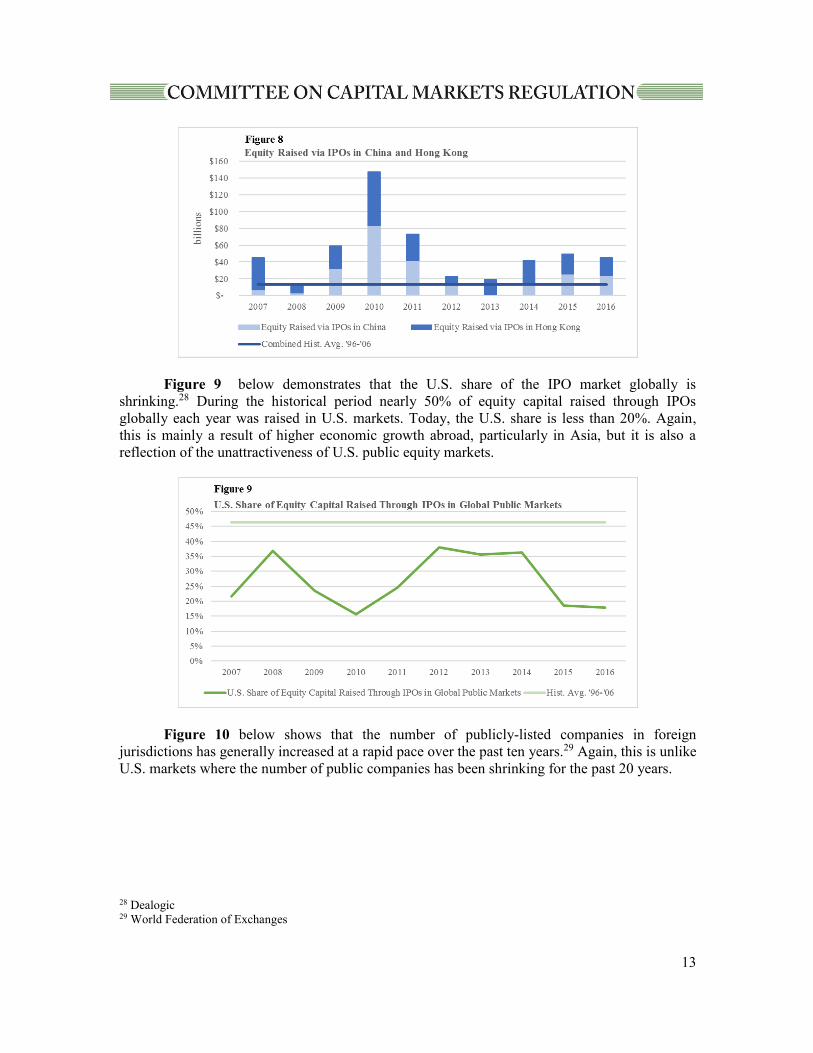

Figure 8 demonstrates that the IPO markets in China and Hong Kong have been strong in recent years, particularly as compared to historical averages.27 The value of IPOs in Chinese markets now regularly exceeds the value of IPOs in the United States. In 2016 almost $50 billion was raised through IPOs in China and Hong Kong, whereas only $24 billion was raised through IPOs in the United States. To a large extent this reflects higher economic growth rates in China but it is significant that public equity markets in both China and Hong Kong have grown increasingly attractive to private companies over the past ten years even though the economic growth rate in China has remained largely flat.

21 Hal S. Scott & Leslie N. Silverman, Stockholder Adoption of Mandatory Individual Arbitration for Stockholder Disputes, 36 Harv. J.L. & Pub. Pol’y 1187, 1192-93 (2013). 22 Id. at 1193. 23 Id. at 1197. 24 Paul Atkins, The Supreme Court’s Opportunity to End Abusive Class Action Securities Laws, Forbes (Mar. 4, 2014), https://www.forbes.com/sites/realspin/2014/03/04/the-supreme-courts-opportunity-to-end-abusive-securities-class-action-lawsuits. 25 See Pfizer Inc., SEC No‐ Action Letter (Feb. 22, 2012); Gannett Co., Inc., SEC No‐ Action Letter (Feb. 22, 2012). 26 Hal S. Scott & Leslie N. Silverman, Stockholder Adoption of Mandatory Individual Arbitration for Stockholder Disputes, 36 Harv. J.L. & Pub. Pol’y 1187, 1221-22 (2013). 27 Dealogic

13

Figure 9 below demonstrates that the U.S. share of the IPO market globally is shrinking.28 During the historical period nearly 50% of equity capital raised through IPOs globally each year was raised in U.S. markets. Today, the U.S. share is less than 20%. Again, this is mainly a result of higher economic growth abroad, particularly in Asia, but it is also a reflection of the unattractiveness of U.S. public equity markets.

