US PE Breakdown - PitchBookfiles.pitchbook.com/pdf/PitchBook_2016_Annual_US_PE... · 2017-01-20 ·...

16

2016 Annual US PE Breakdown In partnership with Co-sponsored by

Transcript of US PE Breakdown - PitchBookfiles.pitchbook.com/pdf/PitchBook_2016_Annual_US_PE... · 2017-01-20 ·...

2016 Annual

US PE Breakdown

In partnership with

Co-sponsored by

FINANCIAL TRANSACTIONS & REPORTING | MARKETING & COMMUNICATIONS FOR REGULATED INDUSTRY | CUSTOMER CONTENT & COLLABORATION SOLUTIONS

MERRILL DATASITE

This year, Merrill DataSite reached the 1 billion mark.

That’s 1 billion pages uploaded to our award-winning virtual data room since 2004.

Thousands of companies worldwide trust us to securely host their confidential information. Our single platform exists to support your rapidly changing needs.

Contact us to see how we can help you with your next transaction.

merrillcorp.com

© Merrill Communications LLC. All rights reserved.

Reaching the summit is no small feat.

1,000,000,000PAGES UPLOADED

41,000+VIRTUAL DATA ROOM PROJECTS SECURED

SINCE 2003

31,000+M&A TRANSACTIONS

SINCE 2003

20TECHNOLOGY AWARDS

IN THE PAST 8 YEARS

14LANGUAGES

SPOKEN

Credits & ContactPitchBook Data, Inc.

JOHN GABBERT Founder, CEO

ADLEY BOWDEN Vice President,

Market Development & Analysis

Content

NIZAR TARHUNI Senior Analyst

DYLAN COX Analyst

BRYAN HANSON Data Analyst

JENNIFER SAM Senior Graphic Designer

Contact PitchBook pitchbook.com

RESEARCH

EDITORIAL

SALES

COPYRIGHT © 2017 by PitchBook Data, Inc. All rights reserved. No part of this publication may be reproduced in any form or by any means—graphic, electronic, or mechanical, including photocopying, recording, taping, and information storage and retrieval systems—without the express written permission of PitchBook Data, Inc. Contents are based on information from sources believed to be reliable, but accuracy and completeness cannot be guaranteed. Nothing herein should be construed as any past, current or future recommendation to buy or sell any security or an offer to sell, or a solicitation of an offer to buy any security. This material does not purport to contain all of the information that a prospective investor may wish to consider and is not to be relied upon as such or used in substitution for the exercise of independent judgment.

Introduction 4

Overview 5-6

Deal Multiples & Debt Levels 7

Q&A: Merrill Corporation 8

Deals by Size & Sector 9

Exits 11-12

Fundraising 13-14

League Tables 15

Contents

The PitchBook PlatformThe data in this report comes from the PitchBook Platform–our data software for

VC, PE and M&A. Contact [email protected] to request a free trial.

IN PARTNERSHIP WITH

3 PITCHBOOK 2016 ANNUAL US PE BREAKDOWN

CO-SPONSORED BY

IntroductionKey takeaways

» Pricing stifles private equity deal flow in 2016

» Heightened company inventory limiting available targets while also raising

suspicion around portfolio company quality

» Tech and energy investment experience growth

» Median equity contributions jump to 5.4x EBITDA

» More managers than ever before hit their fundraising targets in 2016

If 2014 was a record-setting year for PE, and 2015 a turning point, then 2016

can be characterized as the first step toward normalcy. Buyout activity receded

amidst the growing concerns about global trade, rising populism and central

bank policies that we know all too well. It must be noted, however, that PE

transactions occur on a deal-by-deal basis, not a global basis. As such, managers

have continued to find pockets of growth and opportunity, particularly in the

tech and energy sectors.

In today’s tough environment, many large corporates have resorted to competing

with PE firms, thereby pushing up multiples and squeezing out any margin for

error. Due diligence and deal sourcing have become as important as ever before,

and firms will have to become more creative in the ways they produce alpha and

hedge against any downside.

PE exits and fundraising also fell in 2016, though more managers are meeting

their stated fundraising goals. As we look to the coming year, we expect more

of the same in terms of deal flow, but a more competitive environment could

drive down returns and prompt some hesitation around future allocations toward

the asset class. In the end though, the best managers will continue to garner

outsized contributions and return sufficient capital to their partners.

We hope this report is useful in your practice. Please feel free to contact us at

[email protected] with any questions or comments.

DYLAN COX

Analyst

Look up a company.

And its cap table.

And its investors.

And its EBITDA

multiples.

And its board

members.

In seconds.

The PitchBook Platform

has the data you need

to close your next deal.

