U.S.-Canadian Tax and Estate Planning for Cross...

124

The audio portion of the conference may be accessed via the telephone or by using your computer's speakers. Please refer to the instructions emailed to registrants for additional information. If you have any questions, please contact Customer Service at 1-800-926-7926 ext. 10. NOTE: If you are seeking CPE credit , you must listen via your computer — phone listening is no longer permitted. U.S.-Canadian Tax and Estate Planning for Cross-Border Clients Reconciling U.S. and Canadian Law on Trusts, Deemed Dispositions on Death, Situs Wills, and Wealth Transfers Today’s faculty features: 1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific TUESDAY, MAY 16, 2017 Grant Gilmour, International Tax Partner, Gilmour Group CPAs, Vancouver, B.C. C. Edward Kennedy, Jr., CPA, JD, Brady Ware & Company, Atlanta Susan J. Merritt, Senior Fiduciary Officer, Northern Trust, Newport Beach, Calif. Presenting a 90-Minute Encore Presentation of the Webinar with Live, Interactive Q&A

Transcript of U.S.-Canadian Tax and Estate Planning for Cross...

The audio portion of the conference may be accessed via the telephone or by using your computer's

speakers. Please refer to the instructions emailed to registrants for additional information. If you

have any questions, please contact Customer Service at 1-800-926-7926 ext. 10.

NOTE: If you are seeking CPE credit, you must listen via your computer — phone listening is no

longer permitted.

U.S.-Canadian Tax and Estate

Planning for Cross-Border Clients Reconciling U.S. and Canadian Law on Trusts,

Deemed Dispositions on Death, Situs Wills, and Wealth Transfers

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

TUESDAY, MAY 16, 2017

Grant Gilmour, International Tax Partner, Gilmour Group CPAs, Vancouver, B.C.

C. Edward Kennedy, Jr., CPA, JD, Brady Ware & Company, Atlanta

Susan J. Merritt, Senior Fiduciary Officer, Northern Trust, Newport Beach, Calif.

Presenting a 90-Minute Encore Presentation of the Webinar with Live, Interactive Q&A

Tips for Optimal Quality

Sound Quality

If you are listening via your computer speakers, please note that the quality

of your sound will vary depending on the speed and quality of your internet connection.

If the sound quality is not satisfactory, you may listen via the phone: dial

1-866-961-9091 and enter your PIN when prompted. Otherwise, please

send us a chat or e-mail [email protected] immediately so we can address the

problem.

If you dialed in and have any difficulties during the call, press *0 for assistance.

NOTE: If you are seeking CPE credit, you must listen via your computer — phone

listening is no longer permitted.

Viewing Quality

To maximize your screen, press the F11 key on your keyboard. To exit full screen,

press the F11 key again.

FOR LIVE EVENT ONLY

Continuing Education Credits

In order for us to process your continuing education credit, you must confirm your

participation in this webinar by completing and submitting the Attendance

Affirmation/Evaluation after the webinar.

A link to the Attendance Affirmation/Evaluation will be in the thank you email that you

will receive immediately following the program.

For CPE credits, attendees must participate until the end of the Q&A session and

respond to five prompts during the program plus a single verification code. In addition,

you must confirm your participation by completing and submitting an Attendance

Affirmation/Evaluation after the webinar and include the final verification code on the

Affirmation of Attendance portion of the form.

For additional information about continuing education, call us at 1-800-926-7926 ext.

35.

FOR LIVE EVENT ONLY

Planning Considerations for

Cross Border Assets and Clients Grant Gilmour, International Tax Partner

Gilmour and Co.

(604) 888-4200

C. Edward Kennedy, Jr, CPA, JD

Senior Manager, Brady Ware & Co.

(770) 458-5000

Susan J. Merritt, Senior Vice President,

The Northern Trust Company, Orange

County Region [email protected]

(949) 717-5531

4

AGENDA • I – U.S. Estate Tax Regime (Susan)

• II – The Canadian Deemed Disposition Rules (Grant)

• III -U.S. and Canadian Tax Treatment of Trusts (Grant and Susan)

• IV – Tax Treaty Credit Provisions (Ed)

• V - Planning Considerations(Ed)

• VI - Filing and Reporting Deadlines and Timelines to Consider (Grant, Ed, Susan)

• VII – Questions (All)

5

But first, let’s update Ben

Franklin’s famous proverb

6

• Must be a 2 Pronged Approach

• Application of the U.S. Code • Application of Tax Laws in Home Country

I - Planning for U.S. Estate Tax in a Global Community

7

Why is Canada Relevant?

8

• Consider Canadian Statistics

• World’s largest and most comprehensive trading relationship

• 2015 – exchanged US $1.3 million of goods and services every minute

• Longest international border in world – 5,525 miles long; 300,000 people cross it daily

• Ways We See This Cross Border Activity

• Canadians to U.S. – Business owners and C Suite Executives

– Snowbirds – 500,000 in Florida!

– Students

• Americans to Canada – Oil and Gas Industry

– Entertainment industry

– High Tech companies

– Skiers with Whistler vacation homes

– Students

• Cross border families lead to cross border assets, cross border estate plans and cross border issues

General Overview – Canada VS U.S.

United States Canada

Citizenship Central to the U.S. Taxation System Irrelevant; tax system based on

residency

Estate Tax YES - Estates beyond exclusion amount

subject to tax at 40%

No estate tax but deemed

disposition of all property at death;

resultant capital gains tax

Gift Tax YES – gifts beyond annual exclusion or

lifetime exclusion amount subject to tax

No gift tax but most transfers of

property subject to deemed

disposition rule and resultant capital

gains tax; some protected transfers

Generation Skipping

Transfer Tax

YES – distributions to skip persons beyond

exclusion amount subject to tax

No GSTT but trusts have a 21 year

deemed disposition rule regarding

property and therefore, resultant

capital gains tax

Capital Gains Tax All capital gains included in income; $250,000

exclusion regarding “primary residence”

($500,000 per couple)

½ of capital gains included in income;

all gains from “principal residence”

excluded; CDN$800,000 capital gain

from sale of shares of certain small

businesses excluded

9

U.S. Estate Taxes and NRAs: What Is Included?

• Citizens, Residents and Domiciliary: • U.S. citizens (wherever they live) and U.S. “residents”

(regardless of their citizenship) are subject to U.S. gift, estate and generation-skipping transfer taxes on their worldwide assets.

• Non-citizen non-residents: • Subject to U.S. gift, estate and generation skipping transfer

taxes on their U.S. situs assets • Includes

• U.S. real property • U.S. tangible personal property (ex jewelry) • U.S. intangible property (ex domestic stock)

10

U.S. Estate Taxes and NRAs: What Is Excluded?

11

• Citizens/Residents - Nothing!

• NRA’s - some exclusions even though asset may be physically in the U.S.: • U.S. bank accounts, as defined • Works of art on loan in the U.S. • Life insurance • Qualified debt obligations • By treaty, some shares of domestic companies

The U.S. Estate Taxes and NRAs: What Are the Exemption Amounts?

12

• U.S. CITIZENS

• $5 million base amount, indexed for inflation • 2017 = $5.49 million (unified credit of $2,141,800)

• U.S. RESIDENTS • Same but caution re non U.S. spouses

• U.S. CITIZEN MARRIED TO FOREIGN PERSON • QDOTS likely needed

• NRA’s • $60,000 base amount, NO indexing for inflation (unified

credit $13,000) • Treaties may increase the credit

• CAUTION – does Treaty address income tax? Estate tax? Gift Tax?

.

How Does the Canada – U.S. Tax Treaty Address U.S. Estate Taxes?

• Highlights • prorated unified credit to provide some relief against limitations of $60,000

exemption

• Generally, U.S. situs assets are exempt from U.S. estate tax if worldwide assets are less than unified estate tax credit

• Canadian tax credit for U.S. estate taxes paid

• Does NOT apply to U.S. STATE estate taxes

13

NRA’s and the Basic Gift Tax Rules

14

• Annual Gifts

• Same as citizens/residents

• NRA may make gifts of up to $14,000 of U.S. situs assets in 2017.

• Married foreign donors can’t take advantage of gift splitting election available to U.S. persons – gifts from U.S. spouse to non U.S. spouse qualify for $100,000 base annual exclusion ($149,000 in 2017

• Lifetime Exclusion

• None

• No unlimited marital deduction

• Use of QDOT critical

• Tangible versus Intangible Property

• Gift tax only applies to tangible, U.S. Situs asset

• Cash considered a tangible unless from foreign account

• Gifts of intangibles (stock, bonds p’ship interests etc) are not subject to gift tax

• Planning opportunities with real property (i.e. hold in entity versus directly to avoid tax)

• Gifts to Spouses

• NRAs don’t benefit from unlimited gift tax marital deduction

• Annual spousal exclusion of $134,000 adjusted for inflation

Summary Application of the U.S. Code for U.S. Person

vs Foreign Person

15

Exemption Amounts Granted to U.S. Persons Exemption Amounts Granted to Foreign Persons (unless

otherwise increased by Treaty)

Base Amount

under Code

Indexed

for

Inflation?

2017 Amounts Granted to U.S.

Persons

Base Amount

Under Code

Indexed for

Inflation?

2017 Amounts Granted

to Foreign Individuals

Estate Tax $5 million Y $5.49 million ($2,141,800

credit)

$60,000 ($13,000

credit)

N $60,000

Gift Tax – Annual

Exclusion

$14,000 N $14,000; all tangible and

intangible property included

$14,000 N $14,000; only tangible

property as defined

included

Gift Tax – Lifetime

Exemption

$5 million Y $5.43 million None N/A N/A

Gift Tax – Spousal

Gifts

Unlimited N/A Unlimited $100,000 Y $149,000 annual

exclusion

Generation

Skipping Transfer

Tax

$5 million Y $5.49 million $5 million Y $5.49 million

Expatriation

Exemption

$600,000 Y $699,000 N/A N/A N/A

II – Canadian Deemed Disposition Rules

16

Illustrate with two gentlemen

Tim Horton and Uncle Sam

II – Canadian Deemed Disposition Rules

17

II – Canadian Deemed Disposition Rules

18

Tim Horton is a successful entrepreneur with enough wealth to worry about tax planning His last words are “sell everything” This creates a tax liability to the deceased that is usually paid by the estate. The tax is calculated on the “final return” of the deceased. Not on a special estate return as commonly thought. The result of the tax being on the final return is that the tax interacts with: • previous returns of the deceased (for example loss carryforward and back rules)

and • with spouses (for example spousal tax deferred transfers on death) and • with other jurisdictions (for example foreign tax credits) and • lastly to some extent with the first-year return of the testamentary estate created

by death (called a Graduated Rate Estate “GRE” in Canada). In Canada we don’t have a transfer tax but there is tax when you make you a transfer.

