Urgent care

43

(303) 801- 0123 URGENT CARE TRANSACTIONS: CRITICAL INSIGHT FOR OPERATORS AND DEAL MAKERS

-

Upload

curtis-bernstein -

Category

Healthcare

-

view

226 -

download

0

Transcript of Urgent care

(303) 801-0123

URGENT CARE TRANSACTIONS: CRITICAL INSIGHT FOR OPERATORS

AND DEAL MAKERS

2(303) 801-0123

• Per the American Academy of Urgent Care Medicine: “Urgent Care Medicine is the provision of immediate medical service offering outpatient care for the treatment of acute and chronic illness and injury. . . . Urgent care does not replace your primary care physician. An urgent care center is a convenient option when someone's regular physician is on vacation or unable to offer a timely appointment. Or, when illness strikes outside of regular office hours, urgent care offers an alternative to waiting for hours in a hospital Emergency Room.”

• Per the Urgent Care Association of America, Urgent Care is differentiated from other deliver models by providing:• No appointment necessary / walk-in care;• Evening and weekend operating hours;• X-ray on site; and • Capability to perform procedures like suturing, splinting and IV

What Is Urgent Care?

3(303) 801-0123

The phenomenon of the development of urgent care centers is due to the oversupply of physicians, some of whom have opted to engage in a new level of entrepreneurship by expanding the types of services they offer including clinics treating minor medical problems without an appointment

Quotes

4(303) 801-0123

The phenomenon of the development of urgent care centers is due to the oversupply of physicians, some of whom have opted to engage in a new level of entrepreneurship by expanding the types of services they offer including clinics treating minor medical problems without an appointment

Quotes

US New & World Report 1983

5(303) 801-0123

Urgent care centers are one of the innovative alternatives methods that will render hospital emergency departments vulnerable to replacement

Quotes

6(303) 801-0123

Urgent care centers are one of the innovative alternatives methods that will render hospital emergency departments vulnerable to replacement

Quotes

Harvard Business Review 1980

7(303) 801-0123

• Hospital began purchasing independent urgent care centers

• Managed like hospitals with licensed nurses, triage processes, and union wages

• Centers were not marketed cohesively• People did not know what kind of care they could get at

an urgent care center

What Happened?

8(303) 801-0123

• Average emergency room (ER) wait time; Nationally takes an average of:

• 135 minutes before being sent home• 53 minutes to receive pain medication when presenting

with a broken bone• 96 minutes after being admitted to get to a room

• More healthcare cost is shifted to the patient• Average ER bill is estimated between $1,250 to $2,000• Average urgent care bill is <$500• 1/3 to ½ of all ER visits are for non urgent care and the

CDC estimates that moving these cases to urgent care could save $18 billion in healthcare costs

What Has Happened Since?

