UPDATES ON FINANCIAL REPORTING STANDARDS AND THEIR...

46

HIGHLIGHTS OF RECENT FINANCIAL REPORTING STANDARDS AND THEIR IMPLICATIONS ON FUTURE BREED OF ACCOUNTANTS UNIVERSITY MALAYSIA SABAH – MAREF SEMINAR 23 June 2010 DR NORDIN MOHD ZAIN Executive Director Deloitte Malaysia

Transcript of UPDATES ON FINANCIAL REPORTING STANDARDS AND THEIR...

HIGHLIGHTS OF RECENT FINANCIAL REPORTING STANDARDS AND THEIR IMPLICATIONS ON

FUTURE BREED OF ACCOUNTANTS

UNIVERSITY MALAYSIA SABAH – MAREF SEMINAR

23 June 2010

DR NORDIN MOHD ZAIN

Executive Director

Deloitte Malaysia

Theme

• Change

• Tracking the rapids

• Recent standards

• Features of new breed of accountants

Change: Global trends on Financial Reporting Adoption

Europe

2005

Australia

2005

Canada

2009/2011

South Africa

2005

United States

(2014)

Current or committed to using IFRS

Brazil

2010

China

2007

India

2011

Chile

2009

Japan(2010/2015?)

Malaysia, Spore,

Indonesia(2012)

Malaysia’s position

• Pursuant to August 2008 announcement that:

• 1 January 2010 – FRS 139 effective date• Co-terminuous with Basel 2 implementation

• 1 January 2012 – Full blown IFRS in Malaysia• Global trends

4Deloitte @ 2009

Southeast Asian countries follow suit

5

Malaysia Thailand

Indonesia Singapore

VietnamPhilippines

MASB IASB

6 8 IFRS 1 2 3 4 5 6 7 8

27 29 IAS 1 2 7 8 10 11 12 16 17 18 19 20 21 23 24

33 (4) 37 26 27 28 29 31 32 33 34 36 37 38 39 40 41

6 (11) 17 IFRIC 1 2 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18

6Deloitte @ 2009

GAAP gap POSITION @ 31 December 2009

GAAP gap POSITION @ 1 January 2010 - narrowing

MASB IASB

8 9 IFRS 1 2 3 4 5 6 7 8 9

28 29 IAS 1 2 7 8 10 11 12 16 17 18 19 20 21 23 24

36 (2) 38 26 27 28 29 31 32 33 34 36 37 38 39 40 41

16 (1) 17 IFRIC 1 2 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18

7Deloitte @ 2009

Learning point

• Change has taken place globally & locally

• Inevitable

• So much to do

Tracking the Rapids

I F R S

37 Years and Forging Ahead

• 1973 - International Accounting Standards Committee (Committee)

• Historical cost regime

• Accounting regime

• 2001 - International Accounting Standards Board (Board)

• Fair value regime

• Financial reporting regime

I A S

Notable Changes

• Accounting standards have become a law of the country– FRS

– PERS

• Mandatory for companies to comply with accounting standards issued by MASB

• Applies to:– Public Listed Companies

– Financial Institutions under Bank Negara Malaysia

– Companies registered with Companies Commission of Malaysia (Sdn Bhdand Berhad)

• Not required but encouraged use by:– Government agencies

– Cooperatives

• Emergence of a family of standards on Fair Value –IAS 39 Financial Instruments Standards

• Change from Historical Cost to Fair Value

• Disclosure of market value in the notes to financial statements

• And many more

Notable Changes

FRS 139 family

FRS 139 - a Standard never so popular

• Complex

• Changing

• If you have read it and understood . . .

• FRS 139 (IAS 39) IFRS 9

14

What’s in store for 2012

FRS 3

Business

combination

FRS 141

Agriculture

IFRIC 4

Leases

Income

taxes

FRS 7 Fin.

instrument

disclosure

FRS 139

financial

instruments

Financial

statement

presentation

(Phase 1)

FRS 4

Insurance

(Phase 2)