Learn more at

pitchbook.com

IN PARTNERSHIP WITH

4 PITCHBOOK 2016 ANNUAL US PE BREAKDOWN CO-SPONSORED BY

Transaction value stays highOverview

Deal value remained robust

$649 billion in PE transactions were

completed across 3,538 deals last year,

representing 12% and 14% year-over-

year decreases, respectively. As we

noted throughout the year, the falling-

off can be mostly attributed to both an

expensive market and a lack of quality

acquisition targets. Median EV/EBITDA

for M&A transactions (including

buyouts) in the US this year hit 10.9x,

nearly a full turn higher than 2015’s

10.0x and far above the 7.9x figure we

recorded in 2010.

Strategic competition here to stay?

These higher multiples were caused

in part by competition from strategic

acquirers, which continues to

hamstring PE dealmaking. At the

time of this writing, the S&P 500 was

trading at a price-to-earnings ratio

of approximately 26, compared to

a post-financial-crisis low of about

13.5 in September of 2011. That is, on

average, a company in the S&P 500

has about double the purchasing

power now, denominated in their

own stock, as they did five years ago.

Further, this multiple expansion also

re-emphasizes the pricing level at

which PE has to play at today, thus, it’s

no wonder that PE firms are feeling

some of those side effects. In 2017,

we’ll be keeping a close eye on public

company valuations and their effect on

PE pricing.

Lack of buyout targets

In any given sector or geography,

there are a finite number of companies

that can reasonably service the debt

loads necessary for producing the

returns that buyout producers expect.

An expensive market contributes to declining activity amid high value

US PE activity

Source: PitchBook. Unknown deal values are estimated based on known figures.

$513

$905

$366

$165

$357

$422

$477

$512

$650

$737

$649

2,813

3,486

2,732

1,845

2,7103,036

3,423

3,321

4,098 4,131

3,538

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Deal Value ($B) # of Deals Closed

US PE-backed company inventory

1,5181,699

1,9312,260

2,6233,043

3,6054,206

4,7114,923

5,2525,570

5,9236,201

6,5446,912 7,168

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

2011-2016

2006-2010

2000-2005

Pre-2000

Year of Investment

Source: PitchBook

IN PARTNERSHIP WITH

5 PITCHBOOK 2016 ANNUAL US PE BREAKDOWN

CO-SPONSORED BY

Add-ons retain a commanding proportion

US add-on % of buyout activity

At the end of 2016, there were 7,168

PE-backed companies in the US, a 46%

increase from the 4,923 companies

in 2009. This has left investors with

limited quality options for putting

capital to work. Not to say that the US

economy is by any means saturated

in terms of financial sponsorship, but

opportunities will become harder to

find if the pace of capital investment

continues to exceed economic growth.

Add-ons keep adding up

With prices as high as they are, it has

become imperative for firms to use

buy-and-build strategies in order to

blend multiples and create a lower

aggregate pricing for their portfolio

acquisitions. In addition, managers

can utilize this strategy to ensure

a higher exit price as they build a

more comprehensive business. Add-

ons made up 64% of buyout activity

last year, up from 61% in 2015 and

the highest proportion we’ve ever

recorded. As this trend continues to

play out, deal sourcing will become

even more important and single-

platform operational improvements

will be expected at the bare minimum.

Most notably, there were 283 add-

ons in the healthcare industry,

which continues to see increased

consolidation amidst speculation

about potential changes to the

Affordable Care Act.

IT out-computes the rest

The tech sector saw more investment

from PE firms in 2016 than it did at

any time in the last 15 years. 567

deals were completed, worth a total

of $159.8 billion. Granted, $60 billion

of that sum can be attributed to the

Dell/EMC take-private that closed in

September. But even excluding that

transaction, PE investment in the IT

sector would have grown by 10.8%

this year. As more venture-backed

companies stay private for longer

amidst a sluggish VC-backed exit

market, we see an opportunity for PE

investors to step in and help provide

liquidity for aging venture portfolio

companies. Further, we believe the PE

operational and management model

is well-suited for already established

and fast-growing companies, and the

ability to enter transactions as patient

capital will also allow PE sponsors

to move such companies through

lucrative exits down the road.

Energy

PE investors purchased $55.8 billion

worth of energy companies in 2016,

up 31% from the prior year. It seems

as though investors are finally getting

used to $50-a-barrel oil and that

the gap between buyer and seller

expectations for the future of industry

has narrowed. Supporting the truism

that necessity is the mother of

invention, many E&P companies are

finding new ways to stay profitable

in the low oil-price environment.

Lastly, all signs from the incoming

administration point to deregulation in

the industry, which could spur a new

wave of investment activity.

1,11

1

1,33

2

1,50

4

1,41

5 1,85

5

1,92

2

1,71

9

938

993

1,16

3

952

1,17

7

1,20

9

963

54%

57%56%

60%

61% 61%

64%

2010 2011 2012 2013 2014 2015 2016

Non Add-on Add-on Add-on % of Buyout

Source: PitchBook

Boom in IT deal value

US PE activity in IT & energy

210213

551 567

0

100

200

300

400

500

600

$0

$50

$100

$150

$200

$250

2010 2011 2012 2013 2014 2015 2016Energy Deal Value ($B) IT Deal Value ($B)

# of Energy Deals Closed # of IT Deals ClosedSource: PitchBook.

Unknown deal values are estimated based on known figures.