9(303) 801-0123

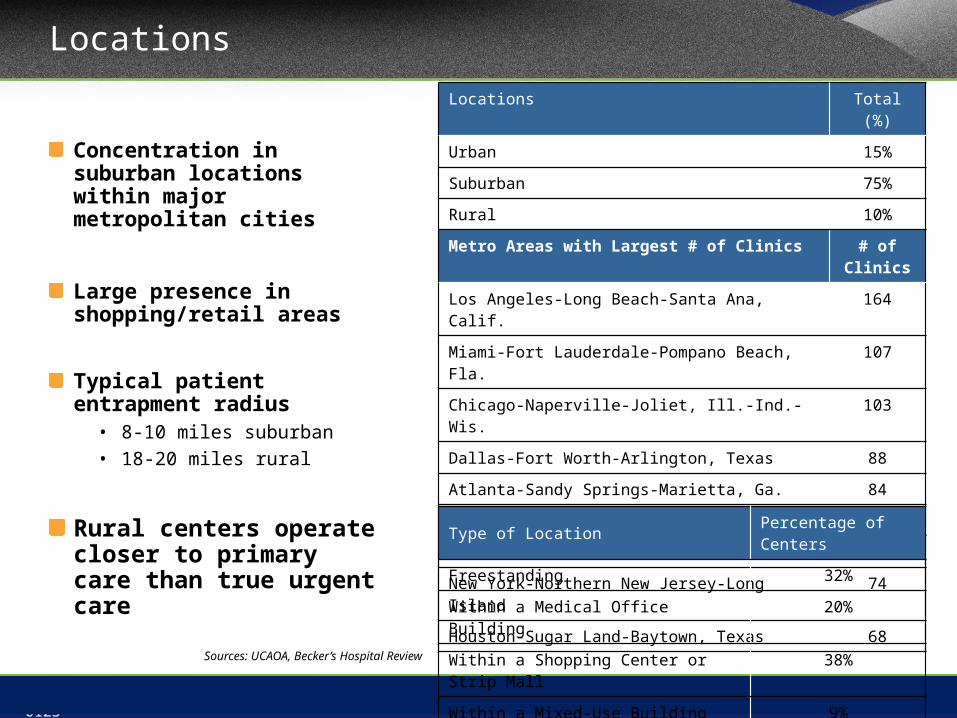

Locations

Concentration in suburban locations within major metropolitan cities

Large presence in shopping/retail areas

Typical patient entrapment radius

• 8-10 miles suburban• 18-20 miles rural

Rural centers operate closer to primary care than true urgent care

Locations Total (%)

Urban 15%

Suburban 75%

Rural 10%

Metro Areas with Largest # of Clinics # of Clinics

Los Angeles-Long Beach-Santa Ana, Calif. 164

Miami-Fort Lauderdale-Pompano Beach, Fla. 107

Chicago-Naperville-Joliet, Ill.-Ind.-Wis. 103

Dallas-Fort Worth-Arlington, Texas 88

Atlanta-Sandy Springs-Marietta, Ga. 84

Phoenix-Mesa-Scottsdale, Ariz. 80

Detroit-Warren-Livonia, Mich. 76

New York-Northern New Jersey-Long Island 74

Houston-Sugar Land-Baytown, Texas 68

Type of Location Percentage of Centers

Freestanding 32%

Within a Medical Office Building 20%

Within a Shopping Center or Strip Mall 38%

Within a Mixed-Use Building 9%Sources: UCAOA, Becker’s Hospital Review

10(303) 801-0123

Average Payor Mix

Private Insurance55%

Medicare17%

Out-of-Pocket Payments

10%

Other5%

Medicaid5%

Worker’s Com-pensation

5% Other Government4%

Commercial insurance is most prominent payor

• Case rates are common

• Patient out-of-pocket higher compared to primary care visit (i.e. 30%-50% of total visit reimbursement from patient)