Deadlines

-6 -5 -4 -3 -2 -10

1 2 3 4 5 67

8 9 10 1112

13 14 15 n n24

17

2011Half 2

FRS 3IFRIC 15

2010

FRS 139FRS 7FRS 4Interpretations

Qtr 1

First Qtrresult onFRS 139compliant

Opening IFRScompliant Balance Sheet

2012

Full suite IFRSFull suite IASAmendments

Deloitte @ 2009

Learning points

• Many more new things to come; exciting

• Train to be comfortable with pro-forma financial statements• speak to CFOs to understand areas of compliance & potential risk areas of

non-compliance

• simulate impact – understand areas with most impact

• stress test results – organizational impact & investors reactions

• Ensure accuracy of FRS 139 financial statements• Verification necessary before result is released to the regulators, public

• Balance Sheet remediation may be useful

• Lesson: Engage with professionals, practitioners

Communicate with them early

18

Pressure Points And Beyond

-6 -5 -4 -3 -2 -124

1 23

4 5 6 7 8 9 10 11 12 13 14 15 n n 24

19

2012 2013 2014

Full suite IFRSFull suite IASAmendments

•Exp Draft

IASB

•Standard

IASB•Simultaneous

•adoption

MASB

CAPACITY BUILDING – UNIV PLAYS A BIG ROLE

First QTRresult on Full suite ofIFRS + comparative

2011

Learning point

• Change is rapid; may be too rapid for some

• Skills building• Nothing beats this

20

Recent changes

• 1 July 2010 - Presentation of financial statements– (see article)

• 1 July 2010 - IFRIC 15– (see annexure)

• Agriculture– (see article)

• IFRS 9– (see annexure)

• Insurance Phase 2

Features of new breed of accountants

• New things to learn

• Technically sound

• Quick

• Judgemental

• Soft touch

• Communication

Implications on academics

• Keeping up with changes

• Research areas are abound

• Literature can be a challenge

• Quantum leap forward through frequent engagements with practice

Conclusion

• Change necessitate changes to the professionals in the accounting profession

• Inevitable change but opportunities are abound

• Track these changes to be ahead

• Success for those who differentiates

• Skill building is a must

• Accountants are the new breed of financial reporters of tomorrow

Deloitte @ 2009 25

Annexure

IFRIC 15 Agreement for the

Construction of Real Estate

Industry So Unique ….

• Sell OFF-plan

• Then construct

• Meanwhile, purchasers imagine

• Happy if completed…. or …. Sad & angry if not

vs

• Register interest, 10% down

• Wait for construction to complete

• Or, purchase completed house

• Happy

So Unique …. with so many rules

• LAWS OF MALAYSIA FOR HOUSING DEVELOPMENT

• Principle Act 663 Building and Common Property (Maintenance and Management) Act 2007 12/04/2007 Principle Act 118 Housing