II – Canadian Deemed Disposition Rules

19

The deemed disposition rule primarily applies to capital assets. Those are assets with gains and losses in them. There are different sub-categories. • Listed personal property • Real property • Depreciable property • Publicly traded shares and securities • Qualified small business shares and/or Qualified fishing or farming property. As well a concept similar to a deemed disposition rule applies to pension funds held at death. These are deemed paid to the deceased immediately prior to their death. Other income is treated “normally” but is prorated on a reasonable basis to consider the date of death. And if this other income might not have been received until later if there was no death, there are provisions to carve that income that would have been delayed and put it on a separate tax return. “Rights and things” return

II – Canadian Deemed Disposition Rules

20

The consequences is that there is a fair bit of tax that can result when a Canadian resident dies. As well for non-residents the same rules generally apply but only to Canadian situs assets such as pensions, stock portfolios and real property.

II – Canadian Deemed Disposition Rules

21

There is automatically created a new taxpayer called a Graduated Rate Estate immediately after a death. The GRE holds all of the same assets that the deceased beneficially and titled held that are not otherwise distributed. What this means is that a person can plan for death and have assets transferred outside of a will to other people. Only those assets that do not have direction outside of a will, will become part of the GRE.

II – Canadian Deemed Disposition Rules

22

This leads us to a discussion of the corner stone of estate planning in Canada. Planning for assets not to be affected by the deemed disposition rules. The key strategy is to have them outside of the asset list that would become part of the GRE. We will discuss this more later in the presentation. Various forms of trusts are used to change the ownership of an asset before death and thus avoid the deemed disposition.

II – Canadian Deemed Disposition Rules

23

Uncle Sam • His last words are also “sell everything”. Many of the

same rules apply to him as apply to Tim. But importantly they only apply to assets with situs in Canada.

• Withholding taxes can kick in here and there is some treaty relief on these. These can be mitigated by the Tax Treaty.

• GRE’s do not apply here. • Security for taxes can be an issue as often the phrase

“land rich and cash poor” applies.

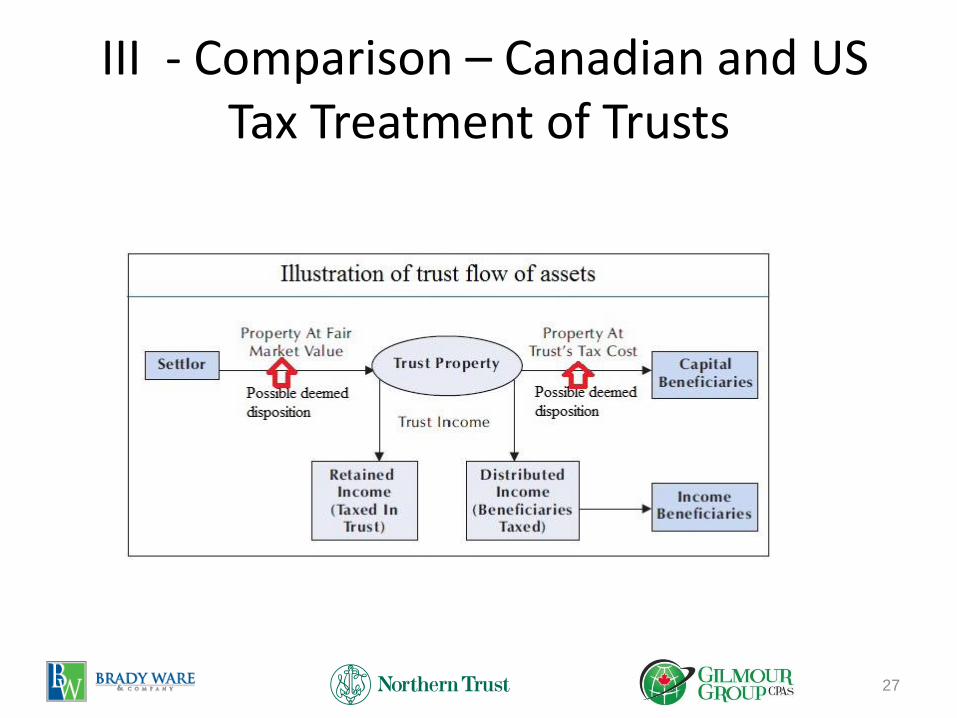

III - Comparison – Canadian and US Tax Treatment of Trusts

24

Canadian tax treatment of Trusts

Trusts are a favored method of estate and tax planning in general in Canada.

III - Comparison – Canadian and US Tax Treatment of Trusts

25

Trusts are a favored method of estate and tax planning in general. Key elements that make them appealing • Ability to control the timing of a deemed disposition. You can’t make the

deemed disposition rule go away but you can control the timing and in controlling the timing control the tax.

• Ability to take assets out of the estate and thus avoid “death” and its tax

consequences. • Ability to treat income and capital beneficiaries differently and thus

spread the wealth and the tax in a manner that fits family estate planning • Ability to grant discretion to trustee

III - Comparison – Canadian and US Tax Treatment of Trusts

26

• Big changes in trust planning in Canada.

• Previously a testamentary trust could be established and proceed for a long time at preferred (lower) tax rates.

• Now new rules push most trusts into new rules called Graduated Rate Estates.

• These are time limited (three years). This limits the estate planning available with a testamentary trust.

III - Comparison – Canadian and US Tax Treatment of Trusts

27

III - Comparison – Canadian and US Tax Treatment of Trusts

28

Canada USA Comments

Inter vivos trust - Similar to Grantor Trusts but

in Canada, there is a deemed

disposition of the assets

being transferred to the trust

Generic term for a trust

created while alive. Subject

to the highest tax rates.

Trusts are usually flow

through instruments. So, the

tax rate is irrelevant if the

income is distributed.

Family Trust – This is a type

of Inter vivos trust

Similar to Grantor Trusts.

Rather than attribution rules,

the USA imposes the gift tax

rules. Could be set up as a

GSTT Exemption Trust,

Irrevocable Gift Trust,

Dynasty Trust

Created before death.

Deemed disposition or actual

disposition occurs upon

contribution of assets.

Subject to attribution rules.

These are rules to prevent or

undo income splitting.

Alter Ego Trust - This is a

type of Inter vivos trust

Similar to a Grantor Trusts

but in Canada, this trust can

only be used if over the age

of [69]? No deemed

disposition on transfer in

Created while alive – used to

avoid challenges to a will and

to avoid probate fees.

III - Comparison – Canadian and US Tax Treatment of Trusts

29

Canada USA Comments

Spousal trusts inter vivos Similar concept in US but no

deemed disposition of assets

when transferred. Must be

mindful of whether spouse is US

citizen due to gifting limitations

Same as one created upon death

but tax is slightly different as the

deemed disposition is applied at

a different point in time.

Joint Spousal trusts Similar in concept to US Marital

Trust created on death. All

income must flow to surviving

spouse. Note that with alter ego

trusts, can only be used if over

the age of [69] and no deemed

disposition on transfer in. in

concept in US

Similar to spousal but includes

both spouses.

III - Comparison – Canadian and US Tax Treatment of Trusts

30

Canada USA Comments

Testamentary trusts Similar in the US – trusts created

on death whether by will or trust.

Taxed at higher rates.

Generic term for trusts created as

an instrument of a will or

otherwise created upon death.

These are by default taxed at the

highest tax rate unless they can

squeeze in to the GRE definition.

Trusts are usually flow through

instruments. So, the tax rate is

irrelevant if the income is

distributed.

Spousal trusts testamentary

Similar in concept to US Marital

Trust or US Bypass Trust

Created upon death to ensure

that capital beneficiaries

designated by the deceased can

receive assets after a spouse dies.

Often found in a second marriage

situation or when the deceased

worries about a potential second

marriage of their spouse after

their death.

III - Comparison – Canadian and US Tax Treatment of Trusts

31

Canada USA Comments Graduated Rate Estates Defined term for a trust

created upon death and used

by an executor to distribute

assets as per the will. Can also

capture other types of trusts.

These are so new that there is

still speculation on what

exactly is included or

excluded. Key point is these

trusts have access to lower tax

rates

Some special trusts for

disability. Previously known

as Henson trusts.

Outside the scope of this

discussion

Non-resident trusts These from a Canadian point

of view are trusts outside

Canada with Canadian

Beneficiaries

III - Comparison – Canadian and US Tax Treatment of Trusts

32

Canada USA Comments Trusts with non-resident

beneficiaries

These from a Canadian point

of view are trusts inside

Canada with Non-resident

beneficiaries. Can create tax

issues with have a mix of

resident and non-resident

beneficiaries

III - Comparison – Canadian and US Tax Treatment of Trusts

33

• Overall, we also need to be aware of requirement

to withhold on distributions across a border

• A Trust in Canada is used as a flow through tool. It can allocate income to beneficiaries and as much income it designates it will not have to report and pay tax on itself.

III - Comparison – Canadian and US Tax Treatment of Trusts

34

• Challenges and opportunities with trust

• Major Challenge. – US beneficiaries are treated differently than Canadian beneficiaries.

• Best response – don’t blend beneficiaries in the same trust. Set up side by side trusts

III - Comparison – Canadian and US Tax Treatment of Trusts

35

• Major challenge – dying triggers probate fees in Canada

• Best response – transferring assets prior to death to a trust avoids probate fees

III - Comparison – Canadian and US Tax Treatment of Trusts

36

• Major challenge – Dying triggers all assets to be “deemed disposed” at death.

• Best response a structured plan of liquidating assets prior to death or of crystalizing gains prior to death can step of the cost basis and make tax upon death small.

III - Comparison – Canadian and US Tax Treatment of Trusts

37

• Major challenge – Trusts have a “tax bomb”. That is tax possibly due because of a tax free/deferred roll over at the front end. Now tax is due at the back end.

• Best response – use the ability to pick and treat each asset differently. The best example is if there is an asset with a gain and one with a loss you do not need to transfer both at a tax-free rollover value. You have the option of picking market value. And the selection of market value might trigger tax that you can use to your advantage.

IV - Tax Credit Treaty Provisions

38

.

How Does the Canada – U.S. Tax Treaty Address U.S. Estate Taxes?