Low government payors• Reimbursement generally through

Medicare Part B – bill via the Physician Fee Schedule on a fee-for-service basis

• Medicare patients do not have time pressure

• Some clinics do not accept Medicaid

Discounts (typically 15-20%) available for patients without insurance

11(303) 801-0123

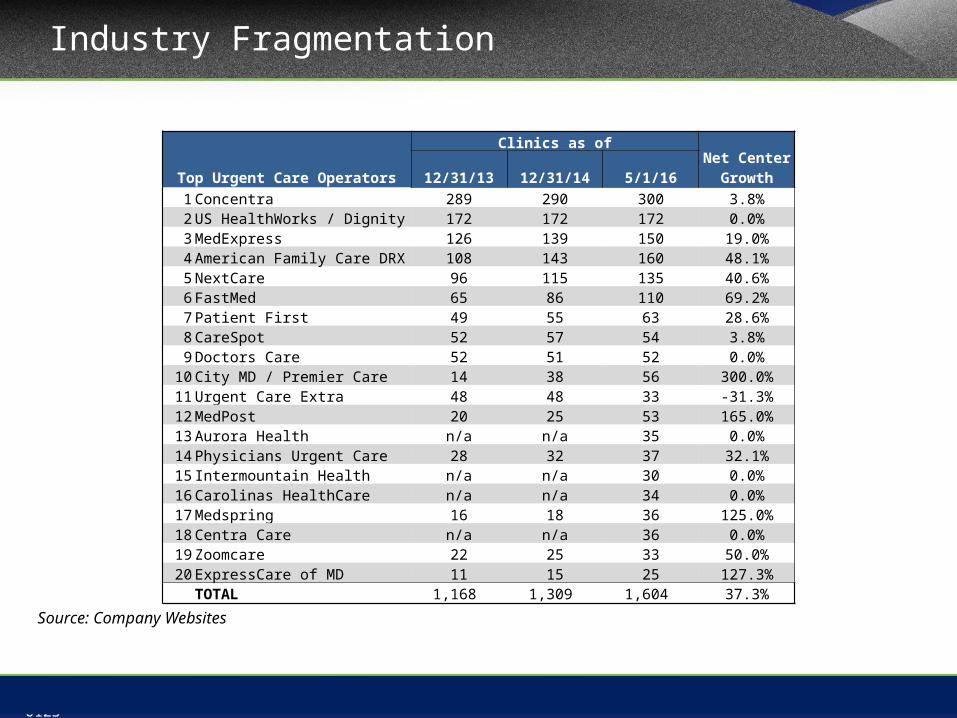

Industry Fragmentation

Source: Company Websites

Top Urgent Care Operators

Clinics as ofNet Center

Growth12/31/13 12/31/14 5/1/161 Concentra 289 290 300 3.8%2 US HealthWorks / Dignity 172 172 172 0.0%3 MedExpress 126 139 150 19.0%4 American Family Care DRX 108 143 160 48.1%5 NextCare 96 115 135 40.6%6 FastMed 65 86 110 69.2%7 Patient First 49 55 63 28.6%8 CareSpot 52 57 54 3.8%9 Doctors Care 52 51 52 0.0%

10 City MD / Premier Care 14 38 56 300.0%11 Urgent Care Extra 48 48 33 -31.3%12 MedPost 20 25 53 165.0%13 Aurora Health n/a n/a 35 0.0%14 Physicians Urgent Care 28 32 37 32.1%15 Intermountain Health n/a n/a 30 0.0%16 Carolinas HealthCare n/a n/a 34 0.0%17 Medspring 16 18 36 125.0%18 Centra Care n/a n/a 36 0.0%19 Zoomcare 22 25 33 50.0%20 ExpressCare of MD 11 15 25 127.3%

TOTAL 1,168 1,309 1,604 37.3%

12(303) 801-0123

Current Drivers of Urgent Care M&A

M&A activity in the Urgent Care market continues at a feverish pace.el

lSDrivers of Seller Interest

•Historically high transaction multiples•Narrow Networks•Increased and Stronger Competition •Increase complexities and cost•Need to invest in growth or align with a larger operator•Growth Capital•Add sophistication

Drivers of Buyer Interest

•The Affordable Care Act/Healthcare reform •Highly Fragmented market•Scalability and industry growth •Overcrowded Emergency Rooms •Lack of Access to primary care•Access to Patients-New Patients into system/Networks•Consumerism•Low cost of debt•Competitive Landscape• Shift in healthcare cost burden

13(303) 801-0123

Urgent Care Buyer Universe

Hospital Health Systems Pure Play Consolidators

Private Equity Commercial Insurance Payors

14(303) 801-0123

Urgent Care Buyer Universe

15(303) 801-0123

New Center Growth

1 2 3 4 5 6 7 8 9 10 11 12 13 $-

$5

$10

$15

$20

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

$10.14 $10.63 $11.29 $12.31 $13.19 $14.17 $15.77 $16.73 $17.82 $19.01 $20.08

$21.43 $22.58

8,000 8,100 8,700 8,800 9,300 9,428 9,899 10,434 11,350 11,350 12,099

12,299 12,845

Number of Urgent Care Centers & Industry RevenueAmount in BillionsIndustry Revenue # of Centers

2008-2015ECAGR # of Centers: 4.4%

2015P-2020PCAGR # of Centers: 4.2%

Sources: IBIS World, HarrisWilliams&Co., McguireWoods

~ 9,500 urgent care centers | $16 billion industry

16(303) 801-0123

• Private Equity investment in UC has remained strong• Higher than average number of PE-backed start ups and growth

equityMore than 15 Private Equity investments in Urgent Care since 2007

and more wanting in• Demand for bolt on deals have skyrocketed over the last few years

and will continue for the longterm The 1-3 center ownership comprises about 65% of the market and

represents the greatest opportunity

• Hospital lead health systems are now leading the charge• Since 2014 hospitals have been aggressively pursuing urgent care

• Managed Care is making their move• Historically payors have made minority investments but that has

changed

Urgent Care M&A Trends Driving Growth

17(303) 801-0123

• Select Medical Holdings and Welsh Care team up to buy Concentra from

Humana

• United Healthcare/Optum purchases MedExpress

• ABRY Partners purchase FastMed (PE TO PE)

• Crestline Investors invest in Urgent Team

• HCA purchases Urgent Care Extra’s Nevada operations and 14 centers

• FastMed acquires Texans Urgent Care 14 locations

• USPI Purchases Carespot and 35 centers from Welsh Carson which is also in a JV

with Tenet in USPI

• HCA purchased 18 of CareSpot Express locations in Nashville and Kansas City

Noteworthy Transactions

18(303) 801-0123

Valuation Multiples and Observations

Small Size Company Medium Size Company Large Size Company0.00 x2.00 x4.00 x6.00 x8.00 x