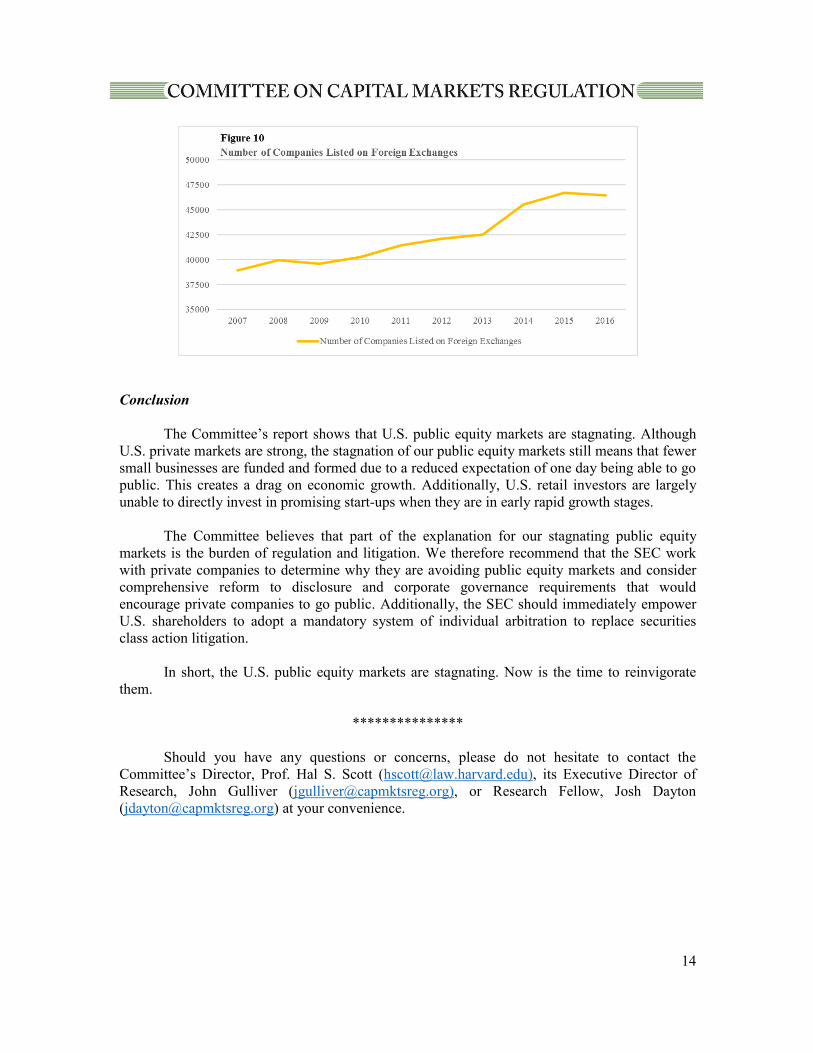

Figure 10 below shows that the number of publicly-listed companies in foreign jurisdictions has generally increased at a rapid pace over the past ten years.29 Again, this is unlike U.S. markets where the number of public companies has been shrinking for the past 20 years.

28 Dealogic 29 World Federation of Exchanges

14

Conclusion

The Committee’s report shows that U.S. public equity markets are stagnating. Although U.S. private markets are strong, the stagnation of our public equity markets still means that fewer small businesses are funded and formed due to a reduced expectation of one day being able to go public. This creates a drag on economic growth. Additionally, U.S. retail investors are largely unable to directly invest in promising start-ups when they are in early rapid growth stages.