IN PARTNERSHIP WITH

6 PITCHBOOK 2016 ANNUAL US PE BREAKDOWN

CO-SPONSORED BY

Pricing pressures take tollDeal multiples & debt levels

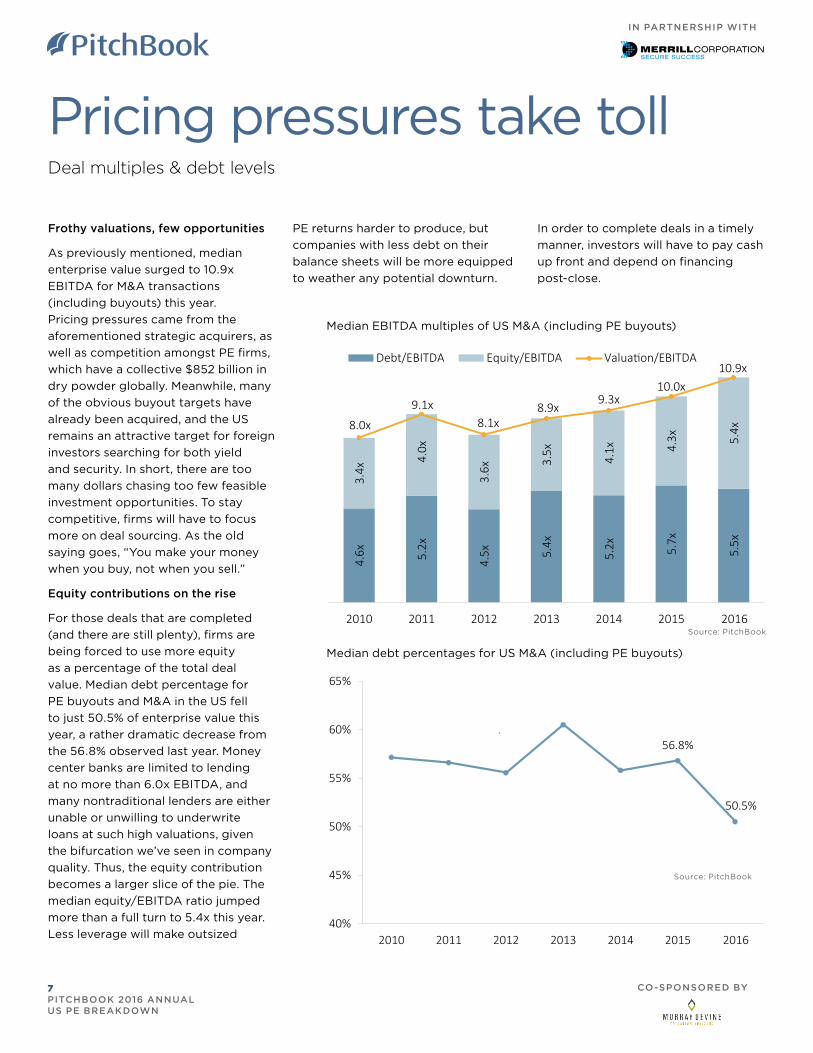

Frothy valuations, few opportunities

As previously mentioned, median

enterprise value surged to 10.9x

EBITDA for M&A transactions

(including buyouts) this year.

Pricing pressures came from the

aforementioned strategic acquirers, as

well as competition amongst PE firms,

which have a collective $852 billion in

dry powder globally. Meanwhile, many

of the obvious buyout targets have

already been acquired, and the US

remains an attractive target for foreign

investors searching for both yield

and security. In short, there are too

many dollars chasing too few feasible

investment opportunities. To stay

competitive, firms will have to focus

more on deal sourcing. As the old

saying goes, “You make your money

when you buy, not when you sell.”

Equity contributions on the rise

For those deals that are completed

(and there are still plenty), firms are

being forced to use more equity

as a percentage of the total deal

value. Median debt percentage for

PE buyouts and M&A in the US fell

to just 50.5% of enterprise value this

year, a rather dramatic decrease from

the 56.8% observed last year. Money

center banks are limited to lending

at no more than 6.0x EBITDA, and

many nontraditional lenders are either

unable or unwilling to underwrite

loans at such high valuations, given

the bifurcation we’ve seen in company

quality. Thus, the equity contribution

becomes a larger slice of the pie. The

median equity/EBITDA ratio jumped

more than a full turn to 5.4x this year.

Less leverage will make outsized

Median EBITDA multiples of US M&A (including PE buyouts)

Median debt percentages for US M&A (including PE buyouts)

4.6x 5.

2x

4.5x 5.

4x

5.2x 5.7x

5.5x

3.4x

4.0x

3.6x 3.