10.00 x12.00 x14.00 x16.00 x

TIC/EBITDA Multiple Ranges

MultiplesRecord high multiples of trailing earnings for platform acquisitionBuyers are typically paying for earnings rather than revenue

Types of Buyers

Strategic buyers are more common today than in previous yearsM&A has historically been dominated by private equity firmsHospitals and health systems are exhibiting growing of interest and

presence in the space

Drivers of Value

Growth opportunities and factors affecting demand Competitive environment and regional density Stage in business cycle and profitability Infrastructure and support (platform vs. stand-alone) Reimbursement and payor mix

19(303) 801-0123

• 2007 MedExpress was acquired by Excellere Partners, a private equity group

• 2010 Excellere sells MedExpress to General Atlantic and Sequoia Capital after only 3 years into their investment

• 50 Locations• $110M 2010 Rev• EV $450M• 4.1X EV/R• ~ 20X TTM EBITDA

• 2015 Optium, a subsidiary of UnitedHealth Group acquires MedExpress

• 134 Locations• $279M 2014 Rev• EV $1.5B• 5.4X EV/R• $11.2M Price Per Center• Assuming a 20% to 25% EBIDTA margin, +/- 25X TTM EBITDA

MedExpress Case Study

Source: PrivCO and Ambulatory Alliances, LLC

20(303) 801-0123

Overview

• Structuring with an Eye Towards an Exit• Getting Your House in Order• Before You Share: The DO’s and DON’T’s of Sharing Confidential

Information• Generally• Privileged Materials • HIPAA and PHI• Competitively sensitive information

• Certain Key Substantive Due Diligence Issues• Corporate Structure and Corporate Practice of Medicine

Issues• Misclassification• Stark Law Compliance• Coding Compliance• Others

21(303) 801-0123

Structuring with an Eye Towards an Exit

“Beginning with the end in mind”

• Choice of Entity

• Corporate form – often limited by corporate practice of medicine prohibition

• Be careful not to self-limit (e.g., DE professional corporation)

• Tax election (for corporations and LLCs)

• To MSO or Not to MSO

22(303) 801-0123

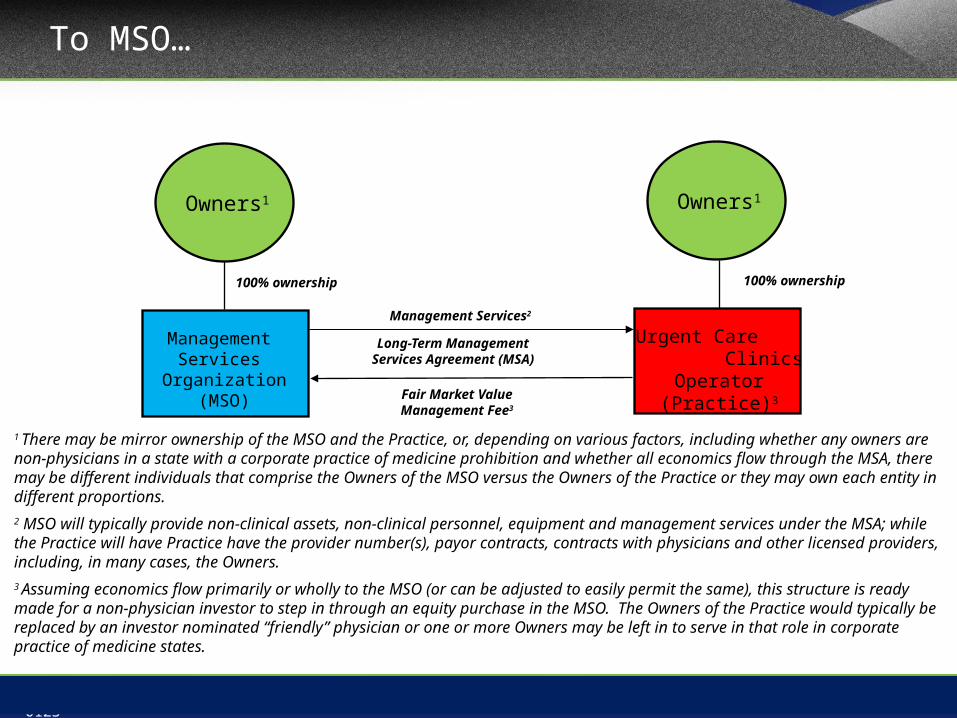

To MSO…

Fair Market Value Management Fee3

Long-Term Management Services Agreement (MSA)