KEY CONCEPTS

• ARTICLE XXIXB(2) • prorated unified credit to provide some relief against limitations of $60,000

exemption*

• The pro rata share is calculated on the relative value of the U.S. estate over the value of the gross worldwide assets of the decedent

• Generally, U.S. situs assets are exempt from U.S. estate tax if worldwide assets are less than unified estate tax credit*

• ARTICLE XXIXB(3) • can claim increased unified credit beyond that authorized by code re: marital

deduction; QDOT may not be needed

• ARTICLE XXIB(6) • Canadian tax credit for U.S. estate taxes paid*

• Does NOT apply to U.S. STATE estate taxes

39

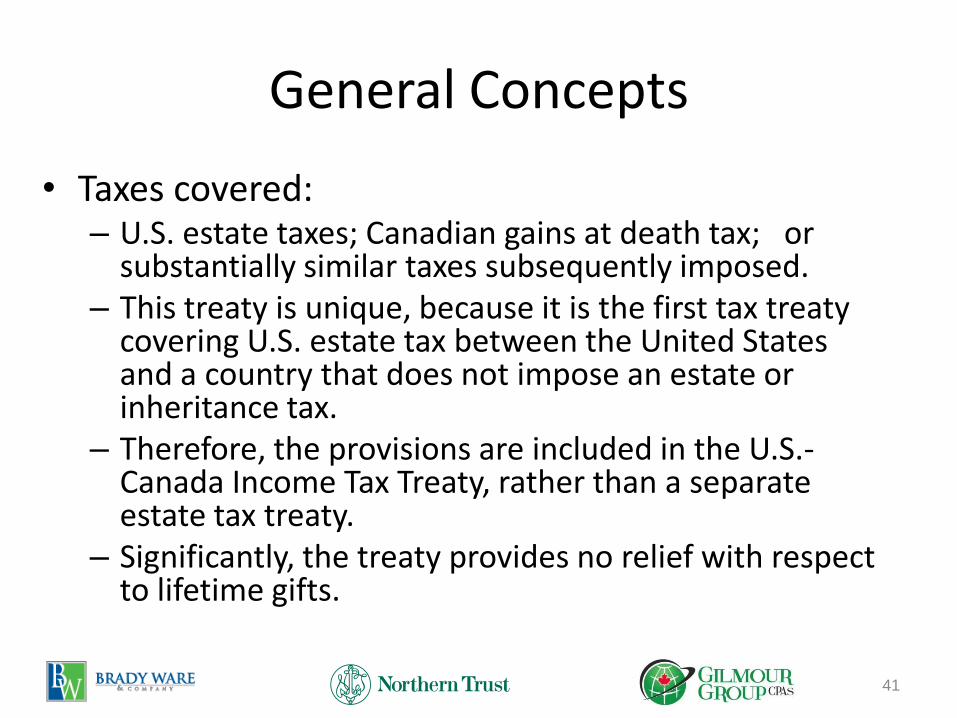

General Concepts

41

• Taxes covered: – U.S. estate taxes; Canadian gains at death tax; or

substantially similar taxes subsequently imposed. – This treaty is unique, because it is the first tax treaty

covering U.S. estate tax between the United States and a country that does not impose an estate or inheritance tax.

– Therefore, the provisions are included in the U.S.-Canada Income Tax Treaty, rather than a separate estate tax treaty.

– Significantly, the treaty provides no relief with respect to lifetime gifts.

Applicable Territories Covered - Article III(1)

42

• For the U.S. - United States, but not Puerto Rico, Virgin Islands, Guam, or any other possession or territory;

• For Canada - The territory of Canada;

• For both: Any area in which the country may exercise rights with respect to seabed and subsoil and their natural resources. (Effectively the IRC §638 definition for U.S.)

Individuals covered

43

• U.S. citizen or resident

• Canadian resident

Basis of taxation- domicile v. residence Article IV

44

• The U.S. / Canadian treaty is based on a federal income tax definition of “residence” rather than a federal transfer tax definition of “domicile.”

• Because U.S. transfer tax law is based on domicile v. residence, it is possible that a decedent may not be treated as a U.S. resident for purposes of the treaty but as a domiciliary for purposes of U.S. transfer tax law.

• In such a situation this may result in the application of U.S. transfer taxes and Canadian gains at death taxes, without the benefit of relief under the treaty.

Basis of taxation- domicile v. residence Article IV(1)

45

• An individual's “residence” is based on whether the individual is subject to tax liability, under the country's national income tax law, due to domicile, residence, or citizenship.

• In the case of a U.S. citizen or resident alien, that person is, nevertheless, a resident of the United States for purposes of the treaty only if the person has a substantial presence, permanent home, or habitual abode in the United States and that person's personal and economic relations are closer to the United States than any other country.

• Thus, U.S. citizens or residents are not necessarily resident under the Treaty unless they meet the residency definition above. For example, the person's personal or economic relations may be closer to another country.

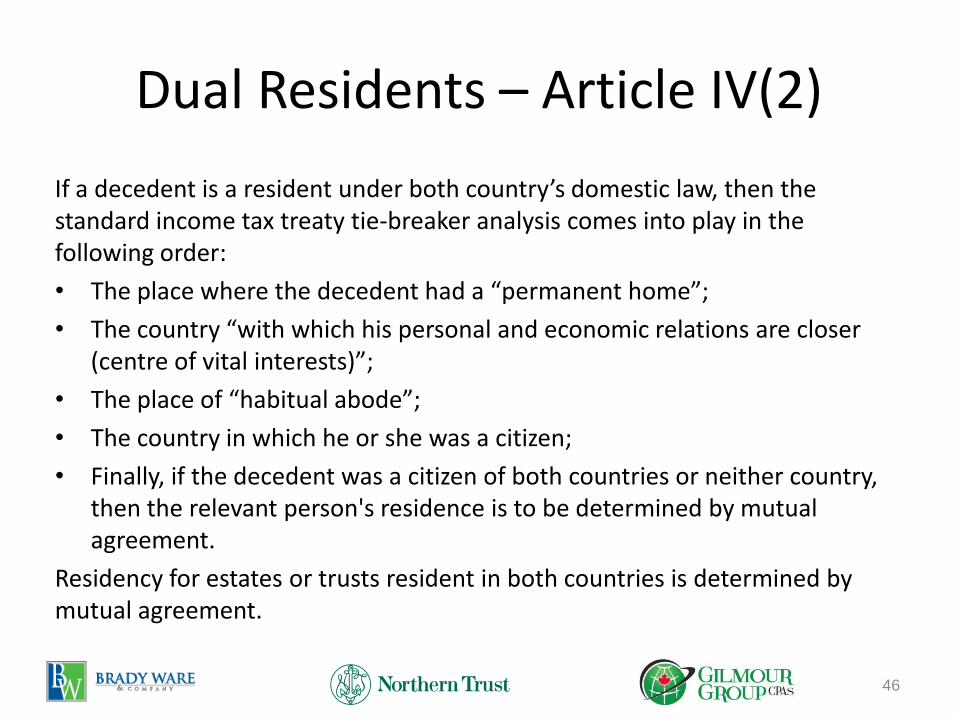

Dual Residents – Article IV(2)

46

If a decedent is a resident under both country’s domestic law, then the standard income tax treaty tie-breaker analysis comes into play in the following order:

• The place where the decedent had a “permanent home”;

• The country “with which his personal and economic relations are closer (centre of vital interests)”;

• The place of “habitual abode”;

• The country in which he or she was a citizen;

• Finally, if the decedent was a citizen of both countries or neither country, then the relevant person's residence is to be determined by mutual agreement.

Residency for estates or trusts resident in both countries is determined by mutual agreement.

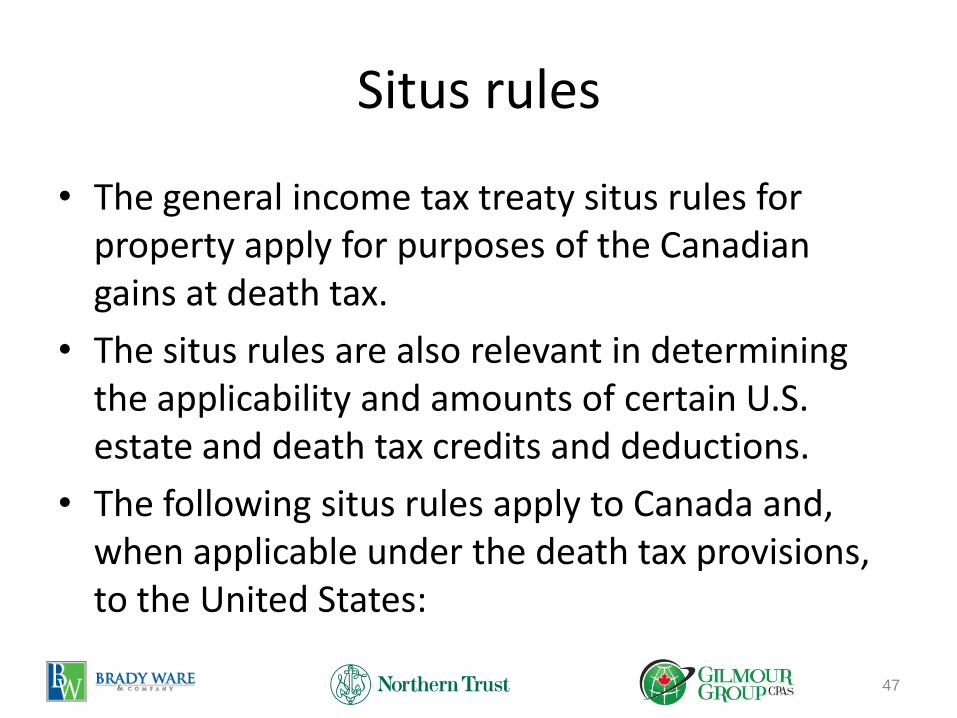

Situs rules

47

• The general income tax treaty situs rules for property apply for purposes of the Canadian gains at death tax.

• The situs rules are also relevant in determining the applicability and amounts of certain U.S. estate and death tax credits and deductions.

• The following situs rules apply to Canada and, when applicable under the death tax provisions, to the United States:

Situs continued

48

• Gains from the alienation of real property may be taxed where situated – Articles XIII(1); VI(1)

• Gains from the alienation of personal property that forms part of the business property of a permanent establishment or fixed base that a resident of one country has in the other country, may be taxed by that other country. Article XIII(2) – The permanent establishment or fixed base may no longer be in

existence, but the treaty still applies if it was in existence in the other country within the 12 months before alienation. Article XIII(2)

– Gains from the alienation of business property of a permanent establishment and assets pertaining to a fixed base used for the performance of professional services are taxable by the country where situated. They may still be taxed by the residence country. Article V

• Property not mentioned — all other gains from the alienation of property may not be taxed by the situs state simply because it is the situs state. Article XIII(4)

Charitable Deductions Article XXIX(1)

49

• U.S. domestic law limits charitable deductions to contributions made to U.S. charities.

• Pursuant to the 1995 Protocol, contributions to qualifying tax-exempt organizations in either of the treaty countries were treated as though made to tax-exempt organizations resident in the taxing country.

• This meant that the treaty permitted a Canadian resident who is not a citizen or domiciliary of the United States to claim a charitable contribution deduction for transfers at death of property includible in the U.S. taxable estate to a Canadian charitable organization.