5x 4.1x 4.

3x 5.4x8.0x

9.1x8.1x

8.9x9.3x

10.0x10.9x

2010 2011 2012 2013 2014 2015 2016

Debt/EBITDA Equity/EBITDA Valuation/EBITDA

56.8%

50.5%

40%

45%

50%

55%

60%

65%

2010 2011 2012 2013 2014 2015 2016

Source: PitchBook

Source: PitchBook

PE returns harder to produce, but

companies with less debt on their

balance sheets will be more equipped

to weather any potential downturn.

In order to complete deals in a timely

manner, investors will have to pay cash

up front and depend on financing

post-close.

IN PARTNERSHIP WITH

7 PITCHBOOK 2016 ANNUAL US PE BREAKDOWN

CO-SPONSORED BY

How would a rise in interest rates

affect the financing packages

available to PE investors?

Not as much as you would have

thought back when the “taper

tantrum” was fresh in everyone’s

memory. Since its move was

telegraphed throughout the year, the

Fed’s decision was hardly surprising

and consequently fund managers and

lenders were prepared to price in an

increase. That said, investors will do

well to plan for subsequent increases

by maintaining intensive scrutiny of

prospective targets, keeping close

watch on the ability of some of their

pricier recent acquisitions to service

debt loads, and continuing to utilize

nonbank mid-cap lenders that employ

select syndication on deals to minimize

execution risk.

We saw PE EBITDA multiples grow

even higher in 2016. Do you think the

current pricing is sustainable from a

returns standpoint?

In a few cases the pricing will turn

out to be sustainable or worthwhile.

However, it will be a tall order for

many fund managers to ensure that

the high prices they paid recently

end up being worth it. There are ways

and means to do so, all of which take

considerable time and effort, which is

why we’ve been hearing more about

lengthening fundraising cycles and

investment timelines in limited partner

agreements plus observing decreasing

buyout activity. Some firms will be able

to handle these adjustments sooner

than others, while all would do well to

emphasize the long term to their fund

investors.

Richard A. Martin, Jr. Senior Director

Merrill Corporation

Richard A. Martin, Jr. is a Senior Director at Merrill Corporation, responsible for Merrill DataSite’s global marketing group. His 18 years of marketing experience working and residing in the US, U.K. and Europe has developed Martin’s understanding of disparate business cultures and the global financial industry, evidenced by a successful record of growing businesses. Martin currently works closely with financial professionals to provide first class virtual data room (VDR) solutions for their transaction and due diligence needs. Prior to joining Merrill, Martin led the hedge fund marketing strategy group at Morgan Stanley Capital International and the global equity product strategy group at Reuters International, London. He received his B.A. from Dartmouth College, a marketing certificate from the University of Michigan Business School and currently resides in New York City with his wife and children.

If the Affordable Care Act is repealed

or replaced, how will that affect PE

investors in the healthcare sector?

There are still stable and growing

healthcare needs. The bigger question

mark is around the significant growth

of the number of insured within the

US. Those PE firms that targeted

acquisitions looking to capitalize on

expansion of coverage to underserved

populations or similar population

growth will have to take repeal into

account, but as there would be

significant political costs from taking

away insurance policies without some

type of replacement offered that could

end up being effectively similar, it is

still definitely a waiting game. Frankly,

the typical challenges of investing

in healthcare are still PE managers’

primary concerns.

Secondary buyouts made up a larger

portion of PE-backed exits this year.

Do you expect this trend to continue

in 2017?

Yes in terms of proportion, not

necessarily in terms of actual counts.

PE firms will still be looking to either

execute a rapid sale of their best-

positioned portfolio companies while

valuations remain high or further

optimize their portfolios by offloading

businesses with which they’ve done as

much as they could to more specialist

PE managers. Obtaining liquidity will,

of course, always remain a consistent

driver, and in light of slowly declining

M&A plus the choppy IPO market,

there only remain so many other

means of sale.

ABOUT MERRILL CORPORATION

Merrill Corporation provides technology-enabled platforms for secure content sharing, regulated communications and

disclosure services. Clients trust Merrill’s innovative applications and deep subject expertise to successfully navigate the

secure sharing of their most sensitive content, perfect and distribute critical financial and regulatory disclosures, and create

customized communications across stakeholders. With more than 3,800 people in 41 locations worldwide, clients turn to

Merrill when their need to manage complex content intersects with the need to collaborate securely around the globe.