Management Services Organization

(MSO)

100% ownership 100% ownership

Friendly Physician1

Urgent Care Clinics Operator

(Practice)3

Owners1Owners1

Management Services2

1 There may be mirror ownership of the MSO and the Practice, or, depending on various factors, including whether any owners are non-physicians in a state with a corporate practice of medicine prohibition and whether all economics flow through the MSA, there may be different individuals that comprise the Owners of the MSO versus the Owners of the Practice or they may own each entity in different proportions. 2 MSO will typically provide non-clinical assets, non-clinical personnel, equipment and management services under the MSA; while the Practice will have Practice have the provider number(s), payor contracts, contracts with physicians and other licensed providers, including, in many cases, the Owners.3 Assuming economics flow primarily or wholly to the MSO (or can be adjusted to easily permit the same), this structure is ready made for a non-physician investor to step in through an equity purchase in the MSO. The Owners of the Practice would typically be replaced by an investor nominated “friendly” physician or one or more Owners may be left in to serve in that role in corporate practice of medicine states.

23(303) 801-0123

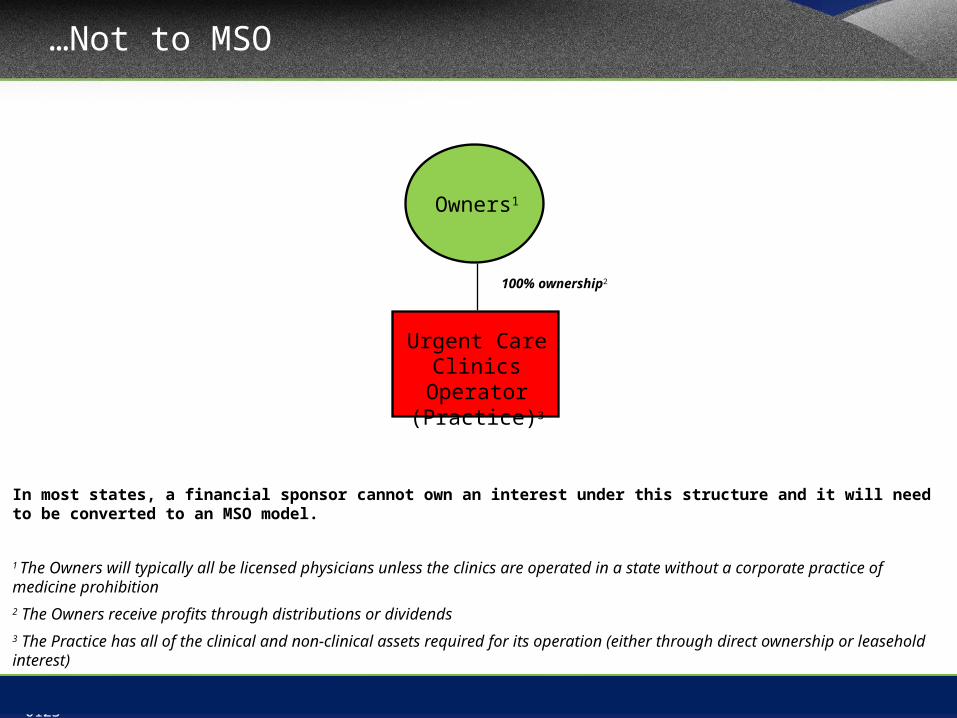

…Not to MSO

100% ownership2

Friendly Physician1

Urgent Care Clinics Operator

(Practice)3

Owners1

In most states, a financial sponsor cannot own an interest under this structure and it will need to be converted to an MSO model.

1 The Owners will typically all be licensed physicians unless the clinics are operated in a state without a corporate practice of medicine prohibition 2 The Owners receive profits through distributions or dividends3 The Practice has all of the clinical and non-clinical assets required for its operation (either through direct ownership or leasehold interest)

24(303) 801-0123

Structuring with an Eye Towards an Exit (cont.)

• Capitalization

• Compensation structure

• Thankfully, Most Structures Can Be Fixed

• Avoid Critical Errors

“If you don’t have time to do it right, when are you going to have time to do it over” – John Wooden

25(303) 801-0123

Fast Forward To….SUCCESS

You did a great job building your business….but are you ready for an exit?