• Transfers of property not included in the U.S. taxable estate are not allowed as U.S. deductions, In that case one looks to the pro rata share of all assets included in the worldwide estate and multiplies the charitable deduction by that percentage

Pro Rata Unified Credit Article XXIX(2)

50

• With respect to the estate tax, but not the gift tax, the United States will provide a pro rata unified credit to Canadian residents who are not U.S. citizens.

• The pro rata unified credit equals the greater of: – (a) the unified credit allowed to the estates of U.S. citizens

multiplied by the fraction of the total worldwide gross estate situated in the United States; and

– (b) the unified credit allowed to a nonresident not a citizen of the United States.

• This credit is reduced by any prior credits for gifts made by the decedent. Article XXIX B(2)

Pro Rata Unified Credit Example

51

• Canadian resident, Tim Horton, has a $2 million U.S. vacation home and has worldwide assets of $10 million

• STEP 1 - Calculate U.S. Estate tax otherwise payable:

= $2 million x 40% = $800,000

• STEP 2 - Calculate credit available under the Treaty:

= 2/10 x 2017 unified credit of $2,141,800 = $428,360

• STEP 3 - Reduce Estate tax payable by Treaty calculation:

= $800,000 - $428,360 = $348,360

• STEP 4 - Pay the U.S. Estate Tax!

• STEP 5 - Any state estate tax?

• STEP 6 - Any capital gains tax payable in Canada?

• STEP 7 - Any Treaty relief available

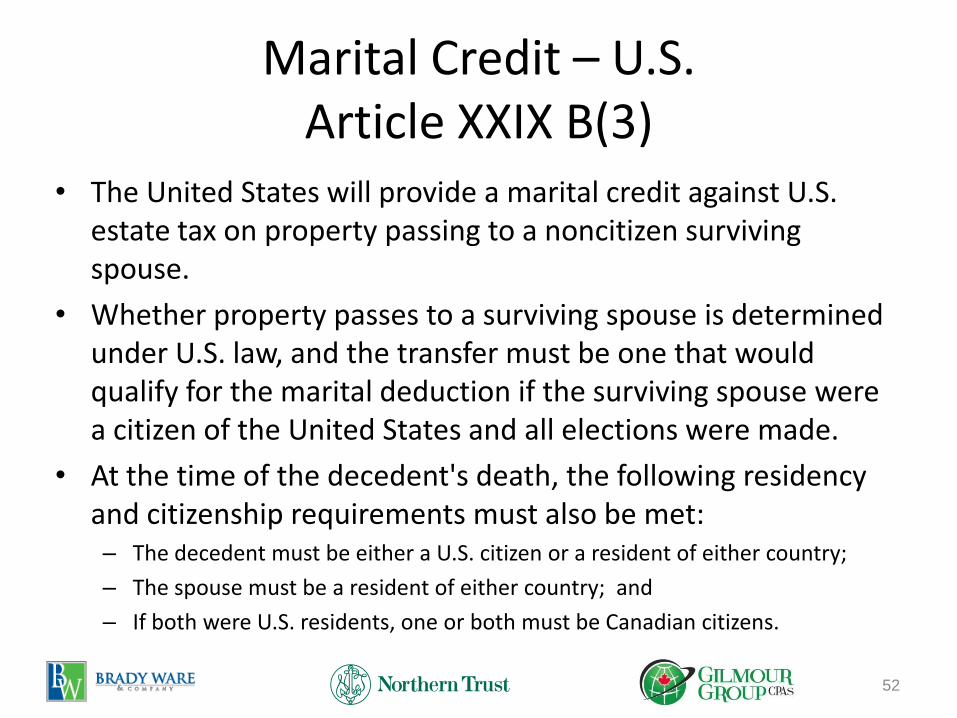

Marital Credit – U.S. Article XXIX B(3)

52

• The United States will provide a marital credit against U.S. estate tax on property passing to a noncitizen surviving spouse.

• Whether property passes to a surviving spouse is determined under U.S. law, and the transfer must be one that would qualify for the marital deduction if the surviving spouse were a citizen of the United States and all elections were made.

• At the time of the decedent's death, the following residency and citizenship requirements must also be met: – The decedent must be either a U.S. citizen or a resident of either country;

– The spouse must be a resident of either country; and

– If both were U.S. residents, one or both must be Canadian citizens.

Marital Credit – U.S. Article XXIX B(3)

53

• Other requirements: – The credit is only available if the executor of the decedent's estate

irrevocably waives the benefits of any U.S. estate tax marital deduction that may otherwise apply.

– The credit equals the lesser of (1) the amount of the unified credit allowed under the treaty or under U.S. domestic law, and (2) the amount of the U.S. estate tax that would “otherwise be imposed” on the transfer of qualifying property to the surviving spouse.

• The marital credit is in addition to the pro rata unified credit.

Operation of the Marital Credit

54

• H, the decedent, and W, his surviving spouse, are Canadian citizens resident in Canada at the time of the decedent's death

• They both meet all the marital credit requirements

• Assume unified credit is $2 million and estate tax rate is a flat 40% rate on estates over $5 million

Marital Credit Example

55

• H has a worldwide gross estate of $10 million.

• He bequeaths U.S. real property worth $5 million to W.

• The remainder of H's estate consists of Canadian situs property.

• U.S. estate tax otherwise payable is $2 million ($5 million X 40%)

• H's estate would be entitled to a pro rata unified credit of $1 million (($2 million x ($5 million/$10 million))

• H’s estate would also be entitled to a marital credit in the same amount (the lesser of the unified credit allowed ($1 million) or the U.S. estate tax that would otherwise be imposed on the property transferred to W ($2,000,000 [tax on U.S. taxable estate of $5 million])).

• The pro rata unified credit and the marital credit combined would in this example eliminate all U.S. estate tax with respect to the property transferred to W

Benefit of Marital Credit

56

• In certain cases, these provisions may affect the U.S. estate taxation of a trust that would meet the requirements for a qualified terminable interest property (“QTIP”) election, for example, a trust with a life income interest for the surviving spouse and a remainder interest for other family members.

• If, in lieu of making the QTIP election and the qualified domestic trust election, the decedent's executor irrevocably waives the benefits of any U.S. estate tax marital deduction that may otherwise apply, the provisions of Internal Revenue Code sections 2044 (regarding inclusion in the estate of the second spouse of certain property for which the marital deduction was previously allowed), 2056A (regarding qualified domestic trusts), and 2519 (regarding dispositions of certain life estates) will not apply.

• 7

Canadian Treatment of Certain Transfers Article XXIX(5)

57

• The provisions of paragraph 5 relate to the operation of Canadian law.

• They are intended to provide deferral (“rollover”) of the Canadian tax at death for certain transfers to a surviving spouse and to permit the Canadian competent authority to allow such deferral for certain transfers to a trust.

• For example, they would enable the competent authority to treat a trust that is a qualified domestic trust for U.S. estate tax purposes as a Canadian spousal trust as well for purposes of certain provisions of Canadian tax law and of the Convention.

• These provisions do not affect U.S. domestic law regarding qualified domestic trusts. Nor do they affect the status of U.S. resident individuals for any other purpose.

Marital Deduction – Canada Article XXIX B(6)(a)

58

• Canada will provide an exemption to the gains at death tax for transfers to a surviving spouse or “spousal trust” if, immediately before the decedent's death, the decedent was either a Canadian or U.S. resident, and the surviving spouse (or spousal trust) was a Canadian resident.

• Subparagraph 6(a)(i) allows a credit for U.S. tax against the total amount of Canadian income tax payable by the decedent in the taxable year of death on any income, profits, or gains arising in the United States

• Under Canadian law, a spousal trust is treated as a Canadian resident if the trustee is a Canadian resident or a Canadian corporation.

– However, upon request by a U.S. resident trust, the Canadian competent authority may agree to treat the trust as a Canadian resident for purposes of the marital exemption.

– Because a U.S. qualified domestic trust (QDOT) requires a U.S. resident trustee, this provision is intended to allow a QDOT to qualify as a spousal trust for purposes of the Canadian gains at death tax.

Marital Deduction – Canada Article XXIX B(6)(b)

59

• Subparagraph 6(b) provides rules for a second category of cases—where the U.S. tax is imposed upon the death of the surviving spouse. In these cases, Canada agrees to allow a credit against the Canadian tax payable by a trust for its taxable year during which the surviving spouse dies on any income, profits, or gains

– arising in the United States on U.S. situs real property or business property, or

– from property situated in the United States.

• These rules are intended to provide a credit for taxes imposed as a result of the death of the surviving spouse in situations involving trusts.

• To the extent that taxes are imposed on the estate of the surviving spouse, subparagraph 6(a) would apply as well.

• In addition, the competent authorities are authorized to provide relief from double taxation in certain additional circumstances involving trusts.

Marital Deduction - Example

60

• A U.S. decedent with a Canadian spouse sets up a qualified domestic trust holding U.S. and Canadian real property

• The decedent's executor elects, for Federal estate tax purposes, to treat the entire trust as qualifying for the Federal estate tax marital deduction.

• Under Canadian law, because the decedent is not a Canadian resident, Canada would impose capital gains tax on the deemed disposition of the Canadian real property immediately before death.

• In order to defer the Canadian tax that might otherwise be imposed by reason of the decedent's death, the competent authority of Canada shall, at the request of the trustee, treat the trust as a Canadian spousal trust with respect to the Canadian real property.

• The effect of such treatment is to defer the tax on the deemed distribution of the Canadian real property until an appropriate triggering event such as the death of the surviving spouse.

Additional Credit for Spousal Trusts

61

• There is also a credit for U.S. federal or state estate or inheritance taxes payable by a trust, which are imposed upon the death of the surviving spouse.

• These taxes can be deducted from the Canadian tax otherwise payable on income or other gains arising in the United States under Article XXIV(3), or from property situated in the United States, during the taxable year of the surviving spouse's death.

• The countries may provide relief from double taxation by mutual agreement, in cases where no relief is otherwise available, for distributions or disposition of property by a QDOT or spousal trust.

U.S. Credit Provisions Article XXIX B(7)

62

• The United States allows a credit against U.S. Federal estate tax imposed on the estate of a U.S. resident or U.S. citizen decedent, or upon the death of a surviving spouse with respect to a qualified domestic trust created by such a decedent (or the decedent's executor or surviving spouse).

• The credit is allowed for Canadian Federal and provincial income taxes imposed at death with respect to property of the estate or trust that is situated outside of the United States. The credit applies to the estates of U.S. resident and U.S. citizen decedents, or upon the death of a surviving spouse with respect to a QDOT created by such decedent.

• The credit is available regardless of the definition of residency under Canadian law, and it may be claimed only to the extent it is not also claimed as a credit or deduction against any other U.S. tax.

Relief for Small Estates Article XXIX B(8)

63

• There is a total U.S. estate tax exemption for small estates of non-U.S. citizens residing in Canada.