Development (Control and Licensing) Act 1966 29/08/1969 Amendment Act A402 Housing Developers (Control and Licensing) (Amendment) Act 1977 10/06/1977 Amendment ActA 703 Housing Developers (Control and Licensing) (Amendment) Act 1988 01/12/1988 Amendment Act A1142 Housing Developers (Control and Licensing) (Amendment) Act 2002 01/12/2002 Amendment Act A1289 Housing Developers (Control and Licensing) (Amendment) Act 2007 12/04/2007 Subsidiary PU (A) 58/1989 Housing Development (Control and Licensing) Regulations 198901/04/1989 Amendment PU(A) 446/1998 HOUSING DEVELOPERS (CONTROL AND LICENSING) (AMENDMENT) REGULATIONS 1998 04/12/1998 Amendment PU(A) 473/2002 HOUSING DEVELOPERS (CONTROL AND LICENSING) (AMENDMENT) REGULATIONS 2002 01/12/2002 Amendment PU(A) 42/2003 HOUSING DEVELOPERS (CONTROL AND LICENSING) (AMENDMENT) REGULATIONS 2002-CORRIGENDUM 07/02/2003 Amendment PU(A) 226/2003 HOUSING DEVELOPERS (CONTROL AND LICENSING) (AMENDMENT) REGULATIONS 2003 01/12/2002 Amendment PU(A) 395/2007 HOUSING DEVELOPERS (CONTROL AND LICENSING) (AMENDMENT) REGULATIONS 2007 01/12/2007 Amendment PU(A) 190/2008 HOUSING DEVELOPERS (CONTROL AND LICENSING) (AMENDMENT) REGULATIONS 2008 09/06/2008 Amendment PU(A) 200/2008 HOUSING DEVELOPERS (CONTROL AND LICENSING) (AMENDMENT) REGULATIONS 2008 17/06/2008 Subsidiary PU (A) 231/1991 Housing Developers (Housing Development Account) Regulations 199126/08/1991 Amendment PU(A) 474/2002 HOUSING DEVELOPERS (HOUSING DEVELOPMENT ACCOUNT) (AMENDMENT) REGULATIONS 2002 01/12/2002 Order PU(A) 293/2007 HOUSING DEVELOPMENT (CONTROL AND LICENSING) (EXEMPTION) ORDER 2007 06/09/2007 Order PU(A) 294/2007 HOUSING DEVELOPMENT (CONTROL AND LICENSING) (EXEMPTION) (NO 2) ORDER 2007 06/09/2007 Order PU(A) 295/2007 HOUSING DEVELOPMENT (CONTROL AND LICENSING) (EXEMPTION) (NO 3) ORDER 2007 06/09/2007 Order PU(A) 296/2007 HOUSING DEVELOPMENT (CONTROL AND LICENSING) (EXEMPTION) (NO 4) ORDER 2007 06/09/2007 Order PU(A) 297/2007 HOUSING DEVELOPMENT (CONTROL AND LICENSING) (EXEMPTION) (NO 5) ORDER 2007 06/09/2007 Order PU(A) 298/2007 HOUSING DEVELOPMENT (CONTROL AND LICENSING) (EXEMPTION) (NO 6) ORDER 2007 06/09/2007 Order PU(A) 299/2007 HOUSING DEVELOPMENT (CONTROL AND LICENSING) (EXEMPTION) (NO 7) ORDER 2007 06/09/2007 Order PU(A) 017/2008 HOUSING DEVELOPMENT (CONTROL AND LICENSING) (EXEMPTION) ORDER 2008 21/01/2008 Order PU(A) 109/2008 HOUSING DEVELOPMENT (CONTROL AND LICENSING) (EXEMPTION) (NO 2) ORDER 2008 10/04/2008 Order PU(A) 111/2008 HOUSING DEVELOPMENT (CONTROL AND LICENSING) (EXEMPTION) (NO 3) ORDER 2008 14/04/2008 Order PU(A) 120/2008 HOUSING DEVELOPMENT (CONTROL AND LICENSING) (EXEMPTION) (NO 4) ORDER 2008 24/04/2008 Order PU(A) 111/2008 HOUSING DEVELOPMENT (CONTROL AND LICENSING) (EXEMPTION) (NO 3) ORDER 2008 14/04/2008 Order PU(A) 063/2009 HOUSING DEVELOPMENT (CONTROL AND LICENSING) (EXEMPTION) ORDER 2009 16/02/2009 Subsidiary PU (A) 476/2002 Housing Development (Tribunal for Homebuyer Claims) Regulations 2002 01/12/2002 Subsidiary PU (A) 475/2002 Housing Development (Compounding of Offences) Regulations 2002 01/12/2002 Supplement PU (B) 307/2004 DELEGATION OF POWERS UNDER SUBSECTION 9(1) OF THE HOUSING DEVELOPMENT (CONTROL AND LICENSING) ACT 1966 05/08/2004 Principle Act 318 Strata Titles Act 1985 01/06/1985 Amendment Act A573 STRATA TITLES (AMENDMENT) ACT 1990 23/02/1990 Amendment Act A951 STRATA TITLES (AMENDMENT) ACT 1996 02/08/1196 Amendment Act A1290 STRATA TITLES (AMENDMENT) ACT 2007 12/04/2007 Subsidiary PU (A) 164/1988 Strata Titles (Federal Territory of Kuala Lumpur) Rules 1988 23/04/1988 Subsidiary PU (A) 5/2003 Strata Titles (Federal Territory of Putrajaya) Rules 2003 09/01/2003 Subsidiary PU (A) 503/2002 FEDERAL TERRITORY OF PUTRAJAYA (MODIFICATION OF STRATA TITLES ACT 1985) ORDER 2002 27/12/2002 Principle Act 133 Street, Drainage and Building Act 1974

Supported by unique accounting standards

• MAS 7 issued by MICPA/MIA

• MASB adopted MAS 7 in 1998

• Revised in 2004 as FRS 201

– Percentage of completion

– Completed method allowed alternative

– Matching

– Lots of guidance

Uniqueness given way to convergence

• IASB issued draft IFRIC 15 in March 2007

• Deliberation

• IASB issued IFRIC 15 in July 2008

• Deliberation

MASB issued IFRIC 15 on 1 Jan 2010, effective 1 July 2010Supersedes FRS 2012004

IFRIC 15 in essence

• IAS 18 (Revenue) and IAS 11 (Construction Contract) as bases

• Is it a sale or an obligation to construct?