26(303) 801-0123

Getting your House in Order

27(303) 801-0123

Getting your House in Order

Talk to Your Team What has been keeping them up at night? Remember all those things you left on the back burner…

Consider “Sell-Side” Due Diligence Can be comprehensive or high-level Can be formally led by outside counsel or an informal process in

consultation with counsel

Give the “Explanation Before the Accusation” In a process, it is better to know which bidders may be scared off by an

issue early on, then to lose the winning bidder after everyone else is gone

28(303) 801-0123

Before You Share: The DO’s & DON’T’s of Sharing Confidential Information

• What Can I Share Without a Confidentiality Agreement?

• Confidentiality or Non-Disclosure Agreement• Needs to be signed • Scope and carve-outs• Non-solicit?

• Can I Share Privileged Materials?• If so, when?• Common Interest Privilege

29(303) 801-0123

Before You Share: The DO’s & DON’T’s of Sharing Confidential Information (cont.)

• HIPAA and Other Privacy Laws• Surprisingly overlooked in many instances• Try to avoid PHI disclosure whenever possible, and always

adhere to “minimum necessary” standard• Disclosure of PHI permitted for due diligence under HIPAA

• 45 CFR § 164.501 defines “health care operations” to include “the sale, transfer, merger, or consolidation of all or part of the covered entity with another covered entity, or an entity that following such activity will become a covered entity and due diligence related to such activity”

• What if the buyer is not a covered entity and will not become one?

• Disclosure to third party advisors?

• What happens if there is a breach?

30(303) 801-0123

Before You Share: The DO’s & DON’T’s of Sharing Confidential Information (cont.)

• Sharing of Competitively Sensitive Information• The sharing of competitively sensitive pricing information

among competitors can be a violation of Antitrust laws• In the urgent care context, the concern will typically center

around payor contracts• Where a potential buyer is a competitor in the relevant

market that needs to understand parameters of the target’s reimbursement, a “black box” analysis is needed

• This is surprisingly overlooked, particularly in smaller transactions

• Be careful to avoid “gun jumping”

31(303) 801-0123

Certain Key Substantive Due Diligence Issues

• Corporate Structure and Corporate Practice of Medicine Issues

• Understanding the corporate structure and ownership is fundamental

• Some form of corporate practice of medicine prohibition in most jurisdictions

• Pitfalls of the “Friendly Physician”/“Captive Practice”/ “MSO Model”

• Overreaching into clinical decisions or otherwise with respect to control can invalidate arrangement

• Payors suits• “Friendly” physician risk

• Fee-splitting• Management fees must be fair market value for commercially

reasonable services being performed• Valuation and fee adjustments

32(303) 801-0123

Certain Key Substantive Due Diligence Issues (Cont.)

• Misclassification of Personnel• Employees versus Independent Contractors• The form of agreement does not control• Many urgent care operators contract with personnel as

independent contractors despite treating them like employees under IRS guidance*:

• Behavioral: Does the company control or have the right to control what the worker does and how the worker does his or her job?

• Financial: Are the business aspects of the worker’s job controlled by the payer? (these include things like how worker is paid, whether expenses are reimbursed, who provides tools/supplies, etc.)

• Type of Relationship: Are there written contracts or employee type benefits (i.e. pension plan, insurance, vacation pay, etc.)? Will the relationship continue and is the work performed a key aspect of the business?

• No one factor is determinative and must examine each case

33(303) 801-0123

Certain Key Substantive Due Diligence Issues (Cont.)

• Misclassification of Personnel (cont.)• Tax liability for employer withholdings and penalties• Potential liability for overtime (if personnel at issue are not exempt)• Independent Contractors may not want to transition to employment• Can create a Stark Law issue…

• Stark Law Compliance• DHS (typically X-ray and lab in urgent care space, occasionally may

be others)• If DHS referring physicians own the urgent care provider, then need

to meet “in-office ancillary services” exception• This will often require that the entity meet the group practice definition

under Stark• Group practice definition has a number of requirements, including that

Independent Contractor physicians cannot provide 25% or more of total patient encounters.

34(303) 801-0123

Certain Key Substantive Due Diligence Issues (Cont.)

• Stark Law Compliance (cont.)• Where physicians are not owners, can rely on employment or

personal services arrangements exception• However, ownership of MSO can trigger Stark as well, particularly

if not relying on the in-office ancillary services exception (and arguably, even then)

• Good news for urgent care: DHS revenue is often a small component of overall revenue

• Bad news: • It is not uncommon for Stark issues to be found in urgent care

providers• To avoid what are often technical errors from becoming false

claims, must complete a timely investigation and voluntary repayment

• In certain circumstances, a formal self-disclosure under the CMS SRDP may be needed

35(303) 801-0123

Certain Key Substantive Due Diligence Issues (Cont.)