SPONSORED BY

8 PITCHBOOK 2016 ANNUAL US PE BREAKDOWN

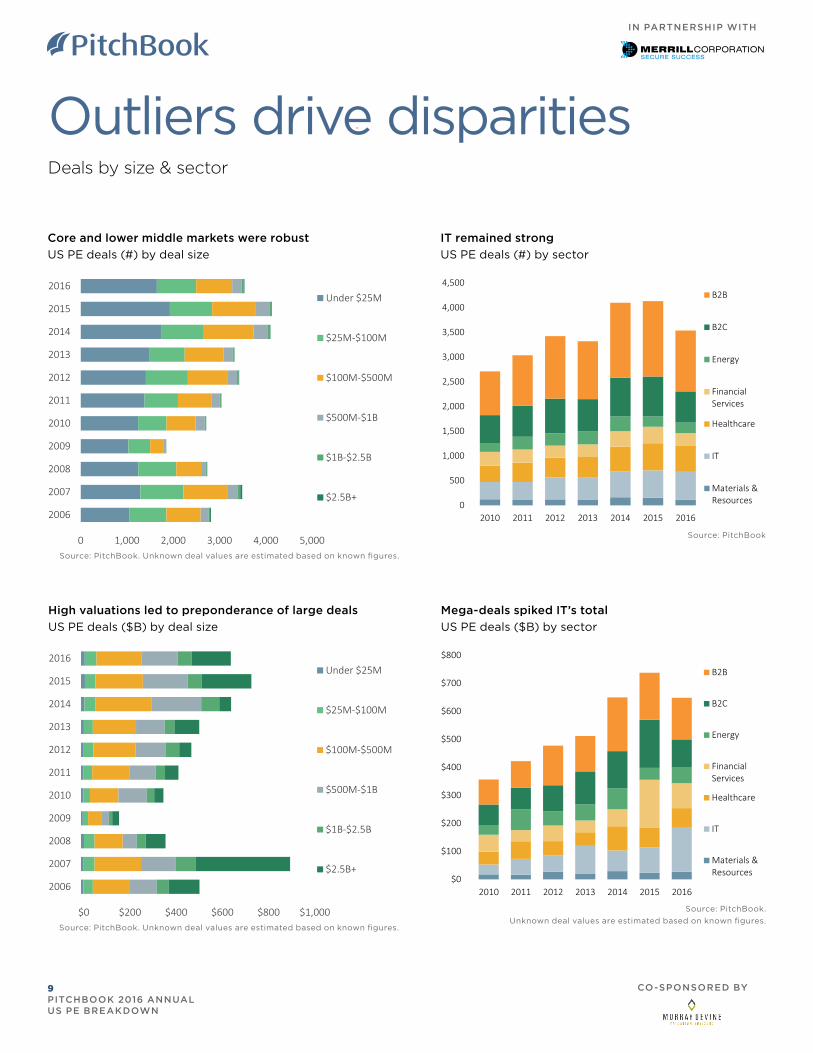

Mega-deals spiked IT’s total

US PE deals ($B) by sector

IT remained strong

US PE deals (#) by sector

Core and lower middle markets were robust

US PE deals (#) by deal size

High valuations led to preponderance of large deals

US PE deals ($B) by deal size

0 1,000 2,000 3,000 4,000 5,000

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016Under $25M

$25M-$100M

$100M-$500M

$500M-$1B

$1B-$2.5B

$2.5B+

$0 $200 $400 $600 $800 $1,000

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016Under $25M

$25M-$100M

$100M-$500M

$500M-$1B

$1B-$2.5B

$2.5B+

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

2010 2011 2012 2013 2014 2015 2016

B2B

B2C

Energy

FinancialServices

Healthcare

IT

Materials &Resources

$0

$100

$200

$300

$400

$500

$600

$700

$800

2010 2011 2012 2013 2014 2015 2016

B2B

B2C

Energy

FinancialServices

Healthcare

IT

Materials &Resources

Source: PitchBook

Source: PitchBook.

Unknown deal values are estimated based on known figures.

Source: PitchBook. Unknown deal values are estimated based on known figures.

Source: PitchBook. Unknown deal values are estimated based on known figures.

Outliers drive disparitiesDeals by size & sector

IN PARTNERSHIP WITH

9 PITCHBOOK 2016 ANNUAL US PE BREAKDOWN

CO-SPONSORED BY

FOCUSED. RELIABLE . RESPONSIVE . WWW.MURRAYDEVINE .COM/BEGREATER

BE GREATER

Gain a competitive advantage with an experienced valuation provider.

Providing valuation services to the country’s most respected private equity firms, hedge funds, banks and corporations for over 25 years.