• Rights and obligations

• Compels players to take a look at the agreement

• New concept called ‘continuous transfer’

IFRIC 15 in simple terms

IAS 18 revenue

risk & reward

rights & obligation

IAS 11 construction

IFRIC 15 Agreement

NO

NO

IFRIC 15―Quick reminder

NO

Revenue when criteria met

Agreement for construction of real estate

YESIFRIC 15 construction contract?

Agreement is a construction contract –

IAS 11% completion

YESAgreement only for

services?% completion

Agreement is for services – IAS 18

YESAgreement is for sale of goods – IAS 18

Criteria for goods met on continuous basis?

% completion

YES

YES

YES

Disclosure requirements

IAS 11 IAS 18 IFRIC 15

(a) How entity determines which agreements meet all the criteria in IAS 18.14 continuously as construction progresses.

(b) The amount of revenue arising from such agreements in the period.

(c) The methods used to determine the stage of completion of agreements in progress.

For agreements in progress:

(a) The aggregate amount of costs incurred and recognized profits (less recognized losses) to date; and

(b) The amount of advances received.

IFRIC 15 – ‘continuous transfer’

Implications

Quarterly submission

State of readiness

Readiness to change

Must change

Must bear with the change

Summary

• IFRIC 15 driven by convergence decision

• Has impact on industry so unique to Malaysia and to some others

• Since accounting is law in Malaysia, decision to adopt makes IFRIC 15 mandatory for companies sooner rather than later

• Implications can be significant on industry, income taxes, systems and bottom line

Annexure

The Beginning of the End for IAS 39

The Beginning of The End for IAS 39

• IFRS 9 Financial Instruments is the first phase of a complete rewrite of IAS 39

• Second phase covering amortised cost and impairment

• Third phase, hedge accounting

38

39

• Debt instruments meeting both a “business model” test and a “cash flow

characteristics” test are measured at amortised cost

• Investments in equity instruments can be designated as “fair value through

other comprehensive income” with only dividends being recognised in profit

or loss

• All other instruments (including all derivatives) are measured at fair value

with changes recognised in the profit or loss

• The concept of “embedded derivatives” does not apply to financial assets

within the scope of the standard and the entire instruments must be

classified and measured in accordance with the above guidelines

• Unquoted equity instruments can no longer be measured at cost less

impairment (must be at fair value).

IFRS 9 Changes

40

• In determinining amortised cost or fair value, an entity must use

two criteria:-

• a business model test

• a cash flow characteristics test

• If the financial asset satisfies the two criteria:-

• the financial asset must be measured at amortised cost

41

• Business Model Test

• to assess whether its business objective is to collect the

contractual cash flows of the assets

• rather than realise their fair value change from sale

• this determination is made at business unit level not an

individual financial instrument level

• therefore is not based on management’s intent for individual

instruments

Key changes under IFRS 9

Investments in equityinstruments

Often classified as ‘available for sale’ with gains and some losses deferred in other comprehensive income. Impairment losses recognised in profit or loss.

Measured at fair value with gains/losses recognised in profit or loss, unless designated at fair value through other comprehensive income in which case only dividends recognised in profit or loss

Available for sale debtinstruments

Recognised at fair value with gains/ losses deferred in other comprehensive income. Impairment losses and reversalsrecognised in profit and loss

May be measured on amortised cost basis if the ‘business model’and ‘cash flow characteristics’ tests are met, otherwise measured atfair value through profit or loss

Convertibleinstruments

Embedded conversion option bifurcated and separately recognised at fair value, underlying debt instrument may bemeasured at amortised cost

Entire instrument must be classified and measured. Results inmeasurement at fair value with gains/losses in the profit or loss