• Coding Compliance• Any historic third party audits (e.g., CMS, RAC, commercial

payors)?• Internal auditing procedures?

• How often, who does them, what is the scope?• Buyer auditing of target

• Consultant or in-house team?• Common Issues

• Poor documentation• Is the process “overly automated”

36(303) 801-0123

Certain Key Substantive Due Diligence Issues (Cont.)

• Other Key Issues• Compensation Arrangements

• FMV and Bonuses

• HIPAA

• Supervision Arrangements and Documentation

• Medical Malpractice

• Etc.

37(303) 801-0123

• Healthcare is evolving from fee-for-service medicine toward value-based

reimbursement — and toward population health management.

• Hospitals are financially incentivized to reduce admissions

• Payors are looking for providers that can provide high-quality, cost-effective care

• Payors are demanding lower-cost settings of care

• Providers and Payors are becoming more involved in patient management and care

delivery

• Increased collaboration between and among providers

• Patients are seeking more convenient access to healthcare services

• Access, cost and convenience is overriding the once-sacred patient-physician

relationship

The Future of Urgent Care

38(303) 801-0123

• Full Price Transparency- flat straightforward pricing for medical services

• On-Demand injury, illness and well care. Rx on-site 365 days a year

• On-Demand worldwide video visits for minor injury and illness

• Convenient labs On-Demand

• Primary, Chronic and Episodic care at one location

• On-Demand access to specialist such as orthopedics and cardiologist

• On-Demand Surgery you schedule on your phone

• ER doctors On-Demand with Onsite X-Ray/CT/Ultrasound for $299

• Prescriptions filled at the clinic

Redefining Urgent Care

39(303) 801-0123

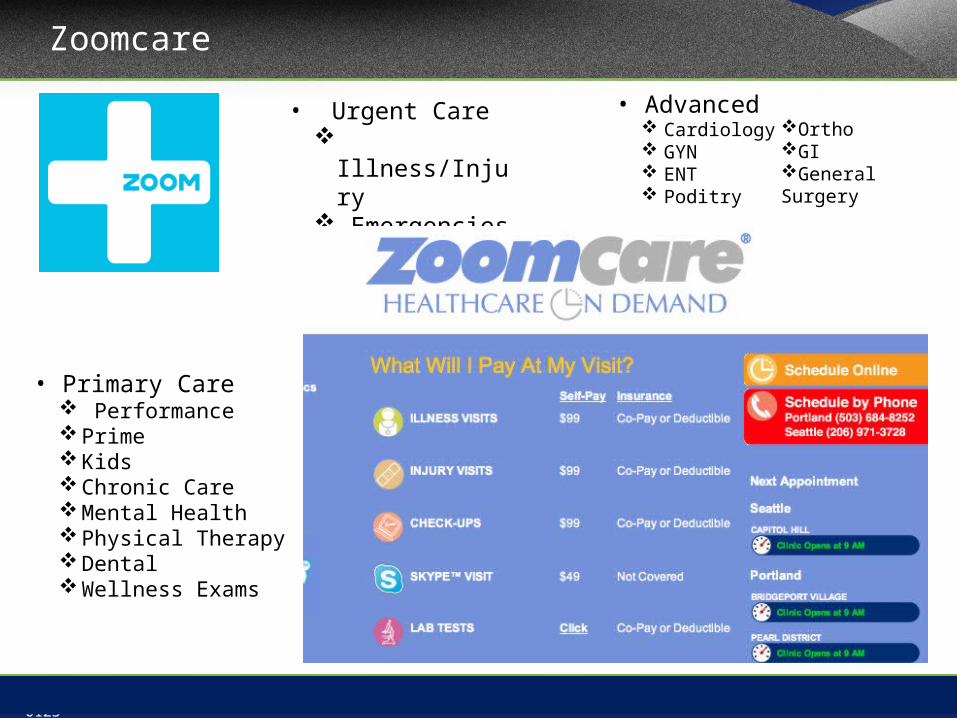

Zoomcare

• Urgent Care Illness/Injury Emergencies Video Visits

• Advanced Cardiology GYN ENT Poditry

• Primary Care Performance Prime Kids Chronic Care Mental Health Physical Therapy Dental Wellness Exams