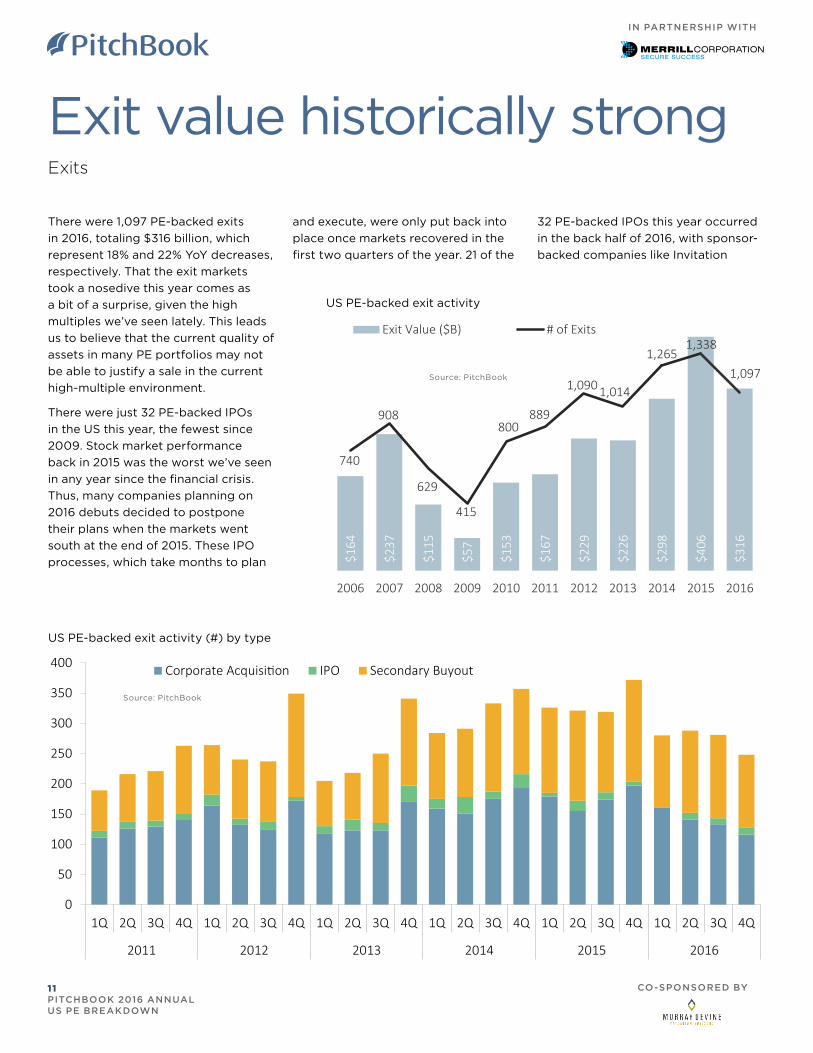

Exit value historically strongExits

There were 1,097 PE-backed exits

in 2016, totaling $316 billion, which

represent 18% and 22% YoY decreases,

respectively. That the exit markets

took a nosedive this year comes as

a bit of a surprise, given the high

multiples we’ve seen lately. This leads

us to believe that the current quality of

assets in many PE portfolios may not

be able to justify a sale in the current

high-multiple environment.

There were just 32 PE-backed IPOs

in the US this year, the fewest since

2009. Stock market performance

back in 2015 was the worst we’ve seen

in any year since the financial crisis.

Thus, many companies planning on

2016 debuts decided to postpone

their plans when the markets went

south at the end of 2015. These IPO

processes, which take months to plan

US PE-backed exit activity (#) by type

Source: PitchBook

US PE-backed exit activity

and execute, were only put back into

place once markets recovered in the

first two quarters of the year. 21 of the

32 PE-backed IPOs this year occurred

in the back half of 2016, with sponsor-

backed companies like Invitation

Source: PitchBook

0

50

100

150

200

250

300

350

400

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q

2011 2012 2013 2014 2015 2016

Corporate Acquisition IPO Secondary Buyout

IN PARTNERSHIP WITH

11 PITCHBOOK 2016 ANNUAL US PE BREAKDOWN

CO-SPONSORED BY

$164

$237

$115

$57

$153

$167

$229

$226

$298

$406

$316

740

908

629

415

800889

1,090 1,014

1,2651,338

1,097

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Exit Value ($B) # of Exits

Source: PitchBook

$0

$50

$100

$150

$200

$250

$300

$350

$400

$450

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Corporate Acquisition

IPO

Secondary Buyout

Source: PitchBook

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2010 2011 2012 2013 2014 2015 2016

B2B

B2C

Energy

FinancialServices

Healthcare

IT

Materials &Resources

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2010 2011 2012 2013 2014 2015 2016