• To qualify, the value of the worldwide gross estate, at the time of death, must be no more than $1.2 million.

• The United States may still tax U.S.-situs property that forms part of the exempt estate, but only if gain derived from the alienation of the property would have been subject to income tax by the United States under Article XIII (Gains).

Savings Clause Exceptions

64

• General saving clause exceptions are provided for paragraphs 1 (charitable bequests), 5 (Canadian treatment of certain transfers), and 6 (credit for U.S. taxes) of Article XXIX B.

• Saving clause exceptions are provided for paragraphs 2 (pro rata unified credit), 3 (marital credit), 4 (computation of the marital credit), and 7 (credit for Canadian taxes), except for the estates of former U.S. citizens referred to in paragraph 2 of Article XXIX7

Provisions Contained in Paragraph 7 of the 1995 General Note – not the treaty

65

Special Rules for Equity

66

• Subparagraph 7(a) of the General Note applies where an individual who immediately before death was a resident of Canada held at the time of death a share or option in respect of a share that constitutes property situated in the United States and that Canada views as giving rise to employment income (for example, a share or option granted by an employer).

• The United States imposes estate tax on the share or option in respect of a share, while Canada imposes income tax on income from employment. Subparagraph 7(a) provides that any employment income in respect of the share or option constitutes income from property situated in the United States.

• This provision ensures that the estate tax paid on the share or option in the United States will be allowable as a deduction from the Canadian income tax.

RRSPs which invest in U.S. Assets

67

• Subparagraph 7(b) of the General Note applies where an individual who immediately before death was a resident of Canada held at the time of death a registered retirement savings plan (RRSP) or other entity that is a resident of Canada and that is described in subparagraph 1(b) of Article IV (Residence) and such RRSP or other entity held property situated in the United States.

• The United States would impose estate tax on the value of the property held by the RRSP or other entity (to the extent such property is subject to Federal estate tax), while Canada would impose income tax on a deemed distribution of the property in the RRSP or other entity.

• Subparagraph 7(b) provides that any income out of or under the entity in respect of the property is, for the purpose of subparagraph 6(a)(ii) of Article XXIX B, income from property situated in the United States.

• This provision ensures that the estate tax paid on the underlying property in the United States (if any) will be allowable as a deduction from the Canadian income tax.

U.S. Residents Owning RRSPs or Other Entities

68

• Subparagraph 7(c) of the General Note applies where an individual who immediately before death was a resident or citizen of the United States held at the time of death an RRSP or other entity that is a resident of Canada.

• The United States would impose estate tax on the value of the property held by the RRSP or other entity, while Canada would impose income tax on a deemed distribution of the property in the RRSP or other entity.

• Subparagraph 7(c) provides that for the purpose of paragraph 7 of Article XXIX B, the tax imposed in Canada is imposed in respect of property situated in Canada. This provision ensures that the Canadian income tax will be allowable as a credit against the U.S. estate tax.

V – Planning Considerations

69

Marital Planning Considerations

70

• Planning for marital transfers in connection with the treaty can prove extremely complex.

• A major opportunity relates to the use of a QTIP (Qualified Terminal Interest Property) trust in the case of a U.S. citizen spouse.

• If the QTIP form is used, and assuming all other requirements are met, the treaty's marital credit will be available.

• It will make sense, however, not to make a QTIP election under the Code. Thus, there will be a waiver of the right to claim the deduction under §2056(b)(7).

• Taking the marital credit under the treaty instead of the deduction under the Code can prove beneficial. Much will hinge on the relative value of the U.S. property. – For example, if the entire estate consists of U.S. property, and the taxable

estate is $7,500,000, the first $5,490,000, assuming no prior unified credit allowed for gifts, will be covered by the applicable exclusion amount for decedents dying in 2017. The marital credit, which can be no greater than the unified credit, will cover the rest.

Marital Planning Considerations

71

• If the property does not pass in full, then the unified credit is first used for the other transfers.

• Assume that the property all passes to the spouse, however, in the form of a QTIP trust, but that there is no election under the Code.

• While the decedent's entire $7,500,000 estate will be sheltered, what happens when the surviving spouse dies? – Under the Code, §2044 would have required inclusion of the remaining trust

property in the spouse's gross estate. – However, under the treaty there is no such provision. – Because the surviving spouse only had an income interest, nothing is

includible in his or her gross estate. – Admittedly, this is not the preferred course for larger estates, because the

marital credit will be limited in amount. Thus, any excess if the marital credit route were chosen will pour into the marital credit trust without any benefit or into the typical unified credit shelter trust, again without any benefit. A qualifying marital deduction trust will not be available

Traps for the Unwary

72

• The Section 94 Canadian Non Resident Trust Rules complex set of rules that can deem an otherwise non resident trust to be deemed to be resident in Canada for tax purposes

• 21 Year Deemed Disposition Rule with a US Beneficiary

• Income Tax Act allows for distribution of trust property at cost to Canadian resident beneficiaries; does not apply to non resident beneficiaries

• Certain U.S. States Tax RRSP Income

• can defer U.S. taxation on accrued RRSP income so long as income not distributed and election under Treaty made

• Some states (California) view RRSPs like savings accounts - Franchise Tax Board taxes accrued income on annual basis

V – Filing and Reporting Deadlines and Timelines to Consider

73

Reporting Requirements

74 08/12/2016

Reporting Requirements - Canada

75

Reporting Requirements - Canada

76

• Final return

– April 30 of the year following death – exception made for

• Returns with qualifying as business they have June 15th

• Deaths occurring between November 1 and December 31. Have 6 months from the date of death

– Worthwhile to note that this deadline is often missed as probate is not obtained in time. CRA will charge penalties and then refund them upon a request for fairness.

• Trust returns in general

– 90 days after year end. Most trusts have December year ends

• Graduated Rate Estates.

– Also, have 90 days but can use a non-calendar year end to coincide with anniversary of death.

Reporting Requirements - Canada

77

• Clearance certificates.

– Cannot be filed before a return is assessed.

– Should not be filed more than three years after a return is assessed as it might open a return that would naturally time out or go statute barred.

• Elective returns - not discussed in depth here. There are some elective returns that can apply in special circumstances where assets continue to produce income after death that relates to before death. These have the same deadlines as the final return. For example rights and things.

• Extensions. Generally, there is no such thing as an extension in Canada. However, we can effectively create one for a tax return by overpaying the estimated tax. That is because penalties are calculated of the basis of tax not paid at the filing deadline. By overpaying the estimated tax, we have no tax due thus no penalty. There are other penalties for failure to file information that cannot be avoided. We distinguish between a tax return and an information return. Information returns have penalties triggered by non-filing. Tax returns have penalties triggered by non-payment.

Reporting Requirements - Canada

78

- T1 personal tax return- due April 30 – unless extension automatically granted due to death late in year.

- It can have various attachments. They are all due at the same time. The attachments can sometimes be filed separately or with the spouse, especially the ones related to elections and to information.

- Election to split pension income is an example

- T1135 generally considered an attachment to a T1 return. It discloses foreign assets held by a Canadian resident tax payer

- T2 corporate tax return. Due six months after year end or deemed year end. Death of a controlled share holder resident in Canada generally does not trigger a year end. Death of a controlling non-resident shareholder can trigger a year end.

Reporting Requirements - Canada

79

- T3 Trust return. Due 90 days after year end. Trusts with calendar year ends often struggle to make filings on time due to timing of various other reporting components.

- T4 and T4A – due February 28 on calendar year basis. Not generally the responsibility of the deceased or estate but in a closely held family group these can become the responsibility of the executor and we can get a circular filling deadline issue as other returns need these to be prepared and issued.

- T5 – due February 28 on a calendar year basis. Also not generally the responsibility of the deceased or estate. Same issues though with interrelated returns.

Reporting Requirements - Canada

80

- NR4 slips due march 31 following a calendar year. Report distributions to non-residents. Many of the distributions from an estate or our other tax planning can trigger these and related withholding.

- T1135 reports foreign assets held by Canadian resident person or corporation or trust. – due when related T type return is due. I.E. T1 due in April this is due in April.

- T1134 discloses foreign controlled assets held by Canadian resident. (generally private corporations)

- T5013 Statement of partnership income can be included on other T type returns as an attachment and has its own deadline that depends on who is a partner. Usually March 31 following a calendar year.

- FAPI disclosure. Does not have its own schedule or return but is often not known until after a deadline has passed. Is often tough to segregate from other investment income on the returns.

Filing and Reporting Requirements – U.S.

82

Filing Deadlines

83

• Decedent's Final Income Tax Return – April 15 in year after death

• Gift Tax Return –

– Who must file: citizens, residents and nonresidents who made taxable gifts of >$14,000.

– When to file: return is due April 15th of following year – can be extended until October 15th

Filing Deadlines

84

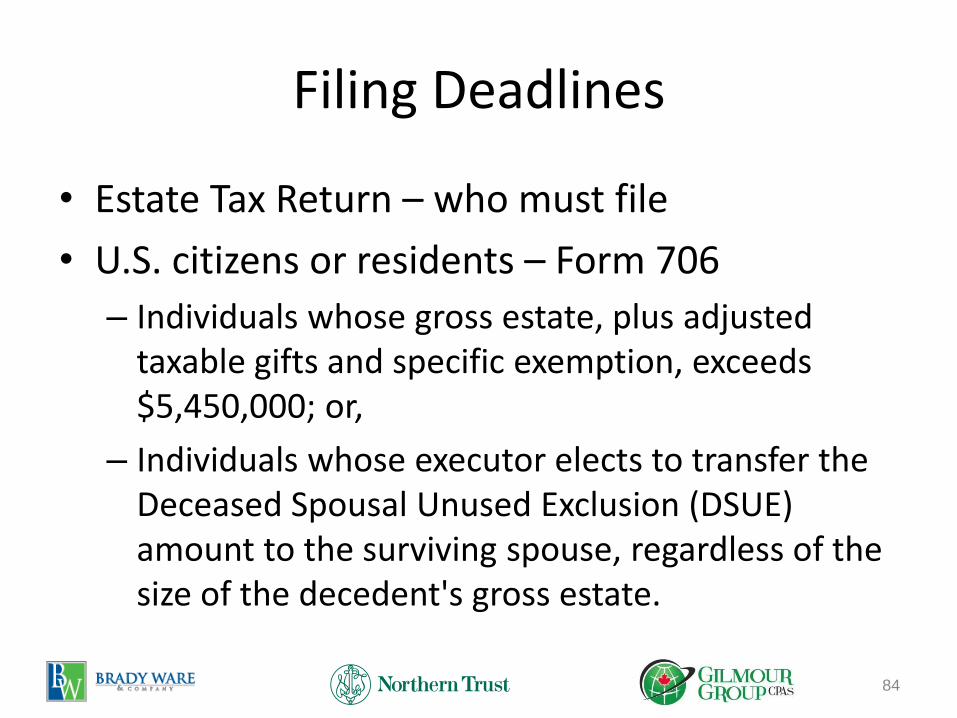

• Estate Tax Return – who must file

• U.S. citizens or residents – Form 706

– Individuals whose gross estate, plus adjusted taxable gifts and specific exemption, exceeds $5,450,000; or,

– Individuals whose executor elects to transfer the Deceased Spousal Unused Exclusion (DSUE) amount to the surviving spouse, regardless of the size of the decedent's gross estate.