OrthoGIGeneral Surgery

40(303) 801-0123

Outpatient Networks

Outpatient Networks, lead by urgent care will replace hospitals as the hubs of healthcare

41(303) 801-0123

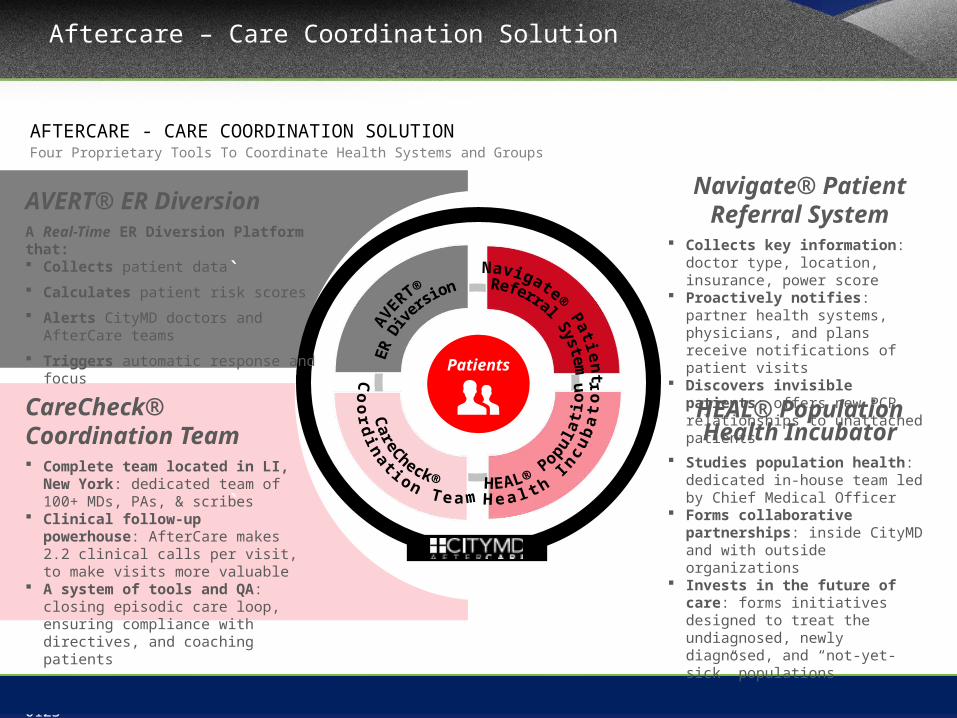

Aftercare – Care Coordination Solution

`

`

Patients

CareCheck® Coordination Team Complete team located in LI, New York:

dedicated team of 100+ MDs, PAs, & scribes

Clinical follow-up powerhouse: AfterCare makes 2.2 clinical calls per visit, to make visits more valuable

A system of tools and QA: closing episodic care loop, ensuring compliance with directives, and coaching patients

AVERT® ER DiversionA Real-Time ER Diversion Platform that: Collects patient data Calculates patient risk scores Alerts CityMD doctors and AfterCare teams Triggers automatic response and focus

Navigate® Patient Referral System

Collects key information: doctor type, location, insurance, power score

Proactively notifies: partner health systems, physicians, and plans receive notifications of patient visits

Discovers invisible patients: offers new PCP relationships to unattached patients

HEAL® Population Health Incubator

Studies population health: dedicated in-house team led by Chief Medical Officer

Forms collaborative partnerships: inside CityMD and with outside organizations

Invests in the future of care: forms initiatives designed to treat the undiagnosed, newly diagnosed, and “not-yet-sick” populations

AFTERCARE - CARE COORDINATION SOLUTIONFour Proprietary Tools To Coordinate Health Systems and Groups

42(303) 801-0123

THE CARE COORDINATION SOLUTION II: NAVIGATEThe End Goal Of Channeling Patients to The Right Providers

PCP 1

PCP 2

Specialist 2

Specialist 3

Specialist 4

Specialist 1Hospital 1

Urgent Care

Hospital 2

Hospital 3

43(303) 801-0123

Blayne Rush, President, Ambulatory AdvisorsPhone: (469) 385-7792 || Email: [email protected]

Adam Rogers, Partner, DLA PiperPhone: (305) 423-8527 || Email: [email protected]

Curtis Bernstein, Principal, Pinnacle Healthcare ConsultingPhone: (561) 901-5300 || Email: [email protected]

Contact Information