The Committee believes that part of the explanation for our stagnating public equity

markets is the burden of regulation and litigation. We therefore recommend that the SEC work with private companies to determine why they are avoiding public equity markets and consider comprehensive reform to disclosure and corporate governance requirements that would encourage private companies to go public. Additionally, the SEC should immediately empower U.S. shareholders to adopt a mandatory system of individual arbitration to replace securities class action litigation.

In short, the U.S. public equity markets are stagnating. Now is the time to reinvigorate

them.

***************

Should you have any questions or concerns, please do not hesitate to contact the Committee’s Director, Prof. Hal S. Scott ([email protected]), its Executive Director of Research, John Gulliver ([email protected]), or Research Fellow, Josh Dayton ([email protected]) at your convenience.

15

Mea

sure

N

o.

Mea

sure

s ($

in b

illio

ns)

His

tori

cal

Ave

rage

(1

996-

2006

)

2016

20

15

2014

20

13

2012

20

11

2010

20

09

2008

20

07

1 To

tal E

quity

Cap

ital

Rai

sed

Thro

ugh

IPO

s in

U.S

. Mar

kets

$5

7.47

5 $2

4.26

0 $3

6.16

9 $9

5.88

6 $6

1.71

8 $4

7.24

8 $4

1.22

5 $4

4.09

3 $2

7.02

0 $3

0.50

6 $6

4.27

8

2 To

tal N

umbe

r of I

POs i

n U

.S. M

arke

ts

333

111

172

290

227

145

133

164

62

45

272

3 N

umbe

r of C

ompa

nies

Li

sted

on

U.S

. Ex

chan

ges

N

/A

4381

43

69

4180

41

02

4171

42

79

4401

46

66

5109

4 Eq

uity

Rai

sed

via

Priv

ate

U.S

. Reg

D

Off

erin

gs

$1

12.3

38

$128

.830

$1

30.1

93

$85.

192

$83.

256

$86.

134

$93.

144

N/A

N

/A

N/A

5 N

umbe

r of P

rivat

e U

.S.

Star

tup

Com

pani

es

Val

ued

at $

1B o

r Mor

e

91

89

53

32

N/A

N

/A

N/A

N

/A

N/A

N

/A

6 To

tal V

alue

of P

rivat

e U

.S. S

tartu

p C

ompa

nies

V

alue

d at

$1B

or M

ore

$3

46.6

00

$314

.000

$1

94.5

00

$75.

100

N/A

N

/A

N/A

N

/A

N/A

N

/A

7 N

umbe

r of F

eder

al

Secu

ritie

s Cla

ss A

ctio

ns

File

d 21

5 30

0 22

8 21

8 22

1 20

9 22

7 22

8 20

5 24

7 19

5

8 To

tal S

ecur

ities

Cla

ss

Act

ion

Settl

emen

t Val

ue

$3.5

00

$6.4

00

$5.0

00

$2.9

00

$6.6

00

$3.3

00

$2.7

00

$11.

600

$5.1

00

$4.5

00

$7.5

00

9 Eq

uity

Rai

sed

via

IPO

s in

Chi

na a

nd H

ong

Kon

g C

ombi

ned

$13.

255

$45.

398

$49.

540

$41.

625

$18.

885

$22.

503

$73.

145

$146

.951

$5

9.38

0 $1

1.26

0 $4

5.01

5

10

Tota

l Equ

ity C

apita

l R

aise

d Th

roug

h IP

Os i

n G

loba

l Mar

kets

$1

32.3

68

$135

.947

$1

94.2

87

$263

.926

$1

73.6

88

$124

.646

$1

68.7

71

$281

.354

$1

14.8

73

$82.

804

$298

.213

11

U.S

. Sha

re o

f Equ

ity

Cap

ital R

aise

d Th

roug

h IP

Os i

n G

loba

l Pub

lic

Mar

kets

46.3

%

17.8

%

18.6

%

36.3

%

35.5

%

37.9

%

24.4

%

15.7

%

23.5

%

36.8

%

21.6

%

12

Num

ber o

f Com

pani

es

List

ed o

n Fo

reig

n Ex

chan

ges

46

425

4670

7 45

528

4249

9 42

100

4143

6 40

268

3958

2 39

953

3889

9

50 Church Street, 3rd Floor, Cambridge, MA 02138 www.capmktsreg.org

16

134 Mount Auburn Street, Cambridge, MA 02138www.capmktsreg.org