Filing Deadlines

85

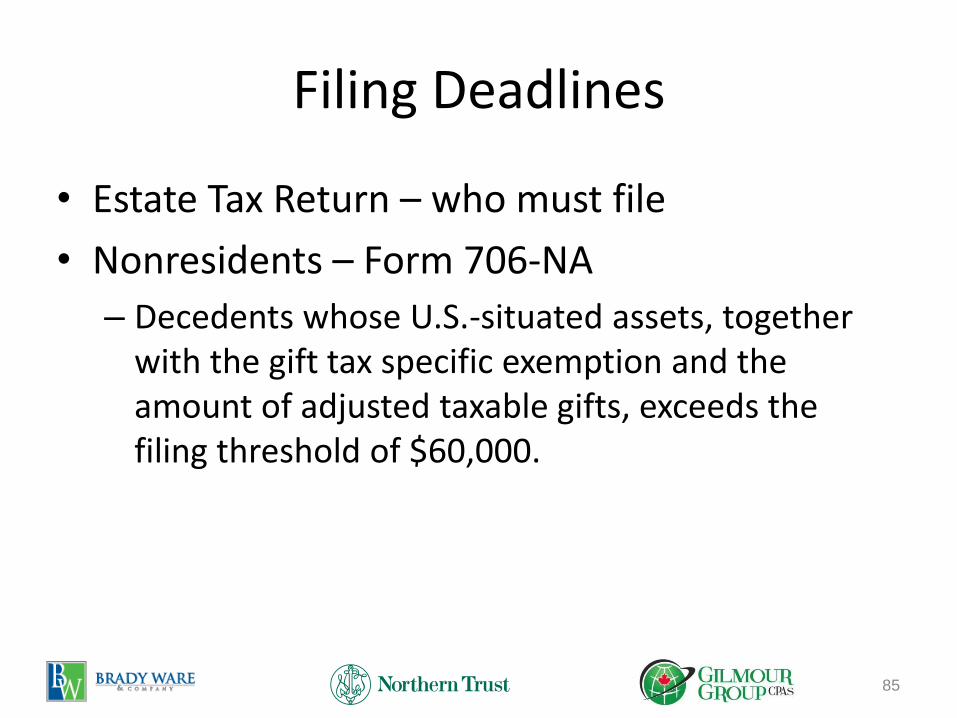

• Estate Tax Return – who must file

• Nonresidents – Form 706-NA

– Decedents whose U.S.-situated assets, together with the gift tax specific exemption and the amount of adjusted taxable gifts, exceeds the filing threshold of $60,000.

When to File Estate Tax Return

86

• Generally Form 706 and 706-NA are to be filed within 9 months after the date of the decedent's death.

• A six month extension is available.

Reporting Requirements

87 08/12/2016

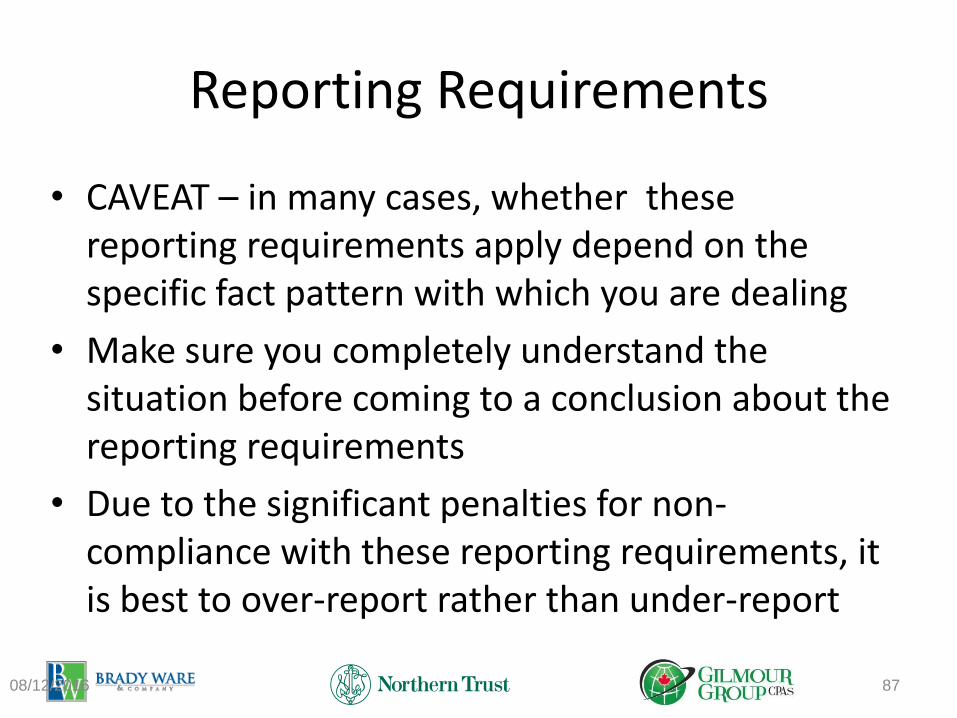

• CAVEAT – in many cases, whether these reporting requirements apply depend on the specific fact pattern with which you are dealing

• Make sure you completely understand the situation before coming to a conclusion about the reporting requirements

• Due to the significant penalties for non-compliance with these reporting requirements, it is best to over-report rather than under-report

Reporting Requirements

88 08/12/2016

Here are the most likely forms which may need to be filed by the beneficiary when property is gifted or inherited

– FinCEN 114 (Foreign Bank Accounts)

– Forms 3520 and 3520-A (Foreign Trusts)

– Form 5471 (Controlled Foreign Corporation)

– Form 8621 (Passive Foreign Investment Company or PFIC)

– Form 8865, Return of U.S .Persons with Respect to Certain Foreign Partnerships

– Form 8858, Information Return of a U.S. Persons with Respect to Foreign Disregarded Entities

– Form 8938 (Foreign Financial Asset Reporting)

Reporting Requirements

89 08/12/2016

• Other forms also may be required in unusual situations, but are likely not relevant for purposes of today’s discussion:

– Form 926, Return by a U.S. Transferor of Property to a Foreign Corporation

– Form 5472, Information Return of a 25% Foreign Owned U.S. Corporation or a Foreign Corporation Engaged in a U.S. Trade or Business

• Be aware of these in case any of these apply to a particular situation

Grantor Trust Considerations • The grantor trust rules tax a grantor on trust income or

income of a portion of the trust over which the individual: – Has a reversionary interest in excess of 5 percent at its

inception – Retains excessive powers to control the beneficial

enjoyment of trust income and property – Holds prohibited administrative powers that enable him to

deal in an advantageous way with trust property – Retains a power to revoke the trust – Either the individual or spouse has a right to receive trust

income • In addition, foreign trusts with U.S. beneficiaries are

generally treated as grantor trusts

90

Grantor Trust Considerations

• Foreign grantor trusts are reportable on Form 3520, Annual Return to Report Transactions with Foreign Trusts and Receipt of Certain Foreign Gifts and Form 3520-A, Annual Information Return of Foreign Trust With a U.S. Owner

91

Form 3520 Penalties

• A penalty generally applies if Form 3520 is not timely filed or if the information is incomplete or incorrect. The initial penalty is equal to the greater of $10,000 or – 35% of the gross value of any property transferred to a foreign trust for

failure by a U.S. transferor to report the creation of or transfer to a foreign trust or

– 35% of the gross value of the distributions received from a foreign trust for failure by a U.S. person to report receipt of the distribution or

– 5% of the gross value of the portion of the trust's assets treated as owned by a U.S. person for failure by the U.S. person to report the U.S. owner information

92

Filing Considerations – Form 3520-A

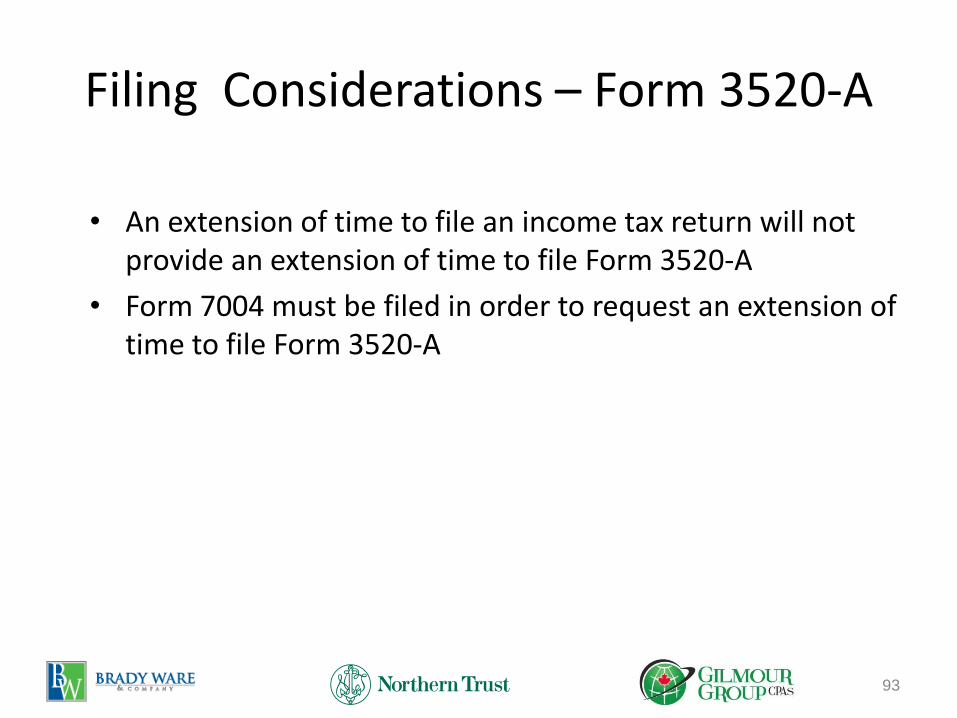

• An extension of time to file an income tax return will not provide an extension of time to file Form 3520-A

• Form 7004 must be filed in order to request an extension of time to file Form 3520-A

93

Form 3520-A Penalties

• A penalty generally applies if Form 3520 is not timely filed or if the information is incomplete or incorrect. The U.S. owner is subject to an initial penalty equal to the greater of $10,000 or

• 5% of the gross value of the portion of the trust's assets treated as owned by the U.S. person at the close of that tax year

• Additional penalties will be imposed if the noncompliance continues for more than 90 days after the IRS mails a notice of failure to comply with the required reporting

94

Form 8621 (PFIC) Reporting Considerations

• Does investment constitute a PFIC?