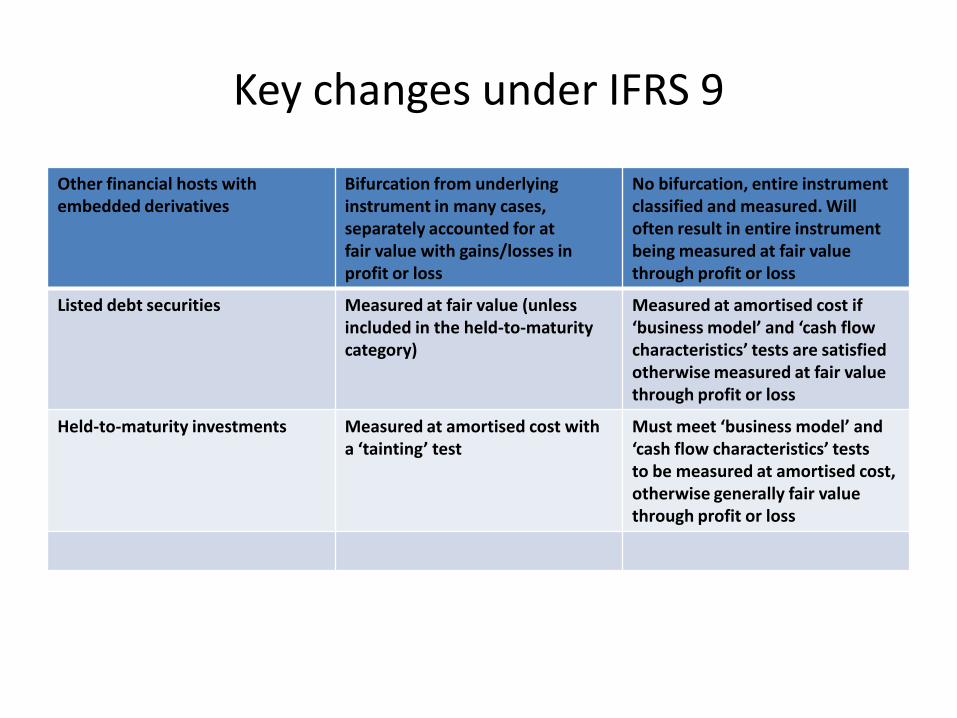

Other financial hosts with embedded derivatives

Bifurcation from underlying instrument in many cases, separately accounted for atfair value with gains/losses in profit or loss

No bifurcation, entire instrument classified and measured. Will often result in entire instrument being measured at fair value through profit or loss

Listed debt securities Measured at fair value (unless included in the held-to-maturity category)

Measured at amortised cost if ‘business model’ and ‘cash flowcharacteristics’ tests are satisfied otherwise measured at fair valuethrough profit or loss

Held-to-maturity investments Measured at amortised cost with a ‘tainting’ test

Must meet ‘business model’ and ‘cash flow characteristics’ teststo be measured at amortised cost, otherwise generally fair valuethrough profit or loss

Key changes under IFRS 9

Summary

• Attempts to make IAS 39 simpler

• Phase 1 looks friendly

• Subsequent phases undergoing debate

• More to come

Further technical resources

• Deloitte International Accounting Manual

• Deloitte IFRS model financial statements

• Deloitte IFRS Compliance Checklists

• IAS Plus website (www.iasplus.com)

• IFRS Knowledge Resource Centre

• Global Technical Library (techlibrary.deloitteaudit.com)

• iGAAP 2009

• IFRS Specialists

• IFRIC 15 – Agreements for the construction of real estate

• iGAAP 2009 – chapter 23 Revenue

Deloitte @ 2009 46© 2010 Deloitte Touche Tohmatsu

Contact

Dr. Nordin Zain

Executive Director / Client

Service Leader

Tel: +603 7723 6556

Dr Nordin was formerly the Executive Director with the Malaysian

Accounting Standards Board for 9 years where he was responsible

for developing conventional and Islamic accounting standards for

Malaysia. He joined Deloitte in February 2009 and is responsible

for IFRS implementation and Islamic finance. He is a member of

the Malaysian Institute of Accountants, a Board member of AAOIFI

and sits on the Asia Pacific Financial Reporting Advisory Group in

Melbourne. He was formerly a corporate banker, an internal

auditor, a lecturer and a consultant to the United Nations.

Please request for permission from the author if you wish to

reproduce the materials herein.