B2B

B2C

Energy

FinancialServices

Healthcare

IT

Materials &Resources

Source: PitchBook

Source: PitchBook

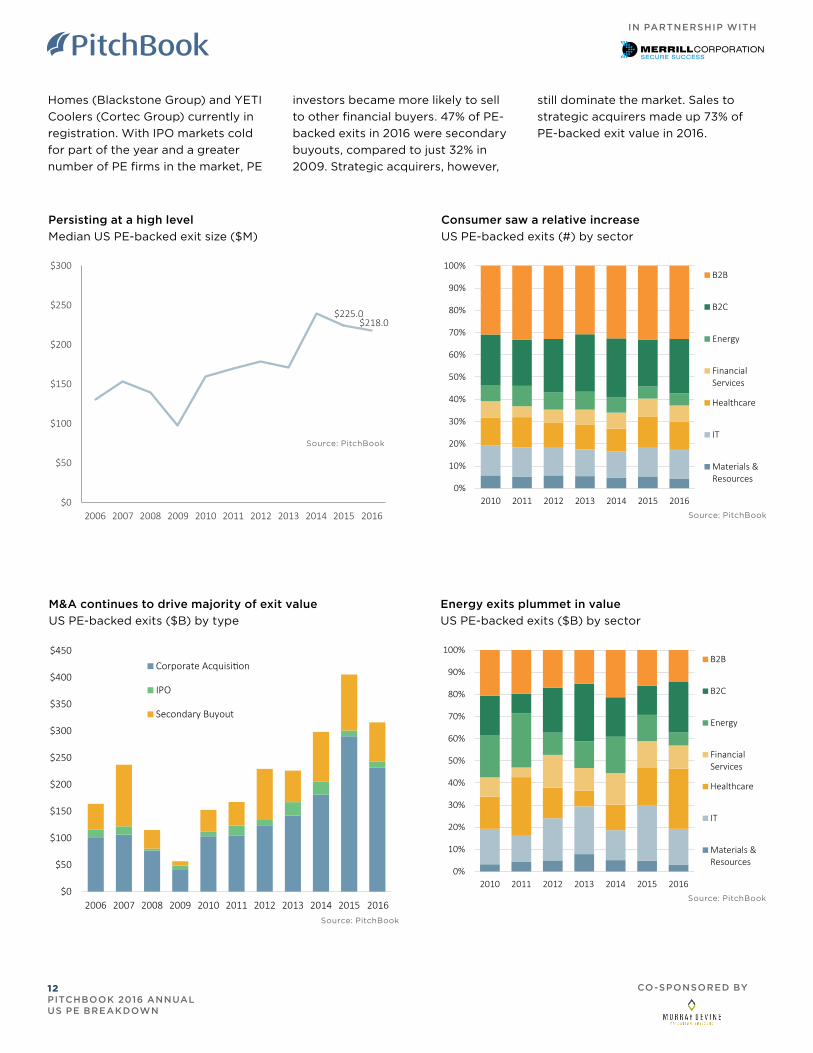

Homes (Blackstone Group) and YETI

Coolers (Cortec Group) currently in

registration. With IPO markets cold

for part of the year and a greater

number of PE firms in the market, PE

investors became more likely to sell

to other financial buyers. 47% of PE-

backed exits in 2016 were secondary

buyouts, compared to just 32% in

2009. Strategic acquirers, however,

still dominate the market. Sales to

strategic acquirers made up 73% of

PE-backed exit value in 2016.

IN PARTNERSHIP WITH

12 PITCHBOOK 2016 ANNUAL US PE BREAKDOWN

CO-SPONSORED BY

Energy exits plummet in value

US PE-backed exits ($B) by sector

Consumer saw a relative increase

US PE-backed exits (#) by sector

M&A continues to drive majority of exit value

US PE-backed exits ($B) by type

Persisting at a high level

Median US PE-backed exit size ($M)

$225.0$218.0

$0

$50

$100

$150

$200

$250

$300

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

LP interest remains healthyFundraising

PE commitments ebb

252 PE vehicles closed on $180.2

billion worth of commitments in

2016, representing 11% and 10%

YoY decreases, respectively. The

decrease, which more or less mirrors

the downturn in deal flow this year, is

indicative that limited partner interest

in the asset class is still strong, but has

receded since the highs of 2013-2015.

Larger funds outraise

One major theme we noticed in 2016

is the relative success that larger

funds experienced. Median buyout

fund size increased to $250 million

this year—up from $202 million in

2015—and the highest figure we’ve

recorded since 2010. Further, smaller

vehicles have become a smaller

part of the marketplace. Funds with

commitments under $100 million fell

to just 32% of final closes this year—the

smallest percentage since 2009. The

Capital raised stays strong

US PE fundraising

Source: PitchBook

$184

$272

$181

$121

$71

$88

$110

$201

$195

$200

$180

269

311

262

161158

189202

294318

283

252

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Capital Raised ($B)

# of Funds Closed

Fund sizes tick back upward

Average & median US PE fund size ($M)

$797.4 $816.8

$202.0 $250.0

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Average Buyout Fund Size ($M)

Median Buyout Fund Size ($M)

Source: PitchBook

causes here are twofold: First, some

LPs are simply choosing to work with

fewer GPs in an effort to decrease

administrative costs and increase

negotiating leverage when it comes

to fees. Second, the more established

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2010 2011 2012 2013 2014 2015 2016

$5B+

$1B-$5B

$500M-$1B

$250M-$500M

$100M-$250M

Under $100M

Capital concentrates in larger funds

US PE funds ($B) by size

Source: PitchBook

IN PARTNERSHIP WITH

13 PITCHBOOK 2016 ANNUAL US PE BREAKDOWN

CO-SPONSORED BY

US PE funds (#) to hit target

Time between funds soars to decade high

US PE fund time metrics (months)

5.86.6

5.97.3

14.6

14.414.3

16.2

0

3

6

9

12

15

18

21

24

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Average Time Btwn Buyout Funds

Average Time Btwn All PE Funds

Average Time to Close Buyout Funds

Average Time to Close All PE Funds

Source: PitchBook

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Hit Target

Missed Target

Source: PitchBook

managers raising the largest funds

are perceived by many to have more

expertise and capital flexibility in case

of a macroeconomic downturn, so LPs

are more comfortable contributing to

those funds. In addition, larger funds

may benefit from the luxury of having

first pick over the plethora of deals

coming across their desks.