– A PFIC is foreign corporation which meets either the income or asset test described below.

• Income test: 75% or more of the corporation's gross income for its taxable year is passive income (as defined in section 1297(b)).

• Asset test: At least 50% of the average percentage of assets (determined under section 1297(e)) held by the foreign corporation during the taxable year are assets that produce passive income or that are held for the production of passive income

95

Form 5471

96

• Controlled Foreign Corporations (CFC)

• When is reporting required?

– U.S. persons who acquire or sell 10% of more of the stock of a foreign corporation have certain reporting requirements

– U.S. persons who own 10% or more of a foreign corporation is more than 50% owned by U.S. persons have different reporting requirements

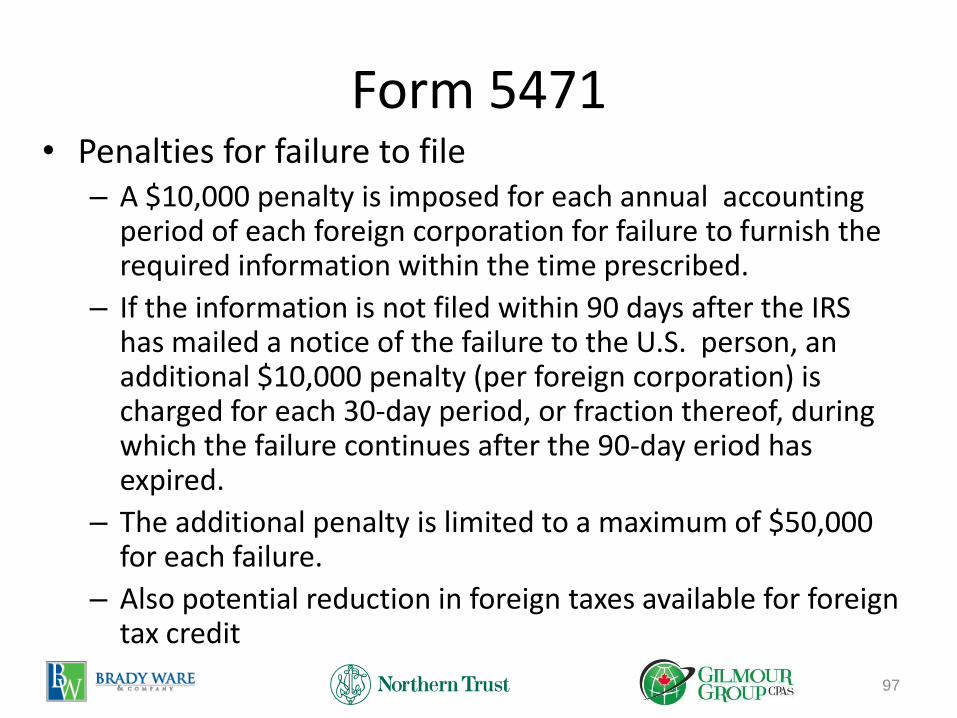

Form 5471 • Penalties for failure to file

– A $10,000 penalty is imposed for each annual accounting period of each foreign corporation for failure to furnish the required information within the time prescribed.

– If the information is not filed within 90 days after the IRS has mailed a notice of the failure to the U.S. person, an additional $10,000 penalty (per foreign corporation) is charged for each 30-day period, or fraction thereof, during which the failure continues after the 90-day eriod has expired.

– The additional penalty is limited to a maximum of $50,000 for each failure.

– Also potential reduction in foreign taxes available for foreign tax credit

97

Form 8858

Information Return of U.S. Persons With Respect To Foreign Disregarded Entities

• Who must file – U.S. Persons that are tax owners of FDEs at any time during the U.S.

person's taxable year or annual accounting period.

– Certain U.S. persons that are required to file Form 5471 with respect to a controlled foreign corporation (CFC) that is a tax owner of an FDE at any time during the CFC's annual accounting period

– Certain U.S. Persons that are required to File Form 8865 with respect to a controlled foreign partnership (CFP) that is a tax owner of an FDE at any time during the CFP's annual accounting period

98

Form 8858

Information Return of U.S. Persons With Respect To Foreign Disregarded Entities

• Penalties for failure to file – A $10,000 penalty is imposed for each annual accounting period of each

foreign corporation for failure to furnish the required information within the time prescribed.

– If the information is not filed within 90 days after the IRS has mailed a notice of the failure to the U.S. person, an additional $10,000 penalty (per foreign corporation) is charged for each 30-day period, or fraction thereof, during which the failure continues after the 90-day period has expired.

– The additional penalty is limited to a maximum of $50,000 for each failure.

– Also potential reduction in foreign taxes available for foreign tax credit

99

Form 8865

Return of U.S. Persons With Respect to Certain Foreign Partnerships • Who must file

– U.S. Person who controls the partnership • Control is a >50% in the partnership

– U.S. Persons with more than 10% ownership if partnership is controlled by U.S. persons (total interest of all U.S. persons is >50%)

– U.S. Persons who make certain contributions to the partnership

– U.S. Persons who have “reportable events” during the year

100

Form 8865 Return of U.S. Persons With Respect to Certain Foreign Partnerships • Penalties for failure to file

– A $10,000 penalty is imposed for each annual accounting period of each foreign corporation for failure to furnish the required information within the time prescribed.

– If the information is not filed within 90 days after the IRS has mailed a notice of the failure to the U.S. person, an additional $10,000 penalty (per foreign corporation) is charged for each 30-day period, or fraction thereof, during which the failure continues after the 90-day period has expired.

– The additional penalty is limited to a maximum of $50,000 for each failure.

– Also potential reduction in foreign taxes available for foreign tax credit

101

Form 8938 Reporting Considerations

• Are the assets considered “Specified Foreign Financial Assets (SFFAs)”?

– Specified foreign financial assets include the following:

• Financial accounts maintained by a foreign financial institution.

• Foreign financial assets which are personally held for

investment - stocks, bonds, etc.

102

Form 8938 Reporting Considerations

• Are the assets considered “Specified Foreign Financial Assets (SFFAs)”?

– SFFAs are reported on Form 8938, unless required to be reported elsewhere

– Form 8938 has a failure to file penalty of $10,000 plus additional $10,000 penalty up to a maximum of $50,000 for each 30 day period that failure to file continues after 90 days following IRS notice

103

Form 8938 Filing Thresholds

104 08/12/2016

Filing Status Total Value of all FFAs at end of Year

Maximum value of all FFAs at any time during year

Single and Married Filing Separately (MFS) – living in U.S.

$50,000 $75,000

Single and MFS – living outside the U.S.

$200,000 $300,000

Married Filling Jointly (MFJ) – living in U.S.

$100,000 $150,000

MFJ – living outside the U.S.

$400,000 $600,000

Form 8938 is required to be filed if all SFFAs (including SFFAs reported on other forms) exceed the

following amounts:

FBAR (FinCEN 114) Filing and Reporting Considerations

• Is the investment held in a foreign bank or financial account?

– FBAR filing requirement – U.S. person with a financial interest in or signature authority over foreign bank and financial accounts

105

What is a Financial Account? • A financial account includes, but is not limited to, a

securities, brokerage, savings, demand, checking, deposit, time deposit, or other account maintained with a financial institution (or other person performing the services of a financial institution).

• A financial account also includes a commodity futures or options account, an insurance policy with a cash value (such as a whole life insurance policy), an annuity policy with a cash value, and shares in a mutual fund or similar pooled fund (i.e., a fund that is available to the general public with a regular net asset value determination and regular redemptions).

106

What is a Foreign Financial Account?

• A foreign financial account is a financial account located outside of the United States.

• For example, an account maintained with a branch of a United States bank that is physically located outside of the United States is a foreign financial account.

• An account maintained with a branch of a foreign bank that is physically located in the United States is not a foreign financial account.

107

What is a Financial Account?

• Due to the expansive definition of financial account, it is recommended that any account which might be considered a foreign financial account be reported

108

What is a Financial Interest?

A United States person has a financial interest in a foreign financial account for which:

• The United States person is the owner of record or holder of legal title, regardless of whether the account is maintained for the benefit of the United States person or for the benefit of another person; or

109

What is a Financial Interest?

A United States person has a financial interest in a foreign financial account for which:

• The owner of record or holder of legal title is one of the following: – A trust of which the United States person: (i) is the trust grantor

and (ii) has an ownership interest in the trust for United States federal tax purposes;

– A trust in which the United States person has a greater than 50 percent present beneficial interest in the assets or income of the trust for the calendar year; or

– Any other entity in which the United States person owns directly or indirectly more than 50 percent of the voting power, total value of equity interest or assets, or interest in profits.

110

FBAR (FinCEN 114) Filing and Reporting Considerations

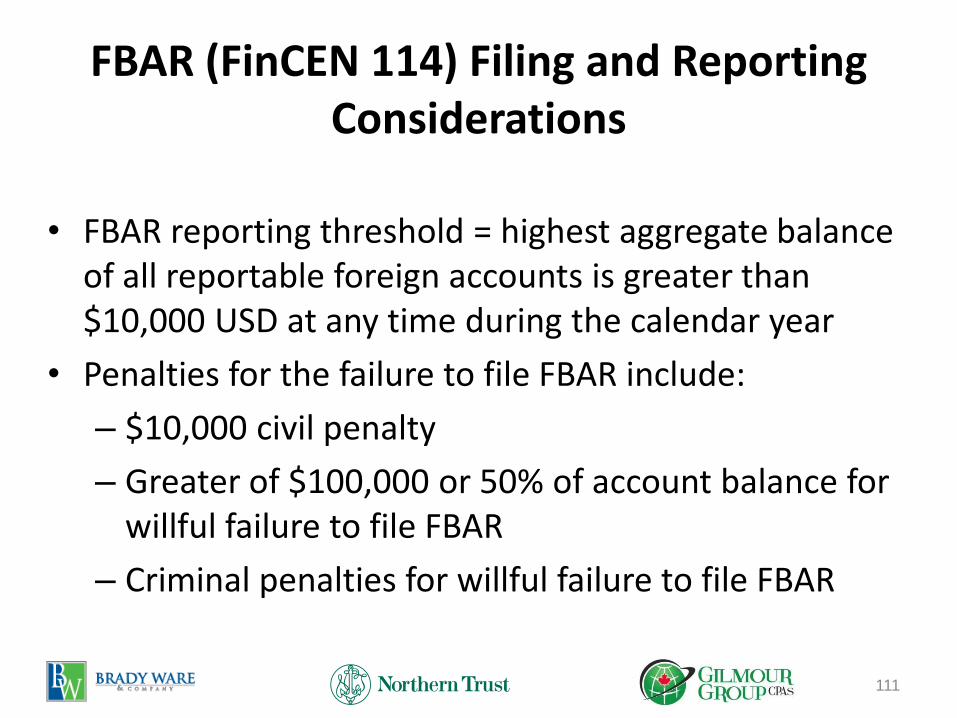

• FBAR reporting threshold = highest aggregate balance of all reportable foreign accounts is greater than $10,000 USD at any time during the calendar year

• Penalties for the failure to file FBAR include:

– $10,000 civil penalty

– Greater of $100,000 or 50% of account balance for willful failure to file FBAR

– Criminal penalties for willful failure to file FBAR

111

IRS AMNESTY PROGRAMS FOR FAILURE TO PROPERLY REPORT

OFFSHORE ASSETS

112

IRS Amnesty Programs for Delinquent Filers

• 2012 Offshore Voluntary Disclosure Program • The IRS Offshore Voluntary Disclosure Program is working

with taxpayers whose penalties may be reduced. • The IRS began an open-ended OVDP in January 2012

because of strong interest in the 2009 and 2011 programs. The IRS may end the 2012 program at any time in the future.

• The IRS is offering taxpayers with undisclosed income from offshore accounts another opportunity to get current with their tax returns.

• The 2012 OVDP has a higher penalty rate than the previous programs, but offers clear benefits to encourage taxpayers to disclose foreign accounts now rather than risk detection by the IRS and possible criminal prosecution.

113

IRS Amnesty Programs for Delinquent Filers

• Streamlined Filing Compliance Procedures

– Eligibility criteria for the streamlined procedures

• Taxpayers must certify that conduct was not willful.

• IRS has not initiated a civil examination of taxpayer's returns for any taxable year.

• Taxpayers eligible to use streamlined procedures who have previously filed delinquent or amended returns must pay previous penalty assessments.

• Taxpayers who want to participate in the streamlined procedures need a valid Taxpayer Identification Number.

114

IRS Amnesty Programs for Delinquent Filers

• Streamlined Filing Compliance Procedures for U.S. taxpayers

– U.S. taxpayers (U.S. citizens, lawful permanent residents, and those meeting the substantial presence test of IRC section 7701(b)(3)) eligible to use the Streamlined Domestic Offshore Procedures must

– For each of the most recent 3 years for which the U.S. tax return due date file amended tax returns, together with all required information returns (e.g., Forms 3520, 3520-A, 5471, 5472, 8938, 926, and 8621),

– For each of the most recent 6 years for which the FBAR due date has passed (the “covered FBAR period”), file any delinquent FBARs (FinCEN Form 114, previously Form TD F 90-22.1),

115

IRS Amnesty Programs for Delinquent Filers

• Streamlined Filing Compliance Procedures for U.S. taxpayers

– Pay all tax and interest due, and

– Pay a Title 26 miscellaneous offshore penalty. • The Title 26 miscellaneous offshore penalty is equal to 5 percent of the

highest aggregate balance/value of the taxpayer’s foreign financial assets that are subject to the miscellaneous offshore penalty during the years in the covered tax return period and the covered FBAR period.

– The full amount of the tax, interest, and miscellaneous offshore penalty due in connection with these filings should be remitted with the amended tax returns.

116

IRS Amnesty Programs for Delinquent Filers

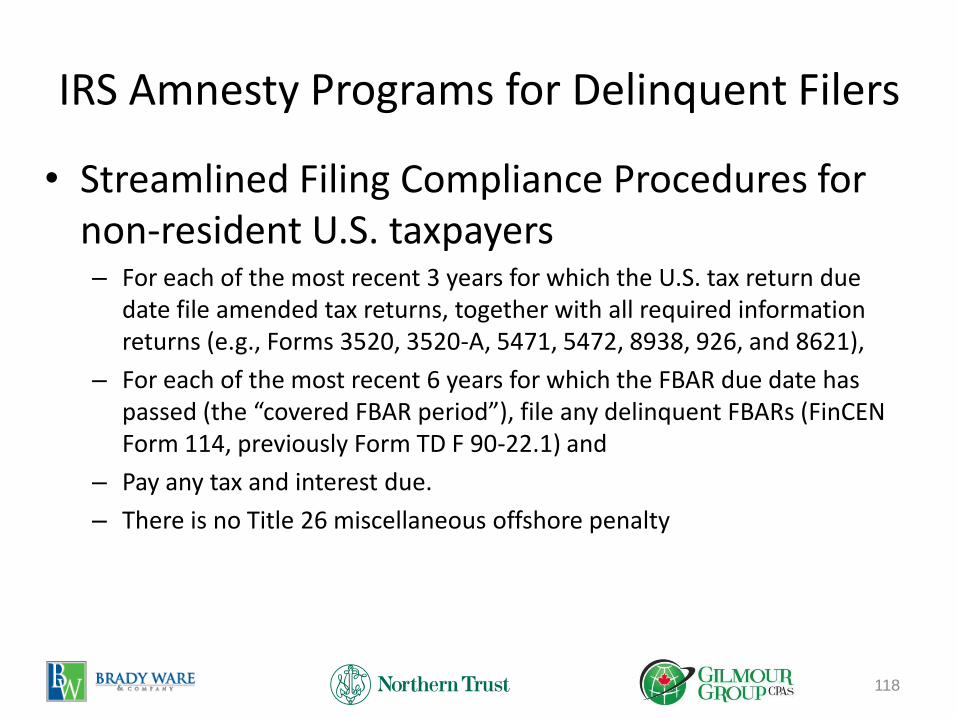

• Streamlined Filing Compliance Procedures for non-resident U.S. taxpayers

– Individual U.S. citizens or lawful permanent residents, or

estates of U.S. citizens or lawful permanent residents, meet the applicable non-residency requirement if, in any one or more of the most recent three years for which the U.S. tax return due date (or properly applied for extended due date) has passed, the individual did not have a U.S. abode and the individual was physically outside the United States for at least 330 full days.

117

IRS Amnesty Programs for Delinquent Filers

• Streamlined Filing Compliance Procedures for non-resident U.S. taxpayers – For each of the most recent 3 years for which the U.S. tax return due

date file amended tax returns, together with all required information returns (e.g., Forms 3520, 3520-A, 5471, 5472, 8938, 926, and 8621),

– For each of the most recent 6 years for which the FBAR due date has passed (the “covered FBAR period”), file any delinquent FBARs (FinCEN Form 114, previously Form TD F 90-22.1) and

– Pay any tax and interest due.

– There is no Title 26 miscellaneous offshore penalty

118

IRS Amnesty Programs for Delinquent Filers

• Failure to file information returns with no tax due – Taxpayers who do not need to use the OVDP or the

Streamlined Filing Compliance Procedures to file delinquent or amended tax returns to report and pay additional tax, but who:

• have not filed one or more required international information returns,

• have reasonable cause for not timely filing the information returns,

• are not under a civil examination or a criminal investigation by the IRS, and

• have not already been contacted by the IRS about the delinquent information returns

• should file the delinquent information returns with a statement of all facts establishing reasonable cause for the failure to file.

119

IRS Amnesty Programs for Delinquent Filers

• Failure to file FBAR returns • Taxpayers who

– have not filed a required Report of Foreign Bank and Financial Accounts (FBAR) (FinCEN Form 114, previously Form TD F 90-22.1),

– Who reported all income for the foreign financial accounts on their tax returns,

– Are not under a civil examination or a criminal investigation by the IRS, and

– Have not already been contacted by the IRS about the delinquent FBARs

– Should file the delinquent FBARs according to the FBAR instructions

120

Grant Gilmour Partner International Tax Gilmour Group CPA’s

Grant is a corporate tax advisor. He has been in the CA business since 1988, starting his own practice in 1994. His practice focuses on corporate clients in manufacturing and distribution industries that sell products internationally. Grant has a vast knowledge of tax planning, international tax issues and Scientific Research and Development tax credits, and is a graduate of the CICA In-Depth Tax Course.

GrossDukeNelson & Co.

204-8047 199 Street Langley, Metro Vancouver, BC V2Y 0E2 Tel: 604-888-4200 Fax: 604-882-1210 [email protected]

121

C. Edward Kennedy Jr Senior Manager Brady Ware & Co.

Ed has over 35 years of experience dealing with a variety of international tax matters. He specializes in tax consulting services to a wide variety of clients ranging from closely held companies to multi-national businesses. His expertise includes domestic and foreign income and social security tax planning, tax compliance for individuals and corporations, tax treatment of incentive compensation plans, international assignment program administration and policy design . Prior to joining the firm, Ed was with KPMG LLP, where, in addition to providing the above services, he served as the US firm’s lead for international social security matters. Ed’s technical skills include all aspects of international tax and social security planning, including individual and corporate tax reporting of foreign assets, including controlled foreign corporations, foreign trusts, passive foreign investment companies, and foreign bank accounts, compliance with domestic and foreign income and social security tax planning for individuals and corporations, domestic and international individual and corporate income tax compliance, and tax treatment of incentive compensation plans.

GrossDukeNelson & Co.

2340 Perimeter Park Drive Suite 100 Atlanta, GA 30341 Tel 770-458-5000 Fax 770-451-8900 [email protected]

122

Susan J. Merritt, Senior Vice President,

The Northern Trust Company, Orange County

Region

Susan Merritt is a Senior Vice President and is the Senior Fiduciary Officer for the Orange County region of the Northern Trust Company. She is a member of the State Bar of California and is a non-practicing member of the Law Society of British Columbia. Prior to joining Northern Trust, Susan was a practicing attorney with a large business law firm in Vancouver, Canada wherein her practice focused on tax and estate planning for high net worth individuals and families. In Susan’s current role at Northern Trust, she is responsible for overseeing all aspects of the OC region’s fiduciary practice including oversight of all trust relationships, management and mitigation of fiduciary risk, review of all new trust business, and oversight of all court related matters including administrative petitions and fiduciary litigation. Susan also works with select Wealth Management clients and their advisors to develop integrated tax and estate plans and wealth management strategies

GrossDukeNelson & Co.

Susan J. Merritt,

Senior Vice President

The Northern Trust Company

Orange County Region

(949) 717-5531

123

About Integra International

124

Integra International is an interactive association of CPAs, CAs and Business Advisors that share

knowledge openly and regularly. Member firms offer expanded professional services to their clients,

including meeting their national and international needs.

Founded in 1994, Integra International now has offices in almost every major business center of the

world. Currently there are 123 member firms in 65 countries, with over 4,200 professionals.

The knowledge (both domestic and international) of the individuals involved in Integra International is

available to be drawn upon by any member needing assistance.

For more information please click here to visit Integra International's website.