With these larger funds, we would

expect it to take slightly longer, on

average, to reach a final close. While

that did happen across all of PE, the

average time to close for all buyout

funds actually decreased to 14.4

months. Meanwhile, the average time

between funds jumped to 7.3 years—a

decade high. As new managers

continue to compete for LP dollars,

we suspect that IR teams have created

more robust and targeted processes

to cultivate existing and new LP

relationships ahead of fund launches, a

factor that could be contributing to the

increased time period between funds.

Points of strength

In a sign of health for the industry,

89% of funds hit their stated target

this year, exceeding any other year

in at least the last decade. Even

more impressive is that just 70% of

First-time US PE funds as % of all US PE fundraising

6.0%

10.3%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

First-time US PE funds' % of all US PE funds

Source: PitchBook

managers hit their targets at the

peak of the last fundraising bonanza

in 2007. That so many managers are

meeting their goals speaks to the

continual demand that LPs have for

the asset class.

Another positive indicator is that

10.3% of funds to close this year

were by first-time managers. That’s

up from a bottom of 4% in 2013,

but still well below the 30% we saw

in 2003 (though the industry was

much less developed then). The deal

boom of the last couple years has

given plenty of PE professionals the

requisite experience to run their own

shops, while the simultaneous boom

in PE fundraising has given them the

confidence to go it alone.

IN PARTNERSHIP WITH

14 PITCHBOOK 2016 ANNUAL US PE BREAKDOWN

CO-SPONSORED BY

League tables4Q 2016

HarbourVest Partners 19

Audax Group 18

ABRY Partners 12

AlpInvest Partners 11

Genstar Capital 10

Hellman & Friedman 10

GTCR 8

Maranon Capital 8

NewSpring Capital 8

Kohlberg Kravis Roberts 7

Advent International 6

AEA Investors 6

GoldPoint Partners 6

H.I.G. Capital 6

Kelso & Company 6

Providence Equity Partners 6

The Carlyle Group 6

The Riverside Company 6

Vista Equity Partners 6

Aquiline Capital Partners 5

Charlesbank Capital Partners 5

First Reserve 5

Great Point Partners 5

Leeds Equity Partners 5

LLR Partners 5

Oaktree Capital Management 5

Onex 5

The Sterling Group 5

Warburg Pincus 5

Most active investors by deal count Select PE deals among top 10 in 4Q 2016

Source: PitchBook

Company Investor(s)Deal Size ($B)

Sector

Talen Energy Riverstone Holdings $5.2Energy Production

Rackspace USApollo Global Management, Searchlight Capital Partners

$4.3Systems & Information Mgmt

Lexmark InternationalLegend Capital, Pacific Alliance Group, Apex Microelectronics

$4.0 Computer Parts

Vertiv Platinum Equity $4.0Electrical Equipment

inVentiv Health Advent International $1.9Healthcare Services

Fund ManagerCapital Raised ($B)

Fund Type

Highbridge Principal Strategies HPS Investment Partners $6.6 Mezzanine

Dover Street IX HarbourVest Partners $4.8 Secondaries

Carlyle Global Partners The Carlyle Group $3.6 Buyout

Vista Foundation Fund III Vista Equity Partners $2.8 Buyout

L Catterton VIII L Catterton $2.8 Buyout

Source: PitchBook

Select PE funds among top 10 in 4Q 2016

Source: PitchBook

Company Seller BuyerDeal Size ($B)

Dematic GroupAEA Investors, Ontario Teachers’ Pension Plan

KION Group $3.3

Acrisure Genstar CapitalABRY Partners, management

$2.9

DeltekThoma Bravo, Quilvest Private Equity, Prospect Capital

Roper Technologies

$2.8

CAMP Systems International GTCR Hearst $2.0

Sensus USAThe Jordan Company, Goldman Sachs Merchant Banking Division

Xylem $1.7

Select PE exits among top 15 in 4Q 2016

Source: PitchBook

IN PARTNERSHIP WITH

15 PITCHBOOK 2016 ANNUAL US PE BREAKDOWN

CO-SPONSORED BY

See how the PitchBook Platform can

help your private equity firm close your

next deal.

We do EBITDA multiples,private comps,valuations,market trends,growth metrics.

You build a better portfolio.